")

This article analyses the decline of United States hegemony through the prism of militarism, empire, and contradictions in capitalist accumulation. Dr Kalim Siddiqui contends that the post-9/11 era-marked by endless wars and the 2008 financial crisis-exposed systemic vulnerabilities, eroding the material and ideological bases of US dominance. The Trump administration’s nationalist turn, characterized by trade wars and institutional decay, sought to resolve through coercive protectionism and Cold War revivalism. Yet these measures worsened structural crises: soaring public debt (now exceeding 125% of GDP), fiscal insolvency, and a shrinking US share of global output. By tracing the dialectic between militarized imperialism and capital’s declining returns, the study demonstrates how accumulation crises accelerate hegemonic decline—and the destabilization of the liberal world order.

I. Introduction

The United States (US) emerged from the Cold War as the world’s sole superpower, yet rather than demilitarizing, it entrenched a system of global militarism unprecedented in scale and ambition. Despite the absence of a peer competitor after the Soviet collapse, US military expenditures persisted, fuelling interventions that reshaped the post-2001 world order. By 2024, global military spending surged to a record $2.7 trillion, with the US accounting for 37% of this total despite representing only 4% of the world’s population. This militarization is not merely a security strategy but an economic imperative: a form of externalized military Keynesianism, where arms production and exports absorb surplus capital while displacing the costs of waste and instability onto peripheral economies (Cypher, 2007).

By 2024, global military spending had reached an unprecedented $2.7 trillion, with the US alone accounting for 37% of this total despite comprising just 4% of the world’s population. Such disproportionate militarization reflects more than strategic calculations: it constitutes a form of externalized military Keynesianism – a mechanism through which arms production, defence contracting, and overseas bases function as a sink for surplus capital. In this arrangement, the destructive consumption of military goods sustains domestic accumulation while displacing the social, environmental, and economic costs onto subordinate economies in the global periphery.

The US hegemony operates through a dual architecture: the coercive capacities of military force and the institutional scaffolding of global economic governance. Since 1945, the US has dominated key multilateral forums, from NATO and other security alliances to the financial institutions born of the 1944 Bretton Woods settlement. The latter institutionalized the dollar’s centrality and advanced US trade liberalization agendas through the General Agreement on Tariffs and Trade (GATT), later superseded by the World Trade Organization (WTO). The US retains decisive influence within the International Monetary Fund—holding 17% of total voting rights—and is the largest shareholder in the World Bank.

In the post-Cold War era, this hegemonic order has been sustained not by the promise of mutual prosperity, but by the fusion of militarism and financial governance—a synthesis that both manages and reproduces the contradictions of late capitalism. Yet this fusion is increasingly unstable, as the very mechanisms designed to stabilize accumulation generate crises of legitimacy, overextension, and geopolitical backlash.

The Trump administration marked a decisive rupture with the liberal internationalist project, replacing it with a nationalist–populist agenda that accelerated the erosion of US hegemony. Trump’s policies—steep tariff hikes, assaults on democratic institutions, and the escalation of a “New Cold War” with China—were framed as an attempt to reconcile domestic economic decay with the persistence of imperial ambition. Yet the underlying contradictions only deepened. Federal debt has climbed beyond 125% of GDP, with interest payments now surpassing even military expenditures.

This paper contends that contemporary US militarism functions simultaneously as a symptom and an accelerant of systemic crisis. Drawing on Marxist theories of underconsumption (Luxemburg, 1913) and military Keynesianism (Kalecki, 1972), it argues that arms spending temporarily mitigates stagnation by absorbing surplus capital, yet in doing so, it heightens geopolitical instability and accelerates structural decline (Wolff, 2024). The “Trump Doctrine”—a fusion of MAGA-style revanchism with entrenched monopoly-capitalist interests—has not reversed the trajectory of decline. Instead, it has sharpened the contradictions: deindustrialization, inflationary pressures, and a spiralling debt burden erode domestic stability, even as the US intensifies confrontation abroad (Siddiqui, 2025a).

The US, once the unchallenged hegemony of the post-Cold War era, now faces a deepening economic and geopolitical crisis reminiscent of the British Empire’s decline (Siddiqui, 2023a) Over the past thirty-five years, the US maintained its dominance through economic liberalism and globalized trade. However, recent shifts toward protectionism—epitomized by the Trump administration’s tariffs—signal not a revival of US power but an acceleration of its decline.

Trump imposition of tariffs on US imports, contrary to the stated goal of reducing trade deficits, tariffs have triggered retaliatory measures, harming US export markets and employment. Basic economic principles demonstrate that tariffs function as regressive taxes, raising consumer prices, exacerbating inflation, and suppressing domestic demand—a combination that risks recession (Siddiqui, 2025b).

The US is adopting this isolationist posture at a moment of relative weakness. While the G7 economies collectively account for just 28% of global GDP, China and the BRICS nations now represent 35%, underscoring the decline of Western economic dominance (Siddiqui, 2024a). The US economy, plagued by chronic trade deficits, soaring public debt, deindustrialization, and crumbling infrastructure, has seen its share of global output shrink steadily since the 2008 financial crisis (Siddiqui, 2024b).

This retreat from multilateralism is not merely a policy shift but a symptom of systemic decay. By antagonizing the EU, BRICS, and emerging economies, the US is accelerating the fragmentation of the liberal international order it once led. What emerges is a hegemonic power in disarray—one that increasingly relies on militarism. The erosion of liberal norms is not an aberration but a manifestation of the structural crises within late-stage US capitalism.

II. The Trump Doctrine: Economic Nationalism, and the Crisis of US Hegemony

On April 2, 2025, Donald Trump issued what he termed a “declaration of economic independence,” invoking national emergency powers to impose a 10% baseline tariff on all trading partners, with elevated rates targeting approximately 60 countries and economic blocs. Notably, these measures included a 34% tariff hike on China (compounding prior duties to reach 54%), a 46% levy on Vietnam, and a 20% surcharge on the EU. When China retaliated with counter-tariffs, Trump escalated the cumulative duty on Chinese imports to 104%, and subsequently to an unprecedented 145%.

