This article questions the dominance of global university rankings as the primary measure of success. Drawing on experiences at PSUT’s King Talal School of Business Technology, it highlights alternative indicators such as skills development, societal impact, sustainability, entrepreneurship, and partnerships, arguing for a balanced approach that values transformative contributions over numerical standings.

Every fall, when the latest global university rankings are published, the higher education world holds its breath. Institutions celebrate their ascent or lament their decline; media headlines announce winners and losers; and prospective students scan the tables for guidance. Rankings have become a powerful currency of reputation, shaping decisions about where students study, where faculty work, and where governments allocate resources.

Yet I often find myself asking: What if rankings weren’t the only way to measure success?

Beyond Rankings: Redefining Success in Context

At the King Talal School of Business Technology (KTSBT) at Princess Sumaya University for Technology (PSUT) in Amman, Jordan we believe success cannot be captured solely by league tables. For us, success means equipping students with the skills and mindsets to navigate a rapidly changing world. It means producing research that addresses pressing societal challenges, from digital transformation to sustainable business models. It means forging partnerships with industry, government, and civil society to ensure that our impact is felt beyond campus walls.

This commitment is reflected in our integration of the United Nations’ Sustainable Development Goals (SDGs) into our curriculum. At our school, we have embedded the SDGs into teaching, learning, and research, ensuring that graduates leave with not only technical expertise but also a strong sense of responsibility toward society and the environment. This approach reflects a broader understanding of success—one that emphasizes relevance, resilience, and responsibility.

At PSUT, this vision is further supported by a vibrant entrepreneurship ecosystem that nurtures innovation and impact. The system includes the Entrepreneurship and Innovation in Residence (EIR) program, which connects students with experienced entrepreneurs for mentorship and guidance; the Queen Rania Center for Entrepreneurship (QRCE), which promotes entrepreneurial culture and provides training opportunities; the Venture Lab, where students and faculty can develop, prototype, and scale their ideas; and iPark, a leading incubator that supports startups and spin-offs in their growth journey. Together, these initiatives create an environment where students do not just learn about entrepreneurship—they actively practice it, building ventures that tackle real-world challenges such as digital inclusion, sustainability, and job creation.

These contributions may not dramatically shift a university’s global ranking, but they create tangible value for society. They demonstrate that higher education can be a catalyst for national competitiveness, social mobility, and sustainable development. In many ways, these outcomes represent a truer measure of success than any number on a table.

The Case for Balance

This is not to suggest that rankings are irrelevant. They provide a degree of comparability, and they can motivate universities to improve. But they should not be the sole narrative of success. Instead, we need balance: a recognition that while rankings offer one perspective, the true value of an institution lies in its transformative power—on students, on communities, and on society.

A Call to Action

As deans, educators, and policymakers, we must lead this shift in perspective. We need to champion success stories that do not fit neatly into rankings tables: the small but powerful innovations in teaching, the long-term partnerships that drive community development, the research that quietly changes lives. By doing so, we encourage a culture where institutions strive not only to be the best in the world, but also the best for the world.

The world is facing unprecedented challenges such as climate change, inequality, technological disruption. Meeting them requires universities and business schools to redefine what success looks like. Rankings may tell us who is ahead in the race, but impact tells us whether we are running in the right direction.

And so I return to the question: What if rankings weren’t the only way to measure success? Perhaps then we would begin to value the deeper, lasting contributions of education, the ones that numbers alone cannot capture.

Dr. George Sammouris Associate Professor at Princess Sumaya University for Technology, Jordan. His expertise includes data analytics, business intelligence, and e-learning. He serves on editorial boards and accreditation committees, mentors universities in AACSB accreditation, and has published widely while leading quality assurance and academic development initiatives in higher education.

Oracle, Silver Lake, and Abu Dhabi’s MGX will emerge as the lead investors in TikTok’s American business under a deal expected to reshape ownership of the popular social media platform, according to people familiar with the negotiations.

The three firms will jointly hold about 45% of TikTok USA. ByteDance, the Beijing-based parent company, will retain a 19.9% interest, while the remaining 35% will be divided between existing ByteDance backers and new stakeholders.

President Donald Trump is set to sign an executive order on Thursday endorsing the agreement, which ensures that TikTok remains operational in the United States. The move follows months of uncertainty as ByteDance faced a federal mandate to divest its U.S. operations or risk a nationwide ban. Lawmakers from both parties had raised alarms about the app’s algorithm and its potential ties to Chinese authorities.

Last week, Trump issued an order delaying the divestiture deadline until December 16, giving negotiators additional time to finalize the structure.

Sources said ByteDance’s American investors, including General Atlantic, Susquehanna, and Sequoia, are expected to contribute equity to the new company. The arrangement does not give the federal government an ownership share or special voting rights in the U.S. entity, CNBC reported earlier this week. Instead, a board composed mostly of American members will oversee operations, and Oracle will take charge of data security and compliance.

Trump has frequently highlighted TikTok’s importance, noting its role in mobilizing younger audiences during his election campaign. He has also pointed to billionaire donor Jeff Yass, a significant ByteDance investor through Susquehanna, as a key figure in the deal. Yass also holds a stake in Trump’s own media company, Truth Social.

In addition, Trump recently suggested that media executives Rupert Murdoch and Lachlan Murdoch, along with Oracle founder Larry Ellison and Dell Technologies CEO Michael Dell, could play a role in shaping the future of TikTok USA.

The restructured ownership aims to ease national security concerns while keeping the platform accessible to its more than 100 million American users. The agreement also underscores the high stakes of balancing global tech investment with Washington’s demand for stronger oversight of foreign-linked digital platforms.

Recently, the EU/EC position has toughened on Israel’s genocide in Gaza. But why did the stance change only after the deaths and injuries of a quarter of a million Palestinians and both EC President von der Leyen and EU foreign policy chief Kallas have been charged for genocide?

Recently, EU foreign policy chief Kaja Kallas said that US support for “everything that the Israeli government is doing” limits the EU’s leverage to change the situation on the ground in the Gaza Strip.

That actions taken by the Israeli government in the Palestinian-occupied territories represent a ‘breach of essential elements relating to respect for human rights and democratic principles.

Subsequently, European Commission President Ursula von der Leyen, proposed sanctions to Israeli ministers and partial suspension of Israel trade deal. On Wednesday, the EU Commission’s review discovered – after 21 months of mass atrocities in Gaza and violent pogroms in the West Bank – that actions taken by the Israeli government in the Palestinian-occupied territories represent a ‘breach of essential elements relating to respect for human rights and democratic principles,’ which permits the EU to suspend the agreement unilaterally.

Recently, these sentiments were reinforced with the recognition of the state of Palestine by U.S. allies – the UK, Canada and Australia – and more recently by France.

Observers of Brussels declared that the EU had become tough on genocide. In reality, it was a last-minute effort by the two EU leaders to fuse rising outrage against EU’s Gaza policies and charges they were complicit in Israel’s atrocities.

How Kallas emboldened Israel in Gaza

Addressing the annual EU Institute for Security Studies (EUISS) conference in Brussels, Kajas said that US backing of Israel undermines EU leverage to stop the “Gaza war.” Yet, the United States has supported Israel for more than half a century.

US backing of Ukraine and Israel, division on Gaza

Kallas met with U.S. secretary of state Antony Blinken in Tallinn, 2022 Source: Wikimedia

“We are struggling because 27 member states have different positions,” on the issue, Kallas explained. “Europe can only use full force when it acts together.” In this way, accessorial complicity is first deflected to Washington and then attributed to the absence of European unity, which Kallas has long called for, to confront Russia. In other words, the EU Gaza apology was a thinly-veiled effort for a plea to unity Kallas hoped to turn against Russia in Ukraine.

When asked about “double-standard” accusations towards the bloc on its Gaza policy, Kallas said it is not true that the EU is inactive on Gaza. Yet, previously she had opposed intervention in Gaza. In mid-July, Kallas and the foreign ministers of the EU member states chose not to take any action against Israel over alleged war crimes in the Gaza war and settler violence in the West Bank.

The then-proposed sanctions against Israel would have included suspending the EU-Israel Association Agreement, suspending visa-free travel, and blocking imports from Israeli settlements. This decision emboldened the Netanyahu cabinet, which saw the EU’s decision not to impose sanctions on Israel as a diplomatic victory. It also led UN Special Rapporteur Francesca Albanese to conclude that EU officials like Kallas were complicit in Israeli war crimes in Gaza.

The EU is Israel’s biggest trading partner, accounting for a third of Israel’s total trade in goods with the world in 2024, whereas Israel is only the EU’s 31st largest trading partner. Consequently, the EU could easily have sanctioned Israeli trade right after the first genocidal atrocities in late 2023, yet it chose not to. Why?

How von der Leyen undermined EU’s credibility

Von der Leyen has a track-record of intimate relations with Israel. It was a source of controversy already before the Gaza catastrophe. On the 75th anniversary of Israel’s independence, half a year before October 7, 2023, she referred to Israel as a “vibrant democracy” in the Middle East that made “the desert bloom.” These remarks were criticized as racist by the foreign ministry of the Palestinian Authority because they erased the history of Palestinians in what is today Israel.

After the Hamas offensive, von der Leyen was criticized by EU lawmakers and diplomats for supporting Israel and not calling for a ceasefire. A week after October 7, she rushed to visit Israel to express solidarity, even as the Netanyahu cabinet spoke openly on the coming destruction of Gaza, and the ethnic cleansing of Palestinians. Then-EU foreign policy chief Josep Borrell criticized her for the pro-Israeli stance which “had a high geopolitical cost for Europe.”

The visit and the rhetoric also sparked furor among 841 EU staff who signed a letter to von der Leyen criticizing her stance on the conflict. In their view, the commission was giving “a free hand to the acceleration and the legitimacy of a war crime in the Gaza Strip” and warned that the EU was “losing all credibility and the position as a fair, equitable and humanist broker.”

