By Dr. Kalim Siddiqui

I. Introduction

This article also draws upon the East Asian economies’ abilities to allocate resources to stimulate industries and technological development. Despite differences in economic performance, East Asia including China has hugely transformed in the last mere four decades from being very poor, to achieving higher economic growth and incomes, and most of all reducing unemployment and poverty. The big question for academics and social scientists is how was this success achieved in such a short period?

The well-known, Ricardo’s trade theory of ‘comparative advantage’ is the primarily cost-based theory, but it ignores the historical development of industries in the developed countries. His trade theory explains very little about the factors behind the successful move towards industrialisation by some latecomer countries (Siddiqui, 2018d; see 2017c). More recent trade theories, for example, Krugman (1979) and Findlay (1978) acknowledge the important role of technological transfers in order to achieve higher incomes. They note that those developing countries, which have successfully been able to establish industries and advancements in technology thus catch-up with developed countries by adopting the latter’s technology. This is the same argument put forward by Vernon’s life cycle model (1966), which emphasises that the cost of production is a critical factor behind the choice of production moving to developing countries. It is claimed that the industries would shift at the later stages of the product life, from developed to developing countries, and then the developing countries could gain access to advanced technologies and know-how. As a result, this could trigger a process of expansion of manufacturing.

At present, China has emerged as the world’s second largest economy in gross domestic product terms.

It is argued here that the idea of industrialisation is still valid, feasible and relevant for developing countries. The state intervention policy attempted to improve the business environment or to alter the economic structure towards high-value manufacturing sectors. Soon after independence from the European powers, there was a general consensus among the developing countries until mid-1980s that industrialisation is associated with overall economic advancement and would improve the living conditions of their inhabitants. However, such policy aim became less important due to the debt crisis and pressures from transnational companies who were looking for global market integration to increase their profits (Siddiqui, 1996b).

At present, China has emerged as the world’s second-largest economy in gross domestic product terms. Only forty years ago, China was one of the poorest economies prior to its economic reforms. Understanding China’s policy direction can provide a deeper understanding of this rapid transformation and the lessons it offers to other former colonies or semi-colonial countries (Siddiqui, 2019b; see 2015d). In 1978, Deng Xiaoping launched gradual economic reforms in China to depart from a state-controlled economy. While until 1800, Imperial China was a dominant economic power, its economic growth started to stagnate and decline (Maddison, 2001). Marco Polo (1254-1324) was an Italian traveller, who travelled to Asia from 1271 to 1305 and stayed in China for 17 years, where he joined a diplomatic mission to the court of Kublai Khan, the Mongol leader whose grandfather, Genghis Khan, had conquered Northeast Asia. Marco Polo was the first European to publish a detailed account of Chinese society and its economy. He vividly described what he saw in Asia as a very highly developed civilisation. Others like North African traveller Ibn Battuta (1304-1368) and historian Ibn Khaldūn (1332-1406) also published a detailed account of their journey to Asia and South Europe during the fourteenth century. However, in China the Qing Dynasty was unable to industrialise like Britain and other West European countries and its power was further undermined by a lack of sovereignty to pursue independent economic development as a result of two opium wars and the imposition of unequal treaties by British and French armies (Siddiqui, 2020a; 2020b).

Apologists for the European Empire portray colonialism, the slave trade, European control over resources, and the undermining of sovereignty in Asia, Africa and Latin America as a positive development that transformed these societies and economies. Although defending colonialism is no longer popular, a few apologists still have nostalgia for the British Empire. For instance, Niall Ferguson (2003) tried to discover positive aspects of the British Empire. It seems to indicate a lack of knowledge and ignorance of what did in fact happen in the colonies during the colonial rule. The glorifying of colonial rule, and racial supremacy, is nothing new and was a widely spread myth during the Victorian period (Siddiqui, 2019a; 2009b).

During the reign of Aurangzeb, India was the world’s largest economy, worth over 27% of global GDP, and controlled nearly the entire Indian subcontinent. His rule lasted nearly 50 years (1658-1707), and he was the last great Mughal emperor of India. The British Raj in India was disastrous. In 1700 when a British trading company (i.e. the East India Company) was established in India, India’s share of the world’s GDP was 27% and the British share was merely 1.8%, but by the time the British left India after 200 years of the British Raj, India’s share had plummeted to as low as 3%, while Britain’s rose to 10% of the global GDP in 1947. (Siddiqui, 2017b; 2014) Hence Britain became a prosperous country by impoverishing India. Britain took over the richest country and in 200 years of her rule transformed India into one of the poorest countries in the world. Britain achieved this through a number of measures such as dismantling Indian handicraft industries, raising land rent, expropriating India’s wealth as so-called ‘tribute’ charges, and draining India’s resources to Britain (Siddiqui, 2019a). As a result, Britain became a world-leading economic and military power, and the exploitation of India financed the rise of Britain (Bairoch, 1993; Siddiqui, 2020c).

