Learning Chinese can be tricky, but it doesn’t have to be. Rather than relying on old-school methods like flashcards and rote memorization, you might consider some alternative methods and strategies. Today, let’s explore how to learn Chinese in ways other than using flashcards.

Listen to Chinese Music

For starters, you can learn Chinese quite easily just by listening to Chinese music. If you want to know how to learn Chinese rapidly and efficiently, you need to immerse yourself in that language’s media. Music is one of the best ways to learn Chinese because:

The language content itself is accompanied by music, so you can anticipate certain words once you understand the music or listen to it on repeat

It’s a little more memorable because of the beat or rhythm the music presents

Plus, many of these songs have plenty of entertainment value in and of themselves. Therefore, try to listen to Chinese language music if you want to pick up extra vocabulary and sentence structure patterns without having to read flashcards.

Consume Chinese Media

Secondly, you can consume other forms of Chinese language media to learn Chinese rather rapidly. Books, movies, TV shows, and other entertainment media not only provide you with plenty of access to the Chinese language in its raw form. They also give you important cultural context that is key to speaking Chinese fluently.

You can consume Chinese language media on YouTube, Viki, or other streaming sites. Consuming Chinese language media is one of the best ways to immerse yourself in the language, which experts suggest is the best way to learn any language, not just Chinese.

How to Learn Chinese Learning Programs

For kids, you can alternatively use a Chinese learning program like LingoAce. LingoAce and other online programs offer flexible, personalized learning paths and engaging, high-quality one-on-one lessons for 3-15 year olds. The online lessons are all taught by certified teachers, so you can rest assured that you’ll get a quality education by signing up for one of these programs.

More importantly, many of the best Chinese learning programs allow you to tailor your educational content to your needs, learning preferences, etc. In this way, you don’t have to go through a lesson plan that doesn’t work for how your brain is wired or how you prefer to learn a new language! These are perfect tools if you don’t know how to learn Chinese quickly.

Listen to Chinese Audiobooks

As touched on above, listening to Chinese media in general is advantageous if you are trying to pick up the language quickly. Therefore, listening to Chinese audiobooks can be a great way to consciously and subconsciously absorb the language in a matter of weeks or months.

The best Chinese audiobooks are those you already know the stories to. That way, your brain can anticipate how the sentences should go and make connections between Chinese sentences and English sentences. Of course, Chinese audiobooks are also great for entertaining yourself on long car drives to and from work, while tackling chores, or while just enjoying some time outdoors with a pair of earbuds in.

Hire a Tutor

If you benefit from one-on-one instruction and even more personalized education, it may be beneficial to hire a private tutor. While this does cost some money, it could be arguably the most comprehensive way to learn Chinese without using flashcards or other rote memorization tactics.

Hiring a tutor gives you benefits like:

Direct access to an expert in the Chinese language

Personalized instruction tailored to your unique needs

Someone to correct you if you speak Chinese improperly so bad habits don’t set in

And more

Hiring a tutor is a great choice if you want to make sure your Chinese is perfect or that you never make any pronunciation problems so you can speak Chinese fluently for an upcoming business meeting.

Spend Some Time In a Chinese-Speaking Country

Lastly, consider taking a trip to spend some time in a country or region where Chinese is the primary language. Immersing yourself in the Chinese culture and language is a great way to jumpstart your brain’s understanding of this tongue. If you spend some time in China, you’ll learn much more quickly than if you try to use the materials in America or another primarily English-speaking language.

When you go, try to speak to as many people as possible and continue to absorb Chinese media to maximize your learning progress.

Conclusion

Ultimately, if you’re wondering how to learn Chinese without flashcards, you’re in luck. There are many different methods and tricks you can use to enhance your brain and grasp this complex and fulfilling language in no time at all. For the best results, try to use each of the six methods above – within a few months, you’ll be speaking Chinese fluently!

Numerous sectors have experienced significant transformations in the previous decades as a result of remarkable technological advancements. In addition, the epidemic has taught people how to accomplish tasks more quickly than previously. There is a broader range of payment options in the gambling sector due to the close relationship between businesses and technology.

In the future, newer techniques will be implemented to make payments and withdrawals easier, more convenient, and quicker.

Over the past few years, several nations have welcomed online casino companies and given them all the necessary legal authorizations. Because of this, online casinos require more payment methods in order for the sector to be accepted by and available to practically all societal groups.

What are some of these payment methods, and how do they affect the online gambling sector?

Credit and Debit Cards

Since the introduction of online casino games, credit and debit cards have been among the most popular payment options. This trend will continue into the future. Of course, there have long been controversies around the morality and safety of using credit cards to make deposits at online casinos. Even so, together with the debit card, it remains the leading payment method for online casinos.

One of the most significant advantages of using credit or debit cards is the degree of security you can experience on the go. Except in instances when the gambling site is not adequately secured with high-quality SSL encryption, it is practically impossible for anyone to hack through this payment.

With a card, you control the entire process, and all required codes are supplied to you for payment authentication. You are not obliged to give anyone your personal information, and the gambling platform cannot demand for it.

Visa and MasterCard are the most popular credit/debit card options at casinos. However, there are some other options, though—Discover and Maestro. Check out https://www.gamblingsites.org/gambling/credit-card/ to learn more about credit cards in online gambling.

You will also discover the best gambling sites to use if you prefer to pay through credit/debit cards. Many of these sites, also accept the following payment methods.

E-Wallets

E-wallets are starting to sound triter in the real money online gaming world. This tendency is not anticipated to change soon, given the ongoing advances among the most prominent systems globally. Due to their widespread use, digital wallet processes have a real potential of competing with credit and debit payment options.

At least one out of every three casino patrons is quite aware of how this payment mechanism works. The benefit of this option is that it works well for speedy withdrawals. You may be confident that the platform you choose to play on is one of the fast withdrawal casinos if it offers this choice.

This method of depositing money is just as secure as using debit or credit cards. You can discover many different variations of this payment method online. However, some of the most popular ones include:

PayPal

If you wish to deposit money into your online casino account, PayPal is the most popular e-wallet to use. Over 350 million people use this e-wallet globally, with a sizable portion using it as a payment gateway for their account at an online casino.

Skrill

This e-wallet resembles PayPal. Many users rely on it to make deposits in order to wager on real money online casino games. It’s easy to use this option, and there aren’t any complicated technicalities at all.

Neteller

The majority of online casinos give customers this choice so you may deposit money into your account quickly. You may completely trust this strategy while using the e-wallet form because it has virtually no limitations.

Cryptocurrency

A growing number of online gaming platforms are starting to embrace the digital revolution in banking. The ever-increasing use of cryptocurrencies as deposit options in online casinos is one instance where this shift is pronounced.

Because they were uncontrolled, there were many questions about whether virtual currencies were reliable enough at the beginning of crypto and blockchain in the online gambling market. Time has proven that popular virtual currencies such as Ethereum, Bitcoin, and Dogecoin are highly feasible, even though the worries may not be entirely allayed.

Virtual currencies are now widely accepted as a reliable payment mechanism on many online gambling sites. The advantage of this technique is that it deposits money into an online casino considerably more quickly than most alternatives.

You may be confident that you won’t get into any trouble if you possess a cryptocurrency wallet, and the gambling websites you frequently use to wager on online games allow virtual money as tokens.

Prepaid Cards

Despite the fact that most casino players may not be using this option, it is undeniably one of the best and highest-rated casino payment options available on most platforms. This payment mode is excellent especially if you want to avoid having your identity and personal details recorded by the online gaming site.

When acquired, you can use a prepaid card to transact at online casinos because it is pre-loaded with money. This option is entirely functional if you wish to place your bets anonymously.