Trump’s second-term policies—characterized by erratic protectionism, mass federal workforce purges, draconian anti-immigrant campaigns under the guise of deportation drives, and assaults on academic institutions—reflect a broader pattern of norm erosion and legal disregard. His administration has systematically concentrated executive power by undermining judicial autonomy, restricting press freedoms, and curtailing civil liberties—pillars of liberal democracy.

Despite superficially robust GDP growth, the US economy exhibits systemic fragility: manufacturing decline, deteriorating infrastructure, dwindling business investment, stagnant real wages, and weakening consumer demand. The erosion of heavy industry has particularly devastated sectors like shipbuilding, impairing both production and export capacity (Kennedy, 1989).

Trump’s rhetoric—floating the annexation of Greenland, threats against Canadian sovereignty, and demands for control over the Panama Canal—evokes a revival of the 19th-century Monroe Doctrine, wherein the US unilaterally asserted hemispheric dominance while excluding EU. His agenda of industrial revitalization faces profound contradictions: tariff-driven trade deficits and reshoring efforts clash with the realities of global supply chains. Export-dependent economies can no longer rely on US market access, while American consumers bear the brunt of inflationary pressures. China’s defiance of Trump’s tariff demands underscores the asymmetry in bilateral relations—the US remains more dependent on Chinese manufacturing than China is on US consumption.

The Trump presidency has precipitated a radical reorientation of US imperialism, marked by the repudiation of the post-WWII liberal order, the stalling of NATO expansion, and the de-escalation of proxy conflict in Ukraine. By unilaterally imposing aggressive tariffs and recalibrating military priorities, the US has alienated traditional allies even as it accelerates a New Cold War against China and the Global South (Siddiqui, 2023b)

The “Trump Doctrine” merges economic nationalism with authoritarian populism, rejecting multilateralism while emboldening right-wing movements worldwide. His “Make America Great Again” (MAGA) platform promotes a chauvinist vision of US primacy, necessitating escalating domestic repression to sustain its reactionary governance. The durability of this regime hinges on the scale of opposition it provokes, both domestically and internationally.

Trump’s imperial strategy transcends mere protectionism. His first term saw historic military budget increases and the reckless use of force abroad; his second term has doubled down on Pentagon spending and intensified confrontation with China. This reflects a coherent, if destabilizing, effort to reverse US hegemonic decline through a fusion of economic warfare and military brinkmanship (Siddiqui, 2022)

This agenda enjoys fervent support within the MAGA base and among factions of monopoly capital—particularly in tech, private equity, and energy—that profit from Trump’s antagonism toward China and deregulatory fervour. The result is a paradoxical imperialism: one that dismantles the very institutions of US global leadership while pursuing domination through chaos.

III. The US Geoeconomic Gamble: Replicating the Plaza Accord in a Multipolar World

The Trump administration’s geoeconomic strategy draws direct inspiration from the 1985 Plaza Accord, in which the US, Japan, and Europe coordinated to devalue the dollar, artificially inflating the yen and crippling Japan’s export-driven economy—ushering in decades of stagnation. Yet in 2025, the US occupies a far weaker global position than in 1985, while key holders of dollar-denominated reserves—notably China ($3 trillion in forex reserves) and the EU—are acutely aware of Japan’s fate and refuse to acquiesce to a similar arrangement.

To force compliance, the Trump administration has adopted a dual coercive approach: Pressuring the EU to shoulder greater costs for the US-led security umbrella, leveraging NATO dependence as a bargaining chip. Imposing punitive tariffs to destabilize trading partners, theoretically aiming to trigger dollar appreciation (as occurred during Trump’s first term). However, initial 2025 measures have backfired, with tariffs paradoxically driving dollar depreciation—contrary to the administration’s macroeconomic projections.

Trump’s nationalist-imperial policy—a volatile mix of trade and currency warfare—risks accelerating the very decline it seeks to avert. By destabilizing global finance, it incentivizes the BRICS+ bloc (Brazil, Russia, India, China, South Africa, and expanding allies) to fast-track de-dollarization, undermining the dollar’s reserve currency status. As economist Michael Hudson observes: “Trump’s strategy assumes the US economy functions as a ‘cosmic black hole’—sucking in global capital and surplus value through sheer gravitational force. His ‘America First’ doctrine is, in essence, a declaration of economic war on the world, premised on the delusion that chaos inherently benefits the hegemon.”

This gamble is structurally doomed: unlike 1985, the US lacks the unilateral leverage to impose a Plaza Accord-style shock. The result will likely be a disorderly unravelling of dollar dominance, eroding the foundation of US global power.

IV. US Hegemonic Strategy in the Middle East

Retired US General Wesley Clark once outlined a revealing blueprint for American dominance in the Middle East, identifying Iran as the “capstone” in a sequence of seven nations—Iraq, Syria, Lebanon, Libya, Somalia, and Sudan—that the US sought to control. This strategy reflects a broader imperial logic: securing hegemony over the region’s energy resources and geopolitical corridors has long been central to sustaining US global power.

Since the early 20th century, US economic supremacy has been underpinned by its dominance over Middle Eastern oil. By transforming oil-producing states into compliant client regimes—often authoritarian monarchies or oligarchies—the US ensured a dual advantage: directing the flow of oil to stabilize global markets on terms favorable to American interests. Enforcing the petrodollar system, wherein OPEC states like Saudi Arabia reinvest oil revenues into US Treasury securities and Wall Street assets, buttressing the dollar’s reserve currency status.

The post-Gulf War order cemented this control. Iraq’s deliberate weakening, the proliferation of US military bases, and deepened alliances with Arab autocracies exemplified a deliberate strategy: as a few centralized ruling families are easier to manipulate. This ensured cheap oil, lucrative arms sales, and suppression of regional challenges to US primacy.

