By H. Kent Baker, Hugo Benedetti, Ehsan Nikbakht, Sean Stein Smith, and Andrew C. Spieler

Blockchain is a growing technology that started in the cryptocurrency sphere with bitcoin but expanded to many business fields and beyond. In contrast to a traditional database, blockchain extensively uses cryptography (i.e., writing security codes) and permanently maintains the data. Although many industries worldwide use blockchain for various purposes, we discuss financial applications in the financial services, real estate, and accounting and auditing sectors. Before examining these applications, let’s review some basics about blockchains.

The Anatomy of Blockchains

This section provides an overview of blockchain’s essential elements and presents some additional features tailored to specific use cases. As Figure 1 shows, a blockchain has five key elements: (1) a block structure, (2) a chain sequence, (3) a cryptographic process, (4) a distributed or replicated configuration, and (5) a consensus mechanism.

The block structure refers to the approach used to record data. Think of each block as a filing cabinet containing a cabinet/block number used to identify it, a reference to the previous cabinet/block summarizing its data, the data to be stored in the blockchain, and a timestamp registering the date and time of the cabinet/block creation.

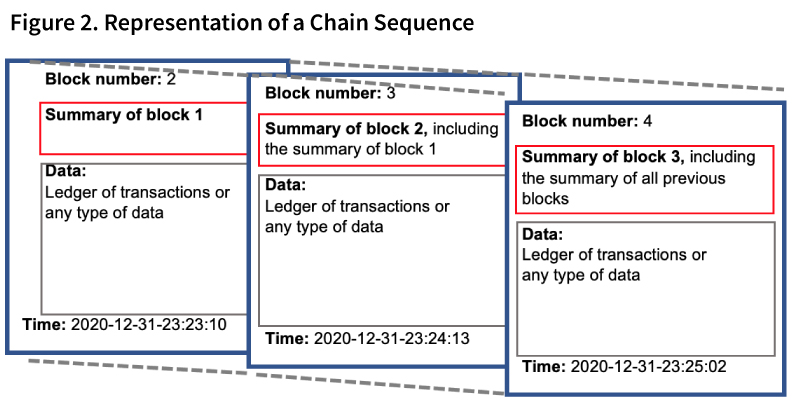

The chain sequence implies a strict ordering of blocks. Each new block of data is ordered sequentially and includes a summary of the previous block’s data. As the last block also contains a summary of its previous block, the chain sequence creates a recursive data recording process. Thus, each block includes a trace of data from all previously recorded blocks. Figure 2 shows a block’s contents and its link in the chain sequence.

The cryptographic process is a data transformation process that creates a unique summary of each block. This transformation uses a one-way deterministic function called a “hashing function” to reduce the stored information’s length to a predetermined number of bytes. The “one-way” qualification means that undoing the transformation is impossible with current technology. The deterministic qualification means that transforming the same input always results in the same output. However, different inputs could lead to the same output, underscoring the difficulty of undoing the transformation. The most used function is the SHA-256 (secure hash algorithm), which reduces any length of data to 256 bytes. The summary of previous blocks corresponds to the hashing process result, called a block’s “hash.”

Thus, a blockchain is a data storage structure that records information on sequential blocks linked together by including the previous block’s hash. Each block contains the hash of its last block, which cryptographically links all blocks. These elements help secure the block’s data. If a block writer modifies data within a block, the block’s hash changes. Most importantly, it changes the hash stored in all subsequent blocks. Data tampering, therefore, becomes evident.

A blockchain is a data storage structure that records information on sequential blocks linked together by including the previous block’s hash.

The fourth element – the distributed or replicated configuration – enables multiple parties to record the blockchain simultaneously. In a replicated blockchain, each participant stores a full copy of the blockchain, while in a distributed blockchain, each participant stores a segment of the blockchain.

The consensus mechanism refers to the rules and incentives to ensure adherence to basic blockchain guidelines. For example, what type of information can a block writer record? Which parties can record and modify data? How do parties agree if they detect different versions of the blockchain?

The last two elements create an additional layer of data security by maintaining several copies of the blockchain. Manipulating data modifies the block’s hash and the following blocks in one of the copies but not others. The consensus mechanism allows the blockchain storing parties to agree on which version of the blockchain is correct.

