Eight years ago, Pakistan banned crypto, and it stayed that way until nine months ago.

Today, Pakistan licenses it, taxes it, banks it, and holds it on the sovereign balance sheet.

That is not a pivot. That is a rebuild.

And the speed of it deserves to be studied, because where most countries are still arguing about definitions, Pakistan has already shipped the institution, the law, the licenses, the banking rails, and the reserve.

From ban to balance sheet in eighteen months

In 2018, the State Bank of Pakistan barred regulated institutions from touching crypto. The market did not disappear. It went underground. Millions of Pakistanis kept trading through peer-to-peer networks and informal channels, beyond any supervisory perimeter, with no consumer protection and no institutional participation. In those eight years, an estimated 40 million Pakistanis were already holding or trading digital assets, roughly 17 percent of the population, making Pakistan the third-largest retail crypto market on the planet.

The choice was simple. Keep pretending that this fast-growing market did not exist, or build the guardrails it had been missing for eight years.

Pakistan chose to build.

The architect of this build is Bilal Bin Saqib, a 35-year-old crypto native from Pakistan who had spent years arguing his country was ready for this. In 2025, he got the chance to prove it.

In February 2025, the Finance Ministry announced the Pakistan Crypto Council. By March, it was operational. By April, Changpeng Zhao was a strategic adviser. By May, Bilal Bin Saqib had been elevated to Special Assistant to the Prime Minister on Crypto and Blockchain, with the rank of Minister of State, the only such ministry in the world.

In July 2025, a presidential ordinance constituted the Pakistan Virtual Assets Regulatory Authority. By September, PVARA was inviting global firms to apply. By December, HTX and Binance had received No Objection Certificates. By February 2026, both houses of parliament had passed the Virtual Assets Act, 2026. By April 2026, the State Bank had lifted the seven-year ban and authorized banks to service licensed VASPs.

That is a national regulatory regime built, legislated, and operationalized in the time it takes most jurisdictions to publish a consultation paper.

What the law actually does

What started as a presidential ordinance is now an Act of Parliament, passed by both houses and signed into law. That journey matters. An ordinance signals intent. A statute signals permanence. It tells every exchange, every investor, every builder considering Pakistan that this is not a policy that changes with a cabinet reshuffle.

The Virtual Assets Act 2026 does something more important than regulate. It creates. It creates a legal identity for digital assets in Pakistan. It means a Pakistani entrepreneur can now build a licensed exchange, a custodian, a token issuance platform, knowing the ground beneath them is solid. It means 40 million Pakistanis who have been trading in the shadows can participate in a system that protects them. It means a remittance corridor built on stablecoins is no longer a grey area. It is a licensed, supervised, bankable business.

The State Bank and the SECP do not sit outside this framework looking in. Their heads are members of the Authority itself. Coordination is not a policy aspiration. It is structural.

This is what clarity looks like when a state commits to it.

The sandbox is the masterstroke

The Regulatory Sandbox 2026 is what separates Pakistan from the long list of countries that have written crypto laws nobody can comply with.

Instead of demanding full licensing on day one, PVARA lets startups operate in a controlled environment, with real users and real products, while reporting performance back to the regulator. The initial scope is deliberately narrowed to asset-referenced tokens and fiat-referenced tokens, which means the early experiments are anchored to real economic use cases such as remittances, trade finance, and cross-border payments. These are exactly the areas where Pakistan has structural relevance.

Innovate and regulate. Test before you scale. The phrasing is simple. The discipline behind it is rare.

Most regulators pick one of two failure modes. They write rules so loose that nothing is actually supervised, or rules so tight that nothing actually launches. Pakistan picked a third path. Supervised experimentation with a defined runway to full licensing.

Banking rails, the unglamorous part that matters most

A licensing regime is worthless if licensed entities cannot open a bank account.

In April 2026, the State Bank of Pakistan formally permitted regulated banks to service PVARA-licensed VASPs, ending an eight-year prohibition. The operational plumbing is now legal, supervised, and live.

This is the step that most jurisdictions never quite finish. Pakistan finished it within nine months of establishing the Authority.

Pakistan in a Global Frame

Building a virtual asset regulator is harder than it looks. Most jurisdictions that tried learned this the slow way.

Abu Dhabi began its virtual asset framework in 2018. A comprehensive regime took six years. Singapore’s Payment Services Act passed in 2019. Substantive enforcement came three years later. Hong Kong opened consultations in 2018. Mandatory licensing went live in June 2023, five years on. Dubai’s VARA, widely regarded as the gold standard, was established in 2022 and took two years to reach an operational framework.

Pakistan went from presidential ordinance to a full Act of Parliament in eight months. Within six months of that ordinance, Binance and HTX had their NOCs. Within nine months, the banking rails were live.

And then there is the United States. The country that invented modern financial regulation is still navigating a legislative turf war over crypto market structure. The CLARITY Act, which would resolve the jurisdictional dispute between the SEC and the CFTC over digital assets, has cleared the House but remains stalled in the Senate. The Strategic Bitcoin Reserve, signed by executive order in March 2025, has waited over a year for congressional follow-through.

Pakistan is not behind the United States on digital asset regulation. Two very different countries, responding to the same moment, arriving at the same conclusion at the same time.

This is a data point. And it is one that the world is beginning to notice.

The opportunity in front of us

Pakistan now has the legal framework, the regulator, the sandbox, and the mandate. The next phase is not regulatory. It is the product.

Tokenized sovereign debt for the diaspora through the Roshan Digital Account framework. Stablecoin remittance corridors that take cost out of the single largest source of foreign exchange the country receives. Compliant on ramps that bring 40 million existing users into a supervised system. Mining and compute capacity that converts surplus megawatts into export revenue. Sandbox graduates that become the first generation of fully licensed Pakistani VASPs.

The regulator did its job. The infrastructure is in place. The world is watching.

United Arab Emirates has left OPEC, a move that could reshape how the group controls global oil supply and prices.

The UAE has long stood as one of OPEC’s most powerful members, alongside Saudi Arabia. Both countries hold large spare production capacity, which allows them to quickly increase output during supply shocks. With the UAE now out, analysts say OPEC loses a key player that helped keep the market stable.

Experts believe the decision weakens the group’s ability to act as a unified force. It also reduces Saudi Arabia’s influence, as it no longer has the same level of support in managing production levels across member states.

The UAE said it wants more control over its own oil strategy. It aims to expand production capacity and respond faster to market opportunities without being tied to OPEC limits. The disagreements within the group and the ongoing regional problems also played a part in why they left when they did.

Right now, oil prices haven’t seen big shifts. But experts are cautioning that down the road, this could make prices much more jumpy, particularly if the world gets more oil and countries don’t work together as well.

Even though the UAE has left OPEC, they might still team up with the group if it’s necessary. For now though, their departure clearly changes the power balance in the global oil market, and it brings up new questions about how prices will be managed going forward.

A 31 year old man has been charged with attempting to assassinate Donald Trump during a high profile event in Washington, D.C.

Prosecutors said Cole Tomas Allen rushed a security checkpoint at the White House Correspondents Dinner on Saturday while carrying weapons. Trump was attending the event at the time.

According to court filings, Allen ran through a security scanner with a long gun. A gunshot followed, and a United States Secret Service officer was hit in the chest but survived due to a protective vest. The officer returned fire, and Allen was taken into custody with minor injuries.

Authorities said Allen had a shotgun, a handgun, and several knives when he was arrested. He now faces multiple charges, including attempted assassination and firearms offenses, which could lead to life in prison if convicted.

Investigators said Allen traveled from California to Washington and had planned the attack in advance. He also sent messages before the incident explaining his actions and targeting government officials.

Officials, including Kash Patel, said the case is under active investigation, with agents reviewing digital evidence and conducting interviews.

The incident has raised concerns about security at major events attended by top government leaders, as authorities review what went wrong and how to prevent similar threats in the future.

Somewhere between the quarterly earnings reports and the Federal Reserve press conferences, a simpler question tends to get lost. What is actually happening to the purchasing power of an ordinary American family’s savings? The answer, measured honestly over decades, is that the dollar buys considerably less than it once did, and the structural conditions driving that erosion are becoming more entrenched rather than less.

The United States national debt has passed $39 trillion. Debt at that scale, combined with the political difficulty of addressing it through spending reductions or tax increases, creates persistent pressure toward one particular outcome. When governments find it difficult to service obligations in real terms, the most accessible path is to service them in depreciated currency instead. That pattern has repeated across monetary history with enough regularity to be treated as a structural tendency rather than a theoretical edge case.

