Trump’s 2026 State of the Union speech was historic—but only in the sense of the longest ever at 1 hour and 47 minutes. Apart from that, the speech was one third misrepresentations about the state of the American economy followed by more than an hour of pure political theater which has come to increasingly presidential SOTU addresses in recent years.

The misrepresentations of the state of the economy covered topics like inflation and cost of living, record stock market prices and asset wealth creation, his $5 trillion tax cuts almost all of which have accrued to corporations, businesses and investors, and his tariffs which have little to do with trade or economics and everything to do with raising revenue for defense spending and political intimidation of other countries.

Jobs

Treated very briefly in passing was the topic of jobs. Trump’s avoidance of the topic is understandable—given that this past year the US economy has created a total of only 181,000 jobs; i.e. barely 15,000 jobs month, a level which isn’t even sufficient to provide employment for new entrants to the labor force which ordinarily averages at least 100,000 every month.

Trump’s avoidance of the topic is understandable—given that this past year the US economy has created a total of only 181,000 jobs.

On the topic of jobs, Trump also made no mention whatsoever of the current unemployment level. When including involuntary part time, temp, and discouraged workers, as well as full time employed, per the government’s own estimates unemployment has been averaging around 8%. That’s more than 11 million US workers jobless! Moreover, even that 8% number excludes the 10 million workers who are self-employed independent contractors which government statistics conveniently ignore by classifying them as business owners, not workers. So the actual unemployment number of unemployed is thus at least 10% when properly estimated.

Trump made passing reference to the fact that the 181,000 jobs created were 100% in the private sector—without indicating the number of course. Nor did he bother to mention that he managed to fire 27,000 federal government workers. It’s true, as he said, the US economy is at the highest employment levels ever in 2025—by 181,000 jobs of course.

Economic Growth

Another economic topic, this time completely unmentioned, was the overall real growth of the economy in 2025. Measured in Gross Domestic Product terms, GDP, the most generally accepted indicator, the US economy grew only 2.2% in all of last year! That’s down from 2.4% in 2024 before he was elected. More ominous, in the last three months of 2025 the economy slowed rapidly even more to only 1.4%. And it was actually even much slower, since the inflation adjustment used by the government, called the Personal Consumption Expenditure (PCE) price index notoriously underestimates inflation which, in turn, boosts the reported GDP numbers. If properly inflation adjusted, actual GDP in 2025 was closer to 1% than even the reported 2.2%.

Nevertheless, Trump on several occasions bragged “we’re the hottest country in the world!”

As for future economic growth Trump continually says other countries have promised to invest $18 trillion in the US economy! But virtually all of that are just verbal pledges, mostly designed no doubt to placate Trump during negotiations over tariffs. It’s difficult to see how the Europeans, Japanese and others—all of whose economies are either in recession or stagnant—are going to invest that amount in America’s economy instead of their own.

Inflation

Trump did spend some time repeatedly claiming that inflation was reduced dramatically during his first year in office. More than once he proclaimed “inflation is plummeting”. He referenced what is called ‘core’ inflation in the PCE price index, which conveniently excludes food prices, housing costs, mortgage rates, and all other kinds of interest rates on autos, credit cards, and other loans—all of which rose last year.

And there was a big problem with the PCE price-inflation index, whether ‘core’ or what’s called ‘headline’, which includes food and energy prices.

Readers might think the PCE is constructed by the government going out and surveying a large sample of the millions of goods and services in the economy. It doesn’t. It takes a conglomeration of other surveys and estimations performed by the US Labor and Commerce Departments, puts their results together somehow, adds assumptions of its down, employs questionable methodologies, and comes up with a number that grossly underestimates actual prices in general. And here’s a bigger problem with the PCE in 2025. In the fourth quarter of 2025 the government shut down for six of the twelve weeks in the October-December period. During that period there were no surveys done by either the Labor or Commerce departments on which the PCE could be based. So half of the quarter had no data available at all. That didn’t stop the government from making up number for the six weeks that it just plugged in the missing six weeks. It said it ‘imputed’ the data. In translation it means it just made up the numbers to smooth out the twelve weeks’ results.

The PCE is also notorious for deriving prices from non-price data. For example, it doesn’t actually ask insurance companies how much they raised their prices last year. It takes their profits (which they conveniently underestimate in order to pay lower taxes) and it ‘derives’ the industry prices from their profits! There’s scores of such questionable methods employed. And remember, no housing prices, no mortgage rate hikes, and no higher interest charges of any kind.

Trump said nothing in his speech about the huge price hikes now penetrating the economy as a result of the cuts to Medicaid and ACA subsidies. Consumers now have to absorb the huge cost increases if they want to continue prior levels of medical insurance coverage. Many won’t. But none of the loss of subsidies will be counted as price increases or be reflected in the PCE.

Stock Markets

Trump always likes to brag that the stock market is doing so great. And it is true that the three main US stock markets—the DOW, S&P 500, and Nasdaq—all hit record levels in 2025. And then they began crashing in 2026 and have all continued to trend down. Why? Because in 2025 they were almost all pumped up by speculative investing in the Artificial Intelligence bubble. In recent weeks, investors have begun getting cold feet about AI, however. The big & tech companies have been pouring hundreds of billions into developing AI but it is becoming increasingly clear to investors they may not be able to recoup the profits on the over-investing. AI is also threatening to undermine the profits of other tech, banks, transport and other companies. So their stock prices are falling as well.

The cryptocurrency markets are now in even greater freefall. The only game that is ‘hot’ is gold and silver. And their escalating rise is the result of Trump/US sanctions, tariff policy, and the devaluation of the US dollar which is now exceeding 10% so far since Trump took office. The US dollar is not doing so good but Trump said nothing about that. If it’s hot, it’s a ‘hot potato’ that other countries are dumping.

Taxation

Trump has been touting his $5 trillion 2025 tax act which his Republican run Congress quickly passed as the first measure out of the box last spring 2025. Half of the $5 trillion wasn’t even new, however. It represented Trump’s 2018 $4.5 trillion package of tax cuts, more than half of which were for large corporations. In 2018 those tax cuts were made permanent forever and didn’t even come up for renewal in Trump’s 2025 tax package. So no net new tax stimulus from that.

What was up for renewal in 2025 were proposals for small business and individuals. The small business provisions were sweetened even more compared to 2018. So were the individual income tax cuts that benefit mostly those with incomes over $250,000 a year.

When touting his 2025 tax bill Trump likes to remind us, and he did again in his speech, that he cut taxes on tips, overtime pay, and social security. But even a brief summary of those provisions in the 2025 tax act reveal something far less. It doesn’t mean no tax on all tips. For example, a worker making $50K/yr and earning $5k on tips will get a tax deduction of only $600. The no tax on overtime pay is capped at only $12k/yr. And the so-called no tax on social security income is a big misrepresentation. It was reduced by Trump’s Congress to a tepid $6k additional tax deduction not an elimination of any tax on social security income. Moreover, all these so-called working class tax cuts phase out completely by 2028—in contrast to the corporate, business, and wealthy individual tax cuts were are now permanent forever!

Trump may be right when he calls his 2025 cuts “the largest tax cuts in history”, but it’s the largest for investors, corporations and businesses with a small token crumb thrown at American workers and all packaged in a heap of misrepresentations and outright lies.

Since 2001, by the way, presidents and Congresses of both parties have passed tax cuts totally more than $20 trillion, eighty percent of which have accrued to businesses and the wealthy.

That $20 trillion contributed significantly to the US economy’s 2025 $1.77 trillion US budget deficit and the US national debt rising from around $36.5 trillion when Trump took office to its current level just shy of $39 trillion. The other major contributions to those deficits and debt are the $9 trillion spent on wars, the Pentagon’s now $1 trillion/yr war budget, and the $1.2 trillion now paid annually to investors in US Treasury securities to pay interest on that debt. No mention of that either, of course. Or that his budget deficit in 2025 was virtually the same as Biden’s $1.8 trillion in 2024! Not a word in his speech about the out of controls annual deficits and debt. Yes, the US economy is ‘hot’, as in the barn is about to burn down hot.

