By Eduardo Cavallo and Tomás Serebrisky

The Latin American and Caribbean region is trapped in a vicious cycle of low savings and poor use of these savings. This article discusses strategic goals for households, firms, and governments across the region to reverse the cycle.

Why should people – and economies – save? The typical answer is to protect against future shocks, to smooth consumption during hard times, in short, to save for the proverbial rainy day. But the question can be approached from a slightly different angle. While saving to survive the bad times is important, saving to thrive in the good times is what really counts. The goal of saving should be to pave the way for individuals to live more productive, fulfilling lives, for firms to grow and provide quality jobs and competitive goods and services, and for government to assure their citizens enjoy a developed infrastructure, efficient public services and a dignified, secure retirement. In short, countries must save for a sunny day – a time when everyone can bask in the benefits of growth, prosperity, and well-being.

To have even a chance of reaching that sunny day, Latin America and the Caribbean must save more and save better. Saving in the region is too low and the savings that do exist are not used efficiently to enhance growth and development. Borrowing from abroad cannot pick up the slack as it may be more costly, is certainly more fickle, and raises the risk of crises. Ultimately, national saving is the only reliable vehicle through which the region can become stable and confident in its own future.

Unfortunately, countries in Latin America and the Caribbean save less than 20 percent of their national income – less than every other region in the world, except Sub-Saharan Africa. By contrast, the high-growth countries in East Asia save about 35 percent of national income (See Figure 1 below). The region is not putting aside enough resources today to build a better, brighter tomorrow.

Sharing the Blame for Low Saving

If saving is so important for growth and development, then why does Latin America and the Caribbean do such a poor job of it? Demographic factors – such as the number of working to non-working age people in a country at a given point in time – matter for saving, but they are not to blame for the region’s low saving rates. Beginning in the 1960s, the region embarked on a “saving-friendly” demographic transition (with decreasing age dependency ratios), very much like high-saving countries in Asia. In 1965, for each 100 individuals of working age, there were 90 dependents, either young or old; today there are fewer than 50. Yet, unlike Asia, national saving rates in Latin America have increased little. If favourable demographic factors had been fully exploited, the average saving rate in the region should be about 8 percentage points of gross domestic product (GDP) higher.1

Various nondemographic factors have kept the saving rates down, despite the demographic bonus. One is the lack of adequate saving instruments. The perennial problems of lack of trust in financial institutions and high costs of doing business with banks discourage households from placing their savings in formal financial institutions. Only about 16 percent of adults in Latin America report saving through a bank, compared to 40 percent in Emerging Asia, and 50 percent in advanced economies.2 Instead, households in the region – especially relatively poorer households – save more through informal mechanisms, or just give up on saving altogether.

The state of the region’s pension systems has also depressed saving. They cover less than half the population and face long-term sustainability challenges. Most people in Latin America and the Caribbean do not save through pension systems, or they do not save for enough years to qualify for a contributory pension at the end of their working lives. Importantly, they do not compensate with higher voluntary saving. The pension crisis in the region is effectively a saving problem, with serious social implications.

Fiscal policy has also been a drag on saving. On the one hand, distorted incentives bias public expenditures toward current spending (consumption) and away from capital investment (saving) over the economic cycle. In good times, political economy incentives encourage governments to increase spending across the board. In bad times, they usually find it politically more expedient to cut capital expenditure projects than other expenditures. Total expenditure in Latin America from 2007 to 2014 increased a whopping 3.7 percent of GDP, but more than 90 percent went into current expenditure, and only 8 percent to longer-term public investment.

A second public finance issue is considerable leakage in spending areas such as social assistance, tax expenditures and subsidies to energy. Rather than limiting their assistance to those who truly need it, government programs end up benefiting the nonpoor to the tune of about 2 percent of GDP in the region. Inefficiencies in health and education spending average another 1 percent of GDP. These leakages and inefficiencies are in essence public saving that is forgone.

Taxation also directly impacts saving because tax revenue is one of the components of public saving. And it indirectly impacts saving through the incentives it provides to individuals and firms to save. Widespread tax evasion – about 52 percent of potential tax collection in the region – is a problem on both fronts: it reduces tax revenues, and it distorts the incentives of compliers versus noncompliers.3 Many countries impose a high tax burden on complying taxpayers but collect relatively little in tax revenue (as a share of GDP). This is the worst possible combination for saving: a tax system that imposes very high tax rates (thereby distorting private saving decisions) and collects very little revenue (thereby adding little to public revenue and public saving).

