By Dr. Kalim Siddiqui

I. Introduction

I examine here the role of China’s bilateral swap agreements (BSAs) and the internationalization of its currency Renminbi (RMB). A bilateral swap agreement, or cross-currency swap agreement, gives a recipient party the right to exchange their currencies at a fixed interest rate. A currency swap involves the exchange of interest and principal from one currency into another currency. We also discuss the US Dollar, which is at present the largest currency used for international trade, as a reserve currency, and in the international debt payments.

During World War II, the United States exported arms and consumer goods to the Allies and were paid in gold; thus the US was able to accumulate the world’s largest reserves of gold. After the war, countries linked their currencies to the US Dollar, which was linked to gold. The US became the lender for many countries that were willing to buy Dollar-denominated US bonds. Since World War II, the Dollar has been the world’s most important currency (Siddiqui, 2020a). It is the most commonly held reserve currency and also the most widely used currency for international trade and other transactions around the world. The centrality of the Dollar to the global economy confers some benefits to the US, including borrowing money abroad more easily and at lower costs. Although, the gold standard ended in 1971, the Dollar’s reserve status remained, and the US still has the privilege to fund massive public and private borrowing. (Hudson, 2003)

In 2020, during the Covid-19 crisis, the US external debts rose sharply; such high levels of debt might be difficult to sustain and the change could be significant in coming years. However, global demands for US Dollars remained high and at present, more than 61% of all foreign bank reserves are denominated in US Dollars, and nearly 40% of the world’s debt is in Dollars.

The US dollar continues to have largest share in international markets, but it is fragile than couple of years ago. In fact, the huge demands of the US dollar provide the US (United States) greater access to global economy. There is growing concern in the European Union too about growing US deficit in recent years. It is said that due to various reasons China may stop pegging the RMB to a basket of currencies and move towards inflation-targeting regime under more market based fluctuating exchange rate regime, especially against US dollar. If China undertakes such policy then it is expected other Asian countries will follow. It is hoped that the US dollar, which at present cater for two-third of world’s GDP, and in near future it will be halved. As Rogoff, argues (2021): “Chinese policy makers face many obstacles in trying to break away from the current Renminbi peg. But, in characteristics style, they have slowly been laying the groundwork on many fronts. China has been gradually allowing foreign institutional investors to buy Renminbi bonds, and in 2016, the International Monetary Fund added the Renminbi to basket of major currencies that determines the value of Special Drawing Rights (the IMF global reserve asset).” He further notes, “In principle, dollar transactions could be cleared anywhere in the world, but United States (US) banks and clearing houses have a significant natural advantage, because they can be implicitly (or explicitly) backed by Fed, which has unlimited capacity to issue currency in a crisis. In comparison, any dollar clearing house outside the US will always be more subject to crises of confidence – a problem with which even the eurozone has struggled.”

In 2016, the International Monetary Fund added the Renminbi to basket of major currencies that determines the value of Special Drawing Rights (the IMF global reserve asset).”

In fact, the US Dollar remains the world’s pre-eminent currency, and is widely used in international trade. Basic commodities such as oil and copper, which are produced worldwide, are generally priced in Dollars, despite that fact that, in 2016, Ben Bernanke, then chairman of the US Federal Reserve, said the nation’s declining share of a growing global economy and the rise of the Euro and Yen meant nations other than the US could also borrow at low rates (Newsweek, 2021).

Since the 1990s, the US economy has witnessed a change in its economic structure, where the manufacturing sector experienced decline, while the financial sector rose sharply. This also coincided with increased financialization of the economy and rising trade deficit. Globalisation has led to the closure of industries and falls in employment in manufacturing, whilst speculative and rentiers activities rose. The US current account deficit stems in part from growth of the financial sector and from its creation of complex and unstable financial derivatives built on risky forms of private debt. Furthermore, this “financial innovation” has itself been a response to the low growth and low profitability of the domestic productive economy (Norfield, 2012). Professor Karolyi, from Cornell University, argues: “During this period of economic uncertainty and human loss during the global pandemic, the US dollar’s role as the reserve currency of the world has been reaffirmed, …There remains robust demand for US Treasury securities at every auction, and approximately 40% of the world’s debt is denominated in US dollars,…It is hard to see this reserve status being unseated as long as the size and core engine of the US economy remains strong and the dominance of US financial markets in the global system continues.” (Newsweek, 2021)