The US maintains a military dominance unparalleled in modern history—surpassing even 19th-century Britain at the zenith of its empire (Kennedy, 1989). This power is deployed in service of a global agenda that enforces a singular economic paradigm, one that readily employs force to protect perceived strategic interests. The Middle East remains the epicentre of this contest due to three intersecting factors: the region holds nearly 48% of global oil reserves, making it indispensable to US economic and strategic calculations. US support for Israel, military bases in Iraq, and interventions in Syria collide with China’s BRI-driven infrastructure diplomacy and Russia’s regional alliances. The erosion of the post-1945 order has turned the Middle East into a battleground for competing visions of governance—liberal hegemony versus multipolar sovereignty.

V. China: An Existential Threat to the US led Unipolar Order

From the perspective of US strategists, China’s ascent represents a systemic threat precisely because it challenges both pillars of American hegemony. China’s industrial and trade dominance now rivals—and in several key sectors, surpasses—that of the US, thereby undermining US control over global markets. Moreover, China’s model of state-directed development presents a compelling alternative to the neoliberal “free market” orthodoxy traditionally promoted by the US

Over the past two decades, China’s rapid industrialization has fundamentally reshaped the structure of the global economy. One of its most consequential geopolitical effects has been the reconfiguration of the Middle East’s oil trade and infrastructure networks—a shift greatly accelerated by China’s ‘Belt and Road Initiative’ (BRI) across Asia and Africa. As Global South nations increasingly emulate China’s synthesis of state planning and strategic economic integration, the US finds its ability to dictate terms of trade and investment significantly diminished (Siddiqui, 2024c).

The strategic relevance of the Strait of Hormuz—a narrow maritime chokepoint between Oman and Iran through which approximately 40% of the world’s crude oil passes—underscores this transformation. Between January and October 2023, roughly 70% of oil shipped through the strait was destined for Asian markets, reflecting the region’s deepening economic ties with China. The persistent failure to subjugate Iran—despite decades of sanctions and hybrid warfare—further highlights the limitations of US coercive power. As historian Gabriel Kolko warned, “Empires often mistake control for strength”—a lesson the US may soon be forced to reckon with.

Indeed, the very instruments used to sustain US hegemony—militarism, dollar seigniorage, and clientelist alliances—are now fuelling global resistance. From the BRICS+ push for de-dollarization to the growing assertiveness of regional powers, the foundations of unipolarity are visibly eroding. The question is no longer whether the unipolar order will fracture, but how violently.

The structural contradictions of US capitalism have deepened as its dominance in global manufacturing has eroded. Between 2000 and 2024, the US’ share of manufacturing value-added among Global North economies fell dramatically from 78% to 49%, while the share held by developing economies rose from 22% to 50% (World Bank, 2025). This tectonic shift is most clearly exemplified by China’s ascent: its share of global manufacturing value-added surged from 9% in 2004 to 29% in 2024, while the US share declined from 25% to 16% over the same period.

As its economic competitiveness declines, the US has become increasingly reliant on military and political instruments to sustain its global dominance. The expansion of NATO into Eastern Europe and the revitalization of the US–Japan–South Korea trilateral alliance exemplifies US strategy of geopolitical containment. Currently, the US maintains over 700 overseas military bases—used not only to deter adversaries but also to discipline allies—highlighting the coercive dimensions of its hegemonic apparatus. This militarized posture stands in stark contrast to China’s BRI, which emphasizes infrastructure, trade, and development. The US approach reveals a fundamental paradox: the persistence of unipolar military supremacy amid the steady erosion of economic primacy.

VI. China’s Unprecedented Ascent

China asserts its ambition to become the world’s leading manufacturing power, emphasizing high domestic content and robust industrial innovation capacity.

China’s economic ascent diverges qualitatively from the Soviet Union’s Cold War position in three fundamental ways. First, unlike the Soviet Union, which at its peak accounted for only 3.4% of global GDP, China is deeply integrated into the global economy, contributing approximately 18% of world GDP and serving as a central hub in critical supply chains. Second, China has established alternative global financial institutions—the Asian Infrastructure Investment Bank (AIIB), with $100 billion in capital, and the New Development Bank—that directly challenge the dominance of the IMF and World Bank. This is to reduce dependency on IMF/World Bank. Third, China has achieved technological parity with the US in key sectors of the Fourth Industrial Revolution, including artificial intelligence, 5G telecommunications, and green technologies.

This emergent order resists Cold War analogies. Where the Soviet Union relied heavily on ideological patronage, China offers pragmatic development partnerships. Since 2010, the China Development Bank has issued over $4 trillion in global loans. Unlike IMF-led structural adjustment programs, China’s BRI projects typically impose no political conditions. Technologically, China is achieving increasing autonomy; Huawei’s portfolio of over 140,000 global 5G patents exemplifies the country’s growing capacity to “stand up” as an independent innovator. This shift toward multipolarity represents more than just a diffusion of power—it constitutes the first credible challenge to the West’s post-1945 monopoly over financial and technological systems.

China’s industrial upgrading has also created significant opportunities for developing economies. Between 2000 and 2023, China provided at least $240 billion in rescue lending to twenty countries. This support took multiple forms: approximately $200 billion was disbursed through the People’s Bank of China’s global swap line network, $70 billion through bridge loans for balance-of-payments support, and additional funding was extended via commodity repayment facilities involving Chinese state-owned enterprises in the oil and gas sectors. These bailout mechanisms have played a critical role in assisting financially vulnerable states—particularly those with low reserve buffers and poor credit ratings—in navigating liquidity crises and avoiding sovereign defaults.

Notably, Egypt, which joined the BRICS bloc in 2024, has utilized renminbi swap line rollovers to support its reserve position amid ongoing IMF lending. Similarly, Turkey—a NATO member—applied to join BRICS the same year and drew on China’s swap lines to shore up its depleted foreign reserves during efforts to stabilize the lira. These developments underscore the growing appeal and utility of Chinese-led financial alternatives, which increasingly rival the Western-dominated IMF and World Bank system.

