Calling Both Clinton and Trump Unpopular and Untrustworthy is Seriously Misleading

Polling results do not demonstrate that Clinton and Trump are nearly equally reviled, notwithstanding the ubiquitous media narrative. To say that voters distrust both candidates confuses two possibilities: that people are uncertain of Clinton’s policy commitments, and that they are certain that Trump is committed to dangerous policies.

One of the most widely accepted media storylines of the 2016 US presidential election is that both of the major-party candidates are widely disliked. While it is easy to find evidence seeming to support the idea that many people are unhappy with a choice between Hillary Clinton and Donald Trump, however, the conclusions drawn from such evidence can be highly misleading.

In June, for example, The New York Times published, “Clinton and Trump Have Terrible Approval Ratings. Does It Matter?” That article provided a welter of data showing that Clinton and Trump had historically low “net favourably ratings”. Such ratings reflect the number of “favourable” responses reduced by the number of “unfavourable” responses for each candidate.

As the Times article pointed out, however, Clinton’s and Trump’s low net favourability ratings might have nothing to do with any unique rejection of those two candidates by the public at large. In an increasingly partisan political environment, more voters in 2016 view the other party’s nominee as truly bad, not merely as the less qualified of the two available candidates. For example, whereas people in 1976 were evenly split between Jimmy Carter and Gerald Ford, few thought that the other party’s candidate was dangerous. Today, when people are more politically polarised and thus hold harsher views of their opponents, the resulting negative ratings will pull down the net favourability numbers for both candidates.

Similarly, the Gallup polling organisation in July published “One in Four Americans Dislike Both Presidential Candidates”. That press release led with a contrast of the number of people who have unfavourable views of both candidates in the 2012 and 2016 elections. Whereas only 11 percent of people rated both Barack Obama and Mitt Romney negatively four years ago, today the same poll shows 25 percent of the respondents disliking both Clinton and Trump.

In another sign of voter discontent, large numbers of the supporters of both Trump and Clinton view their choice as more of a vote against the opposing candidate than an expression of support for their candidate.

Everyone should know, however, that a person who says “I have an unfavourable view of this candidate” is actually providing very little information to a pollster. For example, we know nothing about the intensity with which a person dislikes that candidate.

To its credit, Gallup has tried to elicit more than a mere up/down response by asking questions that attempt to measure intensity. Their “scalometre” uses a ten-point scale to try to measure respondents’ feelings along a continuum from very positive responses (+5) to very negative responses (-5). Gallup deems scores of -4 and -5 to be “very negative,” and it found that “only 4% of the country has a very unfavourable view of both candidates, indicating that even among those who dislike both candidates, one candidate is more strongly disliked than the other.”

Gallup, therefore, did publish polling results that cut against the established media narrative. Even so, the US press continues to focus almost exclusively on favourability ratings, not on Gallup’s intensity ratings or similar results. Indeed, Gallup’s report itself led with the simplistic approach and casually mentioned that the scalometre results would be discussed much later in the press release. Who knows how many people bother to read that far? The evidence strongly suggests that most journalists and headline writers do not.

A similarly misleading analytical approach shows up in a polling analysis that the Pew Research Center released in July, “2016 Campaign: Strong Interest, Widespread Dissatisfaction.” Pew notes: “In another sign of voter discontent, large numbers of the supporters of both Trump and Clinton view their choice as more of a vote against the opposing candidate than an expression of support for their candidate.”

This is apparently meant to lend some support to the idea that voters are generally unhappy with both candidates, that is, that they are choosing the lesser of two evils – and that voters view both evils as especially super-evil this year.

That could be true, but there is no way to know, at least based on Pew’s report. After all, consider a person who thinks that Clinton is a very good candidate and that Trump is a very bad candidate. This person receives a call from Pew and agrees to be interviewed. Asked if he is voting more “for” Clinton or “against” Trump, this person concludes that what makes Trump a scary candidate – his appeals to bigotry, his misogyny, his unpreparedness for office, his serial lies – are more than enough reason to vote against Trump.

In that case, the voter might indeed have been willing to vote for someone whom he truly dislikes – say, Senator Marco Rubio – if the other choice was Donald Trump. But with Hillary Clinton on the ballot, this voter is fortunately able both to vote against a candidate he fears and in favour of a candidate he genuinely admires.

Where, then, is the logic behind the claim that voting against one candidate is proof that votes for the other candidate are cast reluctantly? This is not to say that it is impossible for a person to view this year’s choices as both being terrible, but it is simply a fact that the polling questions do not tell us enough to know whether that is true.

Both Gallup and Pew are high quality polling organisations, and they are deservedly viewed with respect. The problem is that they present their results in ways that feed established media narratives, whereas the evidence on which those conclusions are based is at best ambiguous.

More importantly, what matters most is why voters hold positive or negative views, even intensely held views. Understanding the difference between the negative poll ratings of Clinton and Trump is critical, because what people dislike about the candidates differs. These differences, in turn, provide insights into the candidates’ possible performance as president.

In June of this year, in an analysis of the media’s narrative about both candidates having “high negatives”, I wrote that “Hillary Clinton on her worst day is better than Donald Trump on his best.” I went beyond the positive/negative dichotomy and explored what it means when people use words like “distrust” or “dishonest” to describe the candidates. Even though poll results show that many people are willing to call Clinton “dishonest” or to say that they do not trust her, while a not-that-much-higher percent say the same things about Trump, this simply misses the ambiguous and changing ways in which people use those words.

Voters are generally unhappy with both candidates, that is, that they are choosing the lesser of two evils – and that voters view both evils as especially super-evil this year.

People who say that they do not trust Clinton have expressed worries that she might change her position on one or another issue. For example, supporters of Bernie Sanders could point to her speeches to Goldman Sachs and say, “When push comes to shove, I can all too easily believe that she’ll go soft on Wall Street.” In other words, some people on the left do not trust Clinton to hold to a position that she currently claims to hold. When asked, therefore, they might say that they think she is being dishonest.

And it is fair to wonder what any candidate will do after being elected. Although I have come to believe that Clinton’s changes in policy views over time are based on her understanding that times have changed, and that she has assessed a growing body of evidence on which to base her new views, I could be wrong. She has certainly been pushed by political considerations to change her substantive policy commitments, with an intensifying turn against neoliberalism in the US and the UK making voters unwilling to accept more of the trickle-down policies that Republicans and (Bill) Clinton Democrats championed.

Hillary Clinton, therefore, could either be a genuine convert or a political opportunist. But if she were merely co-opting Sanders’ positions with the intention of abandoning them later, why would she have taken consistent political heat during the primaries by continuing to differ from Sanders? Why, for example, would she have bothered to take a position that fell short of Sanders’ support for a no-exceptions $15-per-hour minimum wage?

To be extremely clear, I strongly support the movement to increase the minimum wage to $15 per hour, and I was thus disappointed by Clinton’s decision not to support that higher level. The point, however, is that she did not act like someone who simply says whatever is necessary to win, all the while secretly holding different views and intending to betray her gullible supporters.

On the other hand, when Clinton is president, there will be times when she will compromise, and the “Clinton cannot be trusted” people will flood the internet with criticisms and gloating. They might be right, or they might simply misinterpret the need for President Clinton to make compromises with a rigid opposition party as proof that she was never really committed to her professed views.

When Barack Obama came into office, a lot of people thought that he was much more liberal than he has turned out to be. I was one of the people who frequently complained that Obama did not drive a hard enough bargain, and it was important to distinguish rightward moves that Obama made under duress from those that he took seemingly of his own volition (such as his surprise announcement that he was freezing the pay of federal workers, for which he received nothing in return from Republicans). Especially on economic issues, it took a lot of liberals quite a long time to accept the fact that Obama was not the progressive that they had hoped he would be.

