There is a certain kind of casino player who opens a slot at 2:15 on a Tuesday afternoon, spins for twenty minutes, loses C$34, shrugs, and gets on with their day.

And then there is the Friday night player.

Different animal entirely.

That second player is not killing time between emails or sneaking in a few blackjack hands before dinner. They are settled in. Phone charged. Drink nearby. Group chat open. Maybe hockey on in the background. Maybe music. Maybe a weird confidence that tonight feels different, which is usually how expensive evenings begin.

That difference matters more than most casino review sites admit.

A lot of content in this space talks about RTP as if it floats above the world untouched by human behavior. Cold number. Fixed number. Theoretical return over millions of rounds. Fine. True enough. But that is not how players experience online casinos, and it is definitely not how sessions unfold in the real world. People do not play the same way at 1PM on a Wednesday as they do at 10:40 on a Friday night. They just do not.

Not to prove that casinos secretly loosen games after dark. That old myth refuses to die and deserves to. But to look at something more interesting, and honestly more useful. Whether Canadian players behave differently after 9PM, and whether those differences make wins feel more frequent, losses hit harder, and sessions spiral faster than they do during quieter hours.

Because sometimes the story is not in the software. Sometimes it is in the person holding the phone.

The wrong question players keep asking

People love asking whether casinos pay more at night. You see it in forums, comment sections, Reddit threads, even in half whispered conversations between friends who know just enough about gambling to be dangerous.

Do slots hit more after 9PM? Is blackjack softer late at night? Are weekend sessions better for winning?

The short answer is no, not in the literal sense. Licensed online casinos serving Canadians do not sit there nudging RTP up and down like a bartender changing the music. That is not how regulated gaming works. Random number generation does not care whether it is Friday or whether you have had two beers and a burst of optimism. If you want the dry, official version of how game fairness is treated in Ontario, the frameworks around regulated internet gaming are laid out by iGaming Ontario and the Alcohol and Gaming Commission of Ontario. Those pages are not exactly bedside reading, but they matter.

Still, the boring answer misses the better one.

Games may not change. Players do.

And when players change, outcomes change in ways that feel suspiciously like the games themselves have shifted.

Friday night is not just another session

The Friday night casino session has its own mood. That matters. Mood changes pace. Pace changes decisions. Decisions change bankroll survival.

Someone playing in the afternoon often treats gambling like a side activity. A few spins while waiting for a meeting. A short live dealer session before heading out. Less commitment. Less emotional load. Less urgency to win something back before logging off.

Night time is messier.

By 9PM, especially on Fridays and Saturdays, people tend to stay longer. They deposit in rounder numbers. They are more willing to jump from low volatility slots into something swingy and dramatic because the point is not just entertainment anymore. The point becomes momentum. They want a run. They want a story. They want that screenshot you send to a friend with too many exclamation marks.

That shift can make wins look bigger than they are. It can also make losses pile up in a way that feels sudden, even when it is just a series of small bad choices made a bit faster than usual.

And speed is the detail most people ignore.

You can survive mediocre decisions if they are spaced out. You can pause. You can think. You can get distracted by the dishwasher or a phone call or life. But compress those same decisions into a tight hour late at night, throw in autoplay, a bonus hunt, maybe a missed sense of where the bankroll has gone, and the whole session starts to feel less like play and more like drift.

Not malicious drift. Human drift.

Why late night sessions feel hotter

Part of this is simple psychology. Part of it is bankroll mechanics. Part of it is that people remember drama more vividly than they remember math.

A player who lands two decent bonuses in a short late night session walks away convinced that evenings are lucky. A player who gets buried after chasing for ninety minutes often says the opposite. What sticks is not the average. It is the emotional spike.

And evening sessions produce more spikes.

Higher bet sizes do that. Longer sessions do that. More volatile games definitely do that.

A person staking C$0.40 a spin in the afternoon can play for a while without much happening. A person staking C$2 or C$3 a spin at night enters a completely different experience. Same casino. Same RTP on paper. Completely different rhythm. Suddenly you are getting the kind of balance swings that make people believe in patterns that are not there.

This is where the liquidity idea gets interesting.

Not liquidity in the corporate finance sense. Not the dull boardroom version. Player liquidity. Session energy. The amount of money entering live gameplay during certain windows because more people are active, more money is being staked, and more risk is being taken per minute. When people ask whether Friday night is better for winning, what they often mean is whether Friday night is louder. Denser. More alive.

And yes, it is.

That does not guarantee better results. It just produces more moments that feel like evidence.

The Canadian angle makes this more interesting

Canada is a particularly good market for this kind of study because player behavior is split across different realities at once.

Ontario has a regulated market with formal oversight and a growing list of licensed operators. The rest of the country remains more fragmented, which means player experiences vary depending on where they are, what sites they use, and what payment methods they trust. Then you add timing. Weather. Sports calendars. Long winters. The fact that people spend half the year looking for ways to stay entertained indoors without putting on boots.

That all filters into gambling behavior.

Cold Friday in January in Ontario. Snow coming sideways. Plans cancelled. You can practically hear the deposit page opening.

And even outside seasonal effects, the Canadian player base has its own quirks. Interac makes deposits frictionless. Mobile play is dominant. Casino sessions often sit alongside sports betting, not separate from it. A player waiting on a third period comeback might open a slot for ten minutes and then stay for an hour because one thing bled into another.

That kind of crossover matters. It changes intent. A pure casino session behaves one way. A casino session that started as a side quest to a hockey bet behaves another way entirely.

What this study should actually measure

If you want to do this properly, you do not just compare wins at 3PM and 10PM and call it insight. That would be junk.

You need to track session conditions.

Average bet size is one. Session length is another. Game type matters a lot. So does whether a deposit was made before the session, whether a bonus was active, whether the player increased stake size after a losing run, whether they switched from table games into high volatility slots after dark. Those patterns tell you more than win rate alone ever could.

Because what you are trying to isolate is not whether the casino changed, but whether the player became a different version of themselves as the evening wore on.

I would also want to separate weekday nights from Friday and Saturday nights. They are not the same creature. Thursday night can still have traces of restraint. Friday tends to arrive with looser habits and a stronger appetite for risk. Saturday is often stranger still. Longer sessions. Less urgency. More bounce between games. More chasing disguised as entertainment.

And one more thing. This matters more than people think.

You would need to account for session endings, not just session starts.

A lot of people start casually and end recklessly. That transition is where the real story probably lives.

Why operators love late night traffic even when nobody says it out loud

Casinos may not change game outcomes at night, but there is no question they understand player rhythms.

Promotions tend to land at convenient times. Push notifications are not sent into the void by accident. A bonus reminder at 8:47PM is not there because someone in marketing suddenly felt poetic. It is there because the operator knows when people are likely to convert a passing thought into a deposit.

And that is the thing about online casinos. The game is only one layer. The product is timing, friction, mood, interface, payment flow, urgency, and the little bits of copy that make a deposit feel normal when maybe it should feel like a choice worth pausing over.

Late night play sits right in the sweet spot for all of that.

People are tired enough to click faster. Relaxed enough to justify it. Bored enough to stay. Hopeful enough to redeposit.

Not everyone, obviously. But enough.

That is why a serious study here has editorial legs. It is not just another casino article. It is consumer behavior. It is digital habit. It is the economics of boredom with a spinning reel on top.

There is also a broader context worth noting. Gambling participation in Canada exists within wider conversations around risk, routine, and public health, which is why resources from groups like the Centre for Addiction and Mental Health are worth keeping in the background of any serious discussion. Not because every player has a problem. Most do not. But because time of day, emotional state, and impulsive spending have never been separate topics.

So do wins spike after 9PM?

Maybe the better way to put it is this.

The experience of winning probably spikes after 9PM.

Not because the math changes. Because the session does.

There are more dramatic bets. More aggressive game choices. More emotional momentum. More willingness to keep playing through a rough patch because the night still feels young and the next bonus round might fix the mood. That environment produces sharper highs and uglier lows, which is exactly why so many players walk away convinced that night time gambling is somehow a different beast.

In practice, it is.

Just not in the way they think.

If this study is done properly, I suspect the result will be less glamorous than the myth but more revealing than the usual affiliate fluff. We will probably find that late night sessions are not inherently luckier. They are just noisier. More volatile. More impulsive. Better at creating the kind of memorable chaos people mistake for evidence.

And honestly, that is the more human conclusion anyway.

Because the casino at 10PM on a Friday is not only a casino. It is a mood. A habit. A little pocket of modern life where convenience, dopamine, and false confidence all decide to meet in the same room.