Indian textiles, for example, were one industry that was ruined. In 1800 India’s share of the world trade was 23%, but by the time British rule ended, trade was totally destroyed and India became specialised in the export of raw materials. The Indian market was flooded with British industrial goods and a tariff was imposed in Britain on Indian textiles, while the tariff on British goods coming into the Indian market was removed. Similarly, India’s steel and shipbuilding were destroyed to make way for imports from Britain. The building of railways was the biggest scam. The purpose of railways was to transport armies and bring raw materials from the interior regions to the coasts, and take British manufactured goods to the interior regions of India. The costs of building railways were very high and the British investors were given guaranteed the highest returns paid by Indian taxpayers. The de-industrialisation led to a rise in the rural population and at the same time, land rent charges were raised from pre-colonial rates of 15% to as high as 45% of the agricultural output, which resulted in increased rural indebtedness and occurrences of famines with greater velocity (Siddiqui, 1996a). By the end of the 19th century, India was Britain’s biggest source of revenue, the worlds’ biggest purchaser of British industrial goods, and the largest source of British high-paid employment at India’s cost.

During the 19th century, the rate of economic growth was very slow everywhere and the differences in living conditions and consumptions of the inhabitants in different countries were comparatively small. However, with the emergence of the industrial revolution, in particular, some countries began to grow exceptionally high in terms of GDP, while others were left behind. A further rise in growth rates was achieved with the establishment of large-scale manufacturing industries. Those who had accumulated more capital and could invest began to develop monopolies and thus could successfully charge higher prices. For example, by 1880, Britain produced two-thirds of the world’s total manufactured goods and was a global superpower. Commenting on the expansion factories in England, Kaldor (1977:196) notes: “For the very system of ‘factory production’ gave a continued and powerful incentive and installation of ‘bigger and better machines’, which were increasingly labour-saving and able to produce goods on an ever-increasing scale. It also gave a continuous incentive for the invention of new products, of new processes, and for increasing specialisation in the making of parts and components”.

Industrial growth also depends on the growth of ‘outside’ demand, which is partly the result of increased market penetration at the expense of other countries’ industries, or small scale pre-capitalist, and in the agriculture sector, partly due to a rise in farmers’ productivity and incomes so they could buy industrial products. The rate of industrial growth depends on the rise of markets for industrial goods outside the industrial sector. The rise in export markets of British manufactured goods from the beginning of the industrial revolution greatly contributed to its industrial development, which could also be called export-led growth. As Kaldor (1977:200) further emphasises: “Britain, being the first country to manufacture goods in factories on a large scale, was able to increase her exports at a fast rate, partly at the expense of other exporting countries (such as France), but largely by competing successfully with small local producers in other countries. The growth of exports of British-made cotton goods to India and China in the 19th century meant a severe shrinkage of local small-scale enterprise – the virtual disappearance of locally made hand-woven cloth – without any compensation in the form of alternative employment opportunities for the people displaced. With the transport revolution, vast areas became accessible to trade, and regions previously self-contained were increasingly drawn into the network of the world economy.”

The ‘forced specialisation’ during the British colonial period created mass poverty and ruined local handicrafts in the colonies to create markets for British industrial goods. Mainstream economists have failed to present the underlying causes of developed countries keeping some countries economically backwards. As Storm (2015: 669) notes: “Development economics appears to have fully come to circle, as interest in and concern for industrialization have made a comeback, echoing major concerns of the early development economists. However, when it comes to the practice of industrialization strategy and industrial policy, the default recommendation is still the market and static comparative advantage – the main task of governments is to impose institutional reforms and improve governance so as to allow markets to perform more efficiently.”

II. Literature Review

The neoclassical economists had nothing to say about the very pertinent questions which occupy the minds of economic historians: why do some countries or regions grow relatively fast while others remain backwards or stay poor? The division of the world into rich and poor countries is, I think, considerably important because it creates misunderstandings and prejudice about the poor countries. In fact, the division of the world into rich and poor countries as exist today is a recent phenomenon in our long human history. In the last three centuries, differences in rates of economic growth only emerged with industrial capitalism, first in England in the last decade of the 18th century, also known as the industrial revolution. The primary sources of capital were profits from the slave trade and colonisation. With the availability of huge capital accumulation, the country was able to invest in defence, education, technology, and thus could control global resources and markets.

Why did certain countries industrialise and become richly endowed with capital and technology and therefore move towards a higher standard of living? The answer is, in England by the 1780s traders and merchants became very powerful due to the development of overseas trade, following the colonisation of North America and Bengal province in India. The other crucial factor which contributed to the industrial revolution in England was agrarian changes i.e. in the form of new crops, the adoption of new methods of agricultural production, and ‘Enclosures Acts’ of Parliament, where the landlords were given possession of land by depriving the peasants of their traditional common lands. The ‘enclosed lands’ were cultivated as much larger units and by using new production techniques; this also cleared the way for increased commercialisation of agriculture. The increased agricultural surplus was sold in the market and those peasants and tenants who lost their traditional means of support were expelled from the land and forced to find employment outside in the cities, i.e. as Karl Marx described it ‘by selling their labour’ i.e. labour itself became a commodity.

Between 1845 and 1874 Britain experienced a dramatic rise in industrial production and this was also the period in which its share of the world’s trade in manufactured goods was at its highest. In fact, the birth of modern industries gave Britain a strong competitive edge over other countries in the first seventy years of the 19th century, as it faced virtually no real challenges to its supremacy in manufacturing and also in military strength after Napoleons’ defeat in 1815 at the battle of Waterloo.