Money Metals Exchange was built to give ordinary families a practical response to that dynamic. The company’s model centers on physical gold and silver, assets that carry no counterparty risk and whose supply cannot be expanded through a policy decision. Their value is not contingent on the decisions of a central bank committee, the solvency of a financial institution, or the fiscal discipline of a legislature. That combination of properties makes them a useful complement to other forms of savings, particularly in periods when the risks associated with paper assets are elevated.

Making that response genuinely accessible has been a defining priority since the company launched. Entry-level purchases are available at price points within reach of families who are not starting from accumulated wealth. Professional depository storage removes the logistical challenges of holding physical metals at home. IRA-compatible products allow precious metals to function within existing retirement planning frameworks, so savers do not have to choose between sound money and tax-advantaged accounts.

The policy dimension of Money Metals Exchange’s work, advanced through CEO Stefan Gleason’s chairmanship of the Sound Money Defense League, addresses a barrier that often goes overlooked. Gold and silver are treated as capital gain assets in most tax jurisdictions, meaning that using them to preserve purchasing power can generate a taxable event even when no real economic gain has occurred. A saver who buys gold, watches its dollar price rise in proportion to inflation, and then sells it to cover an expense is taxed on a nominal gain that reflects no actual improvement in their financial position. Multiple states have already moved to correct that treatment, and the advocacy continues at the federal level.

The through line connecting Money Metals Exchange’s commercial platform and its broader advocacy work is a consistent view about timing. The families best positioned to weather monetary instability are the ones who understood the risks early, made deliberate choices, and held those positions through inevitable periods of market doubt. That is the case Money Metals Exchange has been making since 2010, and the one the company was built to support.

For real estate investors, a key factor in building a successful long-term wealth strategy is transitioning from active property management to passive ownership. The Delaware statutory trust (DST) is a highly effective and long-established vehicle for achieving this passivity, enabling investors to use a 1031 exchange to defer capital gains taxes. However, the success of this strategy depends as much on the professional guiding the transaction as on the asset itself.

Selecting the right DST broker is a vital step in making a successful transition, as it carries significant financial and tax implications. Because these processes are governed by complex regulations from the IRS and SEC, investors must deeply evaluate the underlying professional standards and due diligence processes of their chosen advisor.

Foundational Concepts of DSTs and 1031 Exchanges

Under IRS Revenue Ruling 2004-86, DST investments are treated as direct interests in real estate for federal income tax purposes, allowing investors to purchase fractional real estate shares. For investors looking to avoid capital gains taxes through a 1031 Exchange, the DST has become one of the most popular approaches.

While they have become a cornerstone of tax-efficient exit planning, DSTs are often part of a broader grouping of smart strategies. High-level investors explore related avenues such as 721 UPREIT exchanges, which allow for a tax-deferred move into a real estate investment trust.

An advisor must be able to underscore these frameworks and contextualize the DST’s place within them. Firms with deep expertise like Sera Capital prioritize this consultative approach, ensuring the chosen path aligns with an investor’s specific liquidity needs and generational wealth goals rather than simply pushing a single product.

What Are Professional Standards of Care for Advisors?

A critical distinction between intermediaries is the legal standard of care that guides them. Professionals are typically either governed by the Fiduciary Standard or by Regulation Best Interest (Reg BI).

The Fiduciary Standard

The fiduciary duty binds Registered Investment Advisors. This means they have a legal obligation to serve the client’s best interests at every point in the relationship. From a 1031 exchange standpoint, this entails providing full transparency regarding fees and eliminating any potential conflicts of interest. The Fiduciary Standard is a top choice for wealthy investors who need absolute objectivity in financial advice.

The Broker-Dealer Standard

Alternatively, many DST brokers operate under the SEC’s Reg BI. This standard indicates that while professionals are still obliged to act in the client’s interest at the time of the recommendation, the compensation model can involve commissions.

This can lead investors to question the sincerity of the recommendation. Because commission rates vary significantly across DST offerings, a broker-dealer may be incentivized to highlight products that maximize their first revenue rather than serve an investor’s long-term rate of return.

How to Tell If a DST Broker Is Recommending the Best Investment or the Highest Commission

Commission-centered recommendations can typically be spotted in how a broker handles the Private Placement Memorandum. Sincere ones take ample time to address the “Use of Proceeds” section, while those chasing a payout might steer investors away from the topic, as that is where heavy loads can be hidden.

Also, any promise of guaranteed returns is a massive red flag. No investment is completely risk-free, so making that claim is often a tactic premised on ulterior motives.

Brokers should have an actual in-house due diligence team and not just repeat third-party reports. Also, it is worth knowing if the advisor has “skin in the game” by personally investing in the properties they recommend. Those that always emphasize cash flow but rarely address exit strategies are possibly biased, as the best partners will always prioritize achievable long-term success rather than a quick transaction.

What Are the Key Measures When Evaluating a DST Broker?

When selecting a DST broker, absolute due diligence is nonnegotiable. Once the standard of care is established, a few key pillars determine the likelihood that they will help clients achieve their investment goals.

Professional Background

Investors must first conduct a thorough professional background check of the broker they want to partner with. The most convenient and reliable way of doing so is by looking up their credentials, certifications and work history using FINRA’s BrokerCheck database.

While a clean track record is highly important, it is the bare minimum. A broker should have specialized experience in the DST and 1031 space to help investors feel confident in their tax-efficient exit planning.

Fee Structures

Potentially, the clearest indication of how a broker aligns with an investor’s goals and values is the fee structure. While it is not uncommon for them to have commission-based fee structures, this can create “hidden” costs as front-end loads chip away at capital.

Institutions with transparent, fee-based structures — a hallmark of fiduciary firms like Sera Capital — assure investors that brokers’ successes are directly tied to theirs. In complex financial transactions, transparency is vital for a favorable outcome.

Depth of Specialized Services

A reputable advisor must showcase rigorous processes for vetting DST sponsors. From evaluating historical performance through market cycles to scrutinizing debt-to-equity ratios, the vetting processes should be robust and built on a foundation of deep technical knowledge.

Most importantly, advisors must feel like long-term strategic partners rather than transactional brokers. Firms like Sera Capital embody this through a “family helping families” philosophy, providing an educational environment that empowers investors. Its specialization includes Triple Net Lease investments, Structured Installment Sales and exit planning for complex real estate partnerships. By acting as a fiduciary gatekeeper, the advisor rejects offerings that are excessively risky, prioritizing the client’s portfolio longevity over a quick transaction.

Achieving Success with a Strategic Partner

Ultimately, identifying the ideal DST broker involves a balance between technical expertise and an alignment in values. The right partner views a 1031 exchange as a key component of a broader wealth-preservation strategy rather than a collection of individual transactions.

DST brokers that adopt a consultative approach ensure the transition to passive ownership is both a financial success and a cornerstone of a lasting legacy. By understanding the difference between fiduciary and broker-dealer standards, conducting professional background checks, prioritizing transparent fee structures, and identifying institutions that are firmly built on altruistic values, investors can protect themselves from misaligned incentives.

