By Dr. Kalim Siddiqui

This article examines the structural dynamics of monopoly capitalism, tracing its evolution from national industrial concentration to global digital-finance monopolies. Drawing on Marxist critiques, Dr Kalim Siddiqui analyses how intangible assets, credit systems, and transnational corporations concentrate economic power, suppress competition, increase monopolisation, exacerbate inequality, and constrain innovation. The study underscores the political and economic implications of monopoly capital, highlighting its role in stagnation, financialisaton, and democratic erosion.

I. Introduction

Monopoly capitalism denotes an economic order characterized by the dominance of oligopolistic and monopolistic firms within industrial structures. In advanced economies, industrial concentration has risen substantially, driven predominantly by mergers and acquisitions. Industrial economics conventionally measures such trends through the structure–conduct–performance (SCP) paradigm. Kalecki reformulated this relationship around the concept of the “degree of monopoly,” positing that price–cost margins are determined by market power rather than competitive conditions. Within this framework, margins reflect factors such as industrial concentration, collusion, and barriers to entry—including economies of scale and marketing advantages.

This internalization of trade shifts bargaining power decisively, as the constant threat of relocation disciplines labour and exerts persistent downward pressure on wages.

This study develops a structural analysis of advanced capitalist economies by integrating theories of monopoly capitalism, capital concentration, and globalization. It argues that contemporary industrial concentration is not a transitory or efficiency-led phenomenon but a systemic outcome of capital accumulation, propelled by scale economies, technological change, and corporate strategy. Through an examination of the interplay between globalization, corporate power, and sectoral concentration, the analysis demonstrates how monopolistic tendencies erode competitive dynamism, distort the direction of innovation, and amplify systemic fragility. Ultimately, I intend to reconceptualizes market outcomes not as products of impersonal forces, but as results of transnational corporate strategy, embedded within political-economic processes that reinforce dominance across global value chains.

Modern banking emerged historically from the concentration of loanable money-capital, first extending credit to merchants and traders, and later to industrial capitalists. This system embodies a dual centralization: of money-capital itself, and of borrowing entities. Banks profit from the differential between deposit and lending rates—a core mechanism of financial intermediation.

The rise of financialisation, however, represents a decisive shift from this traditional model. It is defined by several structural transformations: industrial capital has markedly reduced dependence on bank lending; banks have aggressively expanded household credit; and households have become deeply integrated into the financial system, both as debtors and as asset-holders.

This evolution aligns with the analysis of Paul Sweezy, who described “mature capitalism” as a monopolistic system that generates an ever-expanding economic surplus. According to him, the productive sphere becomes increasingly unable to absorb this surplus, leading to tendencies toward economic stagnation and rising inequality within advanced capitalist economies. Ultimately, these developments were facilitated by a new social structure of accumulation. Under this framework, the state gradually withdrew not only from direct economic activities but also from its role as a provider of essential public services—including education, healthcare, and social welfare—thereby accelerating the economy’s dependence on financial institutions (Siddiqui, 2023).

This financial dependence emerged in tandem with the neoliberal paradigm. Since the 1980s, neoliberal policies promoting liberalization, deregulation, and privatization have displaced the earlier Keynesian national models. In practice, these policies have fostered not competitive markets but a system of transnational monopoly capitalism, characterized by dominant multinational corporations, rise of foreign direct investment, and consolidated global supply chains. This configuration marks a distinct historical shift, one that differs fundamentally from earlier economic structures—a divergence exemplified, for instance, by the historically limited role of trade in the United States (US) compared to that of the United Kingdom (UK). (Sawyer, 2022)

Concurrently, in the absence of powerful investment stimuli—such as historic technological breakthroughs like the automobile or huge government spending—advanced capitalist economies have grown increasingly dependent on financialization to sustain profits. While this shift has provided a temporary respite from stagnation, its inherent instability—evident in recent financial market turbulence—reveals it as an unsustainable solution. This financial dependence emerged alongside the neoliberal paradigm, which since the 1980s has displaced Keynesian national models through liberalization, deregulation, and privatization (Sawyer, 2022).

Contemporary globalisation has driven a marked expansion of international trade and foreign direct investment (FDI), alongside a far-reaching reorganisation of production through global supply chains. Although the 2008 global financial crisis temporarily slowed these trends, the global stock of FDI rose from 9 per cent of GDP in 1990 to nearly 44 per cent in 2024. Over the same period, market concentration has deepened in information and communications technology (ICT) sectors, while financialisation has continued to intensify (Siddiqui, 2024a).

The contemporary phase of globalization, characterized by unprecedented corporate concentration and the rising structural power of transnational firms, has demonstrably failed to serve the broader global interest. Instead of delivering widely shared prosperity, it has generated a suite of systemic pathologies: weakened market competition, geographically skewed innovation, rising socioeconomic inequality, and a marked erosion of national policy autonomy. These outcomes fundamentally challenge the dominant narrative that equates globalization with gains in efficiency and inclusive growth, necessitating a critical reassessment of the global economic order.

Within the advanced capitalist economies, these monopolistic tendencies are amplified by the dual forces of financialization and the specific architecture of contemporary trade. The liberalization of capital and goods flows has enabled dominant firms to reorganize production globally, exploit international labour arbitrage, and manage complex supply chains under centralized corporate control. Concurrently, financial markets actively incentivize further consolidation through mergers, acquisitions, and the relentless pressure to maximize shareholder value.

A critical manifestation of this dynamic is the transformation of global trade itself. Post-liberalization, the sharp rise in trade volumes has been accompanied by a qualitative shift: a substantial portion of global commerce now occurs as intra-firm transactions within multinational corporations. This internalization of trade shifts bargaining power decisively, as the constant threat of relocation disciplines labour and exerts persistent downward pressure on wages. Consequently, contrary to theoretical predictions that globalization would heighten competitive pressures, the prevailing dynamics have consolidated market power, thereby elevating the aggregate degree of monopoly in the global economy.

The Chinese model of development differs from that of advanced capitalist economies but is similarly centred on governance structures. State regulation in China has actively shaped the development of major digital platforms, notably WeChat, operated by Tencent, whose expansion has occurred in close alignment with the techno-nationalist strategy of the Communist Party of China (CPC). This strategy prioritises the protection of national interests in the context of China’s late-developing economy. As a result, Chinese “big tech” firms operate under extensive state oversight (Siddiqui, 2024c).