Historically, the development of capitalism in Britain from the early 18th century as the merchant and bank capital had invested heavily in colonial and overseas operations, including slavery, which was backed by the state and the navy. And by the end of the 18th century, industries began to develop, and industrial capital emerged, which was detached from the City of London based on nexus of merchants, bankers, and aristocrats. However, this had disadvantaged manufacturing ever since and the bankers and traders were unwilling to lend to manufactures and these financiers always had been interested in overseas. In contrast to Germany and Japan, where there has been a close relationship between banks and industry. However, in Britain, the industries have had to rely their financial needs on the stock exchange and have had to pay high dividends to shareholders. From the late 19th century the rentiers and speculative capital were reinforced by the development of large urban property estates on high commercial rents and they were closely connected to banks. Also, the exchange rate and monetary policy have been geared in the interests of financial capital. In fact, the exchange rate has been kept at a high level for manufactured exports and interest rates tend to be set high, which produced a chronic deflationary bias, which undermines productive investments (Siddiqui, 2018a; 2015a).

The development of capitalism in Britain from the early 18th century as the merchant and bank capital had invested heavily in colonial and overseas operations, including slavery, which was backed by the state and the navy.

In 1900, nearly 50% of the total British capital was invested abroad, which still continues. As Norfield notes: “in 2013, Britain had the second-largest stock of foreign direct investments [after the US]… Among the top 500 global corporations in 2011…the UK was in second place behind the US, with 34 companies…Of the world’s top 100 non-financial corporations in 2013, ranked by the value of their foreign assets, 23 were US companies, 16 were British and 11 were French, while Germany and Japan each had ten.” (Cited in Calinicos, 2016) After, World War I, despite Britain’s imperial decline, but still it was able to maintain the power of the City of London. And after World War II, the country created tax havens for rich foreigners.

However, later on, due to the continuous loss of foreign markets caused by the growth of industries namely in France, Germany, the US and Japan, British export markets gradually not only declined but also faced increasing competition. These countries utilised the same protective tariffs and other forms of state support as Britain had adopted a century earlier. In the past, advanced economies relied heavily upon government intervention to promote manufacturing and adopted protections of their domestic industries. This included Japan, which escaped colonisation and thus was able to create a path towards industrialisation suited to its needs (Siddiqui, 2015a; 2009a).

In the US, soon after independence from Britain in 1776, there was a discussion among politicians and academics regarding whether the US should undergo industrialisation and produce locally, or buy manufactured goods from Britain. Those with large plantations and big landowners supported focusing on agricultural exports and importing manufactured goods from Britain and such views had also support in Britain. While the critics argued in favour of setting up manufacturing, which they saw as a difficult task in the short-term, but in the long-term, such a policy would provide long-term economic development. They argued that it would have a positive impact not only on industries but also on the agriculture sector and overall productivity, and moreover, industrialisation would make the US a sovereign and economically independent country.

For instance, in the early phase of the development of industries in England, in 1721, British Prime Minister Robert Walpole adopted a number of economic policies to transform the country from an exporter of raw materials into an industrially advanced nation. He brought in legislation to protect and support domestic industries from foreign competition and supported local industries through export subsidies. He also raised tariffs against manufactured imports and banned exports of raw materials and skilled workers leaving the country. Walpole’s economic policy then was not in support of an ‘open market’ and free trade but in support of the protection of domestic industries. However, once Britain’s manufacturing sector developed and became competitive, it had entirely different plans for its colonies in North America and India. As Girdner and Siddiqui (2008: 9-10) notes: “In India too, colonial authorities forced the country to specialise in the production of raw materials such as cotton, jute, opium, tea and so on, Britain banned cotton textile imports from India (calicoes) which were then superior to the British ones…. Successive British governments charted policies in the colonies so that the countries they ruled specialised in the production of raw materials and thus were unable to become competitors with British manufacturers”.

III. The Political Economy Approach

Those who study political economy seek to understand how history, culture, and politics impact economic performance and overall economic development. It also takes into account the international impacts on local economies. The international political economy is ultimately concerned with how political forces influence economic policy structures, and how institutions shape systems through global economic interactions and affect a country’s economic performance. The importance of economic, historical and international factors in attempts to build manufacturing, has been emphasised by researchers such as Myrdal, Baran, Kalecki, Hirschman and Kaldor. (Siddiqui, 2021a; 2018b)

Neoclassical economists explain the expansion of competition through markets and resource scarcity as integral points. Their theories ignore the global power structure and assume the existence of competitive markets in international trade, which is far from the truth. Thus, they are unable to present an explanation of why some countries are rich and powerful, while others remain poor and powerless. Why did the poor countries need to specialise in whatever they could produce at lower costs, which is known as ‘comparative advantage’, to correct their imbalances?

The classical developmental theory defined growth as ‘structural change’ which was backed by Prebisch and Singer’s thesis on the long-term deterioration of the terms of trade against developing countries, due to dynamic economies of scale being more prominent in the manufacturing sector (Siddiqui, 2012a; Siddiqui and Armstrong, 2017a). When manufacturing grows it also creates spill-over effect on other sectors and economic diversification becomes faster. Kaldor (1966) demonstrated the close relationship between long-term growth and structural change, which is known as ‘Verdoorn Law’. According to it, faster growth in output increases productivity due to increasing returns. Productivity growth is the key to economic development. Kaldor’s study on the relative stagnation in the British economy in the 1960s-70s, where he compared British economy to other developed economies and points out that the aggregate labour productivity depends largely on manufacturing output growth. He stresses that the relationship between labour productivity and output growth should be interpreted by the performance of the manufacturing sector. As Kaldor (1966: 106) noted: “productivity tends to grow faster, the faster output expands; it also means that the level of productivity is a function of cumulative output (from the beginning) rather than of the rate of production per unit.”

