")

Not so long ago, the Philippines was promoted as Southeast Asia’s most resilient growth story. But as pre-2022 economies policies have been undermined, fundamentals are plunging.

The latest GDP data shocked even cautious observers. The economy expanded by only 2.8% year-on-year in Q1 2026, far below expectations and dramatically below the 5–6% growth once considered normal for the country.

Inflation has soared to above 7%. Fiscal deficits remain elevated. Public debt has climbed to the highest ratio in two decades.

As I have warned since January, without a decisive change of course the Philippines risks losing its way.

(Not-so-nice) signs of times

Investment growth has slowed sharply, while household consumption — traditionally the main growth engine — is losing momentum under inflationary pressure.

International institutions struggle to maintain medium-term optimism. Even the IMF remains more cautious after downgrading forecasts due to corruption scandals, infrastructure disruptions and energy shocks.

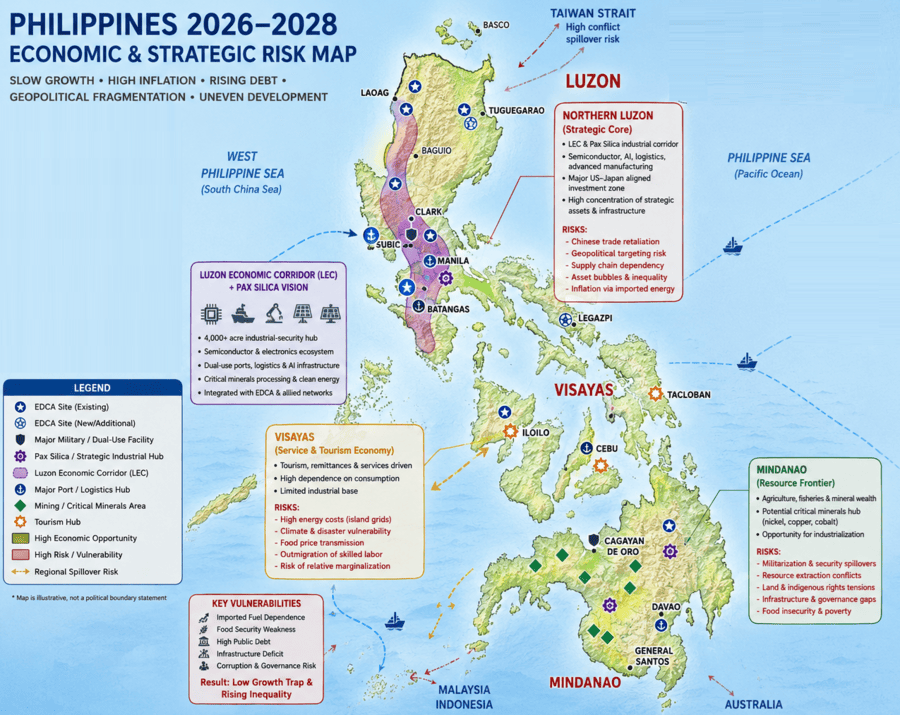

The deterioration matters politically because the Philippines entered 2026 with unusually high expectations. The Marcos Jr. government had framed the country as a future upper-middle-income success story benefiting from supply-chain relocation away from China, as reflected by the Pax Silica gamble.

Instead, the economy has become trapped between high borrowing costs, weakening investor confidence, and deteriorating external conditions.

A more troubling sign is the decline in productive investment. Gross capital formation has weakened substantially, suggesting businesses increasingly doubt the predictability of the policy environment.

Energy, inflation and food insecurity

The inflation surge reflects the Philippines’ high structural vulnerabilities. The country remains highly dependent on imported fuel, making it extremely sensitive to Middle Eastern instability and global shipping disruptions.

Food inflation remains another pressure point. Rice prices had temporarily stabilized in 2025, helping bring inflation down earlier. But renewed energy costs, logistics bottlenecks and climate-related agricultural stress have reversed those gains.

The result is a classic squeeze on lower- and middle-income households. Real wages stagnate while transport, electricity and food prices rise simultaneously. In a remittance-dependent economy, this amplifies dangerous social dynamics.

Overseas Filipino workers continue to support domestic consumption, but migration increasingly functions as a safety valve for weak domestic job creation rather than a supplement to rising prosperity. It is setting the stage for a vicious cycle.