While many large enterprises in China are state-owned and directly controlled by the CPC, private firms such as Alibaba and Tencent are also subject to significant political control and cannot be regarded as independent. Senior executives of these companies are typically members of the Communist Party and are expected to adhere to its policy priorities and ideological framework. Alibaba, through its affiliate Ant Group under the leadership of Jack Ma, provides a notable example: its planned initial public offering was halted by the Chinese authorities in 2020. This intervention illustrates how the Chinese government ensures that the development of the digital economy remains aligned with broader national objectives.

II. Theoretical Discussions

Adam Smith (1776) emphasised competition and freedom of entry for new entrepreneurs. His conception of competition was dynamic rather than static, viewing it as a process that guides the evolution of markets over time. For Smith, the primary concern of antitrust policy was not monopoly per se, but monopolisation—that is, the extension of market power by firms under the pretext of serving social interests. He was critical of exclusive rights and the institutional arrangements that grant firms monopolistic privileges. More broadly, Smith advocated a reconfiguration of the relationship between society and economic organisation, favouring horizontal relationships among equally motivated economic agents over hierarchical structures characterised by segmented and insulated decision-making.

For Karl Marx, capitalist competition played a historically progressive role in dissolving the guild system and dismantling trade restrictions that had characterised feudal society, thereby enabling the emergence of capitalist social relations. He understood capitalist competition as the negation of feudal monopoly, and equally as the negation of the mercantilist monopolies associated with colonial trade and chartered trading companies—institutions that were the primary targets of Adam Smith’s critique. In this sense, competition was historically constitutive of capitalism itself, clearing the institutional obstacles that constrained the free movement of capital and labour (Marx, 1993).

At the same time, Marx argued that capitalist monopoly does not stand outside or in opposition to competition, but rather emerges from it. The development of capitalism is inseparable from the operation of the laws of capitalist competition, and monopoly arises as an outcome of these laws rather than as their negation. Capitalist monopoly is therefore historically distinct from feudal and mercantilist monopolies, which were rooted in legal privilege, political authority, and exclusive trading rights. By contrast, capitalist monopoly is generated endogenously through accumulation, competition, and the concentration and centralisation of capital.

Marx further distinguished between the processes of concentration and centralisation of capital. Concentration refers to the growth of individual capitals through accumulation, while centralisation involves mergers and acquisitions—what Marx described as the “expropriation of capitalist by capitalist.” Centralisation redistributes existing capital into fewer hands and operates more rapidly and forcefully than concentration alone. It accelerates monopolisation by enabling firms to realise economies of scale, adopt new technologies, and reorganise production on an expanded scale. Both concentration and centralisation are propelled by capitalist competition itself, as firms seek to reduce costs, expand market power, and survive competitive pressures (Marx, 1993).

Capitalism is, at its core, a dynamic economic system driven by the relentless pursuit of private profit, a pursuit concentrated among a relatively small number of wealthy individuals and powerful corporations. Under competitive capitalism, surplus value is redistributed among capitals through the equalisation of profit rates, such that individual capitalists’ appropriate profits in proportion to the capital they have advanced (Siddiqui, 2024b). However, as accumulation proceeds, differences in scale, productivity, and access to technology allow some capitals to claim a larger share of total surplus value. The concentration of capital thus enables dominant firms to appropriate disproportionate gains while remaining formally within a competitive framework (Vasudevan, 2022).

Capitalist development thus creates both the social need and the technical means for the emergence of large monopolies. The drive to increase productivity, reduce unit costs, and command larger shares of the market systematically favours large-scale capital. In this way, monopoly is not an external distortion of capitalism, but a structural tendency generated by accumulation and competition.

This understanding highlights a fundamental difference between Marxist and neoclassical conceptions of monopoly. In neoclassical theory, monopoly power is typically derived from market concentration within a defined market and is analysed primarily through price-setting behaviour. By contrast, the Marxist approach locates monopoly power in the concentration and control of capital itself rather than in market structure alone. Capitalist competition implies that a small number of firms appropriate more surplus value than others, and higher rates of accumulation allow these firms to expand their scale of production and secure cost advantages over smaller competitors.

The mainstream economists account that interprets concentration as a temporary or efficiency-enhancing outcome of technological progress. Instead, it emphasises the systemic consequences of monopoly power, including reduced competitive dynamism, distorted patterns of innovation, and heightened vulnerability to economic instability. It also foregrounds the political dimensions of corporate concentration, particularly the growing influence of large firms over regulatory regimes, trade agreements, and national policy frameworks. In this framework, monopoly is rooted not simply in pricing power, but in control over production, technology, and accumulation processes.

The contemporary behaviour of large corporations reflects a structural logic inherent to monopoly capitalism rather than a series of isolated firm-level strategies. Large firms increasingly pursue a dual and mutually reinforcing objective: the expansion of sales and market share on the one hand, and the maximisation of profitability on the other. While neoclassical theory often treats these objectives as potentially conflicting, within monopoly capitalism they converge over time. Market expansion is not merely a route to higher output but a mechanism for consolidating control over demand, supply chains, and technological standards.

This explains why monopoly power in advanced capitalist economies increasingly manifests through oligopolistic structures rather than through single-firm dominance. Contemporary “monopolies” are often systems of coordinated dominance exercised by a small number of firms that collectively shape market outcomes. In such settings, competition persists, but it is competition among giants rather than among a large number of independent producers. This form of rivalry tends to be expressed through non-price mechanisms—such as control over technology, branding, data, and access to distribution channels—rather than through price competition alone.

The prevalence of oligopolistic dominance across diverse sectors—including technology, transportation, finance, agribusiness, and essential services—indicates that monopoly capitalism should be understood as a systemic condition rather than as a sector-specific anomaly. High levels of concentration are closely associated with rising barriers to entry, declining rates of new firm formation, and a growing divergence in profitability between dominant firms and the rest of the corporate sector. These patterns suggest that monopoly power increasingly functions as a means of redistributing surplus value towards large capital rather than as a temporary outcome of superior efficiency or innovation.

This interpretation stands in sharp contrast to mainstream accounts that attribute market concentration primarily to technological progress or consumer welfare–enhancing efficiencies. While technological change undoubtedly plays a role, it operates within institutional and competitive structures that favour the consolidation of capital. Large firms are uniquely positioned to absorb the fixed costs associated with research and development, data accumulation, and regulatory compliance, further reinforcing their dominance. Innovation, rather than undermining monopoly power, often becomes a mechanism through which it is stabilised and extended.

Moreover, the expansion of monopoly power has significant political and macroeconomic implications. The concentration of corporate power undermines competitive wage dynamics, weakens labour’s bargaining position, and contributes to persistent income and wealth inequality. At the macroeconomic level, monopoly capitalism is associated with slower productivity diffusion, underinvestment in productive capacity, and increased reliance on financialisation and speculative activity as outlets for surplus. These tendencies reinforce the “strategic failures” of the global economy identified earlier, including uneven development, fragile growth, and declining democratic accountability (Siddiqui, 2019).

