As Jon Cunliffe states in the opening quote, most people do not know this. They are unaware that when they pay for groceries, purchase a new phone, or renew a software subscription, they are using bank-created digital money. Importantly, it is the central bank that provides the foundation that enables us to rely on this system. To do so, authorities credibly promise to convert certain bank liabilities into the means of exchange—the safe, liquid instrument known as reserves—under as many states of the world as possible. Experience teaches us that this is something central banks committed to price stability can do under more states of the world than private actors. As Cunliffe puts it, we rely on this framework to “tether private money to the public money issued by the state.”

Where does the system fall short? We see two principal shortcomings. Some payments are expensive and slow, and too many people lack full access to the financial system. Advocates see CBDC as the solution to both problems. In our view, we do not need CBDC and its attendant risks either to improve efficiency or to expand access.

Nevertheless, central banks are plowing ahead. According to a BIS survey last year, a majority of central banks already are working on CBDC, spurred by motives that include monetary policy implementation (which may include the ability to set interest rates well below zero), payments safety and efficiency (both domestic and cross border), and financial inclusion.

We see two other important drivers. First, there is a desire to supplant cryptocurrencies like Bitcoin and head off the issuance of private monetary instruments like Libra (now Diem). But governments know from long experience how to handle such private currencies when they become salient—either impose punitive taxes or an outright ban. Indeed, the current financial system is one where only licensed intermediaries can issue liabilities that are convertible at par into the medium of exchange because they are backstopped by the central bank. Second, there is the fear of missing out: central bankers want to make sure that, if others issue CBDC, they can, too—and without delay. In our view, this creates instability: in theory, an unanticipated event could trigger many central banks to mobilize their digital currencies within a short period, so as not to be left behind.

This brings us to a few details about CBDC. Before issuing retail digital currency, a central bank will need to make a series of design decisions. Is it an anonymous bearer instrument, or will it be registered with a named owner? Will there be quantity restrictions on an individual’s holdings, or will it be supplied elastically? Are only residents of the issuing jurisdiction eligible to hold it, or can anyone? And, like paper currency, will it have a zero interest rate, or will it be interest bearing? (We ignore certain technical issues, such as whether it is account-based or token-based. See the BIS General Manager Agustín Carstens’ recent speech.)

