Businesses across finance, logistics, construction, and infrastructure management are rapidly investing in automation technologies to improve operational efficiency and reduce costs. Companies seeking scalable digital ecosystems increasingly rely on providers offering drone software development expertise to create intelligent platforms tailored to complex enterprise operations. Companies such as Wezom help businesses integrate drone technologies into broader automation strategies that support real-time analytics, operational visibility, and long-term scalability.

Why Automation Has Become a Business Priority

Modern enterprises operate in an environment where efficiency, speed, and data accuracy directly influence competitiveness. Companies are expected to deliver faster services, reduce operational downtime, and optimize resource allocation while maintaining high levels of reliability and security.

Traditional operational models often rely heavily on manual inspections, paper-based reporting, and fragmented communication between departments. These processes slow decision-making and create unnecessary operational expenses. As businesses grow, the limitations of manual workflows become even more visible, especially for enterprises managing large facilities, infrastructure networks, or distributed operations.

Drone technologies help solve these challenges by introducing automation into everyday business processes. Instead of relying entirely on human labor, organizations can use intelligent drone systems to collect data, monitor assets, and identify operational issues in real time.

Businesses adopting automation strategies typically focus on several key goals:

Improving operational efficiency;

Reducing long-term infrastructure costs;

Increasing process transparency;

Accelerating data collection and reporting;

Enhancing workplace safety.

Drone software development supports all of these objectives by creating centralized platforms capable of integrating aerial intelligence into larger enterprise ecosystems.

How Drone Technologies Support Business Automation

Modern drone systems are no longer standalone tools used only for aerial photography or surveillance. They have evolved into intelligent operational platforms capable of supporting highly automated business environments.

One of the main advantages of drone technologies is their ability to automate repetitive and resource-intensive tasks. This is especially valuable for industries where inspections and monitoring procedures are performed frequently and across large geographic areas.

For example, infrastructure inspections that once required multiple employees, expensive equipment, and extended operational downtime can now be completed much faster using autonomous drone systems combined with AI-powered analytics.

Drone platforms also improve operational consistency. Manual inspections often depend on human judgment and may vary in quality or accuracy. Automated drone systems follow predefined workflows and capture standardized data sets, reducing inconsistencies and improving reporting reliability.

Another important advantage is accessibility. Drones can quickly reach difficult or hazardous environments where traditional inspections may be dangerous or expensive. This improves safety while allowing businesses to monitor assets more frequently.

Common automation scenarios include:

Facility and infrastructure inspections;

Remote asset monitoring;

Warehouse inventory management;

Construction progress tracking;

Security surveillance operations.

As organizations continue investing in digital transformation, drone automation is becoming a critical component of enterprise operational strategy rather than a supplementary technology.

The Growing Role of Artificial Intelligence in Drone Platforms

Artificial intelligence has significantly expanded the business value of drone technologies. Without AI, drones primarily function as remote data collection devices. With intelligent analytics, they become systems capable of generating actionable operational insights automatically.

AI-powered software can process large volumes of drone-generated data much faster than human teams. This enables organizations to identify problems early and respond proactively before operational issues escalate into costly disruptions.

For businesses managing critical infrastructure, predictive analytics has become especially important. AI systems can analyze visual patterns, thermal imagery, and equipment performance indicators to detect anomalies that may indicate future failures.

Instead of reacting to incidents after they occur, companies can implement predictive maintenance strategies that improve operational reliability and reduce downtime.

Artificial intelligence also improves automation capabilities through:

Intelligent route planning;

Automated image recognition;

Real-time anomaly detection;

Predictive operational forecasting;

Automated reporting and analytics.

As machine learning technologies continue advancing, drone platforms will become even more autonomous and capable of handling increasingly complex operational tasks.

Why Businesses Across Industries Are Investing in Drone Automation

The demand for drone software development continues growing because businesses across multiple sectors face similar operational challenges. Organizations need faster access to accurate information while controlling infrastructure costs and improving efficiency.

In the financial and insurance sectors, drone technologies help automate property inspections, assess infrastructure conditions, and accelerate claims processing. AI-powered analytics improve fraud detection while reducing the manual effort required for operational assessments.

Construction companies increasingly rely on drones to monitor project progress and improve resource management. Real-time aerial intelligence helps managers identify delays, monitor safety conditions, and improve communication between teams and stakeholders.

Logistics and supply chain companies use drone systems to improve warehouse operations and inventory visibility. Automated monitoring reduces inefficiencies while supporting better operational planning.

Energy providers also represent a major area of growth for drone automation. Power lines, pipelines, solar farms, and industrial facilities require continuous monitoring to maintain operational stability. Drone inspections help reduce downtime while minimizing human exposure to hazardous environments.

Several factors are accelerating enterprise drone adoption:

Growing operational complexity;

Rising infrastructure maintenance costs;

Increased demand for automation;

Expansion of AI-powered analytics;

Improvements in cloud infrastructure.

As these trends continue, drone technologies are becoming more deeply integrated into long-term enterprise strategies.

The Limitations of Generic Drone Software

Many businesses initially adopt ready-made drone applications because they appear affordable and easy to implement. However, generic platforms often create limitations once operational requirements become more complex.

Off-the-shelf software is typically designed for broad use cases rather than industry-specific operational needs. This can create significant challenges for enterprises requiring advanced integrations, scalability, or compliance controls.

One of the most common problems is limited flexibility. Generic platforms may not support specialized workflows or custom analytics capabilities required by large organizations.

Integration also becomes a major issue. Enterprise environments often depend on interconnected systems such as ERP platforms, CRM software, cloud environments, and IoT infrastructure. Drone platforms that cannot integrate effectively reduce the overall value of operational data.

Businesses frequently encounter problems such as:

Inflexible reporting structures;

Security vulnerabilities;

Limited automation capabilities;

Poor scalability for enterprise operations;

Restricted customization options.

Custom drone software development allows businesses to create ecosystems tailored specifically to operational goals, infrastructure requirements, and long-term growth strategies.

Security and Compliance in Enterprise Drone Ecosystems

As enterprises automate more operations, cybersecurity and compliance become increasingly important considerations. Drone systems often process sensitive operational and infrastructure data that must be protected against unauthorized access or security breaches.

Industries such as finance, logistics, and critical infrastructure management operate under strict regulatory requirements. Businesses in these sectors need platforms that support secure data management and transparent operational controls.

Modern enterprise drone platforms typically require:

Secure cloud architecture;

Role-based user access management;

Data encryption standards;

Audit tracking capabilities;

Regulatory compliance reporting.

Organizations investing in custom software environments gain greater control over how data is stored, processed, and shared across operational systems.

Security considerations are becoming even more important as businesses expand automation initiatives and integrate drones into broader enterprise ecosystems.

The Future of Drone Software Development

Drone technologies will continue evolving alongside advancements in AI, cloud computing, and enterprise automation. Over the next several years, businesses are expected to adopt increasingly intelligent drone ecosystems capable of operating with minimal human intervention.

Autonomous drone fleets, edge computing, and real-time analytics will significantly expand operational capabilities. Companies will be able to process data faster, improve predictive decision-making, and automate complex infrastructure management tasks at scale.

Future drone platforms will likely focus on:

Autonomous operational workflows;

Advanced AI-assisted analytics;

Real-time infrastructure monitoring;

Integration with digital twin technologies;

Predictive maintenance automation.

As competition increases and operational efficiency becomes even more important, businesses investing early in scalable drone ecosystems will gain stronger long-term advantages.

Conclusion

Drone software development is becoming a critical part of modern business automation strategies. Enterprises across finance, logistics, construction, and infrastructure management increasingly use drone technologies to improve operational visibility, automate repetitive tasks, and reduce long-term operational costs.

While generic software platforms may support basic drone operations, modern enterprises require scalable ecosystems capable of integrating with broader business infrastructure. Custom solutions provide greater flexibility, stronger security, and more advanced analytics tailored to specific operational goals.