Friends during happier times

Von der Leyen with Israeli President Isaac Herzog in Brussels, January 2023. A year later, Herzog said there are “no innocent civilians in Gaza” blaming all Palestinian civilians for Hamas’s attack. Source: Wikimedia

In reality, that credibility has eroded for years. By the early 2020s, more than 800 European financial institutions, including Europe’s most luminous financial giants, had financial relationships with over 50 businesses that were actively involved with Israeli settlements.

Why the belated moral outrage

Recently, the European Commission presented a proposal for tougher measures against Israel to the European Union, which featured suspending parts of the EU-Israel trade agreement and sanctioning Israeli far-right ministers and some West Bank settlers, along with Hamas leadership. These measures are very much in line with the EC chief’s previous warning. But why do they come only now – after 21 months of genocidal atrocities, the obliteration of Gaza and a quarter of a million killed or injured Palestinians?

A qualified majority vote among EU governments will still be required to pass the measures, with the support of at least 15 of the 27 EU members representing two-thirds of the EU population.

Moreover, von der Leyden’s Gaza criticism was carefully calculated to limit the scope of possible sanctions. “Man-made famine can never be a weapon of war,” she said. “For the sake of the children, for the sake of humanity – this must stop.”

Yet, Israel’s weaponized famines did not start few weeks ago. They date from the 2006 Palestine democratic election, which was won by Hamas in both Gaza and the West Bank. It led to Israel’s blockade, which was supported by the U.S. and the EU, and the Israeli-manufactured famine, designed to starve Gaza. The blockade paved the way to almost two decades of impoverishment, hunger, unemployment and thus to October 7, 2023. But it did not trigger condemnations by von der Leyden or the then-EU leaders.

Worse, the world witnessed the first starving victims in Gaza already in spring 2024. Yet, neither von Der Leyden nor other European leaders demanded the end to Israel’s actions at the time. And by the turn of 2023/24, still another famine way ensued, with similar silence in Brussels. It was only the third wave of famine in mid-2025 that changed their views. But why?

“What is happening in Gaza,” von der Leyden said, “has shaken the conscience of the world… These images are simply catastrophic.” That was the difference: not the realities of weaponized famines, which the world had witnessed for almost two decades in Gaza, but the images.

As those photos of starved bodies, particularly of children and babies, could no longer be halted or sidelined in international media, EU politicians, pushed by their constituencies, were compelled to act.

What European leaders chose not to do

It was when the European leaders were charged for accessorial complicity that von der Leyden and Kallas reacted. What the former proposed was “a package of measures” against Israel over its ongoing genocidal assault on Gaza. Or as she put it – and let’s italicize the key terms – “We will propose sanctions on the extremist ministers and on violent settlers. And we will also propose a partial suspension of the Association Agreement on trade-related matters.”

The EU would not use its full arsenal to change Israel’s conduct. It would only go after a few ministers of the Netanyahu cabinet, but not the cabinet itself, even though most of its members had been complicit to the Gaza catastrophe with some supporting even harsher measures, including “nuking” Gaza.

Similarly, the EU would only go after a few token settlers, not the illegal settlements that now house up to 750,000 Jewish settlers. Nor would the EU go after hardline Israeli politicians and civil administrators who have been preparing the incorporation of the West Bank into the pre-1967 Israel since their electoral triumph in late 2022.

The ties between Israel and the United States have expanded from hedging and strategic partnership into a virtual symbiosis. Since 1950, Israel has received more than $120 billion in U.S. aid, most of it in military aid; after October 7, this aid has soared up to $23 billion. But Washington is not Israel’s only ally. In the past half a decade, only three countries—the US (66% of Israel’s total arms imports), Germany (33%) and Italy (1%) —have supplied most of Israel’s arms.

Several other European countries have supplied vital military components, ammunition and services, including the UK, France and Spain. Meanwhile, small EU members like the tiny Finland are increasingly reliant on Israeli arms imports.

The elevated arms transfers reflect the contested European shift toward rearmament, at the expense of welfare and social services – despite the soaring challenges of aging demographics and climate change.

Protesters against the complicity of the EU leaders

Protest in Slovenia against the alleged complicity of Kallas and other EU politicians in the Gaza genocide, September 1, 2025. Source: Wikimedia

Genocide investigation against von der Leyen

Both Washington and Brussels are complicit to mass atrocities, due to their arms exports to Israel and financing through military aid, not to mention diplomatic and intelligence support. Article 3 of the Genocide Convention defines the crimes that can be punished under the convention, and these crimes include complicity.

In May 2024, the Geneva International Peace Research Institute (GIPRI), an NGO with UN consultative status, requested an investigation against the EC president, Ursula von der Leyen, for complicity in war crimes and genocide against Palestinian civilians. Her complicity was attributed to “violations of Articles 6, 7 and 8 of the Rome Statute by her positive actions (military, political, diplomatic support to Israel) and by her failure to take timely action on behalf of the European Commission to help prevent genocide as required by the 1948 Genocide Convention.”

The issue with too many European leaders is no longer only the crime of complicity, but also the concerted effort to deny that Israel’s crimes and atrocities against Palestinians constitute genocide.

According to Professor William Schabas, perhaps the leading scholar of genocide, ”von der Leyen is clearly reflecting a position taken by many EU-governments, which is one of very unconditional support of Israel, and they’re doing this flying in the face of public information suggesting that Israel is committing terrible crimes in Gaza and the West Bank.”

The issue with too many European leaders is no longer only the crime of complicity, but also the concerted effort to deny that Israel’s crimes and atrocities against Palestinians constitute genocide. Such denials should be seen as a form of “incitement” to hatred and violence, condemned by the Genocide Convention.

Legal efforts to go after genocide complicity entered a new stage recently, when a group of lawyers filed a criminal complaint against German Chancellor Friedrich Merz, key government officials and arms trade executives on Friday. A dozen high-ranking officials of the former and current German government and CEOs of arms manufacturers were accused of aiding and abetting Israel’s genocide in Gaza, by the European Legal Support Center (ELSC). “Given the undeniable, genocidal consequences of this support, we seek to hold them accountable,” said Nadija Samour, ELSC’s senior legal officer.

Recently, Spanish Prime Minister Pedro Sánchez noted that “what we’re now witnessing in Gaza is perhaps one of the darkest episodes of international relations in the 21st century.”

Tragically, the European leaders share full accessorial complicity in the decimation of Gaza and the genocide of its residents, plus the incorporation of the West Bank – that is, the massive moral collapse that is likely to cast a long, dark shadow over the 21st century because what has happened in Gaza is likely to be replicated elsewhere, with even more lethal results.

Building on The Obliteration Doctrine, the original commentary was published by Antiwar.com on September 23, 2025.

Government billing and payment modernization improves revenue collection, invoice settlement and service delivery to citizens. Ditching outdated methods in favor of efficient financial technology solutions reduces operational costs to manage limited budgets prudently and enhances security to prevent data breaches and combat fraud.

Discover the best solutions for your department by innovating government billing and payment processes.

Put a Premium on Diversity

Support diverse pull and push payment methods to satisfy different payer preferences and situations. More variety isn’t necessarily better, but accepting different cash and noncash options can balance each other’s strengths and weaknesses.

Integrate in-store, online, and mobile methods and synchronize payment data across all touchpoints through omnichannel payment.

In practice, a payer can begin a transaction on one channel and continue it on another while maintaining preferences and progress. A unified payment gateway handles the back end to ensure a seamless, consistent experience.

Explore Capabilities

Choose a billing and payment solution for government agencies with the best features to help payers initiate transactions painlessly. Seek platforms that support alternative payment methods to serve the unbanked and other underserved sectors of society.

Reliable government billing and payment technologies painlessly produce receipts. They generate reports and offer comprehensive data analytics tools to aid audits and promote transparency. Accessible tech support should be available to troubleshoot issues as quickly as possible.

Prioritize User Experience

Capitalize on user-friendliness to encourage repeated usage. An intuitive and accessible government billing and payment platform ensures anyone can conveniently use it, especially people with disabilities, older adults and the less financially literate.

A mobile-responsive interface, fast loading time, legible typography, straightforward navigation and simplified forms are must-have elements to increase revenue collection. Guest checkout and autofill are just as desirable.

Think About Regulations

Value compliance to uphold privacy, protect sensitive data and neutralize cyberattacks. Compare government billing and payment vendors based on the regulatory frameworks and industry standards they inherently observe.

Compliance requirements depend on the payment methods and currencies you intend to accept. Many solutions are preconfigured to abide by universally adopted standards, like the Payment Card Industry Data Security Standard (PCI DSS). However, bitcoin and other virtual currencies are a new frontier with distinct risks and merit more circumspection.

Consider Ease of Deployment

Understand how easy it is to integrate your prospective billing and payment platform into your system. Plug-and-play software solutions minimize disruption.

Credible vendors extend adequate technical guidance from beginning to end, onboarding your IT professionals properly. Explore after-sales support options to receive reliable assistance when something goes wrong and troubleshoot issues urgently.

Which Billing and Payment Solutions Are Best for Government Agencies? Top 3 Options

Comparing government billing and payment platforms can be overwhelming, so narrow your search with these three vendors.

1. KUBRA

KUBRA offers a citizen-facing portal for self-service interactions and one-click payments. It enables users to transact through web, mobile, an AI-powered interactive voice response (IVR) system, text messaging, in-person kiosks and retail locations. This software solution accepts credit cards, debit cards, automated clearing house (ACH) and digital wallets, including Venmo, Apple Pay, PayPal and Google Pay. This vendor supports bill consolidation, enrolled and non-enrolled payments, real-time processing and automated reminders.

This omnichannel billing and payment platform complies with Service Organization Controls (SOC) 1, 2, and 3, PCI DSS and Secure Stateless Tokenization. KUBRA undergoes penetration testing and annual third-party audits to discover and address vulnerabilities early. This vendor also has disaster recovery plans and carries cyber insurance.