The classical economists in the 19th century, namely Adam Smith, John Stuart Mill, Karl Marx and later on Alfred Marshall showed concerned about unearned income such as ’economic rent’ and suggested how to minimize it. At that time, the main form of ‘economic rent’ they were suggesting to minimize was ‘land rent’. The idea was to remove the landlord class, which was seen as unproductive parasitic class. At present, the rentiers are financial sector. In the advanced economies there is not a landlord class anymore, because two-thirds of Americans own (on the mortgage) their own home. The very high share of financial sector in advanced economies indicate a new concentration of wealth, engaging in a new kind of economic war, not only against labour but against government as well. This is done by getting governments into debt and then forcing them sell off the public infrastructure.

II. The Rise of the US Dollar

The Federal Reserve Bank was created by the Federal Reserve Act of 1913, in response to the instability of a currency system based on banknotes issued by individual banks. At that time, the US economy overtook Britain’s economy as the world’s largest economy. However, Britain was still the center of global business, with the majority of transactions conducted in British pounds. Also, at that time, most of the countries pegged their currencies to gold in order to create stability in currency exchanges.

However, when World War I broke out in 1914, many countries abandoned the ‘Gold Standard’ so that they could pay their military expenses with paper money, which devalued their currencies. Three years into the war, Britain, which had steadfastly held to the gold standard to maintain its position as the world’s leading currency, found itself having to borrow money for the first time. In 1919, Britain was finally forced to abandon the gold standard, which decimated the bank accounts of international merchants who traded in pounds. By then, the US Dollar had taken over the British pound as the world’s leading reserve. (Siddiqui, 2020a)

Throughout history there has been debt cancellation. There was no carryover of war debts after the war ended. In every previous war, for instance, the Napoleonic Wars and the earlier wars Britain had been involved with; the allies forgave all of their mutual debts at the end of the war. However, this was not the case after the end of World War I, and the US insisted that Germany should pay the war debts. However, J.M. Keynes argued that there was no way that debtor countries like the Allies or Germany could pay their debts to the creditor unless the creditor was willing to buy their exports, to provide them with the foreign exchange to pay.

Keynes criticised the US proposal and said Germany could not repay the war debts, but the US rejected it. Hence, Germany was forced to repay war repatriation and had to borrow money to repay the debts. The result was that the policy bankrupted Germany as it was forced to borrow from the US; the US kept Dollar interest rates low to lend more and as a result, the stock market prices rose sharply, which soon crashed. Keynes pointed out the difficulties between taxing the economy to raise a domestic fiscal surplus in German Marks and the transfer problem of paying in foreign currency. The result was bankrupting Germany, causing hyperinflation that was only solved by Germany essentially borrowing the money from the US. German municipalities borrowed the money in Dollars for local spending, and then turned over the Dollars to the Reichsbank to pay the Bank of England and the Bank of France.

At the end of World War II, in 1944, allied countries met in Bretton Wood, New Hampshire in the US, where it was decided that the world’s currencies could not be linked to gold, but they could be linked to the US Dollar, which was linked to gold. The arrangement, which came to be known as the Bretton Woods Agreement, established that the central banks would maintain fixed exchange rates between their currencies and the Dollar. In turn, the US would redeem US Dollars for gold on demand. As a result of the Bretton Woods Agreement, the US Dollar was officially crowned the world’s reserve currency and was backed by the world’s largest gold reserves.

The US had majority of the world’s gold in 1945. Under the gold standard, for countries that settled their balance of payments deficits in gold, this was really the Dollar standard, because the Dollar was defined in terms of gold. However, after the Korean War, America’s balance of payments (BoP) changed abruptly. From 1953 through the 1960s and 1970s, the US experienced a BoP deficit, which was largely due to the rise in military expenditures. The US Dollar outflows became the basis of Europe’s central bank reserves along with gold. With growing concerns over the stability of the Dollar, the countries began to convert Dollar reserves into gold, especially France and Germany.

The Dollar’s status as the leading reserve currency was called the “exorbitant privilege” of the US, by French leader Giscard d’Estaing in 1965. Over time, US trade moved into a sustained deficit, supported in part by global demand for Dollar reserves. This demand helps the US to issue bonds at a lower cost, since higher demand for a government’s bonds means it doesn’t have to pay as much interest to entice buyers, and helps to keep the cost of the US’s external debts down.