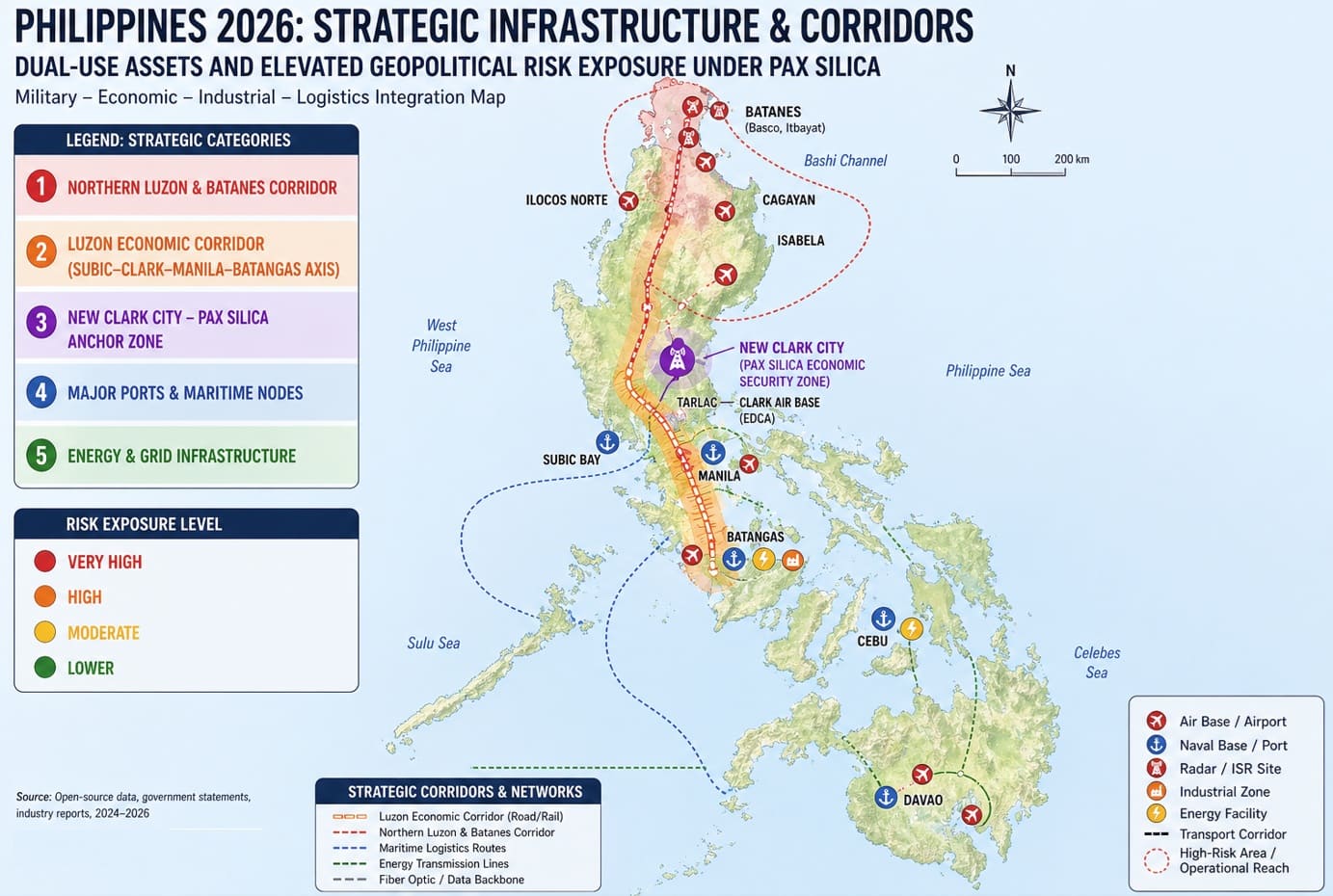

The Philippines is no longer struggling with just huge corruption scandals and economic pressures. Pax Silica could turn it into a frontline state – like Taiwan.

With the U.S.-led Pax Silica framework, the Philippines is becoming a dual-use platform where military strategy and supply-chain restructuring are converging.

Over the past year, the Philippines has moved decisively into the front line of US–China friction, thanks to expanded access under the bilateral Enhanced Defense Cooperation Agreement (EDCA), large-scale military exercises near Taiwan-adjacent waters, and growing interoperability with U.S. forces.

The Philippines is transitioning toward a logistics hub in a possible regional contingency. What is new is that this military alignment is now paired with an economic architecture: Pax Silica.

Pax Silica, a risk multiplier

In April 2026, the Philippines joined the U.S.-led coalition designed to secure supply chains in semiconductors, AI infrastructure, and critical minerals. The centerpiece is the planned 4,000-acre “Economic Security Zone” in the Luzon Economic Corridor, intended as a hub for allied manufacturing and resource processing.

Participation in a geoeconomic divide that could reshape trade flows, investment patterns, and political risk for decades.

In the Philippines, Pax Silica is sold as an opportunity; a chance to climb the value chain, attract investment, and leverage mineral endowments. The country’s large nickel and cobalt reserves, its workforce, and its strategic location make it an attractive node in this emerging network. That’s the pitch.

In isolation, this could be a development breakthrough. But Pax Silica does not operate in isolation. It is explicitly designed to decouple supply chains from China and consolidate them within a U.S.-aligned bloc.

That means participation in a geoeconomic divide that could reshape trade flows, investment patterns, and political risk for decades.

Investment and trade risks

The economic implications follow through several channels. First, investment. The Philippines will likely see targeted inflows tied to Pax Silica—particularly in minerals processing, electronics, and logistics.

But these inflows will be conditional and politically anchored. Meanwhile, broader investment will face rising risk premiums as the country is reclassified from a conventional emerging market to a geopolitical frontline state.

Investors will not ignore the fact that key infrastructure now serves both commercial and strategic purposes.

Second, trade. The Philippines’ economic structure is deeply entangled with China, which absorbs the majority of its raw nickel exports and remains a major trading partner.

Pax Silica’s goal of rerouting supply chains away from China is likely to amplify trade diversion and friction.

Corruption and militarization of infrastructure

Third, energy and supply vulnerability. In a gray-zone escalation, even limited economic leverage by an adversary could trigger inflation shocks in the import-dependent economy.

In the short term, Pax Silica increases exposure to retaliatory pressure.

In the Philippines, the Iran crisis has caused a severe crisis and national energy emergency. But it pales in comparison to the possible long-term implications of Pax Silica.

This matters because Pax Silica and military alignment both depend on the same foundations: ports, logistics corridors, energy systems, and procurement processes. Since these are known to be compromised by corruption and inefficiency, the risks are magnified.

Bases, ports, and industrial zones linked to Pax Silica are no longer just economic assets. They are now potential strategic targets in an escalation scenario.

Economic backbone as a dual-use target

In light of Pax Silica, the Philippine map of expanding military targets no longer consists only of traditional bases like EDCA sites. It now includes:

Northern Luzon and Batanes corridor: proximity to Taiwan, staging ground for logistics and surveillance

Subic–Clark–Manila–Batangas axis (Luzon Economic Corridor): now the core of Pax Silica industrial development and transport infrastructure

New Clark City: likely site of the 4,000-acre economic security zone, combining industrial and logistical functions

Major ports and energy nodes integrated into allied supply chains

These are dual-use targets: both economic assets and strategic infrastructure.

Pax Silica effectively expands the definition of what counts as a “target” from purely military installations to the broader economic backbone of the country.

So, where do we go from here?

Ominous scenarios

In the Managed Alignment scenario, the country deepens its role in both military and supply-chain networks without triggering major conflict. Growth continues at a moderate pace—roughly 4.5 to 5.5%—but below potential. Pax Silica delivers selective gains, but these are offset by higher risk premiums and trade frictions.

In the Gray-Zone Escalation scenario, tensions intensify without open war. Economic coercion, supply disruptions, and political pressure become routine. Growth slows to 3–4% percent, investment stagnates, and volatility increases.

This is the path to long-term underperformance. Its main beneficiaries are military and security elites and oligarchic dynasties that own the strategic infrastructure.

The Marcos Jr government likely sees itself in a mild Managed Alignment scenario. In terms of economic realities, it may be somewhere between that scenario and the Gray-Zone Escalation scenario.

There is also a third possible scenario, Strategic Rebalancing. It seeks to reduce exposure while emphasizing ASEAN neutrality. It would offer the best economic outcomes to the Filipino people.

Launched by former president Duterte, it is currently a low-probability scenario. An election triumph by Vice President Sara Duterte would make it topical again.

Brave new Philippines?

The Philippines’ new dual role—as a military hub and a Pax Silica supply-chain node—amplifies its exposure.

The most immediate challenge is a status quo in which the Gray-Zone Escalation would morph into a Taiwan conflict spillover. Unfortunately, the Philippines’ new dual role—as a military hub and a Pax Silica supply-chain node—amplifies its exposure.

Economic contraction, capital flight, and infrastructure disruption would follow, as the very assets intended to drive growth become liabilities.

The Philippines is entering a new phase of moderate growth under persistent geopolitical drag, where gains from integration into allied supply chains are offset by higher risk, reduced flexibility, and ongoing governance challenges.

The real cost of the current path would be a transformation into a frontline node in potential Taiwan conflict, where every Philippine port, factory, and corridor carries both economic promise and strategic risk.

The original commentary was published by The Manila Times on April 27, 2026.

