By Dr Kalim Siddiqui

Financialised capitalism emerged in the advanced economies during the last four decades. It has opened wider avenues to wealth formation and speculation, as well as caused the recent financial crises and the rising levels of income inequality. In this article, the author discusses the impact of financialisation and neoliberalism on the current state of the global economy.

Financialisation means a relative shift of the economy from one of being production-based to financial-based. In other words, financialisation can be characterised as shift in the centre of gravity of the economy from production to finance. This is resulting in a huge change in economics, trade and society in the advanced economies. Despite the fact that in the past the financial services have played an important role in capital accumulation, something has fundamentally changed in capitalism in the last few decades. Financialisation of the economy stands out as one of the largest and most significant changes in the structure of the advanced economies.

We characterise financialisation as the emergence of a regime of accumulation where the ascendency of the shareholders’ value orientation is important. This seems to act as a drag on the economy and influences government policy in a manner that disfavours workers. Increasing profit in the financial sector has an impact on the labour share of the national income and the distribution of income and profits across sectors; that is, it seems that financialisation of the economy has increased inequality. These changes have been reflected in various aspects of the economy, such as the rising share of the financial sector (FIRE, i.e., finance insurance and real estates) in the economy; increasing the proportion of financial profits in the total profit and increasing debt related to GDP.1 In 1960, manufacturing accounted for 27% of the U.S. GDP while finance accounted only 13%. Since then, the situation has changed dramatically. For example, since 1980, General Electric has made more money through financial services rather than the production of goods. Increased financialisation has led to a decrease in the share of working people’s wages, and globalisation is putting U.S. workers in the same position as the super-exploitative conditions imposed on workers in the developing countries. Capital can move globally, but workers cannot. Such policies are designed to make workers insecure and as a result accept low wages. Financialisation and off-shoring of capital has led to the concentration of wealth amongst the handful of elites and big corporations in recent decades.2

Financialisation has opened wider avenues to speculation and wealth formation with little concern about capital investment in new productive capacity in the manufacturing sector.

Financialisation has opened wider avenues to speculation and wealth formation with little concern about capital investment in new productive capacity in the manufacturing sector, as apparent during the long prosperity of 1950-1973, i.e., the post-war economic boom. This period saw the building of the trade union, public provision of education, health and the development of redistributive progressive tax systems and the creation of the welfare state in the advanced economies. However, the Keynesian demand management, full employment and collective bargaining interfered with the working of market. The banks were regulated, and, during that period, there was no financial crash.3

The Rise of the Financial Sector

Since the 1980s, there have been consorted efforts by the Western governments to increase the importance of financial sector, such as banks and investment companies. The growing influence of finance was noted as a matter of concern by James Tobin, who proposed a financial transaction tax to curb currency speculation. However, in 1999, U.S. President Clinton abolished the Glass Stegall Act, which negated the need for the separation of investment and commercial banking that had previously been in place for more than five decades. The removal of restrictions on banks seems to have contributed to the rise of a financial system where the lines between regulated banks and the so-called shadow banking system have become blurred. The existence of shadow banking, which is directly or indirectly guaranteed by banks, has made it practically impossible to confine the safety to the regulated banking system. This led to an orgy of speculation that, ultimately, resulted in the 2008 financial crisis, the biggest economic crisis since the Great Depression of the 1930s.4

The economic changes in the advanced economies are generally characterised as the coordination of three policies, namely globalisation, neoliberalism and financialisation. Financialisation, as already discussed, means a shift in the centre of gravity of economic activity from production to finance. As Foster(2007) has characterised this development as: “financialisation has resulted in a new hybrid phase of monopoly stage of capitalism that might be termed ‘monopoly-finance capital’. Rather than advancing in a fundamental way, capital is trapped in a seemingly endless cycle of stagnation and financial explosion”. Globalisation, which is also a very important element of contemporary capitalism, means not only expanding into new markets and exploiting workers on the periphery, but also means exploiting the natural resources in those same countries. The rise of financial capital has encouraged speculative asset creation and contributed to huge inequality where, as now for example, forty-two billionaires currently hold as much wealth as half of the world’s population.5

During the financial crisis of 2008, the big banks and corporations were bailed out in the name of being “too big to fail”, while workers’ wages saw a fall in real terms. Under the new era of increased financialisation, accumulation has been progressively removed from the realities of production. Financialisation represents a tendency towards the expansion of the size and importance of the financial sector in relation to the overall economy. As Toporowski (2000:1) argues that “have seen the emergence of an era of finance that is the greatest since the 1890s and 1900s and, in terms of the values turned over in securities markets, the greatest era of finance in history. By ‘era of finance’ is meant a period of history in which finance…takes over from the industrial entrepreneur the leading role in the capitalist development.” 6

In fact, the stagnation in the economy in the 1980s also meant that capitalists increasingly relied on the growth of finance to enlarge their money capital.7 There is an increasing role of finance in the operation of capitalism and a tendency in recent decades towards the increased financialisation of the capital accumulation process. Capitalism is becoming inefficient by increasingly devoting its surplus capital to speculation and casino-like pursuits rather than long-term investment in the real production economy. Despite the fact that neo-classical economists assumption that productive investment and financial investment are tied together, and also that savers purchases financial claim to real assets from the entrepreneurs who then will use the money, thus will acquire to expand production, such an assumption is incorrect.

Neoliberalist capitalism first began to be acceptable in the U.K. in 1979 with the Thatcher era and in the U.S. with the Reagan era in 1980. Neoliberalism is associated with certain specific polices such as deregulation of business and finance, privatisation of public industries and public services, reductions in taxation on corporations and the rich, and the abandonment of wage-productivity policies to favour wage increases. Financial deregulation of financial institutions and banks allowed them to indulge in activities aimed at achieving the highest returns, while growing competition put pressure on companies to seek more profitable activities. The pursuit of increased profits gave rise to speculative activities through such innovative and exotic instruments as subprime mortgages, securitisation, collateralised debt obligations and credit default swaps.1

The financial crisis in 2008 began with mortgage-related securities which had spread in the U.S. and EU and global finance experienced collapse in value. In the U.S., the investment banks Bear and Sterns collapsed, government took over Fannie Mae and Freddie Mac. Fed came to recuse AIG. The financial crisis accelerated sharply in the U.S. and engulfed the entire economy not just in EU, but most of the advanced economies (Siddiqui, 2008a). On the 2008 financial crisis, Crotty (2009:575) explains, “The past quarter a century of deregulation and the globalisation of financial markets, combined with the rapid pace of financial innovation and moral hazard caused by frequent government bailouts helped to create conditions that led to this devastating financial crisis. The severity of the global financial crisis and the global economic recessions that accompanied it to demonstrate the utter bankruptcy of the deregulated global neo-liberal financial system and market fundamentalism it reflects… Several decades of deregulation and innovation grossly inflated the size of the financial markets relative to the real economy. The value of all financial assets in the U.S. grew from four times GDP in 1980 to ten times GDP in 2007.”8