2. CSG Forte

CSG Forte is one of the best plug-and-play platforms for municipal, county and state government agencies. Quick implementation is its calling card, as it can begin processing payments for utilities, permits and taxes in less than 24 hours. Its self-service capabilities include IVR payment processing optimized for touch-tone and speech recognition. CSG Forte also handles cash, ACH, eCheck and digital wallets.

This platform integrates with billing and accounting systems with minimal technical expertise requirements. CSG Forte links to point-of-sale systems optimized for Europay, Mastercard and Visa, allowing it to process contactless payment transactions — whose value reached $7.4 trillion in 2024 and is expected to grow by 113% over the next five years.

3. GovPilot

GovPilot is a cloud-based digitalization platform offering prebuilt payment-related modules that reflect the needs of most municipal governments and customized ones for specific agencies. This solution streamlines revenue tracking and integrates payment processing for online business registration applications and pet licensing. It also facilitates court and permit fee collection.

This vendor’s implementation support includes free consultation, 15-minute tailored demonstrations and dedicated account managers. Depending on your chosen plan, you can enjoy four days of in-person training, legacy data importing and migration assistance. GovPilot is a Microsoft Azure partner and supports data backup, disaster recovery, penetration testing and annual third-party security validation.

Use the Best Billing and Payment Solution for Your Government Agency

Many billing and payment vendors target local, state and federal governments and optimize their features accordingly. Learn more about each software solution’s offerings to find the perfect fit for your agency.

Financial technology, or fintech, is evolving at breakneck speed. To stay ahead, financial institutions and startups alike need software development partners who understand the unique challenges and opportunities of the industry. We’re talking about companies prioritizing speed, compliance and scalability in everything they do. Five fintech software development companies stand out in this area.

Choosing a FinTech Partner

Use these signals to gauge whether a partner can deliver in regulated markets:

Proof of shipping in complex environments with clear service level agreements (SLAs), measurable outcomes and on call ownership

Depth in data, cloud, and security engineering that supports 24/7 uptime and fast rollback

Strong product strategy with discovery, UX and analytics built into the delivery rhythm

A roadmap culture that learns from telemetry, incidents and customer research

These signals show a partner can handle live systems and real risk. SLAs, measurable outcomes and on call ownership mean they own uptime and fix issues fast. Strong data, cloud and security skills, plus a product practice that learns from users and incidents, help teams ship the right features safely and on time.

Why Does Having a Custom Fintech Solution Matter?

Custom fintech software allows businesses to tailor solutions to their unique needs, gaining a competitive edge by addressing specific market gaps or customer demands. This bespoke approach enables enhanced security measures and compliance protocols — crucial for maintaining trust and navigating complex regulatory rules.

Having the right software partner fosters innovation and agility, empowering companies to adapt quickly to market trends and customer needs.

Top Financial and Fintech Software Development Companies

Below are five providers to watch in 2025. Each shows a pattern you can use when selecting a build partner or benchmarking your stack.

1. Sparq

Sparq leads with multidisciplinary agile teams that plan, build and run mission-critical financial software. The firm markets an outcome-based approach that aligns strategy, design and engineering under one delivery model. It supports banks, insurers and fintechs that need compliant releases and ongoing iteration, not staff augmentation alone.

Sparq has also expanded its capabilities with recent U.S. acquisitions that have strengthened data and AI engineering. That added capacity helps ship features faster while tightening quality and security controls. Teams that operate at this level reduce cost overruns, halve handoffs and raise deployment frequency.

2. Nova Money

Nova Money takes a forecasting-first approach to personal finance. It pulls Open Banking data, projects cash flow and flags overspending before it derails goals.

Nova lists TrueLayer as its regulated AISP provider, which adds credibility around data access and permissions. The planning model suits variable income, subscription-heavy budgets and early warning of cash gaps.

3. Vivid Money

Vivid Money combines banking, savings, investing and rewards in one European app. Users can open multiple “Pockets,” each with its own IBAN, to segment spending and goals. Tiered plans expand the number of Pockets and raise cashback limits, encouraging stickiness and higher product utilization. This bundling playbook helps increase lifetime value without piling on complexity.

4. Credello

Credello focuses on decision support. It offers AI-driven recommendations, calculators and payoff planners that help consumers compare loans, cards and strategies.

Its consumer research points to growing comfort with AI chat for money guidance, which supports its product direction and content engine. Modular tools, transparent explanations and simple UX keep friction low while driving organic reach.

5. Revolut

Revolut operates globally across retail and business products. In 2024, it reported £3.1 billion in revenue with strong profitability and bigger customer balances. In 2025, news outlets reported a secondary share sale that implied a valuation near $75 billion. This breadth — paired with fast shipping and growing subscription revenue — makes Revolut a bellwether for digital finance.

Market Signals to Watch Out For

Analysts project the global fintech market to be worth about $394.88 billion in 2025 and reach roughly $1.12 trillion by 2032. That growth path supports investment in modern stacks, stronger data pipelines, and better onboarding flows.

The pandemic accelerated the digital transformation of financial services. Banks and consumers shifted to online channels, raising demand for platforms that handle identity, risk and payments at scale. Global policy groups also note the broader surge in digital adoption across advanced economies, shaping how teams prioritize roadmaps.

When you evaluate top financial and fintech software development companies, ask how teams connect design decisions to compliance outcomes. Look for data lineage, runtime monitoring and rollback plans that align with your risk appetite. Partners that show this discipline can ship faster with fewer surprises.

Choose a Partner Then Validate Results

Set a 90-day target and shortlist two vendors. Ask each for a reference architecture and a one-sprint proof of concept, then score them on deploy frequency, change fail rate, time to recovery and cost per transaction in your environment. Choose the team that demonstrates the most promising results.

Commit to shipping one feature that improves onboarding speed or fraud detection so you can turn careful evaluation into measurable growth.

U.S. President Donald Trump on Monday urged pregnant women and parents to avoid using Tylenol and cautioned against routine childhood vaccinations, reviving claims that scientists and health agencies have repeatedly rejected.

In a White House news conference, Trump advised against acetaminophen, the active ingredient in Tylenol, and suggested that vaccines should not be given together or administered too early in life. “I want to say it like it is, don’t take Tylenol. Don’t take it,” he said. The president also argued for splitting the measles-mumps-rubella vaccine into separate doses and delaying the hepatitis B shot, which is normally given at birth.

Trump’s comments drew immediate criticism from medical groups. The American Academy of Pediatrics, the American College of Obstetricians and Gynecologists, and autism advocacy organizations warned that his statements risked spreading misinformation. “The data cited do not support the claim that Tylenol causes autism and leucovorin is a cure, and only stoke fear and falsely suggest hope when there is no simple answer,” the Coalition of Autism Scientists said.

Standing alongside Health Secretary Robert F. Kennedy Jr., a long-time vaccine critic, Trump also promoted leucovorin, a folinic acid treatment normally used in cancer care, as a potential therapy for autism symptoms. The Food and Drug Administration later said it would expand production and consider Medicaid coverage for the drug, even though researchers caution that only small, inconclusive studies exist.

Kenvue, the maker of Tylenol, rejected the president’s claims. “We believe independent, sound science clearly shows that taking acetaminophen does not cause autism. We strongly disagree with any suggestion otherwise and are deeply concerned with the health risk this poses for expecting mothers and parents,” the company said in a statement.

Britain’s health regulator also reaffirmed that paracetamol, as the drug is known in Europe, remains safe during pregnancy.

Markets reacted swiftly, with Kenvue shares tumbling more than 7% before recovering 5% in late trading. Analysts at Citi said the rebound reflected the absence of new scientific evidence. The stock remains down 14% since early September when reports surfaced that Kennedy planned to push an acetaminophen-autism link.

The Food and Drug Administration announced it would seek new labeling for Tylenol and generic versions, warning of a possible association between prenatal exposure and neurological conditions such as autism and ADHD. Still, the agency acknowledged no causal relationship has been proven.

Recent studies underscore that uncertainty. A 2024 Swedish study of 2.5 million children found no evidence that prenatal Tylenol exposure causes autism or other neurodevelopmental disorders. A 2025 review of 46 studies suggested a possible link, but researchers from Harvard, Mount Sinai, and other institutions said the findings did not prove causation and urged pregnant women to continue using acetaminophen when medically necessary, at the lowest effective dose.

Experts condemned the administration’s stance. “Without showing any evidence to back them up, the announcements become reckless and potentially harmful,” said Dr. Diana Schendel of the A.J. Drexel Autism Institute. Autism specialist Dr. Audrey Brumback of the University of Texas at Austin added that leucovorin trials remain too small and weak to justify its use as a treatment.

Scientists stressed that vaccines are safe, noting they have eradicated diseases such as polio and measles in the United States. UNICEF USA estimates childhood vaccines have saved at least 154 million lives over the past 50 years.

As Generative Artificial Intelligence (Gen AI) continues to revolutionize industries, forward-thinking organizations must develop robust strategies to integrate this transformative technology into their operations. A well-executed Gen AI learning program not only equips employees with the skills to leverage these tools effectively but also fosters a culture of innovation and continuous improvement. Yet, the path to successful implementation is rarely straightforward. A phased approach to deploying a Gen AI learning program can ensure a seamless rollout while driving meaningful business outcomes.

Why a Phased Approach Works for Gen AI Learning

Launching a Gen AI learning program across an organization is inherently complex. Employees bring varying levels of technological proficiency, and different teams have distinct workflows and priorities. A phased approach helps to navigate these challenges by introducing Gen AI training gradually. Starting small—through pilot programs—enables organizations to refine the program, address challenges early, and scale up with confidence.

Departments selected for the pilot phase should demonstrate both high potential for impact and readiness for change.

The phased approach begins with pilot programs in specific departments or teams. These pilots act as testbeds to evaluate the effectiveness of the learning content, training delivery, and support mechanisms. Departments selected for the pilot phase should demonstrate both high potential for impact and readiness for change. For instance, teams in data analysis, customer service, or product development often serve as ideal candidates because they already use AI-adjacent tools or stand to gain significantly from Gen AI integration.