Distortions in financial markets such as the high cost of enforcing contracts, or the lack of information about the creditworthiness of potential borrowers, raise the cost of credit for productive firms. This limits the ability of firms with good investment projects to invest and grow. The result is a misallocation of economic resources and lower aggregate productivity. This, in turn, generates disincentives to save because an economy with low productivity growth is essentially an economy in which returns to saving and investment are also low. Distortions beyond financial markets also matter. Labour markets distorted by high levels of informality, inefficient or inequitable social policy regulations, special tax regimes, or a combination of these factors, change the private profitability of investment projects and lead to socially inefficient investments. Removing these distortions would increase productivity, investment, and savings.

How to Promote Saving for Development

The Inter-American Development Bank’s latest flagship publication, Saving for Development: How Latin America can Save More and Better, outlines how to increase saving for the future in sustainable ways. A comprehensive agenda combines public policies to stimulate saving directly, such as measures related to fiscal policy and pensions, with policies that operate indirectly by removing constraints.

Tackle the pension problem. A solution to Latin America’s saving problem requires fixing broken pension systems. Countries have promised to pay very generous pensions to their retirees, but they have not saved enough to fulfil those promises. The public debate in the region largely revolves around whether pension systems should be based on individual accounts (fully funded) or pay-as-you-go (PAYGO) approaches. However, this debate ignores the reality of the region’s labour markets. Both systems suffer from a lack of inclusion. More than half of the labour force is informally employed, meaning they don’t contribute to pensions. Among the lowest three deciles of income distribution, that figure is as high as 90-95 percent.

Resolving the pension problem requires adjusting the systems’ parameters, such as the retirement age, level of benefits, and required years of contributions. Perhaps more importantly it requires structural changes, beginning with tackling labour informality and its disastrous consequences.

Focus on capital spending. Over the last two decades, improved fiscal frameworks have delivered higher public saving in many countries. Yet more effort is needed just when a challenging economic environment makes doing so more difficult. The good news is that substantial public saving can still be generated without having to rely on the traditional tools of raising taxes or reducing expenditures across the board. Governments have room to boost public saving by increasing the share of capital expenditures, which is low in the region, with respect to current spending, which is high. Moreover, additional resources can be devoted to increasing capital expenditures if governments eliminated leakages in spending programs such as social assistance, tax expenditures and subsidies to energy (that means making sure that spending reaches its intended beneficiaries only). Leakages due to poor targeting of spending programs add up to approximately 2 percent of GDP on average.

Target tax policy better. Income taxes are levied on both individuals (personal income tax) and firms (corporate income tax). But households collectively own firms; therefore tax policy should integrate personal and corporate income taxes, and avoiding double taxation of savings: first, when it is generated by the firm, and then when it is distributed to households as dividends. Personal income taxes across the region should continue evolving into a dual system, with a lower flat tax on capital, in which all forms of capital income (interest payments, dividends, and capital gains) receive equal tax treatment. Corporate income tax rates should fall in line with international trends to facilitate the formalisation of informal firms. This would help expand the tax base, which is currently low.

Promote household saving and create a savings culture. At the household level, saving rates in the region are distorted by a number of factors: high costs of accessing and using the financial system; lack of confidence in the financial system; poor financial regulation; little understanding about banks and how they work; and social pressures and behavioural biases. Successful financial inclusion requires more than just opening new bank accounts. It means tailoring saving products to the demands of potential clients, taking into account the various real-life constraints they face to save, and creating incentives to channel more savings through the formal financial system. Public policy interventions and financial product innovations has been shown to increase household saving and encourage more financial saving in particular. Making more and faster progress in these areas requires more dynamic regulation and supervision of the financial system and the collaborative efforts of financial regulators and bankers to implement reforms and promote even more innovation.

Government initiatives to pay social transfers through bank accounts and to channel remittances through domestic financial systems are useful first steps. Additional progress in encouraging more financial saving demands improvements in the design of the programs: for example, by pairing payments with programs that provide financial education, and/or with instruments to help users overcome the behavioural and social biases that constrain saving. Innovation and technology provide another opportunity to encourage more saving through the formal financial system. While the penetration of mobile telephones is high in Latin America and the Caribbean, the region still lags behind in using mobile technology for financial services because policy and regulations have not kept pace with the mobile telephone revolution.

A promising avenue for creating a saving culture in Latin America and the Caribbean is financial education, with a focus on children and youth. Positive saving habits are easier to instil during the early years, when the brain is still developing and learning is easier.

Fix the financial system. Efforts to create a culture of saving must be complemented by efforts to help the financial system pool and allocate savings efficiently. Only by fixing the problems that discourage the use of financial systems for saving and limit the availability of financing for productive firms, can more saving turn into better saving for development.