Economic development requires the transformation of the productive structure, which was mainly achieved in the past through industrialisation.

For the contemporary developing countries, the stimulus of industrialisation came after their independence, from state intervention in the forms of high tariffs or severe quantitative restrictions on imports. This policy made it profitable to develop home industries in substitution for imports, but by the mid-1970s and 1980s, the slow growth of either the export or agricultural sector put a constraint on markets, and thus the basis for the sustained growth of industrial production was missing, as a result the ‘Import Substitution Industrialisation’ possibility was exhausted (Siddiqui, 2018a).

Economic development requires a transformation of the productive structure, which was mainly achieved in the past through industrialisation. It means promoting structural change from the production of low-value to high-value commodities, and to achieve it, industries could play a vital role. Historically, rapid economic growth and improvement of economic conditions have been associated with the expansion of manufacturing. (Siddiqui, 2015b; 2015c) For example, past experience tells us that the economic development and creation of accumulation depends on the use of knowledge, technology and innovations to increase output and productivity per worker. It also depends on investment, particularly by the government through the use of fiscal policy, as happened during post-war Europe, when the state not only nationalised key industries but also increased funding in research and development of new technologies. It certainly did not leave these crucial aspects to the private sector only, as it is now advising to the developing countries.

IV. Industrialisation in East Asian and Latin American Countries

Why state intervention and the promotion of infant industries were successful in East Asian, but not Latin American countries? The development of the auto vehicle sector in the East Asian economies, for instance, had been strongly supported by the state. South Korea began with small-scale assembly plants and within less than two decades, the country was able to develop a competitive auto sector (Amsden, 2001). As Jenkins (1995: 627) notes: “The two key transactions in the development of the automobile industry have both (South Korea and Taiwan) involved a high degree of state intervention. The crucial form of state intervention in the transition to manufacturing in all countries was the setting of local content requirements for firms that wished to produce locally while giving them substantial protection from imports….. the state also intervened to limit the extent of foreign ownership in the industry. Government intervention also occurred at various times to attempt to rationalise the industry by preventing new entry, encouraging mergers, rationalising production or reducing the number of models in existence.”

Successful industrialisation in East Asian economies seems to have a clear vision where new combinations of productive resources, technology, and a favourable international climate successfully transformed the region during the Cold War. It appears that the state policy in East Asia shaped educational and skill development systems along with capital to generate R&D within increasingly productive enterprises (Siddiqui, 2012b; 2010).

In the 1960s, East Asian countries promoted labour-intensive industries such as footwear and textiles, and gradually shifted from agriculture to manufacturing with a strong potential for productivity growth (Economist, 2010). Their governments realised the significance of the industrial sector for their economies, which continued to deepen over the period. By 2015, East Asia and China had a significantly higher share of manufacturing value-added than other regions (Siddiqui, 2019c). As the heterodox economist Fransman (1984:11) observed: “Technology and technological change are not autonomous forces exerting uni-directional effects on society and neither are they neutral … transcending existing social and theoretical circumstances. The recognition, however, that science and technology interact with important ways and that both are intimately affected by the prevailing social, political, theoretical and economic circumstances have extremely important implications for the way in which we examine technology and technological change.”

For instance, the economic policy adopted in Japan in the 1950s was also followed soon after by South Korea, Singapore and Taiwan. Researchers have found that companies in East Asia established productive linkages and interactions with state, private capital, and institutions that propelled innovations, along with value chains in electronics, chemicals, and auto vehicles in overseas markets (Siddiqui, 2016a; 2016b).

The success of the East Asian economies, particularly South Korea, developed its very competitive auto sector in the 1980s-90s. This policy is described as ‘developmental statist’, which acknowledges that the key factor in the success of East Asian economies is state intervention. (Siddiqui, 1995) There are a number of views such as structuralist and institutionalist economists, which argue that industrialisation requires active intervention. They argue that infant industries under capitalism, due to the problem of market failures, particularly in investment, technology and market coordination require state intervention, therefore, there is a need to ‘socialise risk’ as a means of enhancing the domestic economy and developing strategic assets. The neoclassical economists argue that infant industries do not mature and government incentives encourage unproductive activities.

The success of the East Asian economies, particularly South Korea, developed its very competitive auto sector in the 1980s-90s.

In Brazil, industries grew rapidly in the post-war period but faced a crisis in the mid-1980s due to a rise in external debts and inflation. Brazil’s economy in the last thirty-five years has adopted its short-terms macroeconomic policy while neglecting long-term industrial policy, which resulted in a decline in manufacturing and in catching-up with developed countries. Its manufacturing is still not fully developed and is ‘immature’ in Kaldorian terms i.e. where a large supply of labour still remains in low productive sectors. Countries can only attain the “maturity phase” when productivity levels become aligned between all sectors of the economy as a whole. As Nassif et al. (2018: 360) observe: “One case for premature deindustrialisation may occur when developing economies – which might have a rather diversified industrial base but have not yet completed their industrialisation process-are exposed to external competition without internal defence mechanisms of economic policy to continue the implementation of their structural change. This movement occurred in some Latin American economies in the 1990s and 2000s (especially Brazil and Argentina) following the economic opening according to recommendations of Washington Consensus. Since economies are deprived of defence mechanisms (such as tariff barriers, subsidies for exporting manufactured goods, capital controls, among others).”