As automation, AI, and cloud technologies continue reshaping enterprise operations, drone platforms will play an increasingly important role in helping businesses improve efficiency, scalability, and long-term digital transformation outcomes.

The AI jobs debate has been stuck in two bad extremes. One side insists a white-collar wipeout is already underway. The other waves away every concern because the unemployment rate has not exploded. In Anthropic’s new report, “Labor market impacts of AI: A new measure and early evidence,” Maxim Massenkoff and Peter McCrory cut through that noise with something far more valuable: a way to track where AI is actually entering work, where it still falls short, and where the earliest damage may appear first.

AI is already reshaping the labor market, but the strongest signal today is weaker entry-level hiring in exposed occupations, not a mass unemployment shock

They argue that labor market analysis needs to move beyond abstract capability and toward observed use. Their central contribution is a metric called “observed exposure,” which combines theoretical task feasibility with real-world Claude usage in professional settings, then weights automated use more heavily than simple assistance. That framing matters because AI disruption will not arrive as a single cinematic layoff event. It will show up through specific tasks, specific occupations, and specific hiring bottlenecks long before the broad labor market fully registers it.

Thus, AI is already reshaping the labor market, but the strongest signal today is weaker entry-level hiring in exposed occupations, not a mass unemployment shock. The evidence is serious. The panic is premature. The implications are immediate.

The Most Important Shift Is Measuring Actual Exposure, Not Hypothetical Potential

The report’s biggest achievement is methodological. Instead of asking only what large language models could do, it asks what they are actually doing in work-related settings. The authors build observed exposure from three ingredients: O*NET task data, Anthropic usage data from the Economic Index, and the theoretical exposure framework from “GPTs are GPTs”. That move instantly makes the discussion more grounded.

The report explains that a task counts as covered when it is theoretically feasible with an LLM and has seen sufficient work-related usage in Claude traffic. Fully automated implementations receive full weight, while augmentative use receives half weight, and those task-level values are then averaged up to occupations using time shares. This is a much stronger lens than simple technical possibility because firms do not adopt tools just because a benchmark says they can. Legal risk, workflow friction, verification needs, and software integration all slow deployment in the real world.

That distinction helps explain why theoretical exposure still overstates immediate labor market risk. In “GPTs are GPTs”, Tyna Eloundou, Sam Manning, Pamela Mishkin, and Daniel Rock estimated that around 80 percent of the U.S. workforce could have at least 10 percent of their tasks affected by LLMs, while roughly 19 percent could see at least 50 percent of tasks affected. The paper mapped enormous potential, but it did not claim that firms had already deployed those capabilities at scale. The Anthropic report shows that this gap between capability and deployment is still large. In Computer & Math occupations, theoretical exposure is 94 percent, but observed current coverage in Anthropic’s data is just 33 percent.

That gap is the story executives should be watching. AI is powerful enough to matter now, but still constrained enough that labor market effects will emerge unevenly. That gives employers and policymakers a narrow but real window to respond before abstract risk turns into entrenched displacement.

The Jobs Under Pressure Are Real, but Broad Unemployment Still Has Not Broken

The report’s occupational ranking is striking because it shows where AI is already most present in real workflows. Computer programmers top the list at 75 percent observed coverage. Customer service representatives come next, followed by data entry keyers at 67 percent. At the other end of the spectrum, 30 percent of workers are in occupations with zero measured coverage, including cooks, mechanics, lifeguards, bartenders, and dishwashers. AI is not sweeping across the labor market in one uniform wave. It is advancing first through digital, language-heavy, structured work.

That pattern lines up with outside research. The online vacancies study by Daron Acemoglu, David Autor, Jonathon Hazell, and Pascual Restrepo found that establishments adopting AI reduced hiring in non-AI positions and changed skill requirements in the remaining postings, even while aggregate employment effects remained too small to detect clearly. The message is simple: labor market change often appears in hiring behavior and job design before it appears in top-line unemployment numbers.

That is exactly what the Anthropic report finds. Using Current Population Survey data, the authors report no systematic increase in unemployment for workers in the most exposed occupations since late 2022. Their difference-in-differences estimate is “small and insignificant,” and they note that a sizable white-collar shock should have been detectable in this framework if it had already occurred. That is a major result because it directly challenges the claim that generative AI has already produced broad labor market collapse.

Other recent work points in the same direction. The Budget Lab at Yale’s running labor market tracker says current measures of AI exposure, automation, and augmentation show no clear relationship with broad changes in employment or unemployment so far, and its later updates through late 2025 continue to describe the patterns as flat or modest. Together, these findings support a more disciplined conclusion: AI pressure is real, but the economy has not yet absorbed it as a broad unemployment shock.

The Clearest Early Warning Signal Is Entry-Level Hiring

The sharpest finding in the report is about younger workers. For workers ages 22 to 25, entry into highly exposed occupations fell by about half a percentage point, which the authors translate into a 14 percent drop in job-finding rates in the post-ChatGPT period relative to 2022. They are careful with the claim and note that the estimate is only barely statistically significant, but it is the strongest sign in the paper that disruption may already be visible in the hiring pipeline.

That result becomes much more persuasive when placed alongside outside evidence. In “Canaries in the Coal Mine?”, Erik Brynjolfsson, Bharat Chandar, and Ruyu Chen use ADP payroll data and find that early-career workers ages 22 to 25 in the most AI-exposed occupations experienced a 13 percent relative decline in employment, with the adjustment driven primarily by slower hiring rather than a surge in separations. The symmetry between the two studies matters. Different data sources. Similar warning sign.

When AI strips away the tasks that once trained junior workers, the labor market does not just lose jobs.

This is where the labor market story gets serious. A stable unemployment rate can hide a shrinking career ladder. If firms keep senior workers, automate pieces of junior work, and hire fewer newcomers, then the damage appears first in the on-ramp. That hurts recent graduates, career switchers, and the long-run development of expertise inside firms. It also fits the logic in “Expertise”, where David Autor and Neil Thompson argue that the labor impact of automation depends heavily on what happens to the expertise value of the tasks that remain. When AI strips away the tasks that once trained junior workers, the labor market does not just lose jobs. It loses apprenticeship.

That concern also helps explain why some markets show faster pain than the broader economy. In Organization Science, Xiang Hui, Oren Reshef, and Luofeng Zhou find that freelancers in highly affected occupations suffered reductions in both employment and earnings after the release of generative AI tools. Online freelance markets are contestable, transparent, and easy to benchmark, so substitution shows up faster there. Traditional employment markets move more slowly, but they are not immune.

The strongest reading of the report is neither doom nor denial. AI has not yet triggered a broad unemployment crisis. That is genuine good news. But exposed occupations are already measurable, projected growth is somewhat weaker in those jobs, and the earliest visible strain is showing up where careers begin, not where they peak. That is the signal leaders should respect. The winners will be the organizations that redesign work around human judgment before the hiring pipeline thins out beneath them.

Markets across Asia ended mixed as investors watched rising tensions in the Middle East and prepared for the upcoming meeting between Donald Trump and Xi Jinping. Trade discussions between the United States and China are expected to be a major topic during the talks.

Investor concerns also grew after Trump described the current ceasefire with Iran as weak. At the same time, comments from US officials about possible future military action added more uncertainty to global markets. Oil prices moved lower during trading, though fears over supply disruptions remain.

In Asia, South Korea’s market posted strong gains, while Japan also closed higher. Australia slipped slightly, and Chinese markets showed mixed results. Investors were also reacting to higher than expected inflation data, which added pressure to sentiment.

US markets were mostly flat overnight after recent record highs. Traders are now closely watching both the Trump Xi meeting and developments in the Middle East, as both could affect global trade, energy prices, and investor confidence in the days ahead.

Most people don’t think twice about hair care costs — until they’re standing in a pharmacy aisle, confused by dozens of options, or scrolling through online kits that range from ₹300 to ₹15,000. The price gap is enormous, and it’s rarely explained. If you’re trying to figure out what you actually need and what it’s going to cost you, this breakdown should help.