The economic shutdown during the COVID-19 pandemic, and the Federal Reserve’s injection of billions into the economy, threaten the US Dollar’s standing as the world’s reserve currency.

However, by 1970 the outflows of gold from the US led to fear that a run on the Dollar would deplete US gold reserves. In response, President Richard Nixon took the Dollar off the gold standard in 1971. About two years later, the current system of fluctuating exchange rates had replaced the Bretton Woods Agreement. This devalued the US Dollar and allowed exchange rates to fluctuate more, but it was short-lived. By 1973, the current system of mostly floating exchange rates was put in place.

During the 2008-2009 economic recession, which was sparked by the collapse of the subprime mortgage market, the US economy recovered more quickly and more strongly than the rest of the world. (Siddiqui, 2020b) As a result, US Treasury bonds were considered a safe haven, boosting prices and pushing interest rates lower, since bond prices and yields move in opposite directions.

The economic shutdown during the COVID-19 pandemic, and the Federal Reserve’s injection of billions into the economy, threaten the US Dollar’s standing as the world’s reserve currency. Some investors have moved out of Dollars and into gold, which could be seen as further evidence of the Dollar’s increasing weakness. In March 2020, the US Federal Reserve cut interest rates to 0% – 0.25% to encourage borrowing and consumer spending as the coronavirus pandemic hit.

In fact, the US has been running a BoP deficit for more than the last half a century (See Figure 1), but any other country in a similar situation has to borrow or raise exports or sell assets. The US does not need to do this because the rest of the world needs the US Dollar. It is mainly due to US economic and military domination that the world demands the Dollar. The rest of the world would like to keep Dollars in reserve and also to buy US Treasury Bonds.

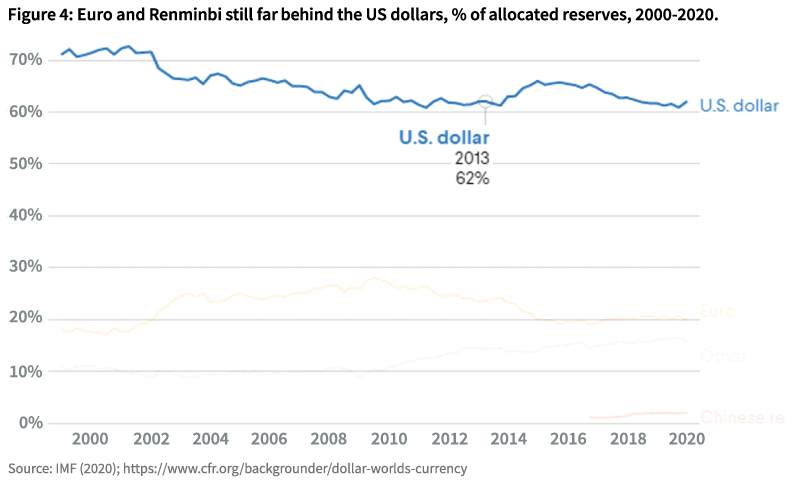

The reserve status is based largely on the size and strength of the US economy and the dominance of the US financial markets. Despite large deficit spending and a rise of trillions of Dollars in debt, treasury securities remain the safest store of money. The trust and confidence that the world has in the ability of the US to pay its debts has kept the Dollar as the most redeemable currency for facilitating world commerce. Moreover, according to the IMF, at present more than 61% of all foreign bank reserves are denominated in US Dollars. Many of the reserves are in cash or US bonds, such as US Treasuries. Also, about 40% of the world’s foreign debt is denominated in US Dollars.

Moreover, the most commonly floated alternatives are the Euro, the Renminbi, and the IMF’s Special Drawing Rights. However, these three existing alternatives have their own challenges and difficulties. The Euro is the second most used reserve currency, accounting for roughly 20% of global foreign exchange reserves. The European Union rivals the US in economic size, exports more, and boasts a strong central bank and robust financial markets – factors that make its currency a viable challenger to the Dollar. But the lack of a common Treasury and a unified European bond market limits its attractiveness as a reserve currency.

