Generative AI (Gen AI) is fundamentally transforming industries, reshaping the way professionals innovate, create, and solve problems. These systems, capable of generating text, images, music, and complex solutions, are not just tools—they are catalysts for a paradigm shift in the professional and creative landscapes. For business leaders, this transformation raises pressing questions about the future of work and the evolving definition of human value in a world increasingly driven by Gen AI, with employees suffering from automation anxiety, the fear that their skills may become obsolete.

How Will Gen AI Shift Skills and Values?

Humanity has always prided itself on its creativity, emotional intelligence, critical thinking, and ethical reasoning. These traits have driven innovation and built meaningful relationships. However, Gen AI is challenging these boundaries, producing outputs that rival or surpass human capabilities in areas like content creation, data analysis, generating innovation, and data-driven decision-making.

As AI encroaches on tasks traditionally performed by humans, it forces us to rethink what makes us unique. Historically, identity and value have been tied to specific roles—craftsman, analyst, writer—but these roles are now at risk of being displaced or significantly altered by AI. Instead of viewing AI as a threat, professionals and leaders must focus on areas where human strengths remain indispensable: emotional depth, strategic foresight, and ethical judgment. By embracing this shift, we can redefine what it means to be uniquely human in a technology-driven world.

Declining Relevance of Certain Skills

With Gen AI’s ability to process and generate information at scale, some skills are becoming less critical in the professional sphere. Tasks that rely on repetitive and predictable cognitive functions, such as data entry, summarizing reports, and even basic coding, are now easily handled by AI systems. Similarly, routine problem-solving and decision-making, where inputs and outcomes are clearly defined, are areas where AI consistently outperforms humans in speed and accuracy.

Content creation in isolation is also losing prominence. AI tools like ChatGPT and DALL-E can produce high-quality drafts, designs, and media instantly, reducing the need for human involvement in the initial stages of creation. This does not mean human creativity is obsolete, but its role is shifting from generation to curation and refinement. Leaders must recognize these changes and guide their teams toward higher-order skills that complement, rather than duplicate, AI capabilities.

The Rise of More Human-Centric Skills

As AI takes over routine and technical tasks, uniquely human qualities will become more valuable than ever. Emotional and social intelligence will be critical in roles that require connection, trust, and understanding. Leaders, counselors, and caregivers will continue to rely on their ability to empathize and foster meaningful relationships—skills that machines cannot easily replicate.

Strategic and holistic thinking will also gain importance. AI excels at processing vast amounts of data but struggles with integrating insights into complex, real-world contexts. Professionals who can synthesize information across domains, anticipate long-term consequences, and align decisions with broader organizational goals will remain indispensable.

Creativity, while still vital, is evolving. Instead of focusing on producing content, humans will increasingly act as curators, guiding and refining AI-generated outputs to align with cultural, ethical, and organizational values. Ethical and moral judgment, too, will become a defining skill as professionals navigate the biases and unintended consequences of AI systems, ensuring that decisions driven by AI align with fairness and societal well-being.

Adaptability and learning agility will round out the skillset of the future. With AI technologies evolving rapidly, the ability to learn and adapt will distinguish those who thrive in this new landscape. Professionals and organizations that embrace lifelong learning will be best positioned to stay ahead.

Collaboration Over Competition

The future of work is not about competing with AI but collaborating with it. The most successful professionals will be those who understand how to integrate AI into their workflows, leveraging its efficiency while maintaining human oversight. This synergy—where humans provide vision, ethical guardrails, and emotional intelligence—will unlock new opportunities for innovation and growth.

Despite AI’s capabilities, the “human touch” remains irreplaceable in fields like healthcare, education, and leadership. Trust, compassion, and cultural understanding are essential in these areas and cannot be replicated by machines. Instead of replacing humans, AI serves as an augmentation tool, freeing up time for higher-value activities. For example, marketing teams can use AI to analyze consumer data, allowing humans to focus on crafting strategic campaigns and storytelling.

Leaders should focus on creating systems that enable this partnership. By blending human insight with AI capabilities, organizations can achieve results that neither could accomplish alone. Thriving in the age of generative AI requires intentional preparation. Lifelong learning should become a core value, with professionals continually updating their skills and knowledge to stay relevant. This includes gaining a baseline understanding of AI tools and how to use them effectively, as well as honing uniquely human strengths like empathy, creativity, and ethical reasoning.

Organizations must invest in fostering adaptability within their teams. This means encouraging experimentation, supporting cross-functional learning, and creating environments where employees feel empowered to explore new ways of working with AI. By aligning professional development with the opportunities created by AI, businesses can future-proof their workforce.