Why Hair Care Kits Vary So Much in Price

The honest answer is that hair care kits in India are priced based on a mix of factors — ingredients, brand positioning, treatment complexity, and whether they include professional consultation. A basic kit might contain a shampoo and an oil. A more complete one might include a dermatologist-reviewed treatment plan, oral supplements, serums, and ongoing support.

That range in content naturally creates a range in price. So comparing a ₹400 kit to a ₹6,000 one without knowing what’s inside each is a bit like comparing a meal kit to a restaurant experience — they serve different purposes.

What’s Typically Inside a Hair Care Kit

Before looking at numbers, it helps to understand what these kits usually contain:

A cleansing shampoo suited to your scalp type

A conditioner or hair mask for moisture retention

A scalp oil or serum targeting specific concerns like dandruff, thinning, or dryness

Nutritional supplements in some cases (like biotin, iron, or herb-based capsules)

A consultation component in premium kits

The more targeted and clinically backed the formulation, the higher the cost tends to be. Generic kits lean on broad-use ingredients. Specialized kits are designed around specific hair loss types, scalp conditions, or deficiencies.

Understanding the Real Cost Behind the Kit

When evaluating whether a kit is worth its price, the ingredient sourcing matters. Ayurvedic or herb-based formulations that are standardized and tested cost more to produce than chemical equivalents. If a kit includes a hair specialist’s review or a customized protocol, that expertise adds legitimate value — but also cost.

For someone dealing with diffuse hair fall, hormonal imbalances, or scalp inflammation, an off-the-shelf kit may do very little. In those cases, spending less upfront might actually mean spending more over time, because the root problem isn’t being addressed.

If you’re curious about how pricing compares across different treatment types, this breakdown of Traya Kit Price In India gives a transparent look at what’s included at each level and why the cost is structured the way it is.

Common Mistakes When Buying Hair Care Kits

A lot of people make the same few errors when choosing a kit, and most of them come down to not matching the product to the actual problem.

Buying based on price alone, either too cheap or too premium without reason

Using a kit designed for hair growth when the real issue is scalp health

Switching products every few weeks without giving them time to work

Ignoring internal causes like stress, nutritional gaps, or hormonal shifts

Expecting a topical kit to fix problems that require internal support

Hair care kits are most effective when they’re part of a larger understanding of your hair’s condition. If you don’t know whether your hair fall is stress-related, nutritional, or genetic, no kit — regardless of price — will consistently work.

What a Good Kit Should Actually Do

A well-designed hair care kit doesn’t promise miracles. It supports the scalp environment, reduces breakage, nourishes the hair shaft, and ideally helps address the cause of your specific concern. Some treatment approaches like Traya focus on identifying the root cause before recommending products, which is why their kits are structured around individual hair health profiles rather than a one-size-fits-all formula.

For people who are also wondering how can i grow my hair faster, the answer almost always starts with scalp health, nutrition, and consistency — not just what product you use.

Final Thoughts

Hair care kit pricing in India reflects a genuine spectrum of need and quality. The cheapest option isn’t always wasteful, and the most expensive isn’t always justified. What matters is whether the kit is designed for your specific issue and whether it addresses the problem at its source. Take time to understand what’s driving your hair concerns before spending money on a solution that may only work on the surface.

This article examines oil control, US-led war, economic crisis, and contested US hegemony. Dr Kalim Siddiqui argues that British imperialism installed Gulf monarchies to secure oil—a structure the US later inherited. Contemporary US hegemony, centred on oil and dollar weaponisation, is now contested by Iran’s resistance and renminbi expansion. Declining US power opens space for South–South energy cooperation, de-dollarisation, and pathways toward a decolonised world order.

I. Introduction

Contemporary international political economy remains dominated by Western-centric frameworks that marginalise the Global South, home to most of the world’s population. The deeper challenge is not only resisting imperialism but dismantling the financial structures—such as the IMF, World Bank, WTO, and SWIFT—through which Western powers sustain economic dominance over post-colonial states. This raises a central question: how can Global South nations break free from the lasting legacies of colonialism and Western hegemony?

What Western policy discourse often frames as a dispute over Iran’s nuclear program or regional influence is, in reality, part of a broader system of imperial coercion.

This paper addresses that question through the case of US-led aggression against Iran and its impact on global oil markets. It argues that sanctions, financial exclusion, military threats, and other coercive measures targeting Iran generate instability in crude oil prices, producing inflationary and recessionary pressures across the global economy. These effects are unevenly distributed: while Western economies benefit from currency privilege, strategic reserves, and stronger financial institutions, Global South countries face rising energy costs, currency depreciation, debt crises, and intensified austerity.

What Western policy discourse often frames as a dispute over Iran’s nuclear program or regional influence is, in reality, part of a broader system of imperial coercion. Through global energy markets, pressure on Iran becomes a mechanism that transfers economic instability to vulnerable post-colonial economies. In this sense, oil price volatility functions as an indirect tax on the Global South within a dollar-centred international order.

The article expands the concept of imperial aggression beyond military intervention to include sanctions, financial warfare, and logistical coercion. It traces the link between pressure on Iran and oil price fluctuations using historical and contemporary examples, and examines how oil shocks disproportionately affect Global South economies. Overall, the paper contributes to a decolonised political economy of energy by showing how seemingly neutral market mechanisms reproduce global inequality (Siddiqui, 2018a).

The dominant worldview remains filtered through a Western lens, often marginalising the perspectives and interests of the Global South—home to approximately 86% of the world’s population. To liberate this majority from the enduring grip of imperialism is not merely a political or economic objective; at stake is our shared humanity. The more profound challenge, therefore, lies in emancipating the Global South from the control and dictates of Western financial institutions (Patnaik and Patnaik, 2015). This raises fundamental questions about the prevailing world order: how can nations break free from the shackles of Western hegemony and the lingering legacies of colonial and neocolonial practices? Addressing these questions is essential to understanding how external aggression—particularly against major oil-producing nations such as Iran—can trigger oil price volatility with cascading effects on the global economy.

To emancipate this majority from the persistent grip of imperialism is not merely a geopolitical aspiration; it is, fundamentally, a defence of collective humanity. Yet the deeper challenge resides in dismantling the institutional architectures through which Western financial power exerts disciplinary control over the developmental trajectories of post-colonial states.

The paper critically examines the concept of “imperial aggression” beyond narrow military definitions, incorporating financial warfare and logistical coercion. I argue that the causal chain from Iran-specific pressures to oil price volatility using historical and recent episodes. The asymmetric transmission of oil shocks to Global South economies.

The United States (US) aggression against the Islamic Republic of Iran and the consequent volatility in global oil markets. This article advances a twofold argument. First, external aggression—understood not narrowly as military intervention but expansively to include economic sanctions, financial exclusion, maritime interdiction, and the threat of regime change—produces acute, non-linear shocks in crude oil prices. Second, these price shocks are not transmitted uniformly across the global economy. While core Western states benefit from exorbitant currency privileges, deep derivative markets, and strategic petroleum reserves that allow them to absorb adjustment costs, peripheral and semi-peripheral economies of the Global South bear a structurally disproportionate burden. For these nations, oil price spikes translate directly into ballooning import bills, current account deficits, currency collapses, sovereign debt distress, and, ultimately, intensified social austerity.

Thus, what is routinely framed in Western policy discourse as a bilateral standoff over Iran’s nuclear program or its regional influence is, in reality, a systemic mechanism of imperial coercion. This mechanism operates through global energy markets as a transmission belt, converting geopolitical pressure on a single resource-rich state into generalised economic vulnerability across the post-colonial world. In this sense, oil price volatility functions as an involuntary tax on the Global South—a tax levied not by any formal authority but by the structural logic of a dollar-centred, Western-dominated financial order.