Financial frictions are like sand in the wheels of the economy; they slow down economic progress. Two types of financial distortions are particularly acute in Latin America and are amenable to policy action. First, banks do not have access to quality information about potential borrowers. While the region has made headway in extending the coverage of credit bureaus that provide this information, the quality and timeliness of the information is still poor in many countries. On average, the regulatory framework in Latin America is less conducive to information sharing than in other regions of the world.

A second problem is the high cost of enforcing financial contracts in the region. The effective protection of property rights is particularly weak in Latin America. Fortunately, examples of successful reforms in the region have helped alleviate this constraint.

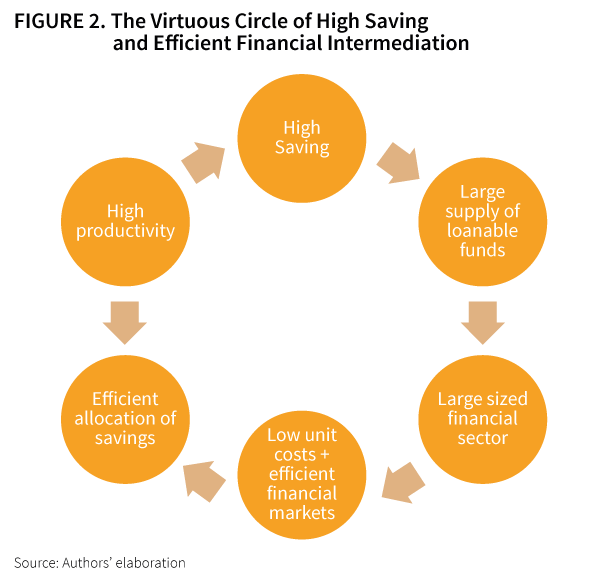

The Virtuous Circle

The key is to create a virtuous circle (Figure 2 below) in which more savings generate more loanable funds, bigger and more efficient financial systems, a better channeling of resources, and higher productivity. Those steps would generate higher savings still and the wheel would keep turning, leading to more development with greater social inclusion.

Featured image: Brokers work at the Buenos Aires Stock Exchange in Buenos Aires, Argentina. Latin America and the Caribbean will post an economic contraction in 2016, the International Monetary Fund forecast in a report issued Wednesday, April 27, 2016. Photo courtesy: AP Photo/Victor R. Caivano, File

About the Authors

Eduardo Cavallo is a Lead Economist at the Research Department of the Inter-American Development Bank (IDB) in Washington, DC. His research interests are in the fields of international finance and macroeconomics with a focus on Latin America. He holds a PhD in Public Policy from Harvard University and a BA in Economics (magna cum laude) from Universidad de San Andrés in Buenos Aires, Argentina.

Eduardo Cavallo is a Lead Economist at the Research Department of the Inter-American Development Bank (IDB) in Washington, DC. His research interests are in the fields of international finance and macroeconomics with a focus on Latin America. He holds a PhD in Public Policy from Harvard University and a BA in Economics (magna cum laude) from Universidad de San Andrés in Buenos Aires, Argentina.

Tomás Serebrisky is the Principal Economic Advisor of the Infrastructure and Environment Department of the Inter-American Development Bank (IDB) in Washington, DC. His specialisations a re the economics of infrastructure investment, Public Private Partnerships, and economic regulation. Tomás holds a PhD in Economics from the University of Chicago and a BA in Economics (summa cum laude) from Universidad de San Andrés in Buenos Aires, Argentina.

re the economics of infrastructure investment, Public Private Partnerships, and economic regulation. Tomás holds a PhD in Economics from the University of Chicago and a BA in Economics (summa cum laude) from Universidad de San Andrés in Buenos Aires, Argentina.

References

1. Cavallo, E., G. Sánchez, and P. Valenzuela (2016). Gone with the Wind: Demographic Transitions and Domestic Saving. IDB Working Paper, no. 688. (Department of Research and Chief Economist, Inter-American Development Bank, Washington, DC).

2. World Bank’s Financial Inclusion (FINDEX) database. World Bank (2014). Global Findex Database. Database. Available at http://datatopics.worldbank.org/financialinclusion/. (World Bank, Washington, DC). Accessed February 2016.

3. Corbacho, A., V. Fretes Cibils, and E. Lora, eds. (2013). More than Revenue: Taxation as a Development Tool. Development in the Americas series. (Washington, DC: Inter-American Development Bank and New York, NY: Palgrave Macmillan).By Eduardo Cavallo and Tomás Serebrisky

{kind=link}