Financialisation, which has intensified since the 1980s, refers to the expanding role of financial markets, institutions, and motives in both national and international economies. Shareholder value has increasingly dominated corporate strategies, reshaping relations between the financial sector and the rest of the economy. As Sweezy argues, financial capital has become increasingly detached from its supportive role in productive activity and has evolved into a relatively autonomous financial superstructure oriented towards speculative self-expansion, reversing the traditional relationship between the financial and real sectors of the economy (Sawyer, 2022).

The development of the credit system is critical in facilitating and shaping long-term investment patterns in the economy. The availability of funds to financial institutions, and their allocation to profitable sectors, significantly influences employment levels, income distribution, productivity, and overall GDP growth. Credit represents a form of capital that can overcome constraints on capital mobility imposed by fixed capital. Moreover, capital liberalisation associated with globalisation has profoundly altered both the movement of capital and the availability of financial resources within domestic economies and private sectors.

The expansion of the credit system also contributed to the emergence of joint-stock companies, which can be regarded as the institutional predecessors of modern multinational corporations (MNCs). These organisational forms provided an effective mechanism for mobilising large-scale financial resources, enabling firms to exploit economies of scale, increase profitability, and move toward greater concentration and monopolisation within specific industries.

The rise of monopolisation and the growing dominance of contemporary MNCs have important implications for the dynamics of capital accumulation. These trends have been associated with increasing income inequality and a declining share of income accruing to workers, contributing to economic stagnation through weakened aggregate demand and consumption. Monopoly capital is further characterised by the coexistence of collusion and rivalry, alongside a shift toward non-price forms of competition, such as expanded marketing efforts and intensified advertising. Such strategies reflect the capacity of monopolistic firms to rely on institutionally and politically supported market power in order to extract monopoly rents (Sawyer, 2022).

Technological innovation under monopoly capitalism exhibits an inherent bias toward scale-intensive production and centralised control over large-scale operations. Mergers and acquisitions frequently function as mechanisms to suppress potentially disruptive innovations that could promote deconcentration, while simultaneously facilitating the acquisition of intangible assets that further entrench monopolistic power. Despite these tendencies, competitive pressures do not disappear under monopoly capitalism; instead, the compulsion to reduce costs and innovate persists, often intensifying competition among workers and exacerbating labour market precarity.

Critics of monopoly capital theory have argued that the internationalisation of capital—by weakening US hegemony and increasing exposure to foreign trade and capital flows—would undermine monopolistic control. However, recent decades have instead been characterised by increasing concentration and centralisation of capital at the global level, with a shrinking number of corporations controlling a growing share of world markets (Siddiqui, 2025a).

III. Credit, Accumulation, Monopoly Capital, and Digital Dominance

The development of the credit system has been central to shaping long-term investment patterns and transforming the organisation of capitalism. By mobilising and allocating funds toward profitable sectors, credit profoundly influences employment, income distribution, productivity, and overall economic growth. As a form of capital, credit partially overcomes the immobility imposed by fixed capital, thereby accelerating accumulation and concentration. Capital liberalisation associated with globalisation has further intensified these dynamics by expanding cross-border capital flows and increasing the availability of financial resources to dominant firms within domestic economies.

At the same time, contemporary digital monopolies differ in important respects from both classical and early twentieth-century conceptions of monopoly. For classical economists, monopoly was typically understood as arising from production conditions and property rights that restricted the mobility of capital, rather than from oligopolistic competition among a small number of large firms. Adam Smith, for example, emphasised the role of monopoly privileges in sustaining mercantilist systems, particularly the capacity of chartered trading companies to extract extraordinary profits through exclusive trade routes in the late seventeenth century. Monopoly, in this view, was fundamentally linked to barriers to entry and the institutional restriction of competition.

Digital technology has further intensified these dynamics. Platform-based firms, characterised by strong network effects, data accumulation, and high barriers to entry, exhibit structural features that favour monopolisation or oligopolistic dominance. Unlike earlier forms of industrial concentration, digital monopolies derive power not only from control over production and distribution, but also from ownership of data infrastructures, algorithmic systems, and standards that govern market access. These firms increasingly function as gatekeepers, shaping the conditions under which other firms, workers, and consumers participate in economic activity.

By situating contemporary developments in production and digital technology within this broader theoretical context, the study seeks to illuminate the structural forces shaping the current phase of global capitalism. This approach provides the basis for assessing not only economic performance, but also the wider social and institutional implications of concentrated corporate power in the global economy.

Monopoly power in the contemporary economy has increasingly emerged through the strategic exercise of network dominance by digital platforms. This form of power challenges conventional approaches to monopoly that focus narrowly on firm size, market share, or concentration within clearly defined single markets. Platform-based firms operate across multiple, interdependent markets and leverage network effects, data accumulation, and ecosystem integration to entrench dominance. As a result, monopoly power is exercised through control over infrastructures, standards, and access conditions rather than through explicit price-setting alone, rendering traditional antitrust frameworks increasingly inadequate.

The rising returns associated with these forms of monopoly power did not initially take the form of sustained price increases, particularly in the period prior to the 1990s. In part, this reflected the continued presence of antitrust enforcement and the strategic deployment of low or zero prices to accelerate user adoption and reinforce network effects. Over time, however, dominant firms have converted network scale into durable market power, enabling new forms of rent extraction through data monetisation, preferential self-placement, exclusionary practices, and the enclosure of digital ecosystems. In recent decades, this economic power has been accompanied by a marked increase in political influence, as dominant corporations have acquired the capacity to shape regulatory agendas, influence public policy, and set de facto rules governing market participation.

These developments strongly resonate with earlier analyses of monopoly capitalism. Baran and Sweezy (1966) identified the emergence of large corporations and oligopolistic market structures as defining features of a distinct phase of capitalist development. Their analysis emphasised the tendency of surplus generation to outpace profitable investment opportunities, leading dominant firms to rely on market control and strategic behaviour rather than competitive efficiency. While their focus was primarily on industrial production, contemporary advances in information and digital technologies have intensified these tendencies by creating new mechanisms for consolidating and extending monopoly power. Digital platforms enhance economies of scale and scope while simultaneously increasing barriers to entry, thereby accelerating the concentration and centralisation of capital anticipated in earlier theoretical work.