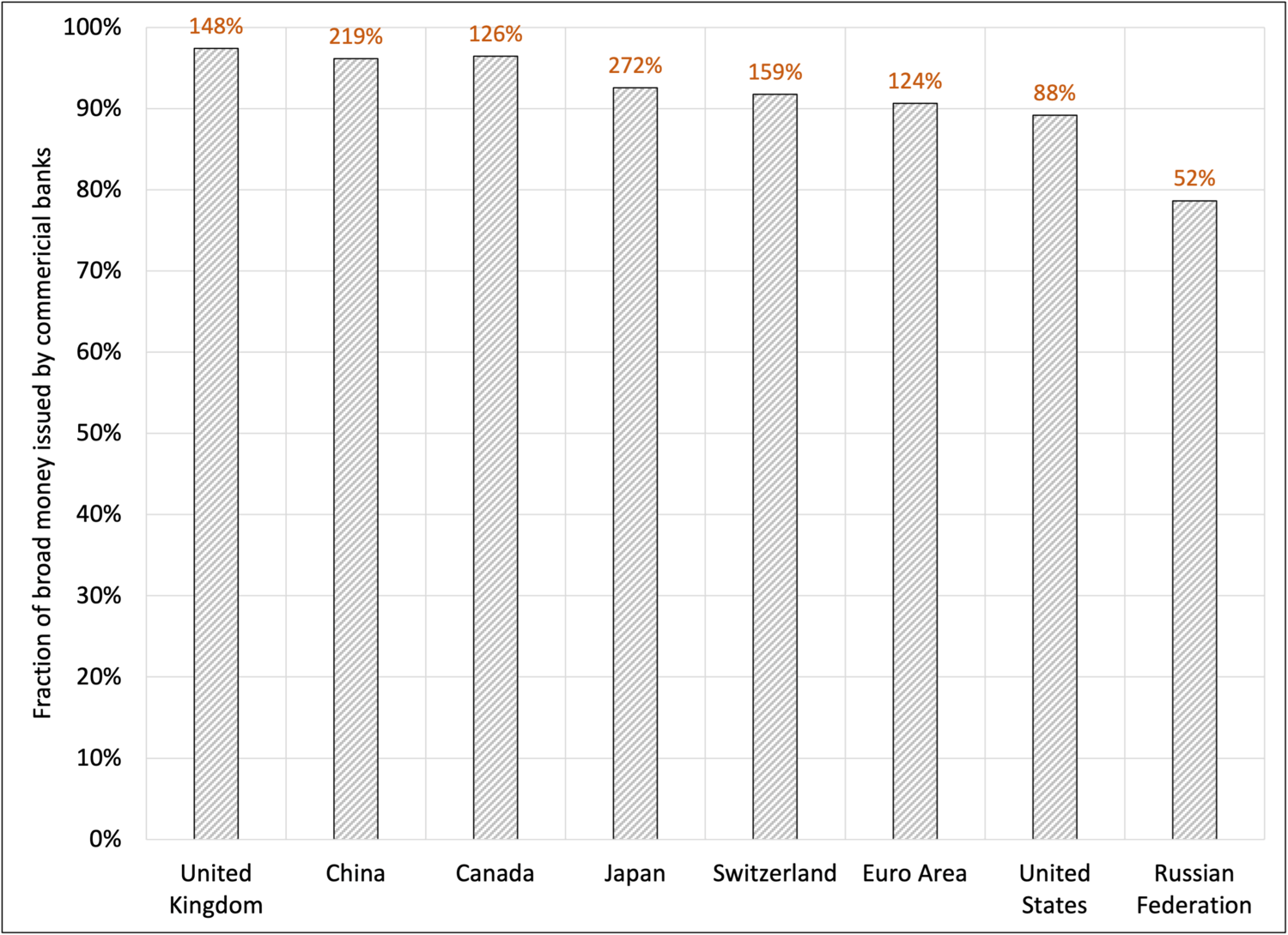

For paper currency, we all know the answers to these questions. It is an anonymous bearer instrument (facilitating illegal use: see here). It is supplied elastically to allow the conversion of certain bank liabilities at par into the medium of exchange without limit in as many circumstances as possible. Anyone can hold paper currency. And, it bears zero interest.

In an earlier post, we argue that the characteristics of CBDC are equally clear. To avoid facilitating criminal activity, CBDC cannot be anonymous. To truly substitute for paper currency, it will have to be supplied elastically. Individuals will be allowed to hold unlimited quantities: otherwise, there would be circumstances when bank liabilities will not be convertible into CBDC at par. Restricting holdings to residents is a version of capital controls, which are both impractical and unwise. Finally, we see two reasons that CBDC would have to bear interest. First, in our view, it is politically unsustainable for a central bank to pay interest on commercial bank reserve deposits but not on the deposits of individuals. Second, without it, policymakers who wish to lower nominal interest rates below the effective lower bound could not do so.

The issuance of such CBDC creates four critical problems: disintermediation, currency substitution, lack of privacy, and the inability to ensure compliance. On the first, while inertia (combined with interest rate increases and service improvements) might keep funds in the banking system for a while, financial strains eventually would prompt uninsured deposits to flee private banks for the central bank. And, for highly trusted central banks that operate in relatively stable political and financial jurisdictions, these inflows will come from abroad as well. Given the current high foreign demand for U.S. paper currency, imagine what would happen if the Fed offered universal, unlimited accounts? The consequences of this could be catastrophic for emerging market and developing economies.

The fact that CBDC is not anonymous leads to the final, related, challenges: privacy and compliance. On the first, everything we do becomes traceable. While we are neither libertarians nor advocates of free banking, in this case we agree with L.H. White: there are enormous risks in allowing governments to have this level of detailed information about our activities. As a result, it is difficult to see why democratic countries would allow such a concentration of power.

Turning to compliance, someone will have to do the work to ensure that the users of CBDC are law abiding. Such know-your-customer and anti-money laundering efforts are costly. We currently outsource these tasks to commercial banks. Banks also provide a host of other services. Who will do this, and who will bear the cost?

One way to manage the privacy and compliance challenges is through the creation of intermediated CBDC (see here). In this framework, brokers (or banks) provide individual account services, guarding privacy, monitoring compliance and aggregating balances into accounts at the central bank (which would presumably bear interest). However, this approach does not eliminate the risks of domestic disintermediation or currency substitution. Funds would still flow into the central bank, just indirectly through what are narrow banks in all but name. And, in the absence of subsidies, narrow-bank services would not be costless to users, limiting the hoped-for impact on access.