Depending on your individual interests, there are several prepaid cards that are acceptable for everyone. You can opt for a virtual, reloadable, or disposable card. Because they have no responsibility and may be obtained from many retailers, these cards are regarded as secure and practical.

Bank Transfer

The well-known instant bank transfer services work just as well for online casino payments. If you prefer that the money be deducted from your account rather than transferred via bank transfers, you can conduct a wire transfer, which is an excellent alternative.

In general, banks have no problems dealing with online gambling platforms, and you can use your account information to transfer money to your preferred platform with ease. Almost all banks provide banking services to casinos. Therefore, if the site where you are wagering offers this option, you should use it since it is a safe payment method.

We have seen major developments in sports betting over the past 20 years. Having previously bet using land-based establishments, online betting was introduced in 1996 but it was not until a few years later that we saw the introduction of today’s major online sportsbooks.

Live betting is another fantastic sports betting innovation but one development that has caught the eye recently in the United States is peer to peer betting. Many in the US will be new to peer-to-peer betting and you can find out more on this guide where P2P betting is explained.

Peer to Peer Explained

If you have had a wager against a friend, you have already participated in peer-to-peer betting. For example, if you have bet on the outcome of a football game with a friend, with each of you choosing a team and one of you winning money on the outcome, you have made a peer-to-peer bet. In terms of online sports betting, peer to peer betting often takes place at what are known as betting exchanges. When betting at a betting exchange, there is no sportsbook involved. The bet is made between yourself and another person who wants to have a wager on the same event but is choosing a different outcome. Therefore, a sportsbook is not setting the odds. For a more depth guide and better understanding, you can read this article on P2P betting explained.

Prophet Exchange is an example of a peer-to-peer online sports betting company. The website is live in New Jersey, and it is the users who set the prices, with Prophet Exchange taking a commission on each bet. So, whereas traditional sportsbooks make their money by collecting losing bets, betting exchanges make their money from taking a small commission from each bet. It is like a small fee for hosting the bet and making the transaction. Wagr is another example of a peer-to-peer betting website to recently go live in the United States. Wagr charges a 5% transaction fee on each bet and the app is available on the Tennessee market.

How Does Peer to Peer Betting Work?

There are some terms you must know before you begin betting at an exchange. The most common types of bets at peer-to-peer betting websites are back bets and lay bets. A back bet is when you place a wager on a team to win. In other words, you are backing the team to succeed. On the other hand, a lay bet is when you bet against the team that the other peer has backed. So, if one person places a bet on Chicago Bears to win, that is the back bet. If you think the Chicago Bears are going to lose, you can place the lay bet. You cannot place a lay bet at a standard sportsbook. You can back the opposing team to win but you cannot bet on a team to lose, which is something you can do when peer to peer betting.

Liquidity plays a key role in peer-to-peer betting. Liquidity is the total amount of money currently on a specific market and you can never bet more than the liquidity. This is because a bet can only be matched if there is enough money to cover the opposing outcome. The current liquidity of a market is usually shown next to odds, and you can decide if it is enough for you to make the bet worthwhile.

Will Peer to Peer Betting Be Popular in the US?

Peer to peer betting is extremely popular in other countries, with the United Kingdom being a good example. One of the advantages of peer-to-peer betting is the odds are usually more generous than those found at traditional online sportsbooks. That may not always be the case but as the betting exchange is making a commission from each bet, it is not overly concerned about the value of the odds. The house edge is usually 0% when peer to peer betting but can be as much as 10% or more when betting at regular sportsbooks.

It will be extremely interesting to follow the development of peer to peer betting in the US to see if it becomes as popular as it is in other countries.

When it comes to moving families in style and comfort, there really is no better option than a luxurious sports utility vehicle. The name may seem a bit misleading since these are by no means the rough and tumble off-roaders that once bore the SUV tag. Nowadays, crossovers and SUVs form a huge part of the market share, and many have been designed specifically for urban lifestyles, bringing into question their sportiness and their utility.

Not many modern SUVs would dare venture off the asphalt, except for those that have been specifically designed to, like a Jeep Wrangler or Land Rover Range Rover. Instead, the segment is characterized by firm yet compliant suspensions, superior back seat and cargo capacity, and readily available all-wheel drive to deal with slippery or snow-covered roads. This is especially true of the premium models. Across the varying classifications within this popular subsegment, these are some of the more noteworthy options:

1. Mercedes-AMG GLE

One of the leading names in premium automobiles is Mercedes-Benz, and when you throw the letters AMG on top of it, you know you’re getting the absolute best the company has to offer. A turbocharged inline-six develops 429 horsepower and decent performance characteristics and a 5.2-second 0-60 mph sprint time. Handling is good, too, but this isn’t what Mercedes is really known for.

The real magic happens inside the cabin, where premium-grade materials and excellent construction result in a cabin that people love to spend time in. Comfort is guaranteed by the plethora of people-centric features like power-adjustable heated seats, multi-zone automatic climate control, and built-in power-operated sunroof. The infotainment system is pretty good, too, and while the base driver-assistance suite could be better, ticking a few options easily makes up for it.

The price tag is almost as appealing as the exterior styling considering the other top midsize luxury SUVs it competes against. However, the subpar fuel economy figures mean that the money you save won’t go very far.

2. Cadillac Lyriq

Still in the midsize category, the Lyric is a brand-new all-electric SUV that shows Caddilac still has what it takes to compete in the premium segment. Of course, it can be argued that the Escalade already proved this point, but the Lyriq does more with less. It isn’t an overly bold and chunky SUV, as sleeker lines fit its electric nature better. Since there aren’t all that many luxury EV SUV models on sale right now, competition is limited. That doesn’t mean the Caddy can’t stand out on its own virtues, though.

Available with one or two motors, it can produce up to 500 hp and deliver a surprisingly engaging driving experience. Its total driving range is pretty good, too, at 312 miles to a full charge. But ride comfort is where the real focus is. Silent running and solid construction, combined with a finely tuned suspension, help it eat up the miles quietly and confidently, while steering remains light and responsive.

In terms of technology, the Lyriq has all the essentials and even a few features that European brands save for the options list. Along with a spacious and, more importantly, practical cabin, this makes the inside of the SUV a very safe and pleasant place to spend time. Unlike the larger Escalade, though, the Lyriq can’t even pretend to be off-road capable, and cross-country trips will take a lot longer with frequent stops to recharge.

3. Lexus NX Hybrid

If you aren’t quite ready to make the change to an all-electric SUV, then a luxury hybrid SUV might be more your speed. There are quite a few options to choose from, but the NX stands out as one of the most balanced models. Not only is it more affordable than an Audi Q5 or Volvo XC60, but its Toyota heritage helps to make it a highly dependable and value-packed choice.

The gas engine is supplemented by an electric motor that can power the SUV for 37 miles while still improving performance ever so slightly. Unfortunately, the CVT holds it back from being a particularly fun drive, and the suspension could be better tuned to handle bumpier roads. Nevertheless, the Lexus still has a lot going for it beyond improved fuel economy.

The interior looks and feels good, though not quite as opulent as a Merc or BMW, and the standard list of features is very extensive. Toyota knows that buyers expect a lot more for their money than they might accept from the European brands, and it has made sure to pack the Lexus NX full of goodies to draw attention away from the flashier competition. The infotainment is a particular highlight, with loads of functionality and a user-friendly interface.

A good project manager always seeks to mitigate risk and protect their investment. One of the best ways to do this is by ensuring that your contractor has the proper insurance.

General liability insurance protects your contractor against claims of bodily injury or property damage arising from their work. If someone is injured on the job site or the contractor damages a client’s property, the insurance will cover the costs of medical treatment or repairs. Let’s take a closer look at why you should ensure your contractor has this insurance.