Mojtaba Khamenei, the newly appointed supreme leader of Iran, said the Strait of Hormuz should remain closed as part of Tehran’s effort to pressure its opponents. The statement marked his first public comments since he took the role earlier this week.

In remarks broadcast on Iranian state television, Khamenei said the closure of the strategic waterway must continue. The Strait of Hormuz is one of the world’s most important oil routes, and a large share of global crude exports normally moves through the narrow passage.

The disruption has already shaken global energy markets. Oil shipments through the strait have slowed sharply since the conflict began, contributing to a sharp rise in international oil prices.

Khamenei wants U.S. military bases in the Middle East shut down right away. He cautioned that if things get more heated, more attacks might happen.

He took over as supreme leader after his father, Ali Khamenei, passed away. Ali Khamenei was killed in air strikes by the U.S. and Israel earlier this year.

Oil prices climbed further after the comments, as traders weighed the risk that the vital shipping route could remain blocked for an extended period.

Meanwhile, Donald Trump criticised the leadership transition in Tehran and questioned whether Iran’s new leadership would move toward stability as the conflict continues.

What happens when traditional lenders retreat and borrowers still need capital? The answer has reshaped global finance over the past fifteen years: an increase in private credit.

Banks pulled back from lending after 2008. Regulators imposed stricter capital requirements on balance sheets already strained by losses. Borrowers needed alternatives, and private credit stepped in to fill the void.

Since then, private credit has become a central component of the global economy, with total global assets under management reaching an estimated $1.7 trillion in 2025, up from $310 billion in 2010.

Within that expansion, equity-backed lenders like EquitiesFirst occupy a distinct position: they provide financing against equity holdings rather than cash flows or physical assets, freeing up liquidity for those with significant equity assets.

Alternative Financing and Rising Equity Values

Private credit in 2026 stands at an inflection point. The asset class has demonstrated remarkable resilience, navigating shifting competitive dynamics with public markets. U.S. Federal regulators withdrew post-crisis leveraged lending guidance in December 2025, enabling banks to compete more aggressively in leveraged transactions and reshaping the competitive environment. Meanwhile, a significant portion of high-yield bonds and leveraged loans are set to mature in 2026 and 2027, creating refinancing demand that private lenders are positioned to capture.

These forces—regulatory shifts, maturing debt, and bank re-engagement—define the current moment for alternative financing and the firms operating within it.

Market conditions in 2025 provided a favorable backdrop for equity-backed financing capacity. The combined market value of listed equities worldwide climbed to $136.3 trillion by October 2025, nearly 15% higher than the previous year. That re-rating expanded the pool of pledgeable assets available to shareholders.

In this environment, corporate founders with concentrated positions, family offices managing multigenerational wealth, and institutional investors holding large stakes increasingly view their portfolios not as locked-in positions but as sources of liquidity. They turn to alternative arrangements that avoid the dilution that would accompany equity issuance and the tax consequences that would follow from liquidation.

Emerging Markets Face Acute Capital Scarcity

Private credit deployment has accelerated fastest where capital remains most scarce. Private lenders deployed $18 billion in emerging markets through 2025, reaching record levels as funds flowed into regions where traditional banking infrastructure lags demand. The World Bank estimates that formal small and medium enterprises across 119 developing economies face a financing shortfall of approximately $5.7 trillion, equivalent to 19% of GDP. Roughly 40% of formal SMEs remain credit-constrained.

That gap has struggled to close through conventional channels. Banks in emerging markets operate under capital constraints, currency risks, and regulatory limitations that restrict lending capacity even when demand is evident.

Alternative financing providers like EquitiesFirst operate across international markets, providing financing to clients in jurisdictions where access to low-cost credit remains limited. Borrowers with substantial equity positions but less access to traditional banking can pledge those holdings to unlock liquidity.

Infrastructure Spending Demands Long-Duration Capital

Capital-intensive sectors tied to digital infrastructure and artificial intelligence are growing faster than traditional bank balance sheets can support. Hyperscalers including Meta, Amazon, Microsoft, Alphabet, and Oracle are projected to increase capital expenditure by 70% year over year, with spending expected to reach $600 billion in 2026. These investments will finance data center construction, networking infrastructure, and computing hardware essential to AI deployment.

Private credit funds have emerged as key financiers of these buildouts, providing long-term capital aligned with infrastructure economics. Club deals involving syndicates of private lenders are replacing portions of the leveraged loan market that banks once dominated, a shift that reflects both the scale of capital required to build out the next generation of tech infrastructure and the structural flexibility private lenders can offer.

Asset-Backed Strategies Gain Share

Corporate lending still makes up most of private credit, but momentum is shifting toward asset-backed finance. While more difficult to track, ABF has the potential to eclipse the size of traditional corporate lending, according to a recent Moody’s report. Alternative asset managers are extending their reach beyond bank and insurance partnerships to finance companies and specialist originators, purchasing loans shortly after origination and expanding into consumer debt and hard assets.

Recent months have seen substantial ABF partnerships emerge. TPG entered a $1 billion forward-flow agreement with Elevex Capital to provide capital for mid- and large-ticket equipment financing. Apollo led a $3.5 billion capital solution for Valor Compute Infrastructure’s acquisition and leasing of compute assets to xAI. Blackstone partnered with Willis Lease Finance to deploy over $1 billion into aircraft engine assets.

These forward-flow agreements commit managers to regularly purchase newly originated loans at set terms, enabling both sides to operate more efficiently and scale faster.

Banks and Private Credit Converge

Private credit has not displaced banks; the two sectors are increasingly integrated. In recent years, major banks have announced partnerships with private credit firms, including Wells Fargo with Centerbridge Partners, Citigroup with Apollo Global Management, and Barclays with AGL Private Credit. These arrangements allow banks to originate and distribute loans without holding them on balance sheet, preserving capital ratios while maintaining client relationships and fee income.

The decision by U.S federal regulators to withdraw leveraged lending guidance that had restricted bank participation in certain transactions gives banks greater flexibility and could expand financing capacity across the market.

2026 Outlook: Growth Continues Across Segments

JP Morgan projects credit assets under management to surpass $2.3 trillion in 2026. Funds raised $131 billion in the first nine months of 2025 alone, according to Preqin data, reflecting sustained investor appetite. Wealthy families and institutional allocators are shifting billions into credit and real estate, reducing venture capital exposure and increasing allocations to income-generating assets.

Market conditions support continued private credit expansion. U.S. interest rate cuts are anticipated in 2026, which should ease debt servicing costs and support mergers and acquisitions activity, where private credit historically thrives. Private equity dry powder has reached $2.7 trillion, creating substantial pent-up demand for acquisition financing as sponsors seek to deploy committed capital.

Private credit has evolved from alternative to necessity. It finances infrastructure, supports mid-market growth, and provides liquidity solutions across asset classes and geographies.

Equity-backed financing from firms such as EquitiesFirst enables shareholders to access flexible capital financed against existing assets. It finances against equity, and as major equity markets have increased and private credit expands into new asset classes and markets, equity-based financing stands to continue to expand alongside corporate lending as an additional tool in a more diverse capital ecosystem.

Several leading technology companies have stepped in to support Anthropic in its legal battle with the administration of Donald Trump. The case follows a decision by U.S. Defense Secretary Pete Hegseth to label the artificial intelligence company a “supply chain risk,” a move Anthropic is challenging in court.

Companies including Google, Amazon, Apple, and Microsoft have filed statements supporting the lawsuit. In legal submissions, they warned that government retaliation against a technology firm could have wider consequences for the industry.

The dispute began after Anthropic resisted requests to remove safeguards in government contracts that restricted the use of its AI tools for mass surveillance or autonomous weapons. The company argued that weakening those protections would raise serious ethical and security concerns.

A joint filing from the tech advocacy group Chamber of Progress also backed Anthropic’s position. The group said the government’s actions could discourage companies from speaking openly about the risks of emerging technologies.

Anthropic claims the designation as a supply chain risk damaged its reputation and business relationships. During a court hearing in San Francisco, its lawyers said government officials had contacted some of the company’s clients and urged them to stop working with the firm.

The case has drawn attention across the technology sector because it highlights growing tensions between artificial intelligence companies and government agencies over how advanced AI systems should be used. Industry leaders say the outcome could shape how firms negotiate future contracts with federal agencies.