The current global political economy is mired in economic stagnation, financialisation, growing inequality, unemployment and ecological disasters. The failure of capitalism can be seen everywhere, with the stagnation in long-term investment through the expansion of the financial sector that came to head with the 2008 financial and economic crisis. Over the last four decades, the real wages in the advanced economies have barely improved, while work intensity and job insecurity has increased. The so-called market, as a self-regulating institution within society, has not worked but the fact is that it has always required constant intervention by the state, as Karl Polanyi (1944) demonstrated. In his book The Great Transformation, he presented a compelling and alternative understanding of the economic and financial crises affecting the economy. He argued that economic activity is embedded within a social and economic context. The market society is not a naturally occurring phenomenon, but is rather a political and social construct.9

Capitalism was known to be a system based on competitive class based on production and exchange geared to accumulation through exploitation of workers to generate profit. However, the greater part of the social and environmental costs of production outside the market were excluded in such calculations, and merely treated as negative externalities.10 Any critique of financial capital which dominates globally must begin with our understanding of capitalism today, and a consideration of the reasons why other alternatives to financialisation seems to be outside the purview of capitalist solutions.

In fact, historically, the development of capitalism can be characterised into distinct patterns and sources of profit. For example, mercantile capitalism in the 17th and 18th centuries was marked by buying and selling goods, and profits were earned by trading companies. Merchants could earn profits by simply taking advantage of price disparities in distance markets. Industrial capitalism in the 19th and 20th centuries was marked by investment in industries and the production of goods, and profits were earned by employing wage labour and through investments in production. Karl Marx identified an additional flow of value added to output per period as capitalist profit, achieved through the exploitation of labour in the production. Classical economists have largely sought to separate the role of finance from the real economy. It was said that accumulation takes place from real capital formation, which increases economic output. They opposed any appreciation of financial assets which increase wealth but not output. Marx (1981:607) argued “In the way that even an accumulation of debts can appear as an accumulation of capital, we see the distortion involved in the credit system reach its culmination.”11

Keynesian View

Neo-classical theory assumes markets “as being neutral”, while Keynes saw money as one of the operative aspects of the economy. He argued (1973:408) “booms and depressions are phenomena peculiar to an economy in which…money is not neutral.” 12 Keynes advocated in favour of restrictions on speculative capital as a tool to control capital flows.13 The advanced economies led by the U.S. and, indeed, the international financial institutions are in favour of removal of capital control in the developing countries.14 They strongly advocate in favour of free capital mobility among the developing countries, in contrast to the policy they themselves adopted when they were building their own economies, soon after the post-war period, when they supported capital regulation. However, after the end of Cold War, the West emerged as a global hegemon. This occurred due to uneven power relations, especially between the developing and advanced economies.

After World War II, economic policy was drawn on the basis of the Keynesian growth model, which targeted full employment and wage increase. The wage increase was tied to productivity growth, and the higher productivity meant higher wages. This ultimately led to an increase in aggregate demand as a result of a rise in employment. However, the active use of fiscal policy can result in inflation, which depreciates accumulated wealth held in monetary form, where the depreciation of such assets is seen as a threat by the capitalists and considered more important than unemployment and economic stagnation. They then turned towards austerity and monetarism to control such situations and used neoliberal policies in defence of corporate capital and wealth.15 As a result, the capital within these groups has not only increased, but by virtue of financialisation, globalisation and the new technological revolution, they are able to amass wealth globally on an unprecedented scale.

With the sharp rise in prices in advanced economies in the 1970s and 1980s, these economies abandoned Keynesian policies and replaced them with neoliberal ones. Neoliberalism, as a government policy, received considerable support with the election of Margret Thatcher in the U.K. in 1979 and the also with that of Ronald Reagan in the U.S. in 1980. The deflationary policies adopted in the U.K. and U.S. in the 1980s resulted in lower inflation, but at the cost of higher unemployment. Thus, controlling inflation became government’s top priority rather than its previous policy of achieving full employment. The link between increases in wage and productivity growth was abandoned.

It seems that financialisation, while boosting capital accumulation through the process of speculative expansion, has also contributed to the decline of the current socio-economic system. Under neoliberalism, wealth is being extracted from the people through financial capital. As Toporowski emphasises, “The apparent paradox of capitalism at the beginning of the 21st Century is that financial innovation and growth are associated with “speculative industrial expansion”, while adding systematically to economic stagnation and decline” (cited in Lapavitsas & Mendieta-Muñoz. 2016:9).4

Financialisation has also had important effects along the international dimension. The liberalisation of international capital flows has led to increased volatility in exchange rates, often culminating in severe exchange rate crises.

Financialisation has also had important effects along the international dimension. The liberalisation of international capital flows has led to increased volatility in exchange rates, often culminating in severe exchange rate crises. Capital liberalisation places serious limitations on governments’ ability to regulate their economies in crucial areas such as capital flows, public debts and rates of interests. The argument in favour of financial globalisation is based on standard neo-classical economics. Proponents argue that financial globalisation would allow capital to be allocated such as to ensure its most efficient use and that it would benefit developing countries. This would mean that it would be expected that capital would flow from advanced economies to developing countries, and that there be a positive correlation between indicators of financial globalisation and growth. However, the experience of last decades is quite different, and financial globalisation and liberalisation have led to frequent exchange rate crises driven by volatile capital flows. Further, due to this the exchange rate movements are increasingly determined by capital flows rather than current account positions.

In recent decades, the banks and large industrial corporations have not come closer, but large corporations are independently engaging in financial transactions. It seems that financial institutions have sought new sources of profitability in financial expropriation and investment banking, while workers, on the other hand, have been increasingly pushed towards relying on private finance to meet their basic needs including consumption, housing, health, education and provision in old age.