Accidents Happen

No matter how safety-conscious your contractor is, accidents can still occur. If someone is injured on the job, you could be liable if your contractor doesn’t have insurance. This is why ensuring your contractor has general liability insurance is crucial. Some common accidents include slips, trips, and falls; scaffolding collapses; electrical shocks, and more. If any of these accidents occur, and your contractor doesn’t have insurance, you could be on the hook for medical bills and other damages. This often brings confidence to the hiring party that risks are being taken care of and they do not have to worry about anything going wrong.

In addition to bodily injury, general liability insurance also covers property damage. If your contractor accidentally damages a client’s property, their insurance will cover the costs of repairs. This can help avoid any legal issues arising from the property damage. Without insurance, you would be responsible for paying for the repairs out of your pocket. This could quickly become expensive, and it’s not worth the risk.

Protection Against Lawsuits

In addition to accidents, your contractor could be sued for defamation, false advertising, and more. If your contractor doesn’t have insurance, you could be liable for any damages awarded in a lawsuit. This is why it’s vital to ensure your contractor is adequately insured.

General liability insurance will protect your contractor against a variety of different lawsuits. This type of insurance will pay for the costs of a lawyer and any damages awarded in a lawsuit. This can help to protect your contractor from financial ruin in the event of a lawsuit. However, before getting any insurance, speak with experts on the best insurance company to target.

Take your research online, whereby you will land on different sites with varying opinions. The most reputable and well-reviewed insurance companies should be your go-to. You can get quotes from different insurance companies, which will help you determine the best rate. The quotes should be based on the coverage you need and the type of work your contractor will be doing. Make sure you understand the policy’s terms and conditions before purchasing it.

Compliance with the State Law

In some states, it is required by law for contractors to have general liability insurance. If your contractor doesn’t have insurance, they could be subject to various penalties. These penalties can include fines, loss of license, and more. In some cases, the state may even require you to pay for any damages awarded in a lawsuit.

It’s essential to check with your state to see if they have any laws regarding contractor insurance. If they do, make sure your contractor complies. It’s not worth the risk of not being adequately insured.

Protection from All Third-Party Claims

When you hire a contractor, you enter into a contract with them. This contract protects you from third-party claims that may arise from their work. However, this contract does not protect you from claims directly against your contractor.

This is where general liability insurance comes in. This type of insurance will protect you from any claims against your contractor. It includes claims for bodily injury, property damage, and more. Without this insurance, you could be on the hook for damages yourself.

Advertising Claims

With the rise of false advertising claims, it’s more important than ever for your contractor to have general liability insurance. If someone claims that your contractor made false or misleading statements in their advertising, you could be held liable. This type of claim can be very costly and not worth the risk.

Ensure your contractor has general liability insurance to protect them from these claims. This type of insurance will pay for the costs of a lawyer and any damages awarded in a lawsuit. It can help to protect your contractor from financial ruin in the event of a false advertising claim.

Theft and Vandalism Claims

You could be held liable if your contractor’s tools or equipment are stolen or vandalized. This is because your contract with your contractor does not protect you from these claims. Without insurance, you would be responsible for paying for the replacement of the stolen or vandalized items.

The insurance will pay for the cost of the replacement items, as well as any other damages that are incurred. This type of insurance can help to protect you from a financial burden if your contractor’s tools or equipment are stolen or vandalized.

Builds Reputation and Establishes Trust

Hiring an insured contractor shows that you are willing to trust them with your property. This can help to build rapport and establish trust between you and the contractor. It can lead to a better working relationship and a higher quality of work.

It’s important to remember that not all contractors are insured. Make sure you ask about their insurance before you hire them. It helps ensure that you work with a reputable contractor in your best interests.

Protection Against Bankruptcy

If your contractor files for bankruptcy, you could be left without recourse. It is because the contract you have with them would be void. Without insurance, you would be unable to collect any damages awarded in a lawsuit.

At times, bankruptcy can be unavoidable. However, you can help to protect yourself by making sure your contractor has general liability insurance. This type of insurance will pay for the costs of a lawyer and any damages awarded in a lawsuit.

It’s essential to make sure your contractor is adequately insured. General liability insurance will protect your contractor against a variety of different lawsuits. This type of insurance can help to protect you from a financial burden if your contractor is sued. Make sure you ask about insurance before you hire a contractor. This will help ensure that you work with a reputable contractor with your best interests in mind.

When you think of Disney, the first thing that comes to mind is the cartoon characters we have seen on television screens over the years. However, the company has come a long way since Mickey Mouse and Disney is now a massive company, with the rights to some of the biggest franchises in the world, such as Star Wars. Could the adventure be about to continue for Disney and are they about to jump on the US iGaming bandwagon?

iGaming in the United States

It is worth noting that legal iGaming, which is online gambling, is still in its infancy in the United States. For example, it was not until May 2018 that the US Supreme Court ruled in favor of allowing sports betting. This put control into the hands of individual states and many have acted to make sports betting legal. Other forms have online gambling have also been legalized in the US, with Philadelphia being an example of state that saw gambling online legalized in 2017. This opened the market to gambling companies who were previously unable to offer their services in the state. So, if Disney are about to make strides into the iGaming market in the US, they are not trying to break into a long established institution. However, that does not mean competition is not stiff and we will investigate that in more detail shortly.

What to Expect from Disney

We must go back to 2019 to find the first link of iGaming and Disney. Disney purchased a large stake in a sports gambling company as they acquired Fox’s stake in DraftKings. This was not a one-off purchase by Disney because the move formed part of a wider deal between Disney and Fox but it signalled the start of Disney’s interest in the iGaming sector. In a statement regarding the acquisition of a stake in DraftKings, Disney CEO Bob Iger said he did not see The Walt Disney Company in the near term getting involved in the business of gambling or facilitating gambling in any way. However, fast forward to 2022 and Disney still hold a minority stake in DraftKings and there is a new Disney CEO in town who seems more open to the idea of Disney becoming involved in the iGaming industry. New CEO Bob Chapek said, “Sports betting [is] a significant opportunity for the company.”

One of the content groups of Disney is ESPN, a dedicated sports service. ESPN could be the perfect vehicle for Disney to test the water in the iGaming market and they can learn from the deal between Caesars Entertainment and DraftKings. There have been rumours that ESPN could move to acquire DraftKings as a major entry point into the iGaming market but it is far from a straightforward business.

Established Operators

There are several leading operators providing iGaming services in the United States. They are all competing for a slice of the pie and the more often new gambling companies enter the market, the more promotions are being offered to tempt players. Free bets are a good example of an iGaming promotion in the United States and is commonly used by sportsbooks. Free bets can be offered as part of a first deposit bonus or as a no deposit bonus, the latter of which is the most sought after for players. Casinos will also offer first deposit bonuses and free spins on the slots is a common bonus for new online casino members. Disney will enter an iGaming market where the competition is already tough and that is why it makes sense to try and acquire a current operator rather than build an iGaming presence from scratch. Many of the big names players in the iGaming industry had a presence prior to 2018 in the form of fantasy sports websites or land based casinos, especially in Las Vegas. They used these as a launch pad into iGaming and Disney may choose to do the same should they jump on the US iGaming bandwagon.

There is enough noise to suggest Disney are going to enter the United States iGaming market and it would not be a surprise if we have some concrete news before the end of 2022.

Hybrid work, remote work, digital nomads: many knowledge workers are experiencing a heap of new possibilities relating to how and where they work. Frontline workers, however, are often bound to fixed places and fixed times. In this talk with Mark Williams, Managing Director for EMEA at WorkJam, the leading digital frontline workplace, Williams discloses the way to a future of unseen flexibility for frontline workers and shares how companies can get help retaining valuable workers through WorkJam’s digital features.

During the covid-crisis, many of us have changed how we work and primarily where we work. In Europe alone, during the pandemic, 100 million workers have swapped the office with working from home – for some, working from wherever they want. To many, this newfound freedom contributes to a better work-life balance.

