The expanding digital landscape and wave of high-impact cyberattacks have prompted governments worldwide to intensify their efforts in cybersecurity regulation. This challenge presents an opportunity. Rather than viewing this process as a tick-box exercise, businesses should focus on addressing the underlying issues of visibility and complexity.

The expanding digital landscape and wave of high-impact cyberattacks have prompted governments worldwide to intensify their efforts in cybersecurity regulation. The EU’s NIS2 directive, implemented by most member states last year, largely mirrors the USA’s Zero Trust mandate, while the UK is preparing to introduce its own Cyber Security and Resilience bill by late 2025.

Stronger regulation is a welcome step, but it is not without challenges. Ten months after the NIS2 enforcement, many businesses are still struggling to meet its rigorous standards. The complexity and scale of modern IT environments often leave organisations without the visibility needed to implement effective governance controls, making regulations seem daunting.

But this challenge presents an opportunity. Rather than viewing this process as a tick box exercise, businesses should focus on addressing the underlying issues of visibility and complexity. By solving these foundational problems, compliance becomes a natural outcome, not just a regulatory requirement.

Diagnosing complex IT environments

According to the European Union Agency for Network and Information Security (ENISA), the primary obstacle to meeting NIS2 regulations is the complexity of modern supply chains and infrastructure, particularly those involving third-party data and a limited view of cloud-based environments. While cloud computing offers huge advantages, its rapid adoption, alongside the explosive growth of the Internet of Things (IoT), has introduced significant challenges.

By late 2024, the number of connected devices worldwide had surged to 16.6 billion, dramatically expanding the attack surface and adding layers of complexity to IT estates. The cloud, while enabling seamless third-party collaboration, also introduces new security risks. NIS2 rightly addresses this by mandating stricter controls over third-party applications and data sharing.

An over-reliance on technology that was once fit for purpose compounds the issue. Many organisations still rely on networking solutions like Software Defined Wide Area Networks (SDWANs), originally built for on-premises environments. In isolation, SDWAN struggles to support the increasingly dynamic nature of accessing data from of any device, to any place storing data, both private and public cloud., often obscuring visibility and complicating governance. In effect, businesses are trying to secure their digital assets without a clear view of what those assets are, a major barrier to both compliance and security.

To meet the demands of today’s threat landscape, businesses must ‘turn on the lights.’ That means investing in modern solutions that enable proactive governance. Only then can organisations secure their attack surfaces and build compliant networks.

Securing cloud environments

Visibility and strong network governance are key drivers of effective compliance. The first step is controlling access in cloud environments, something that isolated SD-WAN solutions struggle to achieve. Instead, organisations should adopt a more holistic, cloud-native approach through Secure Access Service Edge (SASE). SASE builds on the access control strengths of SD-WAN but goes further by integrating advanced security capabilities directly into the cloud. It combines networking and security into a unified framework, enabling granular access controls and consistent policy enforcement across distributed environments.

Crucially, SASE makes cloud-native assets visible, making it easier to identify and mitigate cyber risks. This lays the groundwork for strong governance and is essential for meeting the demands of modern frameworks like NIS2. Moreover, enhanced visibility and access control make it far easier to implement Zero Trust architectures, which are vital for preventing unauthorised access and stopping threats before they spread.

Establishing efficient network governance

The next step is applying precise and effective network controls, and microsegmentation is one of the most powerful tools available. Microsegmentation divides cloud-native networks into segregated and secure zones, making it easier to enforce tailored security and access policies.

Think of it like a house: each room has its own door and light switch. Access to each room requires reauthentication, and the controls within can be customised based on the sensitivity of the data or the function of the zone. This structure not only strengthens Zero Trust architecture but also limits the impact of potential breaches by preventing lateral movement across the network.

More importantly, microsegmentation simplifies control. It gives networking and security teams a clear framework to apply the right protections in the right places, streamlining risk mitigation as a result. This is especially critical in sectors like retail and finance, where sensitive customer and personal data is at stake. By isolating and securing these high-risk areas, organisations can significantly reduce the likelihood of a major breach.

Treating compliance as an opportunity

In line with the increase in everyone’s digital footprints, so attack surfaces are expanding rapidly, and many businesses remain underequipped to meet the challenge. Rising regulatory demands are not just a compliance issue; they are a wake-up call to take control of increasingly complex IT environments, and that control starts with visibility.

Businesses need to approach regulation as an opportunity to address foundational security challenges like fragmented infrastructure, poor visibility and outdated controls. By investing in the right frameworks and technologies, businesses can build safer, more resilient networks.

Jonathan Wrightis Chief Product Officer at GCX Managed Services, where he leads the business transformation strategy and the expansion of all its lines of business.

After a catastrophic accident, medical care takes center stage for those who have been injured. Few know that a ripple effect is created and extends far beyond the hospital walls. When tallied up, severe injuries, once properly treated, create widespread economic disruption that impacts housing markets, strains community resources, and threatens household stability. This article is written to aid businesses, policymakers, and those in small or large communities to understand how these incidents link and create financial consequences that affect the economy.

The Hidden Scale of Catastrophic Injury Economics

We ask readers to take a moment to observe the recent studies highlighting America’s injury crisis. In 2023, preventable injuries led to 222,698 deaths, resulting in a death rate of 66.5 per 100,000. Survivors often suffer from moderate to severe brain damage, spinal injuries leading to paralysis, critical burn wounds, and other conditions that forever alter their lives.

During the last decade, preventable injury deaths have increased by 78%, indicating an economic and medical crisis. There is a dramatic increase in catastrophic injuries, suggesting that traditional safety measures and economic support are no longer adequate.

Household Financial Collapse: The First Economic Casualty

The economic and physical effects of a catastrophic injury can devastate a household. Loss of primary income creates the most immediate crisis. In contrast to temporary disabilities that usually allow workers to return to work, catastrophic injuries often result in a permanent exit from the labor market. When a construction worker suffers a severe spinal cord injury, they lose a lifetime of earning potential, retirement contributions, and career advancement opportunities.

Home modifications can easily exceed six figures when a wheelchair-accessible bathroom is required, specialized equipment is needed, or ongoing home care services are needed.

Besides losing its primary source of income, the family can become swamped with massive new expenses. Those caring for a loved one after a catastrophic injury can experience significant repercussions, not just in terms of their routine but also in terms of their financial security. Each year, work disruptions related to caregiving responsibilities cost employees an average of $2,110 in productivity losses per year, according to a joint report by the Family Caregiver Alliance and the National Alliance for Caregiving. This figure gives a glimpse of how caregiving places a financial burden on the workforce and how households can feel the strain quickly.

The joy of coming home can quickly become a source of anxiety to families when they realize their home is no longer livable, let alone learn of the costs to do so. In truth, home modifications can easily exceed six figures when a wheelchair-accessible bathroom is required, specialized equipment is needed, or ongoing home care services are needed. What catches most families off guard is that insurance rarely covers the modifications.

Sadly, many are forced to drain their savings or exhaust family resources to make their homes livable again. We’ve seen too many cases where insurance policies contain fine print exclusions that leave families financially exposed exactly when they need protection most. The insurance company that gladly collected premiums for years suddenly finds reasons to limit coverage when you need it.

The Productivity Drain on Local Economies

There are approximately 24.8 million physician visits and 26.2 million emergency department visits every year that stem from serious injuries. Each one represents not just personal suffering but massive productivity losses that drain local economies.

To illustrate, take the case of an engineer who suffers permanent disability—suddenly, construction projects grind to a halt, companies scramble to find replacement expertise at premium rates, and some businesses eventually relocate to find the talent they need. The damage spreads quickly. The restaurants where that engineer grabbed lunch, the retail stores where their family shopped, the service providers they relied on—all feel the impact when spending power vanishes overnight.

The transport sector provides an obvious example of disruption. Severe accidents on major transportation routes require immediate medical care and emergency responses. These accidents can disrupt supply chains, delay deliveries, and increase shipping costs—negatively impacting local businesses for months or even years.

Healthcare System Strain and Resource Allocation

Every time we walk into a hospital on behalf of a catastrophic injury client, we see the strain on our local healthcare system. Emergency rooms, trauma centers, and rehabilitation facilities need expensive equipment and highly specialized staff—costs that are passed on to everyone through higher insurance premiums and healthcare costs.

A glance at recent statistics in the US uncovers further proof of this impact. In 2023 alone, 52.6 million Americans sustained serious injuries requiring everything from emergency treatment to months of rehabilitation. That volume overwhelms healthcare systems and drives up costs for entire communities. In rural and smaller urban areas, trauma facilities may not exist, leading to expensive medical transport and capacity challenges in nearby metropolitan areas.

Healthcare workforce shortages compound these issues. Traumatic injuries require neurosurgeons, rehabilitation specialists, and trauma nurses—roles that demand significant community investment in training. Many areas face an impossible choice: spend enormous amounts expanding local capacity or accept that their residents will need expensive out-of-area care when tragedy strikes.

Insurance Markets and Risk Distribution

Catastrophic injuries significantly impact regional insurance markets, affecting households and business operations. Communities with higher injury rates are hit with premium increases across the board—health insurance, disability coverage, workers’ compensation, and liability insurance. Businesses in high-risk areas, such as manufacturing or construction regions, may face much higher insurance costs than those in safer areas. This economic disadvantage can drive companies to relocate, further weakening local economic bases.

Insurance companies have completely restructured their approach over the past decade as injury rates keep climbing. Communities with rapidly increasing injury rates may fall into a cycle of higher premiums, which discourage business investment and, in turn, limit economic growth, reducing tax revenue..