Imperial intervention has a long and recurring history in Iran. Key examples include the 1953 coup against Prime Minister Mossadegh, the U.S.-backed installation of Shah Pahlavi followed by nearly three decades of dictatorial rule, the popular uprising that brought instability and chaos, and the encouragement of Iraq to invade Iran—sparking the eight-year Iran–Iraq War in September 1980. Further interventions include the intensification of sanctions from 2012 to 2016, as well as more recent events between 2020 and 2024.

II. The Political Economy of US Dollar Hegemony, Middle East and Oil Crisis

Donald Trump’s electoral success was largely predicated on his repeated promise to “end the endless wars in the Middle East”—a goal he claimed would be accomplished in one day, with a resolution to the Israel–regional conflict requiring one week. This political mandate reflects a broader US strategic conclusion that the US public no longer supports large-scale land wars involving US troops, not only in Asia but elsewhere (Pappe, 2025).

Much of the existing commentary on US war policy remains narrowly focused on the Israel lobby and neo-conservative actors. Less attention has been paid, particularly by geopolitical issues, to the structural role of the US military-industrial complex, which operates as a powerful domestic constituency for continued intervention.

The US client states in the Gulf—Saudi Arabia, Qatar, Bahrain, and the United Arab Emirates (UAE)—are characterised by a structural asymmetry: they are rich in oil exports but heavily dependent on imports of food, labour and other goods, largely from Asia. Iran has announced that it will deny passage through the Strait of Hormuz, the world’s most critical oil transit chokepoint, to vessels from pro-US countries. More significantly, Iran has declared that Chinese ships—and any country purchasing oil in renminbi—will be permitted passage. This represents one of the most serious challenges to the US dollar’s status as the global reserve currency in recent history.

While the US is a major crude oil producer, it remains dependent on imports of heavy crude, notably from Canada. More broadly, all oil-producing countries rely on imports to secure different crude grades for refining. Consequently, both producing and non-producing nations are dependent on global oil trade.

From a political economy perspective, oil’s systemic importance derives not primarily from its use as fuel but from its role in the circulation of global money (Siddiqui, 2019). The petrodollar agreement of 1973 established with Saudi Arab that oil would be traded in US dollars, thereby securing sustained demand for the currency and stabilising its reserve status. In return, oil-exporting states invested their dollar earnings in US financial assets and Treasury bonds, generating returns for US financial markets and helping to finance US trade deficits. This arrangement is now under threat. A growing number of oil-producing countries have begun to diversify their trade currencies. Russia, Venezuela, and Iran are already conducting transactions in non-dollar denominations, accelerating the erosion of dollar hegemony.

These developments likely signal a broader decline in US geopolitical influence in the Middle East. Recent military interventions may be understood, in this light, as futile attempts to regain control over oil reserves through regime change—resorting to primordial violence in the name of democracy and governance, while accelerating the very decline they seek to reverse.

The war is likely to be protracted, with severe consequences for the global economy. Rising oil and fertiliser prices will drive up food costs worldwide. Food price inflation disproportionately harms the poor, who spend a larger share of their consumption budget on food than wealthier households.

Oil-export-dependent economies that have served as financial safe havens under US military protection will lose their comparative advantage, regardless of the war’s outcome. Meanwhile, the US—increasingly isolated and losing legitimacy as a global power—is seeking to reduce its military expenditures on allied nations. This has already prompted a surge in defence budgets worldwide, crowding out public and social spending and once again hurting the poor. Supply chain disruptions and energy price spikes threaten household consumption, trade, and global growth. The world order is at a crossroads: the empire is in decline, (Siddiqui, 2025a) and the current interregnum signals a massive shift of power from West to East.

Historically, hegemonic powers have been defined by technological dominance, an area where the US is now losing ground. More fundamentally, liberal democracy has reached a new low, as its own rules are deliberately violated by its protagonists. The epitome of capitalism, the US, now resorts not only to institutional mediation and global rules but also to direct colonization and resource extraction to ensure its survival. Facing a deep crisis of legitimacy, it responds with futile vengeance disguised as nationalism—a nationalism born of defeat and decline. No longer representing human progress, it offers only war, blood, and death. The US failed to install puppet regimes in Iraq, Afghanistan, or Libya, and it will not succeed in Iran. The war devastates the conflict zone while sending shockwaves across the global economy. The world’s largest capitalist power has lost its legitimacy and has nothing left to offer but ruins.

It may seem paradoxical that oil accounts for such a small share of the world economy—just 2.3 percent of global GDP in 2023—yet a rise in oil prices can cause massive global disruption. In fact, every other raw material represents an even smaller fraction. This minuscule share has led some writers to question Marxist theories of imperialism that place control over raw materials at their center. However, present developments bear out the continuing relevance of such theories. Only about 20 percent of global oil output (including products) passes through the Strait of Hormuz—roughly 0.6 percent of world GDP. That a disruption to this 0.6 percent can trigger such a profound crisis underscores oil’s critical role in the global economy (The Guardian, 2026).

The dollar, the world’s primary reserve currency, is implicitly tied to oil. This is not to say the dollar price of oil is fixed, but rather that all efforts are made to prevent prolonged expectations of rising oil prices. The stability of the dollar as a reserve currency depends not only on the absence of a credible rival but also on the fact that commodity prices—above all, the price of oil—are not expected to rise permanently in dollar terms. We may no longer operate on a gold standard, but we effectively operate on an “oil-dollar standard.”

At the same time, contemporary geopolitical conflict is accelerating challenges to dollar hegemony. The expanding use of the renminbi is particularly significant. As the largest purchaser of Iranian oil, China increasingly settles transactions in its own currency, while a growing number of states have also adopted renminbi-based trade arrangements. By 2024, approximately 30 percent of China’s external merchandise trade was settled in renminbi.

This shift has been accelerated by the escalating costs of dollar dependence. States and firms that once tolerated the inconveniences of dollar-denominated trade now confront its geopolitical risks directly, as the US weaponise access to the dollar system through secondary sanctions, selective waivers, and blockades that destabilise global energy markets—regardless of a country’s formal relationship with the US. The growing reliance on renminbi settlement therefore reflects not merely economic diversification, but an attempt to reduce exposure to coercive financial power.

However, de-dollarisation through the renminbi and cryptocurrencies constitutes only one dimension of an emerging alternative financial architecture. Beneath formal monetary systems lies a more informal yet equally important network of exchange mechanisms, including hawala systems and barter arrangements. Intensifying sanctions, war, and blockade are likely to push these mechanisms further into the mainstream of regional and international trade, expanding forms of economic coordination that operate partially outside the institutional reach of dollar-centred financial governance (Siddiqui, 2018b).

The US made a serious miscalculation regarding Iran. It now finds itself trapped: rising oil prices threaten dollar stability, the global economy, and the livelihood of working people worldwide (See Figure 1). Popular anger against the system could swell to the point of rebellion—not least because Iran is directly challenging the petrodollar system. For decades, the vast majority of global oil has been priced and sold in dollars. Iran is now challenging that arrangement. In response to US–Israeli aggression, Tehran has closed the Strait of Hormuz—the single most important oil transit chokepoint on Earth. Before the current war, approximately 20 percent of globally traded oil passed through this narrow strait each day (The Guardian, 2026).

Iran’s closure of the Strait of Hormuz—and the resulting surge in global oil prices—is deliberately intended to arouse opposition to the war among Global South countries. It aims to persuade them that the war against Iran is also a war against them, one that will impose severe hardships, and that they cannot remain indifferent. Iranian military commanders have projected oil prices rising to as much as $200 per barrel—a back-breaking prospect for the world’s people, especially in the Third World—unless immediate intervention rolls back the imperialist offensive.

The current silence of Global South governments may prove expensive in an even more sinister sense. As Donald Trump faces domestic popular anger over the inflationary recession triggered by his own increasingly unpopular war, he may seek to shorten the conflict through drastic means—including the use of tactical nuclear weapons against Iran. The US remains the only country ever to have deployed nuclear weapons against another nation. According to the well-known US economist James Galbraith (The Delphi Initiative, March 9), there have been at least three occasions since when internal advice dissuaded the US from repeating that catastrophe. Unless the world firmly opposes the US government and its cynical contempt for international law, a repetition of that drastic step becomes a real possibility.