The Bangko Sentral ng Pilipinas faces an impossible balancing act. Tightening monetary policy risks crushing growth further, while easing risks embedding inflation expectations.

How int’l markets are repricing PH risk

Financial markets typically react when several vulnerabilities begin reinforcing one another. That’s the danger now facing the Philippines.

Slowing growth, persistent inflation, elevated fiscal deficits, rising debt-service costs, political fragmentation and intensifying geopolitical exposure together create the conditions for a gradual repricing of Philippine risk across global markets.

Foreign portfolio investors are usually the first to hit the road. In periods of uncertainty, capital tends to migrate away from lower-yield emerging markets toward perceived safe havens or larger Asian economies with deeper industrial bases.

If growth remains stuck near 3–4% while inflation stays elevated, the country risks entering a cycle of weaker capital inflows, peso volatility and declining investor confidence.

Strategic-industrial projects linked to Pax Silica may attract selective US-, Japanese- and allied-backed investment, but broader private investment could remain cautious, particularly in sectors exposed to domestic consumption, retail, office property and speculative real estate.

Exposed property markets

For years, Philippine urban growth relied on condominium expansion, overseas remittance inflows and expectations of permanently rising land values. Yet, prolonged high interest rates, slowing household purchasing power and weaker foreign demand could trigger a multi-year property market deflation, especially in oversupplied Metro Manila segments.

A sustained real-estate correction would weaken bank balance sheets, reduce construction activity and further depress domestic demand. International credit-rating agencies respond negatively when debt ratios climb while growth weakens.

Any downgrade — or even a negative outlook revision — could raise sovereign borrowing costs, increase interest expenses on public debt and force the government to allocate more fiscal resources toward debt servicing rather than infrastructure or social spending.

Higher borrowing costs would spill into the wider economy through more expensive corporate credit, weaker investment and reduced consumer lending.

Corruption and political ploys

Worse, many reports link the slowdown in public investment partly to corruption involving flood-control and infrastructure projects.

This matters because the Philippine developmental model depends heavily on state-led infrastructure spending. Once public works slow, multiplier effects weaken quickly across construction, manufacturing and services.

Political fragmentation is worsening the situation. At a time when ordinary Filipinos feel squeezed and have real concerns about tomorrow, elite factions compete around questions of geopolitical alignment, and US/China security issues.

The debt trajectory also fuels concern. Public debt has reached over 63% of GDP — the highest in twenty years. Yet, the Philippines lacks the reserve-currency privileges and industrial base that allow richer states to sustain large debt burdens.

Scenarios for 2026-2028

Today, three broad scenarios appear plausible.

Hoped for best-case scenario: Growth recovers modestly toward 4–5% by 2027 as inflation eases and infrastructure spending resumes. Pax Silica projects attract targeted investment, but benefits remain concentrated geographically and socially. Debt stabilizes near current levels.

Erosion scenario: Intensifying US-China tensions reduce tourism, trade and investment diversification. Energy prices remain elevated, inflation stays above target, and growth fluctuates around 3–4%. Fiscal pressures worsen and inequality deepens.

Strategic volatility scenario: Without anti-corruption enforcement, infrastructure efficiency and broader technological capabilities, the Philippines risks becoming a frontline platform in a broader US-China conflict. In this scenario, the economy would enter a prolonged period of strategic and economic turbulence.

Philippine peso is the canary in the mine. Historically, “frontline economies” often experience a persistent risk discount in currency markets. Examples include Ukraine before the full-scale war, and Taiwan during major cross-Strait crises when investors demanded higher risk premiums despite strong industrial sectors.

If the Philippines becomes increasingly perceived as a strategic frontline state in US-China rivalry, international markets may similarly price the peso not as an ASEAN growth currency but more as a geopolitical asset.

That would amplify volatility scenarios.

The original commentary was published by The Manila Times on May 11, 2025.

About the Author

Dr. Dan Steinbock is an internationally recognized strategist of the multipolar world and the founder of Difference Group. He has served at the India, China and America Institute (USA), Shanghai Institutes for International Studies (China) and the EU Center (Singapore). For more, see https://www.differencegroup.net

Dr. Dan Steinbock is an internationally recognized strategist of the multipolar world and the founder of Difference Group. He has served at the India, China and America Institute (USA), Shanghai Institutes for International Studies (China) and the EU Center (Singapore). For more, see https://www.differencegroup.net

{kind=link}