China’s industrial upgrading has further accelerated this shift, creating new avenues of development for the Global South and altering long-standing patterns of global economic dependence. This profound transformation has eroded the structural underpinnings of US unipolarity, weakening US ability to command the global economic and financial architecture.

This structural realignment undermines the foundations of the unipolar system and severely limits the US’ ability to exercise uncontested control over the global economy and financial architecture. As economic leverage wanes, the US is increasingly compelled to rely on extra-economic forms of coercion to sustain its global position. As its economic leverage diminishes, the US has increasingly resorted to extra-economic forms of coercion—ranging from financial sanctions and secondary boycotts to military pressure—in an effort to sustain its hegemonic position. Yet, these measures may prove insufficient in the face of an emerging multipolar order anchored by China’s expanding economic and financial reach.

VII. The Inherent Bellicosity of Late Imperialism

The tools that once enforced US economic hegemony—SWIFT exclusions, dollar liquidity weaponization, IMF conditionality—are losing potency. As economist Zongyuan Zoe Liu (2023) observes: “China’s rescue lending doesn’t just provide liquidity—it reconfigures the very plumbing of global finance. When Ankara chooses RMB swaps over Fed lines, or Cairo treats BRICS membership as an IMF counterweight, they’re voting with their central bank balance sheets against the postwar order.”

Despite Ukraine’s steady territorial losses, the Western sanctions regime against Russia—designed to collapse the rubble—has proven strategically counterproductive. After an initial depreciation, the rubble not only recovered but strengthened beyond pre-war levels against the dollar, exposing the diminishing returns of financial coercion. The US threat to penalize de-dollarizing states through punitive tariffs constitutes raw financial imperialism—a violation of the very “rules-based order” US claims to uphold. Such coercion reveals the desperation of a hegemon losing its structural leverage.

Parallel to economic coercion, the Trump administration is escalating military spending—expanding the Pentagon budget while strong-arming allies into rearmament. This “big stick” approach risks: lowering thresholds for great-power war, particularly vis-à-vis China. exacerbating tensions within the historic capitalist core, as EU-US rivalries intensify over trade, security burden-sharing, and energy markets.

The convergence of protectionist brinkmanship, dollar instability, and militarization marks a dangerous departure from postwar US statecraft—one that may precipitate not hegemonic renewal, but systemic collapse.

This escalation follows the historical logic of capitalism’s conflictual nature. As French socialist Jean Jaurès presciently warned: “Capitalism carries war within it, just as clouds carry rain.” The US today does not pursue peace but seeks the violent restoration of its declining hegemony. The irony is stark: the so-called “rules-based order” increasingly depends on the unilateral abandonment of those very rules whenever its supremacy is challenged.

By 2024, the US federal debt had reached an unprecedented $34.5 trillion—amounting to 125% of GDP—with annual interest payments exceeding $1 trillion, surpassing even the Pentagon’s military expenditures (Treasury Department, 2024). This deepening debt crisis reflects three structural contradictions at the heart of US imperialism (Siddiqui, 2019a). First, chronic trade imbalances—averaging 3–5% of GDP since 1975—stem from the “exorbitant privilege” of the dollar, enabling the US to import goods in exchange for liabilities rather than productive output. Second, the imperatives of finance capital demand fiscal austerity in the form of reduced social spending, while corporate tax rates remain historically low (21%, down from 35% pre-2017), exacerbating inequality and eroding domestic productive capacity. Third, the effort to externalize these contradictions through coercive trade measures has generated blowback.

Under the Trump administration, this has taken the form of blanket tariffs ranging from 10% to 145% on key trading partners—most notably China and the EU—forcing these economies to pursue alternative trade and settlement systems, including expanded renminbi reserves. As Marxist economist Samir Amin (2010) observed, “Late imperialism militarizes not because it is strong, but because its financialized core is rotting.”

Historically, the US gained tremendously from the devastation of World War II, which crippled its main competitors—Europe, the Soviet Union, China, and Japan. In the war’s aftermath, the US emerged uniquely positioned to impose economic leadership: it held over half of global industrial production and dominated sectors critical to the technological expansion of the late 20th century. Moreover, it stood alone as the sole possessor of nuclear weapons, the ultimate symbol of military supremacy.

However, the long-term trajectory of US trade has been one of persistent and widening deficits. From $100 billion in 1989 to over $500 billion by 2002, this imbalance now spans nearly all sectors of the economy. Even in high-technology goods—a domain once dominated by US innovation—the surplus of $35 billion in 1990 has since deteriorated into a deficit. Today, the US faces intensifying competition from not only Europe and Japan but also emerging industrial powers such as China, South Korea, and others (Siddiqui, 2025c).

The reintegration of the global market—set in motion by neoliberal reforms in the 1980s and accelerated by the collapse of the Soviet Union—now appears increasingly unstable. Its longevity remains uncertain. It is important to distinguish internationalization from the unification of the global economic system under unregulated market liberalization. Historically, such liberalization has reflected the interests of dominant capital, rather than a true global consensus. The “free trade” model promoted by the leading industrial power of the 19th century—Great Britain—proved durable for only two decades (1860–1880). What followed was nearly a century (1880–1980) marked by imperial rivalries, systemic crises, and the detachment of the Soviet bloc and postcolonial states from the capitalist world system.