III. Theoretical Framework: Imperial Aggression, and Energy Domination

Conventional understandings of imperial aggression remain tethered to overt military intervention—troop deployments, aerial bombardment, and territorial occupation. While these forms persist, they constitute only the visible tip of a deeper coercive architecture. This study advances a broader, more analytically powerful conception: imperial aggression as a continuum of structural coercion that operates through economic, financial, and logistical channels to subordinate sovereign states without necessarily deploying uniformed personnel.

Drawing on the tradition of critical International Political Economy (Panitch and Gindin, 2012), I identify three analytically distinct yet empirically overlapping modalities of imperial aggression. First, access to Western-dominated financial infrastructures—such as SWIFT, the Clearing House Interbank Payments System (CHIPS), and correspondent banking networks—is not a universal public good, but a privilege revocable at imperial discretion. Control over access to these systems by the US, whether through sanctions, asset freezes, or outright exclusion, constitutes a form of financial warfare capable of crippling target economies without the deployment of military force. Iran has served as a primary laboratory for the development and application of this strategy.

Second, control over maritime chokepoints (including the Strait of Hormuz, Bab el-Mandeb, and the Strait of Malacca), undersea cables, and global supply chains confers the capacity to asymmetrically strangle resource-dependent economies. Naval deployments, “freedom of navigation” operations, and threats to interdict shipping are not neutral acts of global public goods provision, but explicit exercises in coercive logistics. In the Iranian case, the repeated deployment of carrier strike groups to the Persian Gulf and the interdiction of Iranian oil tankers exemplify this strategy.

Third, unlike genuinely multilateral sanctions authorised by the UN Security Council, unilateral sanctions—or those imposed by “coalitions of the willing”—constitute a form of extraterritorial legal coercion that undermines the principle of sovereign equality in international law. The reimposition of secondary sanctions on Iran following the US withdrawal from the Joint Comprehensive Plan of Action (JCPOA) in 2018 demonstrates how a single state can unilaterally compel third parties, including its allies, to comply with its foreign policy objectives under threat of financial exclusion. This is not diplomacy, it is compulsion.

The relationship between energy and imperial power is neither accidental nor merely instrumental. Oil possesses distinctive structural properties that make it a privileged site of imperial contestation. First, oil reserves are geographically concentrated, with the Persian Gulf accounting for approximately 48 percent of global proven reserves (BP Statistical Review, 2022). Second, oil demand is highly inelastic in the short to medium term, meaning that price shocks transmit rapidly into broader economic contraction. Third, oil is traded predominantly in US dollars, creating a symbiotic relationship between global energy markets and dollar hegemony through the so-called “petrodollar” system (Siddiqui, 2026c)

From this perspective, I propose the energy coercion thesis: control over the production, pricing, and financial settlement of oil constitutes a systemic mechanism of core–periphery domination. Imperial aggression directed against major oil-producing states in the periphery or semi-periphery does not merely affect the targeted state itself; it externalizes instability across energy-importing peripheral economies. The target state is punished directly through sanctions, while the broader Global South is disciplined indirectly through transmitted price shocks. Imperial aggression against a single oil producing state therefore functions as a multiplier mechanism—what Hardt and Negri (2000) describe as a “point of command” through which imperial power radiates across the international system.

This framework challenges both neoclassical and mainstream International Political Economy (IPE) accounts. Neoclassical economics typically treats oil price volatility as an exogenous “supply shock” arising from accidents, wars, or cartel behaviour. By contrast, this account understands such volatility as endogenously produced through imperial strategy. Similarly, mainstream IPE, particularly approaches influenced by hegemonic stability theory, often portrays US military presence in the Gulf that guarantees stable energy supply (Siddiqui, 2025b). Here, this assumption is inverted: US military presence is understood not as a neutral provider of stability, but as a coercive apparatus capable of periodically destabilising supply in order to demonstrate and reproduce credible threat capacity.

Ongoing US aggression generates oil price volatility, but its effects are distributed unevenly across the world-system. This asymmetry reflects the structurally unequal positions occupied by core and peripheral states (Arrighi, 1994). I identify four mechanisms through which oil shocks systematically disadvantage the Global South (Siddiqui, 2025c).

First, oil is priced and settled in US dollars. Peripheral economies earn primarily in weaker local or commodity-linked currencies while paying for energy imports in dollars. As oil prices rise, import costs increase while local currencies depreciate amid “flight-to-safety” capital flows toward US dollar assets. The result is a classic scissors crisis: rising external obligations combined with declining monetary capacity. Core states, by contrast, issue reserve currencies and can sustain persistent deficits without equivalent constraints.

Second, peripheral economies lack the institutional buffers available to core states. Advanced capitalist economies maintain strategic petroleum reserves (SPRs), deep futures markets, and currency swap arrangements that help absorb price shocks. Most peripheral states possess no comparable mechanisms. When prices surge, they cannot stabilise consumption through reserves or affordable borrowing, forcing austerity measures or the accumulation of unsustainable debt.

Third, oil shocks transmit directly into the sphere of social reproduction. In peripheral economies, energy constitutes a larger share of both household consumption and productive activity, including transport, agriculture, and manufacturing. Price increases therefore cascade into food inflation, fertilizer shortages, and rising transport costs, disproportionately undermining subsistence wages and informal livelihoods. Core economies, with diversified production structures and stronger welfare systems, are better positioned to absorb these shocks.

Fourth, there exists a structural debt–energy nexus. Most peripheral sovereign debt is denominated in US dollars. Oil price shocks often strengthen the dollar and raise global interest rates, increasing both the real burden of existing debt and the cost of future borrowing. These dynamics frequently culminate in IMF-led “sudden stop” crises and structural adjustment programs that deepen peripheral dependence on Western international financial institutions.

These dynamics can be synthesized through the concept of the Imperial Energy Complex (IEC): the institutional, military, and financial architecture through which core states—led by the US—maintain systemic control over global energy production, pricing, and payments. The IEC rests on three interconnected pillars: (a) military domination of energy-producing regions and strategic chokepoints; (b) dollar hegemony in oil settlement; and (c) sanctions regimes that transform economic exclusion into an instrument of coercive foreign policy (Siddiqui, 2026c).

Within this framework, Iran occupies a strategic contradiction. As a major oil producer with vast reserves, Iran possesses the material capacity to challenge the IEC through alternative payment systems, non-dollar settlements, and South–South energy networks. Yet, as a heavily sanctioned state, Iran also functions as the principal laboratory in which the IEC develops and refines its coercive instruments. Financial exclusion, secondary sanctions, and maritime interdiction deployed against Iran today establish precedents that can be applied to any Global South state that resists core directives.

The contemporary world order, therefore, is not one of sovereign equality but of stratified vulnerability. Imperial aggression against Iran is not an aberration within global capitalism; it is an expression of the system’s normal operation. The concentration of energy rents in core states depends upon the externalisation of instability and volatility onto the periphery. To understand oil price volatility is therefore to understand the political architecture that produces it. To challenge that volatility requires confronting the Imperial Energy Complex at its structural foundations.