Those benefiting from this enormous shift in working culture are primarily knowledge workers. As Mark Williams points out, the conditions have largely remained the same for frontline workers, who still need to be in a certain place at a certain time. However, according to Williams, who, as WorkJam’s Managing Director for EMEA, specializes in the work life of frontline workers, this group of workers is looking for the same kind of choice and freedom: “Frontline workers want the same freedom. If they can work at a location in one city, why can’t they do it in another location where their employer operates??

Frontline workers make up 60 to 70, sometimes up to 80 percent of a country’s workforce, but as Williams puts it, this group has often been ‘the forgotten workers’. WorkJam has set out to change this through several features that make work more fun, make tasks more approachable, and allow for easy communication between frontline workers and the main office. When Mr. Williams is confident that we’re about to see a change towards more flexible work forms, it’s because WorkJam has developed the world’s leading digital frontline workplace, a technology that enables frontline workers to be scheduled in more than one location, operated by their employer. As frontline workers in many big retailers have the same work procedures in multiple stores, an app that connects stores with their staff enables frontline workers to take a shift when is more suitable for them.

And the new generation entering the job market enters it with new expectations: “You’ve got this next generation that is coming through, and they just want something different. They want a more connected workplace, they want a more dynamic, agile workplace. They want to work where and when they can,” Williams says.

Giving workers this added agency, Williams says, is a fantastic value proposition at a time where any extra sign of appreciation is essential for retention: “When you are struggling to identify and recruit and retain the right workforce, you know you need all of these additional value propositions,” he says.

More than a year inside ‘the Great Resignation,’ finding and retaining employees is a challenge for businesses, as workers seem to be a scarcer and more valuable resource than ever. Earlier this year, a survey conducted on LinkedIn disclosed that 58 percent of European workers are considering leaving their current job. In this context, dynamics between employer and employee have changed: “It’s no longer ‘if you don’t work for me, there are ten people that will take your job tomorrow.’ That’s completely flipped,” Williams says.

So there are good reasons for companies to pay close attention to the contentment and well-being of frontline workers. Mark Williams has made that the theme of his career long before the Great Resignation as he’s been part of leading and working close to frontline retail operations for the last 20 years, working at Diageo and Shell before starting in his current position at WorkJam.

His career in and around global retailers has been with the purpose of “trying to solve the complex dilemma of ensuring that frontline workers, the hourly paid workers, are engaged, embraced, feel part of the wider culture and the wider organization.” One way WorkJam does this is by helping companies create communication pathways that are intuitive to those who use them every day.

Communication in real-time between head office and frontline personnel has been essential for worker safety in several cases. It’s also been the case in Ukraine, where WorkJam has helped ensure that co-workers were either relocated to safe parts of Ukraine or evacuated and housed outside the country.

“Frontline workers are used to communicating on social media. They’re used to Facebook, WhatsApp, Twitter, TikTok, whatever it might be. Then you take them into the workplace and it’s almost forgotten. And then we start to talk to them via a back office PC or a handheld retail device that is completely alien to them compared to how they’re communicating in their private lives day in, day out with multiple people at the same time in multiple different ways. And all of these organisations across Europe need to realise that and then pivot and embrace this digital transformation.”

Giving frontline workers access to technology – with an interface that feels familiar – where they can communicate with other frontline workers and head office colleagues allows for several possibilities to ease work life. One of them is a gamified and fun way to enable colleagues to swap shifts. WorkJam’s platform also helps colleagues to get to know each other with the platform sharing bits of information about who their colleagues for their current shift are, including some fun facts about each colleague. This creates a friendly environment that “enables fun and also gets the work done,” as Williams says.

Besides features adding flexibility and fun between colleagues, WorkJam’s platform also allows for two-way communication between the frontline workforce and head office: “It’s not just from the head office and down, we now give the ability to communicate back up. We connect head offices to the frontline workforce in a way that they’ve never been connected or engaged with before.” This also gives senior staff and executives ways of communicating business identity to the people presenting it on the front line. As Mr. Williams says: “Straight away you can have senior executives speaking directly to the frontline worker around the brands, around the initiatives, about the strategy, around their values, and beliefs. And it just changes the whole frontline worker culture.”

Communication in real-time between head office and frontline personnel has been essential for worker safety in several cases. It’s been the case during the covid-crisis, where WorkJam’s platform allowed companies to communicate new policies and procedures or introduce new health and safety requirements. It’s also been the case in Ukraine, where WorkJam has helped ensure that co-workers were either relocated to safe parts of Ukraine or evacuated and housed outside the country.

Worth mentioning in the context of creating company-employee loyalty are the features directed towards employee learning and growth. Here, WorkJam’s tools also look at creating long-term value for employees when it comes to learning and development. Williams says: “Often the frontline worker wants to develop, wants to think about what promotion might look like, what job, what prospects there are, what other roles they may be interested in. And they tend to get forgotten. They don’t know how to tap into that knowledge, so they don’t know how to go about that at work.” Giving frontline workers the tools to develop and experience upward mobility within an organisation equals higher chances of retention.

Where Workjam’s tool gets really powerful, Williams says, is when all the functions are combined, allowing new forms of two-way communication, task management, professional development, and flexible planning. Surely we look forward to seeing how the future flexibility for frontline workers will play out!

Mark Williams is a Managing Director and is leading WorkJam‘s expansion in EMEA. Before joining the company, Mark held the position of Global Enablement Manager of Retail at Shell, where he was responsible for all frontline digital transformation projects. Operating with different structures across the globe, Shell’s challenge was to provide consistently excellent service through a fragmented workforce, without a large directly managed footprint. Under Mark’s leadership, the Enablement Team rolled out WorkJam to 100,000 employees across 35 global business units. Unifying communications, learning, and task management revolutionized how Shell Retail worked, improving turnover, compliance, and employee experience.

Our food production and distribution systems are fundamentally flawed, with consequences for both the planet and its inhabitants. Meiny Prins, CEO of Priva, argues for a hopeful future food system where people, planet, and business thrive. The Sustainable Urban Deltas concept reconnects food production with metropolitan areas and applies innovative technologies in order to procure a brighter future for the generations to come.

What makes Meiny Prins get up in the morning is the belief that she can play a part in creating a positive change in the world. And from someone working with food production and distribution, quite a lot of change is needed. As Prins highlights, the global set-up of food production and distribution has many flaws with serious consequences. That’s underlined by the fact that, globally, we produce enough food to provide for 10 billion people but still cannot manage to feed seven billion. In the USA alone, Prins says, 40 per cent of food is wasted, adding up to a situation where 130 billion meals and more than $408 billion in food are thrown away yearly.

Globally, a third of all food is wasted.

The Russian invasion of Ukraine has tragically emphasised the fragility of food supply chains. As the distribution of Ukraine’s wheat production has been halted, the big importers of Ukrainian wheat – Egypt, Tunisia, Morocco, and others – are suffering.

And distribution is predicted to get even more complex. By 2050 it is expected that 70 per cent of the world’s population will live in cities. As that population urbanises, the expansion of cities means that green belts and agriculture are pushed further away from people and markets. Supply chains are getting longer and more complex; sometimes, in search of the cheapest way to produce, they can stretch halfway around the world, with dire consequences for the climate.

So how can we work around the multifaceted problems in the global food market? Prins seems inspired by a famous Buckminster Fuller quote: “You never change things by fighting the existing reality. To change something, build a new model that makes the existing model obsolete.” Prins says that, rather than fight the power and money that lies in the existing global food system, she knows it is “a far more productive use of resources to build an alternative system, and that is what we are doing”.