Economic Recovery and Long-term Community Resilience

Specific communities can weather catastrophic injury crises far better than others. This is not because of luck but instead because of purposeful intent when making decisions. They focus on creating strong safety-net programs, diversifying their economic base, and prioritizing injury prevention. Although these investments cost money upfront, they pay for themselves through reduced healthcare spending, improved workforce productivity, and the ability to attract new businesses within their safer community.

Our experience has taught us that proper legal representation makes all the difference. When families secure fair compensation after catastrophic injuries, that money stays in the local economy. Families maintain their spending power instead of draining public assistance programs. The ripple effects strengthen entire communities.

The smartest investment any community can make is prevention. Towns that upgrade infrastructure, implement serious workplace safety programs, and fund public health initiatives consistently transform their injury rates. The prevention costs are nothing compared to what communities spend managing the long-term consequences of major accidents.

Policy Implications and Economic Solutions

Catastrophic injuries create economic shockwaves that demand coordinated responses across multiple sectors. For example, healthcare policy must balance emergency care capacity with cost management, and economic development strategies should put injury prevention at the center, not treat it as an afterthought.

The ability to recover economically from catastrophic injuries depends on securing proper legal representation.

Smart zoning and infrastructure policies can slash injury risks while promoting economic growth. Incentive programs work when they favor businesses with proven safety records and comprehensive employee protections. Communities that develop comprehensive injury prevention strategies benefit immediately and for decades to come.

As injury rates continue to rise, comprehensive prevention and response strategies are urgently needed. Adequate preparation helps families and communities maintain long-term economic stability.

Protecting Your Household’s Economic Future

The ability to recover economically from catastrophic injuries depends on securing proper legal representation. Families are often left financially vulnerable when insurance companies minimize settlements or deny coverage for long-term care.

A skilled personal injury lawyer can help families navigate complex insurance systems and secure resources for ongoing medical care, ensuring households receive the financial protection needed to stay stable and recover over time.

O’Brien & Zehnder Law Firmhas an exemplary track record of winning millions of dollars for individuals and families in Elk Grove, California, impacted by catastrophic injuries. Since its founding in 1996, the firm has built a reputation for achieving justice across a wide range of personal injury cases. With a focus on excellence in representation and genuine care for clients, O’Brien & Zehnder Law Firm continues to stand as a trusted ally for those navigating the most challenging moments of their lives.

Europeans are finally coming to grips with the reality that high-intensity warfare between developed, symmetrical countries was not simply eradicated with the end of WWII. Leaders have also woken up to the fact that the continent’s deep precision strike capabilities are inadequate if an aggressor knocks down their door.

Russian and Ukrainian forces have been battling it out for almost four years, marking the return of high-intensity warfare: meaning significant losses, occurring over a sustained period of time and with constant skirmishes over superiority on land, in the air and at sea. One study from The French Institute of International Relations observes: “since the winter of 2023, the stalemate on the Ukrainian front has prompted the belligerents to make greater use of deep precision strikes, in search of a military effect that has become impossible to achieve on the front line”.

Ukraine’s manpower, military budget and arms stockpiles were vastly inferior to Russia’s at the beginning of the conflict, but impressive determination and resourcefulness have helped develop deep precision strike (DPS) capabilities that might turn the tide. And Russian citizens felt the repercussions recently as they faced drastic fuel shortages and record-level gasoline prices – a result of Ukraine’s campaign to bomb Russia’s oil infrastructure and hurt Putin’s war economy. Reuters reports that Ukraine’s long-range strikes have neutralised 17% of Russia’s oil refining capacity in August. This intensive use of deep strikes has raised awareness among European leaders: not only are their countries vulnerable to such threats, but they also have very limited capabilities in this area.

The conflict, amongst others, has demonstrated Europe’s need to have robust air defence systems (IAMD/A2AD) and an array of DPS armaments capable of neutralising high value targets (HVTs) including key people, infrastructure and command centres located far beyond front lines. Beyond their immediate, potential or observed military effect, DPS weapons are an essential tool for STRATCOM due to the fact that by simply having them in one’s arsenal, they serve as a deterrence – of dissuading potential aggressors from crossing the red line.

DPS in Action

While Ukraine has mostly relied on long-range unmanned aerial vehicles (UAVs) for hitting HVTs, they have also been developing long-range cruise missiles that are faster, capable of inflicting greater damage and more difficult to shoot down than UAVs. Ukraine upgraded its Neptune anti-ship missile into a new long-range cruise missile and used it last March to hit an oil refinery in Tuapse, causing a fire that took three days to extinguish. As Ukrainian MP Roman Lozinskyi remarked, “In essence, Putin has quietly confirmed to Trump how much our deep strikes are hurting the Russian energy sector. This is our trump card.” And Ukraine now has a big, new trump card to play.

Ukraine’s Fire Point defence company recently unveiled its Flamingo FP-5, a long-range cruise missile that can carry a one-ton warhead over 3,000 kilometres. Iryna Terekh, Fire Point’s CEO, says the company aims to produce 200 per month and, “We watched Russian reaction to our first missions, and I can tell you the more successful the mission was, the more Russians tried to choke all publicity around it.”

Terekh also highlights another fundamental role of DPS capabilities – to deter. David Kirichenko from the Atlantic Council argues that the sheer size of Russia means its air defence systems cannot defend the whole country from DPS so, “Kyiv policymakers are hoping that if Putin is confronted with a bloody stalemate in Ukraine and the prospect of mounting attacks inside Russia, he may be forced to rethink his current uncompromising stance and seek a settlement to end the invasion.”

Regardless of Ukraine’s future ability to produce these missiles and use them effectively, the Flamingo epitomises the various strengths in owning deep strike capabilities: the ability to physically hit where it hurts, to leverage this as an effective communications tool, using it as a bargaining chip and deterrent from future aggression.

In the Middle East, Iran’s significant arsenal of ballistic and cruise missiles could not deter Israel’s hawkish government from attacking in June because they claimed adding a nuclear weapon to Iran’s arsenal was too imminent. After twelve days of precision strikes, Israel neutralised HVTs in Iran including nuclear scientists, top military brass, missile production facilities and nuclear sites.

The last time Europe truly used its limited DPS abilities was in 2018 during the Hamilton Operation to punish Syria’s then-president Bashar al-Assad for crossing the red line of using chemical weapons against civilians. On April 14th, British, French and American forces successfully destroyed Syrian facilities storing chemical weapons by firing European-made, long-range Storm Shadow (SCALP in French) cruise missiles from the air and five MdCN naval cruise missiles (with a range greater than 1000 km) by sea. Storm Shadow missiles have since been provided to Ukraine by France and the UK.

Changing Geopolitical Realities, Changing Needs

As if the Russian threat were not enough, Europe has had to face the new reality that America is no longer interested in defending freedom and democracy on the continent at today’s cost.

Some leaders lament or try to circumvent transatlantic abandonment. Germany is debating purchasing an American-made Typhon system and Tomahawk missiles (also recently purchased by the Netherlands). EU countries buying American argue it’s faster than developing European-made solutions, but Fabian Hoffmann from the University of Oslo observes, “Only a sustained, long-term missile industrial effort can get Europe back on track in the missile domain. This requires acknowledging that modern war demands thousands of conventional long- and deep-strike capabilities, backed by a robust and continuous order intake.”

Other EU leaders are embracing the opportunity to build European security. France’s President Macron has been promoting European industrial and technological sovereignty and Poland’s Prime Minister Tusk bluntly said last spring, “I will repeat once again what seems incredible but is true: 500 million Europeans are begging 300 million Americans to protect us from 180 million Russians who have not been able to cope with 40 million Ukrainians for three years.”

Luckily, it appears all leaders have woken up to the fact that EU member states must build the DPS capabilities required to deter and defend a Russian, or other, aggression. France and the UK recently signed the Lancaster House 2.0 agreement to order “new Storm Shadow/SCALP missiles following their successful use by Ukraine, upgrading UK and French production lines to bolster national stockpiles to deter adversaries.” They also agreed to begin the development phase (with Italy) of the Future Cruise and Anti-Ship Weapon (FC/ASW) programme, led by European MBDA, to “develop a low observable cruise missile and a highly manoeuvrable supersonic munition.”

The Dutch Ministry of Defence recently announced it is joining the Spanish-led ‘Joint Strike Missile – Submarine Launched’ programme. The new submarine-launched missile is based on the Joint Strike Missile (JSM) from Norwegian Kongsberg Defence & Aerospace. JSM was an evolution from the proven ship- and land-based anti-ship missile Naval Strike Missile (NSM).

Meanwhile, a report from IISS observes that “European countries possess air- and sea-launched cruise missiles; however, no European NATO member has a ground-launched cruise missile having a range of more than 300km except Turkey.” The European Long-Range Strike Approach (ELSA) initiative aims to fill that European capability gap (amongst others) by uniting France, Germany, Poland, Italy, the UK, Sweden and the Netherlands. MBDA’s Land Cruise Missile (LCM), based on its battle-proven naval cruise missile (MdCN), is seen as a prime candidate for a pan-European solution. Regarding ELSA, Sweden’s Defence Minister Pål Jonson maintains, “The lesson learned from the war in Ukraine is that long-range strike capabilities are becoming increasingly important on the battlefield, and of course, also with stronger air defence capabilities.”

These efforts will take a lot of time, and money, to develop. When unveiling her €800 billion “ReArm Europe” plan in May, EU Commission President Ursula von der Leyen, claimed that, “This is Europe’s moment and we must live up to it.“If Ukraine can use ingenuity and determination to build its own deep strike capabilities, shouldn’t Europe be able to do the same?