So, if “trust” is an issue, one version of distrusting someone is suspecting that he or she will disappoint you at times in the future. But another version of distrust is not believing that a person intends to do the right thing – or that he even knows what the right thing is.

[Note that I am not dealing here with the supposed scandals that people attribute to Clinton, because none of those much-hyped feeding frenzies have turned out to have any meaningful content. Interested readers might in particular want to read this summary of the FBI’s recent exoneration of Clinton regarding her use of a private email server.]

When most people say that they distrust Donald Trump, they cannot possibly be expressing concern that he is taking one position now but will betray them later. After all, Trump is obviously making things up as he goes along, and he changes his policy statements from moment to moment. Trump makes suckers out of people who believe him every day, as his wild back-and-forth on immigration policy in late August and early September – seeming to soften his views, then hardening them, then carving out ad hoc exceptions at a national defence forum in New York – vividly demonstrates.

Even though poll results show that many people are willing to call Clinton “dishonest” or to say that they do not trust her, while a not-that-much-higher percent say the same things about Trump, this simply misses the ambiguous and changing ways in which people use those words.

Those are certainly reasons to distrust Trump, but they are very different from expressing worry that Clinton might not carry through on, for example, her promises to provide free higher education to most American students. “I don’t trust Clinton” can mean that a person has a nagging feeling that she might not fight hard enough on progressive issues. “I don’t trust Trump” most likely means that a person cannot even figure out what Trump means from one minute to the next, which makes it nearly impossible to know what he would do if elected.

More importantly, a person who applies the word “distrust” to Trump might also be expressing fear of what Trump actually will do as president. After all, despite the farce of Trump’s ever-changing policy statements and self-contradictions, there do seem to be some things that he wants to do, even if he is not sure how he would do them. He might or might not create a “deportation force” to evict millions of families from the United States, for example, but Trump certainly seems intent on making their lives miserable.

Similarly, while Trump might or might not try to build his ridiculous wall on the US-Mexican border, he would definitely continue to stoke bigotry and divisiveness in the country. In fact, we can be sure that he will do that even after he loses the election.

In short, polls tell us nothing about why people trust or distrust candidates, because the concept of trust is so complex. Does it really matter whether a voter says, “I distrust Trump because I know he’ll do the wrong thing,” or “I trust that Trump will always make the wrong choice”?

All of which means that there are reasons why people might look at Clinton and say, “You know, I’m not sure what she’ll do as president”, using the word “distrust” as a shorthand. I do not think that there is any reason to emphasise those doubts about Clinton more than we would for any other politician who lives in the real world, but I certainly respect people who feel less confident than I do about where she will spend her political capital and where she will draw lines in the sand. On the other hand, even though I am not sure what Trump would do, I trust that it would be terrible.

But the larger narrative, in which people are supposedly equally disgusted with the presidential choices offered up by both parties, is simply a leap beyond the evidence. Repeating that narrative makes two very different candidates look unjustifiably similar.

About the Author

Neil H. Buchanan is an economist and legal scholar, a professor of law at The George Washington University and a senior fellow at the Taxation Law and Policy Research Institute, Monash University, Melbourne, Australia. His research addresses budget deficits, the national debt, health care costs, and the future of Social Security.

Neil H. Buchanan is an economist and legal scholar, a professor of law at The George Washington University and a senior fellow at the Taxation Law and Policy Research Institute, Monash University, Melbourne, Australia. His research addresses budget deficits, the national debt, health care costs, and the future of Social Security.

Latin America’s Challenge: More and Better Saving for Development

By Eduardo Cavallo and Tomás Serebrisky

The Latin American and Caribbean region is trapped in a vicious cycle of low savings and poor use of these savings. This article discusses strategic goals for households, firms, and governments across the region to reverse the cycle.

Why should people – and economies – save? The typical answer is to protect against future shocks, to smooth consumption during hard times, in short, to save for the proverbial rainy day. But the question can be approached from a slightly different angle. While saving to survive the bad times is important, saving to thrive in the good times is what really counts. The goal of saving should be to pave the way for individuals to live more productive, fulfilling lives, for firms to grow and provide quality jobs and competitive goods and services, and for government to assure their citizens enjoy a developed infrastructure, efficient public services and a dignified, secure retirement. In short, countries must save for a sunny day – a time when everyone can bask in the benefits of growth, prosperity, and well-being.

To have even a chance of reaching that sunny day, Latin America and the Caribbean must save more and save better. Saving in the region is too low and the savings that do exist are not used efficiently to enhance growth and development. Borrowing from abroad cannot pick up the slack as it may be more costly, is certainly more fickle, and raises the risk of crises. Ultimately, national saving is the only reliable vehicle through which the region can become stable and confident in its own future.

Unfortunately, countries in Latin America and the Caribbean save less than 20 percent of their national income – less than every other region in the world, except Sub-Saharan Africa. By contrast, the high-growth countries in East Asia save about 35 percent of national income (See Figure 1 below). The region is not putting aside enough resources today to build a better, brighter tomorrow.

Sharing the Blame for Low Saving

If saving is so important for growth and development, then why does Latin America and the Caribbean do such a poor job of it? Demographic factors – such as the number of working to non-working age people in a country at a given point in time – matter for saving, but they are not to blame for the region’s low saving rates. Beginning in the 1960s, the region embarked on a “saving-friendly” demographic transition (with decreasing age dependency ratios), very much like high-saving countries in Asia. In 1965, for each 100 individuals of working age, there were 90 dependents, either young or old; today there are fewer than 50. Yet, unlike Asia, national saving rates in Latin America have increased little. If favourable demographic factors had been fully exploited, the average saving rate in the region should be about 8 percentage points of gross domestic product (GDP) higher.1

Various nondemographic factors have kept the saving rates down, despite the demographic bonus. One is the lack of adequate saving instruments. The perennial problems of lack of trust in financial institutions and high costs of doing business with banks discourage households from placing their savings in formal financial institutions. Only about 16 percent of adults in Latin America report saving through a bank, compared to 40 percent in Emerging Asia, and 50 percent in advanced economies.2 Instead, households in the region – especially relatively poorer households – save more through informal mechanisms, or just give up on saving altogether.

In good times, political economy incentives encourage governments to increase spending across the board. In bad times, they usually find it politically more expedient to cut capital expenditure projects than other expenditures.

The state of the region’s pension systems has also depressed saving. They cover less than half the population and face long-term sustainability challenges. Most people in Latin America and the Caribbean do not save through pension systems, or they do not save for enough years to qualify for a contributory pension at the end of their working lives. Importantly, they do not compensate with higher voluntary saving. The pension crisis in the region is effectively a saving problem, with serious social implications.

Fiscal policy has also been a drag on saving. On the one hand, distorted incentives bias public expenditures toward current spending (consumption) and away from capital investment (saving) over the economic cycle. In good times, political economy incentives encourage governments to increase spending across the board. In bad times, they usually find it politically more expedient to cut capital expenditure projects than other expenditures. Total expenditure in Latin America from 2007 to 2014 increased a whopping 3.7 percent of GDP, but more than 90 percent went into current expenditure, and only 8 percent to longer-term public investment.

A second public finance issue is considerable leakage in spending areas such as social assistance, tax expenditures and subsidies to energy. Rather than limiting their assistance to those who truly need it, government programs end up benefiting the nonpoor to the tune of about 2 percent of GDP in the region. Inefficiencies in health and education spending average another 1 percent of GDP. These leakages and inefficiencies are in essence public saving that is forgone.

Taxation also directly impacts saving because tax revenue is one of the components of public saving. And it indirectly impacts saving through the incentives it provides to individuals and firms to save. Widespread tax evasion – about 52 percent of potential tax collection in the region – is a problem on both fronts: it reduces tax revenues, and it distorts the incentives of compliers versus noncompliers.3 Many countries impose a high tax burden on complying taxpayers but collect relatively little in tax revenue (as a share of GDP). This is the worst possible combination for saving: a tax system that imposes very high tax rates (thereby distorting private saving decisions) and collects very little revenue (thereby adding little to public revenue and public saving).