Tariffs

Trump spent some time hyping his tariff policies. He bragged how his tariffs have brought in hundreds of billions of dollars of new revenues—the exact number he avoided citing since it appears, per the recent Supreme Court decision, he’ll have to give some of that back.

One would have thought he’d say something about how tariffs have reduced imports and thus reduced the USA’s annual almost $1 trillion trade deficit. But he didn’t. Why? Because the tariffs haven’t reduced that trade deficit all that much. They’re not about trade or trade deficits. The tariffs are about raising revenues for a government running $1.8 trillion budget deficits and in desperate need of new revenue sources since it’s simultaneously cutting tax revenues—and it needs to raise more funds to pay for its accelerating defense-war costs. Total US war-defense costs, not just Pentagon spending, are now running $2.1 trillion a year. And Trump says he wants to give the Pentagon, now at $1 trillion, another $400 billion for weapons in his 2027 budget. Tariffs are thus about ‘shaking down’ US allies and the rest of the world economy to generate more US government revenue to pay for tax cuts and more war spending.

Tariffs are also a tool for intimidating foreign governments to ‘toe the line’ on US foreign policy. In that sense, they are an addition to US sanctions policies which haven’t worked all that well in that regard in recent years.

Trump’s tariff policies are all over the map. They are causing real economic strain for many US small businesses and farmers who are losing markets and revenues, as well as to some extent to consumers whose prices for goods imports are rising.

It is true that Trump has raised the average rate of tariffs on imports to the US from a previous 2.4% to around 13%. And those who think legislation or the Supreme Court will prevent him from raising them further are naively mistaken. His vision is tariffs are the economic panacea for all that ails the US economy. As he put it at one point, obviously departing from his prepared speech, he wants tariffs to someday even replace the individual income tax!

That will mean a regressive de facto sales tax on goods imports of at least 30%. At that level, domestic US producers will have sufficient cover to raise prices on US produced goods by at least 10% on average. Double digit chronic inflation anyone?

These were the main economic measures Trump addressed. When considered in more detail, Trump’s touting of the US economy’s performance in 2025 amounts to misrepresentation at best, and outright lies in most cases.

The Trump economy and the USA is ‘hot’ only in the sense it is becoming domestically, and globally, an internal combustion engine heating up as result of insufficient coolant.

The US economy is not robustly growing but slowing. Jobs are barely being created. Inflation is nearly twice that reported by the PCE index, which is over-inflating US GDP in turn. The stock market bubbles of 2025 have begun unwinding, the AI hype has peaked, and the US dollar devaluation is accelerating and the worse since the 1970s. The US budget deficits and national debt continue surging out of control and interest payments to rich holders of US Treasury securities are escalating past $1.2 trillion a year! The tax cuts of 2025, like those of 2018, will provide little if any real stimulus to the economy and the working class cuts are a sham of what’s claimed. Pledges by other countries to invest in the US aren’t worth the verbal assurances given or the paper they’re written on, if in fact they were written. Tariffs are about raising revenue and political intimidation of allies and the rest of the world alike. They are a reflection of the fact the US empire is running short of funds and is searching for radical funding alternatives in lieu of economic growth or debt financing now approaching its limits. Tariffs in turn are upending global supply chains and global trade and will lead to other countries’ turning further away from the US dollar, thus ensuring its further devaluation.

In short, the Trump economy and the USA is ‘hot’ only in the sense it is becoming domestically, and globally, an internal combustion engine heating up as result of insufficient coolant. And when engines become so ‘hot’, their mechanical working parts eventually just freeze up.

Jack Rasmus is author of the recently published book, ‘The Scourge of Neoliberalism: US Economic Policy from Reagan to Trump’, Clarity Press, 2020. He publishes at Predicting the Global Economic Crisis.

Badge lines formed before sunrise, commuter trains filled past standing room, and managers refreshed headcount dashboards as agencies prepared for a reset. President Trump’s January 20, 2025 memorandum delivered a blunt operational direction: end broad remote work and restore full-time, in-person duty stations.

Employees who use telework as a disability accommodation read it as a civil rights test, because their workday depends on more than convenience.

Many leaders treated it as a fast lane back to 2019 norms. Employees who use telework as a disability accommodation read it as a civil rights test, because their workday depends on more than convenience. Many agencies delayed and denied telework requests for those with disabilities despite the widespread use of such accommodations previously, resulting in labor conflicts and lawsuits. That tension sat unresolved until recently, when the Equal Employment Opportunity Commission published federal guidance that tightened the legal and practical limits around any sweeping return-to-office push.

The guidance warned agencies against a blanket approach to denying or rescinding recurring telework accommodations and emphasized individualized assessments. That point matters because a top-down return-to-office order tempts managers to solve compliance with a single line: everyone returns, no exceptions. The EEOC signaled that approach creates legal exposure when disability accommodations sit in the mix.

The commission’s composition amplified the moment. The EEOC regained a working quorum after Brittany Bull Panuccio began service, confirmed by the agency’s tenure announcement. Panuccio joined Chair Andrea Lucas to form a Trump-appointed majority. In that context, the guidance carried extra weight: a pro-Trump majority still drew a compliance boundary that constrained the harshest versions of Trump’s own return-to-office drive.

That boundary sits on federal disability law. For executive-branch employment, the framework runs through the Rehabilitation Act, which bars disability discrimination and requires reasonable accommodation for qualified employees. The EEOC’s FAQ emphasizes a central legal idea: agencies must evaluate whether telework enables an employee to perform essential functions, and they must do that evaluation case by case. Telework can qualify as a reasonable accommodation, and the EEOC has long treated it that way in its telework accommodation guidance, which explains how to assess essential functions and run the interactive process.

The February 2026 guidance also clarified an important management lever. When multiple effective accommodations exist, an agency can select an option other than telework. That line keeps the guidance credible with leaders because it protects operational flexibility. The constraint comes from process and proof. The EEOC warned that rescinding previously granted telework without individualized assessment invites liability when telework functions as the only effective accommodation for a given employee. In practice, that forces managers to define essential functions with precision, document why an in-office requirement matters to the role, and engage employees in a real interactive process rather than a scripted denial.

Private-sector enforcement shows why the EEOC took this stance. For example, the EEOC sued a contractor over an alleged denial of remote work for an employee after a stroke, outlined in the agency’s Osmose lawsuit release. The alleged facts underscore a recurring theme: when duties center on screens, tickets, and customer communications, physical presence often looks less like an essential function and more like a management preference. Courts also back employers when evidence supports in-person essential functions. These outcomes converge on one lesson that the federal guidance reinforces: the facts decide, and the paperwork matters.

Leaders who treat telework accommodations as disposable risk shrinking their talent pool at the same moment competition for specialized skills remains fierce.

The broader workforce trend sharpens the stakes. Labor-force participation among people with disabilities reached record levels in the pandemic era, with remote and flexible work frequently credited as a key driver, according to a SHRM data brief. Leaders who treat telework accommodations as disposable risk shrinking their talent pool at the same moment competition for specialized skills remains fierce.

This episode shows how institutions constrain executive pressure. Even with a Trump-appointed majority, the EEOC put individualized assessment and disability rights ahead of speed, and it gave agencies a clear warning against blanket telework denials under return-to-office mandates. Return-to-office can still move forward, but it must move through the legal gate the EEOC just tightened: a real interactive process, a role-specific essential-function analysis, and a documented decision that respects disability rights while pursuing operational goals.

Air conditioning is now a standard part of modern HVAC systems, built into how we design homes, offices, and entire cities. What started as a breakthrough for comfort and safety has quietly become a default solution for temperature control. But the real question isn’t whether HVAC cooling works, it’s whether we’ve begun relying on it in place of smarter design, adaptation, and resilience.

Are We Seeing Overuse of Air Conditioning

The issue isn’t simply “people use AC too much.” The deeper concern is the overuse of air conditioning as a built-in assumption. We now design buildings expecting mechanical cooling to fix everything. We’re not just seeing behavioral overuse, we’re seeing design dependency. So the overuse isn’t just personal preference. It’s architectural and systemic.