Technology literacy will also be essential. Leaders should ensure their teams understand AI’s capabilities and limitations, enabling them to collaborate effectively with these tools while maintaining critical oversight.

Conclusion: Redefining Humanity in a Gen AI World

Generative AI, when deployed strategically and adapted to effectively, is not a threat but an opportunity—a chance to redefine what it means to be human and to elevate our contributions in the workplace. As machines handle routine tasks, humans can focus on what truly matters: connection, creativity, curation, strategic vision, and ethical leadership.

For business leaders and professionals, the key to thriving in this new era is to embrace AI as a partner. By cultivating adaptability, fostering uniquely human qualities, and investing in continuous learning, we can shape a future where technology amplifies, rather than diminishes, our humanity.

The rise of generative AI is not the end of human relevance but the beginning of a new chapter. In this chapter, humans are not just workers or creators—they are curators, strategists, and ethical stewards, guiding technology to serve the greater good. Together, humans and AI can build a future defined by innovation, empathy, and purpose.

In just days, President Trump has caused a meltdown in world markets and undermined global recovery, as he did in 2017. But now his economic weapons are far more destructive, as evidenced by the three rounds of the tariff wars.

The first round of Trump tariffs, which still built on traditional trade wars, involved mainly Canada, Mexico and China. The second round began with “reciprocal tariffs”, which are unilateral, flawed as stated and wrongly calculated. This round covers most trading economies worldwide. But the trade wars will drastically escalate by Trump’s threat of additional 50% tariff against China.

If the first round was dumb, the second was dumber, and the third is most certainly the dumbest. The first round was dumb because it was unwarranted and driven by geopolitics, not economics. The second round was dumber because it was based on flawed formula which has no basis in either economic theory or trade law. Worse, thanks to erroneous calculation, it over-inflated the tariff impact by up to a factor of four, as demonstrated by the American Enterprise Institute (AEI).

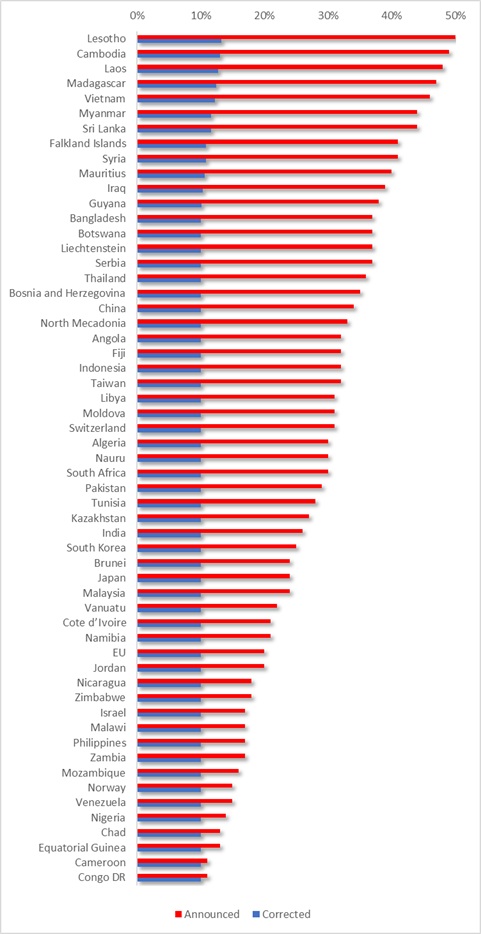

Even if the Trump “reciprocal tariffs” were to be taken seriously, which would be a cardinal mistake, the tariff against Vietnam should be 12%, not 46%; against China, 10% not 34%; against the EU, 10% not 20%, and so on (see Figure).

Figure 1: President Trump’s “Reciprocal Tariffs”: Actual and Corrected

Source: AEI; author

The third round is the dumbest because it builds on unwarranted tariffs, flawed reciprocal tariffs calculated erroneously and, finally, still new tariffs that have more in common with economic blackmail than international cooperation.

President Trump mistakes “medicine” with poison and “negotiations” with paying tribute.

The pre-104% tariff impact on China

What is the impact on China of the accumulative tariffs regarding China (now tariffs above 60%) and the elimination of duty-free for de minimis?

The direct impact of the current US tariffs could shave off up to 1.0% to 1.2% from China’s GDP. This is at par or 20% higher than the initially expected impact. However, it is not the actual impact of the US tariffs.