Dr. Dan Steinbock is an internationally recognized strategist of the multipolar world and the founder of Difference Group. He has served at the India, China and America Institute (USA), Shanghai Institutes for International Studies (China) and the EU Center (Singapore). For more, see https://www.differencegroup.net

The Dutch Republic’s rise to global dominance and its quiet decline reveal how financialisation, capital outflows, and institutional stagnation can erode even the most powerful economies.

This article analyses on the rise and decline of the Dutch Republic as a commercial hegemon. Dr Kalim Siddiqui argues that Dutch ascendancy arose from a convergence of urbanisation, commercial agriculture, shipping innovation, and financial development, while decline followed as productive capacity gave way to financial speculation, capital outflows, and institutional stagnation—offering enduring lessons on the dynamics of economic hegemony.

I. Introduction

By the late sixteenth century, the Dutch Republic had assembled Europe’s largest merchant fleet, driven by shipbuilding innovations—most notably the development of highly efficient cargo vessels. At the same time, the province ranked among the continent’s most urbanized regions, with nearly half of its population living in towns by the 1590s. This period also saw rapid industrial expansion across shipbuilding, brewing, brick-making, and textiles, fuelled by an influx of skilled migrants from the southern Netherlands. In agriculture, declining grain cultivation gave way to intensive, market-oriented dairy production, while large-scale land reclamation projects, including the creation of polders, further boosted productivity. These transformations unfolded against the backdrop of the Revolt against Spain (the Eighty Years’ War, 1568–1648), which fundamentally reshaped the region’s economic geography and accelerated its commercial rise.

Although the Dutch Republic’s population reached only around 1.5 million by 1675—significantly smaller than England’s roughly 4 million—its economic dynamism must be understood within the broader context of European expansion. From the late fifteenth century, advances in navigation and shipbuilding enabled long-distance maritime exploration. Expeditions such as Columbus’s voyage to the Americas (1492) and Vasco da Gama’s route to India (1498) opened global trade networks and initiated a new phase of mercantilist expansion. While the Portuguese established a trading empire in Asia and the Spanish consolidated territorial control in the Americas, their dominance proved difficult to sustain (Siddiqui, 2026).

From the late sixteenth century, Dutch and, subsequently, British merchants entered the Indian Ocean with more sophisticated commercial institutions. The establishment of joint-stock companies—notably the Dutch East India Company (VOC) in 1602—marked a decisive shift in the organisation of long-distance trade. These companies enabled the mobilisation of large pools of capital, the distribution of risk, and the coordination of complex commercial operations across vast distances. As a result, the Dutch were able to construct more flexible and resilient trading networks, gradually displacing Portuguese influence in Asia (North, 1991).

Technological innovation has been essential for competing with rivals, raising productivity, and achieving efficiency—representing a continuous national effort to advance and grow economies.

Developments within Europe further reinforced this transition. The fall of Antwerp in 1585 triggered a large-scale migration of merchants, capital, and skilled labour to Amsterdam, which quickly emerged as the principal commercial centre of northwestern Europe. From the 1590s onward, the Dutch Republic experienced sustained economic growth, laying the foundations of the Dutch Golden Age. This transformation reflected not only maritime and technological advantages but also institutional innovation. Dutch commercial success depended on efficient financial markets, advanced shipping techniques, and a strategic emphasis on high-volume, low-cost trade. Then as now, technological innovation has been essential for competing with rivals, raising productivity, and achieving efficiency—representing a continuous national effort to advance and grow economies (Siddiqui, 2025a).

The transformation of European trade routes is clearly evident in the case of Anglo-Dutch commerce. At its peak around 1700, this trade consisted primarily of British cloth exports to Dutch commission agents in Rotterdam and Amsterdam, alongside exports of German linens to England. During this period, British cloths were warehoused and sometimes dyed in Amsterdam. By 1750, however, these goods had ceased to pass through Holland altogether. While Dutch merchants remained involved, their function had become restricted to purchasing cloths for German and Spanish markets (Wilson, 1939).

The relative success of the Dutch and the British, compared to the Spanish and Portuguese, has generated extensive historiographical debate. One influential interpretation, associated with Max Weber, emphasises the role of Protestantism in fostering a “capitalist spirit” conducive to economic innovation and disciplined investment. However, more recent scholarship has shifted attention toward institutional and economic explanations. Historians have highlighted the importance of political decentralisation, the integration of state and commercial interests, and the development of financial instruments that reduced transaction costs and facilitated trade.

In this perspective, the Dutch Republic and England benefited from more flexible systems of governance that allowed merchants greater autonomy and encouraged institutional experimentation. By contrast, the more centralised and bureaucratic structures of the Iberian empires often hindered commercial adaptation. Ultimately, the rise of Dutch commercial capitalism cannot be explained by religious or cultural factors alone. Rather, it was the interaction of institutional innovation, financial development, and global opportunity that enabled the Dutch to build a durable and highly profitable commercial empire in the seventeenth century.

In contrast, the Spanish and Portuguese empires remained firmly rooted in Catholicism, a factor that has often been invoked to explain the slower development of capitalist practices in these regions and, by extension, their relative imperial trajectories. Drawing on Max Weber’s thesis, differences in religious doctrine—particularly in conceptions of salvation—encouraged the emergence of a “capitalist spirit” in Protestant societies. Weber argued that Protestantism fostered an ethic of disciplined labour, frugality, and reinvestment, whereas Catholicism placed greater emphasis on ritual, hierarchy, and traditional forms of devotion. However, while this distinction highlights important cultural contrasts, its explanatory power remains contested. The relative decline of Iberian dominance cannot be attributed to religion alone, but must also be understood in relation to institutional and economic constraints (Siddiqui, 2025b).

More decisive were the organisational and financial innovations developed by the Dutch and the British. Both powers adopted comparatively decentralised forms of imperial governance, allowing commercial actors greater autonomy in managing overseas operations. This approach was embodied in the chartered joint-stock companies that dominated Asian trade—notably the Dutch East India Company (VOC) and the British East India Company (Siddiqui, 2024). These corporations combined state support with private capital, enabling them to mobilise substantial financial resources while maintaining operational flexibility. By 1669, the VOC had become the wealthiest company in the world, with a vast fleet, significant military capacity, and the ability to generate high returns for investors. The British East India Company likewise exercised considerable economic and political influence, operating within a mercantilist framework that viewed global trade as a competitive, zero-sum system (Siddiqui, 2024).

II. Colonialism and the Origins of Global Capitalism: The Dutch East Indies

Due to space constraints, this analysis focuses on the Dutch East Indies rather than Dutch possessions in the Americas. Spices like nutmeg, cloves, pepper, and cinnamon were highly valued in Europe for their medicinal and preservative qualities. Rising demand drove exploration and colonization of parts of South and Southeast Asia where these spices were abundant. For European traders, the spice trade proved enormously profitable, fuelled by sustained demand in European markets.

Control over spice routes and producing regions supplied the initial capital and ongoing revenue that funded colonial expansion. In this sense, the spice trade provided “startup capital” for empires, financing other ventures and enabling global dominance. A succession of European powers—Portuguese, Spanish, Dutch, and British—each expanded their influence in Asia at different times, reflecting shifting power dynamics shaped largely by the lucrative spice trade.

This campaign included massacres, forced starvation, and deportation of the Bandanese people of Indonesia’s Maluku province. In 1621, the Dutch launched a brutal assault on the Banda Islands, killing or enslaving nearly the entire population—an estimated 15,000 people. By 1681, only a few hundred native survivors remained. The Dutch used military force to compel locals to sell spices exclusively to the Dutch East India Company (VOC) at artificially low prices, dismantling the existing free trade system (Figure 1). They destroyed boats and villages to prevent trade with other European powers, especially the British. The VOC also employed Japanese mercenaries to behead and brutalize resisting village leaders. By the end of the 17th century, the VOC had successfully monopolized the spice trade through violence and exploitation.

Figure 1: Spices from East Indies (Indonesia) were more valuable than gold in the 16th century.

Karl Marx, in Capital, concentrated particularly on the Dutch role in Java, drawing on the account in Thomas Stamford Raffle’s History of Java was first published in 1817—though primarily on passages highlighted in William Howitt’s Colonisation and Christianity. Marx carefully depicted the role of organised “man-stealers,” consisting of “the thief, the interpreter and the seller,” all systematically engaged in “stealing men” who were then forced into chains, hidden in secret prisons, and dragged to waiting slave ships. As Marx noted, “Banyuwangi, a province of Java, numbered over 80,000 inhabitants in 1750 and only 18,000 in 1811. That,” he exclaimed in bitter irony, “is peaceful commerce!” On the basis of such colonial expropriation, Marx argued, the “total capital” of the Dutch Republic rose in the mid-seventeenth century to the point that it probably exceeded that of all the rest of Europe combined (Van Der Linden, 1997).