During the pilot phase, the organization can closely monitor progress, gathering valuable feedback to make iterative improvements. Adjustments might include fine-tuning the curriculum, enhancing user interfaces for training platforms, or integrating additional resources to bridge knowledge gaps.

The iterative refinement doesn’t stop at the pilot stage. As the program expands to other departments, feedback loops remain crucial, ensuring that the learning experience evolves to meet employees’ changing needs. This continuous improvement process positions the organization to maximize the value of Gen AI tools across its operations, while managing risks.

Key Considerations for Implementing a Phased Gen AI Learning Program

Implementing a phased Gen AI learning program requires careful planning and execution. Here are some key considerations to ensure success:

Assess Organizational Readiness: Before launching the program, evaluate the organization’s current technological infrastructure, employee skill levels, and openness to change. This assessment will help identify potential challenges and areas that require additional support.

Define Clear Objectives and Metrics: Establish specific, measurable goals for the Gen AI learning program. These could include improvements in productivity, employee proficiency with AI tools, or the development of new AI-driven products or services. Defining clear KPIs will enable the organization to track progress and make data-driven decisions.

Develop Tailored Training Content: Create training materials that are relevant to the specific needs and workflows of each department. Tailored content will enhance the learning experience and ensure that employees can apply Gen AI tools effectively in their roles.

Foster a Supportive Learning Environment: Encourage a culture of continuous learning by providing ongoing support, resources, and opportunities for employees to practice and apply their new skills. This could include access to AI experts, online forums, or collaborative projects.

Monitor Progress and Solicit Feedback: Regularly assess the effectiveness of the training program through surveys, assessments, and performance metrics. Use this feedback to make iterative improvements and address any emerging challenges promptly.

Scale Strategically: As the program expands to other departments, maintain flexibility to adapt the training content and delivery methods based on the unique needs and feedback of each team. Strategic scaling will ensure that the program remains effective and relevant across the organization.

The Role of Leaders

Leadership plays a crucial role in the successful adoption of Gen AI within an organization. Leaders must champion the initiative, allocate necessary resources, and communicate the strategic importance of Gen AI to all stakeholders. By demonstrating commitment and providing a clear vision, leaders can inspire confidence and motivate employees to embrace the new technology.

Moreover, leaders should prioritize ethical considerations and responsible AI use. This includes ensuring data privacy, addressing potential biases in AI algorithms, and promoting transparency in AI-driven decisions. By fostering an ethical AI culture, organizations can build trust and mitigate risks associated with AI implementation.

Case Study: A High-Tech Manufacturer’s Journey

Consider the case of a high-tech manufacturing company aiming to integrate Gen AI into its product design processes. Recognizing the potential for AI to accelerate innovation, the company hired me as a consultant to help it adopt a phased approach, starting with a three-month pilot program in the product design department.

Consider the case of a high-tech manufacturing company aiming to integrate Gen AI into its product design processes.

The pilot focused on teaching designers how to use Gen AI tools to streamline design iterations, generate creative concepts, and optimize material usage. We gathered feedback through surveys and interviews, which highlighted several areas for improvement. For instance, participants suggested simplifying technical modules and incorporating more practical, hands-on exercises. We made adjustments accordingly, resulting in higher engagement and improved learning outcomes.

After achieving a 40% increase in Gen AI proficiency and an 18% boost in productivity within the design team, we expanded the program to engineering and marketing. Each rollout phase was guided by clear milestones, such as completing specific training modules or achieving measurable productivity gains. By the end of the nine-month implementation, the organization experienced a 14% overall productivity improvement, showcasing the value of the phased approach.

Conclusion

Integrating Generative AI into an organization’s operations offers significant opportunities for innovation and efficiency. However, successful adoption requires a strategic, phased approach to learning and development. By starting with pilot programs, gathering feedback, and scaling thoughtfully, organizations can equip their workforce with the necessary skills and foster a culture of continuous improvement.

Critical raw materials (CRMs) such as lithium, cobalt, rare-earth elements, and copper are central to the green and digital transitions. Dr Kalim Siddiqui emphasises that their economic significance lies not only in enabling technologies—batteries, electric vehicles, renewable energy, and microchips—but also in the concentration of supply chains. China controls about 70 percent of global rare-earth output and 80–90 percent of processing capacity, creating systemic dependencies.

I. Introduction

Critical minerals—especially rare earth elements—are increasingly essential to reducing pollution, lowering carbon emissions, and driving technological innovation toward a more sustainable future. Their significance, however, extends beyond environmental benefits. For advanced economies, secure access to these materials has become a strategic priority, shaping industrial competitiveness and reinforcing corporate power, while simultaneously intensifying geopolitical rivalries over control of critical supply chains. Consequently, rare earth elements have emerged as both a foundation of technological progress and a source of global tension, fuelling new forms of geopolitical rivalry.

These critical raw materials are essential for renewable energy technologies, high-tech manufacturing, and advanced military systems, including electric vehicles, wind turbines, fighter jets, missiles, and radar. As economic historian from Columbia university Adam Tooze (2025) notes, “if fossil fuels heralded the industrial revolution with the West leading it, the green energy transition is clearly being led by Asia, with China as its global leader.” This shift underscores the growing strategic importance of rare earths in shaping global power dynamics.

If fossil fuels heralded the industrial revolution with the West leading it, the green energy transition is clearly being led by Asia, with China as its global leader.

Critical raw materials (CRMs) are indispensable for 21st-century economies, particularly in mitigating global warming and reducing pollution. The green and digital transitions rely heavily on resources such as lithium, cobalt, rare-earth elements, and copper, which are integral to batteries, electric vehicles, renewable energy systems, and microchips. This growing dependence on CRMs has generated new geopolitical vulnerabilities and dependencies, prompting strategies such as the European Union’s Critical Raw Materials Act, which seeks to diversify supply chains through domestic extraction, processing, and recycling (Brown, et al 2024).

This study examines the importance of CRMs in the coming decades, with a focus on their role in global production and supply. It also considers potential counterstrategies for reducing reliance on CRMs, including material substitution, reduced consumption, recycling, and re-use. The adoption of environmentally sustainable technologies (Siddiqui, 2025a) and new energy systems depends fundamentally on securing access to these materials. Yet the supply of CRMs remains heavily concentrated in the Global South and within a handful of large corporations, fuelling tensions among the developed countries.

Under capitalism, development is driven primarily by private corporations, where private investments play an important role in the overall grow. Most of the developing countries lack funds and modern technology to mine and processes the CRMs and convert them into finished products. The current energy transition is likely to reproduce the contradictory socio-spatial dynamics that characterized the carbon-based industrial revolution. These dynamics would likely exacerbate inequality while delivering transformative benefits primarily to the Global North.

The designation of CRMs as “critical” stems from their strategic significance across multiple sectors. They are essential not only to electronics and defence industries but also to renewable energy technologies such as solar panels, wind turbines, and electric vehicles. For instance: Lithium is crucial for batteries used in electric vehicles and renewable energy storage. Cobalt is a vital component in advanced batteries and other emerging technologies (Brown, et al 2024).

Many countries remain heavily dependent on a limited number of suppliers of CRMs—particularly China—for the processing and supply of critical raw materials, creating significant strategic vulnerabilities. In response, the European Union (EU) and the United States (US) have introduced policy initiatives, such as the EU Critical Raw Materials Act, aimed at strengthening supply chain security by enhancing domestic capabilities in mining, processing, and recycling. The availability of rare earths and other CRMs has become indispensable for the US, the EU, Japan, and other advanced economies, particularly given the global expansion of renewable energy technologies, digitalisation, and the proliferation of artificial intelligence–embedded devices.

For most CRMs, many countries are structurally import-dependent, with limited or no viable substitutes. Supply is further constrained by low recycling rates, technological challenges in recovery, and the concentration of production within a few dominant suppliers. This scarcity, combined with rising demand, has intensified global competition to secure access to key materials such as lithium, cobalt, copper, nickel, and other CRMs. Control over these resources is increasingly seen as essential for maintaining technological leadership in the 21st century (OECD, 2023).

According to the International Energy Agency (IEA), China’s dominance in the processing and refining of these minerals’ ranges from 80 to over 90 percent of global capacity, positioning it as a central actor in emerging technology and energy supply chains.

The US–China dispute over rare earths illustrates this vividly. During Trump administration’s tariff war (Siddiqui, 2025b), China temporarily suspended certain rare earth exports to the US because China produces about 70 percent of global output and controls roughly 90 percent of processing capacity, this moves exposed the US’s dependence. Alternative suppliers were unable to compensate for China’s dominance, forcing the US to negotiate for the resumption of supplies. This episode crystallized the geopolitical stakes of resource dependence: securing access to CRMs is now treated by the West as a matter of national security and technological survival.

The US now has sought to diversify its supply base, including exploring opportunities in Greenland and other territories rich in strategic minerals. Yet such alternatives cannot fully replace China’s dominance, since it possesses nearly half of known global reserves of rare earth elements (REEs). The REEs are a group of 17 metallic chemical elements—the 15 lanthanides, plus yttrium and scandium—that share similar properties, such as high conductivity, magnetism, and fluorescence. They are indispensable for high-performance magnets in wind turbines, electric motors, and other advanced applications. They are essential for modern technologies like wind turbines, electric vehicle motors, and consumer electronics, as well as for green energy initiatives (Goodenough, et al 2018).

II. Imperialism, Foreign Markets, and the Struggle for Critical Minerals

This reality resonates with the broader insight of Marxist scholar Rosa Luxemburg that imperialism functions not merely as a project of market expansion, but also as a means of securing indispensable resources beyond the reach of metropolitan capitalism itself. In the twenty-first century, this dynamic is exemplified by the struggle for critical minerals—lithium, cobalt, nickel, rare earths—which has become a defining axis of contemporary imperial rivalries. This phenomenon aligns with Lenin’s analysis of capitalist imperialism, which he theorized as a definitive, high-stage development of capitalism. In this stage, fundamental characteristics like free competition mutate into their opposites: monopoly. Lenin observed this transition as the concentration of production and capital inevitably displaces free competition with monopoly, creating large-scale industry that eliminates smaller competitors. This economic shift fosters a global hierarchy wherein monopolistic powers export capital to less developed countries in pursuit of higher profits, exploiting these regions and ultimately generating the international conflicts that characterize the imperialist epoch (Siddiqui, 2022).