III. What is a reserve currency?

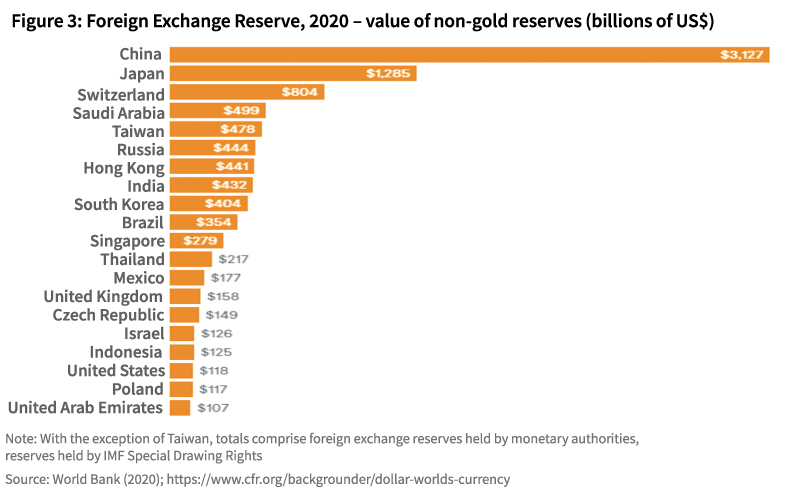

A reserve currency is a foreign currency that a central bank or treasury holds as part of its country’s formal foreign exchange reserves. Countries hold reserves for a number of reasons, including keeping safe against any unexpected economic shocks, pay for imports, service debts, and to moderate the value of its own currency (See Figure 2 and Figure 3). Major commodities such as oil are primarily bought and sold using US dollars (See Figure 4). Some countries, including Saudi Arabia, still peg their currencies to the US dollars.

Most of the developing countries find difficult to borrow money or pay for foreign goods in their own currencies. Because most of the international trade is carried out via the US dollars and therefore need to hold reserves to ensure a steady supply of imports during a crisis and assure creditors that debt payments denominated in foreign currency can be made. (Foreign Affairs, 2021)

China has by far the most reported foreign exchange reserves of any country, with more than US$3 trillion. Japan, in second place, has around US$1.3 trillion. India, Russia, Saudi Arabia, Switzerland, and Taiwan also have large reserve holdings. (Siddiqui, 2021a; also 2021b)

Moreover, the most commonly floated alternatives are the Euro, the Renminbi, and the IMF’s Special Drawing Rights. But these three existing alternatives have their own challenges and difficulties. The Euro is the second most used reserve currency, accounting for roughly 20% of global foreign exchange reserves. The European Union rivals the US in economic size, exports more, and boasts a strong central bank and robust financial markets – factors that make its currency a viable challenger to the dollar. But the lack of a common Treasury and a unified European bond market limits its attractiveness as a reserve currency.

During the Bretton Woods talks, Keynes proposed the creation of an international currency, which would be administered by an international central bank. His suggestions were not accepted but more recently, there have been calls to use the IMF’s Special Drawing Rights (SDR) – an internal currency that can be exchanged for hard currency reserves – as a global reserve currency. The value of SDR is based on five currencies: the Euro, Pound Sterling, Chinese RMB, US Dollar, and Japanese Yen. Proponents argue that such a system would be more stable than one based on a national currency whose issuer must respond to both domestic and international needs. But for SDR to be adopted widely, it would need to function more like an actual currency and be accepted in international transactions with a market for SDR-denominated debt.

However, it seems that the US Dollar will not be overtaken as the world’s leading reserve currency anytime soon. Neither Japan nor China, whose currencies to date have not been very widely used as reserve currencies, are likely to pose a real threat to the Dollar anytime soon. (Siddiqui, 2020c; 2020da) Japan has experienced stagnation for more than the last two decades and thus would not be able to challenge US Dollars hegemony. (Siddiqui, 2015a) Although the Chinese economy has started to grow again after the Covid-19 pandemic, the country is in the midst of a credit bubble of epic proportions and it continues to maintain strict capital controls that would seem to disqualify its extensive use as a reserve currency. (Siddiqui, 2020d; also 2017)

IV. China’s Bilateral Currency

Swap Agreements

The bilateral swap agreement (BSAs), also known as cross-currency swap agreement, gives a recipient party the right to exchange currencies at a fixed interest rate. BSAs are often used to both reduce the risk of currency fluctuations in times of financial volatility, and as a tool to increase cross-border trade. Countries with open capital flows are exposed to liquidity risks when their financial obligations exceed the amount of currency a country can acquire, while swap agreements allow trade activity to proceed by using a given currency to replenish foreign exchange reserves and fulfil the debt obligation.