Blockchain’s five key elements work in unison to provide a secure data storage infrastructure, which can be enhanced to accommodate specific requirements. Some of these features include data and block encryption; differentiated user, validator, and data storage access; interconnections with other blockchains, registries, or physical devices via the Internet of Things (IoT); and a programable blockchain language. The list of potential features continues to expand due to increased research and development in the area.

Financial Services Applications

Blockchains and the associated distributed ledger technology (DLT) can potentially improve many aspects of financial services. For example, record-keeping, shareholder voting, and trade confirmation are time-consuming and subject to human error and potential fraud. Real-time access to transactions and verifiability offer marked improvements. Distributing the data across interested parties reduces and sometimes eliminates the need for centralized marketplaces or intermediaries. This section discusses specific blockchain applications for shareholder voting, dividend payments, foreign exchange transactions, and insurance markets.

Shareholder Voting

Although shareholder voting is primarily electronic, the current system is fragmented and inefficient. Large shareholders tend to vote to support their interests, but small shareholders are often apathetic. Shareholders can vote in various ways, including using a paper ballot, submitting electronically, attending the annual meeting, or proxying votes to a third party. Because maintaining accurate voter rolls is difficult for companies, brokers manage the ownership records in street name. Methods to are available to reduce the current system’s substantial costs involving mailing materials, engaging a proxy solicitor to contact shareholders to meet quorums, and tabulating results, including vote changes. Companies with multiple share classes and time-phased voting rights further complicate the process. Thus, blockchain technology transparency increases shareholder involvement by improving corporate governance, reducing fraud, increasing accountability, and lowering capital costs.

Dividend Payments

The dividend cycle is similar to shareholder voting with redundancies and inefficient record-keeping. The dividend cycle begins when the board of directors declares a dividend (declaration date) and ends with cash or stock distributions. The board also announces the payment date. Cash payments occur via check or bank deposit to the shareholder owning the shares on the record date (holder of record). Between the declaration date and payment date lies the ex-dividend date and holder-of-record date. The ex-dividend date is the last date the shares trade with the dividend, typically one day before the record date. That is, the holder-of-record receives the dividend when the company eventually distributes it. A blockchain can improve the process by distributing the dividends instantaneously into all eligible wallets, withholding or directing tax payments, and identifying the holder-of-record. Blockchains can also benefit international investors where companies make payments in other currencies or situations with different tax rates.

Additionally, companies can pay dividends using different tokens, such as Ethereum, or stablecoins.

Foreign Exchange Transactions

The foreign exchange market, also known as forex, FX, or the currency market, is a vast, decentralized, primarily unregulated market dominated by large institutional players, central banks, and corporations. Trades occur in the spot market for immediate delivery and the forward market for delivery at a future date. The foreign exchange market also includes derivative transactions, including options and swaps. Each trade involves considerable paperwork involving front, middle, and back-office personnel. Further, each trade requires counterparty verification. Each counterparties’ custodian and other interested parties receive information on the trade. Netting of positions occurs to reduce the transactional burden and movement of funds. Permission-based blockchain systems can track position sizes and reduce pricing errors. Therefore, blockchains could transfer and store (“capture”) information about the trade and transfer and store value/currencies directly. For example, JP Morgan developed JPM Coin, a permissioned, shared ledger platform, to allow real-time cross-border USD customer deposits.

Another advancement is Hyperledger (HL), a global enterprise blockchain project offering the necessary framework, standards, guidelines, and tools to build open-source blockchains and related applications for use across various industries. HL intends to be self-sustaining, governed by a collective to maintain and update the network. The primary features include modularity, security, interoperability, cryptocurrency agnostic, and API-friendly. In 2018, Goldman Sachs and Morgan Stanley began using the DLT payment netting service called CLSNet, which may signal increased popularity in the future. More recently, JP Morgan, Citigroup and BNP Paribas joined CLSNet. Benefits include broader market participation, improved intraday liquidity, and risk mitigation for non-CLS banks.

A blockchain solution is also available for other insurance types, including flight insurance. Suppose an airline agrees to pay a fixed amount based on a predetermined condition, such as a flight delay.

Insurance Markets

The insurance industry can also benefit from blockchain technology. Consider life insurance, which is a contract between the insured (payee) and the insurer (responsible party) to make payment to the beneficiary upon a verifiable event (e.g., death of the insured). The blockchain stores the contract terms and payment history. One concern with life insurance is that a lengthy process is required to provide payment if a death benefit is due, but the beneficiary is unaware. Entrusting a third-party with permissioned access to the blockchain allows the third party to identify the event and provide an almost seamless payment to the beneficiary.