In Brazil, the auto industry was dominated by foreign companies, in contrast to this; South Korea’s Hyundai Motor Company was a major part of the country’s conglomerate ‘Chaebols’ (industrial groups). The company’s growth is an interesting story. The company began by assembling Ford in 1966-67 but by 1972-73 the company developed a conflict with Ford over its joint venture plans and the production of the vehicle in South Korea. The joint venture talks ended in failure, and then it decided to develop its own model, which was known as Pony. The government then fully supported Hyundai against Ford and extended financial and technical support to the company to become a major car manufacturer. However, given the small size of domestic markets, it was difficult for Hyundai to increase production and achieve economies of scale, and hence exports became its major long-term objective in order to become a successful vehicle producer.

The difference between East Asia and Brazil as far as export promotion is concerned, is that in Brazil exports were promoted after the development of local markets, while in South Korea exports was promoted from the beginning. South Korea launched its auto manufacturing in the early 1970s, when the government closed various small unit industries and encouraged only four firms to produce vehicles. Effective intervention needs a higher degree of autonomy of the state from the dominant class, which allows the state to focus on key objectives rather than serving and protecting the narrow interests of small groups or short-term interests. In 1973, the government announced its prioritisation of the Heavy and Chemical Industry and its long-term industrialisation included promoting the auto vehicle sector. The aim was to achieve about 90% of local materials and contents for domestic car production and move towards a major exporter by 1982. Under this plan, only three companies were given a license to go ahead. By the mid-1980s, the government further rationalised the auto industry, by reducing it to only two producers.

This development strategy requires close coordination between the macroeconomic and industrial policies. We argue that consistency in the fiscal, monetary policy and exchange rate policy will be able to sustain price stability and low interest rates, which could mean higher profits for investors.

There was no doubt that by 1991, Brazil and South Korea became the world’s most successful and competitive auto producers. South Korea emerged as the worlds’ eighth largest vehicle producing country ahead of the UK, while Brazil was ranked as eleventh in 1991. However, in Brazil, the costs were reduced to approach international levels, but the economic crisis and macroeconomic policies during the 1980s were less favourable to the local auto industry. The domestic market had stagnated and foreign debts rose sharply, which led to a debt crisis and under pressure from the IMF and World Bank, the government had to adopt SAP, which resulted in adverse development of its auto sector. In South Korea, the state played a key role in the success of auto vehicle export promotion. The Amsden study (1989), and a later one by Wade (1990) documented that state intervention and support was an important policy measure. In fact, in South Korea, the state had shown a high degree of autonomy to undertake policy measures in favour of larger interests rather than fractional or narrow interests.

The long-term overvaluation trend of the real exchange rate in Brazil (i.e. in the last three decades) was to boost commodity exports. But the appreciation of the exchange rate of the Brazilian currency has adversely impacted the growth of manufactured goods. For example, in Brazil, the share of primary products and manufactured goods based on natural resources rose from 40.3% to 63% between 2000 and 2015. In the same period, there was a significant drop in the share of engineering, science and knowledge based products from 18.7% to 9.9%; manufacturing exports from 32.2% to 23.1%; and labour-intensive manufactured goods had a significant decline from 8.8% to 4.4% for the same period. The study by Nassif et al. (2018: 370) concludes: “With the rapid trade liberalisation in the 1990s and recurring trend of overvaluation of the Brazilian currency, Brazilian exports deepened her specialisation in primary products and natural resource-based industrial commodities… the Brazilian case of the Dutch disease explained by a sudden discovery of natural resources … nor by an exporter boom of tradable goods in the service sector… the new Dutch disease that has been hitting Brazil from the 2000s onwards with the dramatic deepening of an international specialisation pattern based on the exploitation of natural-resources based industries.”

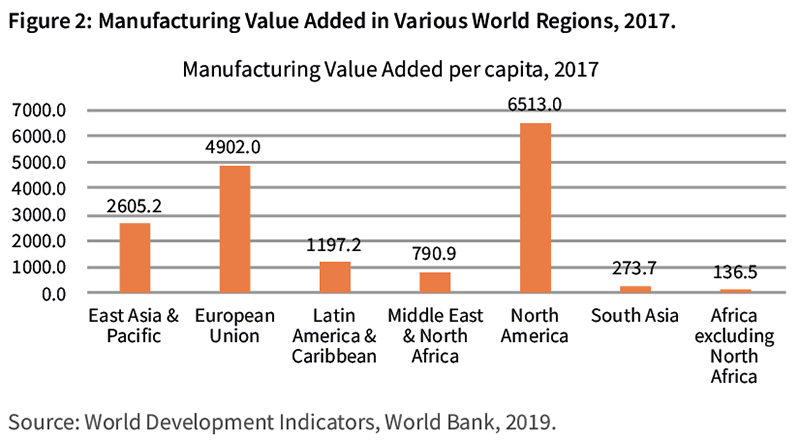

Most of the East Asian countries by the early 1960s followed economic autonomy to pursue national development policies and at present re-emerge as important players in the world economy. The share of the East Asian economy of the global GDP rose six times from less than 4.0% to 25% between 1960 and 2018 (See Figure 1 and Figure 2). The faster economic growth of Asia was the result of the considerable structural transformation as is clear from Asia’s share in world industrial production (See Figure 3), increasing 10 times from a minuscule 4% to over 40% during the same period. (Siddiqui, 2021c) The transformation of East Asia from the most backward and impoverished region, to the growth locomotive of the world economy within forty years is unprecedented in human history and in fact, a positive development for other late-comer industrialising countries.