The Industrial Revolution began in Britain, particularly in Manchester’s cotton textile industry, during the second half of the eighteenth century. Cotton manufacturing was driven by the application of new technologies that dramatically increased productivity. However, Britain neither cultivated the raw cotton required for textile production nor initially possessed the necessary expertise to establish large-scale cotton industries. To overcome these limitations, Britain relied heavily on its colonies—India, Egypt, and later the US—for the supply of raw materials. This reliance had devastating consequences for colonized economies. India’s flourishing textile industries, for example, were systematically dismantled, forcing the country to specialize in the production of raw cotton for British industry.

As British factories began producing textiles in bulk, the demand for foreign markets to absorb this output intensified. This demand was met through the deliberate destruction of India’s indigenous textile industry, which had long exported high-quality cotton and silk to global markets. Consequently, India was transformed from a leading exporter of textiles into a captive importer of British-manufactured goods. In short, the rise of industrial capitalism was predicated on the metropolis securing cheap raw materials from its colonies and dismantling their existing industries.

This dynamic has persisted into the present. While the composition of industrial output in advanced capitalist economies has changed over time—with new products replacing old ones—the structural dependence on external sources of raw materials remains. Many of these essential resources lie outside the territorial domain of metropolitan capitalism, yet their reliable supply remains crucial. Ensuring such access has historically provided, and continues to provide, a powerful motive for imperialist control over resource-rich regions.

In teaching political economy, I emphasize to my students that mainstream economics typically treats the supply of raw materials as if it occurs through “normal” commodity exchange in free markets. The assumption is that these resources are acquired voluntarily and without coercion. Historical reality, however, tells a different story. The extraction and trade of raw materials have long been shaped by colonial domination, coercion, and asymmetrical power relations. Mainstream economists, by ignoring these imperialist dimensions, erases the role of force and dependency in the global supply of raw materials (Siddiqui, 2018a).

A second argument often advanced by mainstream economists against the claim that capitalism drives imperialism concerns the relative insignificance of raw materials in the value composition of metropolitan output. Since the share of such inputs from the “outside” world appears small in quantitative terms, many mainstream economists dismiss the idea that advanced capitalist countries would undertake the immense costs and risks of imperialist expansion simply to secure resources that constitute a minor fraction of total output value.

Marxist scholars, however, have long challenged this reasoning. Harry Magdoff, in The Age of Imperialism (1969), argued that securing vital raw materials and other inputs from colonies has been a paramount necessity for metropolitan capitalism. Agricultural commodities and food crops have historically been central to this logic, as metropolitan powers sought to reorganise land use across the globe to serve both industrial needs and domestic consumption. For the purposes of this discussion, however, the focus is on minerals. The strategic dependence of metropolitan capitalism on external mineral supplies is starkly illustrated by recent US experiences with rare earth elements.

The economic ascent of Western Europe from the 16th to the 19th centuries was not an isolated phenomenon. It was fundamentally predicated on the large-scale extraction of wealth and resources from the global South. This presentation will argue that European capital accumulation and industrialization were directly fuelled by the systematic plunder of Latin America, Africa, and Asia, often through coercive and violent means.

For example, European powers, led by Spain, extracted thousands of tons of silver and significant quantities of gold. A primary source was the Potosí mines in modern-day Bolivia. This extraction is more accurately characterized as plunder rather than equitable trade. The immense influx of precious metals generated massive wealth for colonial powers but also triggered profound economic shifts in Europe, notably the so-called “Price Revolution,” a period of widespread inflation. Historical evidence demonstrates that European industrialization created an insatiable demand for raw materials, which was met through the coercion of African and Asian societies (Siddiqui, 2021).

This exploitative process culminated in the late 19th century with the “Scramble for Africa.” This period of intense imperial competition was fundamentally a race to claim and directly administer African territory and its vast resources, formalizing and intensifying patterns of extraction. This systematic transfer of wealth is central to explaining the “Great Divergence”—the period where Western Europe’s economic power dramatically outpaced the rest of the world. The capital and resources acquired through these practices were not merely supplemental; they were a critical precondition for European industrialization and global economic dominance (Siddiqui, 2018b).

During the Trump administration’s tariff disputes with China, China responded by temporarily suspending certain rare earth exports to the US. Given that China produces around 70 percent of global rare earth output and controls approximately 90 percent of processing capacity, this move left the US in a precarious position. Alternative suppliers could not compensate for China’s dominance, as no other country possessed comparable production capacity. As a result, the US was compelled to negotiate with China, linking the resumption of rare earth supplies to broader trade concessions.

This episode underscores the strategic vulnerability of advanced economies and highlights how access to critical minerals fuels imperialist expansion. In an effort to reduce reliance on Chinese supply, the US has pursued alternative sources, including Greenland, which is rich in a range of mineral resources. While American interest in Greenland predates the rare earth dispute, China’s temporary suspension of exports sharpened US strategic focus on the territory. Yet even these efforts cannot fully replace Chinese dominance, as China controls nearly half of the world’s known reserves of rare earths. This case encapsulates a central motivation for contemporary capitalist imperialism: the drive to secure and control indispensable raw materials, regardless of their proportionate share in the total value of metropolitan output.

Rosa Luxemburg is her book The Accumulation of Capital (1919) highlighted the importances of markets for imperialism, arguing that sustained capital accumulation within the metropolis was impossible without penetrating pre-capitalist markets abroad. For this reason, annexations and interventions in “outside” territories became a structural necessity. While other external stimuli for metropolitan capitalism can be identified—such as demand generated by the capitalist state—these have limited scope, especially in the era of globalization. By contrast, there are no substitute sources within the metropolis for the raw materials it requires. The quest for raw materials, and especially minerals, thus remains a permanent and indispensable motive for capitalist imperialism (Siddiqui, 2022).

The intensity of imperialist intervention has historically escalated whenever countries in the Global South have sought to assert sovereign control over their natural resources. After political decolonization, many states attempted economic decolonization by reclaiming authority over mineral wealth. These efforts often provoked violent backlash from metropolitan powers. The US- and Europe-backed coups against Mossadegh in Iran, Arbenz in Guatemala, Allende in Chile, and Lumumba in Congo were all directly tied to attempts at resource nationalization (Siddiqui, 2021).

With the consolidation of neoliberal globalization, direct coups became less frequent as structural adjustment programs, debt conditionalities, and trade liberalization restored metropolitan capital’s control over resource flows (Siddiqui, 2018a). This institutionalized dependency, embedding neocolonial relations in international financial and legal frameworks. Yet as the neoliberal order falters, US imperialism has sought to manage global imbalances by compelling Global South economies to specialize in raw material exports in order to earn foreign exchange and service external debts. These pressures have, in turn, reignited calls for a new international economic order and renewed struggles for resource sovereignty (Siddiqui, 2025a).

III. China’s Strategic Dominance: Processing as Power

In global supply chains for critical minerals, control over processing—not raw production—determines strategic power. China has secured dominance by investing heavily in refining and processing capacity, even when it is not the largest holder of reserves. China dominates the global rare earth supply chain, controlling roughly 70% of mining and over 90% of refining capacity. It produces around 92% of high-strength permanent magnets, critical for civilian and military applications. China has also strategically invested abroad, partnering with countries in Africa, Latin America, and Southeast Asia, including the Congo, Bolivia, Chile, and Myanmar, often linking mineral extraction with infrastructure under the Belt and Road Initiative (Siddiqui, 2019).

This dominance allows China to exercise leverage over global technology and defence sectors. Even countries rich in raw materials, such as Australia and Vietnam, remain dependent on Chinese refining capabilities, illustrating the structural asymmetry in global mineral supply chains. For example, in the case of natural graphite—vital for batteries, lubricants, and industrial applications—China accounts for about 72% of global production but controls 100% of processing capacity. All graphite destined for global markets must therefore pass through Chinese facilities. While China holds roughly 28% of global reserves, Brazil follows closely with 26%. New suppliers, such as Mozambique (10% of production) and Madagascar (8%), have entered the market, but without processing plants they remain dependent on external technology and investment, leaving China’s dominance intact.