At present, China is the second largest economy in the world and accounts for more than 40% of global trade. However, by May 2020, only 1.79% of global payments were conducted through the RMB. The US Dollar still dominates international currency markets. In recent years, China has moved to sign bilateral currency swaps. China has sought to combat US Dollar dominance and replenish offshore liquidity through its “One Belt, One Road” (OBOR) initiative, a large-scale overseas infrastructure program. (Siddiqui, 2019a and 2019c) Through ‘attractive’ loan packages, China is building new economic relations with other countries and encouraging them to use RMB. China also began signing BSAs with several countries. China has signed agreements of over US$ 500 billion with at least 35 countries to provide RMB liquidity to trade partners with drying markets to boost trade over the long-term.

China has signed BSAs to protect against liquidity crunches and it seems that China is also using it as a tool for currency internationalization. In recent years, it has signed a deal, for instance with Pakistan, and China hopes to support RMB-denominated trade by recycling currency. As Pakistan maintains a trade deficit with China, Pakistani exporters spend more RMB than importers receive, which depletes the country’s RMB reserves. In theory, if Pakistan is to be properly incentivized to continue using the RMB for cross-border trade, Pakistan’s central bank could tap of RMB credit to exchange Pakistani Rupees with the People’s Bank of China for RMB at an interest rate pre-determined by the swap agreement.

Within the last 10 years, China has entered into BSAs with an astounding 35 countries, but despite numerous agreements, very few countries have actually drawn upon their credit lines. Pakistan and Argentina have agreed and have tapped into their BSAs. During the period of BoP crisis and rising foreign debts, both counties used the agreements to obtain RMB and convert it into US$ in offshore markets. Pakistan was the first country to do so when it tapped into its US$10 billion in 2013 after seeing a sharp dip in its foreign reserves. Argentina in 2014 witnessed rapid inflation of the Peso and in deep crisis, the country was unable to obtain US Dollars to import vital consumer goods technology. Argentina drew upon its BSA with China and the RMB was used as part of a two-pronged approach by Argentina to introduce the US Dollar into its domestic economy. In both instances, China did not protest against the RMB being converted to US Dollars.

By providing liquidity during times of crisis, China has proven to be a reliable partner. This reputation may have begun to pay dividends, as the Sino-Pakistani BSA doubled from RMB 10 billion (US$1.42b) in 2014 to RMB 20 billion (US$2.84b) in 2019 and the Pakistani trade settlement in RMB surged by 250% in 2019. As recently as in March 2021, Pakistan proposed that it would further increase trade via BSA to RMB 40 billion (US$5.68b). Similarly, Argentina increased its currency swap agreement with China from RMB 70 billion (US$9.94b) to RMB 130 billion (US$18.47b) in 2019. These deals represent the progress being made on Renminbi internationalization and the potential for bilateral trade to expand in the future as China remains a strong and dependable financial partner.

In Russia, with the western sanctions, the value of the Russian Rouble fell sharply and the country saw an opportunity to increase bilateral trade agreements in local currencies with China. With the Chinese BSAs, Russia was able to subvert US-imposed sanctions, as sanctions largely target operations that use the US Dollar. When Russian transactions were conducted in an alternative currency, they were able to bypass any restrictions. The increase in Chinese and Russian trade was ostensibly driven by Russia’s intent to employ a strategy to undermine US economic and trade sanctions. Russia and China in 2014 signed a three-year currency swap deal worth 150 billion RMB ($24.5 billion). The agreement allows each country’s central bank to gain access to the other’s currency without trading via the US Dollar. Russia, previously a top holder of US sovereign debt, has radically decreased its holdings because of sanctions. Russia’s strategic relations with China deepened after the 2014 partnership and energy-centred agreements. In 2017, Rouble-Renminbi ‘payment versus payment’ started along the OBOR. In 2019, the two countries switched to the Renminbi and Rouble exchange for their US$ 25 billion trade.

In 2020, Turkey too, amidst the rising conflict with the US, signed a number of bilateral economic and trade agreements with China. For example, a US$1.7 billion BSA was signed between the two countries that represented approximately 8% of the total US$21.08 billion trade between the two nations in 2019. With a sharp decline in the value of Turkish Lira in 2019, the government attempted to prop up the Turkish Lira. Turkey had desperately depleted its foreign exchange reserves and sought help from financiers like the IMF and the US. According to the Turkish central bank, while the move was economically motivated, the influx of RMB ultimately increased the RMB-denominated trade settlement.