Distortions in financial markets such as the high cost of enforcing contracts, or the lack of information about the creditworthiness of potential borrowers, raise the cost of credit for productive firms. This limits the ability of firms with good investment projects to invest and grow. The result is a misallocation of economic resources and lower aggregate productivity. This, in turn, generates disincentives to save because an economy with low productivity growth is essentially an economy in which returns to saving and investment are also low. Distortions beyond financial markets also matter. Labour markets distorted by high levels of informality, inefficient or inequitable social policy regulations, special tax regimes, or a combination of these factors, change the private profitability of investment projects and lead to socially inefficient investments. Removing these distortions would increase productivity, investment, and savings.

How to Promote Saving for Development

The Inter-American Development Bank’s latest flagship publication, Saving for Development: How Latin America can Save More and Better, outlines how to increase saving for the future in sustainable ways. A comprehensive agenda combines public policies to stimulate saving directly, such as measures related to fiscal policy and pensions, with policies that operate indirectly by removing constraints.

Tackle the pension problem. A solution to Latin America’s saving problem requires fixing broken pension systems. Countries have promised to pay very generous pensions to their retirees, but they have not saved enough to fulfil those promises. The public debate in the region largely revolves around whether pension systems should be based on individual accounts (fully funded) or pay-as-you-go (PAYGO) approaches. However, this debate ignores the reality of the region’s labour markets. Both systems suffer from a lack of inclusion. More than half of the labour force is informally employed, meaning they don’t contribute to pensions. Among the lowest three deciles of income distribution, that figure is as high as 90-95 percent.

Resolving the pension problem requires adjusting the systems’ parameters, such as the retirement age, level of benefits, and required years of contributions. Perhaps more importantly it requires structural changes, beginning with tackling labour informality and its disastrous consequences.

Focus on capital spending. Over the last two decades, improved fiscal frameworks have delivered higher public saving in many countries. Yet more effort is needed just when a challenging economic environment makes doing so more difficult. The good news is that substantial public saving can still be generated without having to rely on the traditional tools of raising taxes or reducing expenditures across the board. Governments have room to boost public saving by increasing the share of capital expenditures, which is low in the region, with respect to current spending, which is high. Moreover, additional resources can be devoted to increasing capital expenditures if governments eliminated leakages in spending programs such as social assistance, tax expenditures and subsidies to energy (that means making sure that spending reaches its intended beneficiaries only). Leakages due to poor targeting of spending programs add up to approximately 2 percent of GDP on average.

Personal income taxes across the region should continue evolving into a dual system, with a lower flat tax on capital, in which all forms of capital income (interest payments, dividends, and capital gains) receive equal tax treatment.

Target tax policy better. Income taxes are levied on both individuals (personal income tax) and firms (corporate income tax). But households collectively own firms; therefore tax policy should integrate personal and corporate income taxes, and avoiding double taxation of savings: first, when it is generated by the firm, and then when it is distributed to households as dividends. Personal income taxes across the region should continue evolving into a dual system, with a lower flat tax on capital, in which all forms of capital income (interest payments, dividends, and capital gains) receive equal tax treatment. Corporate income tax rates should fall in line with international trends to facilitate the formalisation of informal firms. This would help expand the tax base, which is currently low.

Promote household saving and create a savings culture. At the household level, saving rates in the region are distorted by a number of factors: high costs of accessing and using the financial system; lack of confidence in the financial system; poor financial regulation; little understanding about banks and how they work; and social pressures and behavioural biases. Successful financial inclusion requires more than just opening new bank accounts. It means tailoring saving products to the demands of potential clients, taking into account the various real-life constraints they face to save, and creating incentives to channel more savings through the formal financial system. Public policy interventions and financial product innovations has been shown to increase household saving and encourage more financial saving in particular. Making more and faster progress in these areas requires more dynamic regulation and supervision of the financial system and the collaborative efforts of financial regulators and bankers to implement reforms and promote even more innovation.

Government initiatives to pay social transfers through bank accounts and to channel remittances through domestic financial systems are useful first steps. Additional progress in encouraging more financial saving demands improvements in the design of the programs: for example, by pairing payments with programs that provide financial education, and/or with instruments to help users overcome the behavioural and social biases that constrain saving. Innovation and technology provide another opportunity to encourage more saving through the formal financial system. While the penetration of mobile telephones is high in Latin America and the Caribbean, the region still lags behind in using mobile technology for financial services because policy and regulations have not kept pace with the mobile telephone revolution.

A promising avenue for creating a saving culture in Latin America and the Caribbean is financial education, with a focus on children and youth. Positive saving habits are easier to instil during the early years, when the brain is still developing and learning is easier.

Fix the financial system. Efforts to create a culture of saving must be complemented by efforts to help the financial system pool and allocate savings efficiently. Only by fixing the problems that discourage the use of financial systems for saving and limit the availability of financing for productive firms, can more saving turn into better saving for development.

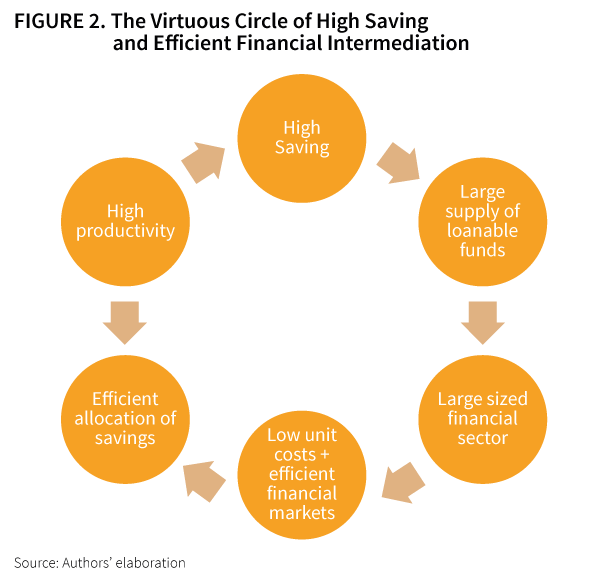

The key is to create a virtuous circle in which more savings generate more loanable funds, bigger and more efficient financial systems, a better channeling of resources, and higher productivity.

Financial frictions are like sand in the wheels of the economy; they slow down economic progress. Two types of financial distortions are particularly acute in Latin America and are amenable to policy action. First, banks do not have access to quality information about potential borrowers. While the region has made headway in extending the coverage of credit bureaus that provide this information, the quality and timeliness of the information is still poor in many countries. On average, the regulatory framework in Latin America is less conducive to information sharing than in other regions of the world.

A second problem is the high cost of enforcing financial contracts in the region. The effective protection of property rights is particularly weak in Latin America. Fortunately, examples of successful reforms in the region have helped alleviate this constraint.

The Virtuous Circle

The key is to create a virtuous circle (Figure 2 below) in which more savings generate more loanable funds, bigger and more efficient financial systems, a better channeling of resources, and higher productivity. Those steps would generate higher savings still and the wheel would keep turning, leading to more development with greater social inclusion.

Featured image: Brokers work at the Buenos Aires Stock Exchange in Buenos Aires, Argentina. Latin America and the Caribbean will post an economic contraction in 2016, the International Monetary Fund forecast in a report issued Wednesday, April 27, 2016. Photo courtesy: AP Photo/Victor R. Caivano, File

About the Authors

Eduardo Cavallo is a Lead Economist at the Research Department of the Inter-American Development Bank (IDB) in Washington, DC. His research interests are in the fields of international finance and macroeconomics with a focus on Latin America. He holds a PhD in Public Policy from Harvard University and a BA in Economics (magna cum laude) from Universidad de San Andrés in Buenos Aires, Argentina.