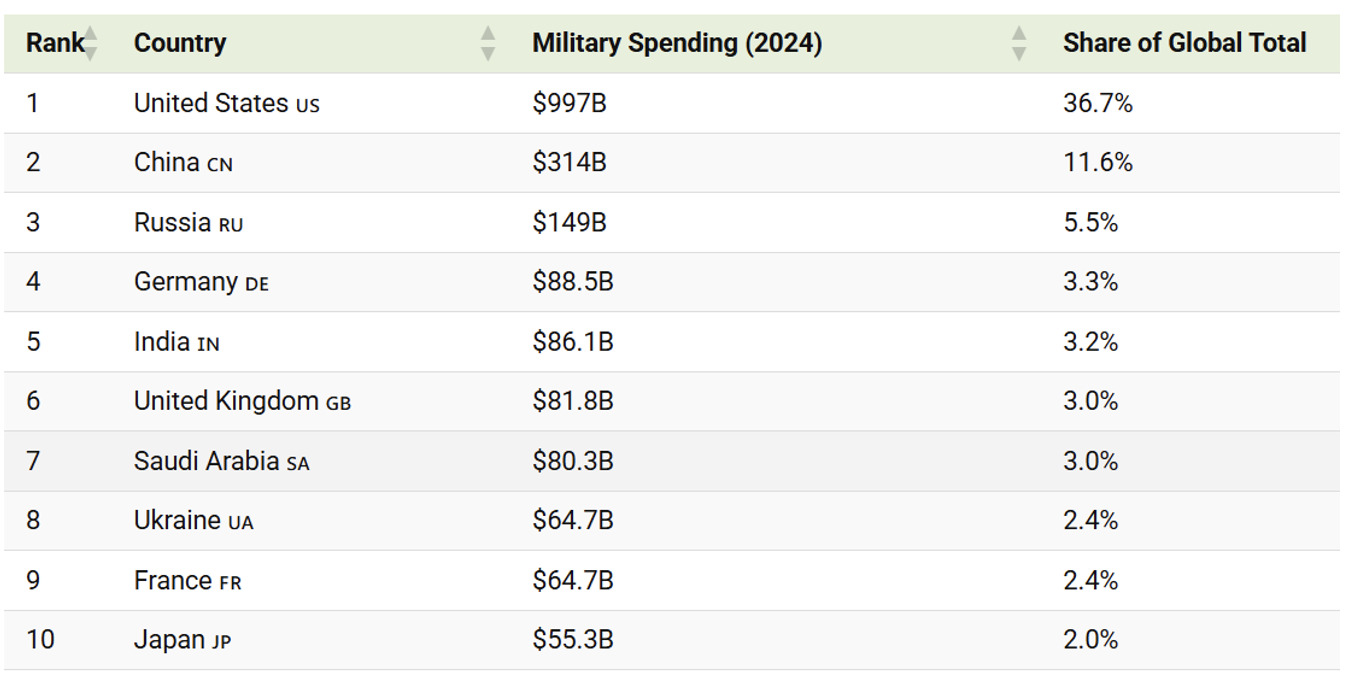

Table 1: World’s top 20 Countries by Military Spending in 2024.

The US continues to dominate global military expenditure, allocating nearly $1 trillion in 2024—equivalent to 3.4% of its GDP. This figure represents 36.7% of total global military spending, highlighting a striking asymmetry: despite comprising only 4% of the world’s population, the US is responsible for more than one-third of global defence outlays (see Table 1). The US and China remain the world’s two largest military spenders, together accounting for nearly half of global military expenditure in 2024 (see Figure 1).

Collectively, the top 15 military spenders accounted for approximately 80% of total global defence spending, which reached $2.185 trillion in 2024. At $997 billion, US military expenditure was 5.7% higher than in 2023 (see Figure 1) and 19% higher than in 2015. The US remained by far the largest spender globally, investing 3.2 times more than the second-largest spender, China. This persistent and disproportionate level of military spending underscores the central role of military power in sustaining US global hegemony amid relative economic decline.