A blockchain solution is also available for other insurance types, including flight insurance. Suppose an airline agrees to pay a fixed amount based on a predetermined condition, such as a flight delay. The flight delay is stored in a public record and easily verified. Similarly, reinsurance companies (insurance for insurance companies) benefit from the blockchain by the trusted record-keeping. Companies often use reinsurance for catastrophic events. It also helps assess the severity by aggregating the losses. Blockchains are a natural solution since companies typically make payments after reaching an aggregate loss level.

Despite the intense competition among insurance companies, the industry is collectively better off by having access to aggregated data stored on a shared blockchain. For example, suppose each company experiences a small number of health-related payouts with no discernible pattern between the seemingly unrelated claims. Analyzing the chain may reveal clusters of similar payouts indicating an environmental problem like a cancer cluster.

Real Estate Applications

Real estate consists of various forms, such as residential properties, commercial properties, and real estate investment trusts (REITs). When buying or selling residential and commercial properties, the acquisition process requires numerous and cumbersome sequential steps. After negotiation between a buyer and a seller for the price and terms, parties exchange a series of memos, documents, and addenda before closing a final deal. The acquisition process may involve many participants: the initial buyer (investor), the seller, the legal team, construction or remodeling firms, engineers for inspections, escrow agents, home insurance companies, title insurance companies, banks, home appraisers, state and local agencies for variances and compliance with local codes, environmental agencies, and town clerks for recording and updates.

Blockchain technology offers opportunities and challenges. On the positive side, blockchain can streamline all or part of the transaction process to acquire and manage real estate properties. Its unique features, including immutability (i.e., data cannot be deleted or altered), contribute to making the real estate transaction process more efficient and accurate. If appropriately used, blockchain is a tool to avoid misunderstanding among parties or potential grievances and help to resolve lawsuits since all transactions are permanently recorded and available to the parties, courts, and regulators if needed. A well-developed blockchain platform can help with due diligence in protecting buyers, sellers, and local authorities’ rights to ensure compliance and resolving variance issues.

Advanced features of blockchain can enhance the existing electronic recording systems used for real estate transactions. It can incorporate all incremental additions and deletions into the block permanently and then review and retrieve them as needed. Thus, blockchain developers have ample opportunities to examine current deficiencies and develop efficient alternatives for real estate transactions.

However, applying blockchain in the real estate industry has challenges. In many municipalities, the ownership and recording data are often incomplete or difficult to retrieve for verification. In most cities, the delivery of property deeds still uses traditional mail. Data are not fully digitized, or if digitized, they do not follow universal standards and are subject to alteration. Searching for real estate data and historical transactions underlying the asset can be cumbersome.

Blockchain applications may also extend to the financing part of real estate. After the initial financial transactions, including second, third, and other mortgages, blockchain allows maintaining data sequentially, broadcasting the data to all parties, and tracing and retrieving the data through blockchain layers if questions arise. Cases exist where a borrower (the property owner) went through multiple lenders for second or third mortgages without the first borrower’s full consent. Blockchain can help avoid such possible unauthorized actions. As soon as a buyer applies for an additional loan, blockchain automatically transfers the information to all parties, such as banks and insurance companies. The process cannot continue without the full consent of prior lenders and title insurance companies. Thus, blockchain can make real estate transactions more transparent and cost-effective for all parties involved

Accounting and Auditing Applications

Blockchain and crypto assets possess far-ranging applications and use cases outside of financial services and real estate. However, realizing the full potential of these technologies requires meeting two conditions. First, the accounting and reporting of blockchain information must be consistently applied and reported across various market actors. Second, the processes confirming or auditing this information must be consistent and replicable in a blockchain-based business environment. Broader use of blockchain and crypto-asset applications requires examining these issues.

Accounting

Although crypto assets, especially cryptocurrencies, are the highest-profile example of blockchain technology, tax and reporting rules remain ambiguous. In the face of no specific guidance from either the Financial Accounting Standards Board (FASB) or the International Accounting Standards Board (IASB), a market-driven approach has resulted in classifying cryptocurrencies as intangible assets. Although this approach seemingly makes sense because cryptocurrencies are assets and are also intangible, implementing this approach generates several unanswered questions. For example, how should these intangible assets be tested for impairment? How often should this impairment testing occur? What exchange price is appropriate since the cryptocurrency marketplace has no opening or closing bell? This classification as an intangible also leads to uncertainty. For example, what happens if, after a write-down or impairment in value, the recovery price exceeds the previous high-water mark, the highest price that the cryptocurrency has reached.