Eduardo Cavallo is a Lead Economist at the Research Department of the Inter-American Development Bank (IDB) in Washington, DC. His research interests are in the fields of international finance and macroeconomics with a focus on Latin America. He holds a PhD in Public Policy from Harvard University and a BA in Economics (magna cum laude) from Universidad de San Andrés in Buenos Aires, Argentina.

Tomás Serebrisky is the Principal Economic Advisor of the Infrastructure and Environment Department of the Inter-American Development Bank (IDB) in Washington, DC. His specialisations a re the economics of infrastructure investment, Public Private Partnerships, and economic regulation. Tomás holds a PhD in Economics from the University of Chicago and a BA in Economics (summa cum laude) from Universidad de San Andrés in Buenos Aires, Argentina.

re the economics of infrastructure investment, Public Private Partnerships, and economic regulation. Tomás holds a PhD in Economics from the University of Chicago and a BA in Economics (summa cum laude) from Universidad de San Andrés in Buenos Aires, Argentina.

References

1. Cavallo, E., G. Sánchez, and P. Valenzuela (2016). Gone with the Wind: Demographic Transitions and Domestic Saving. IDB Working Paper, no. 688. (Department of Research and Chief Economist, Inter-American Development Bank, Washington, DC).

2. World Bank’s Financial Inclusion (FINDEX) database. World Bank (2014). Global Findex Database. Database. Available at http://datatopics.worldbank.org/financialinclusion/. (World Bank, Washington, DC). Accessed February 2016.

3. Corbacho, A., V. Fretes Cibils, and E. Lora, eds. (2013). More than Revenue: Taxation as a Development Tool. Development in the Americas series. (Washington, DC: Inter-American Development Bank and New York, NY: Palgrave Macmillan).By Eduardo Cavallo and Tomás Serebrisky

Implications of Islamic Finance in Africa’s Socio-Economic Development

Africa, a continent which still feels the scars of slave trade, the wounds of colonialism and apartheid, the disaster of neo-liberalisation, and the proliferating neo-patrimonial governance structure. With unblemished evidence that the IMF and World Bank economic prescriptions have consistently delivered too little, what then, are the expectations of Islamic finance?

The Socio-economic Setting of the Africa State

At least Korea, Brazil, India and Nigeria had about the same GDP in 1960. It will now take the whole of Africa till 2050 to become as big as Brazil and India in GDP terms.1 We found relative socio-political stability before slave trade and little or no poverty before colonialism in Africa. As countries gained independence in the 1960s African economies had prospects and the commodity market strengthened these new states. The military started to show interest in state affairs and many were aided by Western powers. The case of Zaire now Democratic Republic of Congo seem a very good example. The “divide and rule” joker of the colonial masters were put on the table again to promote austerity and the structural adjustment programmes through the military in the 80s and the Washington Consensus was given potency. African leaders themselves had no clear and realistic direction and allowed ethno-religious diversity to pollute their focus. The influence of the African triple heritage has indeed come to play – a heritage of Semitic religion, western influence and indigenous bias.2 These three heritages manipulated the mind of Africans and greatly influence decisions; it helped to breed neo-patrimony; good politics but terrible economics; and alignment with foreign economic thoughts without regard for social ontology. Therefore a huge gap was created in Africa – the fissure of unimaginable corruption, uncontrollable state and market capture, and senseless rivalry culminating into extreme poverty, unemployment and widened income inequality.

The Lies of Economic Theories and Disingenuous Washington Consensus

As neo-classical economic theories gained influence after the Second World War, there was also a need to expand markets and trade liberalisation was sold like a life-saving product to the developing nations. South American economies were quick to gain some consciousness and created their own terms for dependency theories, and indeed neo-dependency theories. Raul Prebish, the Argentinian economist stressed on trade protectionism for southern economies as a strategy to allow them to be self-sustaining and favoured import-substitution industrialisation.3 Meanwhile, African economists have become engrossed with knowledge gained from Western universities and enthralled with the books that were shipped from the United States and Great Britain. And so, they were quick to follow the neo-classical schools. And as if Karl Marx and Frederick Engels were of no use to Western Europe with their Communist Manifesto; and as if European bourgeois and monarchies at some point did not produce too many peasants; and as if that was not what lead to the welfare approach in modern Europe, one would have assumed that Western Europe had been such a perfect territory. So African economists rushed after the Nobel Prize winner in economics – Robert Solow who expanded the works of Harrod-Domar by including labour as a second factor and technology as a third independent variable to the growth equation.4 Again, Paul Romer’s endogenous new growth theory sincerely addresses technological spill overs in the industrialisation process, but many policy makers perhaps did not quickly realise that this theory would be fruitless only and until assumptions made are within the realm of reality in a jurisdiction that such theory would be applied. It is at this point that a well-intended theory becomes an inapplicable policy in a developing economy due to lack of adequate information, sound infrastructures, imperfect capital market, ineffective institutions and poor governance indicators. Thus, if the Washington Consensus had imagined that the ten agenda which includes deregulation, trade liberalisation and privatisation among others would be effective, then such a decision was indeed a blunder. So Africa witnessed unguided deregulation and state and market actors’ quickly shared national assets to themselves. Certainly, they could not manage these assets and so their cronies in power provided additional subsides that are still in place. And there was a big mess of the Washington Consensus. At this time South Korea learnt from Japan’s embedded autonomy5 and created a cohesive capitalist state6 even though they distorted the market force mechanism to an extent where state and market formed a symbiotic partnership.

Islamic economics and financial system

A huge gap was created in Africa – the fissure of unimaginable corruption, uncontrollable state and market capture, and senseless rivalry culminating into extreme poverty, unemployment and widened income inequality.

Karla Hoff and Joseph Stiglitz observed that “economist who tried to design policies to fit developing country markets generally assumed rigidities in markets, but did not explain them by reference to a choice-based perspective”.7 With the influence of the triple heritage, Africa is again caught in the web of Islamic finance without Islamic economics, at least in theory. The Islamic economic model is an entire encyclopaedia based on the rules of Islamic commercial jurisprudence. The GCC have created the elite club and it became easy for Islamic finance within these oil rich states to foster. Thus this somewhat new industry is enjoying petro-dollars to spread its message. Malaysia on the other hand built Islamic finance and indeed Islamic economics by learning from scratch while aligning with developmental schools of the Asian Tigers. On the other hand, Europe led by the United Kingdom has become the hub for Islamic finance. Africa indeed now has a new bride – Islamic finance. So what really do Africans want with Islamic finance? Is it just to align with the GCC, Malaysia and the UK as partners in faith? Or, is it to solve the continent’s economic woes? Meanwhile, financial aids from the West are mainly used to pay international consultants and experts to develop economic policies. In the case of Islamic finance, grants, trade lines and direct funding are lodged with African financial institutions and governments. The Standing Committee for Economic and Commercial Cooperation of the Organization of Islamic Cooperation (COMCEC) in the financial outlook of the OIC member countries in 2015 referred to the World Bank income categories and found 13 African states out of the 15 OIC countries in the low-income category. They include Benin, Burkina Faso, Chad, Guinea, Guinea-Bissau, Mali, Mozambique, Niger, Sierra Leone, Somalia, Gambia, Togo and Uganda. In the lower middle income group 9 out of 19 countries are African countries and in the upper middle income countries 4 out of 16 countries are African nations and none in the high income group. This shows that with over 45 years of OIC membership of African states, their economic situation has hardly been positively affected. It also means that the Islamic economic model has now been properly digested into the economies of Africa. More specifically, Islamic economics and finance in the last ten years that it has become more popular has been of little or no effect in the development of Africa. In the same light, issues around poverty, unemployment and closing of the inequality gap is yet to be addressed effectively. Thus, relevant actors would need to visit the strategy desk and represent a proposition that works. The CGG, UK and Malaysia did not look at the poverty side in the development of Islamic finance contracts – of partnership, sales and lease and so they were mainly designed to earn profit. This “profit-only” model would only get more capital into the hands of egocentric state and market actors in Africa. The Islamic Solidarity Development Fund of the Islamic Development Bank (IDB) is focused towards touching lives and reducing the multidimensional poverty index in OIC states. This should work effectively by collaborating more with other multilateral development institutions and donor countries globally, thereby harmonising fragmented programmes into a more cohesive one.