Picture a leadership team announcing a stricter return-to-office policy and expecting a productivity surge. The data tells a different story. Across practitioner reports and peer-reviewed research, including a new report from the Institute for Corporate Productivity (i4cp), organizations that commit to highly flexible models, including remote-first, report strong output, healthier engagement, and faster growth than mandate-driven peers. The gap between intuition and evidence has widened as new results arrive from both the private and public sectors.

The newest practitioner evidence should give leaders confidence. In the i4cp’s Remote-First Organizations report, most leaders in remote-first firms say productivity remains high, with a sizable share reporting it is very high, and the majority avoid invasive monitoring. The research frames remote-first as a deliberate operating model anchored in trust, clarity, and well-designed touchpoints, not a stopgap.

The long-running time series offers leaders an external benchmark for setting policies that reflect labor market realities rather than nostalgic preferences.

Independent national data aligns with these practitioner insights. In October 2024, a U.S. Bureau of Labor Statistics analysis reported a positive relationship between growth in remote work and total factor productivity across industries. A related BLS briefing summarized the same finding for leaders: industries that expanded remote work faster also saw faster productivity growth over the pandemic period. These are not isolated anecdotes; they are economy-wide patterns.

Performance shows up in the P&L as well. The Flex Index, in joint research with BCG, finds that fully flexible companies grew revenues 1.7x faster than mandate-driven firms from 2019 to 2024, even after adjusting for industry and size. That advantage is hard to ignore in a margin-sensitive, rate-constrained environment.

The experimental evidence is equally compelling. A large randomized working paper and subsequent peer-reviewed study of Trip.com’s two-days-from-home hybrid schedule found no decline in performance or promotion rates and a one-third reduction in quits. Randomized trials are rare in management research. When they confirm what observational data already suggests, leaders should take note.

Organizations choose remote-first for what it enables, not what it avoids. The i4cp study emphasizes outcome-based measurement, intentional gatherings, and codified norms to keep teams aligned at scale. Those are management upgrades, not experiments in absenteeism.

Executives do not adopt remote-first for PR. They adopt it to win talent markets. The i4cp report shows leaders prioritize flexibility to widen and diversify their pipelines, to improve well-being, and to sustain trust. Making remote-first the default unlocks national or global hiring, removes zip code penalties, and reduces relocation friction, which translates into faster recruiting cycles and better role-to-skill matches.

The talent upside is measurable. The global Survey of Working Arrangements and Attitudes, maintained by WFH Research, provides a continuously updated dataset that tracks how hybrid and remote work have stabilized since 2022 and how employees value flexibility. The long-running time series offers leaders an external benchmark for setting policies that reflect labor market realities rather than nostalgic preferences.

Public-sector findings point in the same direction. The U.S. Government Accountability Office’s 2025 report on telework noted that agencies used flexibility to maintain operations during the pandemic and to support recruitment and retention afterward. GAO pressed agencies to evaluate outcomes rigorously, but the message to executives in any sector is straightforward: when flexibility is codified and measured, it becomes a dependable lever for organizational health.

The talent case is not only about headcount. It is about who you can reach. Remote-first policies broaden access to caregivers, people with disabilities, and candidates outside premium cost-of-living markets. That reach composes stronger teams and, in a competitive hiring cycle, saves real money.

If flexibility supports performance and expands talent, what do RTO mandates do? A growing body of research answers bluntly: not what their champions promise. A widely cited University of Pittsburgh working paper on S&P 500 companies found RTO mandates did not improve financial performance or firm value, while employee satisfaction declined. Summaries from professional associations and business schools reinforce the point for non-academic audiences, but the core evidence is in the working paper itself. Complementary evidence using distributional synthetic controls found that RTO announcements at major firms shifted tenure and seniority downward, consistent with a higher-skilled talent outflow, in a 2024 analysis.

Leaders sometimes argue that stricter in-office rules are needed to fix collaboration or innovation. The better path is to raise the bar on management, not badge swipes. The i4cp report describes organizations that use “magnet, not mandate” logic, pairing remote-first defaults with intentional gatherings, clear policies, and outcome-based performance management. The combination produces high trust, defined norms, and sustained results.

The risk profile for mandates is asymmetric. If they fail to lift performance, you absorb morale damage and replacement costs while sending a public signal that policy, not management, is your lever. If they “work,” the effect often comes from short-term pressure rather than durable operating improvements. Flexibility, by contrast, compounds. The Flex Index analysis shows fully flexible firms outgrowing mandate-driven peers over multiple years. The BLS research connects remote adoption with productivity gains at the industry level. The Trip.comtrial demonstrates causality on retention without a trade-off on performance. Together, these results form a coherent, leader-ready narrative.

The organizations that choose the latter are building stronger teams and better businesses.

The evidence now spans practitioner fieldwork, randomized trials, federal oversight, and macroeconomic analysis. It points in the same direction. Highly flexible models, including remote-first, sustain productivity, expand access to talent, and strengthen culture when leaders manage for outcomes, codify norms, and invest in purposeful connection. The i4cp report adds practical depth from companies that are already operating this way, while national and academic research shows why it works and what it delivers over time.

Executives face a choice. They can pursue badge-driven control that fails to raise performance and risks losing their best people. Or they can treat flexibility as strategy, design for trust and clarity, and measure what matters. The organizations that choose the latter are building stronger teams and better businesses. The smart move now is not to roll back flexibility. It is to raise the standard for how you lead it.

This paper examines how Indian merchants such as Parsi, Marwari, Baghdadi Jewish and others accumulated capital as junior partners in the colonial opium trade (1773–1900). Dr Kalim Siddiqui argues that operating within the East India Company’s monopoly system, they profited from smuggling opium into China. As the trade faced scrutiny, they diversified into cotton textiles, and other industries leveraging their wealth and networks to lay foundations for Indian industrial capitalism.

I. Introduction

The historiography of Indian capitalism has long been framed within a narrative of de-industrialization and colonial exploitation—a perspective powerfully articulated by nationalist economists such as Dadabhai Naoroji, R.C. Dutt, A.K. Bagchi, Irfan Habib and others. Their influential “drain theory” illuminated the mechanisms through which British rule systematically extracted wealth from the subcontinent, impoverishing its people while enriching the metropole (Siddiqui, 2024a; Habib, 2022). Yet this interpretive framework, for all its analytical power, has inadvertently obscured a parallel history: the accumulation strategies, and complex collaborations of indigenous merchant capital within the colonial political economy. This study addresses this lacuna by examining the critical—and under-theorised—role of Indian merchant communities as active participants in the opium trade that underwrote Britain’s imperial expansion in Asia.

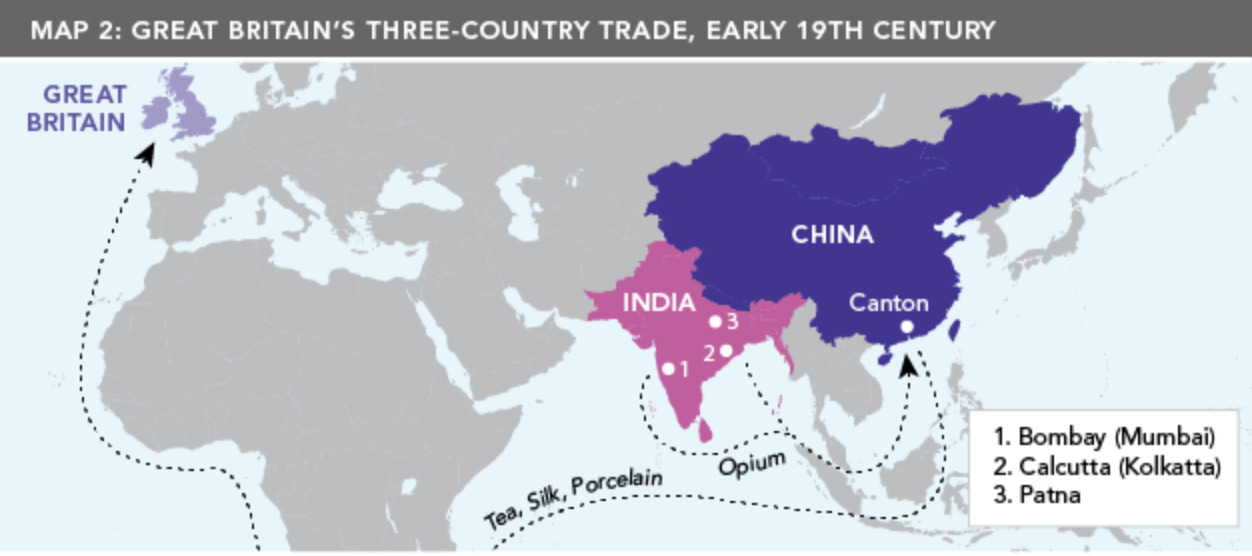

The trade in Chinese commodities, particularly tea and silk, posed significant financial challenges for the East India Company (EIC), a corporation owned entirely by British shareholders, which struggled to finance imports due to the absence of a cost-effective medium of exchange acceptable to the authorities of Qing China. At the time, Britain faced a persistent trade deficit with China, driven by strong European demand for Chinese commodities such as tea, silk, and porcelain, while Chinese consumers showed little interest in British manufactured goods. In response to this imbalance, British merchants increasingly relied on the export of opium to China. Following the Company’s victory at the Battle of Plassey in 1757, it secured political and economic control over key opium-producing regions in India and consolidated a monopoly over its production. Indian peasants were compelled to cultivate opium under this system, and the drug was subsequently smuggled into China, where its sale financed Britain’s purchases of Chinese commodities (Siddiqui, 2024b).