Against this background, it is easy to see why the People’s Bank of China is moving ahead of other central banks in creating a digital renminbi (currently as a pilot program for domestic use). China does not face any of the problems that we outline. Its large banks are typically state owned, so there is little risk of disintermediation—even in a financial crisis. With stringent capital controls in place, there currently are effective limits on inflows into the currency. There already is little expectation of personal privacy. Finally, if the government wishes, state-owned banks can easily subsidize access.

Could China’s CBDC become a problem elsewhere? Perhaps. The most obvious example would a be a meaningful expansion of RMB convertibility that makes the digital yuan more attractive to foreign users. Short of that, one could imagine China offering small countries access to their CBDC, backed by the PBOC’s massive foreign reserve holdings. Such a subsidized extension of the Belt and Road Initiative could have geopolitical ramifications.

Returning to the question at hand: Where is the current monetary system falling short? Our answer is that there is plenty of scope to improve the payments system and broaden financial access without turning to new digital currencies, either from central banks or private issuers.

We already see public and private sectors moving to provide cheaper, faster, more reliable, and more accessible systems that operate both within and across borders. The euro area has the TIPS system, with a processing time of 10 seconds at a cost of €0.002 per transaction. Over the next few years, the ECB will extend this to other currencies. The United Kingdom has Faster Payments, which can take up to 2 hours with a maximum value of £250,000. A group of commercial banks is working to create a pan-Nordic cross-currency real-time system called P27 that will instantly clear both domestic and cross-border payments. Canada is testing Real-Time Rail (RTR) to settle payments in less than a minute. In the United States, the Clearing House has a Real-Time Payments (RTP) system, and the central bank is set to launch its FedNow retail payments service in 2023. None of these requires CBDC.

As for financial access, this is a more complex problem to solve. That said, the case of India is instructive. As we describe in an earlier post, started in 2014, the Pradhan Mantri Jan Dhan Yojana (PMJDY) provides no-frills bank accounts without charge, using the country’s universal biometric personal identification to lower costs. To date, over 420 million people have been brought into the system, with account balances averaging nearly US $50. Again, India’s success did not require the issuance of CBDC.

Putting all of this together, we conclude that it is a bad idea for a central bank to issue elastically supplied, interest-bearing CBDC with universal access. Domestically, it risks disintermediation. And, unless it is a privately intermediated instrument, inflows of deposits directly into the central bank would make the temptation to steer credit directly very difficult to resist. Even if the central bank were to re-circulate the funds to potential lenders through an auction process, the need for an extensive collateral and haircut system would vastly expand officials’ influence on credit allocation. Internationally, there may be a tidal wave of funds fleeing places perceived as less stable and into those thought to be safe, adding to inequality and to the influence of the rich recipients. Finally, there is privacy. While this problem can be addressed (possibly through technical means), CBDC would surely tempt authoritarian governments by providing access to everything we do.

This all leads us to be very concerned. To be clear, we are strong proponents of innovations that reduce costs and improve welfare. But the most important innovations—those that improve the payments system and the supply of credit, do not require universal CBDC and its inherent risks. So, why are central banks so intent on preparing? What is the purpose of such contingency planning?

The problem, as we see it, is that central banks fear being left behind in a way that damages the interests of their jurisdiction. Their solution is to create a form of shovel-ready CBDC programs. But, the resulting framework is unstable. The situation is analogous to the pre-World War I mobilization problem: countries mobilize for fear that delay means losing a war. In the early 20th century, in the absence of trust, an obscure event in a far-off land helped tip this fragile balance into war. In the current financial circumstances, the bad equilibrium would be a world of multiple CBDCs in advanced economies that threaten financial stability domestically and pose a severe threat to monetary control in developing economies.

We see no easy steps to prevent this poor outcome. As in a classic prisoner’s dilemma, there is little way to enforce the cooperative equilibrium in which no one introduces CBDC. First, central banks cannot credibly commit to never issue CBDC. Second, with China already headed down the CBDC road, others now view it as too late to resist: even with full knowledge of the risks, they feel compelled to prepare.

Perhaps the best hope is that they all proceed very slowly and try to “get the design right.” In our view, that will mean stopping well short of universal, elastically supplied, interest bearing CBDC.

The article was first published on Money and Banking.