Can Africa Industrialise with Sukuk?

Thomson Reuters8 referred to the ICD-Thomson Reuters and asserted that total global Islamic finance asset reached USD1.8 trillion in 2014 in which sukuk (Islamic investment certificates) made USD295 billion or 16% of total Islamic finance asset. Islamic banking is however the largest sector with USD1.3 trillion, or 74% of total Islamic finance asset. It was also observed that Malaysia is the world’s sukuk leader in terms of number of issuance, value and sukuk outstanding. In a 2015 survey by Thomson Reuters for preferred market for sukuk shows UAE, Saudi Arabia, Malaysia and the UK consecutively as the most preferred market.9 No African market made the first 12 countries. Out of the 11 emerging Islamic finance markets Egypt and Tunisia made the list in which USA, China and France were the most preferred consecutively. With the free fall of crude oil prices and negative 2016 budget deficit in 5 out of 6 GCC countries, the Thomson Reuters research still shows that the risk in investing in these economies are mild. Senegal, Cote d’Ivoire and South Africa issued sovereign sukuk in 2015 with the support of the Islamic Corporation for the Development of the Private Sector (ICD), a member of the Islamic Development Bank (IDB), and Nigeria is considering to issue one in 2017. Unfortunately, these sukuk do not seem to have guarantees from any multilateral institution making it more difficult for them to attract foreign inflow couple with foreign exchange risk and rapid devaluation of currencies of African markets. Foreign investors including foreign Islamic investments would prefer very short portfolio investment which allows them exit very quickly thereby further destabilising the African economic architecture. Of what benefit then is the Islamic finance proposition and where is the Maqasid al Shariah which seeks to achieve human wellbeing and communal good-life while enriching and safeguarding the human self, faith, intellect, prosperity and wealth?

The Trajectory of Development Rather Than Growth

Africa is yet to have a development model and plan. The African Development Bank (ADB), the Afriexim Bank, Islamic Development Bank together with the United Nations, World Bank/IMF and countries that have demonstrated practical commitments like the Chinese among others need to work with African governments to draw the trajectory for development through the embedded autonomy approach. One would give preference to the Korean style of development where precise goods and services within the realm of import substitution within Africa, and export promotion outside Africa are well articulated. Like a small enterprise, access to required funds for trade and industrialisation, access to defined market needs to be established, and the required skills or capacity and technology needed to set forth this industrialisation agenda be built in Africa in such states where production cost is largely low. It then makes sense to treat Africa like one country where labour may move freely but with consciousness of extreme circumstances. Africa may then relegate those empty GDP and GNI growth to the backdoor and pursue human welfare through employment and good enough governance aimed at industrialisation where gaps from state, market, value and socio reality are properly coordinated yet borrowing from neo-classical, dependency, world system and Islamic economics schools. This indeed may be referred to as integral socio-economic development framework with its “dynamic balance”.10

About the Author

Dr. Basheer Oshodi is the Group Head, Sterling Alternative Finance Proposition and he drives the non-interest banking (Islamic banking) franchise in Sterling Bank. He has over 17 years work experience in banking, real-estate and management consultancy. He is a member of the Securities and Exchange Commission (SEC) Alternative Finance Market Master Plan Committee; and a member of the Islamic Finance Working Group – sponsored by EFInA (DFID programme). Basheer holds a B.Sc. and M.Sc. in Estate Management and General Management respectively from the University of Lagos. He has a PGD from the Institute of Islamic Banking & Insurance (IIBI), London and he is an Associate Fellow of the institution.

Dr. Basheer Oshodi is the Group Head, Sterling Alternative Finance Proposition and he drives the non-interest banking (Islamic banking) franchise in Sterling Bank. He has over 17 years work experience in banking, real-estate and management consultancy. He is a member of the Securities and Exchange Commission (SEC) Alternative Finance Market Master Plan Committee; and a member of the Islamic Finance Working Group – sponsored by EFInA (DFID programme). Basheer holds a B.Sc. and M.Sc. in Estate Management and General Management respectively from the University of Lagos. He has a PGD from the Institute of Islamic Banking & Insurance (IIBI), London and he is an Associate Fellow of the institution.

References

1. O’Neill J. 2013. The BRIC Road to Growth. London Publishing Partner.

2. Mazrui, A. 1986. The African: A Triple Heritage. London. Guild Publishing.

3. Oshodi B. A. 2014. An Integral Approach to Development Economics: Islamic Finance in an African Context. Farnham: Gower Publishing.

4. Todaro M. P. and Smith S. C. 2009. Economic Development. Upper Saddle River, NJ: Pearson Education.

5. Evans P. 1995. Embedded Autonomy: State and Industrial Transformation. Princeton, NJ: Princeton University Press.

6. Kohli, A. 2004. State-directed Development: Political Power and Industrialization in the Global Periphery. Cambridge: Cambridge University Press.

7. Hoff, K. and Stiglitz J. 2008. Modern Economic Theory and Development. Washington, DC: World Bank, Development Research Group –Macroeconomics and Growth Groups, Policy Research Working Paper.

8. Thomson Reuters. 2016. Industry at Crossroads: Thomson Reuters Barwa Sukuk Perceptions & Forecast 2016. Thomson Reuters.

9. Thomson Reuters, page 26

10. Lessem R. and Schieffer. 2010. Integral Research and Innovation: Transforming Enterprise and Society. Farnham: Gower Publishing.

Russia’s Red Line

From the Editors

The United States air force attacked the Syrian Arab Army (SAA) troops last month killing 62 soldiers. The attack continued for nearly two hours despite communications from the Syrians and Russians clearly identifying to the Americans that this was not ISIS or any other terrorist group.

Russia regarded this as a clear demonstration that the USA and its coalition allies are not prepared to countenance any intelligence sharing and or alliance that will destroy the terrorists in Syria.

Overthrowing Assad and the Balkanisation of Syria and the creation of pipeline corridors that benefit American regional partners like Qatar still appears to be the ambition for the US and its coalition allies. This is an ambition that has been a central component of US foreign policy and was set in motion as early as 2009 when Assad refused to allow the Qatari/US/Turkish pipeline project in favour of the Russian/Iranian/Syrian project. Since the intervention of Russia, and complemented by Iranian and Hezbollah troops the plans for regime change are presently mired in a dangerous bog of escalation.

And make no mistake about it, Syria is the red line that cannot be crossed by NATO, the US or other regional actors if there is an attempt to repeat Libya and its infamous no fly zone. As the United States Joint Chief of Staff General Joseph Dunford unequivocally told Congress recently, any attempt at creating a no fly zone in Syria would lead to war with Syria and Russia. An order that he is not prepared to give.

Featured image: Syrian army soldiers stand at a site of an explosion in Bab Tadmor in Homs, Syria in this handout picture provided by SANA on September 5, 2016. (Reuters)

Blinded by Nostalgia

By Yuval Levin

Recourse to a glorious past is of course nothing new in political rhetoric. And Americans suggest that a return to that state – that getting back on that track – should be the goal of American politics.

Whatever the argument being advanced about America’s challenges in our politics in recent years, it is a pretty good bet that it has been rooted in an understanding of that lost era of American greatness – that it has been an argument for understanding our challenges as functions of an unfortunate detour.