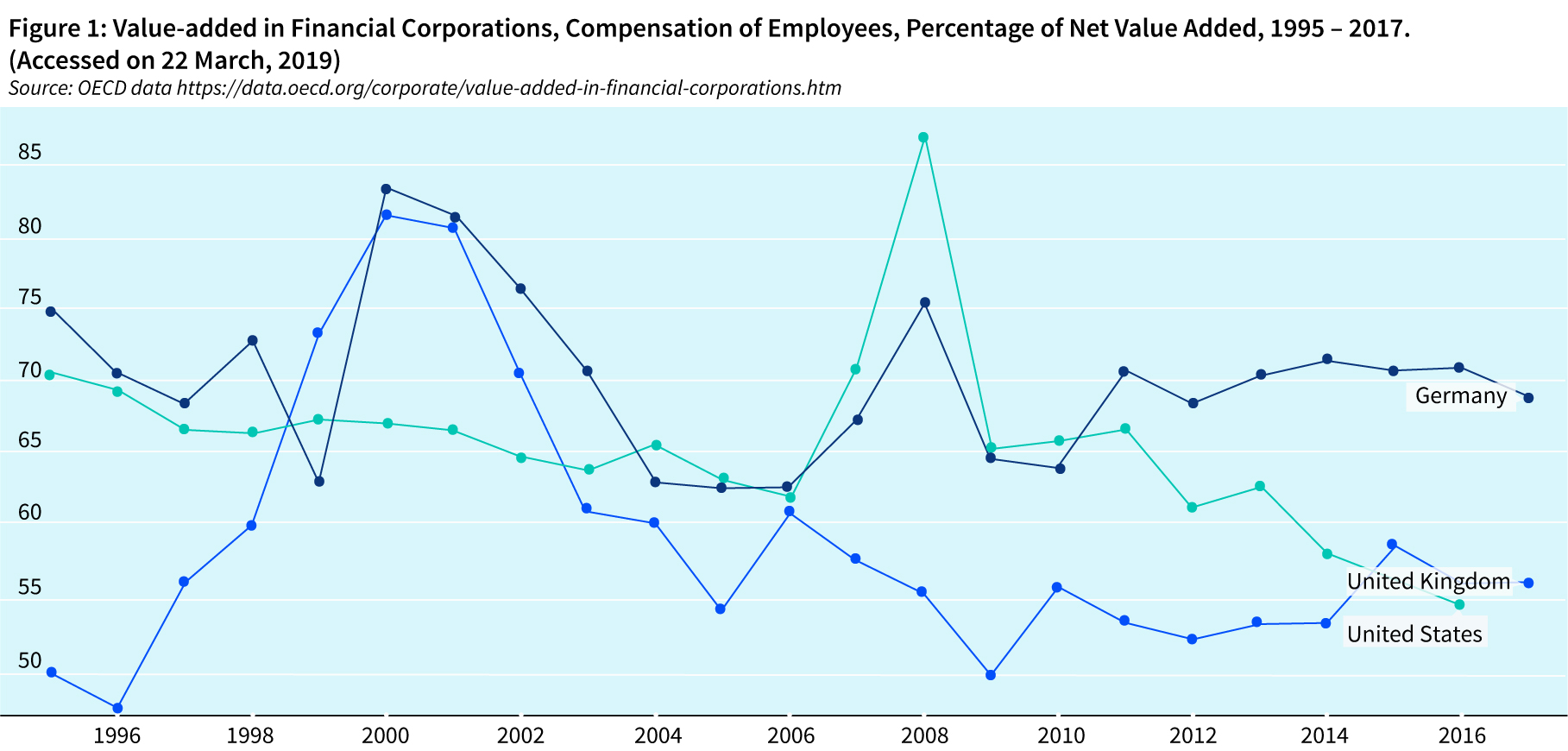

For the last three decades, there has been a shift from industrial to financial capital. Financial capitalism can be described as a form of capitalism in which finance has become the dominant function in the economy, and has extended its influence to other areas of life, e.g., social, economic and political. The explosive growth of the financial market began during the period of stagnation of industrial production. Financialisation is defined as a pattern of accumulation in which profits accrue primarily through financial channels rather than commodity production. Since the 1980s, the majority of U.S. and European corporations have increasingly derived profit from financial activities. The value added in financial corporations has risen in the major advanced countries since 1994, as shown in Figure 1. As a result, the financial sector increased its share of GDP but profits from interest, dividends and capital gains for non-financial corporations have been greater than those from productive investment. It seems that during this period, capitalists and the big corporations responded to increased international competitions by shifting their investments from production to the financial sector, and that financialisation has led to a slowdown of accumulation and also reduced investment in tangible assets.

On the issue of slowdown of accumulation, Van der Zwan (2014:104) notes “the internationalization of global market has been a major impetus for firms to withdraw from productive activities. Faced with increased international competition and domestic demands for shareholder return, American manufacturers have off-shored production and controlled supply chain to cut back on costs.” 19