Meiny Prins’s alternative food system is Sustainable Urban Delta, which she calls a “response to a wasteful system”. Sustainable Urban Deltas are about localising production by finding innovative ways to grow food closer to people. And, as Prins explains, this form of production has a range of advantages, such as inner city employment, fresher food, reduced greenhouse gases, optimal use of water, eliminating pesticides, provide educational and recreational facilities and, of course, sustainability and security for the city’s food supply.

Prins says that a variety of food production facilities can be a part of creating a sustainable Urban Delta: indoor farms, rooftops farm or open fields, but also less demanding set-ups, such as table-top farming, greenhouses, or a backyard vegetable garden. Prins is the CEO of Priva, a company that innovates in various areas related to those ways of producing, from heating glasshouses to automating urban agriculture environments to building automation and energy savings.

In Prins’s view, every technology related to farming practices is optimisable. This perspective has taken Priva far in innovating for a radically different future: “Our predictive technology has the plants themselves communicating directly with our software, guiding the software, and not the other way around. Every plant has a biorhythm, waking up early in the morning, starting to evaporate, and starting to grow leaves or fruits. The software used to be designed to control the environment. Now you have a plant that is designing all these things, to indicate what they need for maximal health and growth at any particular time. Everything can be monitored remotely, too, and controlled from a smartphone.” Another innovative contribution is a robot designed to pick tomatoes, which is a strenuous task for humans, so that its automation can give more space for creativity and fun tasks.

Prins got the idea for the Sustainable Urban Delta from flying over the Netherlands, of which she’s a native: “The vision for Sustainable Urban Delta came from comparing the grey views of endless concrete I saw when flying over most cities to the green mosaic that is the Netherlands, with arguably one large city on its west coast. I realised that my home country is a living, breathing, functioning, and successful example of a food-producing city.”

That the Netherlands has been able to fit in urban farming is quite impressive when looking at the country’s density. As Prins tells us, in the Netherlands, the population density is above 500 people per square kilometre – nearly five times more than the EU average. In the west of the country, it’s double that. Still, there’s a mixture of urban development and farming. Food

is often produced inside the city boundaries or close by in the less populated east of the country. Despite the high density, the Netherlands even sells food to neighbouring countries, exporting around €100 billion and importing just €20 billion.

According to Prins, Sustainable Urban Deltas can be reproduced in cities globally. The most critical resource is engaged locals, urban planners, and entrepreneurs. Prins says: “If we want to successfully bring food production back to the city, creating awareness at the municipality level is crucial. City planners need to provide both the space and infrastructure needed. In addition, they need to make local people enthusiastic about building businesses related to food. Bringing local food production back to the city has the power to transform whole neighbourhoods and communities. For example, when someone builds an indoor farm in a disadvantaged neighbourhood, it will start as a place that provides fresh food to the city, but it will grow and become a place that provides jobs.”

As that happens, entrepreneurs participate in sustainable development while they start to produce the products that farms need. As Prins sees it, cities and urban planners can create space for entrepreneurs to build new ecosystems around food production. That includes nice amenities like restaurants and market halls, but also digital innovation.

As local circuits of food and innovation, reducing carbon footprints, and increasing health and quality of life, in times of volatility the Sustainable Urban Delta shows that we can move forward without compromising on profit, people, or planet.

Not so long ago, Brazil’s BRIC economy soared as working people and the poor were able to join the labor force and formal economy. In just years, a “soft coup” and far-right president derailed Lula’s miracle. What next?

As I am writing this column, Brazil is preparing for its general election on October 2, after the disastrous term of Jair Bolsonaro, the incumbent far-right president and ex- captain, who placed army officers in key cabinet positions.

Elected in exceptional circumstances, Bolsonaro caused exceptional damage in Brazil’s economy and politics, society and military, and ecology.

With more than 156 million registered voters, Brazil is the second largest democracy in the Americas and one of the largest in the world.

But democracy is no assurance that the election outcome will be democratic.

Bolsonaro’s disastrous term

Rolling back protections for indigenous groups and facilitating deforestation, Bolsonaro compounded devastation associated with accelerated climate change.

Under his government, the COVID-19 pandemic effects were downplayed, quarantine measures opposed, and health ministers dismissed. So, the pandemic has killed almost 700,000 Brazilians; more than in India, despite its seven times bigger population.

Seeking re-election, Bolsonaro is facing former president Luiz Inácio Lula da Silva, a veteran trade unionist, who was elected in 2002, reelected in 2006, and left the office as the most popular president in Brazil’s history. In the past six years, he has overcome not just a throat cancer, but the far-right effort to keep him in prison.

Before the election, Bolsonaro, who has never hidden his yearning for a new military junta, made multiple allegations of election fraud. Observers have been quick to condemn such claims as invalid. But widespread concern prevails that false allegations could be exploited to challenge the election outcome, to execute a coup, or both.

After their bitter experience with military dictatorship (1964-85), the last thing Brazilians want is a junta of generals. Their prime concern is the economy and jobs. And that’s why they want Lula back.

Lula’s Boom, Rousseff’s plunge, oligarchs’ coup

In the early 1990s, Brazil still had a reputation as the world’s champion in “unfulfilled agreements with the IMF.” In 2003 Lula inherited a poor, resigned nation on the verge of an economic implosion. Winning the presidency heading the left-wing Workers’ Party (PT), his primary objective was to stabilize the economy and to lay foundation for the struggle against poverty.

Lula’s economic policies were born under favorable stars. In 2001, China joined the World Trade Organization (WTO). A year later, Lula initiated Brazil’s economic reforms. To modernize, Brazil needed demand for its commodities; to industrialize, China needed commodities.

In the 2010s, Lula refocused policy momentum to the expanding middle class. Now the goal became to provide new opportunities for the upwardly mobile, while ensuring income transfers to the poorest.

During those boom days, Brazil overtook Italy as the world’s seventh-largest economy, while living standards soared by almost 60 percent. In Brazil, these were the days of wine and roses, or caipirinha and orchids.

Brazil led Latin America. China spearheaded Asia. Both shunned President Bush’s unipolar foreign policy; each supported a multipolar view of the world.

Washington had a different take of such developments.

15 lost years

When Dilma Rousseff, Lula’s chief of staff, won presidency in 2012, she hoped to build on Lula’s success. In this quest, she failed, due to the lack of time and wrong priorities, tax policies and spending.

Worse, international environment worked against her. World trade plunged, commodity prices collapsed, China’s growth decelerated and the Fed initiated rate hikes. “Hot money” began to flee leaving behind asset shrinkages, deflation and depreciation.

In Brazil, a narrow economic elite reigns over an unequal economy polarized by class and race. It had always opposed Lula and PT, and it was supported by external forces. According to Wikileaks, the U.S. National Security Agency (NSA) tapped some 30 Brazilian government leaders’ phones (Rousseff, ministers, central bank chief, etc), and corporate giants, including Petrobras, the huge petroleum conglomerate that would play a central role in corruption allegations.

Sparked particularly by such allegations, protests erupted and were fostered by conservative and family-owned media oligopolies. That boosted the center-right opposition of juridical authorities and military leaders, conservative social democrats, Democrats, and PT’s more liberal allies.

In the subsequent “soft coup,” Rousseff was impeached by the Congress in 2016. The economic effects were disastrous. During Lula’s two terms, Brazil enjoyed a historical boom. Though sluggish rather than stagnant, Rousseff’s period was undermined by the coup. Bolsonaro’s economic mismanagement proved disastrous.

Following the coup and Bolsonaro, Brazil’s GDP is now where it was around 2007 or so. 15 years have been lost (Figure).

Source: TradingEconomics; World Bank; Difference Group

Biased judges and political ambitions

In 2015 Sérgio Moro gained national attention as one of the lead judges in Operation Car Wash, a criminal investigation into high-profile corruption and bribery scandal involving government officials and business executives. It fueled Rousseff’s impeachment and Lula’s 580-day imprisonment.