In 1773, Warren Hastings, Governor-General of Bengal, declared opium production in Bengal a monopoly of the EIC. The Company subsequently developed inexpensive and large-scale methods of cultivating opium poppies across its Indian territories. Under this system, the Bengal colonial administration controlled both the production and sale of opium, which soon emerged as a highly effective commodity of exchange. Opium not only generated its own demand but also helped offset the mounting costs associated with importing Chinese goods.

However, because the authorities of Qing China had imposed a ban on opium imports, the EIC could not ship the drug directly to China. Instead, it devised an indirect system: opium was auctioned in Calcutta to private merchants, who assumed the considerable risks—and potential profits—of smuggling it into China. This arrangement allowed the Company to avoid directly violating Chinese law while still capturing the bulk of the production surplus generated by the trade (Siddiqui, 2024a).

The opium trade that flourished under this system was among the most profitable and consequential enterprises of the nineteenth century. It resolved Britain’s chronic trade deficit with China, financing the burgeoning national appetite for tea while simultaneously creating a vast, dependent consumer population for opium in the Qing Empire. The trade’s illicit nature did not diminish its scale or sophistication; by the 1820s, opium had become the single largest commodity in world trade, valued at more than tea and coffee combined. Its geopolitical ramifications were equally profound: Chinese efforts to suppress the trade precipitated the Opium Wars (1839–1842; 1856–1860), which culminated in China’s forced opening under unequal treaties and the cession of Hong Kong to Britain.

Opium not only generated its own demand but also helped offset the mounting costs associated with importing Chinese goods.

Less recognized in this familiar imperial narrative is the trade’s transformative impact on economic development within India itself. In Bombay (now known as Mumbai), the opium trade provided an unparalleled avenue for capital formation among indigenous merchant communities. As early as 1803, private Indian enterprises were actively engaged in opium smuggling, often resisting British monopolistic controls through ingenious evasion. This covert commercial resistance contributed significantly to Bombay’s emergence as the preeminent center of economic activity in western India. More importantly, the fortunes accumulated through opium—by Parsi shipowners, Marwari financiers, and Baghdadi Jewish merchants like the Sassoons—would later seed the subcontinent’s industrial transformation. By the end of the nineteenth century, these merchants were leveraging their opium-derived wealth and global commercial networks to establish control over the cotton textile industry, laying the groundwork for modern Indian industrial capitalism (Siddiqui, 1996).

This paper traces that trajectory: from junior partners in an empire of illicit trade to pioneers of indigenous industrialization. In doing so, it offers not only a more nuanced account of Indian agency within colonial political economy but also a case study in the entangled moral economies of empire, where the profits of addiction financed the foundations of national capital.

Mainstream economists, focused on formal institutions and industrial development, have often failed to account for the primary sources of capital accumulation that later fuelled Indian industrial enterprise. They have also neglected the complex, ambivalent relationship between Indian merchant capital and the dominant British mercantile and colonial state. This paper argues that understanding the evolution of Indian industrial capitalism requires rigorous examination of the origins of this capital and the mechanisms of its accumulation during early colonial rule. The opium trade, despite its subsequent notoriety, served as a crucial—if morally fraught—crucible for this process.

The prevailing historical narrative often relegates Indian merchants to the role of passive intermediaries or compradors, mere cogs in the wheel of the British imperial enterprise. This perspective, however, obscures a more complex and dynamic reality. A critical examination of the primary sources of capital accumulation during the British colonial period reveals a foundational, yet fraught, phase in the growth of Indian capitalism. This was an era in which prominent merchant families did not simply serve as junior partners, but actively forged their own paths to wealth and influence, navigating the constraints and opportunities of colonial hegemony. By strategically operating within foreign markets, leveraging colonial trade networks, and selectively adopting new technologies, these business communities laid the groundwork for modern Indian enterprise, all while remaining fundamentally shaped by the unequal power dynamics of the Raj (Siddiqui, 2020a).

This study examines the paradox of Indian capital accumulation under colonial rule, moving beyond the simplistic comprador thesis to argue that Indian merchants functioned as proto-industrial capitalists who devised sophisticated strategies to build their fortunes. Their reliance on the colonial regime for protection and market access signified not passivity, but pragmatic adaptation within a structurally disadvantaged system. Those merchant communities that benefited from British imperialism and its wider Asian markets, recognised that aligning with British capital could facilitate global expansion while offering security, financing, and access to new technologies.

Paradoxically, the very technologies and legal frameworks imposed by the British—including telegraphs, railways, and contract law enforcement—became tools that these enterprising business families could, within limits, leverage to their advantage. Wealth accumulation thus unfolded as a dual process: collaboration with colonial power generated substantial profits, even as a quieter, parallel process built indigenous financial, commercial, and industrial capacity that would ultimately outlast the empire itself (Habib, 2022).

By focusing on specific merchant communities and family dynasties, such as the Parsis of Bombay (like the Tatas and Wadias), the Marwaris of Calcutta (like the Birlas), or the Chettiars of Madras, we can trace the diverse trajectories of this capital formation. Their stories reveal a pattern of beginning as traders, financiers, or collaborators with British capitalists, and then strategically diversifying into nascent industries like textiles, mining, and banking (Habib, 2022). They utilized capital accumulated through trade to challenge British monopolies in certain sectors, demonstrating that the “junior partner” was often learning the business with the intent of one day becoming a competitor. This complex interplay of collaboration and competition, dependence and defiance, constitutes the essential dialectic of Indian capitalism’s formative years. To understand the post-colonial economic might of India, one must first look to this crucial, and often misrepresented, period of gestation under colonial hegemony.

This study challenges this view by analysing their multifaceted involvement in the opium monopoly. From procuring raw opium in Malwa and Benares to its processing, transport, and sale in Calcutta, Indian merchant houses—such as the famous trading firms of Bombay and Calcutta—were indispensable. They operated not as simple agents but as crucial nodes in a complex commodity chain, managing credit networks, supply logistics, and market intelligence that the EIC could not easily replicate. This was not a relationship of pure subordination but one of asymmetrical interdependence. The Company relied on the capital, expertise, and infrastructure of Indian merchants to make the opium enterprise viable, while Indian merchants leveraged this partnership to generate substantial profits and accumulate capital on an unprecedented scale (Farooqui, 2021).

The role of Indian merchants in the opium trade thus demands scholarly attention for reasons extending beyond the history of a single commodity. First, it illuminates the significant agency of a non-European group within the international drug trade, demonstrating that the victims of imperialism could also, under constrained conditions, serve as its intermediaries and beneficiaries. Second, Parsi, Marwaris and other Indian involvement in opium constituted an important component in the rise of profits, the development of the Indian and imperial economies, and the growth of Bombay and other colonial commercial centres. Third, and most significantly, this history reveals the capacity of an illicit commodity to serve the material interests of non-European groups under imperialism. Opium provided not only profits but also the economic foundation for the subsequent social and political development of an Indian merchant class that would, in time, transform itself into a national bourgeoisie (Guha, 1984).

II. Opium, Empire, and Indian Merchants: Production, Exports, and Political Economy

Before examining the role of Indian merchants in the opium trade, it is essential to first understand the scale and expansion of opium exports to China, as well as the political economy of this trade that culminated in the Opium Wars and stiff resistance from the Chinese government. Under Mughal rule, India already possessed a sophisticated money market and complex credit instruments, such as the hundi, which challenge any notion of a passive or underdeveloped merchant class. By the late seventeenth century, merchant-bankers had become integral to the empire’s fiscal machinery, managing tax collection and facilitating the transmission of revenue across vast distances. Prominent financiers like the Jagat Seths of Bengal were not mere moneylenders but diversified capitalists whose financial backing could determine succession battles and the viability of provincial administrations (Farooqui, 2021).