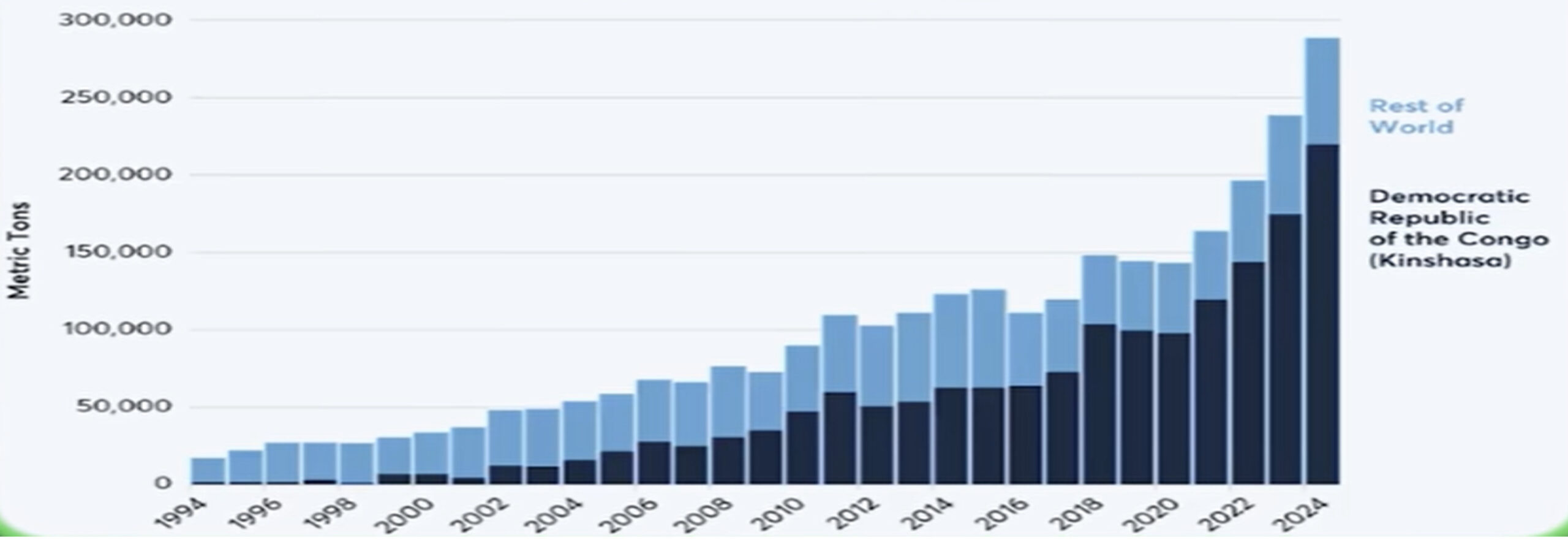

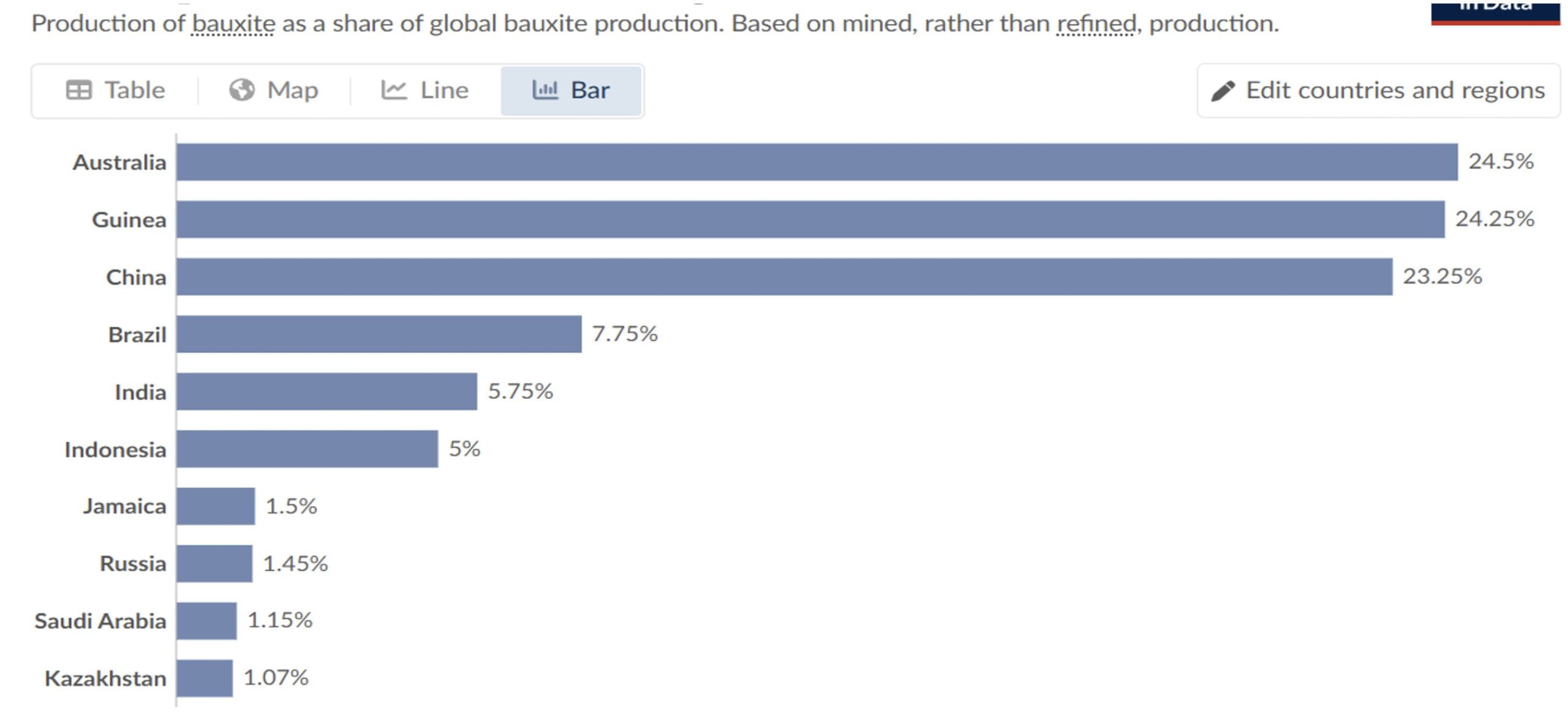

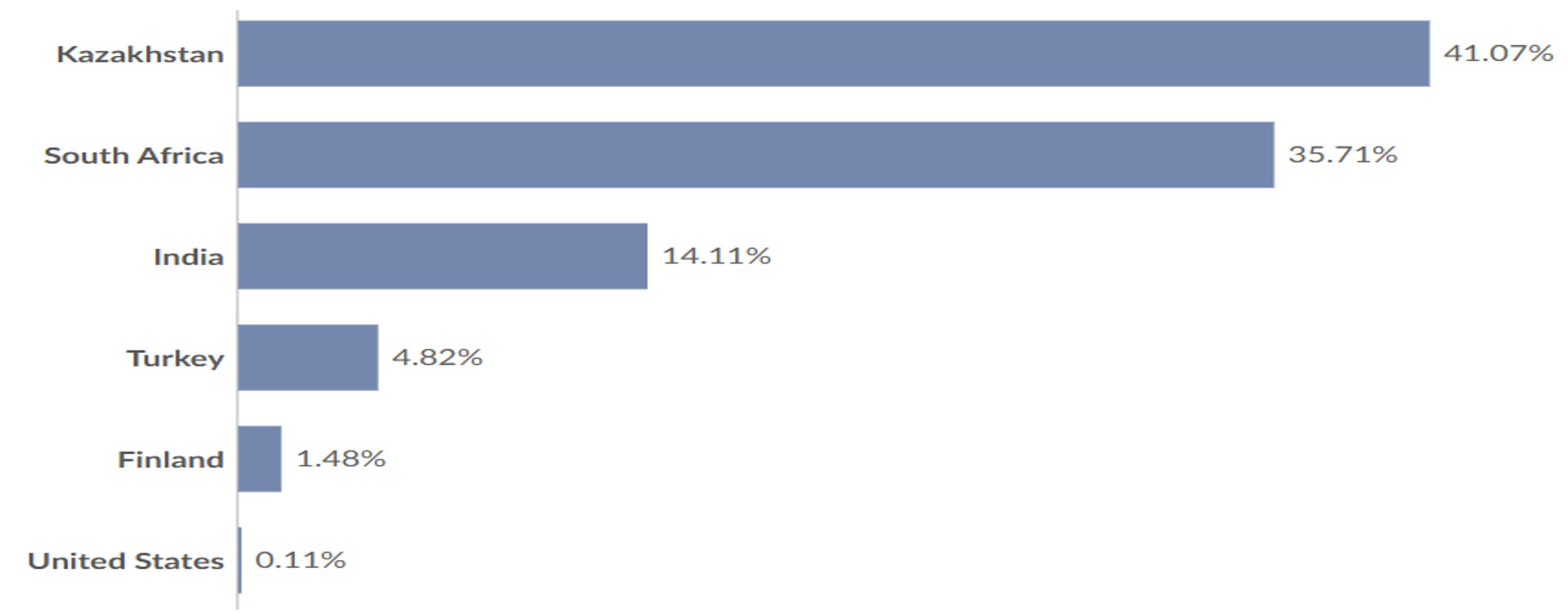

This enduring dynamic is starkly visible in contemporary struggles over CRMs. Reserves are highly concentrated in particular regions: China dominates rare earth production and processing; Congo is the world’s largest cobalt producer (see Figure 1); Chile, Argentina, and Australia hold major lithium reserves; Australia and Indonesia lead in nickel; Brazil and Mozambique in natural graphite; and Australia, Guinea, China, Brazil, India and Indonesia in bauxite (as illustrated in Figure 2). Large reserves of chromium deposits are found in Kazakhstan, South Africa, and Turkey (see Figure 3). Hence, such geographical concentration underpins metropolitan capitalism’s structural vulnerabilities.