Moro, a Harvard-trained judge, had participated in the U.S. State Department’s International Visitor Leadership Program (IVLP). Meanwhile, Brazil’s federal police began broader cooperation with the FBI and CIA.

Moro portrayed himself as untouchable judge with no political ambitions. Yet, afterwards he eagerly joined Bolsonaro’s government as Minister of Justice and Public Security (2019-20), and subsequently the presidential race only to withdraw after his ratings fell.

There was a reason for Moro’s plunge. His “investigations” were prejudicial. Leaked messages exchanged between Moro and prosecutors have led to widespread questioning of his impartiality during the Operation Car Wash hearings.

In June 2021, all cases Moro had brought against Lula were annulled. White House officials admitted that the CIA and other parts of the US intelligence apparatus had been involved in assisting the “War on Corruption,” which jailed Lula and elected Jair Bolsonaro. Even the UN Committee found Moro biased in all cases against Lula.

Toward Lula’s comeback, unless…

In Brazil’s first round of elections, the candidate who receives more than 50% of the total valid votes is elected. If the 50% threshold is not met, the two candidates who receive the most votes participate in a second round of voting on October 30.

All current polls suggest that Lula will win the first round. The projections indicate he could get 45%-48% of the vote, against Bolsonaro’s 30%-36%. Moreover, all current second-round polls suggest Lula’s win by 10% or more.

Then again…

While Washington has urged Brazil to conduct fair elections, Bolsonaro, after his June meeting with President Biden, issued a coded command to the military in which the word “auditable” focused attention on the electronic voting system.

Brazil’s military has a “parallel vote count,” which some consider a risk to democracy. Furthermore, CySource, a controversial Israeli company hired by Brazil’s military, will presumably “supervise” the election against “disinformation.” Meanwhile, Brazilian observers have charged both YouTube and Facebook for pushing pro-Bolsonaro content and supporting coup mongering.

If democratic rules prevail, Lula is likely to make a comeback on October 2, or October 30. If not, current turmoil is just a pale prelude of what’s ahead.

No election is viable without the “consent of the governed” – not even a democracy.

Dan Steinbock is the founder of Difference Group and has served as research director of international business at the India China and America Institute (US) and a visiting fellow at the Shanghai Institutes for International Studies (China) and the EU Centre (Singapore). For more, see http://www.differencegroup.net

This article is the second part of a two-part series. You may read the first part here.

Damages And Causation

In the US, financial economists have assessed damages and causation issues in the context of securities litigation through the use of event studies and other analytical techniques described above. Although uncertainties remain, similar economic considerations and approaches may also be relevant in shareholder actions in the UK.

As the UK litigation landscape continues to unfold, questions regarding damages persist. For example, the initial question of which investors may claim damages under FSMA has not yet been resolved. FSMA Section 90A specifically refers to “any ‘person who has suffered loss’ as a result of the untrue or misleading statement, omission, or delay” and states that “[i]ssuers may be liable to buyers, sellers or holders of securities. . . .”1 Arguably, holders (who, by definition, did not transact in response to any allegedly “untrue or misleading statement, omission, or delay”) would be differently situated than investors who did transact (i.e., purchasers or sellers).

Further, regardless of which investors may claim damages, the methodology (or methodologies) to calculate damages under Sections 90 or 90A of FSMA also remains to be resolved. As the authors of Class Actions in England and Wales note, “FSMA does not specify the basis on which damages arising under [Sections] 90 or 90A will be calculated, and the question has not received any significant judicial treatment to date. This is a complex and difficult area.”2

This section outlines certain economic considerations that may be relevant to assessing damages to purchasers (or sellers) and holders in the UK.

Investors Who Traded: Inflation-Based Damages

A typical claim brought under Section 90A might assert that a company’s public disclosures misstated or omitted (or collectively, misrepresented) certain information during a specified period of time (a “relevant period”). Claimants may assert that the company’s share price was distorted or “inflated” by the alleged misrepresentations, i.e., the share price was higher during the relevant period than it would have been absent the alleged misrepresentations. Claimants would likely also identify one or more “corrective disclosures” that purportedly revealed the previously concealed truth, thereby removing the inflation from the share price by the end of the relevant period.

While the appropriate measure of damages in a particular case is ultimately a legal question, under the theory that the alleged misrepresentations led to an inflated share price, investors who purchased shares during the relevant period would have arguably paid more for the shares than they would have absent the alleged misrepresentations.3

In the Tesco shareholder litigation,4 claimants sought damages that were equal to the highest of four different measures.5 Two of these damages measures compare the price paid for the shares to a subsequent price (the price at which the shares were eventually sold or the price on the date on which the truth was purportedly revealed). These two damages measures fail to account for the fact that the share price over these periods may have changed for reasons unrelated to the allegations. The other two damages measures identified by claimants instead compare the price paid for the shares to an alternative hypothetical price absent the alleged misrepresentations—(1) the “true value [of the shares] at the date of purchase” or (2) “the price that would have been paid [for the shares] if the true facts had been known, or Tesco’s untrue and misleading statements and omissions had not been made.”6

Both of these alternative hypothetical damages measures seem to point to an inflation-based approach similar to the “out of pocket” inflation-based approach (inflation at the time of purchase less inflation at the time of sale) that is used to estimate damages in the context of US securities litigation brought under Section 10(b).7 It is important to note that, if the share price was inflated by the alleged misrepresentations, then any sales during the relevant period would also occur at inflated prices. From an economic perspective, the measure of harm to the investor would need to therefore adjust for (deduct) any “gains” from selling at inflated prices.

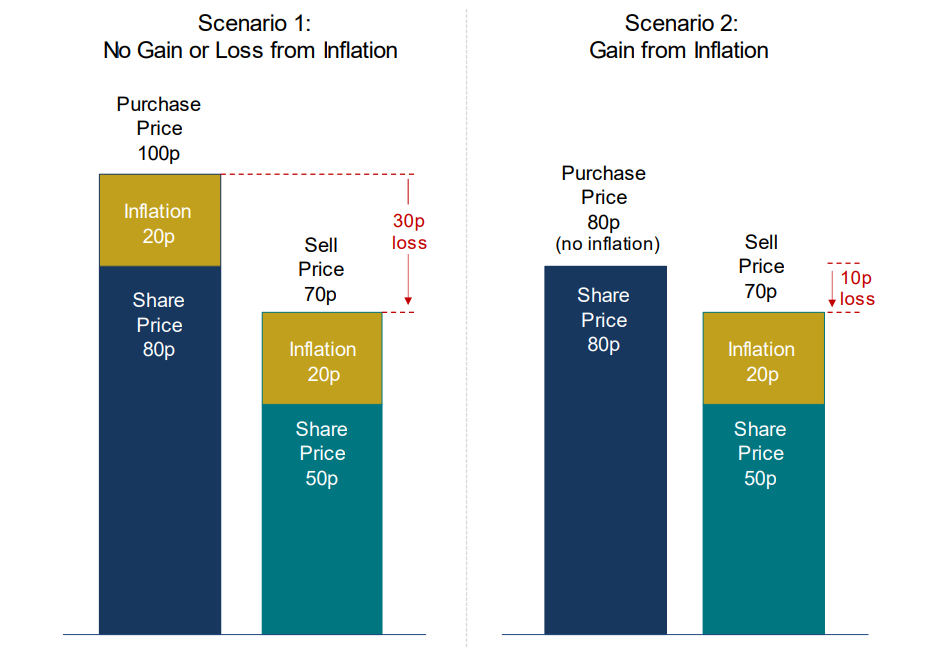

Consider, for example, an investor who purchases a share at a price of 100p at a time when inflation was 20p, i.e., the hypothetical share price absent the alleged misrepresentations was 80p. The investor subsequently sells this share at a price of 70p when inflation is still 20p, i.e., the hypothetical share price absent the alleged misrepresentations was 50p.