IV. Imperialism, Oil, and Crisis of US Hegemony

Imperialism is a system of surplus value extraction and capital reproduction (Amin 2020)—the highest stage of the capitalist world economy. The study by Narayan and Sealey-Huggins (2017:2387-2388) notes, “neo-liberal globalisation has led us to an impasse in the idea of imperialism. Before the effects of neo-liberal globalisation, imperialism was all so simple. The classical theorisations of imperialism had predominantly seen neo-Marxist theoretically expanded Hobson’s thesis that maldistribution of income in Europe was a key to understanding colonial expansion beyond Europe. Writers such as Luxemburg, Lenin and Bukharin examined how factors, such as the rise of monopoly capitalism and internationalisation of capital and labour exploitation, were directly linked to the expansion of Western imperil empire and inter-imperial conflict in the late nineteenth and early twentieth centuries. At the mid-point of the twentieth century the rise of the US geo-political hegemony and the onset of decolonisation, dependency theory advanced this idea of Western-centred imperial world order. Imperialism now not seen only characterised the territorial expanse of formal western empires, but also the West’s informal economic and military oppression of newly independent countries”. (Siddiqui, 2026a; Patnaik and Patnaik, 2015)

Moreover, the rise in overt militarism and imperialism at the outset of the twenty-first century can be largely attributed to dominant global economic interests attempting to control oil supplies. The Gulf monarchies were originally installed by British imperialists to safeguard British oil interests (see map 1), a period marked by the absence of organised political resistance. During the colonial period, no organised political resistance emerged against British in these regimes. Following Britain’s withdrawal from east of Suez, the US assumed Britain’s role, undertaking the protection of these monarchies. In return, the Gulf states offered to serve US interests, purchased Western weapons, deposited their oil revenues in Western banks, invested in Western real estate, and reinforced the US dollar by pricing oil exclusively in dollars—a mechanism known as the petrodollar system (Siddiqui, 2026b).

Map 1: Middle East Region Map – Key Features

A prevalent narrative holds that US military aggression against Iran, Lebanon, and Syria stem primarily from pressure exerted by Israeli Prime Minister Benjamin Netanyahu and the so-called “Israel lobby.” Scholars such as Jeffrey Sachs and John Mearsheimer argue that this lobby has effectively dragged the US toward war with Iran. I disagree with such a narrative. The US possesses a long history of unilateral intervention in the Global South that predates and exceeds the influence of the Israel lobby, including earlier military actions against Venezuela. While the Israel lobby is undeniably wealthy and influential, it exists and operates largely because its objectives align with the broader structural aims of US imperialism: to subordinate the rest of the world to the needs of US-based corporate capital. Should Israel cease to serve this purpose, its political influence in the US would wane accordingly.

Furthermore, the ongoing confrontation with Iran reflects the US declining coercive capacity. Iran has successfully resisted US pressure through a combination of diplomatic manoeuvring, regional alliances, and military deterrence. These dynamic fits a larger historical pattern: British imperialist has been weakening since the early twentieth century. The First World War—an inter-imperialist conflict—severely weakened the European imperial powers. The ensuing thirty-year crisis, encompassing the Great Depression and the Second World War, strengthened nationalist forces and triggered the process of decolonisation, culminating in independence for India and numerous African countries.

However, no significant anti-imperialist movements emerged in the Gulf region during this period. Britain established new states there—characterised by small indigenous populations and vast oil reserves—primarily to serve its imperial interests. As the US assumed leadership of the Western capitalist world, the state of Israel was established in 1948 with decisive Western backing and subsequently functioned as a key imperial ally in the region. Since Israel’s founding, the traditional Arab hinterland—long distinguished by its civilisation, Arabic language, cultural influence, and historical political continuity—has been subjected to repeated destabilisation and military intervention, from Sudan, Somalia, and Yemen to Iraq, Libya, and Syria. Notably, many of these states had consistently supported the Palestinian struggle for self-determination and independence (Siddiqui, 2024a).

V. Slavery, Colonial Expropriation, and the Global Architecture of Capitalism

David McNally (2025) argues that the development of industrial capitalism cannot be understood solely through the extraction of surplus value from wage labour. Capital accumulation also depended on the systematic super exploitation of colonial and postcolonial regions—achieved through slavery, colonialism, dispossession, and permanent indebtedness. Historically, capitalism emerged as an industrial, global, racialised, and imperial system, inseparable from colonial expropriation (McNally, 2025).

Similarly, the study by Smir Amin (2021) provides compelling evidence of the persistent and large-scale transfer of wealth from the Global South to the Global North through mechanisms of unequal exchange. The research estimates that in 2018 alone, the Global North appropriated approximately US$18.4 trillion from the Global South. This staggering figure results from multiple intertwined forms of surplus extraction, including global labour arbitrage—where wage differentials are exploited across borders—unequal terms of trade in natural resources, and the financial and structural asymmetries embedded in global value chains. Amin’s findings underscore how contemporary global economic arrangements continue to systematically drain value from lower-income economies, reinforcing historical patterns of dependency and underdevelopment.

The origins of capitalist accumulation are deeply tied to colonial plunder. Spanish and Portuguese extraction of African gold and American silver provided the initial foundation for plantation economies integrated into an emerging world capitalist system centred on London. Capital accumulated in London then circulated through imperial networks to finance infrastructure and commercial expansion in Latin America, reinforcing new forms of neo-colonial extraction (Siddiqui, 2024b). Claims that Spain or Portugal should have been the first to transition to capitalism overlook the broader geopolitical and financial structures of the period—including the role of Genoese finance and the transfer of Latin American silver from Iberia to Dutch and English commercial expansion.

Capitalism did not emerge as a self-contained national system later projected outward through trade and conquest. It was global from the outset—constituted through dispossession, slavery, colonial extraction, and the violent reorganisation of labour and nature across continents. Plantations, mines, and extractive complexes were not peripheral to capitalist development; they were foundational to the formation of capitalist social relations and the international division of labour. Mechanised discipline and labour control appeared within these colonial spaces long before the British factory system became dominant.

Following the consolidation of the bourgeois property form, colonial violence and expropriation—processes external to contractual exchange—were legally transformed into legitimate property relations. As Karl Marx (volume I, 1967) argued, once looted land, labour, and resources entered the legal framework of bourgeois property, their violent origins became obscured and normalised within capitalist circulation. Confiscated wealth, once legally codified, thereafter functioned as commodity value within capital’s expanded reproduction. In this sense, legal form did not erase colonial dispossession; rather, it continuously reproduced and legitimised colonial inequality by protecting accumulated property relations.

International law, deeply embedded in the historical development of capitalism, has long reproduced conditions of underdevelopment. Emerging alongside colonial primitive accumulation, international legal forms evolved not to dismantle imperial inequalities but to institutionalise and protect them through the sanctification of property rights. The historical relationship between colonisation and international law thus suggests that international law does not merely fail to prevent underdevelopment—it actively reproduces global inequality by legitimising ownership structures created through colonial expropriation.

The consequences of these inequalities are borne disproportionately by the Global South. Yet dominant interpretations of international law acknowledge such inequalities only when they threaten the reproduction of capitalist class hegemony. Otherwise, poverty, hunger, and social collapse in the Global South are treated as internal or “extra-legal” problems, attributed to the deficiencies of the affected societies themselves. Within this framework, famine in Africa is disconnected from the historical and ongoing enrichment of the capitalist core. Mainstream economist discourse maintains that development will follow if peripheral states comply with the conditions imposed by institutions such as the IMF, WTO, and World Bank—thereby enabling continued forms of neo-colonial control, from French monetary influence over former colonies to foreign monopolisation of Niger’s uranium sector.

To deny this history is not merely to misinterpret capitalism’s origins; it is to politically disarm Marxist analysis. Any theory that separates capitalism from imperialism cannot adequately explain uneven development, racialised labour hierarchies, or the persistence of contemporary forms of primitive accumulation. A Marxism analysis of the modern world must therefore begin not only in the English countryside but equally in the plantation, the mine, the colony, and the machine shop.

VI. Post-War Growth and Neoliberal Decline

The post-war period saw strong growth in Western Europe, North America and East Asia. Most people attribute this to capitalism, but it should instead be credited to two factors: a substantial part of the world had become communist, and another substantial part pursued autonomous national development following decolonisation. The state intervention policy pf the post-war period was abandoned and replaced by free market policy also known as neoliberalism, weakening capitalism most severely in the US and UK. US capitalism lost productive dynamism, de-industrialised, financialised, and generated extreme inequality. (Siddiqui, 2024c).