However, the relationship between merchant-financiers and political power, though deeply embedded, remained personal and contingent. The prosperity of merchants rested on an “alliance between the businessman and the state,” but this dependence on individual patronage inhibited the development of institutional mechanisms capable of systematically aligning state authority with commercial interests. The Mughal state met its substantial credit requirements largely through agricultural revenues and loans from prominent bankers, creating a relationship characterized simultaneously by state dependence and the precarious privilege of the financier. This precolonial legacy—of sophisticated commerce operating within politically contingent frameworks—would profoundly shape how Indian merchants navigated the very different political economy of British rule.

The opium trade fundamentally reshaped the economic and political landscape of nineteenth-century China. Britain’s growing national obsession with tea created a chronic trade deficit, as China demanded payment in silver, not British goods. Following its decisive victories at Plassey (1757) and Buxar (1764), the EIC gained control over India’s most fertile regions. From 1773 onward, it established a state monopoly on opium production, compelling peasants in Bengal and Bihar to cultivate poppies for cheap and abundant export to China. While this system generated enormous revenues for the British, it also entrenched economic backwardness in regions such as the Bihar and Eastern Uttar Pradesh, distorting local economies and entrenching dependency.

Although the EIC monopolised British trade with South and East Asia, private ventures operated under its license through “country ships”—vessels chartered to sail between India and China, distinct from the Company’s own ships. Between 1764 and 1800, six of every ten country ships originated from Bombay, with two each from Bengal and Madras. Key Opium exporters were predominantly Englishmen resident in India, alongside a smaller number of Indians namely Parsis and Marwaris (Subramanian, 2017).

Opium occupied a central position in the political economy of British colonialism in India. At its peak, it constituted one-third or more of India’s total exports by value, serving simultaneously as an indispensable source of revenue for the colonial administration and as a primary conduit for remitting the imperial tribute—including the private fortunes amassed by EIC officials and British merchants. Beyond its fiscal functions, the trade financed Britain’s larger imperial commerce: opium sold in China provided the silver necessary to purchase Chinese tea, silk, and porcelain, which yielded enormous profits upon resale in Britain and Europe. The trade thus formed a lynchpin connecting the exploitation of India, the penetration of China, and the enrichment of the metropolitan economy (Farooqui, 2021).

Alongside moneylending, the opium trade served as a critical source of capital accumulation for Indian merchants. During the colonial period, land ownership underwent profound transformation, marked by sharply rising peasant indebtedness, landlessness, rising land rents, and the rise of absentee landlordism. Although cultivation of cash crops—jute, cotton, indigo, and opium—expanded, peasant incomes deteriorated. The agricultural surplus generated was largely siphoned off as tribute to Britain. Unlike in the precolonial era, this surplus was not reinvested in agriculture, contributing to long-term productivity decline and recurrent famines—phenomena largely unknown in the preceding period. The resulting rural impoverishment and mass mortality led to population stagnation over two centuries of British rule. (Siddiqui, 2020b).

Following the conquest of Bengal, the EIC established a monopoly over the opium produce of Bihar, initially through the private dealings of Company servants and later as an official colonial monopoly by the end of the eighteenth century. This monopoly was extended to Banaras, Ghazipur, and other opium-producing districts of the Ganga region as they came under the EIC control. In 1797, a formal policy was introduced under which all opium produced in Company territories in eastern India was directly appropriated from peasant cultivators. (Ghosh, 2008).

Once the EIC assumed control over the opium-growing districts of Bengal and Bihar, British shipping dominated the export of Bengal opium through Calcutta. Despite the Chinese edict of 1729 prohibiting opium smoking, consumption of Bengal opium in China increased fivefold in less than forty years, rising from 200 chests annually in 1729 to 1,000 chests by 1767. Even in the face of illegality, Chinese officials collected tariffs on the trade, reflecting the entanglement of commerce, imperial control, and local governance (Siddiqui, 2020a).

By 1819, confronting the persistent failure of its earlier prohibitionist measures to curb the flow of contraband opium from central India, the EIC adopted a new strategic approach. The objective was to bring the Malwa opium crop under its regulatory and commercial control in a manner analogous to its established monopoly in Bengal. The new policy mandated that the Company purchase the entirety of the Malwa opium harvest, which would then be officially auctioned at the ports of Bombay and Calcutta. From these auctions, merchants could legally (from the British perspective) ship the commodity to the Chinese market. This strategy represented an attempt to transform an uncontrollable illicit trade into a state-managed monopoly that could capture its revenues (Brown, 2002).

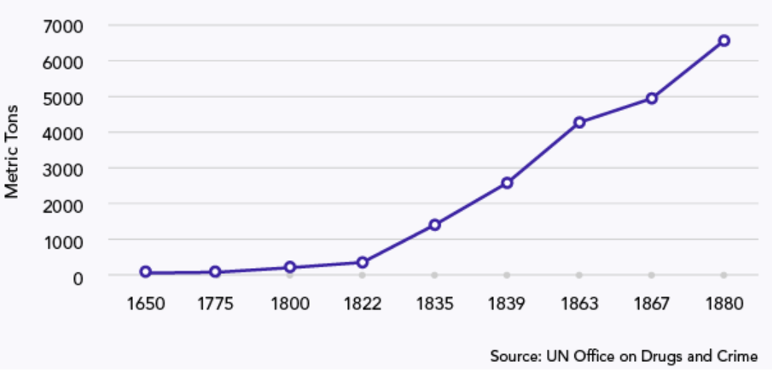

However, this attempt to assert control proved largely unsuccessful, encountering robust resistance from the entrenched commercial networks of Malwa. The region’s sahukars (merchant-bankers) and opium cultivators responded to the Company’s intervention with strategies of evasion and market defiance (Ghosh, 2008). They increased overall production, deliberately cultivated surplus opium to be sold outside official Company channels, and effectively circumvented the EIC’s purchasing mechanism by continuing to smuggle their product. The result was not a decline in the trade but its dramatic acceleration. Official exports of Malwa opium to China surged: from 1,715 chests in 1821–22, they nearly tripled to 4,000 chests the following year, a high volume that was sustained through most of the 1820s. The sharp increase in opium trade due to the Company’s policy is starkly illustrated in Figure 1. While the graph shows a general upward trend in total opium exports to China beginning after 1775—a period coinciding with the EIC’s consolidation of its monopoly over production and exports in Bengal—the curve becomes markedly steeper after 1822. This sharp inflection point visually captures the explosion in trade driven by the unregulated and officially-supplied Malwa opium, underscoring how the Company’s attempt to monopolize the crop inadvertently catalysed an even greater volume of opium entering China (Siddiqui, 2020a).

While much attention focuses on the Company’s military and political activities after 1757, it is important to remember that the EIC remained fundamentally a private commercial enterprise. Its primary objective was to earn profits for shareholders, who received dividends throughout the Company’s rule and even after its dissolution. The Company was formally dissolved in 1874, without loss to its shareholders.

The final commercial privileges surrendered by the Company—most notably the monopoly of the China trade in 1834—did not diminish shareholder returns. On the contrary, the guaranteed dividend payable to shareholders increased slightly, from 10 to 10.5 percent, funded from the Company’s political revenues rather than commercial profits. As Karl Marx observed in 1858, the EIC’s transition from commercial to political revenue effectively maintained shareholder income: “The commercial existence of the East India Company was terminated in 1834, when its principal remaining source of commercial profits, the monopoly of the China trade, was cut off. Consequently, the holders of East India stock, having derived their dividends nominally from trade profits, required a new financial arrangement. The payment of dividends, previously chargeable upon commercial revenue, was transferred to its political revenue. The proprietors of East India stocks were to be paid out of revenues enjoyed by the Company in its governmental capacity” (New-York Daily Tribune, 9 February 1858).

The opium trade not only served imperial interests but also nurtured certain forms of indigenous capitalism in Asia, a dynamic noted by Karl Marx, who examined the broader Asian opium economy encompassing India, China, and Southeast Asia. Subsequent scholarship has highlighted the particularly Indian dimension of this trade, emphasizing the role of local merchants and intermediaries in sustaining the flow of opium to China. This arrangement highlights the inseparable link between colonial governance, commercial monopoly, and shareholder profit, illustrating how the Company’s political authority was leveraged to secure financial returns from its imperial dominions (Siddiqui, 2020a).