V. China’s Sources of Growth

Chinese economic reform approach differed from the Soviet Union and other East European countries. Its reforms were gradual and always remained under government control and were certainly not led by international financial institutions like the World Bank and IMF. China began slowly giving more incentives and freedoms to rural households. The government provided incentives to farmers by introducing the Household Responsibility System. The system was introduced to address two issues in agricultural policies; the introduction of a dual-track pricing system based on both the market and planned system, and providing autonomy to farmers as incentives to produce more output. The government did not establish private property, and the village community retained ownership of farmlands and provided equal land access to farm households. The policy for farmer households having ownership of the lands allowed the agricultural sector to improve as it retained labour in rural areas while keeping their rural migration to the cities under control.

During the 1980s, China focused on domestic industrialisation and to achieve this, the state intervention was seen a pre-condition, as was adopted a few decades earlier by Japan and South Korea. The government opened-up a few coastal areas for foreign investments in joint ventures in industries, where the focus was to encourage the transfer of technology, skills, know-how and exports. Moreover, rural reforms rapidly increased rural productivity and output. As Hazwan (2020:16) observes: “the productivity in the agricultural sector and the subsequent reallocation of labour to the non-state sector developed the rural economy. However, the productivity gains made began to level of as TFP (total factor productivity) rates remained constant between 4 to 5% during the 1990s…. the rural sector contributed to the economy more than the urban sector before it exhausted its productivity gains.” China’s cheap and abundant labour along with high domestic saving rates and also in the early 1990s China became one of the largest inflows of foreign capital in the developing world. The overseas investment initially has enabled the economy to benefit from capital accumulation through overseas investment and thus was able to absorb superior and deploy foreign technology and management skills, which resulted in rapid growth rates. Hazwan (2020:18) concludes: “many foreign firms have viewed China as a source of economical labour, while China has recognised the value of foreign firms, benefiting from capital inflow, managerial knowledge and superior foreign technology that can be absorbed, allowing the economy to benefit more than through simple capital formation… specialising in labour intensive and light manufacturing goods… .”

Trade liberalisation resulted in a rise in regional inequality, because FDI was mostly focused in coastal regions (Siddiqui, 2019d). Moreover, credit-starved small businesses tapped into their friends and family as sources of credits, in the manner of the old cultural traditions of Chinese kinship-based networks known as Guanxi. This informal mechanism operated through the Chinese business culture of trust, based on Confucian philosophy. The state provided preferential treatment in order to attract more capital in special economic zone coastal areas. Initially most of the overseas investors and most of the entrepreneurs came from Taiwan, Hong Kong and Singapore.

In China, the growth of the technological capabilities of telecommunication and similarly the electronic industry in South Korea was not due to so much to the government role per se, but rather, the government was able to strengthen the capability of companies in very effective ways. Here we must take into account the important role of learning capability in technological development and overall industrial growth. South Korea relied on capability building as an important catch-up strategy. These policies in practice differ from country to country. For instance, the state has encouraged capability building in China in recent years, where state policy led to building large state-owned companies aimed at compensating for the poor presence of private companies. While in South Korea, joint ventures were adopted as a strategy to access foreign technologies along with huge public investments in education and technological research which enhanced domestic skills and productivity.

Trade liberalisation was a crucial part of China’s export-led strategy, in addition to the nation’s cheap and abundant labour and capital accumulation through the economy’s high-savings rate. China has become one of the nations that receive the most foreign direct investment, as compared to other developing countries, and such investment has enabled the economy to benefit from capital accumulation and to absorb and deploy superior foreign technologies, resulting in a higher growth rate. This approach echoes the Heckscher-Ohlin theory of specialising in labour-intensive and light manufacturing goods (Samuelson, 1949), as China had an abundance of labour. It was suggested that manufacturing goods accounted for the majority of goods exports due to China’s labour cost advantage and spare capacity in production.

VI. Conclusion

The protection of domestic industries was used in the past by the developed countries in their early stages of industrialisation such as in the UK, Germany, the US and Japan. In the US in the early 19th century, Hamilton argued in favour of ‘infant industry’ by extending support to nascent industries until they attained economies of scale and competitive advantage. In Germany, Friedrich List highlighted the importance of industries, and for him, the productive capability depended on the expansion of manufacturing (Chang, 2002). He saw that Britain’s advice to Germany to focus on agriculture was meant to keep Germany as a backward nation (List, 1909). Similar arguments were made by Lall (1992); the role of learning by doing encouraged the late developer countries to protect domestic industries until their companies had achieved sufficient capabilities to be competitive in overseas markets.

Industrial policy should be seen as an important policy to a country planning to accomplish industrialisation and which needs a long-term policy to reverse pre-mature industrial decline. The industrial policy could be to correct ‘market failure’ and to coordinate a set of state incentives such as subsidies and tariffs on imports. Therefore, state support is crucial in order to establish industries and relying alone on market forces and foreign corporations will be disastrous for the developing countries as shown by the recent experiences of the Latin American countries.

The study found that from the beginning, the East Asian countries began developing their manufacturing sectors by targeting the export markets, and also began for a brief period with ‘import substitution policy’. They realised that their domestic markets were limited and thus manufacturing could not achieve economies of scale. These countries opened their industries to foreign competition, welcomed foreign investment and technologies, and also focused on exports, which was used to stimulate economic development. Manufactured products soon became the principal exports of East Asian economies in contrast to other developing countries that largely focused on exports of agricultural commodities. Currently, East Asia has the second highest share of manufactured goods in total merchandise exports, after Europe.