This conception was later formalised within neoclassical economics, most notably by Marshall, who defined monopoly as a market structure characterised by a single seller exercising market power by restricting output and charging prices above competitive levels. While this framework became central to antitrust theory, it rests on assumptions—such as clearly defined markets, price competition, and observable output restrictions—that are increasingly ill-suited to analysing platform-based capitalism. Digital monopolies often expand output, lower prices, or provide services at zero monetary cost, while simultaneously exercising control over market access, data flows, and competitive conditions.

The political implications of these developments are substantial. The growing concentration of economic power in digital platforms has eroded the capacity of states to regulate markets effectively, particularly in areas such as competition policy, taxation, labour standards, and data governance. Through lobbying, regulatory capture, and the strategic exploitation of jurisdictional fragmentation, dominant firms are increasingly able to shape the institutional environment in which they operate. This reinforces asymmetries of power between capital and labour, incumbents and entrants, and firms and states, contributing to broader patterns of inequality and democratic deficit.

In this sense, contemporary digital monopolies represent not merely a new market structure, but a transformation in the relationship between economic power and political authority. Monopoly power is no longer confined to the sphere of production or exchange; it extends into the governance of economic life itself. Understanding these dynamics requires moving beyond narrow market-based definitions of monopoly towards a political-economic analysis that foregrounds power, institutions, and historical context. Such an approach is essential for assessing the systemic consequences of monopoly capitalism in its digital form and for evaluating the prospects for effective regulation and democratic control in the global economy.

The expansion of credit markets historically enabled the rise of joint-stock companies, which constituted the institutional foundations of contemporary multinational corporations (MNCs). These organisational forms facilitated the large-scale mobilisation of capital, allowing firms to exploit economies of scale, increase profitability, and consolidate market power. Over time, this process generated rising levels of industrial concentration and monopolisation, marking a structural transformation rather than a departure from competitive capitalism.

Monopoly power is no longer confined to the sphere of production or exchange; it extends into the governance of economic life itself.

The growing dominance of monopolistic and oligopolistic firms has had profound implications for capital accumulation and macroeconomic stability. Increasing concentration has been associated with rising income inequality and a declining labour share, contributing to weakened aggregate demand and tendencies toward economic stagnation. Monopoly capital is characterised not by the absence of competition, but by a specific configuration of rivalry and collusion, alongside a shift from price competition to non-price strategies such as marketing, branding, and advertising. These strategies rely on institutionally supported market power and enable firms to extract monopoly rents insulated from competitive pressures.

Technological change under monopoly capitalism exhibits a systematic bias toward scale-intensive production and centralised control. Innovation is increasingly oriented toward reinforcing dominant positions rather than fostering competitive entry. Mergers and acquisitions play a critical role in this process, frequently functioning to neutralise potentially disruptive innovations and acquire intangible assets that deepen monopolistic control. While cost reduction and innovation remain imperatives under monopoly capitalism, competitive pressures are displaced onto labour, intensifying worker competition and exacerbating precarity.

In this sense, contemporary monopoly capitalism represents not a deviation from competitive capitalism, but its logical development under conditions of advanced accumulation, globalisation, and digitalisation. Understanding this transformation requires moving beyond narrow antitrust frameworks toward a structural analysis of power, accumulation, and institutional control.

Digital capitalism represents the most advanced expression of these dynamics. Digital monopolies are fundamentally grounded in property rights over intangible capital, including proprietary technologies, data, intellectual property, and branding. Control over these assets enables dominant firms to construct formidable barriers to entry and restrict capital mobility. Between 2018 and 2023, the intangible asset values of Amazon, Google, and Facebook increased by more than 74 per cent, with intangible assets accounting for nearly 87 per cent of their total asset value. Ownership of such assets positions these firms as critical gatekeepers of the digital infrastructures that underpin information flows, communication systems, and commercial activity.

At the global level, Google dominates internet search, Amazon commands e-commerce and cloud-based business services, and Facebook controls key social media platforms. Together, these corporations reached a combined market capitalisation exceeding $3.7 trillion in 2024. Their dominance has been further consolidated through extensive merger and acquisition activity. Over the past two decades, Google has acquired more than 260 companies, Amazon over 100, and Facebook 63 firms since its founding in 2004. These acquisitions reflect both strategic expansion into new markets and systematic efforts to undermine potential competition. High-profile cases such as Facebook’s acquisitions of Instagram and WhatsApp and Amazon’s purchase of Zappos exemplify how corporate concentration is actively reinforced through institutional and financial mechanisms.

Taken together, these developments illustrate how monopoly capitalism in its digital form is sustained through the interaction of credit systems, intangible property rights, and corporate consolidation, generating far-reaching economic and political consequences in the contemporary global economy. At the global level, there has been a pronounced increase in concentration across the communications, information technology (IT), and media industries, alongside significant merger and consortium activity in formerly public utilities that have undergone privatisation. While these sectors are often portrayed as having been opened to intensified global competition through rapid technological change, mounting evidence suggests that a small number of large corporations are instead emerging as dominant actors at the global scale.

In particular, the provision and servicing of global IT networks increasingly appears to be controlled by only two or three major service providers operating across multiple industries. This concentration reflects not only technological advantages but also strategic control over standards, platforms, and complementary services. Microsoft’s long-standing dominance in software and computer operating systems, for example, has been a persistent source of concern for both US and EU antitrust authorities. Similarly, Google’s near-monopoly position in global internet search has raised significant regulatory and competitive concerns, highlighting the limits of existing competition frameworks in addressing platform-based market power (Siddiqui, 2025b).

Significant consolidation has also occurred within telecommunications, where global consortia and strategic alliances emerged prominently from the late 1990s onwards. This period witnessed a wave of mergers and cross-border partnerships involving the world’s largest telecommunications firms, reinforcing concentration at both national and international levels. These developments are particularly noteworthy given that information and communication technologies were initially regarded as forces capable of undermining monopoly power by lowering entry barriers and decentralising production. Instead, technological change has largely been absorbed into existing structures of accumulation, reinforcing monopolistic control rather than dissolving it.

The contemporary global economy is increasingly characterised by high levels of corporate concentration, the dominance of multinational corporations (MNCs), and the growing importance of digital platforms. While mainstream economic perspectives often treat monopoly power as an aberration from competitive markets, this article argues that monopoly capitalism represents a systematic outcome of capitalist development itself. In particular, the interaction between credit systems, globalisation, and intangible capital has reshaped the organisation of production and competition, giving rise to new forms of monopoly power with far-reaching economic and political consequences.