The drug that poisoned China enriched Bombay, and the fortunes made in its traffic funded the cotton mills that became symbols of Indian industrial aspiration. As Farooqui (1996:2746) notes: “Bombay as a great commercial and industrial centre was born of its becoming an accomplice in the drugging of countless Chinese with opium, a venture in which the Indian business class showed great zeal alongside the British. This is the sordid underside of Bombay’s colonial past. Towards the end of the 18th century Bombay, having been drawn into the vortex of capitalist relations, was assigned its role in the world capitalist system. Through colonial manipulation Bombay was made the main spatial regulator, in western and central India, for the transfer of tribute to the metropolis. In the process the hegemony of capitalism was fomented in the city. In the case of an advanced capitalist country like Britain establishing a colonial relationship with regions in which the capitalist mode of production is not sufficiently developed, or not dominant, problem of transition to capitalism is complicated by the fact that the colonial power seeks to create a mechanism for tribute realisation which as loot/plunder/drug- trafficking may form a part of the prehistory of capitalism.”

The rise of Bombay as India’s premier commercial centre in the nineteenth century was closely intertwined with the colonial opium trade. British opium policy created divergent conditions in eastern and western India. While the EIC maintained a strict monopoly over opium produced in Bengal, Bihar, and Awadh, Malwa and Rajasthan were subject to a more flexible, non-monopolistic system. This allowed private Indian merchants to participate directly in trade and linked the Malwa hinterland to Bombay’s port economy. Between 1821 and 1833, exports of Malwa opium from Bombay rose sharply, from fewer than 5,000 chests to nearly 40,000, reflecting the city’s emergence as a central transshipment hub. Indian merchants’ opium trade financed British purchases of Chinese tea while generating revenue for colonial authorities, forming a triangular system of trade linking India, China, and Britain. This mechanism underscored opium’s centrality to early global commerce and imperial finance.

The Chinese government, recognising the escalating social damage caused by narcotic addiction, had formally banned both the production and importation of opium in 1800. Despite this prohibition, the EIC and the private British merchants who succeeded it persisted in systematically smuggling the drug into China. The scale of this illicit trade grew exponentially. Between 1810 and 1838, annual opium imports surged from approximately 4,500 chests to a staggering 40,000 chests.

This dramatic rise in consumption precipitated a severe economic crisis for the Qing Empire. The massive volume of opium imports reversed China’s traditional trade surplus, leading to a crippling outflow of silver, the country’s monetary standard. The drain intensified rapidly: from an estimated loss of two million ounces of silver annually in the early 1820s, the outflow skyrocketed to over nine million ounces per year by the early 1830s. This monetary haemorrhage destabilised the imperial economy, depleting state reserves and causing severe deflation that burdened the general populace (Siddiqui, 2024b).

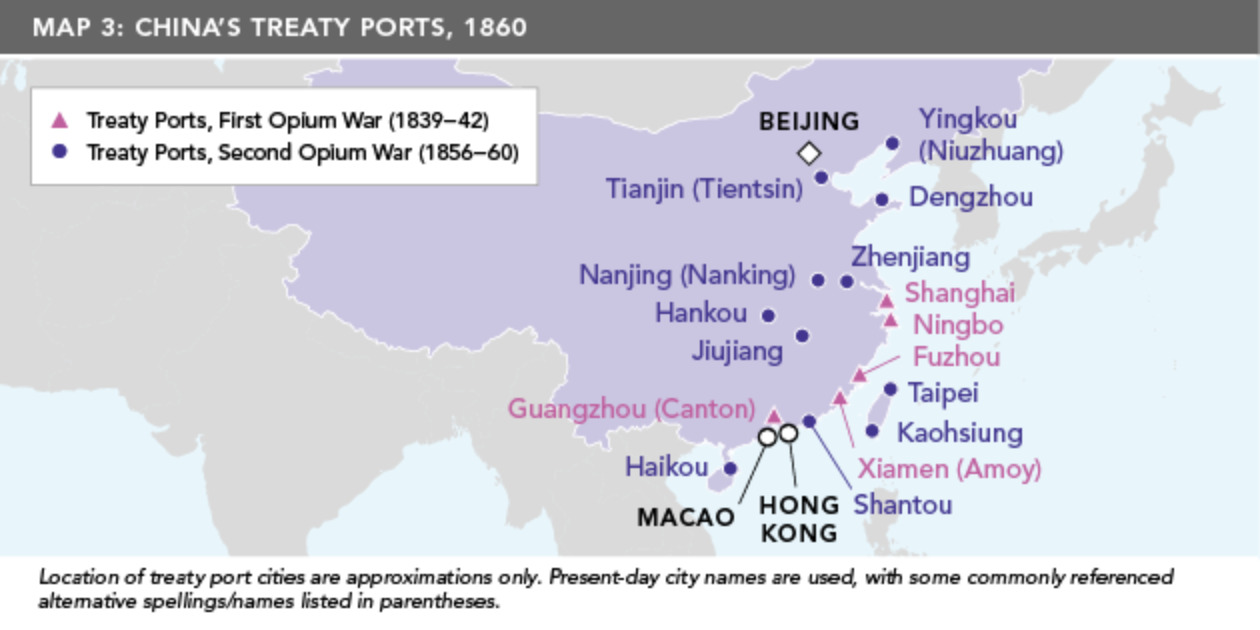

The Qing court’s decisive attempt to halt opium trade by confiscating and destroying over 20,000 chests of opium at Canton (Guangzhou) in 1839 provided the catalyst for armed conflict. In June 1840, a British naval expeditionary force arrived off the Chinese coast, initiating the First Opium War (1839–1842). After bombarding coastal forts and capturing key cities, Britain compelled a preliminary settlement. The conflict formally ended with the Treaty of Nanjing (1842), the first of the “unequal treaties” that would define a century of Chinese subjugation. The terms were entirely one-sided and offered no benefit to China. They forced the Qing to open five treaty ports (including Shanghai and Canton) to foreign trade, grant British citizens extraterritorial rights (exemption from Chinese law), pay a substantial indemnity, and cede the island of Hong Kong to Britain in perpetuity. Crucially, China was forced to halt its enforcement of the anti-opium laws.

Dissatisfied with the commercial access gained and seeking to expand the trade, Britain, allied with France, launched the Second Opium War (1856–1860). And in 1860, British and French troops looted and burned the Old Summer Palace (Yuanmingyuan) in Beijing. Prior to the fire, the forces seized thousands of artifacts, including porcelain, silk, pearl and gold ornaments. In China, this event is regarded as a symbol of national humiliation and imperialist aggression.

This conflict concluded with the humiliating Anglo-French capture and occupation of Beijing. The resulting treaties (the Treaties of Tianjin) imposed even harsher terms on China. Among the most significant provisions was the legalisation of the opium trade itself, albeit subject to a nominal import tax. This effectively forced the Chinese government to abandon its moral and public health stance and accept the drug’s influx as a legitimate article of commerce. The agreements also opened eleven additional treaty ports, imposed further indemnities, and permitted increased Christian missionary activity across the interior.

The consequences of these wars were catastrophic for the Qing Dynasty and Chinese society. The “unequal treaties” crippled the state’s legitimacy, demonstrating its military and diplomatic weakness to its own subjects and the world. Economically, the legalized opium trade continued to drain China’s silver reserves for decades; imports peaked at a staggering 87,000 chests in 1879, exacerbating the very social damage—widespread addiction and poverty—that the original ban had sought to prevent (Siddiqui, 2019). The volume of imports only began to decline by the end of the 19th century and the trade largely ceased during World War I.

The opium economy had permanently reshaped the trajectory of India and China. China’s defeat in these mid-century conflicts signalled the terminal decline of the Qing state, setting the stage for internal rebellions, the fall of the monarchy in 1911, and a “Century of Humiliation.” For Britain, the wars secured a lucrative commodity that helped balance its trade with China and finance its imperial administration in India. The Opium Wars thus mark a pivotal turning point in modern history, where the forces of British imperial capitalism, operating under the banner of ‘free trade’, forcibly dismantled China’s sovereignty and integrated it into a global economic system on profoundly unequal and destructive terms.