The potential growth rate of an economy also depends on its productive structure, its degree of diversification, and its ability to generate higher value-added per capita.

China’s reforms are interesting as its growth path began with reforms in agriculture and only then focused its efforts in the industrial sector, demonstrating a sectoral shift. Furthermore, the level of openness has stimulated competition in the domestic economy, especially since the recognition of patent and protection law in the 1990s, as it encouraged Chinese firms to devote more resources to innovative activities leading to technological progress. The structural changes that China has experienced, however, altered its traditional sources of growth, as the economy reallocated inputs such as the labour workforce from various sectors in the economy, shifting the accumulation of capital through a repressed financial system. Furthermore, the study suggests that relatively poor countries would benefit from industrial expansion and catching up and converging with developed economies, as less developed economies benefit from economic backwardness and technological transfer, thus increasing the levels of economic development. However, the developed countries have opposed any attempt by the developing countries to industrialise and to follow sovereign industrial policy, which could be described ‘kicking away the ladder’, since they do not want to lose their dominant position in the global economic power structure.

Finally, the study concludes that the potential growth rate of an economy also depends on its productive structure, its degree of diversification, and its ability to generate higher value-added per capita. The East Asian industrialisation presents a very useful experience for others for economic transformation, bringing out the diversity of experiences, and analysing the factors explaining their stunning success that have rich lessons for latecomers and other developing countries. Here for late developers, the expansion of the manufacturing sector could play a major role in the transformation of the economy and it seems that economic growth and the development of the productive structure are both connected. Therefore, there is a need in the developing countries to reconsider the role of the state and also to create a favourable macroeconomic environment for capital accumulation, investment, innovation, structural change, overall economic development, and catching-up.

About the Author

Dr. Kalim Siddiqui is an economist, specialising in International Political Economy, Development Economics, International Trade, and International Economics. His work, which combines elements of international political economy and development economics, economic policy, economic history and international trade, often challenges prevailing orthodoxy about which policies promote overall development in less developed countries. Kalim teaches international economics at the Department of Accounting, Finance and Economics, University of Huddersfield, U.K. He has taught economics since 1989 at various universities in Norway and U.K.

Dr. Kalim Siddiqui is an economist, specialising in International Political Economy, Development Economics, International Trade, and International Economics. His work, which combines elements of international political economy and development economics, economic policy, economic history and international trade, often challenges prevailing orthodoxy about which policies promote overall development in less developed countries. Kalim teaches international economics at the Department of Accounting, Finance and Economics, University of Huddersfield, U.K. He has taught economics since 1989 at various universities in Norway and U.K.

References

- Amsden, A. (2001). The Rise of the Rest: Challenges to the West from Late Industrializing Countries, Oxford: Oxford University Press.

- Bairoch, P. (1993). Economics and World History: Myths and Paradoxes, Chicago: The University of Chicago Press.

- Chang, Ha-Joon. (2002). Kicking Away the Ladder: Development Strategy in Historical Perspective, London: Anthem.

- Economist. (2010). “Picking Winners, Saving Losers,” August 5. London. www.economist.com/node/16741043.

- Fransman, M. (1984). “Technological capability in the Third World: An Overview and Introduction to Some Issues”, pp.3-30 in (eds.) M. Fransman and K. King, Technological Capability in the Third World, London: Palgrave Macmillan.

- Girdner, E.J. and K. Siddiqui. (2008). “Neoliberal Globalization, Poverty Creation and Environmental Degradation in Developing Countries”, International Journal of Environment and Development 5(1):1-27, January-June.

- Hazwan, H. (2020). “The Evolution of China’s Modern Economy and its Implications on Future Growth” Post-Communist Economies. https://doi.org/10.1080/14631377.2020.1793610

- Jenkins, R. (1995) “The Political Economy of Industrial Policy: Automobile Manufacture in the Newly Industrialising Countries”, Cambridge Journal of Economics, 19: 625-645.

- Kaldor, N. (1977) “Capitalism and Industrial Development: Some Lessons from Britain’s Experience”, Cambridge Journal of Economies, 1:193-204.

- Kaldor, N. (1966). Causes of the Slow Rate of Economic Growth of the United Kingdom: an Inaugural Lecture. Cambridge: Cambridge University Press.

- List, Friedrich. (1909). The National System of Political Economy, London: Longmans, Green & Co.

- Maddison, A. (2001). The World Economy: A Millennial Perspective, Paris: OECD Development Centre.

- Nassif, A., L.C. Bresser-Pereira and C. Feijo. (2018). “The Case for Reindustrialisation in Developing Countries: Towards the Connection between the Macroeconomic Regime and the Industrial Policy in Brazil”, Cambridge Journal of Economics, 42:355-381.

- Siddiqui, K. (2021a). “The Study of Economic History and the Importance of Understanding the Past”, The World Financial Review, January/February.

- Siddiqui, K. (2021b). “Prospects of a Multipolar World and the Role of Emerging Economies” The World Financial Review, March/April, London.

- Siddiqui, K. (2021c). “Can 21st Century be an Asian Century?” Asian Profile, forthcoming.

- Siddiqui, K. (2020a). “Britain’s Trade with China in the Eighteenth and Nineteenth Century: A Review of the Opium Wars”, Asian Profile, 48(3): 207-221.