Recourse to a glorious past is of course nothing new in political rhetoric. But these kinds of appeals do not hearken to America’s Founders and their principles, or to some heroic peaks of achievement and greatness that might inspire us now to live boldly. They hearken to a living memory so powerfully present for many Americans as to seem like the natural state of American life. And they suggest that a return to that state – that getting back on that track – should be the goal of American politics.

The lost golden age at the centRE of these stories occurred in the decades that followed World War II. A great many of our current political, economic, and cultural debates are driven by a desire to recover the strengths of that period. As a result, they are focused less on how we can build economic, cultural, and social capital in the twenty-first century than on how we can recover the capital we have used up. That distinction makes an awfully big difference.

Liberals are especially nostalgic for the economic and political order of that era. Government was growing, the labour movement was powerful, and large corporations in key sectors seemed content to work with government and labour to manage the affairs of the nation.

This kind of analysis is by no means limited to politicians. In fact, it is precisely because such nostalgia characterises the thinking of so many of our most able and important scholars, journalists, commentators, and social analysts that it poses a problem for our capacity for self-diagnosis. Politicians and intellectuals across the political spectrum articulate what we are missing by pointing to what they miss about midcentury America. This inclination is understandable, but its ubiquity means that its blind spots risk becoming our collective blind spots as a nation.

Although liberals and conservatives both frequently look back to midcentury America with fondness, they long for different things about it, and their distinct nostalgias now frequently give our politics its shape.

Liberals are especially nostalgic for the economic and political order of that era. Government was growing, the labour movement was powerful, and large corporations in key sectors seemed content to work with government and labour to manage the affairs of the nation. This combination seemed to deliver broadly shared prosperity for a generation. Meanwhile, a surge in confidence in government led to the Great Society agenda and to a managerial politics that offered a public program to cure every public problem. Economic analysis on the Left now frequently consist of arguments depicting the past forty years as an era of almost uninterrupted decline from that high point – with wages stagnating or falling, inequality climbing, worker protections diminishing, and the middle class getting squeezed. As we will see (especially in chapters 3 and 5), this depiction of key economic trends over that period leaves a lot to be desired. But it often seems like not so much a narrative history as a form of yearning to return.

That yearning is sometimes made remarkably explicit. In 2007, the progressive economist and commentator Paul Krugman, a leading voice on the Left in this century, published a book entitled The Conscience of a Liberal, laying out his basic views of America’s challenges. The book begins with a chapter called “The Way We Were”, which opens with a characteristic example of the sort of homesickness, or longing for a time that got it right, that so pervades many analyses throughout our politics. Krugman’s opening words were: “I was born in 1953. Like the rest of my generation, I took the America I grew up in for granted – in fact, like many in my generation, I railed against the very real injustices of our society, marched against the bombing of Cambodia, went door to door for liberal political candidates. It’s only in retrospect that the political and economic environment of my youth stands revealed as a paradise lost, an exceptional episode in our nation’s history.”1

Krugman then framed his economic and political analysis and his prescriptions as a recipe for a recovery of what that lost era had to offer – understanding its prosperity and promise as functions of the political and economic order of the time, and therefore as recoverable through efforts to reestablish key components of that order in our own day. An extraordinary number of the most prominent works of social analysis in recent years have followed the same pattern – positing the postwar decades as a standard of excellence against which to assess how America is doing by one important measure or another.

An extraordinary number of the most prominent works of social analysis in recent years have followed the same pattern – positing the postwar decades as a standard of excellence against which to assess how America is doing by one important measure or another.

Many, for instance, point to the relatively low levels of inequality in the United States during the postwar years. In 2015, Robert Putnam, a Harvard political scientist known for tracking key social trends, published a book called Our Kids: The American Dream in Crisis that sought to illustrate how things have changed on that front. The book begins with the same now-familiar brand of nostalgia. Here are his opening words: “My hometown was, in the 1950s, a passable embodiment of the American Dream, a place that offered decent opportunity for all the kids in town, whatever their background. A half-century later, however, life in Port Clinton, Ohio, is a split- screen American nightmare.” But also crucial to what Krugman and many others on the Left want to recover from the postwar era is the political vision that gave shape to public policy through much of the 1960s – a robust faith in the potential of welfare-state liberalism to address the nation’s problems.2

And when Democrats translate their aspirations into policy, they tend to follow just that model – seeking to add more rooms onto the mansion of the Great Society through massive legislation that creates large, centralising, new programs empowering the federal government to manage portions of the private economy and provide benefits to individuals. Thus even the policy innovations, such as they have been, in our twenty-first-century politics have been shaped by a hearkening to the great postwar model. When the House of Representatives voted on final passage of the Affordable Care Act (often called Obamacare) in March 2010, House Speaker Nancy Pelosi gavelled the vote closed using the same gavel that Congressman John Dingell had used when presiding over the passage of Medicare in 1965, highlighting the party’s allegiance to the approach to public policy that characterised the Great Society and its era.

When liberals have confronted political resistance to those efforts in this century, they have again tended to return to memories of a lost paradise – this one characterised by political consensus and bipartisan comity. In his 2006 book, The Audacity of Hope, then senator Barack Obama remarked on how powerful the memory of that time was among critics of twenty-first-century Washington. It is, he wrote, “one of the few things that liberal and conservative commentators agree on, this idea of a time before the fall, a golden age in Washington when, regardless of which party was in power, civility reigned and government worked.”3

In fact, liberals and conservatives agree about more than that. They both approach our challenges nostalgically today, even if conservatives yearn for different facets of the postwar golden age. On the Right, it is often not so much the economic consensus of that era that beckons as the cultural or moral consensus – and it, too, has been fading for decades.

Adapted excerpt from THE FRACTURED REPUBLIC: Renewing America’s Social Contract in the Age of Individualism by YUVAL LEVIN. Copyright © 2016. Available from Basic Books, an imprint of Perseus Books, a division of PBG Publishing, LLC, a subsidiary of Hachette Book Group, Inc.

Featured image courtesy of: Gerald R. Ford School of Public Policy, University of Michigan

About the Author

Yuval Levin is the editor of National Affairs and the Hertog Fellow at the Ethics and Public Policy Center. He is a contributing editor to National Review and the Weekly Standard, and his writings have appeared in numerous publications including The New York Times, The Washington Post, The Wall Street Journal, Commentary, and others. He holds a PhD from the Committee on Social Thought at the University of Chicago and has been a member of the White House domestic policy staff (under President George W. Bush). He is the author, most recently, of The Great Debate: Edmund Burke, Thomas Paine, and the Birth of Right and Left (Basic, 2013).

Yuval Levin is the editor of National Affairs and the Hertog Fellow at the Ethics and Public Policy Center. He is a contributing editor to National Review and the Weekly Standard, and his writings have appeared in numerous publications including The New York Times, The Washington Post, The Wall Street Journal, Commentary, and others. He holds a PhD from the Committee on Social Thought at the University of Chicago and has been a member of the White House domestic policy staff (under President George W. Bush). He is the author, most recently, of The Great Debate: Edmund Burke, Thomas Paine, and the Birth of Right and Left (Basic, 2013).

References

1. Paul Krugman, The Conscience of a Liberal (New York: W. W. Norton, 2007), 3.

2. Robert Putnam, Our Kids: The American Dream in Crisis (New York: Simon and Schuster, 2015), 1.

3. Barack Obama, The Audacity of Hope: Thoughts on Reclaiming the American Dream (New York: Crown, 2006), 38. Obama seemed to recognize that these rec- ollections were at least a little too rosy, but six years later, as president, he offered a similar ode to the old consensus. “Yes, there have been fierce arguments throughout our history between both parties about the exact size and role of government— some honest disagreements,” he told an audience in Cleveland, Ohio, in 2012. “But in the decades after World War II, there was a general consensus that the market couldn’t solve all of our problems on its own. . . . In the last century, this consensus—this shared vision—led to the strongest economic growth and the larg- est middle class that the world has ever known. It led to a shared prosperity.” Barack Obama, “Remarks by the President on the Economy—Cleveland, OH,” June 14, 2012, White House, https://www.whitehouse.gov/the-press-office/2012/06/14/remarks-president-economy-cleveland-oh.