Disclaimer: The views and opinions expressed in this article are solely those of the author and do not necessarily reflect the official policy or position of the journal or its affiliated organizations. The journal does not endorse or guarantee the accuracy or completeness of the information presented in this article. Readers should use their own discretion and judgment when interpreting the contents of this article.

ABC pulled “Jimmy Kimmel Live!” off the air on Wednesday “indefinitely” following the host’s controversial comments linking the alleged killer of conservative activist Charlie Kirk to former President Donald Trump’s MAGA movement.

The decision came hours after Federal Communications Commission Chair Brendan Carr warned that ABC’s broadcast license could be in jeopardy. ABC, which is owned by Disney, confirmed the suspension in a statement Wednesday night. A person familiar with the situation told CNBC that Kimmel has not been fired but will remain off the air until further notice.

Nexstar Media Group, which owns about 10% of ABC affiliates, said earlier in the day that it would no longer carry Kimmel’s program “for the foreseeable future” in its markets. Nexstar is currently seeking FCC approval for a $6.2 billion merger with Tegna, which owns about 5% of ABC affiliates.

In his Monday night monologue, Kimmel suggested that Tyler Robinson, accused of killing Kirk on Sept. 10 at Utah Valley University, was aligned with Trump’s movement. “The MAGA Gang desperately trying to characterize this kid who murdered Charlie Kirk as anything other than one of them and doing everything they can to score political points from it,” Kimmel said.

Carr, appointed to the FCC under Trump, called Kimmel’s comments “truly sick” and warned ABC and Disney that “we can do this the easy way or the hard way.” He suggested the network’s broadcast license could face scrutiny if it did not act.

Trump celebrated the suspension, posting on Truth Social that ABC had “finally had the courage to do what had to be done,” and urged NBC to cancel its own late-night shows hosted by Jimmy Fallon and Seth Meyers.

The White House rapid response account on X also weighed in, calling Kimmel a “sick freak.” Meanwhile, FCC Commissioner Anna Gomez, a Biden appointee, condemned the move, warning that government pressure on speech risked undermining free expression. “Free expression is non-negotiable,” she wrote on X.

The fallout drew swift backlash from unions and free speech advocates. The Writers Guild of America called the suspension an act of “corporate cowardice,” while the American Federation of Musicians labeled it “state censorship.” Ari Cohn of the Foundation for Individual Rights and Expression said the timing showed “the government pressured ABC — and ABC caved.”

Senate Minority Leader Chuck Schumer also criticized the decision, saying it threatened democracy. “Everybody across the political spectrum should be speaking out to stop what’s happening to Jimmy Kimmel,” he wrote.

Nexstar defended its decision, with broadcasting president Andrew Alford saying Kimmel’s remarks about Kirk’s death were “offensive and insensitive” and not aligned with the “values of the local communities” its stations serve. Carr later praised Nexstar for “doing the right thing” and urged other broadcasters to follow suit.

The suspension marks the latest clash between media outlets and regulators over politically charged commentary. Earlier this year, ABC cut ties with correspondent Terry Moran after remarks about Trump, and last December the network paid $15 million to settle a lawsuit with Trump over statements by anchor George Stephanopoulos.

For now, “Jimmy Kimmel Live!” remains off the air as Disney executives prepare to meet with the host about his return.

Running a trade business is a rewarding but risky endeavour. From plumbing to carpentry, electrical work to landscaping, you face potential hazards every single day. That’s why understanding your insurance coverage is absolutely crucial. But let’s be honest, wading through policy documents can feel like deciphering ancient hieroglyphics. What are the real risks, and what protection do you actually have? It’s time to cut through the jargon and get a clear picture of what adequate trade insurance truly means for your livelihood.

Think of it this way: you wouldn’t head out to a job without the right tools, would you? Consider trade insurance as another essential tool in your kit, one that protects you from financial ruin should the unexpected happen. This article dives into the nitty-gritty of trade insurance, exploring the common risks faced by tradies and the different types of coverage available to safeguard your business. We’ll also look at factors that influence the cost of your premiums, helping you make informed decisions about your insurance needs.

Understanding the Risks Faced by Tradies

Before we delve into the specifics of trade insurance, it’s essential to understand the types of risks tradies encounter daily. These risks can range from minor incidents to catastrophic events, potentially leading to significant financial losses.

Property Damage

Imagine this: you’re working on a renovation project, and a faulty wire sparks a fire, causing extensive damage to the property. Or perhaps severe weather damages your tools and equipment stored on a job site. Property damage can be costly, and without adequate insurance, you could be left footing a hefty bill.

Public Liability

Public liability is a significant concern for tradies. Accidents can happen, and if a member of the public is injured or their property is damaged due to your work, you could be held liable. For example, a customer might trip over your equipment, or your work might cause damage to their property. These claims can be substantial, potentially crippling your business if you’re uninsured.

Personal Injury

As a tradie, your body is your most valuable asset. Injuries sustained on the job can prevent you from working, leading to lost income and medical expenses. Whether it’s a fall from a ladder, a back injury from lifting heavy materials, or an accident involving power tools, personal injury can have a devastating impact on your livelihood.

Theft and Vandalism

Unfortunately, theft and vandalism are all too common on construction sites and in work vehicles. Tools, equipment, and materials are attractive targets for thieves, and vandalism can cause significant damage, delaying projects and increasing costs. Replacing stolen or damaged items can be a major financial burden, especially for small businesses.

Professional Indemnity

While not always considered, professional indemnity is crucial for tradies offering design or advice services. If your advice leads to financial loss for a client, they could sue you for negligence. For example, an electrician who designs a faulty wiring system could be held liable for damages caused by the resulting electrical fires.

Types of Trade Insurance Coverage

Now that we’ve explored the common risks faced by tradies, let’s examine the different types of trade insurance coverage available to protect your business.

Public Liability Insurance

Public liability insurance is arguably the most essential type of coverage for tradies. It protects you against claims from third parties for injury or property damage caused by your work. This coverage typically includes legal costs, compensation for damages, and medical expenses. Having adequate public liability insurance is vital for protecting your business from potentially devastating financial losses.

Tool Insurance

Your tools are your livelihood, and replacing them can be expensive. Tool insurance covers the cost of replacing stolen or damaged tools, allowing you to get back to work quickly without a significant financial setback. Policies can vary in coverage, so it’s important to understand what is included, such as coverage for tools left in vehicles or on job sites.

Income Protection Insurance

If you’re unable to work due to illness or injury, income protection insurance can provide you with a regular income stream to cover your living expenses. This type of insurance is crucial for self-employed tradies who don’t have access to sick leave or workers’ compensation benefits. It ensures that you can continue to meet your financial obligations while you recover.

Workers Compensation Insurance

If you employ other people, workers’ compensation insurance is generally required by law. It covers medical expenses, lost wages, and rehabilitation costs for employees who are injured or become ill as a result of their work. This insurance protects both your employees and your business, ensuring that you can meet your legal obligations and provide support to injured workers.

Commercial Vehicle Insurance

Your work vehicle is an essential part of your business, and commercial vehicle insurance protects you against financial losses resulting from accidents, theft, or damage. Policies can include coverage for vehicle repairs, replacement vehicles, and liability for damages caused to other vehicles or property. It’s important to choose a policy that meets the specific needs of your business and the types of vehicles you use.

Contract Works Insurance

Contract works insurance, also known as construction insurance, covers damage to building projects while they are in progress. This can include damage caused by fire, theft, vandalism, or natural disasters. It’s essential for tradies working on construction or renovation projects, as it protects against financial losses if the project is damaged before completion.

Professional Indemnity Insurance

As mentioned earlier, professional indemnity insurance protects tradies who provide design or advice services. It covers legal costs and damages if a client sues you for negligence or errors in your advice. This type of insurance is particularly important for tradies who offer consulting services or design elements as part of their work.

Factors Influencing the Cost of Trade Insurance

The cost of trade insurance can vary depending on a number of factors. Understanding these factors can help you make informed decisions about your coverage and potentially lower your premiums.

Type of Trade

The type of trade you operate can significantly impact your insurance costs. High-risk trades, such as roofing or electrical work, typically have higher premiums due to the increased potential for accidents and injuries. Lower-risk trades, such as painting or landscaping, may have lower premiums.

Business Size and Revenue

Larger businesses with higher revenue generally have higher insurance costs. This is because they typically have more employees, assets, and potential liabilities. Smaller businesses with lower revenue may be able to obtain more affordable coverage.

Coverage Limits

The amount of coverage you choose will also affect your premiums. Higher coverage limits provide greater protection but also come with higher costs. It’s important to carefully consider your potential liabilities and choose coverage limits that adequately protect your business without overspending.

Excess

The excess is the amount you have to pay out of pocket before your insurance coverage kicks in. Choosing a higher excess can lower your premiums, but it also means you’ll have to pay more in the event of a claim. It’s important to strike a balance between a manageable excess and affordable premiums.

Claims History

If you have a history of making claims, your insurance premiums are likely to be higher. Insurers view businesses with a history of claims as higher risk and may charge higher rates to offset that risk. Maintaining a good safety record and minimising claims can help keep your insurance costs down.

Location

The location of your business can also affect your insurance costs. Businesses located in areas with higher crime rates or a greater risk of natural disasters may face higher premiums. Insurers assess the risks associated with different locations and adjust premiums accordingly.

Tips for Finding the Right Trade Insurance

Choosing the right trade insurance can seem daunting, but following these tips can help you find the coverage that best meets your needs.