Classifying cryptocurrencies as intangible assets raises another issue. Given that not every crypto asset is equivalent, they should not be valued, reported, and treated in the same way. Many view crypto assets and cryptocurrencies as an all-encompassing term, but substantial differences exist. The market contains decentralized cryptocurrencies, privately-issued stablecoins, coins and tokens linked to tokenized physical assets, and potentially central bank digital currencies. Treating these assets as equivalent is illogical and inconsistent with treatments for other asset categories. Besides a lack of consistent guidelines and reporting rules, the existing rules and frameworks can vary widely depending on the jurisdiction.

Auditing

Although blockchain technology has potential use cases in many economic sectors and industries, auditing and attestation are where use cases seem to be accelerating in terms of implementation. The fundamental traits of blockchain – traceability, transparency, encryption, consensus methodologies, and real-time updates – already affect the audit processes. An effectively operating blockchain creates a tamper-resistant record available to network members when updated and agreed upon by those same network members. Implementing a blockchain-based or blockchain-augmented data-sharing platform does not render the audit or audit processes obsolete or irrelevant. Instead, it reallocates the time and resources involved in the audit process to cybersecurity or technology-focused role.

Some basic tasks and processes will be rendered less necessary, but doing so does not mean that an audit has value or benefit diminishes over time. Instead, increasingly integrating blockchain into business operations will change some audit tasks. Specifically, the auditor’s role and the audit process need to evolve, focusing less on the information itself and more on how to add to and export data from the blockchain. This process is already underway at many large accounting and audit organizations, which increases the confidence and transparency in this information over time.

In summary, the accounting and auditing of any information form the basis for treating, reporting, and storing data. A consistent and comprehensive accounting and auditing process may foster wider blockchain adoption. No blockchain or crypto-specific guidance or rules are available on how to account for or audit these data. Obtaining blockchain’s full benefits requires developing comprehensive accounting and audit frameworks. Accounting and auditing play an integral role in the functioning of financial markets. This trend is unlikely to change in the blockchain and crypto-asset sectors.

Conclusions

Blockchain applications extend well beyond cryptocurrency and financial applications. This pragmatic and revolutionary technology affects various sectors by creating greater transparency and fairness while saving businesses time and money. It can also make life easier and safer. In the future, examples of real-world blockchain use cases are likely to grow and change how businesses operate.

Some material contained in this article comes from H. Kent Baker, Ehsan Nikbakht, and Sean Stein Smith, The Emerald Handbook on Blockchain for Business (Emerald Publishing, 2021)

About the Authors

Kent Baker, DBA, PhD, CFA, CMA, is a University Professor of Finance in the Kogod School of Business at American University. Professor Baker is an award-winning author/editor of 39 books.

Kent Baker, DBA, PhD, CFA, CMA, is a University Professor of Finance in the Kogod School of Business at American University. Professor Baker is an award-winning author/editor of 39 books.

Hugo Benedetti, PhD, is an Assistant Professor at ESE Business School, Universidad de los Andes (Chile). His research agenda focuses on the implications of blockchain technology adoption in the financial industry. His work appears in The Economist, Bloomberg, The Wall Street Journal, and Nasdaq.

Hugo Benedetti, PhD, is an Assistant Professor at ESE Business School, Universidad de los Andes (Chile). His research agenda focuses on the implications of blockchain technology adoption in the financial industry. His work appears in The Economist, Bloomberg, The Wall Street Journal, and Nasdaq.

Ehsan Nikbakht, DBA, CFA, FRM, is the C.V. Starr Distinguished Professor in Finance at the Zarb School of Business, Hofstra University. His current research is on blockchain applications in finance and investments.

Ehsan Nikbakht, DBA, CFA, FRM, is the C.V. Starr Distinguished Professor in Finance at the Zarb School of Business, Hofstra University. His current research is on blockchain applications in finance and investments.

Sean Stein Smith, DBA, CPA, CMA, CGMA, CFE, is an Assistant Professor at Lehman College, City University of New York. His award-winning research, focusing on blockchain, cryptoassets, and financial market implications, has been featured in Forbes, Bloomberg, and dozens of academic articles.