The First Presidential Debate and Its Aftermath

by Jack Rasmus

A week ago, on Monday, September 26, the 1st Presidential debate was held. 84 million watched the two most disliked candidates in perhaps more than a century square off and debate.

The one, Donald Trump, a self-proclaimed billionaire wheeler-dealer real estate developer backed by billionaire economic advisers and campaign contributors like sleazy Casino magnate Sheldon Adelson, hedge fund vultures Robert Mercer and John Paulson, private equity king Stephen Feinberg and at least a dozen other billionaires that constitute Trump’s current ‘economic team’; the other, Hillary Clinton, a mere multimillionaire worth a paltry $200 million (not counting her foundations valued at around $400 million), who has accumulated her wealth in just the past decade by means of her (and her husband Bill’s) close connections to investment bankers like Goldman Sachs CEO, Lloyd Blankfein, billionaire hedge fund managers like George Soros and James Simons, multinational tech company CEOs, and billionaire corporate media families like the Sabans, Katzenbergs, and Coxes.

The major economic issues raised in the debates included jobs, trade, taxes and the $20 trillion US government debt. On domestic policy, the focus was racism and gun violence. On foreign policy—Isis, Iraq, NATO, China, first use of nuclear weapons, and Russia.

Taxes and Jobs

Trump proclaimed his plan would cut taxes by $12.5 trillion. He proposed to pay for the cuts by repatriating $5 trillion of cash US corporations continue to hoard offshore. The incentive to repatriate the $5 trillion would be to reduce the corporate tax rate to 5% to 7%, instead of the current 35. But Trump conveniently ignored pointing out this repatriation trick was already played in 2005-06 under George W. Bush. US corporations had accumulated $2 trillion offshore, were given by Congress a “pass” and a lower rate of 5.25% to repatriate so long as they created US investment and jobs with remainder of the repatriated funds. They brought it back, all right, but did not create jobs and instead used the excess profits they realised to buy up companies and pay out dividends to shareholders.

But Clinton carefully did not pick up this issue and use it against Trump in the debate. Why? Because Democrats in Congress are currently proposing the same tax repatriation scam as Trump and Clinton admitted she too supported “repatriation” business tax cuts.

While talking in generalities about taxing the wealthy”, Clinton carefully avoided mentioning that tax cuts for business under Obama have been even more generous than they were under George W. Bush. Bush tax cuts from 2001-2008 amounted to approximately $3.7 trillion – of which it is estimated 80% accrued to businesses and wealthiest households. Obama extended the Bush tax cuts for two years from 2008 to 2010, at a cost of another $450 million, then provided another $300 million in his 2009 bailout package, and then struck a deal with Congress to cut taxes another $4 trillion in January 2013 by again extending Bush’s tax cuts another decade through 2022.

In the debate, both candidates supported the myth that tax cuts create jobs. The only difference between them is which cuts. Trump meant corporate tax cuts. Clinton meant a mix of business and non-business.

And conspicuously missing in the debate was that neither candidate commented on whether they supported the further major tax cuts for corporations being planned to passage right after the November elections. That’s because both no doubt will support it when it comes up for voting in Congress soon following the election.

Both candidates avoided responding directly to the moderator’s question: “Would you support raising taxes or reducing taxes on the wealthy”. Instead of substance, the debate on taxes focussed on whether Trump personally paid taxes and why he refuses to release his tax returns. Clinton kept pressing the subject, scoring points repeatedly as Trump fumbled the issue of his personal taxes. He finally responded to why he hasn’t paid taxes or released his tax records with “I guess that makes me smart” – a remark that will no doubt cost him significant votes.

In the debate, both candidates supported the myth that tax cuts create jobs. The only difference between them is which cuts. Trump meant corporate tax cuts. Clinton meant a mix of business and non-business. But the historical record shows clearly there is no relation between tax cuts in general, and business tax cuts, and job creation in the 21st century. US manufacturing employed 18 million workers in 2000. After nearly $10 trillion in tax cuts, it now employs 12 million. Construction employment has similarly declined. While service jobs have increased since 2000, so too have the ranks of the part time, temporary, and those employed in the underground economy. Together with these ranks of partially employed, more than 6 million more have left the labor force in the US – a net poor return in jobs for the nearly $10 trillion in tax cuts.

NAFTA, TPP and Trade

Trump’s business constituency of real estate and financial interests is less concerned with trade deals than Clinton’s. Trump is also targeting small businesses, which typically don’t export but are harmed by imports, as well as white working class in the Midwest whose incomes have been devastated by free trade deals like NAFTA. However, unlike before the debate, he didn’t declare he would discontinue the existing trade deals. He promised first to stop the further offshoring of US jobs – without explaining how he would do this – and also left unexplained how he proposed to get the millions of jobs previously offshore back to the US. Clinton too provided no details how to get the jobs back or what she would do to stop future bloodletting of US jobs offshore.

While declaring NAFTA as “defective”, Trump simply added “we need to renegotiate trade” – a position little different from Clinton’s that we “need to take a new look at trade”. The debate thus talked in generalities that leave the door open after the election for either to support the TPP and undertake token reforms at best regarding NAFTA. More revealing of Clinton’s true intentions perhaps was her off the cuff comment that she’d vote again for CAFTA (Central American Free Trade Agreement) if given the opportunity.

Debt and Defence Spending

Trump several times during the debates referred to the nearly $20 trillion in US national debt. But what he failed to mention is that studies show about 60% of that debt is due to tax cuts and declining US tax revenues. Another $3 trillion at least is due to US war spending since 2003. Yet in the debate Trump called for accelerated war spending, while Clinton said nothing about whether she would increase war spending or reduce it. Her silence spoke volumes on that topic, however, as did her repeated references to the need to confront Russia and China. While Trump directly indicated he would not use nuclear weapons first, Hillary avoided answering the moderator’s question, implying perhaps she would, which has been the US official position to date.

The Silly Subjects

Much of the time of the debate was also consumed by extensive discussion of such silly issues as whether Obama was born in the US, whether Hillary had the “stamina” to be President or Trump the “temperament”, Trump’s personal bankruptcies, and whether each would accept the outcome of the vote.

The Missing Debate

More important perhaps than what was said was what was ignored and not discussed by the candidates during the debate – like the stagnating and declining incomes of tens of millions of working and middle class Americans since 2000, the simultaneous approximate 10 trillions of dollars in capital gains, dividends and interest income obtained by the wealthy 1% over the same period, the collapsing pension and retirement systems today in the US, the increasingly unaffordable rents and healthcare insurance costs, US drug companies’ price gouging and unraveling of Obamacare, the US central bank’s policy of low interest rates destabilising the economy, the consistent violation of regulations by bankers, the new US military adventures now being prepared for Russia’s east Europe border and China’s coast, the militarisation of US police forces, what to do about racism and gun violence besides meaningless calls to ‘improve community-police relations’. Nothing was said about global climate crisis by either candidate; nor about the opaque manipulations, by both candidates, of their personal foundations for political use.

The Aftermath

In the days immediately following the debate, the general consensus was that Trump’s rambling and unfocused responses to Clinton meant he had clearly performed poorly and had lost the debate. Clinton recovered in the polls, pulling even or just a few points ahead in national polling and assuming a slight lead in several of the “swing states”. But with 87% of voters having already decided, national poll results are largely irrelevant, and the margin of error in the polling in the swing states still remains so narrow, post-debate, that it is insignificant in most of the swing states.