Although this investor “paid” inflation of 20p at the time of purchase, all of that inflation was recovered when the share was sold, and, as such, from the perspective of a financial economist, the investor was not harmed by the alleged misrepresentations. In other words, although the investor lost 30p per share on the transaction, the same 30p loss would have occurred even if there had been no alleged misrepresentation. Given that the investor incurred the same “nominal loss” (the difference between the purchase and sales prices) of 30p in the actual world as they would have absent the alleged misrepresentations, the investor’s out of pocket damages are zero.

If the same investor had purchased a share at 80p prior to any alleged misrepresentations (i.e., before there was any inflation in the price), and sold the share at 70p when inflation was 20p, then, from an economic perspective, the investor would have benefited from the inflation. Although the investor suffered a nominal loss on this transaction (selling at 10p lower than the purchase price), the investor nonetheless benefited from the inflation—the hypothetical share price absent the alleged misrepresentations would have been 50p, and the investor’s nominal loss would have been a larger 30p per share.

Potential Issues with a Simplistic Approach to Estimating Inflation

Potential Issues with a Simplistic Approach to Estimating Inflation

In US securities litigation brought under Section 10(b), plaintiffs’ experts frequently attempt to utilise an event study analysis to estimate the inflation removed from the share price at the time of the alleged corrective disclosure(s). They then assert that the share price was inflated by that same amount earlier (and throughout) the relevant period, i.e., they “back-cast” the inflation that they claim was removed from the share price by the alleged corrective disclosure(s) to earlier points in time. However, there are several critical conceptual issues with such an approach that could render the resulting estimate of inflation-based damages unreliable as a measure of harm.

To illustrate some of these issues, consider an extension to the stylised example of ABC discussed earlier:8

At the beginning of 2021, market participants expect the company’s revenues for the coming year to be £10 million. In an efficient market, ABC’s share price reflects, inter alia, market participants’ expectations of £10 million in 2021 revenues.

On April 1, 2021, ABC learns that an important customer has terminated its contract, leading to a reduction in ABC’s revenues for 2021. If the company were to remain silent about the contract termination or reaffirm publicly that 2021 revenues are expected to be £10 million (in line with market expectations), no new information is conveyed to the market that would change market participants’ expectations regarding ABC’s future cash flows.

Then, as previously discussed, on February 1, 2022, ABC announced disappointing 2021 revenues of £9 million, attributing the shortfall to the contract termination and slower sales caused by now-resolved supply chain issues, and ABC experienced a company-specific price decline of 12.4% (or £5).

Typically, a plaintiff’s expert might argue that £5 is the amount of inflation that was removed by the alleged corrective disclosure and that this amount has been in the share price since April 1, 2021, when ABC learnt of (but did not disclose) the contract termination. However, there are several problems with this argument.

First, although the misstatement or omission on April 1, 2021, may have introduced inflation into ABC’s share price, an event study cannot be used to reliably measure its magnitude at that time. To the extent that market participants would have revised downwards their expectations for the company’s future cash flows earlier had the contract termination been disclosed earlier, then a misstatement (reaffirming expected 2021 revenues) or omission (remaining silent) regarding the contract termination artificially maintains ABC’s share price at a higher level than it otherwise would have been. Accordingly, although there is no price response observed at the time of the alleged misstatement or omission (no observable “front-end” price impact), the company’s share price is nonetheless inflated. However, given that there is no observable price movement on the date of the alleged misstatement or omission, an event study analysis cannot be used to measure that inflation.

Second, even in this stylised example, event study analysis alone cannot isolate the inflation removed from the share price at the time the truth was revealed (i.e., on the “back end”). When ABC eventually disclosed lower 2021 revenues (attributable in part to the termination of the customer contract), the price decline that followed reflected the release of other information as well (e.g., the supply chain issues and the plant fire). In other words, although the corrective disclosure removed inflation from the share price, the event study analysis alone can only measure the price decline associated with the total mix of information disclosed, which does not provide a reliable measure of the inflation that was removed from the share price.

Third, even if it were feasible to reliably isolate the inflation removed from the share price following the corrective disclosure (i.e., the portion of the price decline due only to the termination of the customer contract), it is not reasonable to simply assume that the inflation would remain the same throughout the relevant period. For example, if the anticipated revenues from the customer that ultimately terminated the contract changed over time, then the amount of inflation from failing to disclose the contract termination would also vary accordingly.

While a back-casting approach asserting that inflation throughout the relevant period is £5 may be relatively easy to understand and compute mechanically, in order for the approach to provide a reliable estimate of inflation throughout the relevant period, one must establish that a number of underlying assumptions hold. For example, the corrective information disclosed is assumed to be the same as (or economically equivalent to) what allegedly could and should have been disclosed on the first day of the relevant period and everyday thereafter, i.e., the nature and severity of the misrepresentations do not change over time. In the hypothetical example, back-casting requires that ABC knew and was able to disclose the amount of revenues lost due to the contract termination as early as April 1, 2021. Further, under the back-casting approach, it must be assumed that the corrective information disclosed would have had the same effect on the share price had it been disclosed earlier. In other words, back-casting assumes that the price effect of the information is the same over time, regardless of any changes to the total mix of information in the market. Again, market and industry conditions as well as the total mix of information about ABC could change substantially over time.

More generally, if any of the assumptions implicit in the back-casting approach does not hold, then the back-casting approach does not provide a reliable estimate of inflation during the relevant period.

In summary, while the issue of quantum of damages in shareholder actions is ultimately a legal one, and while plaintiffs in Section 10(b) securities litigation in the US often use back-casting to estimate out of pocket inflation-based damages, it is important to consider and address the potential challenges to reliably measuring the quantum of damages under such an approach.

Investors Who Did Not Sell: Holder Claims

The inflation-based damages approach discussed earlier focuses on the difference between the actual share price and the “but for” or hypothetical share price had there been no alleged misstatements or omissions. Under the inflation-based approach, investors’ purchases and sales of shares absent the alleged misrepresentations are assumed to be the same as they were in the actual world, albeit at different prices. Consequently, the inflation-based approach will assess damages only to shares that were acquired during the relevant period (when the share price was purportedly inflated by the alleged misrepresentations).9 Accordingly, an investor who purchased shares before the beginning of the relevant period (when there was no inflation in the share price) will not incur damages under an inflation-based approach.10

However, Section 90A refers to “any ‘person who has suffered loss’ as a result of the untrue or misleading statement, omission, or delay” and states that “[i]ssuers may be liable to buyers, sellers or holders of securities. . . .”11 Although the statute does not specify as much, if holders are investors who already held shares at the beginning of the relevant period and who would claim they continued to hold the shares because of the alleged misrepresentations,12 from an economic perspective, this raises a number of interesting issues with respect to damages. For example:

Investors who already held shares at the beginning of the relevant period necessarily acquired these shares at a “fair” price, as the shares were acquired prior to any price distortion from the alleged misrepresentations. And, if the shares were acquired at a “fair” price, holders did not “suffer loss” due to the alleged misrepresentations at the time the shares were acquired.

Until the alleged misrepresentations were eventually corrected, and the share price declined as a result, could the holders “suffer loss as a result of” the alleged misrepresentations from continuing to hold the shares? If holders did not hold the shares through at least one corrective disclosure, could they “suffer loss” due to the alleged misrepresentations?

Any claim that investors continued to hold shares because of the alleged misrepresentations implies that holders would instead have sold their shares absent these alleged misrepresentations. This arguably implies that alleged misrepresentations would have had to be corrected (i.e., there would have to be some earlier corrective disclosure) in order for the holders to have sold their shares. However, had there been an earlier corrective disclosure, the share price would arguably have declined in response, in which case the holders arguably would have incurred at least that price decline before choosing to sell their shares. Should any economic analysis of damages therefore exclude that hypothetical price decline?