During Trump’s first term, the tariff war targeted primarily China and a few other trading economies. Now it targets most if not all non-US economies. To a degree, this will reduce the adverse impact on China. Moreover, China is prepared to cushion the US tariff impact in part by fiscal stimulus, monetary easing and structural reforms.

For all practical purposes, the US administration’s decision to eliminate duty-free de minimis treatment for low-value imports seeks to undermine Chinese global low value e-commerce platforms. Yet, these players, including Shein and Temu, are already working with more US sellers and opening warehouses in America.

But the move will prove costly to those Americans who are most reliant on affordable prices. It will hit the hardest American small businesses, the shrinking US and lower-middle-class and particularly working Americans and the laboring poor.

Toward a “global economic pandemic”

How would you evaluate the Chinese retaliation decisions?

Last week, the Trump administration imposed a 34% tariff on Chinese goods, following the 20% rate imposed earlier in the year. Two days later, China imposed a 34% tariff on all U.S. imports. It is a part of China’s full retaliatory package, which includes a 15% tariff on certain US agricultural commodities and 10% on others in March. Additionally, China added 16 US entities to its export control list and another 11 firms into its unreliable entity list, plus import restrictions on rare-earth products.

Relative to the Trump administration’s overblown “reciprocal tariff” measures, China’s responses have been measured, coordinated and broad. The Trump administration has now opened the Pandora’s Box of wholesale decoupling of the world’s two largest economies. That will penalize US consumer, business and investor confidence more than initially anticipated. In the process, the probability of an impending US contraction is likely to increase substantially.

If President Trump will carry out his threat to raise the tariff on Chinese goods by an additional 50%, global economic prospects may face a new kind of global pandemic.

Death of outsourcing?

What about the extreme tariffs regarding Vietnam, Laos, Malaysia and Cambodia. Is this the end of the outsourcing model?

With the Trump administration’s uncertainty and weaponization of tariffs, it is premature to presume any final trajectories. The Trump administration is targeting Cambodia with 49%, Laos with 48%, Vietnam with 46% and Malaysia with 24% tariffs. Calculated right, these tariffs should be 13% to Cambodia, 13% to Laos, 12% to Vietnam and 10% to Malaysia. But Trump tariffs are devoid of economic rationality.

India was taken back by the US’s 26% reciprocal tariff, which exceeds the current tariff gap by more than 2.5 times. But Indian policymakers seek to avoid retaliation, hoping first to gain a bilateral trade agreement with the US and then lower the effective tariff rate.

The message is loud and clear: Those countries that are most exposed to the United States are now the most vulnerable to inflated, illicit and erratic trade measures.

The dissipation of almost $7 trillion in the US markets in just two days is a prelude to more extensive market losses and volatility. Such losses will translate to a broad and deeply adverse impact on the real economy.

How will Southeast Asia respond?

Why aren’t Southeast Asian states retaliating?

The simple answer: By staying united. On Monday, Malaysian Prime Minister Anwar Ibrahim called for Southeast Asian countries to “stand firm together” after they were among the hardest hit by US tariffs. These words matter since Malaysia is this year’s rotating chair of the 10-member Association of Southeast Asian Nations (ASEAN). As Anwar put it, “We must stand firm together as ASEAN, with a population of 640 million and an economic strength that is among the top in the world.”

But Southeast Asia is very diverse. Exporters like Vietnam, Cambodia and Laos, even Thailand and Malaysia are taking disproportionate hits. More insular, large commodity producers like Indonesia are no longer immune. Advanced tiny states such as Singapore seek to hedge bets with cautious balancing. In the Philippines, the pro-US Marcos Jr dreams of trade exemptions, in exchange for geopolitical concessions.

For now, ASEAN nations are trying to avoid tit-a-tat tariffs against the US. But if US tariffs prevail and escalate, this stance will be harder to retain. Worldwide, US trade wars will reinforce regionalization; no longer globalization.

Would East Asian MNCs opt for “Americanization”?

Do you think the big Japanese, Taiwanese and South Korean multinationals will delocalize for US soil?

A full-scale “Americanization” of East Asian multinationals (MNCs) would make these companies even more exposed to future US tariff and non-tariff measures, which is very much not in the interest of these companies and the sovereign countries in which they are headquartered.

As the Taiwanese semiconductor giants have seen in the past few years, full localization in the US could undermine their technological competitiveness – which is precisely why President Trump and his trade authorities seek to localize those MNCs in America.

These East Asian MNCs are all US’s major non-NATO allies. So, when the Trump administration imposed 32% tariffs on Taiwan, 25% on South Korea and 24% on Japan, it came as a major surprise to each. And the timing is challenging. In Taiwan, domestic divides are on the rise. South Korea is heading to election amid a lingering constitutional crisis. Japan is struggling to keep its economic focus.