Financialisation, Economic Performance and Income Distribution

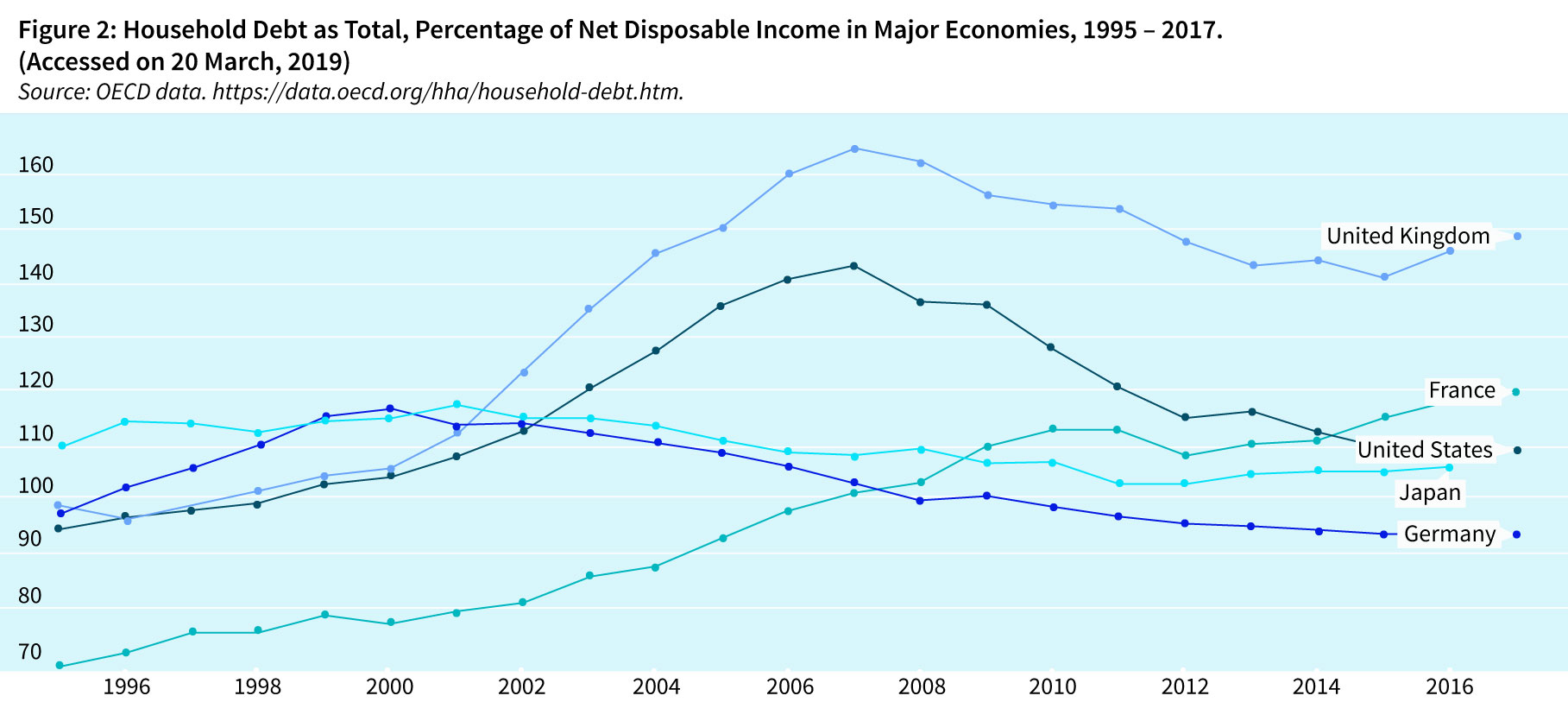

The impact of financialisation on economic performance and income distribution has been negative. The finance-dominated accumulation regime has been characterised by a sluggish economic performance with increasing financial instability due to rising debt levels (Siddiqui, 2019a). The shortfall of disposable income has been compensated by credit and increasing debt levels. The property boom allowed households to take out loans that they could not afford given their income, but this seemed reasonable to banks who assumed that property prices would continue to increase. The result was a credit-financed consumption boom that came with current account deficits. Capital inflows again fuelled the property bubble. Household debts, as total of net disposal income, increased steadily from the mid-1990s and reached their peak in 2006; after the financial crisis, they fell all major economies, where in the U.S. they fell more sharply.

Households have become used to relying on credit. This has involved changes in attitudes as well as changes in financial institutions and instruments, among which the widespread use of credit cards is the most obvious. Household debt levels have increased sharply since the mid-1990s in the advanced economies (see Figure 2). In contrast, the incomes of finance owners and financial companies increased substantially throughout the 1980s and 1990s. It seems that the victory of the rentiers has come at the expense of the workers, who have experienced stagnation in real wages and increased indebtedness.

The financialisation within society has been facilitated by crucial developments in technology and institutions since the 1980s. In fact, the advancements in information technology and telecommunications spurred the investment in banking, encouraging people to become investors. During this same period, there have been profound institutional and political changes, especially in the U.K. and U.S., the most obvious of which was the deregulation of the financial system and labour markets, when neoliberalism replaced the Keynesianism of the long post-war period of prosperity and the construction of the welfare state. Also, at the same time, the development of new financial products has increased in a number of areas of personal life. This is supported by intermediaries that connect individual households to the global financial markets, such as pension funds and banks, and also the development of products such as derivatives and asset-backed securities. The financialisation of the everyday has been facilitated by risk-taking and self-fulfilment, as government policy initiative was to move away from the economic security provided by the post-war boom and welfare measures. Under neoliberalism, the common people are encouraged to deal with uncertainties themselves. These risks are not only due to withdrawal of welfare measures and high unemployment, but also the uncertainty created by the vitality of the financial markets. Under such circumstances, people are encouraged to take risks, and only through taking greater risks can they achieve higher investment returns to protect against uncertainties such possible unemployment, sickness and retirement.

Financialisation has certain distinctive features such as non-financial companies becoming financialised and increasingly drawing profits from financial operations undertaken on their own accounts.

Financialisation is largely ignored by mainstream economists. Financialisation has certain distinctive features such as non-financial companies becoming financialised and increasingly drawing profits from financial operations undertaken on their own accounts; banks have shifted their sources of profit away from investment in production (the real economy) to transactions in financial markets, including lending to households.

Over the last four decades, global production and trade have been dominated by multinational corporations (Siddiqui, 2017c), which were created through successive waves of mergers and acquisitions. Despite all measures to woo foreign investment by the developing countries16 the bulk of FDI (foreign direct investment) takes place among the advanced economies. However, in recent decades there has been a substantial increase in FDI into developing countries, mostly in China, East Asia and India. Competition has intensified globally and the rise of multinational corporations has been accompanied by a shift of manufacturing away from advanced economies to places such as China.17