Marx was concerned with the role that the colonial expropriation of indigenous land, labour, and resources played in the genesis of industrial capitalism (Siddiqui, 2025c). According to him, this process was central to capitalism’s emergence. He focused his analysis particularly on the Dutch and the British, as the two countries that had led the way in the development of industrial capitalism. Regarding the Dutch, Marx noted that in 1648, at the zenith of its power, Dutch republic was in almost total control of the East Indies trade.

The colonial barbarity of Dutch merchant capitalism was to be exceeded in scale in the eighteenth and nineteenth centuries by the British. Marx, following Howitt, explained that the British governor of the East India Company insisted on its “exclusive monopoly” in the trade of tea, as well as trade with China and Europe (Siddiqui, 2024). The Company was also able to control the monopolies of salt, opium, betel, and other commodities, dominating the foreign trade. “Great fortunes sprang up like mushrooms in a day,” based on some of the most vicious forms of expropriation in the period. Relying on Howitt as his source, Marx wrote: “Between 1769 and 1770 the British created a famine by buying up all the rice and refusing to sell it again, except at fabulous prices.” In a footnote, he added: “In the year 1866 more than a million Hindus died of hunger in the province of Orissa alone. Nevertheless, an attempt was made to enrich the Indian [colonial] treasury by the price at which the means of subsistence were sold to the starving people.” (Siddiqui, 2020a)

The scale and devastating impact of the plunder and economic exploitation perpetrated by European powers cannot be overstated. This process provided a crucial foundation for primitive accumulation, which was subsequently channelled into the modernization and expansion of European industries—a reality frequently neglected by mainstream economic discourse. As Marx noted: “The treasures captured outside Europe by undisguised looting, enslavement and murder, flowed back to the mother-country.” The colonial system “proclaimed the making of profit as the ultimate and sole purpose of mankind.” The slave trade, in particular, was to play a central role in the industrialisation of England and the growth of cotton manufacturing. Counting the slave ships plying the Liverpool trade in the years leading up to the Industrial Revolution, Marx observed: “In 1730 Liverpool employed 15 ships in the slave trade; in 1751, 53; in 1760, 74; in 1770, 96; and in 1792, 132.” (Van Der Linden, 1997)

Eric Hobsbawm (1960:107) noted: “The Dutch, who managed to capture the Portuguese system in the Indian Ocean, retained their economically unprogressively methods of colonial exploitation until well into the eighteenth century. Had the British been as successful as Dutch, there is little doubt that they would have less to develop their methods of colonial exploitation, out to be rather more useful for our subsequent industrialisation. The second phenomenon is more complex. Briefly, development of modern capitalism cannot be understood single national economy or of the national economic separately, but only in terms of an international economy. of course, what Marx meant when emphasising the “Broadly speaking, the capture of this entire world market of it by a single national economy or industry could prospects of rapid and virtually unlimited expansion modest and confined capitalist manufacture of the period yet achieve itself, and thus make it possible for this sector to break through its pre-capitalist limit.”

Crucially, these processes—slavery, colonial extraction, and coercive trade—were not incidental features of early capitalism but primary sources of the capital accumulation that funded the Industrial Revolution, technological advancement, and the subsequent rise of the West (Siddiqui, 2020b). This reality, however, is often overlooked by mainstream economists. By treating capital accumulation as the result of internal factors such as thrift, innovation, and efficient markets, mainstream economic narratives erase the role of imperial violence, resource plunder, and exploitation. This omission is not a neutral oversight but a foundational silence that allows the West’s development to be presented as a self-generated miracle rather than what it was: a process profoundly shaped by the dispossession and underdevelopment of the Global South. This exploitative structure entrenched a lasting economic divide, creating the vast wealth gap that continues to separate the Global North from the Global South (Siddiqui, 2022).

The mechanisms of this exploitation are starkly illustrated in specific historical cases. British colonial policy in India, for instance, deliberately destroyed its world-leading textile industry, reducing the subcontinent from a manufacturer of finished goods to a supplier of raw cotton and a consumer of British Lancashire cloth. Similarly, in Ireland, British mercantilist restrictions crippled the emerging wool industry to eliminate competition and protect British commercial interests. In both cases, the colonial power actively deindustrialized its possessions to concentrate manufacturing and wealth at home (Siddiqui, 2025d).

Apologists for colonialism often attempt to rehabilitate this history by citing purported benefits—such as infrastructure, railways, telegraphs, education, and administrative institutions—arguing that colonial rule introduced “modernization.” This framing, however, misrepresents the nature and purpose of colonial development. Such infrastructure was not built to foster indigenous prosperity but to enable resource extraction: railways carried raw materials to ports, ports served ships bound for the metropole, and administrative systems extracted land rents, taxes, and labour discipline.

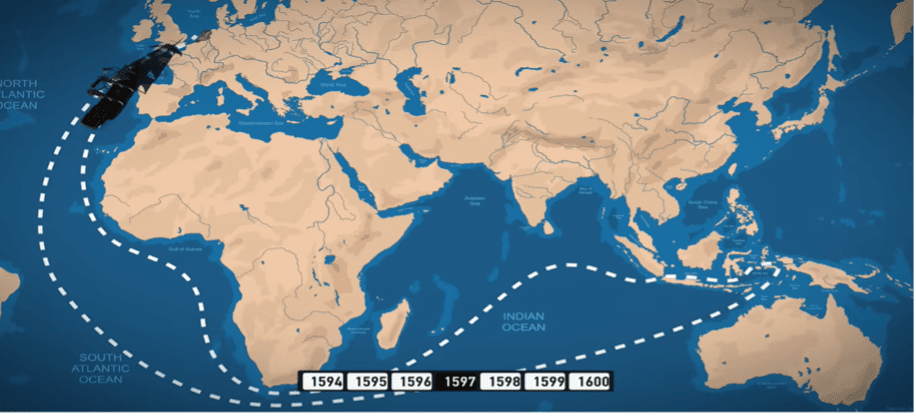

The Dutch East India Company (Vereenigde Oostindische Compagnie, or VOC) was established in 1602. By the mid-17th century, its logo appeared on the Dutch guilder, the dominant currency for trade in East Asia. By the mid-18th century, the Dutch controlled key sea trade routes (Map 1). Concurrently, the Dutch established trading colonies in the New World, though these proved less successful than their Asian counterparts.

Map 1: Cartography of Commerce: Spice Trade Flows from the East Indies to the Dutch Republic in the 16th century.

The Dutch East India Company (VOC), one of the earliest joint-stock enterprises, became the primary engine of Dutch colonial expansion. With a statutory capital of roughly 6 million guilders—about eleven times that of the British East India Company—the VOC wielded quasi-sovereign powers, including the ability to raise armies and navies, conduct diplomacy, and exercise legal authority in its territories.

In the 16th century, the Dutch faced competition in East Asia from the Portuguese (Siddiqui, 2026), whose military and commercial position was already weakening. The Dutch disrupted Portuguese shipping and displaced rivals from key spice, tea, and raw-material markets. They first established forts in present-day Indonesia and, from 1609 onward, systematically seized territories held by the Portuguese and local Muslim sultanates, ultimately expelling the Portuguese from the region. Under Jan Pieterszoon Coen, they also captured the Republic of Formosa (modern-day Taiwan), later driving out the Spanish. In these conquered territories, the Dutch established spice plantations reliant on the exploitation of local populations.

A key priority for the VOC was establishing trading posts in India. Its first settlements were in Orissa, where the Dutch traded spices, precious stones, and textiles for European markets, often exchanging them for weapons and ammunition. With support from local allied elites, VOC forces expelled the Portuguese from the Malabar and Coromandel coasts and captured Cochin, expanding spice and rice cultivation. The VOC also seized Portuguese Ceylon, which later became one of its most profitable colonies.

In the second half of the 17th century, the VOC reached its peak. Its fleet comprised around 200 ships, supported by a private army of roughly 10,000 soldiers, while its shares rose about 10% annually. At the same time, the Dutch faced growing opposition in India from the British East India Company, which sought to eliminate European rivals. The three Anglo-Dutch Wars were driven by competition over colonies and supply markets across Asia, Africa, and the Americas. Though Britain enjoyed a more advantageous geographic position and greater manpower, the Dutch Republic initially held stronger financial resources and a slight edge in merchant shipping.