The development of the credit system has played a central role in shaping long-term investment patterns and transforming capitalist accumulation. By mobilising savings and directing funds toward profitable sectors, credit influences employment, income distribution, productivity, and overall economic growth. As a form of capital, credit partially overcomes the immobility imposed by fixed capital, accelerating accumulation and enabling the concentration of economic power.

Capital liberalisation associated with globalisation has further intensified these processes by facilitating cross-border capital flows and expanding access to financial resources for large firms. Historically, the expansion of credit markets enabled the emergence of joint-stock companies, which provided the organisational foundations for modern MNCs. These firms were able to mobilise large volumes of capital, exploit economies of scale, and consolidate market power across national boundaries.

The rise of monopolisation should be understood as a structural transformation of capitalism rather than a departure from competition. Increasing concentration has been associated with rising income inequality and a declining labour share, contributing to weakened aggregate demand and tendencies toward economic stagnation (Siddiqui, 2018). Monopoly capital is characterised by a specific configuration of rivalry and collusion, alongside a shift from price competition to non-price strategies such as branding, marketing, and advertising.

Under monopoly capitalism, technological innovation is increasingly oriented toward reinforcing dominant market positions rather than facilitating competitive entry. Mergers and acquisitions serve as key mechanisms in this process, frequently neutralising potentially disruptive innovations and consolidating control over strategic assets. While the imperative to reduce costs and innovate persists, competitive pressures are increasingly displaced onto labour, intensifying worker competition and labour market precarity.

Digital capitalism represents the most advanced expression of monopoly capitalism. Digital monopolies are grounded in property rights over intangible capital, including proprietary technologies, data, intellectual property, and branding. Control over these assets enables dominant firms to construct formidable barriers to entry and restrict capital mobility.

Between 2018 and 2023, the intangible asset values of Amazon, Google, and Facebook increased by more than 74 per cent, with intangible assets accounting for nearly 87 per cent of their total asset value. Ownership of such assets positions these firms as critical gatekeepers of digital infrastructures underpinning information flows, communication systems, and commercial activity. At the global level, Google dominates internet search, Amazon controls large segments of e-commerce and cloud services, and Facebook exercises substantial power over social media ecosystems.

These positions have been reinforced through extensive merger and acquisition activity. Over the past two decades, Google has acquired more than 260 companies, Amazon over 100, and Facebook 63 firms since its founding in 2004. High-profile acquisitions such as Facebook’s purchases of Instagram and WhatsApp and Amazon’s acquisition of Zappos illustrate how corporate concentration is actively reproduced through institutional and financial mechanisms.

Beyond digital platforms, there has been growing concentration across communications, information technology (IT), and media industries, alongside significant merger and consortium activity in formerly public utilities following privatisation. Although these sectors are often portrayed as having been opened to intensified competition through technological change, evidence suggests that a small number of global corporations dominate key markets.

The servicing of global IT networks increasingly appears to be controlled by only two or three major providers, reflecting strategic control over standards and infrastructures. Microsoft’s long-standing dominance in software and operating systems has repeatedly attracted scrutiny from US and EU antitrust authorities, while concerns over Google’s near-monopoly in internet search underscore the limitations of existing regulatory frameworks.

Similarly, telecommunications have experienced substantial consolidation since the late 1990s, marked by mergers and strategic alliances among the world’s largest firms. These developments are particularly significant given early expectations that information and communication technologies would erode monopoly power. Instead, technological change has largely reinforced existing structures of accumulation and control.

From a political-economy perspective, the central issue is not simply market concentration but the structural control exercised by large corporations over the conditions of production and exchange. In digital sectors, this control is exercised through ownership of platforms, data infrastructures, and technological ecosystems that function as essential inputs for other firms. Network effects, interoperability constraints, and user lock-in generate self-reinforcing barriers to entry, allowing incumbent firms to maintain dominance even in the absence of explicit collusion or price increases. These mechanisms enable firms to appropriate rents not only from consumers but also from dependent producers, advertisers, and workers operating within platform-controlled environments.

Vasudevan (2022) argues that the rise of modern corporations in the twentieth century harnessed economies of scale and network externalities in ways characteristic of natural monopolies, strengthening capitalism’s capacity to organise and control production while accelerating capital mobility and concentration. The liberalisation of international capital markets extended this process globally, enabling transnational corporations to extract monopoly rents. He further contends that the geographical flexibility of transnational production has weakened organised labour by allowing capital to evade national constraints, contributing to the global decline in labour’s income share since the 1980s and reflecting capital’s enhanced monopoly power over labour (Vasudevan, 2022:1277).

Critics of monopoly capital theory have argued that the internationalisation of capital—by weakening US hegemony and increasing exposure to global trade and capital flows—would reduce monopolistic power. However, recent developments point to the opposite outcome: rising global concentration and centralisation of capital, with a shrinking number of corporations controlling an increasing share of world markets.

Monopoly capitalism displays a persistent tendency towards monopolisation, as firms adopt strategic behaviour to limit competition and deter entry. Cowling and Tomlinson highlight the implications of this corporate power for income distribution and realisation crises, arguing that contemporary capitalism is dominated by oligopolies with substantial market power. The degree of monopoly reflects market concentration, collusion, and demand elasticity, which large firms can influence through advertising and product differentiation, thereby weakening competitive pressures (Cowling and Tomlinson, 2005).

Sawyer (2022:1226) argues that the degree of monopoly provides a framework for understanding income distribution in which power plays a central role, extending beyond product markets to encompass capital’s power over labour. Surplus is divided between profits and managerial rewards. In contrast, neoliberal doctrine presents markets as inherently beneficial, emphasising competition, incentives, deregulation, and the extension of market mechanisms into previously non-market domains. Drawing on Austrian and neoclassical economics, neoliberalism assumes that competitive markets generate efficient and Pareto-optimal outcomes.

IV. Monopoly Power, Competition, and Democracy

The rise of monopolisation has profound implications for the nature of competition and strategic rivalry under contemporary capitalism. Within the industrial economics literature, monopolised and oligopolistic markets are typically characterised by a combination of strategic entry deterrence, tacit or explicit collusion, and persistent price levels above those predicted under competitive conditions. As prices increasingly diverge from competitive benchmarks, monopoly power becomes structurally embedded rather than episodic. These dynamics have significant implications for income distribution between capital and labour and, ultimately, for macroeconomic performance.

Monopolisation tends to raise the aggregate profit share, often at the expense of wages. In practice, a substantial portion of these profits may be absorbed within corporate hierarchies through executive compensation, managerial bonuses, and administrative expenditures, rather than being translated into productive investment. The resulting decline in the wage share contributes to weakened aggregate demand, reinforcing stagnations tendencies identified in monopoly capital and post-Keynesian traditions (Baran and Sweezy, 1966; Kalecki, 1971).