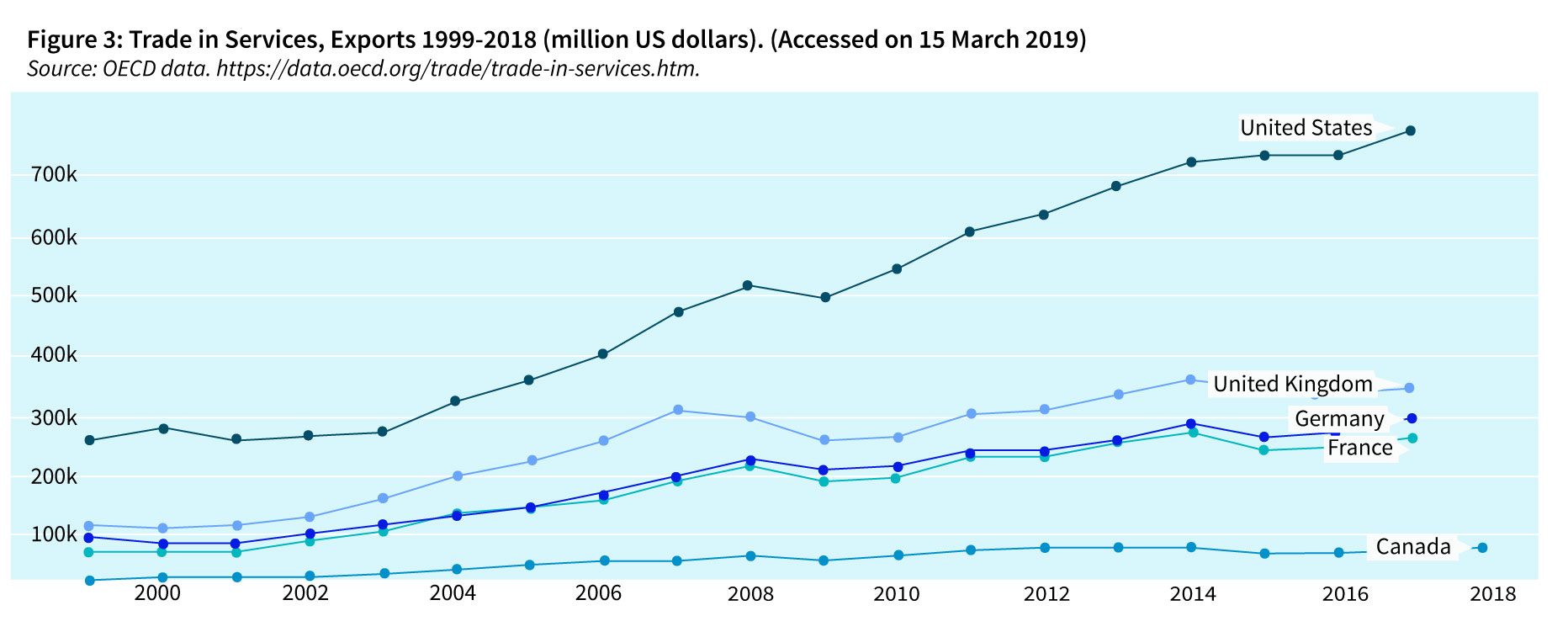

Trade in service exports has risen sharply in recent decades in all major economies. The trade in services in advanced economies has increased in recent decades (as shown in Figure 3) and in the U.S. in particular services have played an increasingly important role in the balance of payments.

The logic of U.S. capitalism seems to be driven by a wealth maximising rentier class and imperial-like ambitions to control, whether directly or indirectly, other countries under the direction of the U.S.. The policy undertaken to support financialisation includes de-regulation of foreign inflows of capital and rates of interest. The slowdown of accumulation in the U.S. economy during the economic crisis in the 1970s, such as the slow growth in the productivity related to U.S. industry compared to other advanced economies such as Japan and Germany.18 Despite certain policy measures adopted during the Carter administration, businesses began to see higher profits in finances rather than in the real economy, and hence began the process of the deindustrialisation of the U.S. economy.

The rise of profits relative to wages further increased the concentration of income and wealth into rich households, who were faced with huge increases in surplus funds that exceeded the available productive investment opportunities. These funds were diverted to the purchase of real estate or securities. The growth of profits at a faster rate than wages may be good for creation of surplus value, but it creates a realisation problem and inadequate growth of aggregate demand. Since workers consume the bulk of any goods, then a decline in wages does not help, which coincided with austerity measures and drastic reductions in welfare spending.

Financialised capitalism emerged in the advanced economies during the last four decades, which was marked by the increased domination of finances and profit, as earned in the sphere of circulation and finance. This period also witnessed a tremendous growth of financial profit through financial expropriation, i.e., the systematic extraction of profits from income flow and stock of money wealth. Figure 4 shows that financial profit as a percentage of corporate profits in the U.S. has risen sharply since 1985. For instance, financial profits, as percentage of corporate profits, were a little over 10%, which was the same level as in 1955. However, by 1994 this had reached 30%, and just before the crisis in 2006 had further risen to 37%. However, during the 2008 crisis, it sharply declined to 7% but has since risen again to 25% as of December 2015.

Moreover, there were also changes in the economic structure of the advanced economies along with the sharp rise in unemployment. The service sector expanded, while the manufacturing sector, both in terms of contribution to GDP and employment, declined. All these changes in the economy also weakened the position of employees. Furthermore, in the 1990s, globalisation and deregulation of capital put workers in the West in international competition with the rest of the world. With increased capital mobility, multinational companies could move somewhere else if pressurized with higher wage demands. Neoliberalism also included labour flexibility policy, which coincided with the policy of austerity. All these measures reduced the bargaining power of the workers and created particular hardship for the working people. For example, between 1981 and 2010, the workers wage share declined 7.0 points of the GDP in the EU 15 member countries: specifically, 9.4 points in France; 7.5 point in Germany; 10.2 points in Italy; and 11.9 points in Spain. Surprisingly, it declined much less in U.K. (2.2 points) and, in the U.S., 6.3 points for the same period. Unemployment rose sharply. For example, in 2010, the unemployment in the EU 15 countries was 9.6%, but in particular for Spain, 20.1%, for Germany, 7.1%, the U.K., 7.8%, and the U.S., 9.6%.

We are witnessing a crisis of financialisation and neoliberalism and its ability to promote the expansion of output through consumer debt has effectively reached a dead end. Financial capital, once removed from its original role of assisting production to meet human needs, under neoliberalism has been taken over by speculative capital and has grown enormously in recent decades. Capital accumulation has always been the driving force of the capitalist system, and it was said that this adds to wealth and income in countries where it takes place. However, there were also otherwise periodic crises and breakdowns, and in particular the benefit of this growth has not been equally distributed to the various sections of society.

Financialisation also has had profound effects on income distribution such as there has been rise of ‘rentiers’ income’, i.e., interest and dividend income as well as capital gains. The rise of income in the financial sector has widened income disparity, and financialisation seems to have shifted the power balance between capital and labour. Since the 1980s, wage shares have fallen by nearly 10 percentage points in the EU and a bit more in Japan; however, surprisingly in the U.S. and U.K., this fall was less than about 5 percentage points. Under neoliberalism, trade unionist and collective bargaining was not assigned appropriate importance and labour markets were made more flexible by permitting companies to hire workers on zero-hour contracts, and also allowing them to be fired more easily. All these policy measures benefitted corporations and they secured a bigger share of the gains of growth. Also, with the constant threat of globalisation, corporations could hold down wages. The current period represents a gigantic concentration of wealth, rising income inequality, and uncertainty for the common people and which are the exploitative aspects of financialised capitalism.

In conclusion, the financialisation and neoliberalism is associated with rising levels of income inequality in the advanced economies. For instance, in the mid-1970s, the top 1% of households in the U.S. accounted for 9% of the income generated in the country, but by 2010 this share had risen to nearly 25%. Rising inequality seems to be a root cause of the present crisis in the advanced economies, because rising inequality creates a downwards pressure on aggregate demand (in the Keynesian model) since workers and poor income groups have high marginal propensities to consume. Also, financial deregulation has allowed countries to run larger current account deficits, such as the U.S. is facing at present. In fact, it appears that financialisation offered a solution to the U.S. crisis of hegemony due to increased international competition confronting U.S. companies and the loss international prestige after the disaster of the Vietnam War. Capital deregulation started at the end of Cold War, and further the IMF and World Bank imposed ‘Structural Adjustment Programmes’ in developing countries; both these policy measures kept them firmly under Western control.