III. The ascent of Parsi and Jewish Merchants in the Opium Trade

The Parsis were distinct from the village-based Hindu caste society of Gujarat. Even if they had integrated with Hindu artisans, intra-village jajmani production relations would likely have remained tenuous. This structural separation, however, allowed Parsi small producers to bring larger marketable surpluses than their Gujarati caste-based counterparts, particularly during the commercialisation of Mughal India.

Under British rule, Parsis who adopted new business practices—working as brokers, agents, and intermediaries for Europeans—were well positioned to succeed financially, provided their ambitions remained within colonial limits. Their skills in carpentry enabled some to establish manufactories producing horse coaches and bullock carts. Yet such activities, though cultivating small-scale capitalists and a capitalist outlook, accounted for only a fraction of the wealth the community had accumulated by 1840 (Guha, 1984).

The Parsis, descendants of Zoroastrians who migrated from Iran to India in the eighth century, constitute one of the country’s smallest communities. As migrants, they settled in urban areas, rapidly adopting the Gujarati language and leveraging their commercial skills. They enjoyed a special status in western India as enterprising traders, and were quick to appreciate the advantages of the British connection in the Indian Ocean trade, specifically with China, from the latter half of the 18th century. Parsis participation in the opium trade represents an important non-European contribution to imperial commerce, facilitating the accumulation of wealth in western India while supporting the expansion of both the Indian and imperial economies. Under British India, however, they transformed from a relatively insular group into one of the subcontinent’s most prosperous, educated, and influential communities. From their ranks emerged prominent merchants whose participation in the opium trade with Qing China generated substantial capital, much of which was reinvested in other profitable ventures (Palsetia, 2008).

The opium trade provided a vital opportunity for capital formation, allowing the community to evolve from petty traders and contractors in the 18th century to major shipbuilders, brokers, and merchants by the 19th century. From the early eighteenth century, Bombay emerged as the primary centre for the Parsi community. Migrating from Gujarat and surrounding regions, Parsis capitalised on the security offered by the EIC and the growing opportunities from trade and urban expansion. They played a key role in transforming Bombay into a thriving commercial hub, distinct from entrenched port cities like Surat. Their economic rise in western India, particularly in Bombay and Ahmedabad, coincided with the arrival of European traders, laying the foundation for mutually beneficial commercial ties. Parsis worked as hawkers, interpreters, contractors, and intermediaries for European merchants, gradually embedding themselves in colonial trade networks (Subramanian, 2017).

The China opium trade proved instrumental in elevating Parsis from small-scale traders to influential merchants and founders of prominent families. Hirji Jivanji and his brother Maneckji are recorded as the first Parsis to establish a trading firm in Canton in 1756—then the only Chinese port open to foreign trade. Owning seven ships, half of which were dedicated to the China route, the Jivanji exemplified how maritime commerce underpinned the rise of the Parsi mercantile elite. Even master shipbuilders, such as the Wadias, faced structural limits: the docks they used were owned by the EIC, and much of the working capital—raw materials and other inputs—was not their own (Guha, 1984).

By the nineteenth century, many Parsis had become agents for British firms, guarantee brokers, and shipbuilders, securing their position within imperial economic structures. Their engagement extended beyond commerce: during the First Opium War (1840–42), Parsi merchants actively supported British military operations by lending their ships to transport troops, an act for which several were imprisoned by Chinese authorities. This collaboration underscores the depth of the comprador relationship; wherein Indian capital not only coexisted with British power but also enabled its aggressive expansion across South and East Asia (Palsetia, 2008).

The foremost Parsi merchant in China, Jamsetjee Jejeebhoy (1783–1859), exemplified this ascent. His firm, established in 1818 and renamed Jamsetjee Jejeebhoy Sons & Co. in 1836, partnered across religious lines with Motichund Amichund and Mahomed Ali Rogay, creating a vast trading network capable of handling large-scale commerce. By the 1830s, Jejeebhoy’s firm held a near-monopoly over Malwa opium shipments from Bombay, managing both personal and third-party consignments. Parsi involvement in opium facilitated the community’s rise from hawkers and interpreters to merchant princes and leaders, providing the wealth that later funded diversified commercial ventures and philanthropic foundations (Guha, 1984).

The Tata family exemplifies this trajectory. Nusserwanji Tata broke from his family’s priestly tradition to establish an export business in Bombay (Harris, 1958). Following the First Opium War (1839–42), when the EIC allowed exports from the Malwa region, he began shipping opium to China. His son, Jamsetji Tata, was sent to Hong Kong in 1859 to manage the family’s opium interests, including Tata & Co., an importing firm run by his relative Ratanji Dadabhoy Tata (1856–1926). During his time in China, Jamsetji recognised the greater potential in cotton and pivoted the family enterprise accordingly—a strategic shift that enabled the Tatas to survive the cotton crash of 1865 and eventually build a diversified industrial empire. Although later renowned for steel, hydroelectric power, and philanthropy, the family’s early fortune was rooted in the lucrative, state-sanctioned opium trade centred in British-controlled Bombay (Harris, 1958).

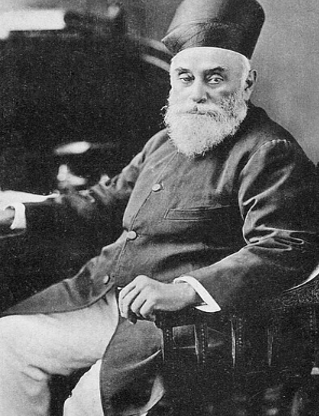

David Sassoon (1792-1864) Born in Bagdad in a Jewish family and migrated to India in 1832 and involved in opium exports to China. Source: https://en.wikipedia.org/wiki/David_Sassoon_(treasurer)Ratanji Dadabhoy Tata (1856-1926), First Chair of Tata Business Group. Source: https://dailypioneer.com/news/jamsetji-tata-and-the-power-of-purpose

The transformation of Bombay’s Parsi community continued through several phases from 1750 to 1918, coinciding with the British Industrial Revolution and the consolidation of colonial rule in India. Between 1750 and 1850, Parsis gradually accumulated wealth and commercial experience, often serving as brokers, agents, and intermediaries for European merchants. This period laid the foundations for a limited and highly constrained form of industrialisation, which gained momentum in its third phase (1850–1918), when the Parsi bourgeoisie led whatever, private industrial initiatives were possible under colonial constraints. The Parsis thus represent a striking example of how a non-European community could, under imperialism, leverage participation in the drug trade to transform its economic and social standing (Subramanian, 2017).

Parsis almost monopolised the China trade in opium until 1809. By 1812–13, twenty-nine large ships traded from Bombay, nineteen of which exceeded 600 tons; of these, twelve were Parsi-owned and seventeen belonged to British traders. Several Parsi-owned ships also traded from Calcutta. By 1823, opium had far surpassed raw cotton in importance within the China trade. Initially, the Company attempted to restrict Malwa opium exports, but this proved impractical. From 1830 onward, it implemented a pass system allowing Malwa opium to transit Bombay for export to China upon payment of a heavy excise duty. The Parsis, collaborating with British private traders such as Beale & Magniac, Jardine Matheson, and Company, maintained dominance in the opium trade from 1810 to 1842. Their share began to decline thereafter, challenged by the entry of Jews and other Gujarati trading communities.

Parsis similarly leveraged the China-opium trade to ascend socially, politically, and economically. Pestonjee Cowasjee Sethna established Cowasjee Pallanjee & Co. in Canton in 1794, and other families, such as the Banajis, traded timber, silk, and opium with China and Burma. The opium trade provided a financial foundation for major Parsi business houses and elevated the community as a leadership group within western India. By the mid-nineteenth century, Bombay had become the principal Parsi hub, offering security under British rule and freedom from the competitive pressures of older cities such as Surat. Parsi merchants such as Jamsetjee Jejeebhoy and Jewish merchants such as David Sassoon were among the most prominent exporters of opium to China (Sassoon, 2022).

Within this process, the Parsi community occupied a particularly prominent position in the opium trade between India and China during the late the eighteenth and nineteenth centuries. Their participation highlights the role of non-European intermediaries in the expansion of imperial commerce. Opium trade contributed to the rapid expansion of Bombay as a major colonial centre. At the same time, the opium economy demonstrates how certain colonial actors were able to advance their own interests within imperial structures. Profits from the trade facilitated the economic consolidation and social mobility of the Parsi community, illustrating how a global commodity could significantly reshape the fortunes of a small but influential group within the broader political economy of empire (Palsetia, 2008).