The colonial system that took shape in the mid-seventeenth century became a central—arguably decisive—factor in laying the foundations for the Industrial Revolution. As Eric Hobsbawm (1960) argued, this system fully developed only in countries excluded from earlier colonial structures, and only after their collapse, from the mid-seventeenth century onward.

In this context, the driving force of colonial enterprise from the sixteenth to eighteenth centuries shifted away from the spice trade toward plantation economies. The spice merchant profited by monopolising scarce, high-value goods such as pepper and extracting high margins per transaction. By contrast, the sugar planter generated wealth through the mass production of sugar at falling prices, capturing expanding global markets and achieving greater aggregate profits. For similar reasons, the development of a cotton industry proved more economically transformative than reliance on luxury goods such as silk.

Prominent British economic historian Eric Hobsbawm (1960:106) states: “It happened under the peculiar historical conditions of Europe in the sixteenth to nineteenth centuries, i.e., a) under conditions when nobody planned or knew enough to plan industrialisation, and b) when the main dynamic force in the economy was private enterprise urged along by the motive to make and accumulate maximum profits. For the first (and therefore most difficult) industrial revolution, the initial breakthrough in world history, was achieved by and through capitalism, and could almost certainly, in seventeenth-and eighteenth-century conditions, not have been achieved in other ways, though today such other ways are available, and indeed preferable. On the other hand we know that the actual process of the rise of industrial manufacture.”

III. The Dutch Golden Age: Commerce, Expansion, and Trade

The Dutch colonial system was initially a trade-based system that derived most of its influence from merchant enterprise and from Dutch control of international maritime shipping routes through strategically placed outposts, rather than from expansive territorial ventures. The Dutch were among the earliest empire-builders of Europe, following Spain and Portugal, and were one of the wealthiest nations of their time. Spanish and Portuguese expansion, for instance, being based on robbery and monopoly, failed to stimulate European exports (Siddiqui, 2026).

The Dutch Republic experienced high growth and rising merchant profits during what is known as the ‘Dutch Golden Age’—a period of immense wealth generated through global trade, advanced shipping industries, and pioneering financial systems. The Dutch Golden Age, spanning the 17th century, marked an era when the Dutch Republic emerged as one of the world’s most dominant economic, scientific, and cultural powers.

This growth was driven by the Dutch East India Company and the Dutch West India Company, which transformed the Dutch Republic into a global trader. Amsterdam emerged as the world’s leading financial hub, pioneering stock exchanges and speculative trading, exemplified by the Tulip Mania. The period was shaped by the Eighty Years’ War (1568–1648), culminating in the Peace of Westphalia, which recognised Dutch independence.

Dutch imperial expansion relied on a maritime sector and state-backed chartered companies, granted monopolies over key global routes via the Strait of Magellan and the Cape of Good Hope. Their dominance helped drive the seventeenth-century Dutch Golden Age, marked by commercial expansion and cultural growth. Dutch navigators charted regions including Australia, New Zealand, and parts of North America, while trade with the Mughal Empire—especially Bengal Subah—supplied most imported textiles and silks.

Economic success was further supported by early industrialisation using wind, water, and peat, alongside agricultural advances. By the mid-seventeenth century, the Dutch enjoyed Europe’s highest living standards, with merchant fleets dominating trade routes from the Baltic to Asia. Shipping was not peripheral but the foundation of Dutch global power (Wilson, 1939).

Trade has long been central to the economic development of the Global North, particularly in Western Europe and North America (Siddiqui, 2015). Its foundations were laid during the era of mercantilist expansion and later evolved into the global spread of capitalism. The rise of commercial—and subsequently industrial—capitalism was financed and sustained through slavery, colonialism, and unequal trading systems imposed by imperial powers (Siddiqui, 2020b). This so-called “free trade” served imperial interests: it dismantled indigenous industries and self-sufficient economies in colonised regions, forcing them into specialised raw-material production and turning them into captive markets for metropolitan manufactures.

In South Asia, Dutch fortunes declined. The British East India Company expelled the Dutch East India Company from Bengal in 1760, effectively ending Dutch trade with India. Although both companies were marked by corruption, this did not necessarily equate to economic decline. By this stage, the VOC—like its British counterpart—had evolved beyond a purely commercial enterprise into a vehicle of political influence, offering not only profits but also patronage networks in Asia and leverage within European politics (Wilson, 1939).

Figure 2: Seventh Century Amsterdam: A Glimpse into the Dutch Golden Age.

The Dutch Golden Age rested not only on trade but also on colonial violence. The Dutch East India Company transformed the Dutch Republic into a major global power, yet its wealth was built in part on coercion. In the Moluccas—especially the Banda Islands—the VOC enforced a monopoly over nutmeg and mace through conquest and mass violence. Under Jan Pieterszoon Coen, the islands were systematically depopulated to secure control of production.

Trade wealth was reinvested into urban expansion. Amsterdam grew into a global financial hub, with canals, warehouses, and commercial districts reshaping the city. Trade increasingly dictated urban planning, governance, and public priorities.

Three main interpretations seek to explain this rise. First, the migration of merchants from Antwerp to Amsterdam after its decline helped transfer capital and expertise. Second, Max Weber linked capitalism to Protestantism—either through a work ethic or through higher literacy and “human capital.” While the Dutch Republic showed relative religious tolerance, the Dutch Reformed Church remained dominant and Catholics faced discrimination, suggesting tolerance was pragmatic rather than ideological. Third, Douglass North and Elinor Ostrom emphasised the role of institutions, arguing that prosperity depended on effective governance structures, often rooted in civic participation rather than imposed from above.

A relatively high level of urbanisation distinguished the Dutch Republic. By the mid-sixteenth century, around 15% of its population lived in towns of over 10,000 people—compared to 3.5% in England and 13% in Italy—and this rose to 32% a century later. Unlike England, where urban life was concentrated in London, the Dutch Republic had a broad urban network, including Amsterdam (about 175,000 inhabitants), making it one of Europe’s largest cities.

Van der Linden (1997) argues that while neither Marx nor Engels attempted a systematic analysis of the development of merchant capitalism in seventeenth-century Dutch Republic, both did refer to this “model capitalist nation” in their writings. Their analysis stressed that Dutch capitalism was based on the exploitation of non-capitalist forms of production, and that the decline of the Dutch Republic in the eighteenth century represented the history of the subordination of commercial capital to industrial capital.

Marx saw a direct connection between the rise of Dutch merchant capital and the changes in international trading routes. Before the circumnavigation of Africa, colonies were still unknown, “America did not exist yet for Europe,” “Asia existed only through the inter-mediary of Constantinople,” and “the Mediterranean was the center of commercial activity” (Marx, 1976). But towards the end of the 15th century the old Italian merchant republics received a deadly blow. Venice was pushed aside, as it were: “The privileges of its neighbourhood to Constantinople and Alexandria, then the centres of Asiatic trade, were forfeited by the circumnavigation of the Cape of Good Hope, transferring the center of that trade first to Lisbon, then to Holland, and afterward to England” (Marx, 1976, cited in Van Der Linden, 1997:162).”

In the seventeenth century, the Dutch merchants were rich in the world. They possessed the global reserve currency, the strongest navy, the most advanced financial system, and the highest standard of living in human history. They were the masters of the universe. And yet, over the course of fifty years, they slowly, quietly, and methodically ceased to be a superpower. They did not lose a catastrophic war that destroyed their homeland. They suffered because their elite class—the merchants, the bankers, and the politicians—realised that there was no more growth to be had at home. They realised that the cost of maintaining the empire was higher than the profit it generated. So, they decided to export their wealth. They decided to lend their capital to their enemies. The Dutch pattern is the blueprint for how a hegemonic power hollow itself out. It is about how a nation of producers becomes a nation of speculators, and how a ruling class separates its own destiny from the destiny of its people.

In the 1600s, the Dutch were the workshop of the world. They were the innovators. They invented the sawmill. They perfected the fluyt ship, which could carry more cargo with fewer crew than any other vessel. And they mastered the art of wind energy. They imported raw timber and iron, processed it with superior technology, and exported finished ships and machinery. This productivity created a massive surplus of capital. Amsterdam became the richest city on Earth because it was the most productive city. The Dutch guilder was the world reserve currency—not because of a military decree, but because everyone wanted Dutch goods. The currency was backed by the sweat, the engineering, and the physical dominance of the Dutch economy.