Assess Your Risks

Start by carefully assessing the risks associated with your trade and business operations. Consider the types of accidents, injuries, or property damage that could occur and the potential financial impact. This will help you determine the types of coverage you need and the appropriate coverage limits.

Shop Around

Don’t settle for the first insurance quote you receive. Shop around and compare quotes from multiple insurers to find the best rates and coverage options. Use online comparison tools or work with an insurance broker to streamline the process.

Read the Fine Print

Before you commit to a policy, carefully read the fine print to understand the terms and conditions, exclusions, and limitations. Make sure you understand what is covered and what is not, and ask questions if anything is unclear.

Consider Bundling

Some insurers offer discounts for bundling multiple types of coverage, such as public liability, tool insurance, and commercial vehicle insurance. Consider bundling your policies to save money and simplify your insurance management.

Review Your Coverage Regularly

Your insurance needs may change over time as your business grows and evolves. Review your coverage regularly to ensure that it continues to meet your needs and that you’re not paying for coverage you no longer need. Update your policies as necessary to reflect changes in your business operations.

The Peace of Mind that Comes with Adequate Trade Insurance

While insurance might seem like an added expense, it’s an investment in the long-term security of your business. Knowing you have adequate insurance coverage provides peace of mind, allowing you to focus on your work without constantly worrying about potential financial risks. It’s about protecting yourself, your employees, and your livelihood from the unexpected events that can derail even the most successful businesses.

From navigating public liability claims to ensuring your tools are protected, having the right options for trade insurance is not just a good idea; it’s a fundamental aspect of running a responsible and sustainable business. By understanding the risks, exploring your coverage options, and making informed decisions, you can build a safety net that protects your hard work and secures your future.

Bezalel Smotrich is one of political leaders of Israel’s Messianic far-right. But he is also a shrewd administrator executing a biblical “decisive plan” of ethnic cleansing in Gaza, which he is incorporating into Israel.

Notorious both in Israel and abroad, yet beloved as a visionary by his constituencies, Bezalel Smotrich is the far-right leader of Israel’s National Religious Party-Religious Zionism and Prime Minister Netanyahu’s current Minister of Finance.

Ridiculed and underestimated abroad, Smotrich has consistently exploited the Gaza hostilities, in order to bring about the annexation of the West Bank to the pre-1967 Israel.

A self-proclaimed racist and fascist, Smotrich has promoted the blockade of the Gaza Strip since October 2023. He calls for a “voluntary emigration” of the Palestinians from Gaza to other countries. His ultimate objective is to transform Israel from a secular democratic state to a religious autocracy ruled by the Jewish biblical law.

The official Bezalel Smotrich, 2023 Source: Wikimedia

Restoring the Torah justice system

Smotrich has lived his life in Jewish settlements, which are illegal by international law. The descendant of a Ukrainian-Jewish family that lost most of its members in the Holocaust, he grew up in an Orthodox-Jewish and Zionist milieu. But it was distinctively Messianic.

Studying in Mercaz HaRav Kook, Yashlatz, and Yeshivat Kedumim, Smotrich was educated by the apocalyptic ideals of rabbi Abraham Isaac Kook, the father of Messianic religious Zionism. His political career took off in the mid-2010s, when the political clout of the Messianic far-right Jewish groups began to be felt nationwide. In 2019 he campaigned for the Ministry of Justice, saying that he sought the portfolio to “restore the Torah justice system.”

It is an old religious-Zionist goal, touted in the past by the violent Jewish-American rabbi Meir Kahane. It is premised on the idea that democratic institutions are a Hellenic, goy thing, whereas only the Five Books of Moses can serve as a foundation of law in a Jewish state. Smotrich’s extremist politics aim at replacing the secular rule of law with traditional Jewish law.

In 2021, Smotrich, emboldened by his growing popularity, declared that Israel’s first prime minister, David Ben-Gurion, should have “finished the job” and kicked all Palestinians out when Israel was founded. In his view, members of Israel’s Arab minority communities are citizens, but only “for now.”

Violence to undermine Israeli withdrawal from Gaza

In spring 2023, when Smotrich took over a large chunk of the administration of the West Bank, he did not condemn settler violence. Instead, he urged Israel to react “in a way that conveys that the landlord has gone crazy” and called for “striking the cities of terror and its instigators without mercy, with tanks and helicopters.” That became his rallying cry after October 7, 2023.

Gaza is personal to Smotrich. In the early 2000s, he saw Israel’s withdrawal from the Strip as blasphemy. During the protests against the Israeli disengagement from Gaza, he was arrested in 2005 while in possession of 700 liters of gasoline.

According to Shin Bet, Israel’s domestic security, the arrest was motivated by suspicion that he was participating in an attempt to blow up Ayalon Highway, a major arterial road. He was held in jail for three weeks but not charged after he refused speak.

Like all religious fanatics, Smotrich has walked his talk. He has a plan and he is determined to realize it. It isn’t a new plan. It is more than half a decade old.

Once scorned as religious humbug, it is now becoming still another new fact on the ground.

Smotrich’s “Decisive Plan” for Gaza

In 2017, Smotrich, then still a young Knesset member, presented his “Decisive Plan” in closed religious Zionist circles. It represented an endgame of sorts for the Israeli-Palestinian conflict.

The plan portrayed the conflict as devoid of any reconciliation. It rejected partition. It shunned any idea of a Palestinian state, any idea of Palestinian presence. Smotrich envisioned a singular state from the sea to the river, for one nation only: the Jewish people. True to his beliefs, he built on biblical allegories, which to him were no allegories at all:

When Joshua entered the land, he sent three letters to its inhabitants: Those who want to accept [our rule] will accept; those who want to leave, will leave; those who want to fight, will fight….

When they have no hope and no outlook, they will leave, just as they left in 1948.

Since October 7, Smotrich has championed what he describes as a “humane” solution for Gazan non-combatants: a “voluntary” population transfer.

The two-state model was a dead end. Smotrich’s solution was simpler: Eliminate the adversary, resolve the dilemma.

Smotrich is close to US Jewish neoconservatives Smotrich with US Ambassador to Israel David M. Friedman in October 2017

“Leave!”

A month after October 7, 2023, U.S. Secretary of State Antony Blinken presented his outline of what America would not accept as the “day after” in Gaza:

No forcible displacement of Palestinians from Gaza. No use of Gaza as a platform for launching terrorism or other attacks against Israel. No diminution of the territory in Gaza and a commitment to Palestinian land governance for Gaza and the West Bank and in a unified way.

In light of the on-the-ground realities, Blinken was living in a parallel universe. Most Gazans had already been displaced, the attacks continued, the infrastructure had been leveled and the path was paved for mass starvation.

To the Messianic far-right in Israel, the White House is a convenient asset in God’s plan for Israel; not more, not less. In their view, America is not just rich and powerful, but soft and manipulable.

So, while the Netanyahu cabinet’s official emissaries paid tribute to their American sponsors by regularly bowing to liturgical phrases, such as a “two-state solution” and “no displacement,” they were tenaciously building the institutional framework for a singular Jewish state and for displacing more than 2 million Palestinians in Gaza.

In Smotrich’s view, Arabs owned no land. Jews were the landlords. Palestinians were just short-term tenants. Jews stayed; Palestinians were visiting. In a while, the world will forget all about the West Bank and Gaza, even the terms themselves. Those lands will be Judaized and know by their Hebrew terms as Judea and Samaria, and Azza.

So, when Netanyahu entrusted Smotrich with the administration of the occupied West Bank, he did it deliberately and purposely. It was a signal to Palestinian Arabs: Leave!

The original commentary was released by Informed Comment (US) on Sept. 18, 2025.

For many players, the biggest barrier to trying online casinos is the risk of losing money before they even know if they’ll enjoy the experience. This is where no deposit casino bonuses come in. These offers give players a chance to test out real-money games without having to make an initial deposit. They’re one of the most attractive promotions in the industry, allowing you to explore slot machines, table games, and live dealer titles at no cost.

But how do these bonuses work, what are the potential downsides, and where can you find the best deals? This guide will help you understand how to play without risk while making the most of these special offers.

What Is a No Deposit Casino Bonus?

A no deposit casino bonus is exactly what it sounds like: a bonus provided by a casino without requiring you to deposit any of your own money. These bonuses usually come in two forms:

Free credits – A small balance added to your account to play selected games.

Free spins – A set number of spins on a particular slot or group of slots.

These bonuses are particularly popular among newcomers who want to explore games risk-free, but they’re also useful for experienced players trying out new platforms.

Why Casinos Offer No Deposit Bonuses

You might wonder why casinos give away free money. The answer is simple: it’s a marketing tool. No deposit bonuses attract new customers by reducing the initial barrier to entry.

Once players enjoy the platform, explore the games, and experience the convenience of casino apps for iOS and Android, many are more likely to make deposits and continue playing. For the casino, it’s an investment in building loyalty.

Wagering Requirements and Conditions

No deposit bonuses are never completely free of strings. Most come with wagering requirements, which determine how many times you must bet the bonus amount before withdrawing winnings. For example, a $10 free credit with a 30x wagering requirement means you need to place $300 in bets before you can cash out.

Other common conditions include:

Game restrictions – Some bonuses are limited to certain slots or categories.

Maximum withdrawal limits – Casinos often cap how much you can cash out from no deposit wins.

Time limits – Free credits or spins may expire after a set period, usually 7–14 days.

Understanding these terms is key to making the most of the offer without disappointment.

Benefits of No Deposit Bonuses

Despite the conditions, no deposit casino bonuses come with clear advantages:

Risk-free play – You’re not putting your own money on the line.