Beyond its economic effects, the expansion of monopoly power raises fundamental questions regarding the compatibility of democracy and freedom within systems of monopoly capitalism. As demonstrated throughout this article, the global economy is increasingly dominated by large transnational corporations whose strategic interests often diverge from broader social and democratic objectives. The concentration of economic power enables these firms to exert disproportionate influence over political institutions, regulatory frameworks, and public discourse, frequently marginalising alternative voices and constraining democratic participation. In this sense, the retreat of democracy has accompanied the rise of corporate concentration.

However, this erosion of democracy should not be understood as a necessary condition for economic efficiency. Contrary to the notion of a trade-off between democracy and performance, greater substantive democracy—understood as enhanced participation, accountability, and collective control over economic decision-making—may contribute to superior economic outcomes. More democratic institutional arrangements can restrain rent extraction, redirect surplus toward socially productive uses, and support more inclusive and stable patterns of growth. From this perspective, the tension between monopoly power and democracy reflects not an efficiency requirement, but a structural feature of advanced capitalism.

Empirical evidence reinforces these claims. Market concentration in advanced economies has increased markedly over the past two decades, particularly within specific industries. Data from the OECD and IMF point to a general shift toward more concentrated market structures, implying rising market power among leading firms. This trend is evident across major advanced economies, including the US, the UK, Japan, and other European countries such as France, Germany, and Italy. Importantly, the increase in concentration has not been uniform across sectors. Industries such as general merchandise retailing, information goods, digital technologies, pharmaceuticals, and banking exhibit especially high and rising concentration ratios.

The business concentration is starkly evident in the US. The telecommunications sector, for instance, is dominated by just four major players, with AT&T and Verizon alone controlling approximately 70 percent of the market. Furthermore, the pinnacle of American capitalism reveals a striking trend toward digital monopoly. The three most valuable companies in the nation are all digital giants—relatively new entities that have achieved extraordinary market dominance. In fact, five of the top eight and twelve of the top thirty-two most valuable U.S. companies are digital powerhouses. Their names are familiar: Alphabet (Google), Microsoft, Apple, Amazon, Meta (Facebook), and Cisco. And, of course, legacy telecom titans like AT&T and Verizon remain firmly entrenched in this elite group, beneficiaries of the same system.

While accounting for international trade can reduce measured concentration in certain manufacturing industries—since import competition expands the effective market—many nationally oriented sectors remain highly concentrated. Utilities, telecommunications, and a range of service industries continue to exhibit oligopolistic or monopolistic structures and often require regulatory intervention. Table 1 indicates the market concentration ratios and trends among some advanced economies for 2024-2025. Market concentration is commonly measured using the N-firm concentration ratio, such as the combined market share of the four or five largest firms (CR4 or CR5), or the Herfindahl–Hirschman Index (HHI). A CR4 exceeding 40 per cent is generally indicative of oligopolistic market structures, highlighting the prevalence of concentrated economic power in contemporary advanced economies.

Table 1: Concentration Ratios and Trends Among Selected Economies for 2024-2025.

| Economy/Region |

Industry Example |

Concentration (Approx) |

Trend |

| UK |

Mortgage Lending (2023) |

CR4: 50.3% |

Stable/Slight Increase |

| UK |

Supermarkets |

CR5: 74.6% (2025 est.) |

Increasing (driven by discounters) |

| US |

Domestic Airlines (2024) |

CR4: 68% |

High Concentration |

| US |

Book Stores (2023) |

CR4: 71% |

Sharp Increase since 1990s |

| European Union |

Average

(all industries) |

Share of high concentration industries doubled (16% to 37%) |

Substantial Increase (since 1998) |

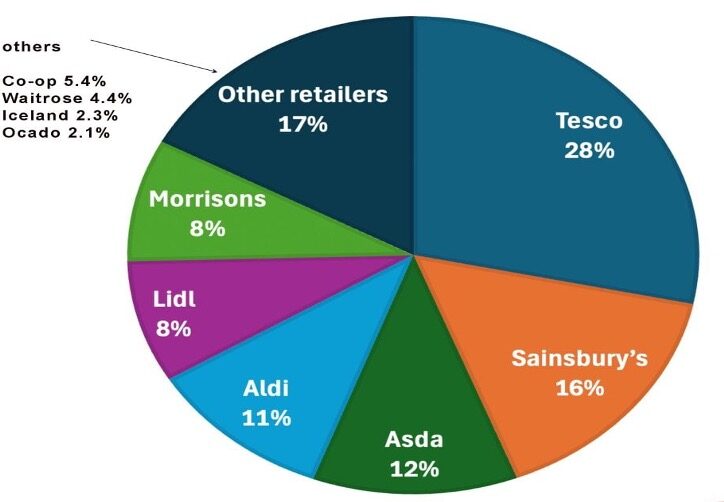

Table 2: Five Firm Concentration Ratio of UK’s Supermarkets, 2024-2025 (%).

| 1. Tesco |

28.3 |

| 2. Sainsbury’s |

15.8 |

| 3. Asda |

11.6 |

| 4. Aldi |

10.6 |

| 5. Lidl |

8.3 |

| Total Five Firm Concentration Ratio of UK’s Supermarkets |

74.6 |

Figure 1: Market Share in UK’s Supermarkets in 2024-2025.

Taken together, these developments underscore that monopoly capitalism reshapes not only market competition, but also income distribution, democratic governance, and macroeconomic stability. Addressing these challenges therefore requires moving beyond narrow antitrust approaches toward a broader political-economy framework capable of confronting the structural concentration of economic and political power.

Concentration ratios measure the proportion of total market output or sales accounted for by the largest firms within an industry. Commonly used indicators include the three-firm concentration ratio (CR3) and the five-firm concentration ratio (CR5), which represent the combined market share of the three or five largest firms, respectively. Concentration ratios are widely employed to assess market structure and the degree of competitiveness within an industry. Figure 1 shows market concertation of only 5 monopolies has a huge concentration of market share in the UK markets (also see Table 2). Higher concentration ratios indicate greater market power among leading firms and a reduced intensity of competition. For example, markets are typically characterised as oligopolistic when the five-firm concentration ratio exceeds 50 per cent, signalling that a small number of firms dominate a substantial share of total market activity.