Setting aside these conceptual considerations, the specific damages approach claimants may assert regarding Section 90A “holder claims” remains to be seen. It also remains to be seen whether and how the proposed approach tethers the quantum of damages to the alleged misrepresentations, which could be important if the company’s share price has declined significantly over the relevant period, particularly for reasons other than the alleged misrepresentations.

Reliance

In addition to the economic issues that arise in shareholder actions regarding causation and damages, financial economics may also be relevant in assessing other aspects of litigation, such as reliance. While the legal landscape is evolving with respect to shareholder actions in the UK and Europe and it remains to be seen how courts will address issues of reliance, the economic concepts discussed earlier in this article can also provide insights on the subject.

Section 90A of FSMA expressly requires “reliance” on the alleged misrepresentations,13 but it remains to be seen how courts in UK shareholder actions will adjudicate this legal question.14 To the extent that UK courts require claimants to establish reliance, financial economists could play a meaningful role in assessing the issue. Courts in the US have allowed plaintiffs an indirect presumption of reliance based on a “fraud on the market” theory,15 and the same approach has also gained recent traction in Australian courts.16

The fraud on the market theory is predicated on the notion that, in an efficient market, a share price reflects all publicly available information, including the alleged misrepresentations (as long as they were public). Accordingly, if the market is efficient, an investor who purchased shares at the market price is presumed to have relied (indirectly) on the alleged misrepresentations. If claimants are not able to establish market efficiency, they arguably would not be able to invoke this indirect presumption of reliance. It is worth noting that, in the context of Section 10(b) securities litigation in the US, even if the market were deemed efficient, courts have offered defendants an opportunity to rebut the indirect presumption of reliance if they can establish that the alleged misrepresentations did not have an impact on the share price.17

To date, there is no definitive case law in the UK on the issue of reliance or fraud on the market in shareholder actions.18 Commentators have observed that a broader presumption of reliance (beyond expressly having read and relied on the at-issue statements) may be appropriate, but this “remains a highly controversial and untested question.”19 To the extent that an assessment of market efficiency or price impact is warranted in addressing the legal issue of reliance in UK shareholder actions, the analysis will likely involve financial economics techniques and tools discussed earlier in this article.

Conclusion

Economic analysis will be informative in the context of shareholder actions under Sections 90 and 90A of FSMA, to the extent that such actions materialise in the future. While the litigation landscape in the UK is still evolving, experience in securities litigation in the US suggests that various approaches in the field of financial economics (such as event study analysis, fundamental analysis, etc.) may be applied in assessing causation and damages issues in shareholder actions. It is important to recognise the limitations of these approaches to draw reliable inferences and conclusions in shareholder litigation.

The discussion in this section focuses on “inflation” and “purchasers,” but the same economic intuition would apply to “sellers” if the share price were “deflated” due to the alleged misrepresentations, i.e., if the share price were artificially lower than it would have been absent the alleged misrepresentations.

Manning & Napier Fund Inc v Tesco Plc (Claim no 2016-003088).

See Class Actions in England and Wales, p. 437.

Class Actions in England and Wales, p. 437

The out of pocket approach is used to measure damages in US securities litigation under Section 10(b) of the Securities Exchange Act of 1934 and SEC Rule 10b-5 promulgated thereunder.

The stylised example reflects a single alleged corrective disclosure. In practice, there may be multiple alleged corrective disclosures at issue, in which case the back-casting approach often proffered by plaintiffs in US securities litigation under Section 10(b) instead calculates inflation on any day in the relevant period as the aggregate amount of inflation that is purportedly removed by all alleged corrective disclosures that occur subsequent to the day in question. The Role of Economic Analysis in UK Shareholder Actions | Page 10 www.cornerstone.com

The inflation-based approach would assess damages for these shares if they were sold subsequently during the relevant period, but when the amount of inflation in the share price was lower; or if they were retained until after the last corrective disclosure (when there was no inflation left in the share price).

As noted earlier, if these shares were sold before the end of the relevant period, they would be sold at an inflated price, i.e., the investor would benefit on this transaction from the alleged misrepresentations. To measure loss resulting from alleged misrepresentations from an economic perspective (although what is recoverable is ultimately a legal question), any such inflation-based gains for a particular investor should be netted against inflation-related losses suffered by the same investor on shares purchased during the relevant period.

Class Actions in England and Wales, p. 405 (emphasis added).

For example, in the Particulars of Claim in the G4S litigation, the claimants allege that they “suffered loss and damage by acquiring or continuing to hold G4S Shares . . .” (Particulars of Claim, filed 15 June 2020, p. 1).

“A loss is not regarded as suffered as a result of the statement or omission unless the person suffering it acquired, continued to hold or disposed of the relevant securities—(a) in reliance on the information in question, and (b) at a time when, and in circumstances in which, it was reasonable for him to rely on it.” FSMA Schedule 10A, ¶ 3(4).

As a 2019 article observed, “[I]mportantly for tracker funds and retail investor claims, it remains to be seen whether [Section] 90A requires an investor actually to have read and relied upon the published information.” Peter de Verneuil Smith QC et al., “Claims under [Section] 90A of FSMA for Dishonest Statements Made to the Market: An Underutilised Remedy?,” Butterworths Journal of International Banking and Financial Law, March 2019, pp. 154–158 at 154, https://www.3vb.com/images/uploads/vcards/Claims_under_s_90A_of_FSMA_for_dishonest_sta.pdf.

Basic Inc. v. Levinson, 485 US 224 (1988).

“Court Endorses Market-Based Causation in Myer Class Action,” Stewarts Law, 22 January 2020, https://www.stewartslaw.com/news/courtendorses-market-based-causation-in-myer-class-action/ (“The significance of the court accepting market-based causation is that it was not necessary to show that a company’s misleading disclosures or omissions had induced a shareholder to purchase shares at an inflated price. Rather it was sufficient to show that the misleading disclosures or omissions had caused the market to trade the shares at an inflated price and that a shareholder who had acquired shares would not have done so at that price but for the market’s reaction to the misleading disclosures or omissions.”).

Halliburton Co. v. Erica P. John Fund Inc., 573 US 258, 134 S. Ct. 2398 (2014)

In the Tesco litigation, “the claimants initially ran a ‘fraud on the market’ argument, which Hildyard J described as ‘intriguing’, but abandoned it. . . .” “Rise in UK Stock Drop Claims Not Checked by Tesco,” Clifford Chance, October 2019, https://www.cliffordchance.com/content/dam/cliffordchance/briefings/ 2019/10/securities-litigation-client-briefing-on-tesco-strike-out-s90Aand-reliance-(judgment-update)-done.pdf.

“Although reliance is an express requirement of the statute . . . , a construction requiring investors to have read the financial statements in question would exclude ‘fraud on the market’ type claims. Such a construction would not sit comfortably with the intention behind the Transparency Director to achieve ‘a high level of investor protection.’ Instead, a broader interpretation of reliance may be appropriate where tracker funds and retail investors rely upon the market price as factoring in the as-represented financial position of the issuer, based in part upon published statements of the issuer. Pursuant to such a construction, reliance on the market price would itself constitute reliance (albeit indirectly) upon the published information.” Peter de Verneuil Smith QC et al., “Claims under [Section] 90A of FSMA for Dishonest Statements Made to the Market: An Underutilised Remedy?,” Butterworths Journal of International Banking and Financial Law, March 2019, pp. 154–158 at 154, https://www.3vb.com/images/uploads/vcards/Claims_under_s_90A_of_ FSMA_for_dishonest_sta.pdf.