To achieve stable growth, governments should enact policy in favour of income and wealth distribution, financial regulation and increased aggregate demand. A fairer, equitable distribution of income and wealth would be essential in order to achieve stable growth, for which wage growth is crucial in order to increase consumption and reduce household debt and to create a more balanced economy. Progressive tax reforms should be used to raise taxes on rich individuals and big corporations in order to fund welfare measures for the less well-off. Governing capital flows between countries is important in order to stabilise the economy. This could be achieved through an appropriate international directive.

Dr Kalim Siddiqui is an economist, specialising in International Political Economy, Development Economics, International Trade, and International Economics. His work, which combines elements of international political economy and development economics, economic policy, economic history and international trade, often challenges prevailing orthodoxy about which policies promote overall development in less developed countries. Kalim teaches international economics at the Department of Accounting, Finance and Economics, University of Huddersfield, U.K.. He has taught economics since 1989 at various universities in Norway and U.K..

Dr Kalim Siddiqui is an economist, specialising in International Political Economy, Development Economics, International Trade, and International Economics. His work, which combines elements of international political economy and development economics, economic policy, economic history and international trade, often challenges prevailing orthodoxy about which policies promote overall development in less developed countries. Kalim teaches international economics at the Department of Accounting, Finance and Economics, University of Huddersfield, U.K.. He has taught economics since 1989 at various universities in Norway and U.K..

References:

1. Siddiqui, K. 2019a. “Government Debts and Fiscal Deficits in the UK: A Critical Review”, 10(1) World Review of Political Economy, Pluto Journals, forthcoming.

2. Siddiqui, K. 2017a. “Financialization and Economic Policy: The Issues of Capital Control in the Developing Countries”, World Review of Political Economy 8 (4): 564-589, winter, Pluto Journals.

3. Siddiqui, K. and P. Armstrong. 2017b. “Capital Control Reconsidered: Financialization and Economic Policy”, International Review of Applied Economics, 32(6): 1-19, March.

4. Lapavitsas, C. and I. Mendieta-Muñoz. 2016. “The Profits of Financialization”, Monthly Review, July, New York.

5. Foster, J.B. 2007. “The Financialization of Capitalism”, Monthly Review, April, New York. https://monthlyreview.org/2007/04/01/the-financialization-of-capitalism/.

6. Toporowski, J. 2000. The End of Finance, London: Routledge.

7. Siddiqui, K. 2019b. “The Political Economy of Essence of Money and Recent Development”, International Critical Thought, 9(1): 1–24.

8. Crotty, J. 2009. “Structural Causes of the Global Financial Crisis: a Critical Assessment of the ‘New Financial Architecture’”, Cambridge Journal of Economics, 33: 563-580.

9. Siddiqui, K. 2008a. “Recent Global Financial Crisis”, Klassekampen, (in Norwegian) 20 October, Oslo, Norway.

10. Siddiqui, K. 2008b. “Free-Market Illusion and Global Financial Crisis”, Mainstream, vol.49, 25 November, New Delhi.

11. Marx, K. 1981. Capital vol. 3, London Penguin.

12. Keynes, J. M. 1973. “A Monetary Theory of Production”, in Keynes Collected Writing, vol. 1, London: Macmillan.

13. Siddiqui, K. 2019c. “Corruption and Economic Mismanagement in Developing Countries”, The World Financial Review, January-February.

14. Siddiqui, K. 2018 “Imperialism and Global Inequality: A Critical Analysis”, Journal of Economics and Political Economy, 5(2): 266-291.

15. Siddiqui, K. 2017c. “Globalisation, Trade Liberalisation and the Issues of Economic Diversification in the Developing Countries”, Journal of Business & Economic Policy, 4(4):30-43.

16. Siddiqui, K. 2016. “Will the Growth of the BRICs Cause a Shift in the Global Balance of Economic Power in the 21st Century?” International Journal of Political Economy, 45(4): 315-338, Routledge Taylor & Francis.

17. Siddiqui, K. 2015a. “Foreign Capital Investment into Developing Countries: Some Economic Policy Issues”, Research in World Economy, 6(2):14-29.

18. Siddiqui, K. 2015b. “Political Economy of Japan’s Decades Long Economic Stagnation”, Equilibrium Quarterly Journal of Economics and Economic Policy, 10(4): 9-39.

19. Van der Zwan. 2014. “The State of the Art: Making Sense of Financialization”, Socio-economic Review, 12: 99-129.

")

")

")

{kind=link}

Trump and the Taiwan Gambit

By Peter Koenig

Taiwan has become a new “eastern pivot” for Donald Trump. Against all international laws and UN charters, he is approaching Taiwan, as indicating to the world that regardless of the established world rules which make Beijing, the Peoples Republic of China (PRC), the official and legitimate Authority of China, with Taiwan being a part of China – the self-styled emperor, Mr. Trump, pretends he prefers dealing with Taiwan as an independent country. By doing so, he intends to invite others to do likewise. Trump wants to make Taiwan an ‘ally’ – dreaming of setting up a US base on the island, thus further encircling China. It is the old game, divide to reign. But he can’t be as ignorant as to believe it will actually work. It’s just one more thing to annoy PRC. Frankly – seen from a step back, it looks more like attempting to dump one of those primitive Trumpish ‘diplomatic’ bombshells on PRC’s back. – Provoking the Dragon?

Dragons can be lethal, especially if exposed to nonstop strings of insults and debasement, attacks, and threats, sanctioned with trade wars, subjecting US$ 200 billion worth of Chinese exports into the US with 25% import tax, and, mind you, Trump just issued a new threat –raising the ante to US$ 300 billion, in case China refuses to attend the G20 summit in Osaka, Japan on 28-20 June 2019. Can you imagine – the insolence, ordering President Xi to attend the G20 summit?!? The man has indeed no manners, diplomatic or otherwise.

Trump further bragged on Monday, 10 June, that China will make a deal with the United States “because they’re going to have to.” – And what would be the deal? He never explained. He added that “China has lost trillions of dollars since he, Trump, was elected president”.– Imagine this impunity in recklessness! – Well – surely, President Xi Jinping will not be duped or blackmailed by joker Trump.

On another front, Trump threatened Mexican’s new President Andrés Manuel López Obrador, AMLO for short, with a 5% tariff on Mexican agricultural exports to the United States, if illegal immigration to the US would not stop. AMLO approached President Trump with an open letter, saying that he seeks peace and not confrontation, dialogue not war, and that AMLO’s government will do whatever is in its power to stop illegal migration to the US.

He stated, correctly, that a trade war would do more harm than good to both nations. Trump then dropped the threat, with worldwide publicity, to make sure his ‘goodness’ is recognized the world over. However, just a few days ago, Trump threatened Mexico again with the 5% tax, in case AMLO’s promise doesn’t hold and poor Mexicans keep illegally crossing the border into the great Promised Land (no, not Israel, but the western extension of Israel).