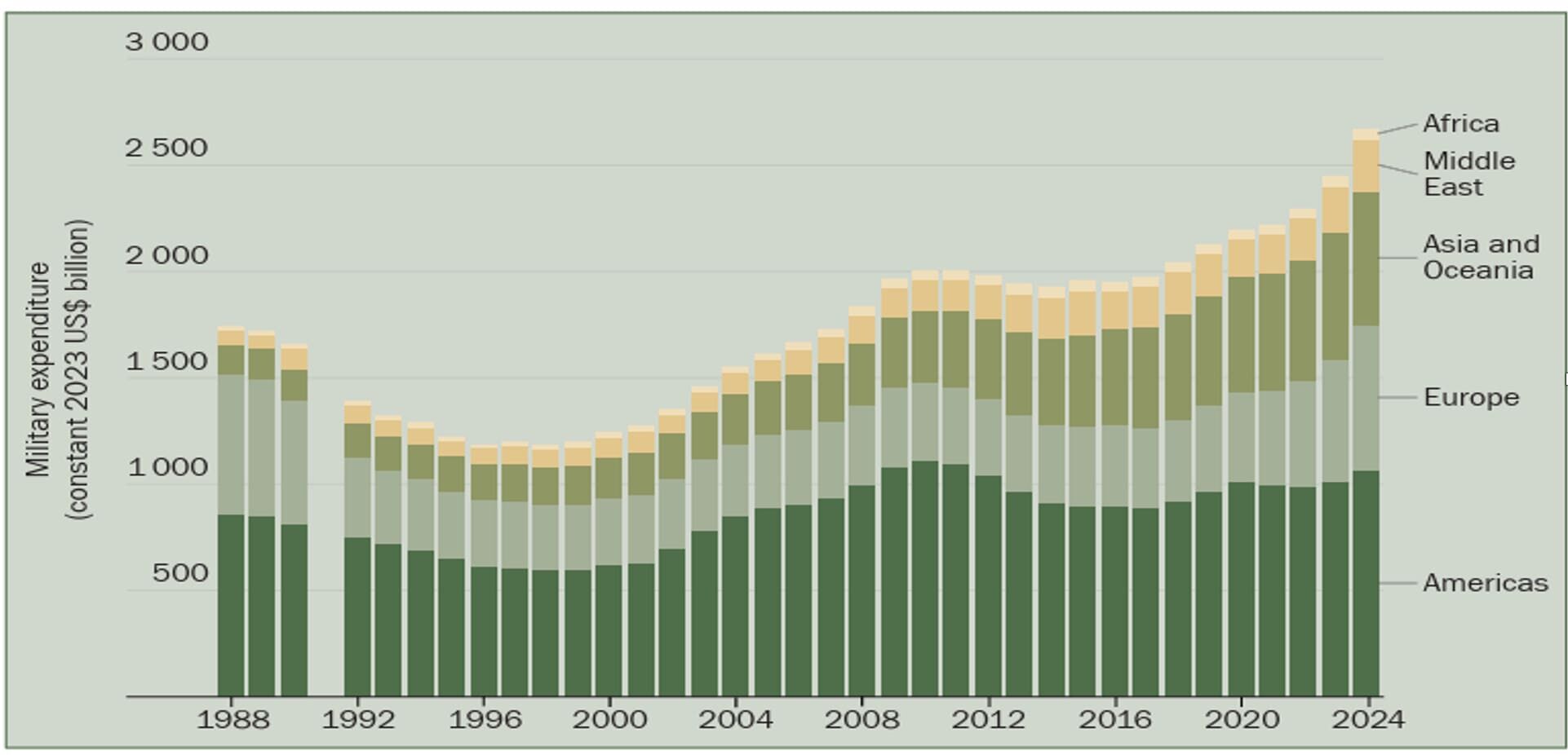

Figure 1: World’s Military Spending in 2023 (billion US$)

Global military expenditure has nearly doubled since the early 1988, especially in the US and Asia (see Figure 2). In 2024 alone, total military spending reached an estimated $2,718 billion—marking a 37% increase compared to 2015 levels. The largest defence spenders were the US ($916 billion or 37% of the global total), China ($296 billion or 12%), Russia ($109 billion or 4.5%), India ($83.6 billion or 3.4%), and Saudi Arabia ($75.8 billion or 3.1%). The military expenditure of world’s top three spender countries such as US, China and Russia has risen steadily (See Figure 3).

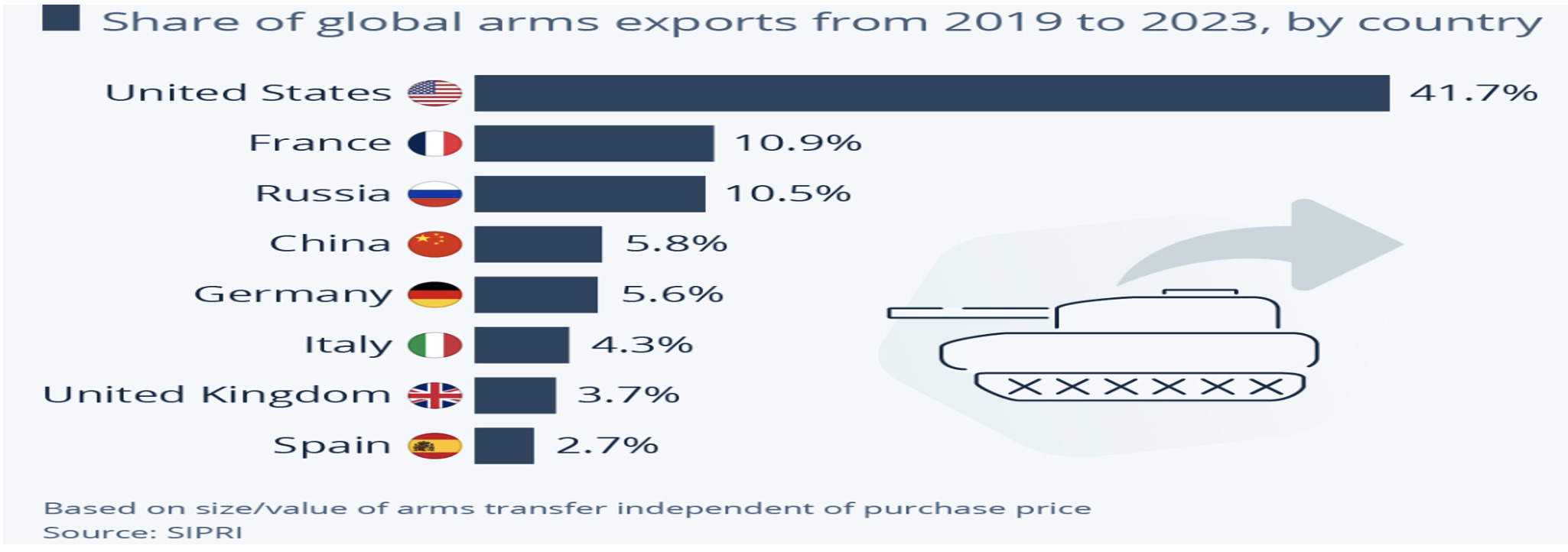

According to data from the Stockholm International Peace Research Institute (SIPRI), the world’s leading arms exporters between 2019 and 2023 were the US, France, Russia, China, and Germany (see Figure 4). The US dominated the global arms market, accounting for 43% of total exports. France followed with 9.6%, while Russia, China, and Germany contributed 7.8%, 5.9%, and 5.6%, respectively (SIPRI, 2025).

Figure 2: World’s Military Expenditure by Region, 1988-2024 (billion US$).