Platform testing – A great way to evaluate user experience, customer support, and game variety.

Real winnings possible – While capped, you can still cash out actual money from free bonuses.

Mobile convenience – Easily accessible on casino apps for iOS and Android, so you can try games on the go.

Where to Find the Best Offers

Not every bonus is equal, so choosing carefully is important. Start with casinos with high payouts since these platforms often combine fair RTP (Return to Player) percentages with transparent bonus terms. High-payout casinos also have reputations for fast withdrawals, making it more worthwhile when you do win.

New players should also explore comparison sites and review platforms that list the most recent and generous no deposit promotions. This way, you’ll know which casinos have the lowest wagering requirements and the best withdrawal policies.

Tips for Making the Most of No Deposit Bonuses

Read the fine print – Always check wagering requirements, game restrictions, and withdrawal caps.

Play high RTP games – Use your free credits or spins on games with favorable odds for better chances.

Set realistic expectations – Treat no deposit bonuses as a way to explore, not as a guaranteed way to win big.

Stay with licensed casinos – Only claim bonuses from regulated operators to ensure security and fairness.

Conclusion

No deposit casino bonuses are one of the best ways to experience online gambling without taking financial risks. They allow players to explore games, test platforms, and even win real money—all without spending a cent upfront. By sticking to casinos with high payouts and taking advantage of reliable casino apps for iOS and Android, you can maximize your chances of enjoying these offers safely and responsibly.

Whether you’re a beginner curious about mobile slots or a seasoned player testing out a new platform, no deposit bonuses are a risk-free gateway to the exciting world of online casinos.

The Federal Reserve on Wednesday lowered its benchmark interest rate by a quarter percentage point, bringing the federal funds rate to a range of 4% to 4.25%. It is the lowest level in nearly three years and marks the first step in what officials signaled will be a series of cuts.

The rate move had been widely expected, but markets closely watched the Fed’s updated “dot plot” projections for future policy. The outlook pointed to two more reductions this year, another in 2026, and one more in 2027, leaving the rate near 3%—the level the committee views as “neutral.”

Markets reacted with mixed signals. The Dow Jones Industrial Average gained 260 points, but both the S&P 500 and Nasdaq closed lower. Treasury yields fell on short-term bonds while climbing on longer maturities, a dynamic that could complicate the Fed’s effort to manage growth and inflation risks.

Chair Jerome Powell described the move as a “risk management” cut, underscoring concerns about a slowing labor market. “The only way for any voter to really move things around is to be incredibly persuasive, and the only way to do that in the context in which we work is to make really strong arguments based on the data and understanding of the economy. That’s really all that matters, and that’s how it’s going to work,” Powell said during his press conference.

The pace of easing is expected to be front-loaded. The Fed projected two additional cuts at its October and December meetings, followed by just one in 2026 and another in 2027, with no cuts in 2028. The uneven path left investors uneasy about the balance between dovish and hawkish signals.

The meeting also featured the debut of Governor Stephen Miran, who cast the lone dissenting vote. He argued for a larger half-point reduction, highlighting divisions within the committee. A narrow 10-9 vote determined that two more cuts this year were preferred over just one, reflecting a wide range of views among policymakers.

Analysts weighed in on the implications. Dan North, senior economist at Allianz Trade North America, suggested that members rallied to avoid broader dissent. Rick Rieder of BlackRock warned that the Fed’s biggest challenge ahead would be preserving jobs, noting that “the hiring environment for people is becoming considerably less healthy.” Joseph Brusuelas of RSM cautioned that the central bank may tolerate inflation “well above target” in the coming years as leadership changes take shape.

The Fed’s latest decision reflects its delicate balancing act—easing policy to sustain growth while trying to avoid reigniting price pressures. With political and economic uncertainty on the horizon, markets are bracing for more volatility as the central bank navigates the path forward.

The 2025 Shanghai Cooperation Organisation (SCO) summit in Tianjin, which brought together twenty-six heads of state, underscored the organization’s growing relevance amid intensifying geopolitical fragmentation. Dr Kalim Siddiqui argues that for many Global South countries, unsettled by US protectionism and coercive tariff policies, the SCO offers a strategic alternative to West and a platform for policy coordination, and collective action.

I. Introduction

The international system is undergoing a profound transformation marked by the decline of unipolarity and the rise of competing centres of power. At the heart of this shift is the Shanghai Cooperation Organization (SCO), a regional grouping that has evolved from a narrow security arrangement into a broad platform for political, economic, and strategic cooperation. At present, with 10 full members—including China, Russia, India, Pakistan, Iran, Kazakhstan, Kyrgyzstan, Tajikistan, Uzbekistan and Belarus—and a growing number of dialogue partners such as Saudi Arabia, Türkiye, and Qatar, the SCO represents a potential alternative to Western-led international organisations.

The SCO was established in 2001 by six founding members—China, Russia, Kazakhstan, Kyrgyzstan, Tajikistan, and Uzbekistan—with the primary goal of fostering security cooperation in Central Asia (Siddiqui, 2023). Over two decades, the organization has expanded its membership. Today, the SCO’s agenda spans security, economic development, energy cooperation, connectivity, and cultural exchange.

The 2025 Shanghai Cooperation Organisation summit in Tianjin, which convened a record twenty-six heads of state, demonstrated the organization’s significant growth amidst a period of global geopolitical fragmentation. For many Global South nations alarmed by rising US protectionism and coercive tariff policies, the SCO is increasingly seen as a strategic alternative to Western-dominated institutions. It offers a crucial platform for non-Western countries to align policies, advance mutual interests, and collectively project influence. This paper analyses the SCO’s rising prominence, its internal dynamics with member states, and its broader role in facilitating a multipolar world order.

This development must be situated within a broader global context increasingly characterized by geopolitical fragmentation.

At the recent SCO summit, Indian Prime Minister Narendra Modi held a meeting with Chinese President Xi Jinping, signalling a potential step toward the normalization of strained bilateral relations. This development must be situated within a broader global context increasingly characterized by geopolitical fragmentation. Although deep-seated challenges persist between India and China—including territorial disputes, strategic competition, and enduring trade imbalances—the SCO provides an institutionalized framework for dialogue and confidence-building among its member states. Such mechanisms are particularly significant in a period marked by heightened instability in the global economy. The continuation of tariff-based trade policies, initiated under former US President Donald Trump, has disproportionately affected India, reinforcing the importance of diversifying multilateral engagement.

India’s active participation in platforms such as BRICS, the Russia–India–China trilateral, and the SCO reflects a deliberate effort to expand its strategic partnerships while mitigating the risks of great-power rivalry. These interactions not only strengthen India’s regional influence but also enhance its role in shaping global governance structures (Siddiqui, 2016).

In this context, India faces the responsibility of demonstrating leadership among developing countries. By advancing the principles of collective strength, multipolarity, and the democratization of international institutions, India can contribute to the construction of a more balanced and representative global order.

For India, participation in the SCO reflects both opportunity and challenge. Situated between the competing influences of China, Russia, and the United States (US), India trying to navigate a complex web of economic dependencies and strategic rivalries. India also faces domestic economic pressures and mounting US trade restrictions, including high tariffs. Diversifying trade with China, while cautiously managing security concerns, may help India reduce external vulnerabilities and strengthen its economic resilience.

The SCO has become an indispensable component of India’s foreign policy strategy, particularly in the context of managing its complex relations with China and Russia. While challenges remain, India’s continued participation in the SCO reflects both pragmatic considerations and its aspiration to shape the contours of a multipolar world order. The organization’s future trajectory will depend on how its members reconcile divergent interests, but it is already clear that the SCO represents a significant arena in which India seeks to project influence and safeguard its long-term strategic interests (Bajpayee and Jie, 2025).

Furthermore, the SCO presents opportunities for India to deepen ties with the Global South and position itself as a bridge between Asia and other developing regions. By leveraging SCO mechanisms, India may enhance regional connectivity projects, promote economic integration, and build coalitions around issues such as climate change, energy security, and equitable development.