Modern homes are often tightly sealed, built with large glass surfaces, poorly shaded, and designed without cross-ventilation. Buildings are now constructed assuming mechanical cooling will compensate for poor orientation, excessive glass, lack of shading, and minimal airflow strategy. AC isn’t supplementing design, it’s replacing it.

Instead of using passive cooling like shade, airflow, and insulation strategy, we rely on mechanical cooling as the default solution. That creates a cycle: hotter cities lead to more AC use, which expels more heat outdoors, which makes cities even hotter. That feedback loop fuels the overuse of air conditioning at scale. When architecture stops solving climate, machines take over.

Can You Overuse an AC?

When indoor comfort standards drop to 68-70°F in summer, people physiologically adapt to cooler indoor climates. Humans are adaptable, and when we live in narrow temperature bands (68-72°F year-round), our thermal tolerance shrinks. Mild heat feels intolerable, tolerance to warmth decreases, and natural temperature swings feel “wrong.” That’s how comfort baselines shift.

It already has, but the deeper shift is biological. Over time, we don’t just prefer cooler air, we lose flexibility.

The bigger risk isn’t health panic headlines claiming air conditioning bad for health. The real issue is resilience. Overdependence reduces our ability to function during power outages, extreme weather, or grid strain. That’s where the conversation about overuse belongs.

Is Air Conditioning Bad for Health

The idea that air conditioning bad for health is a common narrative, but it’s oversimplified. Air conditioning itself isn’t harmful – a lack of proper air conditioner service is.

AC protects people from heat stroke, sleep disruption, and cardiovascular strain during heat waves. It reduces heat-related illness, improves sleep quality, lowers humidity and mold growth, and improves filtration when filters are clean. In fact, many measurable health effects of air conditioning during extreme heat are positive, especially for vulnerable populations.

Concerns about the effects of air conditioning on health usually stem from dirty filters, mold inside ductwork, extremely low temperatures, neglected AC maintenance, very dry indoor air, poor ventilation, and static environments. When air is over-dried or recirculated without fresh intake, discomfort follows, not because cooling is inherently dangerous, but because the indoor ecosystem is poorly managed.

Blaming AC entirely feeds the “air conditioning bad for health” myth. The system isn’t the problem, neglect and imbalance are.

Effects of Air Conditioning on Health Indoors

The effects of air conditioning on health depend entirely on how the system is operated. Reduced heat stress, lower humidity that limits dust mites and mold, filtered airborne particles, and a more stable indoor environment for asthma sufferers are clear benefits.

Negative outcomes appear when systems are mismanaged. The real health effects of air conditioning become noticeable when humidity drops too low, airflow is too aggressive, or temperatures are set unnaturally cold. Dry eyes, throat irritation, sinus congestion, headaches, and muscle stiffness usually result from imbalance, not from cooling itself.

Very cold indoor environments can trigger subtle vasoconstriction, increase muscular tension, and create low-level thermal stress. This is why people in overly cooled offices report fatigue or brain fog. These are contextual effects of air conditioning on health, not evidence that cooling technology is inherently unsafe.

Long-Term Health Effects of Air Conditioning

There’s no strong evidence that AC causes serious long-term disease in healthy individuals. In fact, during extreme heat events, the measurable health effects of air conditioning include lower mortality rates and reduced hospitalizations.

The better long-term question is about adaptation. Repeated claims that air conditioning bad for health often miss the bigger issue: reduced environmental resilience. If we never experience moderate warmth, our acclimatization capacity declines.

Long-term behavioral patterns may include reduced outdoor heat exposure, lower heat tolerance, increased sedentary indoor time, and chronic dryness sensitivity. These are subtle effects of air conditioning on health, but they relate more to environmental narrowing than to pathology. The conversation isn’t about illness, it’s about adaptability.

Signs of Overuse of Air Conditioning

The overuse of air conditioning isn’t about runtime hours. It’s about context and dependency.

Setting temperatures below 70°F during summer, feeling cold indoors while it’s hot outside, running cooling during mild evenings, or keeping windows closed year-round are lifestyle signals. Complaints of dryness or constant indoor chill may reflect the excessive use of air conditioner, not a flaw in the technology itself.

Forget thermostat numbers. Look for perception shifts: temperature shock when stepping outside, viewing 75°F as “too hot,” or rarely using passive airflow strategies. These patterns suggest dependency.

A practical test: if you need a sweater inside in August, the system may be compensating more than necessary, a subtle form of overuse of air conditioning.

When Excessive Use of Air Conditioner Becomes a Habit

The excessive use of air conditioner becomes a habit when the thermostat is the first response instead of the last. Lowering the temperature the moment it feels slightly warm removes seasonal awareness from daily life.

Instead of adjusting clothing, using ceiling fans, opening windows at night, shifting activity timing, or using shading strategically, we default to mechanical cooling. That shift marks the difference between comfort management and dependency.

Over time, that automatic response reinforces both physiological narrowing and behavioral reliance, a quieter but more meaningful outcome than headlines claiming air conditioning bad for health.

Is the Overuse of Air Conditioning a Modern Problem

The overuse of air conditioning reflects how we design buildings and cities. Sealed glass towers in hot climates, identical indoor temperatures year-round, aesthetics prioritized over passive cooling, these choices drive reliance.

At the urban scale, the excessive use of air conditioner systems increases heat rejection into city streets, intensifying urban heat islands and further raising demand. That loop isn’t about individual preference; it’s structural.

Air conditioning is one of the greatest public health inventions of the last century. The discussion isn’t whether it’s good or bad. The measurable health effects of air conditioning during heat waves are lifesaving. The challenge is designing systems where it isn’t the only strategy.

The future isn’t less cooling, it’s smarter cooling: insulation, shading, passive-first design, zoned systems, ceiling fans, moderate setpoints (74-78°F), humidity balance, and fresh air integration. That’s a far more intelligent conversation than framing it as simply “air conditioning bad for health.”

The Supreme Court of the United States decision to strike down former President Donald Trump’s sweeping global tariffs has rattled US trade partners — but it may have strengthened China’s position.

The ruling came just weeks before Trump is scheduled to meet Chinese leader Xi Jinping in Beijing for a three-day summit focused on trade, technology and Taiwan. For years, Trump relied on tariffs as a primary negotiating tool. The court, however, found that he exceeded his authority by invoking emergency powers under the International Emergency Economic Powers Act.

Although Trump quickly moved to reimpose temporary 15% tariffs under a different trade statute, the decision stripped away one of Washington’s strongest pressure tactics.

Chinese commentators framed the ruling as a win for Beijing. Since the first trade war erupted in 2018, China has worked to reduce its exposure to US tariffs by diversifying agricultural imports and expanding trade with other markets. Last year, it recorded a record $1.2 trillion trade surplus, buoyed by redirecting exports abroad.

Beijing has also tightened controls on rare earth mineral exports, materials critical to advanced electronics and defense systems, reinforcing its leverage.

Analysts at Morgan Stanley estimate that average US tariffs on Chinese goods could fall significantly under the revised framework, narrowing the gap between China and other Asian exporters.

While tensions remain high, the court’s decision shifts momentum, at least temporarily, toward Beijing as both sides prepare for high-stakes talks.

In the industrial sector, there is a constant search for technological solutions that can make production processes more efficient and cost-effective, without compromising the quality of the final product. Twin screw extrusion is a classic example of advanced and versatile technology which is used in several industrial sectors, including polymers, food, and pharmaceuticals.

The main feature of twin screw extrusion is that it turns complex materials into regular, repeatable products. In other words, this technology allows you to work with different ingredients or polymers (complex materials) and convert them into regular products that can be produced over and over again with identical features (repeatable).

How does a twin-screw extruder work?

In the industrial sector, extrusion is carried out using special machines called extruders, which can be single screw, twin screw, or triple-screw. During processing, the raw material is mechanically transformed and shaped through a die.

A key part of the extruder is the cylinder, which contains the two screws. It represents the “heart” of the system, because it is inside the cylinder that the material undergoes the various processing stages that lead to a homogeneous distribution of the various ingredients (polymers, food, chemicals, etc.).