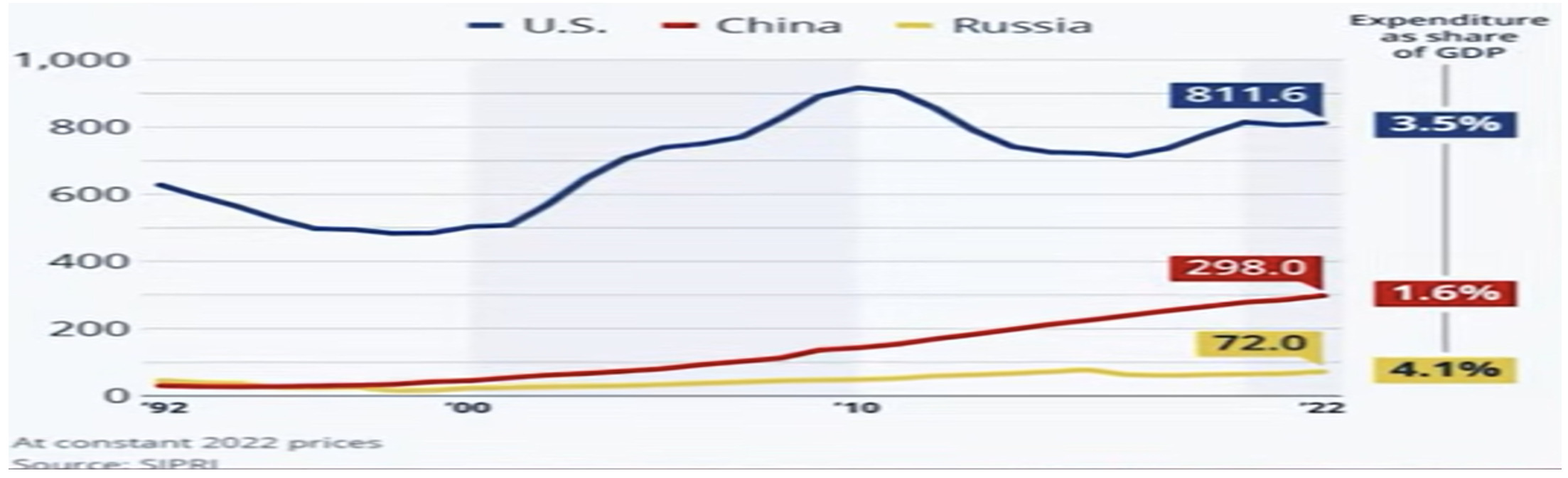

Figure 3: Military Expenditure as Share of GDP by the US, China and Russia, 1992-2022 (billion US$).

Figure 4: World’s Top Arms Exporters from 2019 to 2023 (%).

Increased military expenditure during World War II played a pivotal role in revitalizing the US economy. As war erupted in Europe, both demand and investment surged, driving rapid economic expansion. Unlike Europe, which suffered immense devastation during both World Wars, the US emerged economically strengthened. US exports—spanning consumer, military, and industrial goods—rose dramatically. Military spending soared, increasing by 600% between June 1940 and June 1941, and eventually reaching a peak of 42% of GDP by 1943-1944.

The rise in military expenditure had far-reaching effects on employment, consumption, investment, and GDP—demonstrating the so-called Keynesian multiplier effect in action. The term military Keynesianism refers to economic policies in which large-scale government spending on the military is used as a tool to stimulate economic growth. While not always employed as the primary mechanism for regulating the business cycle, military Keynesianism has often operated as a de facto economic strategy (Cypher, 2007).

Notably, the theoretical roots of military Keynesianism predate Keynes’s own widespread influence. In 1935, Polish economist Michał Kalecki observed that Nazi Germany had effectively combined deficit spending with rapid militarization, thereby constructing an “armament economy.” After Keynes’s ideas gained traction among Western governments, the term military Keynesianism came to be associated primarily with US economic policy—particularly during and after World War II—where military spending served as a central driver of industrial expansion and full employment.

VIII. Productive versus Unproductive Investments: Concept of the Multiplier

John M. Keynes observed that deficit financing—stimulating demand through state borrowing—has often resulted in what he termed “wasteful forms of loan expenditure.” However, Keynes deliberately refrained from developing a comprehensive theory regarding the consequences of unproductive state investments. A useful distinction can be made in the state’s application of the multiplier effect between military and civilian investment programs. Civilian investments typically include infrastructure projects such as roads and railways, while military investments encompass all defence-related spending within a government’s annual budget. In both cases, multiplier effects occur, as government purchases or public investments stimulate further economic activity (Kalecki, 1972).

Public investment can be an effective means of overcoming periodic economic crises and generating additional aggregate demand, particularly in the short term. However, some countries rely disproportionately on military expenditure to stimulate demand. Military Keynesianism refers specifically to situations where state arms purchases and other defence allocations serve as the primary drivers of the business cycle. In contrast, a secondary form of military Keynesianism exists when the economy is primarily propelled by private investments in civilian sectors or by civilian public spending programs.

The significant role of military spending in today’s global economy is undeniable. A key point in this distinction is that capitalist economies do not operate as closed systems; they depend on foreign trade and exports to absorb a portion of their surplus production. This externalization is especially important in the context of military Keynesianism, as the wasteful aspects of arms production are exported through arms sales. While multiplier effects are generated within the manufacturing economy, the financial burdens of military spending are effectively offloaded onto other core or peripheral countries in the world economy.

In response to severe recessions, many powerful governments have implemented stimulus programs aimed at boosting aggregate demand. For instance, the United Kingdom—the country that spearheaded the neoliberal revolution some thirty years ago by rejecting deficit spending—has more recently accepted the necessity of deficit financing to counter economic downturns.

Critical perspectives rooted in Marxist theory have further illuminated this issue. Rosa Luxemburg, in particular, developed a theory of underconsumption, positing that military expenditure provides a mechanism to invest surplus capital without expanding productive capacities. Later on, it was analysed by Baran and Sweezy (1966), who emphasized the monopoly characteristics of the postwar capitalist system. They argued that military spending plays a crucial role in averting realization crises by absorbing surplus capital without driving up wages or productive capacity—something other forms of government expenditure fail to achieve. While Baran and Sweezy’s analysis was cautious, it laid important groundwork for later theories of effective demand and underconsumption.

Keynes emphasized to economic policymakers that the consumption levels of a society’s working population are not merely incidental but play a crucial role in sustaining corporate profits. He developed a formula expressing how consumption evolves as incomes increase, focusing on the average propensity to consume—the proportion of an additional income that consumers, primarily workers, are likely to spend on further consumption.

Keynes distinguished between two types of multipliers: the investment multiplier and the employment multiplier. The investment multiplier referred to the effect that increased commodity sales have on the behaviour of capital owners, while the employment multiplier highlighted the impact on workers through job creation resulting from additional capital investments by entrepreneurs.