Neoliberalism has driven global capitalism into a cul-de-sac. It has deepened economic crises, intensified inequalities within and between countries, and increased foreign debt and economic vulnerability. By shifting production from the global North to the Global South, it suppressed Northern wages while keeping Southern wages depressed through rapid productivity gains. The result: rising global surplus relative to wages, weakening consumption, and chronic demand deficits—manifesting as stagnation, precarious work, and hidden unemployment (Siddiqui, 2025d).

The state cannot resolve this crisis. Keynesian solutions require deficits or higher taxes on the wealthy, but globalized finance capital opposes both. With capital mobile and states border-bound, governments that defy markets risk capital flight. Neoliberalism thus produces a crisis it cannot overcome (Siddiqui, 2023).

Neoliberal capitalism—marked by increasingly unregulated markets—has intensified the atomization of economic and political life. It has fragmented the class alliances that once underpinned anti-colonial struggles and weakened the Non-Aligned Movement, which had embodied collective resistance to imperial domination. What was once a coordinated anti-imperialist project has largely been replaced by political accommodation and economic dependency.

This explains the erosion of the rules-based order. Recolonization requires the Global North to shed neoliberal constraints at home while imposing them abroad. Capitalism’s universal promise is exhausted: some may escape stagnation only by deepening others’ subordination. Governments in the Global South accept this because local bourgeoisies integrated with metropolitan capital benefit—while workers, peasants, and small producers lose. Recolonization thus succeeds by fragmenting the anti-colonial alliances that once won decolonisation.Bottom of Form

This decline created deep social divisions and a political crisis in which no established party can reliably win elections, opening the door for Trump. He correctly noted the US economy was struggling but cannot speak the truth: decades of neoliberalism caused this decline. Neoliberalism serves the very classes Trump aims to serve.

To manage the impasse, capitalism turns to neo-fascism: corporate-political alliances that scapegoat minorities. Yet neo-fascism cannot avoid economics. Trump’s strategy, for example, abandons neoliberal orthodoxy for the US while enforcing it abroad—protecting US industry via tariffs and bilateral deals, forcing countries like India to lower barriers and remain subordinate. The goal is to reshore production by exporting stagnation to the global South, resembling colonial treaties and amounting to recolonisation. The same logic applies to oil resource control in Venezuela and Iran. If neoliberalism reversed post-Second World War decolonization, Donald Trump aims to complete it.

Over decades, neoliberalism has eroded both the concept of the nation-state and the principles of non-alignment, stripping them of their anti-imperialist foundations. In their place, frameworks that prioritise alignment with imperial powers and the pursuit of external approval have taken hold. The current situation is a direct outcome of this historical transformation.

Under these conditions, meaningful solidarity with Iran is more likely to come from the peoples of the Global South than from governments that increasingly serve domestic elites and transnational capital. Iran’s confrontation with the US–Israeli alliance thus carries significance beyond the immediate conflict: it raises the broader question of whether the Global South can reclaim political sovereignty and resist external domination.

Historically, imperial powers have treated strategically vital regions—and their resources—not as partners deserving mutual respect, but as spoils to be dominated and exploited. Any major escalation against Iran would likely trigger a sharp rise in global oil prices, given Iran’s control over the Strait of Hormuz, through which roughly one-fifth of the world’s petroleum passes. Such a shock would reverberate across the global economy, fuelling inflation, slowing industrial production, and disproportionately harming energy-importing developing nations. In this sense, efforts to destabilize Iran pose not only a military and geopolitical risk but also a profound economic threat with far-reaching global consequences.

VII. Conclusion

If Iran continues to oppose US and Israeli designs in the Middle East successfully, this would further undermine US imperialism and accelerate the decline of its expansion and control over the oil-rich regions.

This article has argued that control over oil resources, US-led military interventions, and recurring economic crises are central to understanding contested US hegemony today. British imperialism installed the Gulf monarchies as instruments of oil security—a structure the US later inherited and preserved. While some analysts attribute US military actions against Iran, Lebanon, Libya, Sudan, and Syria primarily to the Israel lobby, these interventions reflect a deeper imperial logic: subordinating the Global South to the needs of US corporate capital. Iran’s successful resistance to US coercion is not an anomaly but a symptom of declining US power, consistent with a longer historical arc of imperial weakening since the early twentieth century. If Iran continues to oppose US and Israeli designs in the Middle East successfully, this would further undermine US imperialism and accelerate the decline of its expansion and control over the oil-rich regions. The Gulf’s artificial state system, created by Britain, remains an exception to global decolonisation—yet continues to generate regional destabilisation.

Israel is now fully committed to a Zionist state in which Palestinians possess no rights and can survive only as refugees in neighbouring Arab countries. Backed by Christian Zionists such as Mike Huckabee, the US Ambassador to Israel, Zionist leaders have also declared Israel’s “biblical right” to occupy lands from the Nile to the Euphrates. As long as settler-colonial and ex-colonial states—the US and its European allies—provide weapons, money, and political support to Israel, the crisis of the Middle East will persist (Pappe, 2025).

As this decline in US coercive power accelerates, so too does the search for alternative financial architectures. The growing reliance on renminbi settlement, cryptocurrencies, and barter arrangements—discussed earlier—represents not merely economic diversification but a strategic attempt to reduce exposure to a dollar-centred system increasingly weaponised by the US. These mechanisms, operating partially outside the institutional reach of US financial governance, offer peripheral states tangible tools for resisting imperial pressure.

Finally, I would like to draw three policy-relevant implications: the strategic necessity of South–South energy cooperation; the accelerated pursuit of de-dollarisation and alternative payment systems; and the construction of parallel financial institutions capable of insulating peripheral economies from core–periphery shock transmission. Collectively, this analysis aims to contribute to a decolonised political economy of energy—rendering visible the violence embedded in ostensibly “neutral” market mechanisms, illuminating how contemporary imperialism operates, and charting a plausible pathway toward a more just world order.

Dr. Kalim Siddiquiis an economist specializing in International Political Economy, Development Economics, Trade and Economic Policy. Since 1989, he has been teaching economics at various universities in Norway and the UK. Dr. Siddiqui’s research interests encompass a wide range of topics, including political economy, international trade, and economic history, South Asia, and emerging economies. He has presented papers at international conferences across numerous countries, reflecting his global engagement in the field. His scholarly pursuits span six broad domains: Political Economy, Development Economics, Economic History, Economic Policy, Globalization, and International Trade. Dr. Siddiqui has made significant contributions to research in areas such as trade policy, globalization, and political economy. His work has been published in chapters of edited books and articles published in peer-reviewed journals. For inquiries, Dr. Siddiqui can be reached at: [email protected]

References

McNally, D. (2025) Slavery and Capitalism: A New Marxist History, Berkeley: University of California Press.

Narayan, J. and Sealey-Huggins, L. (2017) “Whatever Happened to the Idea of Imperialism?”, Third World Quarterly, 38(11): 2387-2395.

Panitch, L. and Gindin, S. (2013) The Making of Global Capitalism: The Political Economy of American Empire, New York: Verso.

Pappe, I. (2025) Israel on the Brink: Eight Steps for a Better Future, London: Oneworld Publications.

Patnaik, U. and Patnaik, P. (2015) “Imperialism in the Era of Globalization” Monthly Review 67(3), New York.

Siddiqui, K. (2026a) “Monopoly Capitalism and the Concentration of Capital in Production and Digital Technology”, World Financial Review, January.

Siddiqui, K. (2026b) “The US, the Petrodollar, and Multipolarity: Strategic Intervention in an Age of Monetary Decline” World Financial Review, January.

Siddiqui, K. (2026c) “The Unravelling of Dollar Hegemony: Debt, Rentier Power, and the Crisis of US Global Dominance” World Financial Review, February.

Siddiqui, K. (2025a) “The Reasons Behind the Decline of the US Economy” World Financial Review, May.