The screws contained in the cylinder can be co-rotating – the most common – or counter-rotating. In the first case, they rotate in the same direction, while in the second case, they rotate in opposite directions. The choice between co-rotating and counter-rotating screws depends on the type of processing required. For example, the counter-rotating are particularly suitable for applications where high compression force is required.

Twin-screw or single-screw extruders?

As mentioned above, the choice between twin screw and single screw extruders essentially depends on the type of processing. It is worth pointing out the differences between the two options, as both have pros and cons.

For example, from a cost perspective, twin screw extruders are definitely more expensive, as this type of machine is capable of delivering the highest quality performance with complex and/or heat-sensitive materials. For less complex processes, a single screw extruder is a perfectly suitable choice, as it offers good performance, lower energy consumption, and very simple maintenance.

Therefore, the choice should be made according to processing requirements: for less complex processes, single screw extrusion is an efficient and economically attractive solution. If, on the other hand, higher performance is required (blending of complex, viscous, and abrasive materials, precise temperature control, etc.), the twin screw extruder remains the preferred choice for most. A good example is compounding, which refers to mixing polymers with additives, colorants, and different types of fibers to create a material with specific features.

Twin-screw extrusion: which are the main areas of application?

One of the sectors that makes the most use of twin screw extrusion is the plastics industry. Here it is used for compounding, for the production of plastics reinforced with carbon or glass fibers, for the processing of thermoplastics (PVC, PP, PE, PET, and similar products), recycled materials, etc.

Extrusion is also used in the food industry for the production of snacks, pasta, cereal-based products, vegetable proteins, etc. This technology is also used in the chemical and pharmaceutical industries. The high level of precision guaranteed by twin screw extruders is essential in the preparation of materials for the production of granules, capsules, and tablets, where the equal distribution of active ingredients and excipients is a prerequisite. In fact, it is necessary to get rid of the risk of differences between batches.

What are the characteristics of twin-screw extrusion?

The twin screw extrusion process has some interesting aspects. Among these, one of the main ones is the intensive and homogeneous mixing of materials, including those that are more difficult to process (and for which single-screw extrusion may not be adequate). This feature ensures homogeneity and repeatability, two fundamental aspects in certain specific industrial sectors. Modern extruders also guarantee maximum precision in terms of temperature control (which in some processes does not always have to be the same) and pressure.

However, it is important to keep in mind that the quality guaranteed by a twin screw extruder involves a significant upfront investment, which should be taken into account when calculating the costs to be recovered over time. Operating and maintenance costs are also generally high because this is a very complex machine. The training of those who will use it is yet another thing to think about, as this type of machine requires qualified operators.

The Digital Operational Resilience Act came into full effect in January 2025, and its requirements around privileged access management are more specific than most organizations initially expected.

This is especially the case because DORA’s articles effectively mandate architectural controls that many traditional Privileged Access Management (PAM) tools were never designed to provide.

For PAM specifically, DORA mandates two things. One is strict access control with separation of duties, and the other is management of third-party ICT concentration risk. DORA compliant PAM tools like SplitSecure are used because their distributed architecture satisfies both requirements by design rather than by policy i.e. with cryptographic controls for logging and managing access to secrets.

In this article we want to give you the exact DORA articles that reference PAM capabilities, a mapping of how different tool categories address them, and the case for architectural compliance over policy-based compliance.

DORA Has Five Articles That Reference PAM Capabilities

DORA does not mention “privileged access management” by name, but five DORA articles contain requirements that map directly to PAM capabilities.

Article

Requirement

PAM Relevance

Article 9(4)(c)

Access rights based on need-to-know, least privilege, and segregation of duties

Core PAM requirement: enforce least privilege and separation of duties for privileged accounts

Article 9(4)(d)

Strong authentication, including multi-factor where appropriate

MFA enforcement for all privileged access sessions

Article 9(4)(e)

Logging and monitoring of access to critical systems

Immutable audit trail for every privileged access event

Article 28

Third-party ICT concentration risk assessment

Evaluate whether PAM tool creates single-vendor dependency for critical credentials

Article 11

Backup policies ensuring recovery without over-reliance on ICT providers

Backup admin credentials must function independently of third-party availability

How Different PAM Tools Address DORA Requirements

Not every PAM tool addresses every DORA requirement equally. The gap between tools shows up most clearly around separation of duties enforcement and third-party concentration risk.

Hub-and-Spoke Vault PAM (CyberArk, BeyondTrust)

Enterprise PAM platforms handle most DORA requirements through configuration. Role-based access control enforces least privilege. Session recording and credential rotation provide audit trails. MFA integration is standard.

The gap is in separation of duties enforcement. Traditional PAM relies on policy configuration to prevent a single identity from taking catastrophic actions.

If the policy is misconfigured, or if an admin account is compromised with sufficient privileges, the architectural control does not exist. DORA Article 9(4)(c) requires segregation of duties, and policy-based enforcement is weaker than architectural enforcement.

On Article 28 (concentration risk), on-premises deployments avoid third-party dependency. Cloud versions of CyberArk and BeyondTrust reintroduce it.

Cloud-Native SaaS PAM (Akeyless, HCP Vault)

Cloud-native platforms handle access control and audit logging well. The developer experience is stronger than enterprise PAM, and integration with cloud infrastructure is native.

The DORA gap is Article 28. Both Akeyless and HCP Vault operate as SaaS platforms. Your ability to retrieve credentials depends on their platform availability. For DORA compliance teams assessing ICT third-party concentration risk, this dependency requires documented risk mitigation and exit strategies. It is manageable but creates compliance overhead.

Distributed Secrets PAM (SplitSecure)

SplitSecure addresses DORA requirements differently. Separation of duties is not configured through policy but is cryptographically enforced. No single device holds a complete credential, and no single identity can perform catastrophic actions unilaterally. This satisfies Article 9(4)(c) by architecture.

On Article 28, SplitSecure eliminates the concentration risk question for secrets management. There is no vendor dependency on the secrets management platform. If SplitSecure ceased operations, deployments would continue functioning.

On Article 9(4)(e), every access generates an immutable audit trail automatically. You cannot use the system without creating a log entry. This is not a feature that is enabled or enforced by policy but is a fundamental function of how the technology works.

DORA Compliance By Architecture

The easiest way to meet any regulation is to be architecturally compliant. That means having systems in place where compliance does not need to be enforced by policy or process but happens as a technological default.

For DORA PAM requirements specifically, the question compliance teams should ask each vendor is: “If policy is misconfigured, does your architecture still prevent a single compromised account from causing irreversible damage?” Tools where the answer is yes by architecture – not by correct configuration – carry lower compliance risk.

If the future of work were determined by headline volume, the office would already be overflowing. Inside most companies, the picture is quieter and more consistent. Work location patterns in the United States have settled into a resilient hybrid equilibrium that has barely budged since 2022, according to Gallup’s newest research. Leaders still debate productivity, culture, and collaboration, yet the numbers tell a steadier story than the news cycle suggests.

Headlines Say Return, Data Says Plateau

Employees and managers have learned how to orchestrate hybrid weeks, and that behavioral learning dampens the impact of new memos.

The center of gravity remains hybrid. Gallup’s research shows only small shifts in recent quarters, with the share of remote-capable employees in hybrid dipping from 55 percent to 51 percent while fully on-site and fully remote each ticked up by two points. Across the same period, hybrid employees report spending about 46 percent of the week in the office, or roughly 2.3 days. That in-office time rose during 2023 and then leveled off, signaling that the post-pandemic adjustment has matured. The stability is striking because it resists the narrative of a sweeping return to full-time on-site work.

External indicators confirm the plateau. Office occupancy has hovered in a mid-week-heavy pattern, with big city averages stuck just over the halfway mark on keycards according to the continuing Kastle Systems barometer.

The broader mix of where Americans work has steadied as well. The WFH Research team’s Survey of Working Arrangements and Attitudes shows that remote, hybrid, and on-site shares have moved within a narrow band since 2023, reflecting a new normal rather than a temporary detour. Taken together, these signals point to habit formation. Employees and managers have learned how to orchestrate hybrid weeks, and that behavioral learning dampens the impact of new memos.