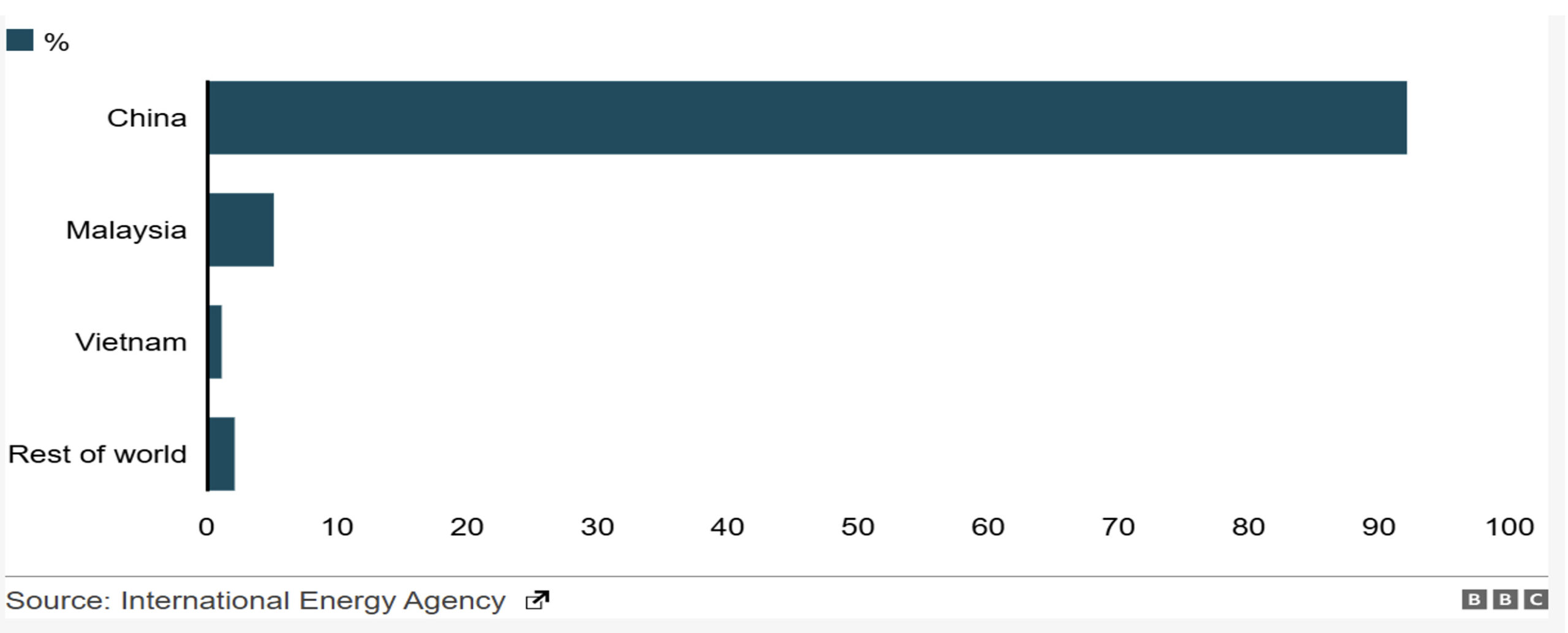

Rare earth elements (REEs) illustrate this dynamic even more clearly. Despite accounting for around 70% of REEs mining and 90% of processing, China’s leverage derives primarily from its refining capacity rather than from reserves alone (as shown in Figures 4a and 4b). The US (14% of production) and Australia (6%) contribute to extraction but continue to rely heavily on China for processing, highlighting the structural asymmetry of the supply chain.

China’s willingness to absorb these costs—backed by long-term state support—has allowed it to capture a near-monopoly over the most value-added segment of the supply chain.

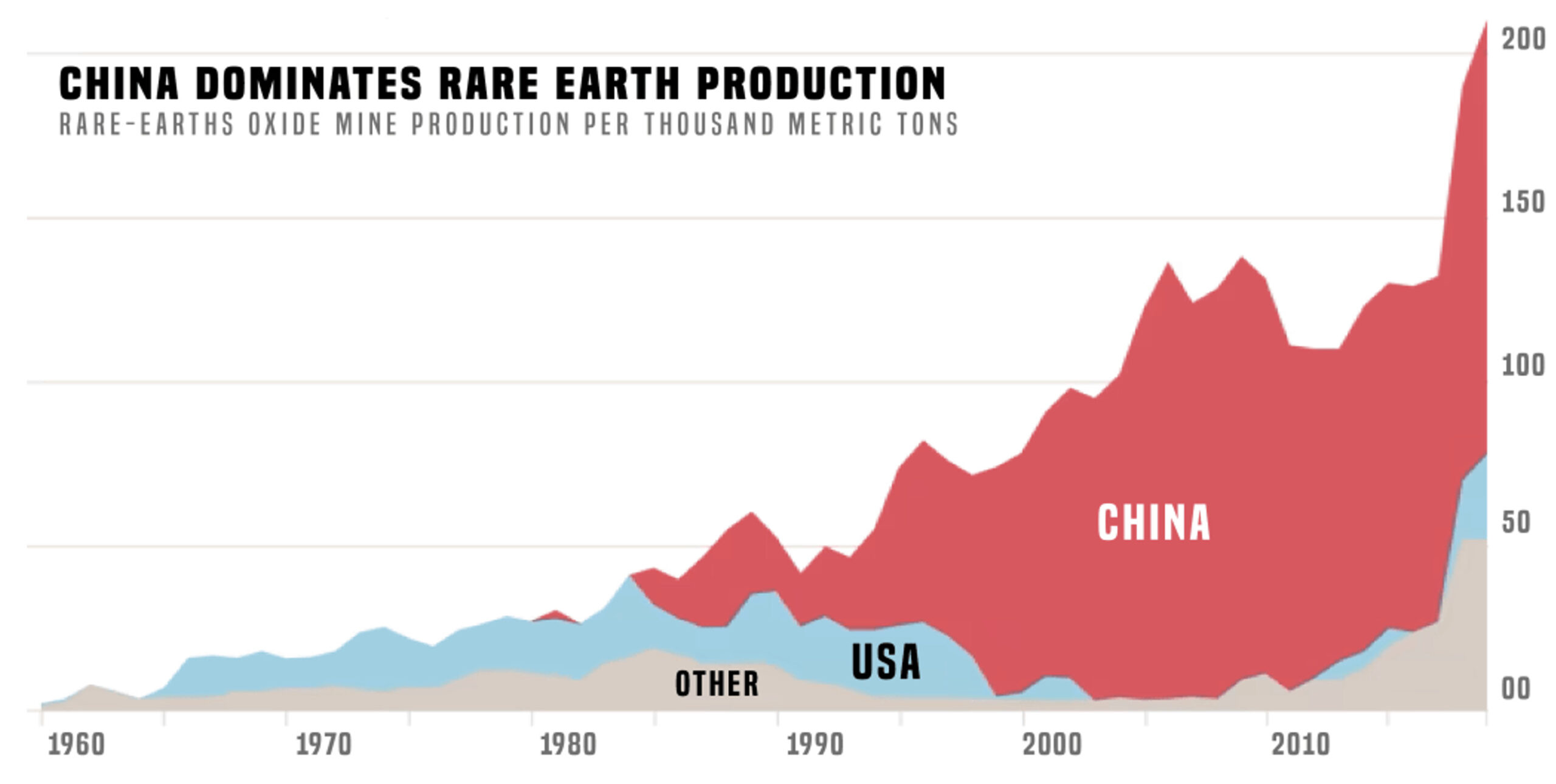

Over the years China has invested heavily in both production and processing of rare earth elements (as illustrated in Figure 5). Hence, this dominance is not accidental. Processing rare earths and other strategic minerals is technologically complex, capital-intensive, and environmentally costly. China’s willingness to absorb these costs—backed by long-term state support—has allowed it to capture a near-monopoly over the most value-added segment of the supply chain.

Figure 4a: Known Rare Earth Elements Reserves by Country (metric tons), 2024.

Figure 5: China’s Production of Rare Earth Elements, 1960-2024.

The US and the EU have begun to respond. In 2023, three US-based recycling facilities for strategic minerals became operational, aiming to reduce dependence on imports and diversify supply chains. Similar initiatives in Australia, Canada, and the EU mark an important shift, though they remain in their early stages.

Overall, China’s overwhelming control of processing capacity reveals the central paradox of the critical minerals’ economy: resource abundance alone does not confer strategic advantage; control over processing does. By dominating refining capacity, China has positioned itself as the indispensable hub of global supply chains, securing both economic leverage and geopolitical influence in the transition to clean energy and advanced technologies.

IV. The United States Dependence

The US depends heavily on rare raw materials on China for its strategic industries, including defence, renewable energy, and high-tech manufacturing. Estimates suggest that the US relies on China for roughly 70% of its rare earth compound and metal imports. This dependence is compounded by the fact that China dominates both mining volumes and, more importantly, the processing capacity required to transform raw materials into usable inputs. Over 50% of another 29 critical minerals are imported by the US. It plans to reduce this dependence include developing domestic mining and processing capabilities, recycling initiatives, and partnerships with allied countries such as Australia and Canada (OECD, 2023).

Policy measures across administrations highlight the growing strategic importance of mineral supply chains. Executive Order 14017 under Biden and the use of the Defence Production Act under Trump demonstrate recognition of the vulnerabilities posed by reliance on foreign refining capacity (Siddiqui, 2025c). However, building a complete, resilient supply chain remains a long-term challenge, requiring investments in extraction, refining, manufacturing, and recycling. Recognizing these vulnerabilities, US has increasingly sought to diversify its supply chains and reduce reliance on China. Efforts include expanding domestic mining and processing capabilities and forging partnerships with resource-rich allies such as Australia and Canada. These measures by the US aims to develop alternative supply chains that are both secure and resilient.

US policy responses have evolved across administrations. The Trump administration first designated rare earths as critical to national security but notably exempted them from the 2018 tariffs imposed on Chinese goods. The Biden administration adopted a more structured approach, issuing Executive Order 14017 on America’s Supply Chains and allocating dedicated funding for critical minerals. Under Biden, multilateral initiatives such as the Minerals Security Partnership were also launched to coordinate supply chain diversification with allied countries. The second Trump administration has since intensified these efforts, invoking Section 232 of the Trade Expansion Act, activating the defence Production Act, and proposing major funding increases for domestic mining and processing in the upcoming fiscal year.

These measures underscore a growing recognition in the US that reducing dependence on China requires more than securing raw materials—it requires investment in processing, recycling, and international partnerships. Still, given China’s entrenched dominance, US efforts remain in the early stages and face significant challenges in scaling to match the strategic risks (Kuo, 2021).

V. Critical Minerals as Geopolitical Competition

Critical minerals have emerged as central instruments of geopolitical power. China illustrates this most clearly: it accounts for roughly 70% of global rare earth mining and more than 90% of refining capacity. It also produces around 92% of the world’s high-strength permanent magnets, which are indispensable for technologies ranging from electric vehicles to advanced military systems such as submarines, fighter jets, missiles, and radar (Brown, et al 2024).

China also moved early to secure resources abroad. Through investments in Africa and Latin America—particularly in the Congo, Bolivia, and Chile—China has paired mineral extraction with infrastructure projects under the Belt and Road Initiative (Siddiqui, 2024b), including ports, railways, and industrial facilities. This integration has given China not only access to raw materials but also influence over the logistics and trade routes that move them.