- Siddiqui, K. (2020b). “The Rise of the Chinese Economy and Growing Concerns in the United States”, The World Financial Review, September October, pp. 40-49.

- Siddiqui, K. (2020c). “Globalisation, International Trade and the Developing Countries”, The European Financial Review, August September, pp.60-71.

- Siddiqui, K. (2019a). “The Political Economy of Global Inequality: An Economic Historical Perspective”, Argumenta Oeconomica Cracoviensia, 21(2): 11-42.

- Siddiqui, K. (2019b). “Economic Transformation of China and India: A Comparative Political Economy Perspective”, Asian Profile, 47(3): 243-259.

- Siddiqui, K. (2019c). “India: Neoliberal Reforms and the Difficulties of Industrialisation” Alternatives Sud (in French) 26(4): 119-134.

- Siddiqui, K. (2019d). “The Political Economy of Inequality and the issue of ‘Catching-up’” The World Financial Review, July/August, pp. 83-94.

- Siddiqui, K. (2019e). “One Belt and One Road, China’s Massive Infrastructure Project to Boost Trade and Economy: An Overview”, 9(2): 214-235. International Critical Thought. Taylor & Francis Group, Routledge.

- Siddiqui, K. (2018a). “David Ricardo’s Comparative Advantage and Developing Countries: Myth and Reality”, International Critical Thought, 8(3): 1-28, September. Taylor & Francis Group.

- Siddiqui, K. (2018b). “The Political Economy of India’s Post-Planning Economic Reform: A Critical Review”, World Review of Political Economy, 9(2): 235-264, summer.

- Siddiqui, K. (2018c). “Imperialism and Global Inequality: A Critical Analysis”, Journal of Economics and Political Economy, 5(2): 266-291.

- Siddiqui, K. (2018d). “U.S. – China Trade War: The Reasons Behind and its Impact on the Global Economy”, The World Financial Review, November/December, pp.62-68.

- Siddiqui, K. and P. Armstrong. (2017a). “Capital Control Reconsidered: Financialization and Economic Policy”, International Review of Applied Economics 32(6): 1-19, March.

- Siddiqui, K. (2017b). “The Bolshevik Revolution and the Collapse of the Colonial System in India”, International Critical Thought 7(3): 418-437. Routledge Taylor & Francis.

- Siddiqui, K. (2017c). “Hindutva, Neoliberalism and the Reinventing of India”, Journal of Economic and Social Thought, 4(2): 142-186, June. ISSN 149-0422.

- Siddiqui, K. (2017d). “Financialization and Economic Policy: The Issues of Capital Control in the Developing Countries”, World Review of Political Economy 8 (4): 564-589, winter.

- Siddiqui, K. (2016a). “International Trade, WTO and Economic Development”, World Review of Political Economy, 7(4): 424-450, winter.

- Siddiqui, K. (2016b). “Will the Growth of the BRICs Cause a Shift in the Global Balance of Economic Power in the 21st Century?” International Journal of Political Economy 45(4):315-338, Routledge Taylor & Francis.

- Siddiqui, K. (2015a). “Political Economy of Japan’s Decades Long Economic Stagnation”, Equilibrium Quarterly Journal of Economics and Economic Policy 10(4):9-39.

- Siddiqui, K. (2015b). “Perils and Challenges of Chinese Economic Development”, International Journal of Social and Economic Research 5 (1): 1-56.

- Siddiqui, K. (2015c). “Trade Liberalisation and Economic Development: A Critical Review”, International Journal of Political Economy 44(3):228-247.Taylor & Francis.

- Siddiqui, K. (2015d). “Challenges for Industrialisation in India: State versus Market Policies”, Research in World Economy 6(2):85-98.

- Siddiqui, K. (2015e). “Foreign Capital Investment into Developing Countries: Some Economic Policy Issues”, Research in World Economy 6(2):14-29.

- Siddiqui, K. (2014). “Contradictions in Development: Growth and Crisis in Indian Economy”, Economic and Regional Studies 7(3):82-98.

- Siddiqui, K. (2012a). “Developing Countries’ Experience with Neoliberalism and Globalisation”, Research in Applied Economics 4(4):12-37, December.

- Siddiqui, K. (2012b). “Malaysia’s Socio-Economic Transformation in Historical Perspective”, International Journal of Business and General Management, 1(2):1-50, November.

- Siddiqui, K. (2010). “The Political Economy of Development in Singapore”, Research in Applied Economics 2(2):1-31.

- Siddiqui, K. (2009a). “Japan’s Economic Crisis”, Research in Applied Economics 1(1):1-25.

- Siddiqui, K. (2009b). “The Political Economy of Growth in China and India”, Journal of Asian Public Policy 1(2):17-35, March. Routledge, Taylor & Francis.

- Siddiqui, K. (1996a). “Growth of Modern Industries under Colonial Regime: Industrial Development in British India between 1900 and 1946”, Pakistan Journal of History and Culture 17(1):11-59, January.

- Siddiqui, K. (1996b). “The Debt Crisis – Need for a New Strategy”, The News, May 17.

- Siddiqui, K. (1995). “Role of the State in South-East Asia”, The Nation, May 27.

- Storm, S. (2015). Debate on Structural Change, Development and Change 46(4):667-699.

- Wade, R. (1990). Governing the Market: Economic Theory and the Role of Government in East Asian Industrialisation, Princeton: Princeton University Press.

- World Bank. (2019). World Development Indicators, Washington DC: World Bank.