There are exceptions worth watching. In technology, remote-capable employees split almost evenly between fully remote and hybrid, and only a small minority are fully on-site. In federal government, policy moved behavior far more abruptly. After a change in direction in 2025, the share of federal employees working in flexible hybrid arrangements fell sharply while fully on-site rose to levels that are well above the national average for remote-capable workers. Those changes show up clearly in the Gallup data and mark Washington as an outlier. For most private employers, the pattern is still a broadly hybrid workforce that has stabilized after a period of experimentation.

Hybrid Works When Teams Coordinate, Not Lone Wolves

Hybrid succeeds when teams set common rules, not when every individual optimizes for themselves. Gallup’s scheduling data indicates a gradual shift from purely self-determined hybrid calendars toward schedules influenced by managers or decided collectively by teams. About one third of hybrid employees say the cadence is entirely up to them, another third point to the manager or team, and the remaining third cite employer or leadership decisions. That distribution matters because it correlates with perceptions of fairness. Employees who say their team sets the schedule are just as likely to view the policy as fair as those who set their own, while employer-determined calendars trail significantly on perceived fairness.

Fairness is not the only outcome at stake. Gallup’s analysis also shows trade-offs for purely self-determined schedules. Relative to team-decided arrangements, employees who control their own cadence are 76 percent more likely to identify burnout or fatigue as their greatest challenge, 57 percent more likely to cite reduced work-life balance, and 52 percent more likely to point to meeting customer needs as the top issue. The conclusion is practical and actionable. Teams that agree on a shared rhythm reduce coordination costs, increase predictability, and make the most of in-person time by aligning complex, interdependent work to the same days.

When teams design the week, those office days gain purpose. Leaders can earmark co-located time for activities that benefit from proximity, such as onboarding, sales workshops, code reviews, and cross-functional design sessions. Remote days then become focus time for deep work that suffers in noisy environments. This approach does more than keep calendars tidy. It improves retention and avoids productivity penalties. A large randomized trial at Trip.com found that hybrid schedules did not reduce performance while they did cut quits, with the biggest gains among longer-commute employees and non-managers. When the cadence is planned at the team level, the model becomes a talent advantage rather than a concession.

Financial signals point the same way. Joint research by Flex Index and Boston Consulting Group associates greater workplace flexibility with stronger revenue growth relative to rigid models. The mechanism is straightforward. When companies broaden their talent funnel and reduce attrition, they compound skill density over time. That dynamic shows up in the top line, especially in knowledge work where learning curves and network effects matter.

Trust And Measurement Beat Mandates

The limiter on hybrid performance is not software or seating charts. It is trust. Gallup’s latest findings show that just over half of managers who lead remote or mixed teams strongly agree they trust their people to be productive when working from home, and a similar share of employees say they feel that level of trust from their manager. That gap between policy and confidence fuels heavy-handed attendance rules that often chase the wrong variable. Attendance is visible. Output is what customers buy.

Trust grows when managers make the basics routine. Communication must be timely and consistent regardless of where people are sitting so that remote and on-site employees receive the same context. Community must be cultivated deliberately through inclusive rituals and shared decision logs so that no one loses access to social capital on their at-home days. Accountability must be explicit and focused on outputs so that expectations travel with the work. Development must be equitable so feedback, coaching, and stretch assignments do not disappear when employees are off campus. Gallup’s analysis links these practices to markedly higher feelings of trust among employees and more confidence among managers.

This managerial playbook also answers a common fear. Some executives assume that stricter attendance rules will fix performance problems. The evidence suggests that clarity and measurement do more. When teams agree on the purpose of in-office days and leaders measure outcomes, productivity follows. The randomized Trip.com trial is a powerful example because it separates preference from policy and still shows stable performance with improved retention. Hybrid is not a workaround. Done well, it is a performance system that channels the right work to the right setting.

Leaders who accept that fact and design for it will find themselves ahead of rivals who manage by headline rather than by evidence.

None of this denies the realities of certain jobs. Roles with heavy customer handling, secure facilities, or specialized equipment will always be more on-site. The Gallup data even shows that among fully on-site remote-capable employees, a growing share now work with colleagues spread across locations, which means coordination still matters. What changes is how leaders think about levers. If the goal is better collaboration, use team-level design to get people together for the right reasons. If the goal is higher output, anchor performance in clear metrics and regular feedback. If the goal is culture, reinforce shared rituals that include everyone, regardless of where they sit on Tuesday.

Conclusion

The return-to-office storyline is loud, but the labor market is not listening. The measured reality since 2022 is a stable hybrid model with modest shifts at the margins, a mid-week occupancy peak, and a settled cadence that people have learned to run. Gallup’s latest analysis reinforces that hybrid works best when teams coordinate schedules, employees understand the rules, and managers build trust through communication, community, accountability, and equitable development. External evidence from the WFH Research survey, the Kastle Systems barometer, the Trip.com trial, and Flex Index research all point to the same destination. Hybrid is no longer a moment. It is the operating system of modern work. Leaders who accept that fact and design for it will find themselves ahead of rivals who manage by headline rather than by evidence.

The Philippines is preparing for a Taiwan war. That’s known. But the costs of that “inevitable war” are not. It‘s time to address them.

In August 2025, President Marcos Jr. said that “a war over Taiwan will drag the Philippines, kicking and screaming into the conflict.”

Pushing for preparation, the government has boosted US-Philippine military cooperation, military modernization, joint military exercises and the installation of US mid-range missile systems and anti-ship missile launchers.

These measures are said to foster Philippine prosperity and security.

But how would a major military conflict in the Taiwan Straits, with the active support of Manila’s military logistics, affect the economic futures of the Philippines?

How PH becomes a “co-belligerent”

In the past decade, globalization has given way to geoeconomic fragmentation, replacing economic efficiency along geopolitical lines. Recently, this has morphed into “Cold War II”; a prolonged, systemic rivalry risking substantial, long-term global GDP losses.

By providing significant military logistical support to the belligerents, Manila becomes a de facto co-belligerent in the conflict.

A Taiwan contingency is the kind of shock in which fragmentation becomes nonlinear under conflict, as the World Bank and the International Monetary Fund (IMF) have warned – implying that economic and human costs will soar. With that backdrop, let’s integrate a major Taiwan conflict with Manila’s logistics support (bases, ports, airspace, supply, etc.) into a real-GDP scenario.

In this status quo, the EDCA sites – US military bases and facilities in the Philippines – are used for logistics, refueling, repair, transit. They may have no direct combat role, but they represent de facto alignment.

Faced with the US missiles’ offensive capabilities, China defends itself, and treats Philippines as a “non-neutral,” hostile rear-area state.

By providing significant military logistical support to the belligerents, Manila becomes a de facto co-belligerent in the conflict, according to international law (Hague Conventions of 1907, V and XIII) and customary law.

Short-term Taiwan shock

So, let’s assume two Taiwan contingencies. In one case, there is a major level shock, a one-time GDP hit in the first 2-3 years. This is the scenario that geopolitical analysts favor, perhaps because its costs are lower.

In this case, a short war ensues and lasts 3–6 months. The lethal conflict is followed by a ceasefire.

Here’s what happens with major economic transmission channels. First, there will be a trade disruption as shipping insurance spikes in South China Sea (which Manila calls the West Philippine Sea). Port risk premium soar for Manila, Subic, Batangas, and Cebu. Semiconductor and electronics global value chains (GVCs) are disrupted. A regional growth shock ensues.

ASEAN trade volume contracts sharply.

As investors start treating the Philippines as a riskier place to keep money, wealthy Filipinos and foreign investors move part of their money abroad (to Singapore, the US, etc. (a trend that’s already nascent); or they demand higher returns to keep it in the country.

Markets charge the Philippine government more to insure its debt against default, which increases risk premium. Repricing raises borrowing costs, discourages long-term investment, and drains domestic capital toward safer jurisdictions, reinforcing inequality. Peso depreciation pressure will soar.

Targeted retaliation ensues, with Chinese import bans, the collapse of tourism and the freeze of foreign investments. China rejects Philippine products and services. Tourists shun risky regions (Chinese tourism collapsed already in 2023-24). Foreign investors avoid potential military targets.