Sean Stein Smith, DBA, CPA, CMA, CGMA, CFE, is an Assistant Professor at Lehman College, City University of New York. His award-winning research, focusing on blockchain, cryptoassets, and financial market implications, has been featured in Forbes, Bloomberg, and dozens of academic articles.

Andrew C. Spieler, Ph.D., CFA, FRM, CAIA, is the Robert F. Dall Distinguished Professor in Business at the Zarb School of Business, Hofstra University. He has received numerous research and teaching awards and authored over 50 articles and book chapters.

Andrew C. Spieler, Ph.D., CFA, FRM, CAIA, is the Robert F. Dall Distinguished Professor in Business at the Zarb School of Business, Hofstra University. He has received numerous research and teaching awards and authored over 50 articles and book chapters.

How the World Press Freedom Index Was Politicized – Long Before the New Cold Wars

By Dr. Dan Steinbock

For years, the press freedom index by the Reporters Without Borders (RSF) has been widely quoted, even though its methodology is biased and RSF was long led by a white supremacist with a penchant for US-led regime change. Now RSF is targeting Asia.

According to the recently-issued new World Press Freedom Index (WPFI), the greatest media freedoms prevail in Western Europe and North America and the worst in emerging and developing economies.

Most media NGOs are led by veteran journalists, whereas the organization behind the Index was founded by Robert Ménard whose media experience was limited to a pirate radio station and an unpopular magazine that performed so poorly it had to be closed down.

It was then – in 1985 – that Ménard and three of his colleagues co-founded the Reporters sans Frontières (Reporters Without Borders, RSF).

RSF founder’s white supremacist ventures

As the RSF’s secretary general and its director-general, Ménard ruled the organization almost three decades (1985-2012), like the autocrats it presumably opposes. In the process, he managed to alienate all other co-founders.

The RSF’s stated aim is to “safeguard the right to freedom of information.” Yet, Ménard’s political ambitions overshadowed the organization’s mandate. In spring 2008, he and his colleagues tried to disrupt the lighting of the Olympic Flame before the Beijing Summer Olympics, presumably as a protest for Tibetan civil rights. These stunts coincided with campaigns by U.S. neoconservatives, CIA and the National Endowment for Democracy (NEDA), which have funded RSF activities.

Inspired by political extremism since a child, Ménard grew of age in a family with links to the far-right terrorist OAS; a French paramilitary group that contributed to Algeria’s massacres in the 1950s and terrorism in France, including assassination attempts against President De Gaulle and philosopher Jean-Paul Sartre.

Toward the end of his RSF reign, Ménard embraced far-right publicly. Since 2014, he has served as Mayor of Béziers in Southern France. A known Islamophobic, he has warned Muslim refugees they are not welcome in France. Like ex-President Trump’s far-right mobs, he touts the white genocide conspiracy that “Jews and globalists” seek to replace whites with Muslims from the Middle East.

More recently, the RSF has been led by Christophe Deloire, who is more cautious in rhetoric but shares Ménard’s geopolitics and touts the RSF’s new Information and Democracy Forum. Like his predecessor, Deloire has alienated the RSF organization, thanks to restructuring, departures and layoffs.

Regime change from Latin America and Middle East to Asia

From Ménard to Deloire, the RSF has cherished odd bedfellows. Amid the 2002 coup against Venezuela’s Hugo Chavez, the RSF sided with the plotters, as it did in the coups against Haitian President Jean-Bertrand Aristide, Manuel Zelaya in Honduras, and Evo Morales in Bolivia. According to critics, as Ménard and his colleagues have acknowledged, the RSF has cooperated and coordinated with US State Department against Cuba, Bolivia, Venezuela, and Nicaragua.

The regime-change activities were funded by USAID Cuba Program, “Freedom of Information” initiatives and the NEDA. In return, the Bush administration funded RSF and like-minded NGOs. In 2007, the thankful RSF justified the Iraq invasion, with Ménard arguing for the legality of torture. Similar joint interests mark RSF activities in the Middle East (Libya, Iran, Iraq).