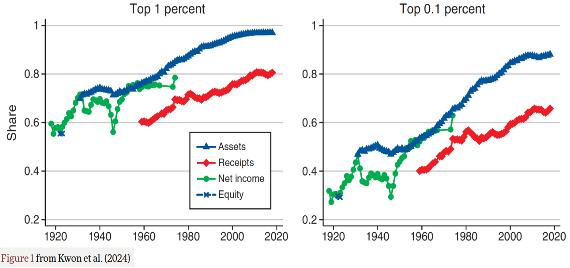

Kwon, Ma, and Zimmermann (2024) provide a long-run analysis of business concentration in the US, documenting a steady increase in the shares of assets, sales, and net income accruing to the largest firms since the early twentieth century. Using official data on the size distribution of US corporations, Figure 2 illustrates aggregate concentration trends among the largest firms over the period 1918–2018.

Figure 2 shows the shares of the top 1 percent of US corporations on the left panel and the top 0.1 percent on the right. The blue, red, and green lines represent shares of assets, sales, and net income, respectively. Both panels reveal a pronounced upward trend in concentration. Notably, the asset share of the top 1 percent increased by 27 percentage points between 1931 and 2018, reaching 97 percent, while the asset share of the top 0.1 percent rose even more rapidly. Overall, the evidence points to a sustained rise in business concentration in the US economy over the past century (Kwon, et al, 2024).

Figure 2: The Aggregate Concentration Trends among the Largest US Corporations, 1918-2018.

The IMF (2021) study underscores these trends, noting that corporate market power has risen in advanced economies and is likely to increase further following pandemic-related bankruptcies. Rising concentration and higher price markups—up roughly one-third—have doubled profitability and are concentrated among a small group of dominant firms. This persistent market power is accompanied by declining business dynamism, including a lower share of activity by young firms and reduced dispersion of growth rates. While not the sole driver of reduced dynamism, increasing corporate power has contributed to these patterns and has moderate negative effects on growth, investment, innovation, and the labour income share.

Taken together, these developments illustrate that monopoly capitalism reshapes not only market structures, but also income distribution, democratic governance, and macroeconomic stability. Addressing these challenges requires moving beyond narrow antitrust approaches toward a structural political-economy framework capable of confronting concentrated corporate power in the contemporary global economy (IMF, 2021).

V. Rise of Monopolies since Globalisation and Radical Critiques

Globalisation and the expansion of international competition initially led many economists to consider monopoly power a declining concern. By the mid-1980s, some observers argued that aggregate concentration in the US economy was rising only slowly, and that industries such as US automakers “surely have far less monopoly power than they did twenty years ago” (Baran and Sweezy, 1966). This perception contributed to decreased attention to monopoly capital in both mainstream and radical economic debates.

However, contemporary confusion surrounding monopoly stems less from theoretical disputes than from an underestimation of globalization’s transformative impact. Influential Marxian political economists—including Paul Sweezy, David Harvey, Dominique Lévy, and Prabhat Patnaik—have explicitly centred globalization and the internationalization of production in their analyses of economic concentration. This focus distinguishes their work from earlier generations of Marxian theorists by directly linking monopoly power to transnational structures.

Building on this foundation, contemporary Marxist economists have continued to advance the monopoly capital framework. Magdoff, for instance, analysed how stagnation under monopoly capitalism facilitated the late-twentieth-century shift toward financialization and the emergence of a monopoly-finance regime. He emphasized that transnational production was reconfiguring the nature of monopolistic rivalry, accelerating the concentration and centralization of capital globally. As Magdoff (1978) observed: “The very process of concentration and centralization of capital is spurred by competition and results in intensifying the struggle among separate aggregates of capital, albeit on a different scale and with altered strategies.”

This perspective underscores that globalization has not rendered the concept of monopoly capital obsolete; rather, it has fundamentally transformed the latter’s operational scale and competitive dynamics. Consequently, it demands renewed analytical focus on the intertwined phenomena of corporate concentration, financialization, and transnational monopolistic competition.

Keith Cowling (1982) extended the monopoly capital framework by highlighting the internationalisation of oligopolies. He argued that global corporate elites formed “smaller, tighter, international oligopoly groups” in which attempts by individual firms to expand market share—through mechanisms such as tariff reductions—would be countered by immediate responses from competitors, sustaining monopoly power in each country. Cowling emphasised that free trade facilitated the growing dominance of transnational corporations, shifting profits away from global labour and smaller firms. Moreover, the expansion of international firms meant that stagnation tendencies in one country were quickly transmitted globally, amplifying the systemic effects of monopoly capitalism.

The post-1980s phase of monopoly capitalism is best described as global monopoly-finance capital, in which economic concentration, financialisation, and transnational production intersect. Samir Amin (2018) highlighted the political and social implications of this phase: the intertwining of oligopolistic capitalism, the political power of oligarchies, financialisation, US hegemony, militarised globalisation, declining democracy, and resource plunder, particularly at the expense of the Global South (Siddiqui, 2025c).

While feudalism and slavery function through overt mechanisms of domination, capitalism has demonstrated a unique capacity for legitimation by framing corporate profit imperatives as vehicles for individual equality and social advancement. It was the seminal contribution of Karl Marx, in Capital, to pierce this illusion. He identified the law of surplus value, revealing that behind the apparent freedom and equity of the market lies the hidden abode of production. There, labourers are compelled to work far beyond the time required to reproduce the value of their wages, generating the fundamental profit upon which the system depends (Amin, 2018).

The task of extending Marx’s critique to contemporary global structures was taken up by Samir Amin. Synthesizing the work of radical political economists—including Michal Kalecki, Josef Steindl, Paul Baran, and Paul Sweezy—Amin reframed Marxian theory for the age of modern imperialism. Central to his analysis is the concept of “imperialist rent,” accrued through the systemic wage differential between the Global North and the Global South for equivalent labour. This disparity is not incidental but structural, underpinning a global system of oligopolistic capitalism in which finance capital commands worldwide production and distribution. (Siddiqui, 2022).

Samir Amin (2018) crucially advanced the theory of economic surplus developed by Baran and Sweezy, reframing it within a globally monopolized system. In his analysis, Marx’s foundational “law of value” is superseded by a “law of globalized value,” a systemic mechanism that institutionalizes the super-exploitation of peripheral labour. His volume, Modern Imperialism, Monopoly Finance Capital, and Marx’s Law of Value, provides a comprehensive examination of this theoretical evolution, constituting an indispensable resource for scholars engaged with contemporary Marxian political economy and its critiques of global capitalism.

Long before its consequences became widely acknowledged, Marxist political economists provided early and rigorous documentation of the inequalities generated by neoliberalism, emphasizing the constitutive roles of financialisation and debt. Advancing this critique requires a renewed focus on monopoly power as a crucial analytical step. It is through the lens of monopoly that we can best understand the profound concentration of economic and political power, persistent stagnation, and the structural drivers of twenty-first-century capitalism (Siddiqui, 2023).