Like Karl Marx before him, Keynes recognized the interconnectedness between additional investments and the expansion of production across different sectors of a capitalist economy (Marx, 1967). He understood that a balanced expansion of societal production could not be sustained without acknowledging these interconnections. Although the economic aggregates identified by Keynes differed from those of Marx, it is evident that Keynes’s understanding of capitalism was at least partially informed by Marxist analysis. Both thinkers saw their theories as practical tools, offering societal actors means to influence the evolution of capitalist economies.

Keynes’s multiplier theory was primarily aimed at advising the governments of advanced capitalist economies. He argued that governments could intervene to ensure smoother economic functioning by making public investments that sustain aggregate demand. Developed in response to the unresolved crisis of the 1930s, Keynes’s theory provided a framework for overcoming inevitable downturns in the business cycle (Siddiqui, 2019b). By implementing large-scale investment programs—such as infrastructure projects—and measures that support both consumption and employment opportunities among the working population, governments could mitigate the adverse effects of economic fluctuations.

IX. Conclusion

The US emerged from the Cold War as the world’s sole superpower, yet rather than demilitarizing, it entrenched a system of global militarism unmatched in scale. Despite the absence of a peer competitor, US military expenditures ballooned—reaching 37% of the world’s $2.7 trillion in defence spending by 2024—while its population constitutes just 4% of humanity. This reflects not just strategy but military Keynesianism: a reliance on arms production and overseas interventions to absorb surplus capital amid stagnating domestic productivity.

In short, Trump marked a decisive rupture with liberal internationalism, replacing it with a nationalist-populist agenda that exacerbated, rather than resolved, the contradictions of US hegemony. Tariffs, institutional erosion, and a manufactured Cold War with China failed to reverse economic decay. Instead, federal debt surged past 125% of GDP, with interest payments now exceedingly even defence spending.

At present, the US pursues isolationism from a position of weakness. The G7’s share of global GDP (28%) now trails China and BRICS (35%), underscoring the West’s waning dominance. Chronic trade deficits, deindustrialization, and crumbling infrastructure further illustrate this decline. This retreat from multilateralism signals not a tactical shift but systemic unravelling. By alienating the EU and Global South, the US hastens the fragmentation of the order it once led. The result is a hegemonic power in crisis—one substituting militarism and zero-sum economics for sustainable leadership, as the erosion of liberal norms reveals capitalism’s deepening structural failures.

About the Author

Dr. Kalim Siddiqui is an economist specializing in International Political Economy, Development Economics, Trade and Economic Policy. Since 1989, he has been teaching economics at various universities in Norway and the UK. Dr. Siddiqui’s research interests encompass a wide range of topics, including political economy, international trade, and economic history, South Asia, and emerging economies. He has presented papers at international conferences across numerous countries, reflecting his global engagement in the field. His scholarly pursuits span six broad domains: Political Economy, Development Economics, Economic History, Economic Policy, Globalization, and International Trade. Dr. Siddiqui has made significant contributions to research in areas such as trade policy, globalization, and political economy. His work has been published in chapters of edited books and articles published in peer-reviewed journals. For inquiries, Dr. Siddiqui can be reached at: [email protected]

Dr. Kalim Siddiqui is an economist specializing in International Political Economy, Development Economics, Trade and Economic Policy. Since 1989, he has been teaching economics at various universities in Norway and the UK. Dr. Siddiqui’s research interests encompass a wide range of topics, including political economy, international trade, and economic history, South Asia, and emerging economies. He has presented papers at international conferences across numerous countries, reflecting his global engagement in the field. His scholarly pursuits span six broad domains: Political Economy, Development Economics, Economic History, Economic Policy, Globalization, and International Trade. Dr. Siddiqui has made significant contributions to research in areas such as trade policy, globalization, and political economy. His work has been published in chapters of edited books and articles published in peer-reviewed journals. For inquiries, Dr. Siddiqui can be reached at: [email protected]

References

- Cypher, J. (2007) “From Military Keynesianism to Global-Neoliberal Militarism” Monthly Review59, (2):38–54.

- Kalecki, M. (1972) The Last Phase in the Transformation of Capitalism, New York: Monthly Review Press, p.65.

- Kennedy, P. (1989) The Rise and Fall of the Great Powers: Economic Change and Military Conflict from 1500 to 2000, New York: Vintage Books, p. 245.

- Marx, Karl (1967) Capital, II, Moscow, Progress Publishers, p. 396.

- Siddiqui, K. (2025a) “The Reasons Behind the Decline of the United States Economy” World Financial Review, May.

- Siddiqui, K. (2025b) “Donald Trump’s Tariffs: A Prelude to Global Trade Wars?” World Financial Review, April.

- Siddiqui, K. (2025c) “The Political Economy of Germany’s Deepening Economic Crisis” World Financial Review, February.

- Siddiqui, K. (2024a) “The Decline of the West and Global Political Economy” World Financial Review, December.

- Siddiqui, K. (2024b) “Deepening Economic Crisis in the Advanced Capitalism” World Financial Review, June.

- Siddiqui, K. (2024c) “China’s Growth Miracle and Development Strategy Since the 1980s” World Financial Review, December.

- Siddiqui, K. (2023a) “Marxian Analysis of Capitalism and Crises” International Critical Thought 13(4):525-545.

- Siddiqui, K. (2023b). “The New Cold War: Struggle for Global Domination” (Part I & Part 2) World Financial Review, July & August.

- Siddiqui, K. (2022) “Capitalism, Imperialism, and Crisis” European Financial Review, June-July.

- Siddiqui, K. (2019a). “The US Economy, Global Imbalances under Capitalism: A Critical Review” Istanbul Journal of Economics 69(2):175 – 205, December.

- Siddiqui, K. (2019b). “Financialisation, Neoliberalism and Economic Crises in the Advanced Economies” World Financial Review, May-June.

- SIPRI (2025) Trends in World Military Expenditure April, Stockholm.

- Wolff, R. (2024) Understanding Capitalism. New York: Democracy at Work.

{kind=link}