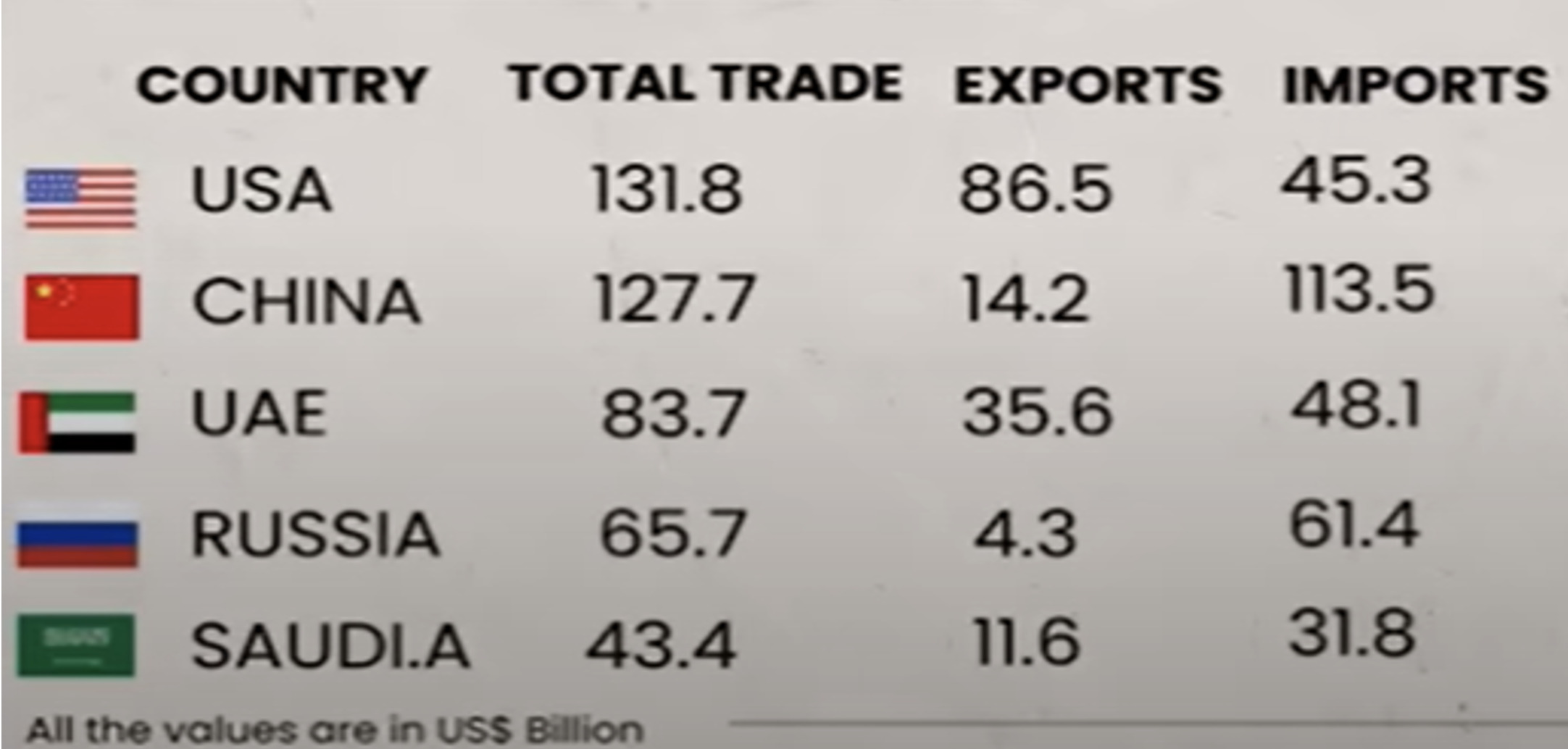

The SCO summit brought together some of the strongest emerging economies, including India and Russia, which, along with China, account for more than one-fifth of the world’s gross domestic product (GDP). Trilateral trade between China, India and Russia accounted for $452 bn in 2023, up from $351 bn in 2022.

II. Political and Economic Significance of the SCO Summit

The enlargement and diversification of the SCO underscores its growing geopolitical relevance. For post-colonial countries, participation in the organization offers an alternative platform outside Western-dominated institutions (Siddiqui, 2025a). For India, active engagement in the SCO allows it to advance its strategic autonomy, improve relations with China, and contribute to the construction of a more pluralistic global governance system (Bajpayee and Jie, 2025).

International politics is increasingly shaped by geopolitical fragmentation, India’s engagement with China and Russia acquires heightened significance. While global instability persists—exacerbated by factors such as US tariff policies under former President Donald Trump, which have particularly affected India—multilateral forums like BRICS and the SCO provide important avenues for dialogue and cooperation. As a major developing economy, India is called upon to demonstrate global responsibility, set an example for the Global South, and contribute to advancing the multiploidization of world politics and the democratization of international institutions.

The SCO summit brought together several of the world’s most significant emerging economies, most notably China, India, Russia, and Iran, which collectively account for more than one-fifth of global GDP. The economic interdependence of these countries is evident in trade statistics: trilateral trade among China, India, and Russia increased from US$ 351 bn in 2022 to US$ 452 bn in 2023, highlighting their deepening economic ties despite global disruptions (Aljazeera, 2025).

The improvement in Sino-Indian relations, their cooperation could potentially serve as a driving force in international politics. Such a development might also galvanize the Russia–India–China trilateral process, a format championed by Yevgeny Primakov in the late 1990s. Primakov envisioned a multipolar world order in which Eurasian powers would collaborate to balance Western dominance. Three decades later, the international correlation of forces has indeed shifted in directions broadly consistent with his vision (Siddiqui, 2023).

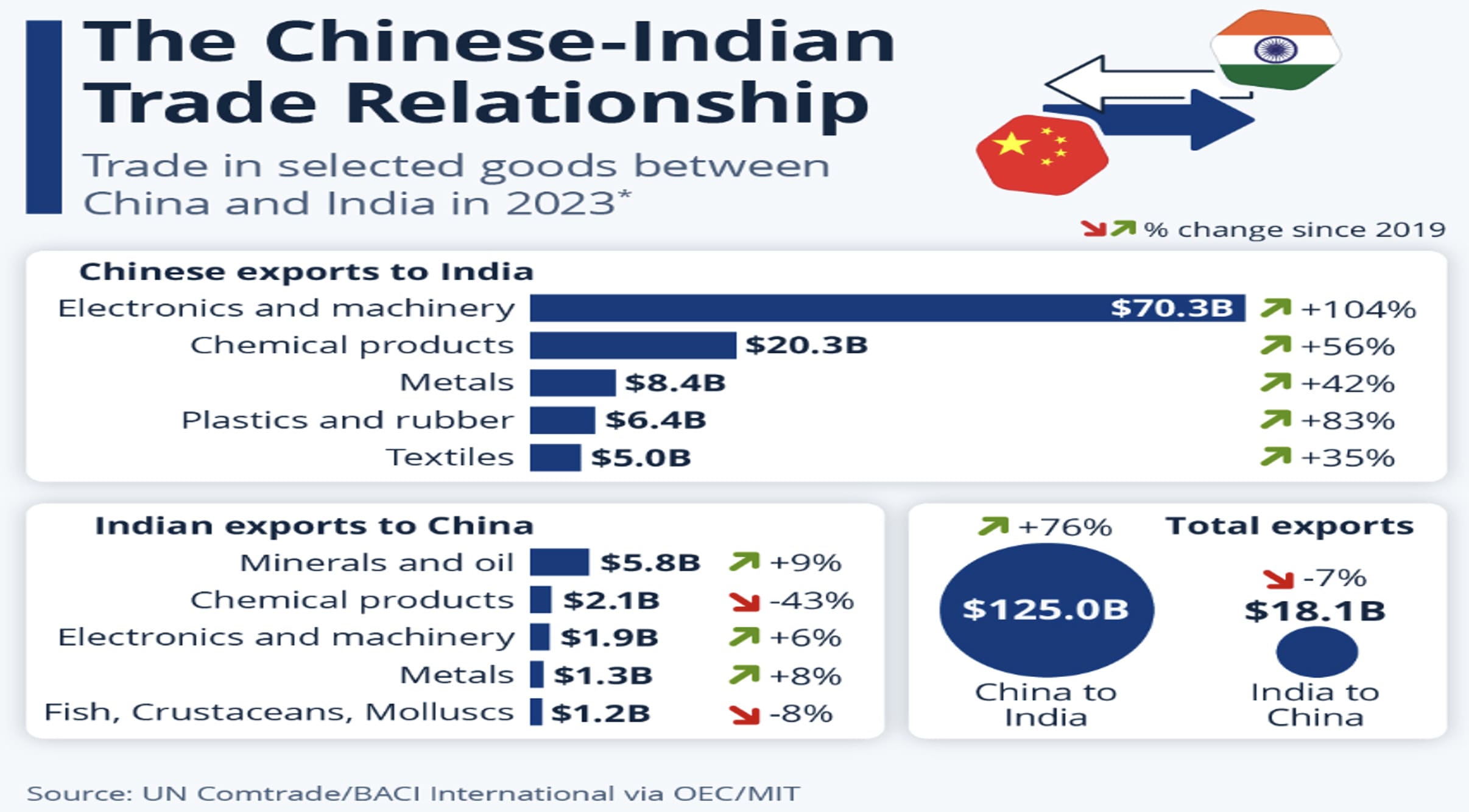

However, on economic front, India runs a substantial trade deficit with China, importing nearly seven times more goods than it exports. In 2023, China exported US$ 125 bn worth of goods to India, mainly machinery and chemical products, while India’s exports to China totalled only US$ 18.1 bn, largely consisting of oil and fuel products. Yet despite asymmetries, the relationship remains vital: India depends on Chinese investments, technologies, and raw materials to sustain its manufacturing and export sectors. India runs a major trade deficit with Russia, importing far more than it exports. In 2023, Russia sold $66.1 bn worth of goods to India, with energy products – primarily crude oil and natural gas – making up about 88 percent of these imports, much of which India buys at a discounted rate.

China is the largest Russia’s trading partner, accounting for 14.6 percent ($72.1bn) of Russian exports in 2021, Russia also had a broad range of European partners. The Netherlands was Russia’s second-largest partner, with 8 percent ($39.5bn) of total exports, followed by the US at 5.5 percent ($27.3bn) in 2021.

Before the Ukraine conflict, Russia maintained a diverse set of trading partners. In 2021, China was Russia’s largest trading partner, absorbing 14.6 percent (US$ 72.1bn) of Russian exports. The Netherlands (8 percent, US$ 39.5bn) and the US (5.5 percent, US$ 27.3bn) also figured prominently.