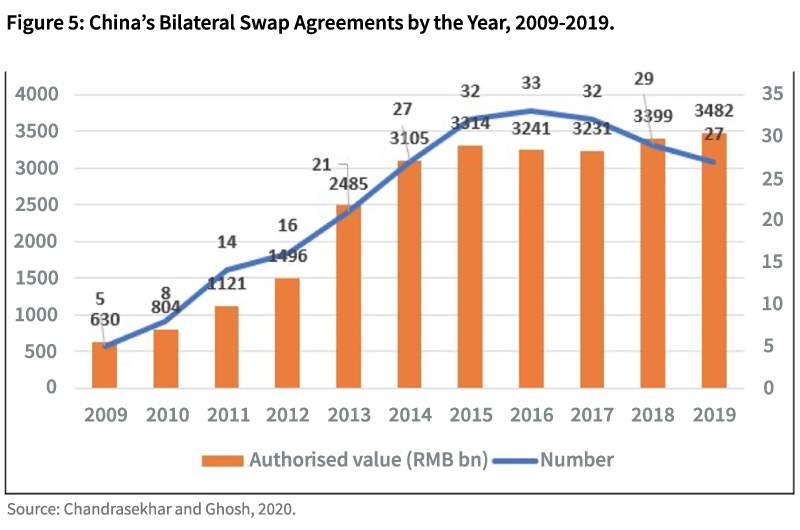

During the last ten years, the Peoples Bank of China has entered into bilateral swap arrangements with 41 countries (See Figure 5). Despite the slight decline in the number of active arrangements between end-2016 and end-2019, the total authorised value of such arrangements has been relatively stable, averaging RMB 3,333 billion between 2015 and 2019. (Chandrasekhar and Ghosh, 2020)

Given the importance of China as a provider of goods and a source of investments and credits to many developing countries, and its effort to internationalise the RMB by designating an increasing share of those transactions in RMB instead of dollars, these swaps suit both China and its partners. (Chandrasekhar and Ghosh, 2020) For example, recently China has signed free-trade agreement with 16 Asian countries and the potential pact is expected to form a union of nearly 3.4 billion people based on a combined US$ 49.5 trillion economy, which accounts for nearly 40% of the world’s GDP.

China is internationalising the RMB which is included in IMF basket, and currently it has risen to fifth place as global currency and represents 15% of global currency holding. Russia has 25% of Chinese RMB international reserves. Of course, the problem remains that the RMB is not deep, open and liquid enough for financial markets. At the same time, most countries would not want the Renminbi to become a mirror image of the dollar in its ability to manipulate financial sectors.

Dimitri Simes (2020) notes, that Russia and China have drastically cut their use of the US Dollar in their bilateral trade over the past several years. As recently as 2015, approximately 90% of bilateral transactions were conducted in Dollars. Following the outbreak of the US-China trade war, and a concerted push by both Russia and China to move away from the Dollar, however, the figure dropped to 51% by 2019. De-dollarization has been a priority for Russia and China since 2014; replacing the Dollar in trade settlements became a necessity to sidestep US sanctions against Russia. The process gained further momentum after the Trump administration imposed tariffs on hundreds of billions of Dollars’ worth of Chinese goods. Russia and China signed a deal in 2019 to replace the Dollar with national currencies for international settlements between them. The biggest beneficiary of this move was China, which saw its share of Russia’s foreign exchange reserves jump from 5% to 15% after the central bank invested US$44 billion into Chinese currency. As a result of the shift, Russia acquired a quarter of the world’s Renminbi reserves.

China is trying to internationalize its own currency, the Renminbi, which was included in the IMF basket alongside the US Dollar, the Japanese Yen, the Euro, and the British Pound. It has recently made several steps towards strengthening the Renminbi, including accumulating gold reserves, launching Renminbi-priced crude futures, and using the currency in trade with international partners.