Of course, this tariff has nothing to do with trade. It is punishment, a sheer demonstration of supremacy. And – never mind, Trump probably doesn’t understand that California’s agriculture thrives on the low-wage illegal Mexican and Central American immigrants.

It is nevertheless amazing that the (western) world stands by and dares say NOTHING. The threats of sanctions seem to be effective. Anybody, or any nation that refuses to go along with Washington’s thuggish criminal behavior may be subject to punishment, be it by trade and / or financial sanctions, or outright military intervention. There is no international law, no rules of the community of nations, no political common sense that is respected by Trump and his handlers, and the world is afraid. Even though so far most of the threats have amounted to nothing more than ridiculous blabber and saber rattling.

More threats were thrown at Iran, with more sanctions and economic strangulations if Iran doesn’t “behave” – actually there are hardly any explanations given what “good vs. bad behavior” would mean for the US, other than Washington’s repeated empty accusations of Iran being a nuclear threat, disregarding the Joint Comprehensive Plan of Action (JCPOA), or nuclear deal signed in 2015, freeing Iran of any further accusation of wanting to become a nuclear power (which, by the way was a farce in the first place – the subject for another essay).

This so-called nuclear deal was signed by the 5 UN Security Council members, including the US. But as we know, under pressure from Netanyahu, Trump reneged last year from the deal – and since then horrendous sanctions of economic strangulations and foreign asset confiscations – outright theft, in clear text – were imposed by the US on Iran, with ongoing pressure on the EU to do likewise. According to Trump – and his two minion mouth-pieces, Pompeo and Bolton – more are to come.

To that, Iran’s Foreign Minister, Mohammad Javad Zarif, stated that Iran will not be blackmailed and added the philosophical observation that Trumps economic wars around the globe will eventually backfire. Well, yes. Trump’s reckless playing with tariffs, sanctions and other punishments around the globe will eventually drive everybody away from dealing and trading with the US, including away from the western monetary system. It’s the silver lining of the dark-dark US cloud. Its economics 101.

Propelled by German business interests (but at the same time limited by Washington [and Brussels] on what he is allowed to say), German Foreign Minister, Heiko Maas, visited Iran a few days ago to seek a compromise for Germany and other EU members to still hold on to the Nuclear Deal, because Germany’s economy wants to deal with Iran, yet, seeking concessions from Iran that may assuage Washington. But Iran’s Foreign Minister, Zarif, didn’t fall for it. The meeting ended in nothing. Good so, because there is nothing, absolutely nothing, that any ally (except Israel) could do to change the Bully’s mind on Iran.

Frankly, does Trump seriously believe he possesses all that power over other world leaders? Or is he, Trump, just a convenient lackey of a force much stronger behind him, a force that controls both the Pentagon and, more importantly, the western financial and banking system – the Zionist designed western dollar-based monetary system. This Ponzi scheme has been able for the last 100 years or so – and as we witness, every day more – to usurp the world, holding it hostage, with artificially created economic booms and busts, with economic sanctions, strangulations, confiscation, with the theft of nations’ foreign assets and even their reserve funds, if they don’t bend to the will of the self-proclaimed super power USA.

Yes, it’s a fading super power, but it still has control over its forced allies and vassals – many of whom, by now are sick and tired of their ally-cum-vassal status, as they realize what their losses are. They believed in economic, diplomatic and military privileges, but are gradually awakening to reality. Progressively they see the empire as what it is, a shiny, blustering, preposterous house of cards that may come crashing down at any time. Their anger and courage of Washington’s vassalic allies is slowly raising, and they will eventually break out from their repressive situation. When that happens – and Trump is hastening that moment with his erratic ‘sanction-prone’ behavior around the world – a grand geopolitical shift for the better may take place.

—

With all the flattering and roses the leaders of Taiwan may get from Trump, do they realize that their role will just be that of one more enabler to enhance the empire’s dominion and increase the US’s wealth by helping it steal more of the world’s resources?

In the end, Taiwan may just become a mess, a chaotic island with lots of loose ends, with people pulling in different directions, as they realize that their government has been “bought” to give away their partial sovereignty and well-being – and they will raise up.

Taiwan, just look around the world! – The latest example being Sudan. Orchestrated chaos is controlling Iraq, Afghanistan and Syria? – And look what is being planned, so far without success, in Venezuela? – Taiwan will just be another pawn on Zbigniew Brzezinski’s legendary Grand Geopolitical Chessboard.

The US has been fomenting worldwide hostility against China and Russia for the last 100 years, and especially since WWII, intensified by the fake and false Cold War, made possible thanks to an all-western-dominating AngloZionist lie-propaganda machine.

—

We know about “Russia Gate”, the never-ending bashing of President Putin and Russia. The more subtle US attempts to destabilize China have started soon after China had become fully self-sufficient and autonomous, when she gradually opened her borders to integrate into the world with exports and attracting foreign investments in the 1980’s. The so-called Nixon ‘ouverture’ to China, Nixon’s one-week trip in 1972 to Beijing, Hangzhou, and Shanghai, was perhaps the first attempt by Washington to use the huge Chinese market for US exports, and at the same time constraining China’s rapid and foreseeable economic growth. Indeed, China grew exponentially and in 1986 gained observer status at GATT (General Agreement on Tariffs and Trade), a precursor to WTO, and started negotiating membership of the World Trade Center – of which she eventually became a member in 2001.

Trade, Chinese highly competitive exports was then – and is today – a key issue for the US goal of world hegemony. In anticipation or rather to prevent China from becoming a world economic powerhouse, Tiananmen Square protests were introduced in 1989. The leadup to the so-called massacre was a huge false flag. A student protest movement, funded by the US State Department, through the infamous NED (National Endowment for Democracy – an “NGO” specialized in “regime change” operations – see also Venezuela). The 4th of June crackdown had been prepared months before, guided by the bloody hands of US Secret Services, CIA, NSA, and most probably MI6. The “students” had no common cause for the protest, just a sudden desire for more “freedom”, “reforming the communist party” without citing specifics they wanted reformed.

The 4th of June 2019 anniversary of the ‘massacre’ 30 years ago, is used by the western media to propagate against Chinese “tyranny”. The news of the massacre was repeated every hour on the hour by almost all radio and TV stations throughout Europe, lest you might forget, and the too-young-to-remember – should learn and be prepared for the coming Chinese monster. That’s the goal of the corporate presstitute. And they may succeed, as sleeping people have no clue of the truth, nor are they interested in abandoning their comfort and facing the inconvenient truth.