Consequently, analysing the concentration of capital and monopoly power is essential—not only for explaining economic phenomena like stagnation and financialization, but also for comprehending contemporary geopolitical structures and entrenched global inequalities. The struggle for substantive democracy and social justice is inextricably linked to confronting the political power of a corporate plutocracy that commands the world’s largest firms. For any transformative political project, therefore, effectively articulating this structural reality to those impacted by corporate dominance is central to maintaining analytical relevance and advancing a credible agenda for change.

VI. Conclusion

Monopoly capitalism represents a structural and recurrent feature of advanced capitalism, intensified by the converging forces of globalisation, financialisation, and digitalisation. The concentration of economic power within a handful of transnational corporations has fundamentally reshaped competition, labour relations, and macroeconomic stability. Through rising market concentration, persistent price markups, and the dominance of intangible assets, these firms extract monopoly rents, suppress the wage share, and constrain productive innovation—thereby reproducing the stagnationist tendencies long theorised by Baran and Sweezy.

The concentration of economic power within a handful of transnational corporations has fundamentally reshaped competition, labour relations, and macroeconomic stability.

As Marxist analysis underscores, this monopoly power is not merely a market inefficiency but a systemic outcome of capital accumulation, wherein competition paradoxically drives the concentration and centralisation of capital. This process systematically subordinates social needs to the logic of profit. The internationalisation of monopoly capital globalises these dynamics, exporting stagnation and inequality while deepening the structural divide between labour and capital. This trajectory finds its most evolved manifestation in digital monopoly-finance capital, which merges corporate dominance with financialisation, the extractive control of data and platforms, and a consequent erosion of democratic accountability.

These developments are sustained by an interrelated system of credit, intangible property rights, and corporate consolidation. Rather than undermining monopoly, globalisation and digitalisation have reinforced corporate dominance by intensifying concentration. The resulting in rising inequality, weakened aggregate demand, and heightened labour precarity that cannot be remedied by narrow antitrust frameworks alone, necessitating a structural political-economy approach.

In tracing the evolution from national industrial concentration to today’s globalised digital-financial monopolies, this study demonstrates how financialisation and the control of intangible assets exacerbate inequality, suppress competition, and weaken democracy. Understanding this system is therefore indispensable for interrogating the political foundations of twenty-first-century capitalism. Consequently, any meaningful project of democratic transformation must confront the concentrated power of global monopolies and the structural mechanisms that reproduce their dominance.

About the Author

Dr. Kalim Siddiqui is an economist specializing in International Political Economy, Development Economics, Trade and Economic Policy. Since 1989, he has been teaching economics at various universities in Norway and the UK. Dr. Siddiqui’s research interests encompass a wide range of topics, including political economy, international trade, and economic history, South Asia, and emerging economies. He has presented papers at international conferences across numerous countries, reflecting his global engagement in the field. His scholarly pursuits span six broad domains: Political Economy, Development Economics, Economic History, Economic Policy, Globalization, and International Trade. Dr. Siddiqui has made significant contributions to research in areas such as trade policy, globalization, and political economy. His work has been published in chapters of edited books and articles published in peer-reviewed journals. For inquiries, Dr. Siddiqui can be reached at: [email protected]

Dr. Kalim Siddiqui is an economist specializing in International Political Economy, Development Economics, Trade and Economic Policy. Since 1989, he has been teaching economics at various universities in Norway and the UK. Dr. Siddiqui’s research interests encompass a wide range of topics, including political economy, international trade, and economic history, South Asia, and emerging economies. He has presented papers at international conferences across numerous countries, reflecting his global engagement in the field. His scholarly pursuits span six broad domains: Political Economy, Development Economics, Economic History, Economic Policy, Globalization, and International Trade. Dr. Siddiqui has made significant contributions to research in areas such as trade policy, globalization, and political economy. His work has been published in chapters of edited books and articles published in peer-reviewed journals. For inquiries, Dr. Siddiqui can be reached at: [email protected]

References

- Amin, S. (2018) Modern Imperialism, Monopoly Finance Capital, and Marx’s Law of Value, New York: Monthly Review.

- Baran, P. and Sweezy, P. (1966) Monopoly Capital. New York: Monthly Review Press.

- Cowling, K. and Tomlinson, P. (2005) “Globalisation and Corporate Power” Contributions to Political Economy 24(1):33-54.

- IMF (2021) Rising Corporate Market Power: Emerging Policy Issues, March, IMF.

- Kwon, S.Y., Ma, Y. and Zimmermann, K. (2024) “100 Years of Rising Corporate Concentration” American Economic Review, 114 (7):2111–40.

- Marx, Karl (1993) Grundrisse, London: Penguin Books.

- Sawyer, M. (2022) “Monopoly Capitalism in the Past Four Decades” Cambridge Journal of Economics, 46:1225-1241.

- Siddiqui, K. (2025a) “The United States’ Future in an Imperial Mirror: Lessons from Britain, Spain, Abbasids, Rome, and Beyond” World Financial Review, November.

- Siddiqui, K. (2025b) “The Reasons Behind the Decline of the United States Economy” World Financial Review, May.

- Siddiqui, K. (2025c) “Reconfiguring US Hegemony: Militarism, Empire, and the Crisis of Capitalist Accumulation” World Financial Review, August.

- Siddiqui, K. (2024a) “The Decline of the West and Global Political Economy” World Financial Review, December.

- Siddiqui, K. (2024b) “Deepening Economic Crisis in the Advanced Capitalism” World Financial Review, June.

- Siddiqui, K. (2024c) “China’s Growth Miracle and Development Strategy Since the 1980s” World Financial Review,

- Siddiqui, K. (2023) “Marxian Analysis of Capitalism and Crises” International Critical Thought 13(4):525-545.

- Siddiqui, K. (2022) “Capitalism, Imperialism, and Crisis”, European Financial Review, June/July.

- Siddiqui, K. (2019). “Financialisation, Neoliberalism and Economic Crises in the Advanced Economies” World Financial Review, May/June.

- Siddiqui, K. (2018). “Capitalism, Globalisation and Inequality” World Financial Review, November/December.

- Vasudevan, R. (2022) “Digital Planform: Monopoly Capital through a Classical-Marxian Lens” Cambridge Journal if Economics 46:1269-1288.

Dr. Gleb Tsipursky PhD

Dr. Gleb Tsipursky PhD

")

")

Dr. Dan Steinbock

Dr. Dan Steinbock

")