The Golden Age began to fade in the early eighteenth century due to costly wars with rival empires—particularly England and France—stagnation in trade, and shifting economic power. However, success also breeds a specific kind of crisis. As the Dutch grew wealthier, wages rose and living standards soared. Consequently, building ships in Amsterdam became more expensive than in rising competitors such as England and France. Dutch capital holders—the merchant families who ran the Dutch East India Company and the Bank of Amsterdam—observed declining returns on investment for domestic manufacturing. Labour was too costly, and the domestic market had become saturated. In response, the Dutch shifted from an economy of production to an economy of finance. They ceased to be the workshop of the world and became its banker.

IV. The Decline of Dutch Commercial Capitalism: From Trade to Finance

To understand how the Dutch lost everything, you first need to understand what they were actually holding. By 1602, the Dutch Republic was in a state of furious innovation. For decades, small independent Dutch trading companies had been sailing to the East Indies, fighting off pirates, negotiating with local rulers, and bringing home spices that sold for enormous markups in European markets. But these companies were burning each other out. They competed so aggressively with one another that they were driving up the prices they paid in Asia and driving down the prices they received in Europe, destroying the margins that made the whole enterprise worthwhile.

One of the most significant aspects of British trade policy in the eighteenth century was to remove the Dutch commercial dominance. This rivalry, which had simmered throughout the previous century, intensified as Britain sought to assert its own maritime and industrial supremacy. A striking illustration of this protectionist turn was the 1736 Act, which required every British ship to carry at least one set of sails manufactured in England (Siddiqui, 2018). This legislation was directly aimed at undermining the Dutch cloth industry, a key sector of the Dutch economy that had long supplied maritime nations across Europe. Such measures, combined with a series of Navigation Acts and tariff policies, systematically eroded the competitive advantages that had underpinned Dutch commercial hegemony.

The organisation of commerce in Dutch Republic during the eighteenth century, however, made the transition from trading to banking and finance peculiarly seamless. Dutch merchants had long operated within a sophisticated commercial infrastructure that proved adaptable to changing global circumstances. Traders were divided roughly into three categories: overseas traders, who maintained factors and supercargoes across the world; second-hand merchants, who purchased goods from the former to sell on their own account; and commission traders, who facilitated transactions between parties without taking ownership of the goods themselves (Wilson, 1939).

In the eighteenth century, the Dutch colonial empire began to decline as a result of the Fourth Anglo-Dutch War of 1780–1784, in which the Dutch Republic lost a number of its colonial possessions and trade monopolies to the British Empire, alongside the British East India Company’s conquest of Mughal Bengal at the Battle of Plassey. Nevertheless, major portions of the empire survived until the advent of global decolonisation following World War II, namely the East Indies and Dutch Guiana. Three former colonial territories in the West Indies islands around the Caribbean Sea—Aruba, Curaçao, and Sint Maarten—remain as constituent countries represented within the Dutch Republic.

From the third quarter of the 17th century onward—that is, earlier than suggested in recent literature—the tide seems to have turned, and stagnation set in the Dutch economy, which resulted in a rise of real freight rates and a worsening of competitiveness. The inability to improve shipping efficiency after the first quarter of the seventeenth century made the Dutch vulnerable to competition. The stagnation in shipping efficiency from the 1620s onward not only harmed the competitive position of the Dutch mercantile fleet but also likely affected the general economic development of the Republic. One of the most strategic sectors had turned from being a source of rapid productivity growth into a source of stagnation (Wilson, 1939).

Many economists attribute this decline to the financialisation of the economy, which they view as the natural evolution of a developed nation. Throughout the 1700s, the Amsterdam Stock Exchange increasingly resembled a casino. The Dutch elite pioneered complex financial instruments—derivatives and futures contracts—and fuelled speculative bubbles in exotic assets. They grew richer, yet the real economy was squeezed. Shipyards closed. Skilled engineers declined without replacements. Fishing fleets shrank. And the middle class—once the backbone of the Golden Age—began to fracture (Wilson, 1939).

These were a few of the economic activities in Dutch Republic in the first quarter of the eighteenth century, and it is necessary to emphasise that the natural changes in this economy were not catastrophic. As Wilson (1939: 113) noted: “They may be summed up as follows: first, Dutch Republic lost her intermediary position in world trade as other European countries developed their own shipping and port facilities, and direct trading routes were established between nations which had previously used Dutch shipping and trading agents. Secondly, this decline in the stapling organisation was not counterbalanced by any industrial development, such development being hindered by the high level of wages and the conflict of interests between the powerful free-trading staplers and the protectionist industrialists. Thirdly, there was a gradual shift of interest from trade to finance-to-insurance and credit banking, and, because of the low rate of interest in Dutch Republic, to foreign loan business and speculation.”

For Marx and Engels, there was no doubt that—certainly in the seventeenth and eighteenth centuries—merchant capital dominated Dutch society. For a further analysis of this domination, it is important to note that Marx distinguished between two kinds of merchant capital: commercial capital and money-dealing capital. This distinction applies clearly to the Dutch case, for “the history of Holland’s decline as the dominant trade nation is the history of the subordination of commercial capital to industrial capital”.

In the eighteenth century, Dutch Republic ceded its hegemonic position to England. “By the beginning of the eighteenth century, Dutch Republic’s manufactures had been far outstripped. It had ceased to be the nation preponderant in commerce and industry”. While its role as commodity trader was thus played out, its function as money trader remained important until the nineteenth century. Just as declining Venice had once formed “one of the secret foundations of Dutch Republic’s wealth in capital,” to which it lent great sums of money, so too did “the lending out of enormous amounts of capital, especially to its great rival England” become an extremely important activity for the Dutch (Marx, 1976 cited in Van Der Linden, 1997).

Two causes of the decline were emphasised above all. One was the absence of a genuine centralised state, which could only have emerged if the stadtholders had overcome the particularistic city interests. However, they could have succeeded in this only if they had done “the inconceivable, to call seriously on the power of the popular masses to help them bring the provincial regents to heel. After all, the economic and financial preponderance of Dutch Republic and Amsterdam over the other regions and other ruling classes and groups was so oppressive and crushing, that only a consciously marshalled, permanent popular movement would have been able to neutralise this preponderance in exchange for civil rights.” The monarchy, “which historically was the highest state form achievable for Western Europe at the time, therefore was not established.”

The war with England followed several years of political and financial indecision in the Dutch Republic. Until about 1779, all Dutch financial ties were with England. Dutch money had seen the British government through several difficult periods. But after Britain was expelled by America, Dutch confidence weakened, and Dutch investors began to listen to those Francophile advisers who recommended that they sell out their British holdings while they could.

While its role as commodity trader was thus played out, its function as money trader remained important until the nineteenth century.

The merchant class obstinately refused to recognise that a new economic order had come into being, superseding the era when the Dutch had been carriers and paymasters for an economically undeveloped Europe. As late as 1824, a Dutch writer remarked that Holland’s trade rested on surer foundations than England’s because it depended only to a small extent on industrial products, while 70 percent of British exports came from factories. It remained for King Willem I to bring the Dutch Republic into line with contemporary economic ideas, reestablished the Netherlands Bank as a bank of issue, cherishing the colonial trade, protecting the textile and metal industries, and making what could be made of the previously despised transit trade (Wilson, 1939).

The Dutch bankers began to lend massive amounts of capital to the British government and British corporations. They bought British bonds. They invested in the British East India Company—the direct competitor to their own national interests. They funded the very navy that would eventually blockade their ports and strangle their economy. They did it because the return on investment was higher in England. The Dutch Republic collapsed, yet the Dutch elite remained rich because their assets were safely parked in London, earning 5 percent interest guaranteed by the British crown.

V. Conclusion

The rise and decline of the Dutch Republic as a commercial hegemon offers a compelling case study in early modern economic expansion and its structural vulnerabilities. Dutch ascendancy in the seventeenth century stemmed from a unique convergence of geographic, institutional, technological, and political circumstances—high urbanization, a commercialized agricultural sector, and shipping innovations like the fluyt—that created an economy of unparalleled efficiency.