The first scenario represents a severe but time-bounded disruption. But what if the conflict lasts longer?

In the second scenario, a prolonged blockade can last up to 3–5 years. It doesn’t necessarily mean a formal war, but sustained interdiction: a continuous, long-term, and coordinated effort to divert, disrupt, delay, or destroy the Philippine military supplies, and logistics.

This scenario would translate to greater and longer-lasting “kinetic” damage. Now there is a permanentgrowth penalty, due to higher risk and decoupling.

Don’t blame the messenger. This is the way war shocks are modeled in the IMF Article IV stress tests.

The semiconductor and electronics GVCs are broken. Global insurers stop covering ships, cargo, or investments linked to the Philippines, due to geopolitical risk.

Permanent rerouting ensues, as trade and logistics flows are redesigned to bypass the country altogether. This is not temporary, but built into long-term supply chains—so business simply goes elsewhere.

The Taiwan shock becomes Philippines’ structural nightmare.

Revised real GDP scenarios

A short war generates a level shock. By contrast, a long blockade virtually ensures a level shock and a permanent growth downgrade.

In the immediate shock, some first 3 years after conflict, trade volume will plunge by 15%, tourism by 50% and foreign investment inflows by 60%. Investment ratio will decrease by 3-4 percentage points of GDP. In this case, the one-time real GDP loss would amount to 6–10%.

These shock assumptions are conservative, however.

As militarization is likely to crowd out civilian investment, inequality soars and poverty spreads.

In the second scenario, the long-run effects will feature greater cost of capital and a partial exclusion of Philippines from China-centered Asia trade. As militarization is likely to crowd out civilian investment, inequality soars and poverty spreads. The best and brightest leave, followed by recurrent streams of blue-collar OFWs.

In the case of the longer shock, the Philippine real GDP index would plunge -43% behind the baseline by 2050, lower than in many Latin American countries. The country would look like Ukraine after 2022.

In the process, the country gets stuck in the middle-income trap, which becomes structural.

The end of the dream

By 2035, the Philippines loses roughly a quarter of its potential income per person. This is equivalent to 10–15 years of development delay.

In the second scenario, the devastation wipes out 20–40% of long-run real output potential by 2050. Instead of a lost decade, a generation is wasted.

By then, the Philippines is no longer regarded as a potential ASEAN catch-up promise. It is seen as a textbook case of a growth story that lost its way.

This shorter version of the original commentary was published by The Manila Times on February 23, 2026.

Dr. Dan Steinbockis an internationally recognized strategist of the multipolar world and the founder of Difference Group. He has served at the India, China and America Institute (USA), Shanghai Institutes for International Studies (China) and the EU Center (Singapore). For more, see https://www.differencegroup.net

The erosion of US dollar hegemony—driven by structural debt, financialisation, geopolitical fragmentation, and reserve diversification—signals a historic inflection point in the global monetary order. Dr Kalim Siddiqui argues that this crisis of rentier dominance generates acute instability for the Global South, yet also creates opportunities to build sovereign, development-oriented financial institutions beyond dollar-centred extraction.

I. Introduction

The erosion of dollar hegemony—rooted in mounting structural debt, the accelerating financialisation, and geopolitical fragmentation, and the strategic diversification of reserves into gold and alternative currencies—signals a decisive historical inflection point. This transition reflects not merely cyclical instability but a deeper crisis in the rentier foundations of United States (US) global dominance. As Western cohesion weakens and emerging economies pursue monetary and institutional alternatives, the international monetary order is undergoing a structural realignment toward multipolarity.

This study argues that the transformation presents the Global South with profound risks—heightened financial volatility, intensified geopolitical rivalry, and the threat of renewed dependency—yet also opens a historic opportunity to challenge rent-based extraction and construct more sovereign, development-oriented financial architectures. The outcome will depend on whether emerging economies can convert systemic rupture into coordinated institutional innovation.

If the twentieth century saw power migrate from London to New York, the current decade witnesses its diffusion—challenging the capitalist equilibrium established eighty years ago.

The 1944 Bretton Woods Conference established a new international monetary order through the creation of the International Monetary Fund (IMF) and the World Bank (Siddiqui, 1994). This agreement solidified the US dollar as the global currency, a position underpinned by the sheer dominance of US. It supplanted the gold standard and institutionalised the US dollar as the de facto global reserve currency for finance and trade. At the time, the US accounted for approximately 35% of global GDP, and its industrial corporations, functioning as the world’s primary exporters, generated substantial trade surpluses. This concentration of economic power enabled the US to accumulate two-thirds of the world’s official gold reserves, thereby rendering the dollar “as good as gold” and anchoring the new system to US fiscal credibility (Siddiqui, 2020).

For over eighty years, the existence of an uncontested hegemonic power—a recognised leader of global capitalism—provided the geopolitical and economic stability necessary for transnational capital accumulation. This unipolar configuration reduced transactional uncertainty, enforced the institutional frameworks of the Bretton Woods system, and created the stable conditions under which international business could be conducted and profits secured. In this regard, the longevity of US hegemony was not merely a political phenomenon but a structural prerequisite for the post-war expansion of global finance and trade (Siddiqui, 2025a).

In the 19th and early-20th century, during the heyday of the British Empire, global finance and trade was conducted within the framework of the ‘Gold Standard’. At that time, British imperialism was the world’s hegemon, playing a similar role to that of US imperialism in the postwar period – providing the stable economic and political foundations upon which world trade and industry could flourish.

The British economists like Adam Smith and David Ricardo then developed the ideas of bourgeois ‘political economy’, championing liberalism, free trade, and the ‘invisible hand’ of the market. By the end of the 19th century, however, it was clear that British capitalism was being overtaken by its rivals. The First World War catalysed the changing balance of forces between the powers. Britain, France, and Germany economies were weakened from the war. The Treaty of Versailles left Germany heavily indebted to Britain and France, who in turn owed huge sums to the US. Meanwhile, the war accelerated the migration of global financial activity from the City of London to New York’s Wall Street.

By the interwar period, Britain could no longer sustain its role as the guarantor of global trade and finance. The Gold Standard, weakened by geopolitical strains and economic instability, collapsed during the Great Depression. In response, capitalist powers adopted protectionist “beggar-thy-neighbour” policies, raising tariffs to curb imports. These measures deepened the global slump, triggering a decade of stagnation.

The collapse of Bretton Woods ended the monetary certainty of the postwar boom. Today, the global economy enters a third era of upheaval. Massive US sovereign debt, rising fiscal deficits and the weaponisation of financial sanctions have accelerated a pivot toward multipolarity. If the twentieth century saw power migrate from London to New York, the current decade witnesses its diffusion—challenging the capitalist equilibrium established eighty years ago.

The structural stability of the US-led order is increasingly undermined by the US diminishing share of global output and its continued reliance on the dollar’s ‘Exorbitant Privilege’. For decades, successive US administrations have sustained a debt pile exceeding $38 trillion through deficit financing and easy money. This model depends on the world’s willingness to absorb US Treasuries—a dynamic that functions as a hidden transfer of surplus from the global periphery to the US (Vasudevan, 2008).

The concept of US hegemony remains inextricably linked to what Valéry Giscard d’Estaing famously termed the “Exorbitant Privilege” of the US—the unique capacity to borrow in its own currency, run persistent balance of payments deficits, and finance external liabilities without the constraint faced by other nations. This privilege endures to the present day, and its persistence counsels against the assumption, prevalent in some analyses, that the dollar’s dominance is undergoing a gradual but inexorable decline (Siddiqui, 2025a).

A more nuanced reading of monetary history suggests that the trajectory of dollar hegemony is neither linear nor predetermined. The Nixon shock of 1971 offers a particularly instructive parallel. When President Nixon unilaterally suspended the dollar’s convertibility into gold, conventional wisdom anticipated the collapse of the Bretton Woods system and, with it, the dollar’s privileged position. What transpired instead was a remarkable feat of monetary alchemy: the dollar was simultaneously devalued and enhanced. The immediate effect was a reduction in the dollar’s external value, stimulating US exports, while bond yields adjusted to reflect the new regime. Yet far from diminishing the dollar’s global role, the Nixon shock inaugurated an era of renewed—indeed, intensified—dollar dominance, as the world shifted to a pure fiat dollar standard with no convertibility constraint whatsoever (Palley, et al, 2024).