Let’s just juxtapose the forced memory of Tiananmen Square with real atrocities being perpetrated by the west, as these lines go to press. Take Yemen, devastated by the west and its proxies, chiefly Saudi Arabia and Qatar, with weapons and funding from the US, the UK and France. Yemen is a non-aggressive peaceful country. Tens of thousands of people have been killed in the last 4 years of this atrocious war, most of them children and women, thousands from cholera and other water and improper hygiene related diseases; two thirds of the population suffer from famine. The related death toll is in the tens of thousands. This is exacerbated by the Red Sea Port of Hudaydah, the gateway for most of Yemen’s imports, being shut by Saudi and Qatari armed forces, so that not even emergency aid enters the country. The UN calls it the largest humanitarian crisis in recent history. – You hardly hear anything in the western news about this western funded and executed atrocious mass killing.

False flags from Tiananmen Square, to 9/11, to the Ukraine Maidan, to the sporadic string of terror killings in Europe and the United States, by ISIS / IS Al-Qada and associated groups – all funded by the empire and it’s proxies and vassals – to the more recent ‘regime change’ or Color Revolution type protests in Hong Kong, the Umbrella Revolution of 2014 and street protests of the last week, with thousands of protesters in the street against a Beijing initiated extradition law to be introduced by Hong Kong’s legislation – are all US / western instigated, funded and guided so as to provoke and destabilize China. And foremost, demonize China in the eyes of the western world. Most western countries have extradition laws for criminals to be turned over to the jurisdiction of the country where they may have committed the crime. But that’s not mentioned by the corporate lie-propaganda.

These permanent aggressions against the world power China – a world power with a pacific non-expansive life philosophy, could badly backfire. Just imagine, Beijing may eventually get sick and tired of Washington and its vassal-allies meddling in PRC’s internal affairs, could easily repeal Hong Kong’s semi autonomy and incorporate the city fully into the territory of the PRC – complete with Chinese laws, obligations and benefits. As simple as that. What would Washington do? What would the west do? – Scream murder? – Well, they do that already, so it couldn’t be much worse. A military aggression on China? – Hardly. The West wouldn’t dare. Attacking China is attacking Russia. There is a strong alliance between the two countries, one that was made even stronger by several new agreements signed between Presidents Putin and Xi during the recent St. Petersburg International Economic Forum.

Similar provocations are planned and take place with Taiwan. In April 2019 the US sent two destroyers into the Taiwan Straits, claimed by mainland China as their territorial waters. Germany – which according to their armistice status’ obligation of non-confrontation and non-aggression – is considering sending a war ship to join the US and French warships in an attempt to demonstrate to the world that these are international waters.

What if such provocations, rather than gathering more world recognition of Taipei’s self-styled autonomy, they prompt President Xi Jinping to close in on Taiwan and actually absorb the island as a PRC owned territory? This would just conform to what Taiwan nominally already is since 25 October 1971, when the UN General Assembly Resolution 2758 declared The Peoples Republic of China as the sole legal China.

Switch to another corner of the world with a different but very much connected scenario. Early this morning, 13 June, in the Strait of Oman, about 25 km from the coast of Iran, a Japanese-owned and a Norwegian oil tanker (the owner of which is an old friend of Iran’s) were attacked. Explosions and fire broke out, some seamen were injured, and 44 were actually rescued in the Gulf of Oman by Iranian ships. As of now, it is not clear what happened and who the perpetrators were. Never mind, Pompeo immediately accused Iran for the attacks – and keeps doing so, stating falsely that video evidence – never offered to be seen by the public – showed it was Iran. Why would Iran attack a Japanese oil tanker, while Japanese Prime Minister, Shinzo Abe, is visiting Iran’s Supreme Leader Ayatollah Ali Khamenei in Tehran on Thursday, the very day of the attacks, for talks to maintain the treaties of the Nuclear Deal?

World! Let’s face it. Only an idiot will believe that the world is idiotic enough to believe that Iranians are so idiotic as to attack foreign vessels in the Gulf, clients and friends of Iran. If this smells like a false flag – it is a false flag. Carried out by whom? Could be the Saudis, Israel, the Emirates, Mossad, the CIA, MI6… any one of the puppet allies of the emperor.

People, where are we going? – As a result of this incident oil prices rose immediately by up to 4% for fear that worse might happen, namely that Iran might close the Strait of Hormuz through which about 25% of the world’s hydrocarbon are shipped. A closure could have oil prices jump to USD$ 200 / barrel or more – and sink the world in the worst recession of recent history. In the meantime, Wall Street bankers, notably Goldman Sachs, who have ample experience with oil price manipulation, are already playing with oil futures which under such a scenario could bring them hundreds of billions while the rest of the world goes belly up.

On another, but very much related topic: Many, especially unaligned countries, are losing trust in the US and especially in the US-dollar. They are quietly switching their reserves to Chinese yuans and / or gold. Trump’s handlers know about it. They may be contemplating as a last resort a new kind of gold standard. Losing out on dollar hegemony is one of the reasons they are pushing The Donald into a trade war with China. The (US) expectation is that a trade war with China would debase the Chinese currency, thereby discredit it and make it unattractive as a reserve money.

Creating a conflict between PRC and Taiwan, might, from a US point of view, have the same effect, degrading the yuan, in addition to bringing other Asian countries on board, those who are themselves worried about their territorial waters, i.e. the Philippines, Malaysia, Indonesia.

And yet, in an opposite corner of the world, namely in the swamp of Washington, the same Pompeo who just found another reason to increase sanctions on Iran, is utterly upset that his plans in Venezuela didn’t work out, because the stupid opposition cannot unite, cannot be trusted. That would leave only the ‘military option’ on the table – but that military option is too risky with Venezuela being supported by her strong allies, Russia and China.

Friends – what you must be aware of – all the dots of conflicts, wars, threats, harassments, false flags, sanctions and otherwise punishments, lies and lies and lies around the world, are dots that must be connected. Only then you get the Big Picture – and to understand the Big Picture is crucial. It is at once hilarious for the phantasy it portrays and catastrophic for the danger it presents. For the owners of this Big Picture, the Washington Swamp and Israel, it represents the illusion and desire to achieve the US-Pentagon-Banking plan – within the PNAC (Plan for a New American Century), a wishful thinking of Full Spectrum Dominance.

This Big Picture is best portrayed by Chris Black’s latest master piece: This Outlaw Power: America’s Intent is to Dominate China, Russia and the World

About the Author

Peter Koenig is a Research Associate of the Centre for Research on Globalization.

First published by the New Eastern Outlook – NEO