However, following Russia’s invasion of Ukraine in February 2022, sweeping Western sanctions forced Russia to reorient its trade. By 2023, the bulk of Russian exports shifted decisively toward Asia. China accounted for one-third (US$ 129 bn) of Russia’s exports, while India absorbed 16.8 percent (US$ 66.1bn) and Türkiye 7.9 percent (US$ 31bn). Together, Asian markets consumed more than three-quarters of Russia’s total exports. In 2023, China exported $110bn worth of goods to Russia, led by machinery and transport equipment. The top export items from China to Russia were cars. That same year, Russia sold $129bn worth of goods to China – mostly mineral products, including oil and natural gas. Russia has run a trade surplus with China, mostly due to energy products, which make up nearly three-quarters of its exports (Aljazeera, 2025).

The SCO has increasingly become a critical platform where shifting economic alignments between India, China, and Russia are negotiated against the backdrop of global instability. The redirection of Russia’s trade toward Asia highlights the deepening interdependence within the SCO space, while India’s engagement demonstrates both opportunities and constraints. As India seeks to balance its relations with Russia and China, its active role in the SCO will be central to advancing a vision of a more multipolar and democratized global order.

India continues to experience a significant trade imbalance with China, importing nearly seven times more goods (by value) than it exports. In 2023, China exported US$ 125bn worth of goods to India, dominated by machinery and chemical products. By contrast, India’s exports to China totalled only US$ 18.1bn, with oil and fuel-related products constituting the largest share (Aljazeera, 2025). This persistent deficit underscores both structural asymmetries in bilateral trade and the challenges India faces in diversifying and upgrading its export basket.

The US has expressed strong opposition to India’s purchase of discounted Russian oil, arguing that such transactions provide Russia with significant revenue to sustain its war in Ukraine. Beyond energy, US has also sought greater access to India’s agricultural sector, pressing for the entry of US agribusiness corporations, which could enable them to offload surplus production into Indian markets. At a strategic level, the US increasingly perceives India as a potential systemic challenger to American hegemony, complicating the bilateral relationship despite their growing defence and technological cooperation (Siddiqui, 2025b).

Despite the US pressure, India has deepened its energy and trade relations with Russia. By 2024, Russia accounted for approximately 37 percent of India’s total oil imports, highlighting Russia’s centrality to India’s energy security. Bilateral trade between the two countries reached a record US$ 68.7bn in the 2024–25 financial year, with Indian imports from Russia valued at around US$ 64 bn, compared to exports worth only US$ 5bn. The trade relationship remains heavily skewed in Russia’s favour, largely due to energy purchases, but both governments have articulated ambitions to expand bilateral trade to US$ 100 bn by 2030.

The SCO represents more than a regional forum; it embodies the aspirations of non-Western powers to shape a multipolar world order. For India, success will depend on reducing border tension with China and taking a clear stand to diversify its economy and building relations with China, Russia and other emerging economies to advance its long-term interests. As envisioned by prominent Russian diplomat Yevgeny Primakov, the shifting correlation of forces suggests that the world is indeed moving toward multipolarity, even if the path remains fraught with rivalry and uncertainty.

III. India, China, and US Power Politics: Interdependence and Strategic Rivalries

The Indian diaspora in the US, particularly the Gujarati business community, and the large number of Indian-origin CEOs leading major US corporations, highlight the depth of India–US economic linkages. Moreover, India’s IT sector is deeply integrated with US businesses and markets, while bilateral cooperation also extends to the nuclear sector (Siddiqui, 2025c).

At the same time, India’s manufacturing capacity is closely tied to Chinese investment and raw material supplies. Many of India’s export-oriented industries depend on Chinese inputs, technologies, and critical minerals, underscoring India’s economic dependence on China. This dual reliance on both the US and China complicates India’s foreign policy, especially in an era of heightened great-power rivalry.

India’s foreign policy choices are further complicated by internal divisions. A strong pro-American lobby exists within India, encompassing sections of the intelligentsia, the diaspora, and segments of the political and business elite. This camp champions a deepening strategic partnership with the US, often describing it as the defining relationship of the 21st century.

During the Trump administration, the tension between India and US became explicit. Peter Navarro, a senior adviser to President Trump, argued in the Financial Times that the US should not transfer “cutting-edge” military technologies to India as long as India appeared to be “cozying up” to Russia and China. Such statements underscore the limits of US trust in India’s strategic choices and highlight the ongoing challenge for India in pursuing multi-alignment without alienating major partners.

The US has adopted a strategy of containing China, viewing China’s rapid economic rise as a precursor to military strength and geopolitical influence. For much of the past quarter century, economic interdependence between major powers was seen as a pathway to shared prosperity. Indeed, both India and China benefited substantially from globalization over the last 25 years. However, China’s ascent has been far more dramatic, enabling it to emerge as the principal power in East Asia. Since 2017, the rise of Chinese economy and technology is seen by the US as challenger to its dominance in Asia.

Over the past three decades, China has achieved remarkable economic growth, enabling it to emerge as a regional power in East Asia with global ambitions (Siddiqui, 2024a). As China strengthens both its economic and military presence in the region, the US views this as a direct challenge to its long-standing hegemony. US’s approach toward China mirrors its earlier strategies of containing other rising powers. In this respect, China’s current trajectory parallels the US experience in the 19th century, when US asserted dominance over the Western Hemisphere through the Monroe Doctrine (Siddiqui, 2025a).

However, India’s relations with China remain clouded by negative perceptions and longstanding mistrust, which cannot be easily overcome. Despite increasing reliance on trade and investment cooperation with China, Indian domestic narratives often highlight China as a strategic rival, reinforcing scepticism toward closer engagement despite growing economic interdependence (Bajpayee and Jie, 2025).

The India–Pakistan military conflict has underscored the limitations of the SCO as a security platform. The organization has struggled to respond effectively to intra-member crises, revealing weaknesses in its flexibility and crisis management mechanisms. These shortcomings highlight the need for structural reforms and enhanced internal coordination. There is a need for resolving conflict between India and Pakistan because both are members of the SCO. And if it continues to be constrained by bilateral disputes, its geopolitical relevance risks further erosion in comparison to Western-led alliance systems, which maintain more cohesive structures and crisis-response capabilities.

Another conflict, namely the India–China border dispute, which has its origins in British colonialism, particularly the agreements and maps drawn by the British Raj in the early 20th century. The McMahon Line of 1914, intended to demarcate the boundary in the eastern sector, left several regions ambiguous, including Aksai Chin in the western sector. These colonial-era arrangements were insufficient for the needs of an independent India and have contributed to ongoing territorial disputes since Britain’s withdrawal.

The 2020 border clashes marked the most serious tensions in over four decades, placing the issue at the forefront of bilateral relations. De-escalation and stabilization along the border are now widely regarded as prerequisites for broader engagement, including economic and strategic cooperation. A breakthrough in resolving the border dispute could transform regional dynamics in Asia, reduce decades of hostility, and potentially diminish US influence over India in regional affairs.

Despite recurring challenges, particularly over the disputed Himalayan border, India and China have simultaneously cultivated growing economic and trade ties. In recent years, both countries have recalibrated their approaches to bilateral engagement, aiming to stabilize the border while enhancing commercial collaboration (Xue and Balazs, 2025).