This historical precedent suggests that the Trump administration’s apparent objectives—to weaken the dollar while preserving its preeminent status—may be less contradictory than they appear. The successful replication of the Nixon formula would require a delicate balancing act: inducing holders of dollars to sell, thereby depressing the currency’s external value, while simultaneously ensuring that the proceeds of those sales are not channelled into rival currencies capable of challenging the dollar’s reserve status.

The feasibility of this manoeuvre depends critically on the behaviour of other major economic actors, particularly China. More consequential is the trajectory of the yuan and the broader BRICS constellation. The critical question is whether China will pursue a strategy of simple currency internationalization—encouraging the use of the yuan in cross-border transactions—or whether it will aspire to construct a more ambitious institutional framework along the lines of a Bretton Woods system for the BRICS area (Siddiqui, 2024a). In such a system, the yuan would assume the role played by the dollar in the original Bretton Woods architecture, with China, as the surplus country, recycling its surpluses through loans, development finance, and direct aid to other countries.

The original Bretton Woods system was built precisely on these factors: the US, as the dominant surplus country, provided liquidity to the system through its balance of payments deficits and recycled its surpluses through official channels to reconstruct and integrate the EU and Japanese economies. China’s current position—running substantial trade surpluses with much of the Global South and accumulating claims on future production—bears more than a passing resemblance to the US position in 1944.

The contemporary global order is defined by the US’ capacity to impose financial blockades through its control over the dollar-based payment architecture. This choke point was starkly demonstrated in Venezuela between 2016 and 2021: following aggressive US sanctions, oil production collapsed by 75%. The subsequent economic implosion—hyperinflation and a two-thirds decline in GDP per capita—represented a humanitarian catastrophe more severe than many conventional conflicts. This model of economic crushing, recently reiterated in US policy discussions regarding Iran, confirms that access to the dollar is no longer a commercial right but a geopolitical lever.

This reality has triggered an unprecedented diplomatic realignment. In early 2026, the influx of Western leaders to Beijing—including Keir Starmer, Mark Carney, and Michael Martin—signals a departure from the unipolar era that followed the Soviet Union’s dissolution in 1991. That this marks the first visit for a Canadian Prime Minister since 2017 and a British Prime Minister since 2018 highlights the urgency of the moment. These middle powers, traditionally dependent on the US market, can no longer afford to be collateral damage in a bipolar rivalry they did not create. For an export-dependent economy like Germany, where one in four jobs relies on international trade, the risk of being caught in the crossfire of financial sanctions is an existential threat.

The current global transition is unfolding through a deliberate strategy of systemic insulation. Central banks are no longer merely diversifying; they are actively reducing exposure to long-duration US assets and expanding bilateral settlement frameworks in alternative currencies. As Mark Carney articulated at the 2026 Davos World Economic Forum, the imperative for middle powers is now one of collective agency: “If you’re not at the table, you are on the menu.”

II. The Erosion of US Hegemonic Power

A new equilibrium emerged only after the devastation of the Second World War. The US assumed the role of global stabiliser, providing essential public goods to Europe: military protection, open markets, credits, a stable reserve currency, and lender-of-last-resort functions. The dollar’s status as the global reserve currency allowed the US to borrow at lower interest rates, enjoy cheaper imports, and finance military spending through deficits (Vasudevan, 2008).

Despite robust growth during the post-war period in the West, known as capitalism’s “Golden Age,” however, the US entered a phase of relative decline. Reconstructed rivals—especially West Germany and Japan—regained industrial competitiveness, eroding the market share of US monopolies. By the early 1970s, chronic US fiscal and trade surpluses had turned to deficits. Expanding the money supply to fund foreign wars, acquire overseas assets, and fuel speculation generated systemic inflationary pressures. As a result, dollar–gold convertibility—the cornerstone of Bretton Woods—became untenable. Following speculative attacks on an overvalued currency, President Richard Nixon unilaterally suspended gold convertibility on 15 August 1971. This “Nixon Shock” effectively ended the Bretton Woods system, ushering in an era of floating exchange rates and competitive devaluations (Vasudevan, 2008).

The Nixon Shock precipitated the 1973–75 global crisis, the first of several ruptures marking the exhaustion of the postwar boom. Paradoxically, the collapse of Bretton Woods entrenched the dollar more deeply at the core of the international system.

Though no longer anchored to gold, the dollar persisted as the universal medium of exchange required by an expanding global economy. US institutions were the primary beneficiaries, yet Western ruling classes acquiesced, leveraging the US-led framework to export capital and embed themselves in global supply chains.

This “exorbitant privilege” enabled the US to run massive deficits without currency collapse—effectively taxing the rest of the world to fund US military expansion and domestic consumption. Yet the very dollar outflows that supplied global liquidity eroded confidence in gold convertibility, rendering the fixed-rate system unsustainable.

Moreover, while the Nixon Shock of 1971 forced a transition to floating fiat currencies, 2026 is witnessing a move toward Central Bank Digital Currencies (CBDCs) and a strategic resurgence in sovereign gold reserves. These developments signal a concerted effort by nations to bypass the SWIFT system and insulate their economies from the weaponisation of the US dollar.

Figure 1: The US Dollar Value Against Six Major Currencies, 2026.

By early 2026, the US dollar had retreated to its lowest valuation in four years, triggering a flight to traditional safe havens such as gold and the Swiss franc. Depreciating 1.3% against a weighted basket of currencies—and marking a cumulative 10% decline over the previous year—the downturn reflects a broader global recalibration (See Figure 1). While a weaker dollar can ease debt-servicing burdens for emerging markets, its volatile decline underscores the fragility of the dollar’s so-called exorbitant privilege (The Guardian, 2026).

This ‘exorbitant privilege’ remains a cornerstone of US economic power. Robust global demand for dollar-denominated assets—particularly US Treasuries and equities—enables US firms to borrow at preferential rates, directly bolstering capital accumulation. Moreover, the world’s appetite for US debt has historically granted the federal government exceptional fiscal latitude, allowing it to sustain persistent deficits that would trigger balance-of-payments crises elsewhere.

Furthermore, the dollar-centric architecture serves as a potent instrument of extra-territorial power. By controlling the world’s primary medium of exchange, the US can weaponise finance: seizing foreign sovereign assets, imposing comprehensive sanctions, and effectively excommunicating adversaries from the global economy. This financial statecraft ensures the US dollar remains not merely a tool of trade but a fundamental pillar of imperialist hegemony (Siddiqui, 2023a).

This economic divergence is now manifesting in the monetary sphere. By the end of 2025, the US dollar’s share of global currency reserves had fallen to approximately 57%—its lowest level since 1994 and a sharp decline from 73% in 2001. While the dollar remains dominant, facilitating 88% of foreign exchange transactions and 81% of trade finance, its status is no longer uncontested.

Yet the material foundations of the US currency and economic hegemony are eroding. The US share of global nominal GDP has stagnated at roughly 26%, while China’s share has surged from 2.5% four decades ago to over 22% by 2025. This shift is not merely quantitative but qualitative: Chinese corporations such as BYD and DeepSeek now challenge US dominance in frontier industries like electric vehicles and advanced AI, directly threatening the profit margins of established US capital.

Russia and China are actively constructing alternative financial architectures—most notably the Cross-Border Interbank Payment System (CIPS)—to bypass the SWIFT messaging network and insulate themselves from US-led sanctions. As foreign investors increasingly seek assets beyond the reach of US extra-territorial jurisdiction, the global financial system is transitioning from a unipolar dollar standard toward multipolarity.