Siddiqui, K. (2025b) “Reconfiguring US Hegemony: Militarism, Empire, and the Crisis of Capitalist Accumulation” World Financial Review, August.

Siddiqui, K. (2025c) “Geopolitics and the Persistence of Global Uneven Development: A Critical Analysis” World Financial Review, July.

Siddiqui, K. (2025d) “The US Future in an Imperial Mirror: Lessons from Britain, Spain, Abbasids, Rome, and Beyond” World Financial Review, November.

Siddiqui, K. (2024a) “Palestine, Imperialism and the Settler Colonial Project” World Financial Review, February/March.

Siddiqui, K. (2024b) “Neo-colonialism: An analysis of international factors on the development of the Global South” World Financial Review, December/January.

Siddiqui, K. (2024c) “Political Economy of Globalisation and Issues of Global Governance” World Financial Review, September.

Siddiqui, K. (2023) “Marxian Analysis of Capitalism and Crises” International Critical Thought 13(4): 525-545.

Siddiqui, K. (2019) “Challenges and Importance of Institutions in the Developing Countries” World Financial Review, May/June.

Siddiqui, K. (2018a) “Imperialism and Global Inequality: A Critical Analysis” Journal of Economics and Political Economy, 5(2): 266-291.

Siddiqui, K. (2018b) “David Ricardo’s Comparative Advantage and Developing Countries: Myth and Reality” International Critical Thought, 8(3): 1-28, September.

The Guardian (2026) “Imperialist undertones’: Global South Condemns US-Israeli war with Iran”, 3rd March, London.

A warehouse manager walks the floor and sees pallets stacked with loose bins, strapped together with stretch wrap, shifting every time the forklift moves them. It works, technically. But it’s slower, less stable, and takes up more space than it should. The fix is often simpler than a full rework of the storage system.

Sometimes it’s just the right container, and pallet boxes solve this problem more elegantly than most people realize.

What Makes a Pallet Box Different From Everything Else

A pallet box is exactly what it sounds like: a container with an integrated pallet base and solid walls that functions as both a storage unit and a shipping platform in one piece. No separate pallet needed, no loose bin sliding around on top, or extra strapping to keep things together.

That integrated design helps with stability, handling speed, and floor space. Forklifts pick them up cleanly, they stack predictably, and pallet boxes move through a facility without the improvised rigging that standard pallets with loose containers sometimes require.

Plastic vs. Metal Pallet Boxes: Picking the Right Material

Plastic pallet boxes dominate most general-purpose applications for good reason. They’re lighter, corrosion-resistant, easier to clean, and available in food-grade versions that meet FDA requirements. For produce, pharmaceuticals, food ingredients, and consumer goods, plastic is usually the first and best answer.

Metal pallet boxes hold their ground in heavy industrial environments. Steel construction handles sharp, abrasive, or extremely heavy contents that would stress a plastic wall over time. They also perform better in high-temperature situations where plastic softens and loses structural integrity.

5 Places Pallet Boxes Outperform the Alternatives

Automotive parts: Irregularly shaped components need containment that holds its form under weight. Pallet boxes keep parts organized and protect them better during transport than open pallets with dividers.

Produce distribution: Food-grade plastic pallet boxes are washable, stackable, and built for the cold chain. They move from farm to distribution center without transferring contaminants.

Pharmaceutical returns: Reverse logistics in pharma require clean, documentable containers. Pallet boxes offer consistent specs and easy cleaning between uses.

E-commerce bulk staging: High-volume fulfillment operations use pallet boxes to stage products efficiently before it breaks down into individual orders. The uniform footprint makes slotting predictable.

Cold chain logistics: Consistent wall construction and tight-fitting lids help maintain temperature integrity during transport better than open-top alternatives.

Understanding Pallet Box Specs Before You Buy

Load capacity is the number most buyers check first, and rightfully so. But interior dimensions matter just as much. A box rated for 2,000 pounds is useless if your product doesn’t fit the opening or the floor dimensions don’t match your racking system.

Stack height ratings are frequently overlooked. Most pallet boxes carry a rated stack limit, usually expressed in the number of loaded boxes. Exceeding that limit creates a safety risk that no amount of savings justifies. Verify this spec before committing to a purchase, especially if vertical storage is part of the plan.

Collapsible vs. Rigid Pallet Boxes: The Return Freight Factor

Rigid pallet boxes are the more common choice for facilities where boxes stay on-site or ship one-way. They’re simpler, generally stronger, and less expensive upfront.

Collapsible pallet boxes make financial sense when empty containers need to travel. A collapsed box takes a fraction of the floor and truck space of a rigid one. For operations running closed-loop supply chains in which boxes regularly return to the origin, the freight savings on returns can pay for the price premium in a surprisingly short time.

Where to Shop Pallet Boxes Without Overpaying

When you’re ready to source, it pays to compare across both new and used options. New pallet boxes come with full specs and no history, which matters for regulated applications. Used pallet boxes can deliver the same performance at significantly lower cost for general-purpose storage, and the supply is often plentiful because facilities upgrade or downsize regularly.

It’s best to shop pallet boxes through a dedicated industrial container marketplace, which gives you access to a much wider range of options than a single supplier can offer. You can compare sizes, materials, and price points side by side without committing to one vendor’s catalog.

The Right Pallet Box Pays Back Quickly

Switching from improvised pallet-and-bin setups to purpose-built pallet boxes tends to have a fast payback. Faster handling, fewer damaged loads, better use of vertical space, and a cleaner floor all add up quickly.

Container Exchanger is a North American marketplace where businesses buy and sell new and used pallet boxes across industries. Whether you’re outfitting a new operation or replacing aging containers, it’s a straightforward way to find the right box at the right price without the usual back-and-forth of traditional procurement.

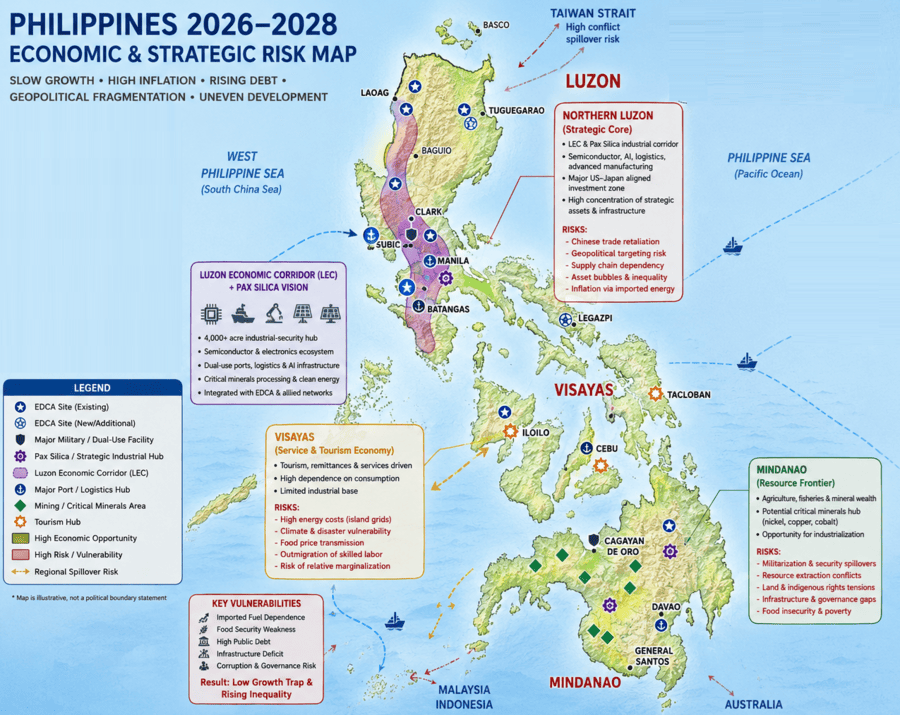

Not so long ago, the Philippines was promoted as Southeast Asia’s most resilient growth story. But as pre-2022 economies policies have been undermined, fundamentals are plunging.