How is it that Trump could have performed so poorly in the TV debate and the race still remain so close? What the past week does show is that despite Trump doing all he can to put his foot in his mouth, and help Clinton with outrageous sexist and racist statements, there still remains a large, widespread and hardened discontent with Clinton. The first debate should have clearly “put Trump away”, and locked in an eventual November victory for Clinton, but it hasn’t. Which candidate turns out its traditional base to vote in November in the swing states still remains the key element for who wins the election.

Given that strategic reality, it’s not surprising that Clinton in the past week has intensified efforts toward trying to convince millennials to turn out to vote for her. A Democrat Party “full court press” has been launched targeting the under-35 voters, many of whom had defected to Sanders in the primaries as well as to the Libertarian candidate, Johnson, and Green Party candidate, Jill Stein.

The first debate should have clearly ‘put Trump away’, and locked in an eventual November victory for Clinton, but it hasn’t. Which candidate turns out its traditional base to vote in November in the swing states still remains the key element for who wins the election.

In synch with this effort, this past week the anti-Trump mainstream corporate media has stepped up its critique and efforts to marginalise both Johnson and Stein, pressing the old theme that “a vote for a third party is a vote for Trump”. The past week Clinton campaign thus began mobilising Sanders and liberal darling, Elizabeth Warren, having them tour college campuses pitching the theme to millennials to “get out and vote”. Simultaneously, Clinton herself has begun to prioritise themes of college tuition and child care more in her speaking engagements and in her media advertising. In the remaining weeks before the election, watch for the Clinton camp to launch new initiatives as well to shore up her weak base among white working class voters in the Midwest swing states, and among Latinos there and in Florida, Virginia-Carolinas, Colorado-New Mexico-Nevada.

The Clinton campaign has clearly not yet turned out the defections of the youth, under-30 vote, lost during the primaries. Nor has it been able to excite Hispanics and Latinos as did Obama in 2008 and 2012 with false promises of Dream Acts and Immigration justice. And the white, non-college educated working class in key Midwest states remains all but lost to Trump for good.

The continuing hard core discontent with Clinton has its roots not only in her own political record on war, trade, and her intimate ties to the banking and corporate elite, but in the poor economic legacy left by Obama policies and programs over the past eight years. Clinton presses her point the US economy has not been as bad as Trump claims, but for many constituencies – especially youth, minorities, and non-college educated white workers – it is not believable. In fact, for many it has been a disaster. But you won’t hear that truth from the mainstream corporate media or the Clinton camp.

Behind Clinton’s troubles in this election is the “gray eminence” of failed Obama economic and social policies that Democrats refuse to own up to – i.e. creation of only low pay, part-time, temp and “gig” service jobs with no benefits, crushing levels of student debt, escalating rents and health insurance costs under Obamacare, declining savings for tens of millions of retirees after eight years of near zero interest rates by the Federal Reserve under Obama, continuing free trade destruction and offshoring of US manufacturing, millions of homeowners still “under water” on their mortgages, chronically rising household debt, perpetual wars in the middle east, intensifying racism and police violence throughout the US, record levels of immigrant deportations, etc. – in other words, the “legacy of Barack Obama”, which hangs like a thick political fog over the Clinton campaign threatening key constituency voter turnout while holding up support for Trump despite his best efforts to scuttle his own campaign with his mouth.

This article was first published on counterpunch.org on October 4, 2016

Featured image courtesy of: www.nytimes.com

About the Author

Jack Rasmus is the author of ‘Systemic Fragility in the Global Economy’, Clarity Press, 2015. He blogs at jackrasmus.com. His website is www.kyklosproductions.com and twitter handle, @drjackrasmus.

Jack Rasmus is the author of ‘Systemic Fragility in the Global Economy’, Clarity Press, 2015. He blogs at jackrasmus.com. His website is www.kyklosproductions.com and twitter handle, @drjackrasmus.

The Informal Sector in India: Prosperity or Persistence of Misery?

By Saumya Chakrabarti, Daipayan Sarkar and Ankita Biswas

Based on the recent publication of Saumya Chakrabarti’s Inclusive Growth and Social Change: formal-informal-agrarian relation in India (2016) published by the Oxford University Press, the article offers a critique of the “inclusive growth” programme from the perspective of India’s non-agricultural informal sector.

It is widely recognised now, that India is one of the fastest growing countries of the world. Internationally, Indian economy is attracting huge attention for its growth stories. But, despite this prolonged growth process of over two decades a very large part of the Indian economy is suffering badly with acute under-employment and human-underdevelopment. Indian economy actually posits a paradox: while the macro-economy, at the surface, shows enormous agility and the “mainstream” economy is truly “shining”, there is an ever-growing problem of ballooning misery in the fields of petty agriculture and also in the non-farm informal sector. It is true that, with growth, some parts of the population is moving out of agriculture, but, these people are unable to get engaged in the remunerative formal/modern activities – the advanced manufacturing and services; contrarily, most of these migrants are compelled to throng the under-remunerative rural-urban informal sectors. Thus, instead of a so-called comprehensive transformation of the Indian economy towards an inclusive capitalistic environment, a deep “dualism” persists stubbornly and at times, it is even being reproduced and aggravated: along with growth and prosperity of the fortunate few a very large part of India goes on languishing.

In this very context, we posit our following critical analysis of the Indian non-agricultural informal sector. We start with the fundamental question: Is India able to achieve a growth process in which people, in different walks of life, feel that they too benefit significantly from the ongoing transformations?

India is huge in terms of its diversity and population. The formal sector consists of people working in large traded companies, incorporated or formally registered entities, corporations, modern factories, shopping malls, hotels, and large and modern businesses. On the other hand, the non-farm informal sector refers to economic activities such as owner manned petty/kirana stores, handicrafts and handloom workers, rural-urban petty traders, petty manufacturing and repairing etc. It is believed that the informal sector has a huge promise for the betterment of living standards for the people engaged in its different segments (especially when agriculture is reeling under deep crisis).

Indian economy actually posits a paradox: while the macro-economy, at the surface, shows enormous agility and the “mainstream” economy is truly “shining”, there is an ever-growing problem of ballooning misery in the fields of petty agriculture and also in the non-farm informal sector.

Is that so in reality? Our detailed empirical study projects rather a gloomy picture, especially for the overwhelmingly large rural-urban self-employment segments of the Indian informal sector. While the formal/modern sectors and the people associated with it are able to reap the benefits of globalisation and growth, the overwhelming majority of the informal sector population is found to be unable to gain out of these processes. While the volume of informality is ballooning, only the larger firms with better asset-positions and locational advantages are able to prosper; and contrarily, the vast segment of petty self-employment is found to suffer or even lose! These bare facts push us for a critical analysis of the Indian informality.

We question certain crucial aspects of the projected process of “inclusive growth” in India and ask specifically, why the vast informal sector of India could not be included into the mainstream of economic activities, despite a high growth rate of the economy driven by its formal/modern sectors. There remains an element of doubt over the proposed “win-win” scenario, for both the formal and informal sectors, as posited by the mainstream literature. It has been argued time and again that, with the help of a well-functioning government, the efficient market can lead to an optimum allocation of scarce resources, through which not only the formal sector but also the informality can benefit. But, our observations do not strengthen such enthusiasm for the informal sector; it rather leaves behind a marked dose of disappointment. On the main, the reason underlying the abysmal performance of the informal sector may be the complex formal-informal relationship. The detailed process could be delineated as below:

Focusing on the inter-sectoral associations in India, one can find that there is a positive relation between the formal sector and the urban informal sector through the demand and supply side linkages. However, the formal sector and the rural informal sector are two disjointed categories, as far as direct exchange relations are concerned. Further, both the urban and rural informal sectors are found to be positively related to the small-and-marginal-farming based agriculture. Finally, while the formal sector and the urban informal sector are associated with aggregate economic activities, the rural informal sector is found to remain largely isolated.