IV. Economic Ties Between India and China

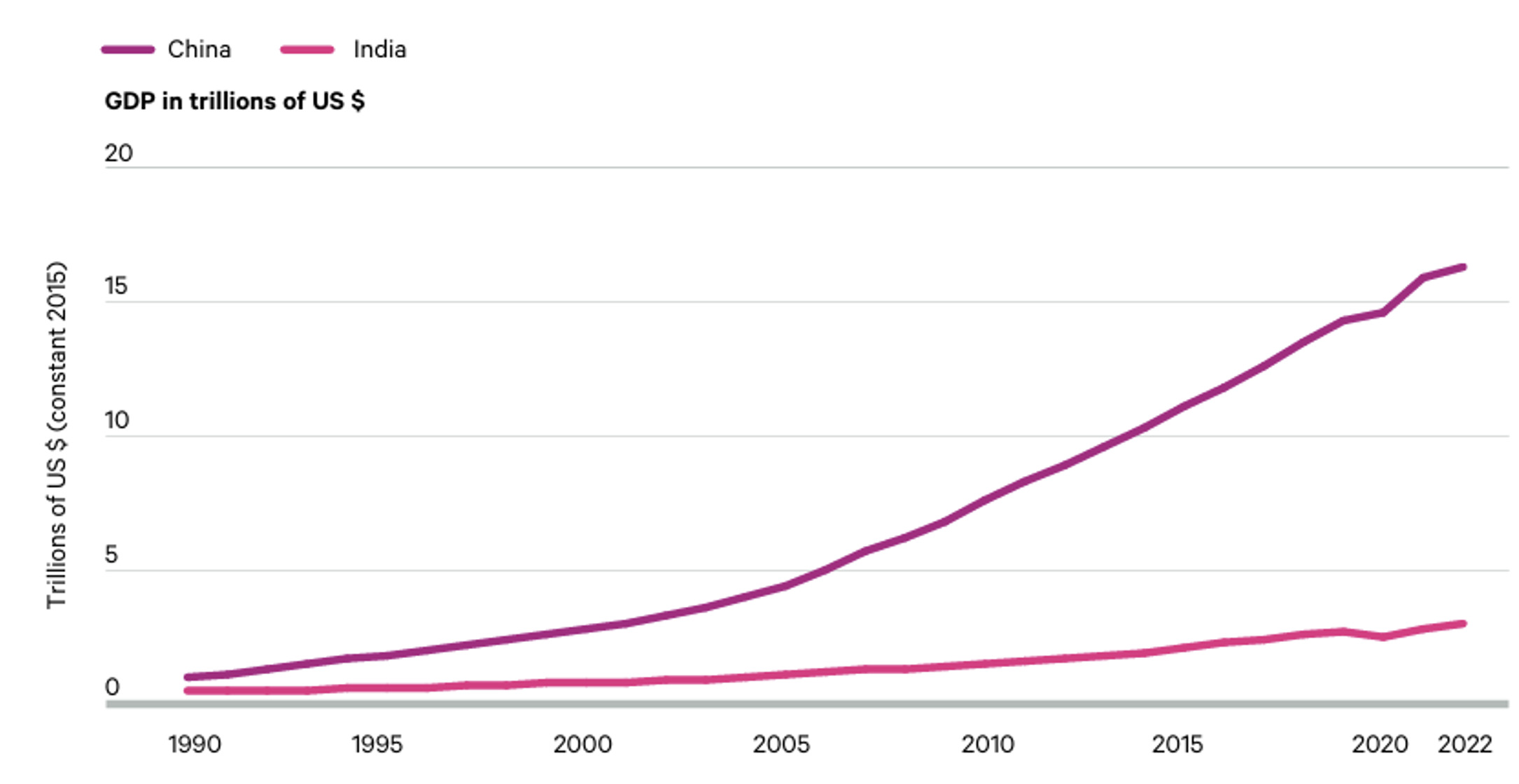

China’s economy is nearly six times larger than India’s in terms of GDP in 2023 (see Figure 1) (Siddiqui, 2020). In addition, China has become a leading global supplier of critical raw materials with high economic importance in the 21st century. These include rare earth elements, lithium, cobalt, copper, gallium, germanium, natural graphite, silicon, and platinum. Such minerals are indispensable for the green and digital transitions, powering technologies like electric vehicles, solar panels, wind turbines, and advanced electronics. They are, therefore, central to future economic competitiveness and strategic autonomy. Against this backdrop, Chinese cooperation is vital not only to strengthen India’s manufacturing capacity—through the supply of raw materials, technology, and capital investment—but also to expand its export sector (Xue and Balazs, 2025).

Figure 1: The Growth of Gross Domestic Production of China and India, 1990-2022 (US$ trillions)

India’s growing manufacturing sector presents opportunities for economic convergence with China. As the two most populous economies in the world, enhanced collaboration in trade, investment, and industrial development could generate mutual benefits. India has the potential to attract manufacturing transfers, which may complement or, in some sectors, compete with Chinese exports. Strengthening communication and cooperation between the two countries could therefore drive regional economic growth and foster stability while balancing broader geopolitical pressures (Siddiqui, 2024d).

The significant decline in foreign direct investment (FDI) inflows from China to India is largely attributable to India’s revised FDI policy for countries sharing land borders, implemented in response to the Sino-Indian border tensions of 2020. Despite this, Chinese investment in India continues to focus on strategic sectors such as electronics (smartphones, telecom equipment), household appliances, power equipment, steel, engineering machinery, and e-commerce. Prominent investors include Xiaomi, VIVO, OPPO, Huawei, Haier, Shanghai Automotive, Sany Heavy Industry, and TBEA.

Conversely, Indian investment in China has also declined, with FDI totalling US$ 6.32 million in 2021, representing a 47.4 percent year-on-year decrease. Nevertheless, Indian companies have increasingly established operations in China across diverse sectors, including pharmaceuticals, manufacturing, IT services, and trade, specifically on manufacturing industries, such as pharmaceuticals, auto components, and renewable energy (wind power).

FDI flows between the two countries have fluctuated due to geopolitical tensions, yet both governments continue to explore joint ventures in emerging sectors, including electric vehicles (EVs) and telecommunications. China remains a critical supplier of industrial goods to India, while India seeks to attract Chinese firms to establish local production facilities.

This pattern of investment reflects both economic pragmatism and a shared understanding that stable economic relations are essential for broader political and strategic stability, particularly amid the complex security and geopolitical environment in Asia.

This pattern of investment reflects both economic pragmatism and a shared understanding that stable economic relations are essential for broader political and strategic stability

This reliance persists even as India restricts Chinese investment in sensitive sectors and bans several Chinese-owned apps, including TikTok and WeChat. The reality is that India’s ambitions to become a global manufacturing hub cannot be achieved without Chinese components and raw materials. As the Economic Survey 2023–24 cautions, “it may not be the most prudent approach to think that India can take up the slack from China vacating certain spaces in manufacturing.” Instead, the report argues, India’s integration into global supply chains is contingent on its integration into China’s supply chain.

Despite political frictions, China remains India’s leading trading partner. The trade data highlights a widening imbalance: Chinese exports to India exceeded US$100 bn, while Indian exports to China totalled just over US$15 bn in 2022. In strategically significant sectors—such as pharmaceuticals and renewable energy—India’s dependence is especially pronounced. More than 40 percent of India’s pharmaceutical imports originate in China, and India’s largest supplier of generic drugs to the US relies on China for over half of its active pharmaceutical ingredients (Bajpayee and Jie, 2025).

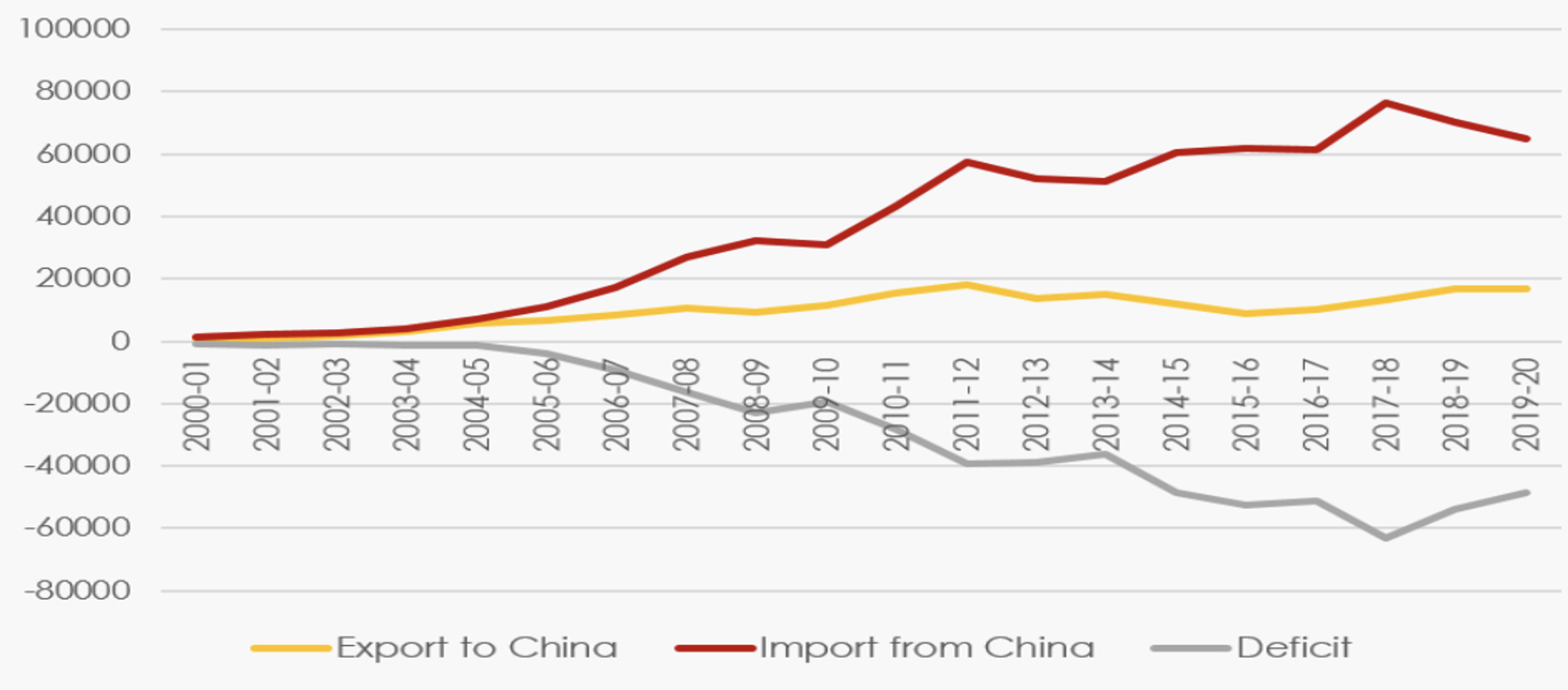

Trade has long functioned as a stabilizing factor in India-China relations, even amid political frictions. In 2024, bilateral trade reached US$ $118.4 bn, with India importing $101.7 bn worth of goods while exporting only $16.67 bn (See Figure 2). However, despite border disputes and trade between India and China has steadily grown over the years (as illustrated in Figure 3). China is second among the top trading countries for India (as shown in Table 1) and also China is the key supplier of critical raw materials for India’s manufacturing.

This stark asymmetry underscores both the depth of India’s dependence on Chinese supply chains and China’s centrality to India’s economic calculations. Rare earth elements provide another critical layer of interdependence. While India possesses domestic reserves, it lacks advanced processing capabilities, leaving it strategically vulnerable to China’s dominance in global rare earth supply chains—essential for electronics, renewable energy, and defence applications.

Figure 2: The Chinese-Indian Trade Relationship in 2023.

For centuries, Europe and North America controlled the bulk of global resources and technological innovation while dictating political and economic terms to the rest of the world. Today, that asymmetry is diminishing. Rising powers such as China, India, Russia, Indonesia, and South Africa—propelled by rapid growth, expanding higher education, and technological development—are altering the global balance of power, as underscored by the recent SCO summit. These dynamics point to the emergence of a genuinely multipolar order (Siddiqui, 2020b).