Turkish President Erdogan attempted to end the US Dollar monopoly via a new policy that is aimed at non-Dollar trading with the country’s international partners. Later, Turkey’s leader announced that his government was preparing to conduct trade through national currencies with China, Russia and Ukraine. Turkey also discussed a possible replacement of the US Dollar with national currencies in trade transactions with Iran. Donald Trump opted to withdraw from the 2015 nuclear deal signed between Iran and 5+1 other countries (i.e., the US, UK, France, Germany, Russia and China). Iran has once again become a target for severe sanctions resumed by Washington. Sanctions have forced Iran to look for alternatives to the US Dollar as payment for its oil exports.

V. Conclusion

The ongoing trade conflict between the US and China, as well as sanctions against China’s biggest trading partners have forced China to take steps towards relieving the Dollar dependence of the China.

The Chinese economy, despite the adverse impact of Covid-19, has again begun to grow faster than US and other EU countries, and the Chinese RMB is coming under increased pressure to adopt a flexible exchange rate. China has introduced swap facilities in participating countries to promote the use of the Renminbi. The BSAs seem to be an instrument to encourage other countries to increase reliance on Chinese goods and on RMB loans to buy them. Hence, enhancing its economic influence, as well as furthering the goal of internationalising the RMB and establishing it as an alternative reserve currency.

The ongoing trade conflict between the US and China, as well as sanctions against China’s biggest trading partners have forced China to take steps towards relieving the Dollar dependence of the China. The People’s Bank of China has been regularly reducing the country’s share of US Treasuries. Still the number-one foreign holder of the US sovereign debt, China, has cut its share to the lowest level since May 2017.

China has also been trying to increase the role of the Renminbi as a global reserve currency. It currently accounts for only 2% of global reserves, and China has strict controls on the flow of money through its economy, but global usage of the RMB has been steadily increasing. China is also pushing to increase the use of the Renminbi to denominate its own trade. There is a greater possibility that in the next decade the international economy will be shared by three currencies: namely US Dollar, Euro and Renminbi.

Historically, the global demand for gold increased in 1970, and then in 1971 the US President Nixon intervened to de-link the Dollar from gold, which led to the floating exchange rates that exist today. After the 1973 oil crisis, US political and economic power ensured that OPEC surpluses were recycled through the private channels of the Eurodollar markets. As the Dollar-denominated surpluses of the OPEC countries came to be recycled through this market in the 1970s, the market grew to be a full-fledged capital market, expanding from US$9 billion in 1964 to US$145 billion in 1971 and $1.4 trillion in 1981 just before the global debt crisis unravelled in the mid-1980s.

A question arises about the Dollar’s worthiness as a reserve currency. There are three implications here: First, the argument is not that the Dollar should be completely displaced, since even in the basket that constitutes the SDR, the Dollar commands an influential role. Second, there is no other country or currency that is at present seen as being capable of taking the place of the US Dollar in the near future. And, third, the search is not for a currency that can be used with confidence as a medium for international exchange, but for a derivative asset that investors can hold without fear of a substantial fall in its value when exchange rates fluctuate, because its value is defined in terms of, and is stable relative to, a basket of currencies. What is needed is an accepted currency of exchange which would also serve as a relatively stable store of value, to be held as a reserve or as a stock in order to settle future flow requirements.

Global tensions caused by economic sanctions and trade conflicts triggered by the US have forced targeted countries to take a fresh look at alternative payment systems currently dominated by the US Dollar (Siddiqui, 2018; also 2019d). The answer is that to some extent there needs to be gold as a means of settlement. However, China, Russia, Iran, and other countries are going to mutually hold each other’s trading currencies. They are replacing Dollars with gold and with each other’s currencies. That essentially is the response that the world could have taken after World War I, but did not, and could have taken after World War II if it had followed Keynes’s policies.

The study has found that the US will certainly try hard to keep as many as countries possible within US Dollar dominated transactions just as Britain did at the end of the 19th century as the world’s then-largest trading country. However, China long ago surpassed the US as the top trading nation of the world. Chinese currency Renminbi will not become a global currency overnight; evolving into a global currency could take a longer period. Between World War I and World War II, the US Dollar became an international currency and then had about the same weight in central bank reserves as the British Pound Sterling, which had dominated the international currency reserves since Napoleonic wars; nevertheless, the US Dollar finally replaced the British Pound Sterling in 1944.