Yet the very mechanisms enabling hegemony contained the seeds of decline. The eighteenth-century finance-driven economy generated immense private wealth but could not sustain the productive industrial base on which Dutch prosperity had rested. The merchant class rationally exported capital to rivals, notably Britain, funding the competition that would eventually supplant Dutch dominance. The Fourth Anglo-Dutch War (1780–1784) exposed this fragility, triggering a collapse of confidence from which the Republic never recovered.

Three broader conclusions emerge. First, Dutch shipping productivity gains between 1550 and 1620 proved unsustainable once the political environment shifted. Second, the VOC’s success encouraged financial speculation and rent-seeking that undermined long-term competitiveness. Third, the Dutch pattern of decline featured elite separation from national vitality, hollowing out of productive capacity, and capital export to rivals.

In short, the Dutch Golden Age and its decline were not merely a prelude to British ascendancy but a distinct model of capitalist development. The Dutch trajectory reminds us that sustained economic leadership requires not only innovation and expansion but also the ability to renew productive foundations amid shifting pressures—a challenge as pertinent today as in the eighteenth century.

Dr. Kalim Siddiquiis an economist specializing in International Political Economy, Development Economics, Trade and Economic Policy. Since 1989, he has been teaching economics at various universities in Norway and the UK. Dr. Siddiqui’s research interests encompass a wide range of topics, including political economy, international trade, and economic history, South Asia, and emerging economies. He has presented papers at international conferences across numerous countries, reflecting his global engagement in the field. His scholarly pursuits span six broad domains: Political Economy, Development Economics, Economic History, Economic Policy, Globalization, and International Trade. Dr. Siddiqui has made significant contributions to research in areas such as trade policy, globalization, and political economy. His work has been published in chapters of edited books and articles published in peer-reviewed journals. For inquiries, Dr. Siddiqui can be reached at: [email protected]

References

Hobsbawm, E.J. (1960) “The Seventeenth Century in the Development of Capitalism” Science & Society, 24(2):97-112.

North, D.C. (1991) “Institutions, Transaction Costs, and the Rise of Merchant Empires” in J. D. Tracy (ed.), The Political Economy of Merchant Empires: State Power and World Trade, 1350–1750, Cambridge: Cambridge University Press, pp.26-27.

Siddiqui, K. (2026) “Crusade and Commerce: Portuguese Mercantilism in the Indian Ocean, 1500-1600” World Financial Review, February.

Siddiqui, K. (2025a) “Innovation, Investment Criteria, and Economic Growth in Late-Industrializing Economies” World Financial Review, December.

Siddiqui, K. (2025b) “Ibn Khaldun and the Dynamics of Social and Economic Transformation” World Financial Review, September.

Siddiqui, K. (2025c) “The United States’ Future in an Imperial Mirror: Lessons from Britain, Spain, Abbasids, Rome, and Beyond” World Financial Review, November.

Siddiqui, K. (2025d) “Geopolitics and the Persistence of Global Uneven Development: A Critical Analysis” World Financial Review, July.

Siddiqui, K. (2024) “The Multinational Corporations, Capitalism, and Imperialism: The Case Study of East India Company” World Financial Review, July.

Siddiqui, K. (2022) “Capitalism, Imperialism, and Crisis”, European Financial Review, June/July.

Siddiqui, K. (2020a) “The Political Economy of Famines under Colonial India: A Critical Analysis” World Financial Review, July/August.

Siddiqui, K. (2020b). “The Political Economy of the Slave Trade, Capital Accumulation and the Rise of Britain” World Financial Review, January/February.

Siddiqui, K. (2018). “David Ricardo’s Comparative Advantage and Developing Countries: Myth and Reality” International Critical Thought, 8(3):1-28, September.

Siddiqui, K. (2015). “Trade Liberalisation and Economic Development: A Critical Review” International Journal of Political Economy 44(3):228 – 247.

Van Der Linden, M. (1997) “Marx and Engels, Dutch Marxism and the Model Capitalist Nation of the Seventeenth Century” Science & Society 61(2):161-193.

Wilson, C.H. (1939) “The Economic Decline of the Netherlands” Economic History Review, 9(2):111-127.

The operational challenge of translating complex regulatory texts into consistent, auditable action represents a persistent point of friction across regulated industries. In financial services, this often manifests as a reliance on manual interpretation, procedural checklists, and disparate systems that struggle to align global policy with local jurisdictional requirements. McKinsey insights indicatethat banks paid $19.3 billion in penalties in 2024 alone, a figure higher than ever before, and that two-thirds of global banks have lost clients due to slow and inefficient onboarding and KYC processes. This environment creates significant operational latency, introduces inconsistencies, and embeds considerable audit and regulatory risk within core client lifecycle processes.

My engagement with this challenge began within the operational core of client due diligence in 2006, where early systems prioritised document storage over decision logic. At that time, processes were largely manual, running on platforms like IBM Lotus Notes and FileNet, and lacking integration, risk-modelling, or scalability. The pivotal evolution in my approach occurred during my responsibility for global sign-off on a large-scale client lifecycle management platform deployment for a major international bank. That was a role that challenged me for a transition: moving away from assessing procedural compliance to guaranteeing engineered outcomes. It was during that experience that I discovered a fundamental gap: compliance platforms were often built as digitised checklists rather than as systems capable of applying policy logic.

This insight informed the development of a systematic methodology designed to bridge policy, process, and technology. The approach, known as Policy-as-Code, is centred on the principle that regulatory intelligence should be embedded within systems as executable logic rather than confined to procedural manuals. The following blueprint details the practical components of this methodology, providing a structured framework for deconstructing regulatory language, architecting scalable decisioning systems, and implementing a sustainable model for governed, business-led compliance operations.

Decomposing Policy into Regulatory Atoms

The first and most critical step is to decompose the voluminous amount of compliance manuals and regulatory texts into their fundamental components. A full policy document must be broken down into discrete logic statements. This process involves identifying the universal building blocks, which I refer to as regulatory atoms, that constitute regulatory requirements across all jurisdictions.

These regulatory atoms typically fall into several core categories: the client’s industry classification, their geographic jurisdiction, the financial products they intend to use, and specific AML/CFT risk factors such as ownership structure or anticipated transaction patterns. Furthermore, each requirement dictates necessary data points to be collected and validated, as well as the documents that serve as evidence. A regulation does not simply state “perform enhanced due diligence”. What it should do in reality is to specify that for a corporate client in a high-risk industry, operating in a particular jurisdiction, specific data on ultimate beneficial owners must be gathered and certified articles of incorporation must be obtained.

The outcome of this decomposition is a structured taxonomy of policy, which transforms subjective interpretation into objective classification. It allows any regulatory requirement to be expressed as a combination of these atoms, such as: if the industry is classified as high-risk and the jurisdiction carries elevated regulatory requirements, then the risk tier is set to high and specific documentary evidence is required. This structured logic becomes the foundation for all subsequent coding, and such taxonomies support transparency, auditability through version control, and facilitate compliance with regulatory standards across multiple jurisdictions.

Architectural Foundations: The 80/20 Model

With a clear taxonomy defined, an architecture must be established to host and execute this logic at scale. The most effective model for global operations is what I call the “80/20 architecture,” a design that separates the immutable core of an institution’s global policy from the necessary configurations for local regulatory variation.

The 80% core represents the enterprise’s standardised compliance framework, encoding the principles that apply to every client irrespective of location. This includes the master data model defining client and counterparty entities, the foundational risk-scoring methodology, the standard lifecycle stages from onboarding to offboarding, and universal control procedures like global sanctions screening. This core is designed for stability and auditability, providing the consistent backbone of the compliance programme.

The 20% configuration layer is reserved for jurisdictional implementation, where the decomposed regulatory atoms for specific countries are stored and managed. It contains the local rules that modify or augment the global core, such as a requirement for a jurisdiction specific due diligence data and document collection, unique national tax identifier, a jurisdiction-specific risk assessment form, or a locally mandated additional controls and cooling-off period. This layer is designed for managed adaptability without requiring changes to the core system’s fundamental code.

This architectural separation proves vital in practice. It ensures that the institution maintains global consistency on principles while permitting necessary local flexibility in practice. Updates to local regulations are confined to the configurable 20% layer, which dramatically reduces the complexity and risk of change management compared to modifying a monolithic application. In my experience implementing this architecture across 50+ markets, the approach enabled unified platforms for CDD, MiFID, CRS/FATCA, and full lifecycle events while supporting regional variation without creating silos.

Implementation: Selecting and Employing Rules Engines