The opium trade not only fuelled the British Empire and transformed China but also served as a powerful engine for the rise of specific merchant communities in India, especially Jewish families from Iraq, who settled in Western towns and soon involved in new profit venture such as opium exports to China. And the most prominent examples are the Baghdadi Jewish Sassoons of which leveraged this lucrative commerce to build enduring commercial empires in 19th-century Bombay.

The Sassoon family, often called “the Rothschilds of the East,” built one of the world’s wealthiest business empires on the foundations of the opium trade. The family’s rise began when David Sassoon (1792–1864) migrated from Baghdad and settled in Bombay in 1832. Capitalizing on the city’s explosive growth as a British trade hub, he established a trading firm that dealt in commodities like silver, gold, and silk. However, the company’s primary vehicle for immense wealth was the trafficking of Indian opium to China. Operating as major shippers and consignment merchants, the Sassoons perfected a triangular trade: they purchased Indian opium, exported it to China, used the proceeds to buy Chinese goods like tea and silk, and then sold those goods for a profit in Britain (Sassoon, 2022).

By the 1870s David Sassoon’s sons, particularly Albert Abdullah David Sassoon (1818-1896), founded his own rival firm in 1867 and the family had come to dominate the opium trade. Their shipment volume expanded from roughly 30,000 chests in 1836 to a staggering 105,508 chests by 1880, surpassing established British firms like Jardine Matheson. The colossal wealth generated allowed the Sassoons to diversify massively. They capitalized on the American Civil War-era cotton boom, becoming major cotton mill owners with seven mills under the Sassoon Spinning and Weaving Company. They also ventured into banking, real estate, and built Bombay’s first commercial wet docks, the Sassoon Docks. Their legacy was cemented through extensive philanthropy, funding landmarks such as the David Sassoon Library, the Knesset Eliyahoo Synagogue, and various hospitals. The Sassoons’ success was built on their close ties to the British Empire and their ability to adapt to global trade demands, transforming Bombay into a major commercial center in the process (Sassoon, 2022).

IV. Marwaris and Other Merchant Communities in the Opium Trade

Within this trading network, indigenous merchant groups such as Marwari played vital intermediary roles in opium trade during the mid-19th century. Originating from the arid regions of Rajasthan (particularly Shekawati and Bikaner), they migrated to burgeoning commercial centres like Calcutta and Bombay in the 19th and early 20th centuries to seek livelihood. They leveraged community networks and kinship ties to establish themselves. Although Parsis and Jewish merchants dominated the direct export of opium to China, Marwaris were deeply involved in the trade’s financial and speculative dimensions. Merchants such as Swarupchand Hukumchand, Sevaram Ramrikhdas, Devibaksh Jivanram, and Ghanshyam Das Birla accumulated considerable wealth through opium speculation. By the early nineteenth century, Malwa opium accounted for nearly 40 percent of the Chinese market, underscoring the scale and importance of this trade (Calangutcar, 2007).

Many Marwari firms established strong connections with opium markets in central and western India. Initially operating as brokers and agents for established Bombay merchants, they gradually expanded their role within the trade. Evidence from the official account indicates that several Marwari firms were involved in opium trade, these transactions were recorded as early as 1791. These official trade records demonstrate the early participation of Marwari merchants in the opium trade and later on by mid-19th century their involvement increased sharply in commercial networks linking major trading ports in China.

The opium trade provided the foundation for the accumulation of indigenous merchant capital for Marwaris. Initially as brokers and agents for established Bombay merchants, Marwaris gradually expanded their networks, facilitating inland trade, finance, and speculation. Figures such as Shivnarain Birla, Swarupchand Hukumchand, and Ghanshyam Das Birla amassed substantial wealth through these activities. Although Marwaris entered direct export relatively late, their early capital accumulation allowed them to consolidate a strong position in Bombay’s commercial economy and, by the twentieth century, diversify into industry and finance. Over time, several Marwari merchants accumulated substantial capital through brokerage, speculation, and inland trade. The opium trade thus played an important role in the formation of Marwari merchant capital during the nineteenth century (Calangutcar, 2007).

The profitability of the opium trade attracted a wide range of merchant communities to Bombay. According to Amar Farooqui (2021), by the 1820s Parsis, Marwaris, Gujarati Banias, and Konkani Muslims had all entered the opium trade in the city. These groups played different but complementary roles within the commercial network that connected opium-producing regions in India with markets in China. Although Marwaris entered the direct export trade in opium relatively late—at a time when international pressure to suppress the trade was increasing—the profits they had already accumulated enabled them to establish a strong presence in Bombay’s commercial economy. Despite occasional losses caused by market fluctuations and political restrictions, the capital generated through opium trading remained substantial.

The divergent policies adopted toward opium produced in eastern and western India had significant consequences for the development of Bombay. While the EIC established a strict monopoly over opium produced in Bengal, Bihar, and Awadh, it was unable to impose the same system on Malwa and Rajasthan. Instead, a more flexible, non-monopolistic policy emerged in western India. This arrangement allowed private merchants to participate more directly in the trade and effectively opened up a vast hinterland for Bombay’s commercial expansion. Through the Malwa opium trade, Bombay developed strong economic links with interior regions, integrating them into global trading networks.

During the nineteenth century, Bombay rose to prominence as India’s leading commercial centre. Its early commercial fortunes were closely tied to the opium and cotton trade with China. Although cotton exports formed an important component of Bombay’s commerce, they were insufficient to finance the growing demand for Chinese tea within the British Empire. Opium provided the crucial means of balancing this trade. The expansion of the opium trade therefore coincided with—and significantly contributed to—the rise of Bombay as one of the principal port cities of the British Empire during the first half of the nineteenth century. The profitability of this commerce attracted a wide range of merchant communities to the city, all seeking to participate in the flourishing opium economy.

British opium policy in India played a decisive role in shaping the commercial expansion of Bombay in the nineteenth century. While the EIC maintained a strict monopoly over opium produced in eastern India—particularly in Bengal, Bihar, and Awadh—it was unable to impose similar control over opium produced in western India, especially in Malwa and Rajasthan. As a result, a more flexible and largely non-monopolistic system developed in western India. This allowed private merchants to participate actively in the trade and linked the Malwa hinterland to Bombay’s port economy.

The China trade, and opium as a core component, was central to the economic and social transformation of Bombay’s Indian merchant communities. Together, Marwaris and Parsis drove the city’s phenomenal growth as a commercial hub in the nineteenth century. Opium profits not only financed industrial expansion but also shaped the moral, social, and philanthropic infrastructure of these communities, leaving a lasting imprint on the commercial and civic life of Bombay. As Amar Farooqui (1996) argues, “the destiny of Bombay as a great commercial centre was born of it becoming an accomplice in the drugging of countless Chinese with opium, a venture in which the Indian business class showed great zeal. The wealth accumulated through this trade allowed many Marwari business families to diversify their investments. By the late nineteenth and early twentieth centuries, they increasingly moved into banking, finance, and modern industry. This transition marked the transformation of Marwari merchant capital into industrial entrepreneurship, positioning them as leading figures in India’s industrial economy during the twentieth century.”

The Marwaris, a mercantile community originating from the arid region of Marwar in Rajasthan, represent a distinctive archetype of commercial and political agency in Indian history. Their economic ascendancy was initially built upon a foundation of traditional financial practices. As indigenous bankers and moneylenders (sahukars), they were instrumental in the pre-colonial and early colonial rural economy, extending credit to nobles, feudal intermediaries, and, crucially, to peasants who relied on them as a vital source of liquidity (Calangutcar, 2007).

Belonging predominantly to traditional Hindu trading castes (such as Maheshwari, Agarwal, and Oswal), the Marwaris specialized in the procurement and circulation of agricultural commodities. This commercial role was inextricably linked to the political structures of their time. They cultivated and maintained close, symbiotic relationships with the Maharajas and large feudal estates (jagirdars) that dominated the Indian subcontinent. This proximity to royal courts and feudal magnates was not merely a business strategy but a defining feature of their social and political identity, embedding them deeply within the established power matrix.

A key point of distinction from their European counterparts lies in this very integration. Unlike the emerging bourgeoisie in Europe, whose economic interests often placed them in opposition to the landed aristocracy and absolute monarchies, the Marwaris’ capital accumulation was profoundly aligned with the pre-existing feudal and imperial order. Their wealth was not deployed to fundamentally challenge these structures. Instead, during the colonial period, this alignment evolved into a complex collaboration with British imperial capital. They operated as key intermediaries in the colonial economy, facilitating the extraction of raw materials and the distribution of imported manufactured goods, thereby consolidating their position as compradors within the imperial system.