In contrast, the US has only recently begun to frame critical minerals not merely as commodities but as strategic assets central to national security. Escaping China’s grip will require more than expedited mine permits or short-term funding. It demands a coherent, long-term strategy to construct a resilient supply chain that encompasses domestic capabilities, reliable alliances, and investments across the full spectrum: mining, refining, magnet production, and recycling. This will require targeted investment, permitting reform, and close coordination with trusted partners.

The strategic stakes are high and the REEs underpin a wide range of defence technologies, including modern fighter aircraft, submarines, Tomahawk missiles, radar systems, and advanced communications equipment. Yet the US is already on the back foot: China is rapidly expanding munitions production and fielding advanced weapons systems at a faster pace. Ultimately, critical minerals are no longer simply inputs to industry—they are levers of geopolitical influence. China recognized this early, while the US and its allies are only beginning to respond. The struggle for control over these supply chains will shape the balance of power in both the global energy transition and the future of warfare.

Rare earth elements form the foundation of renewable energy technologies, especially through their use in high-efficiency permanent magnets. These magnets power mobile phones, wind turbines, electric vehicles, and aerospace applications, while also serving critical military functions in drones, missiles, and radar systems. Just as the US has imposed export controls on semiconductors, China has used its dominance in rare earths to restrict flows abroad. Export licensing requirements for certain REE products highlight the asymmetric leverage China holds in today’s technology wars.

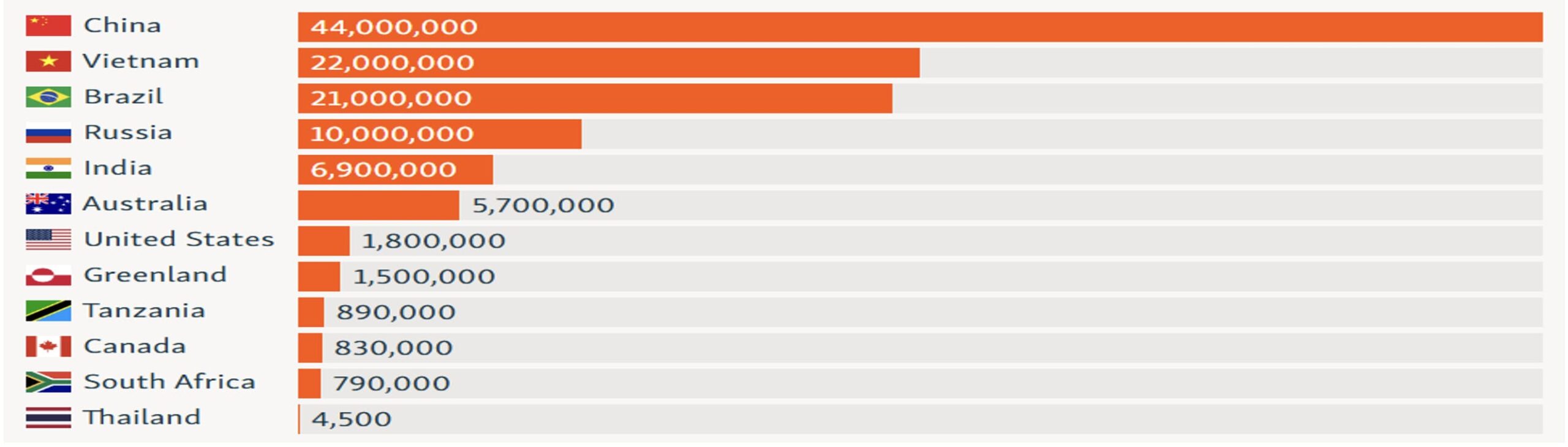

Although China holds an estimated 44% of global rare earth reserves—followed by Vietnam (22%), Brazil and Russia (21% each), India (6.9%), and Australia (5.7%)—its real power lies not in geology but in processing. China controls nearly 90% of global refining capacity, including material mined elsewhere, such as in Australia, Myanmar, and Vietnam. Since the 1980s, when REEs were primarily used in colour televisions, glassmaking, and oil refining, China has steadily built a near-monopoly across the rare earth supply chain. Today, these materials are indispensable to rapidly growing industries such as wind energy, electric vehicles, robotics, and advanced aerospace, as well as in military systems ranging from lasers and tanks to precision-guided missiles (Tooze, 2025).

This dependency is rooted not only in China’s rise but also in the long-term decline of US industrial capacity. In pursuit of cheap labour and higher profits, American firms offshored critical sectors, hollowing out domestic processing industries. In the 1950s, the US led the world in zinc refining; today it accounts for only 6% of global output, compared to China’s 33%. The US was once the top uranium producer; now it imports its entire supply, including from strategic rivals such as Russia. These structural vulnerabilities illustrate that the rare earth struggle is not just about resources, but about the long-term erosion of industrial and technological sovereignty.

The pursuit of critical minerals has become a focal point of geopolitical competition. The US, seeking to secure access to strategic resources, has pursued agreements with mineral-rich countries. For example, on April 30, the US signed a mineral deal with Ukraine, which possesses 117 of the 120 most-used industrial minerals. However, much of these resources are located in territories contested or occupied by Russia, illustrating the inherent geopolitical and logistical challenges of such projects.

Developing mineral resources is neither simple nor guaranteed. Projects require enormous capital investment, and many involve constructing new mines in regions where resource estimates remain unconfirmed. In Greenland, for instance, harsh climatic conditions and icy terrain present significant obstacles. In the US, mining development is notoriously slow, with an average of 29 years required to bring a mine from exploration to production.

Environmental sustainability often remains secondary in the pursuit of strategic resources. For instance, Canada’s Ring of Fire—a wetland and forest serving as an important carbon sink—contains an estimated $67 billion in rare earth minerals. Exploiting these resources could release substantial greenhouse gases, illustrating the environmental trade-offs inherent in mineral extraction under current economic systems.

These dynamics reveal the structural tensions inherent in the global mineral economy: strategic competition, environmental degradation, and economic instability are interlinked outcomes of the current system. Addressing these challenges requires approaches that prioritize long-term sustainability, equitable resource management, and careful consideration of the geopolitical implications of critical mineral development.

VI. Rare Earth Critical Minerals: Geopolitics, Supply Chains, and Capitalist Power

The US President Donald Trump expressed interest in acquiring Greenland, an autonomous territory under Danish sovereignty, citing its strategic value and vast resource potential. The proposal was widely interpreted as motivated, at least in part, by Greenland’s significant reserves of REEs, which have attracted growing international attention. Both Denmark and Greenland firmly rejected the idea, emphasizing that Greenland is not for sale and asserting their sovereignty over resource management. While Greenland is estimated to hold approximately 1.5 million metric tons of rare earth elements, the island does not currently produce these metals. Nevertheless, it hosts two major projects with substantial reserves—the Tanbreez project and the Kvanefjeld project—which could position Greenland as a significant supplier in the future (Goodenough, et al 2018).

The US interest in Greenland reflects broader geopolitical competition over critical minerals essential to renewable energy technologies and defence industries. China currently dominates the global processing of rare earths, accounting for the vast majority of refining capacity, and has in the past signalled its willingness to use this dominance as a strategic tool. From a US perspective, securing alternative sources of rare earths, such as those potentially available in Greenland, is therefore not only an economic issue but also a national security concern. Greenland, situated in the Arctic—a region of increasing strategic importance due to climate change and emerging shipping routes—thus represents both a potential resource frontier and a geopolitical flashpoint in the contest between great powers (Tooze, 2025).

The case of Greenland reflects a broader geopolitical dilemma: the location of mineral reserves does not necessarily translate into supply chain power. For example, cobalt—an essential input for lithium-ion batteries that power electric vehicles (EVs) and renewable energy technologies—is overwhelmingly concentrated in the Congo, as it accounts for about 73% of global cobalt mine output and holds roughly 57% of the world’s reserves, giving it an unparalleled role as a supplier. Yet the strategic value of these reserves is diminished by the fact that China controls approximately 74% of global cobalt processing. Because processing is the stage that transforms raw materials into battery-grade components, China ultimately wields leverage over the downstream supply chain (Goodenough, et al 2018).

Lithium, another indispensable mineral for EV batteries, demonstrates a similar asymmetry. While Australia produces around 51% of global lithium output and Chile 26%, China—despite being a relatively minor producer—dominates refining, with 65% of global processing capacity. This control over processing capacity, rather than raw production, grants China disproportionate influence over global supply chains.

Taken together, these cases illustrate a central paradox: resource-rich states such as the Congo, Chile, or potentially Greenland may command geological abundance, yet their strategic position is weakened when processing and technological capacities are concentrated elsewhere. China’s dominance in mineral processing highlights a structural vulnerability for countries seeking to secure supply chains for clean energy technologies. It also underscores a shift in geopolitical competition: from traditional control over raw resources to control over the value-added stages of the supply chain.

The US, in contrast, is heavily dependent on imports for critical minerals. It relies on China for roughly 70% of its rare earth imports and is entirely dependent on imports for 12 of 50 critical minerals, while over 50% of another 29 come from foreign sources. US efforts to diversify supply chains and develop domestic capabilities include mining initiatives, recycling programs, and strategic partnerships with allies like Australia and Canada. Policy measures across administrations—ranging from Executive Order 14017 under Biden to invoking the defence Production Act under Trump—illustrate the growing recognition that supply chain security is central to national security. Yet building a complete domestic or allied supply chain remains a long-term challenge, requiring investment not only in extraction but also in refining, manufacturing, and recycling.

Under colonialism, the extraction and control of rare earth minerals were intrinsically linked to capitalist imperialism, facilitating the exploitation of labour and natural resources. This process established enduring neocolonial economic structures that primarily benefit dominant powers and their multinational corporations. Despite being essential for modern technology and defence, the mining of these minerals often exacerbates global inequalities rather than generating broad societal benefit (Siddiqui, 202016).