This shift is not merely a change in destination but a total reshaping of currency and investment behaviour. Oil is no longer traded as an isolated commodity; instead, it has become the anchor for comprehensive multi-sector industrial ecosystems. Major Chinese hubs, particularly Shenzhen, are now exporting high-tech industrial equipment and infrastructure solutions to the Gulf countries that are no longer settled in dollars by default. Contracts are increasingly structured around long-term project financing, technology transfer, and digital settlement and infrastructure projects, which bypasses the SWIFT system to enable instant cross-border settlement.

China’s strategy effectively merges energy procurement with industrial integration. By bundling oil purchases with the development of 5G networks, AI infrastructure, and logistics corridors, China has repositioned itself at the centre of long-term global demand growth. This bundled integration alters exporters’ bargaining power and gradually erodes the dollar’s monopoly. As energy trade merges with industrial strategy, the resulting shift in settlement behaviour represents a decisive move toward a multipolar financial order. While the Saudi riyal remains pegged to the dollar, the kingdom has begun negotiating oil sales in alternative currencies—including the yuan—to gain better leverage. In late 2025, major energy contracts between Saudi Arabia, Iran, and China are being settled in yuan, signalling a weakening of the petrodollar’s once-absolute monopoly. (Siddiqui, 2026a).

Mainstream economists frequently underestimate the velocity of this transition by focusing on currency mechanics rather than the underlying payment architecture. The traditional petrodollar system has not merely encountered competition; it has inadvertently incentivised the construction of comprehensive alternatives. The watershed moment occurred in 2022 with the freezing of $300 billion in Russian sovereign reserves. This event demonstrated that a high concentration of reserves in US dollars represents a systemic vulnerability rather than a security. For global central banks, this single act of financial statecraft shifted the logic of reserve management from return on investment to sovereign survivability.

Simultaneously, the economic gravity of the global system has migrated toward Asia. Over the last two decades, East and Southeast Asian economies have accounted for higher economic growth and the vast majority of incremental global energy demand (Siddiqui, 2025c), with China’s consumption now exceeding that of the US and the EU combined. This shift is reinforced by national transformation initiatives, such as Saudi Vision 2030 and the UAE’s industrial diversification plans. These projects require long-term industrial partners capable of delivering integrated packages—including refineries, infrastructure and development of ports, 5G networks, and logistics corridors—rather than simple commodity buyers.

As China has emerged as the primary trading partner for these regions, it has successfully deployed parallel financial institutions. While the Cross-Border Interbank Payment System remains smaller than SWIFT, its growth is driven by bilateral trade deals—such as those with Brazil—that settle in local currencies to bypass dollar-denominated friction. This does not portend a dramatic, overnight collapse of the dollar, but rather a slow leakage of hegemony. Dominance has bred overconfidence in the West, delaying adaptation while emerging economies quietly restructure their supply chains. The result is a gradual evolution toward a multicurrency energy trade, where financial fragmentation rises not through a singular crisis, but through the rational, gradual diversification of countries seeking to insulate themselves from markets attacks.

By strategically engaging with China and fostering parallel payment architectures, these nations are moving to neutralise the risks of weaponised interdependence. This theoretical framework explains how the US, by controlling the choke points of global finance—the dollar and SWIFT—can extract concessions or effectively dismantle rival economies. However, the recent diplomatic surge in Beijing indicates a profound shift. Even core Western allies are now adopting a hedging strategy, refusing to be forced into a binary choice between superpowers. Instead, they seek to maximise their own security and economic sovereignty within a fragmented, multipolar landscape.

III. Tariffs and the Precarious Position of Foreign Creditors

The imposition of tariffs, such as those announced by the Trump administration, presents a complex and often counterintuitive dynamic for the US dollar. While tariffs are ostensibly designed to protect domestic industries and reduce the trade deficit by making imports more expensive, their immediate effect is often to boost the dollar’s value. This occurs because significant trade policy uncertainty drives global investors toward the perceived safety of US assets, increasing demand for the dollar. Consequently, the resulting currency appreciation counteracts the intended price effects of the tariffs, offsetting downward pressure on both imports and the overall trade deficit.

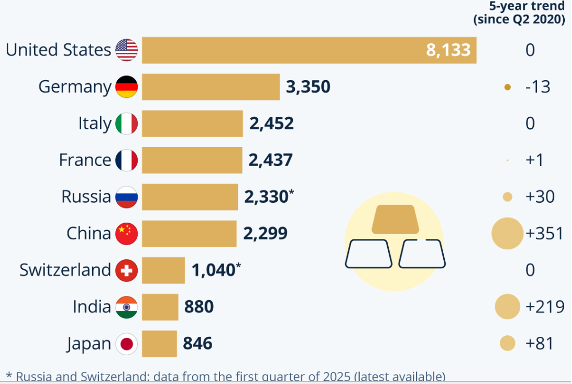

This dynamic is further complicated by concurrent domestic economic policies. Large-scale tax cuts, particularly those favouring higher income brackets and big corporations, are expected to stimulate an influx of foreign capital seeking higher returns. While this influx further strengthens the dollar, it simultaneously exacerbates the underlying structural imbalance that is the root cause of the US trade deficit: the gap between domestic savings and investment. Foreign capital flows into the US are, by accounting identity, the mirror image of the trade deficit, meaning that policies attracting such capital inherently widen, rather than narrow, the deficit.

This phenomenon underscores a fundamental paradox of the US dollar’s near-monopoly in international finance: in times of global economic uncertainty or domestic turmoil, the dollar tends to appreciate. Investors flock to the depth, liquidity, and safety of US Treasury markets, reinforcing the very currency strength that harms the competitiveness of US exports. This creates an inherent tension: the very tools used to project economic strength and protect domestic industry often reinforce the structural conditions that perpetuate the trade imbalance.

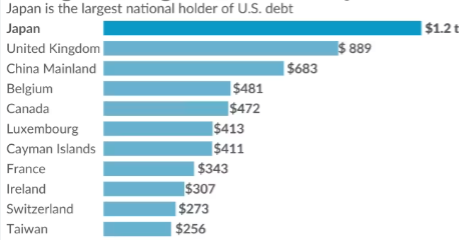

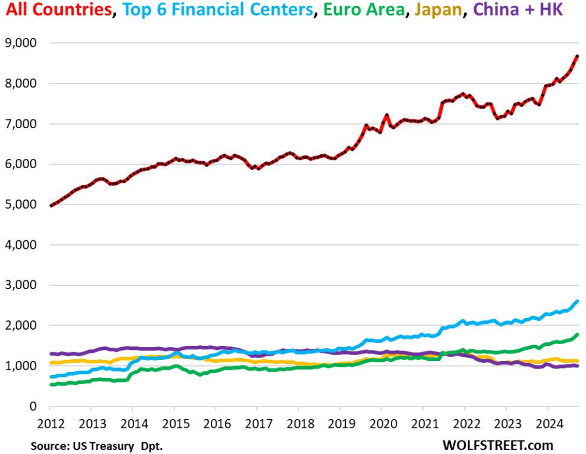

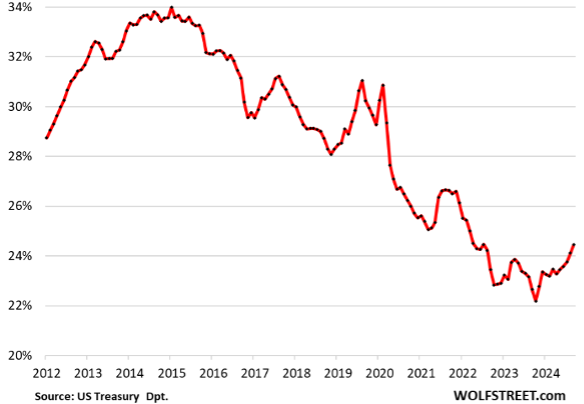

Recent data from the Treasury Department reveals a significant shift in the composition of foreign holders of US debt, challenging the conventional narrative that the US government relies primarily on Japan and China to finance its fiscal deficits (see Figure 2). According to the latest report, all foreign entities combined added $170 billion to their holdings of US Treasury securities in the most recent period, bringing total foreign holdings to a record $8.67 trillion. Notably, well over half of this increase was attributable to the Euro Area. Over the past 12 months, foreign holdings have increased by a substantial $880 billion, representing a growth rate of 15.4 percent.