Now RSF hopes to achieve the same in Asia. In 2017, it appointed Cédric Alviani the head of its first Asia bureau based in Taiwan, in convergence with the goals of the Trump administration and Taiwanese government. Alviani aligned RSF with Hong Kong’s turmoil, while offering interviews to the Epoch Times, which has touted RSF and Alviani for “warning people to beware of China’s disinformation about the Chinese Communist Party virus, commonly known as novel coronavirus.” The key supporter of ex-President Trump, the QAnon and conspiracy stories, the Epoch Times is a far-right Taiwanese media outlet whose cultist members believe that in the Judgment Day they will rise to Heaven and all Communists will go to Hell.

Like some of his RSF colleagues, Alviani is not a veteran journalist. The longtime Taiwan resident is an ex-head of the Taiwan European Film Festival funded by Taiwanese government and ministries, after stints in other Taiwanese-related and French foreign ministry posts.

Biased methods, funders’ agendas

Today, the RSF’s total budget is 6.1 million euros. It funds only 20% of its activities internally. Over 40% is based on “institutional grants” (French foreign ministry, French defense ministry), whereas 35% stems from “private foundations and NGOs” (e.g., NEDA, Ford Foundation) and “corporate and individual donations” (e.g., American Express, French bank Société Générale).

Through their funding, billionaires, including George Soros via his Open Society and Pierre Omidyar, have indirectly shaped RSF activities. In return for French and US funds, the RSF has been largely silent about media abuses in France and the West.

Behind the official facades, the RSF’s Index (WPFI) has attracted much controversy. As it should: it is something of a racket.

Officially, the WPFI “is determined by pooling the responses of experts to a questionnaire devised by RSF.” The questionnaire presumably evaluates very broad criteria, such as “pluralism, media independence, and self-censorship.” The qualitative analysis is augmented with quantitative data on abuses and acts of violence against journalists. Yet, questions about media ownership and concentration are effectively ignored.

Moreover, when a limited sample of some 150 journalists and 18 NGOs are asked to analyze and respond to 87 questions for each country, the probability of biases and thus disconnect with realities increases accordingly.

Furthermore, many of the respondents and NGOs are funded by the RSF, while researchers, jurists and human rights activists, which are said to be selected by the correspondents. Such pre-selections tend to reinforce the agendas and priorities of RSF’s sponsors – foundations and NGOs – since it lacks adequate internal funding.

A simple example: Even as the Philippine 2021 WFPI ranking fell, the UNESCO World Press Freedom Prize was awarded to CEO Maria Ressa of Rappler, a key player in the recent South China Sea media debacles. Previously, Ressa had served as the prize jury’s member and its president. Like RSF, Ressa and her Rappler have been funded by billionaire Pierre Omidyear. Ressa has a dual US-Filipino citizenship and upscale properties in both countries, although Rappler is no cash cow and remains in a legal quagmire.

Media predators only in developing economies

The RSF publishes a gallery of “Predators of Press Freedom,” presumably highlighting the most international violators of press freedom, based on its Index. The slick image of “predators” reflects the RSF’s reliance on campaign ads by Saatchi & Saatchi that once orchestrated the campaign that brought Margaret Thatcher to power in the UK.

Most RSF Predators are countries that the US has broadly criticized, sanctioned, or targeted in new cold and hot wars, and regime change efforts, including China, Venezuela, North Korea, Iran, Turkey, Russia, Syria, Yemen, Pakistan, and so on.

Some 15 years ago, Singapore’s then-PM Goh Chok Tong denounced the Index as “a subjective measure computed through the prism of Western liberals.” Not much has changed since then. The RSF gallery does not feature a single Western country, despite known media abuses in the high-income Western countries. Indeed, the French daily Libération, which has funded the RSF, has criticized it for keeping mum about the abuses of the Western media: “Many blame the group for its ferocity against Cuba and Venezuela, and indulgence toward the United States.”

Here’s the problem: Some RSF targets do have a questionable media record. But as the RSF and its sponsors politicize and weaponize its mandate, methodology, targets and objectives, an objective scrutiny of media freedoms is undermined.

What is needed is a global media watchdog that comprises both rich and poor major economies and methods that cannot be easily weaponized for ulterior agendas.

An organization that represents reporters with borders is not a solution. It is part of the problem.

About the Author

Dr. Dan Steinbock is an internationally recognized strategist of the multipolar world and the founder of Difference Group. He has served at the India, China and America Institute (USA), Shanghai Institutes for International Studies (China) and the EU Center (Singapore). For more, see https://www.differencegroup.net