About the Author

Dr. Kalim Siddiqui is an economist, specialising in International Political Economy, Development Economics, International Trade, and International Economics. His work, which combines elements of international political economy and development economics, economic policy, economic history and international trade, often challenges prevailing orthodoxy about which policies promote overall development in less developed countries. Kalim teaches international economics at the Department of Accounting, Finance and Economics, University of Huddersfield, U.K. He has taught economics since 1989 at various universities in Norway and U.K.

Reference:

- Chandrasekhar, C.P. and Ghosh, J. (2020). “Bilateral Swaps in China’s Global Presence”, Business Line, December 15.

- Foreign Affairs. (2021) “The Dollar: The World’s Currency”. https://www.cfr.org/backgrounder/dollar-worlds-currency

- Hudson, M. (2003). Super Imperialism: The Origin and Fundamentals of US World Dominance, London: Pluto Press.

- Newsweek. (2021). “Will the US Dollar Lose Its Place as the World’s No. 1 Reserve Currency?” May 19, New York. https://www.newsweek.com/will-us-dollar-lose-its-place-worlds-no-1-reserve-currency-1567224

- Rogoff, K. (2021). “The US dollar’s hegemony is looking fragile”, Guardian, April 2, London.

- Simes, D. (2020). “China and Russia Ditch Dollar in Move towards Financial Alliance”, Financial Times, August 16, London.

- Siddiqui, K. (2021a). “Can 21st Century be an Asian Century?” Asian Profile, 49(1): 1-19, March.

- Siddiqui, K. (2021b). “Trade Liberalisation, Comparative Advantage, and Economic Development: A Historical Perspective”, World Financial Review, May-June, pp.

- Siddiqui, K. (2021c). “The Importance of Industrialisation in Developing Countries”, World Financial Review, January February, pp.60-73.

- Siddiqui, K. (2020a). “The US Dollar and the World Economy: A critical review”, Athens Journal of Economics and Business, 6(1): 21-44. January.

- Siddiqui, K. (2020b). “Can Global Imbalances Continue? The State of the United States Economy”, Argumenta Oeconomica Cracoviensia, 23(2): 11-32.

- Siddiqui, K. (2020c). “Prospects of a Multipolar World and the Role of Emerging Economies”, World Financial Review, November/December, pp. 65-77.

- Siddiqui, K. (2020d). “The Rise of the Chinese Economy and Growing Concerns in the US”, World Financial Review, September/October, pp. 40-49.

- Siddiqui, K. (2019a). “The Political Economy of Essence of Money and Recent Development”, International Critical Thought, 9(1): 85-108.Routledge.

- Siddiqui, K. (2019b). “The US Economy, Global Imbalances under Capitalism: A Critical Review”, Istanbul Journal of Economics, 69(2): 175-205, December.

- Siddiqui, K. (2019c). “One Belt and One Road, China’s Massive Infrastructure Project to Boost Trade and Economy: An Overview”, International Critical Thought, 9(2): 214-235. Taylor & Francis Group, Routledge.

- Siddiqui, K. (2019d). Financialisation, Neoliberalism and Economic Crises in the Advanced Economies, World Financial Review, May/June, pp.22-30.

- Siddiqui, K. (2018). “US – China Trade War: The Reasons Behind and its Impact on the Global Economy”, World Financial Review, November/December, pp.62-68.

- Siddiqui, K. and P. Armstrong. (2017a). “Capital Control Reconsidered: Financialization and Economic Policy”, International Review of Applied Economics, 32(6): 1-19, March.

- Siddiqui, K. (2017b). “Financialization and Economic Policy: The Issues of Capital Control in the Developing Countries”, World Review of Political Economy, 8 (4): 564-589, winter.

- Siddiqui, K. (2016). “Will the Growth of the BRICs Cause a Shift in the Global Balance of Economic Power in the 21st Century?” International Journal of Political Economy, 45(4): 315-338, Routledge.

- Siddiqui, K. (2015a). “Political Economy of Japan’s Decades Long Economic Stagnation”, Equilibrium Quarterly Journal of Economics and Economic Policy, 10(4):9-39.

- Siddiqui, K. (2015b). “Foreign Capital Investment into Developing Countries: Some Economic Policy Issues”, Research in World Economy, 6(2): 14-29.

- Siddiqui, K. (2009). “The Political Economy of Growth in China and India”, Journal of Asian Public Policy, 1(2): 17-35, March, Routledge.

- World Bank. (2017). Global Economic Prospects: A Fragile Recovery, June. World Bank: Washington DC.