In the past, US military allies were seen as preferred trade partners and vice versa. That era is now gone. The ongoing trade wars are multidimensional. But so will be the responses.

Toward global contraction?

How do you see the next chapter of ongoing trade war between Trump and his adversaries?

If President Trump will carry out his threat to raise the tariff on Chinese goods by an additional 50%, China will retaliate accordingly.

The Trump administration is not imposing tariffs. It seeks to charge economic rents it is not entitled to.

From the Chinese perspective, the Trump tariffs have little or nothing to do with economics, which most international economists would agree with. They regard those tariffs as blackmail and bullying, at the expense of the Global South.

Dr. Dan Steinbock is an internationally recognized strategist of the multipolar world and the founder of Difference Group. He has served at the India, China and America Institute (US), Shanghai Institutes for International Studies (China) and the EU Center (Singapore). For more, see https://www.differencegroup.net

The current world population of over 7 billion people is estimated to increase to 9.8 billion by 2050. How would we solve this looming problem of food insecurity if sustainable and innovative approaches such as greenhouse farming are not employed?

Everything has evolved, including farming and agribusiness. The basic tenets have remained unchanged, but the way it has been done has through iGrow News. The change is necessary to meet the increasing food demand and to curb the effect of climate change on food security. Managing fresh food supply chains presents major challenges owing to specific characteristics, such the perishability of food items. Some of these chains are marked by increasing concerns about food quality and safety, alarming levels of food waste and food loss, and lack of economic sustainability.

The rate of product deterioration can be faster depending on the condition of the product and its environment and can also be largely affected by supply chain’s design and planning, since it affects the duration that products spend in each facility and vehicle. That means perishable products should be harvested, procured, processed, and marketed in a timely manner to avoid a set of negative consequences to these supply chain players, society and environment, such as catastrophic waste volumes, financial crises for farmers, societal distress, and economic losses across the marketplace.

Technology has, however, offered a solution to this through greenhouse market farming. The effects of climate change on agriculture will depend on the rate and severity of the change, as well as the degree to which farmers and ranchers can adapt. U.S. agriculture already has many practices in place to adapt to a changing climate, including crop rotation and integrated pest management.

Faced with increasing weather unpredictably, many growers are erecting greenhouse structures to grow their crops and even raise animals. When combined with farm management software for highly efficient operations, new technology in greenhouse structures and controlled environment growing techniques represent a scalable solution to sustainable food production.

Climate Change, Sustainability and Greenhouse Farming

While extreme weather conditions have always been part of farming, global warming caused by increasing greenhouse gases in our atmosphere is contributing to more frequent and extremely unfavorable weather events and threatening global food security. According to the United Nations, the planet is averaging 1.1 degrees Celsius above pre-industrial temperatures. While that may not seem like a lot, increased air temperatures change traditional weather patterns, causing more catastrophic heat waves, extreme precipitation events and other weather-induced events, like rising sea levels from melting glaciers.

Greenhouse farming is seen as one solution to combat all these changes. Greenhouse structures can mitigate high and low temperatures while growing food in regions where food production wasn’t previously possible, thereby reducing carbon emissions due to transportation, lessening the impact of supply chain shocks, and conserving water and nutrient use as compared to traditional agricultural production.

Types of Greenhouse Farming

Greenhouse farming can be accomplished using multiple types of structures, depending on the goal and needs of the farming operations. They vary depending on the system, the material used to cover them and the construction technique.

1. Hoop Houses and Poly Tunnels

Hoop houses, also known as polytunnels, are greenhouses built on a hoop. The hoop frame can be made of any appropriate materials. Bamboo is traditionally used in hoop houses built in regions of the world where bamboo grows abundant. Hoop houses are relatively inexpensive to build and can be erected as temporary, seasonal structures or even designed to be portable. Many hoop houses are built so side walls can be lowered and raised, which allows natural airflow to lower temperatures and reduce humidity. Because of their low cost, flexibility and ease of construction, hoop houses are popular structures for lower budgets and simpler management goals.

2. Polycarbonate and Glass Houses

Because of the solid nature of polycarbonate and glass, greenhouses built with these materials are built on structures with flat or angular roofs, not hoop frames. Polycarbonate and glass are more expensive to install but longer-lasting than plastic-covered hoop houses. They are more commonly seen in commercial greenhouse house enterprises. The frame configurations for a polycarbonate or glass house come in many forms, including gable, flat arch and gothic styles. Sometimes, a greenhouse might be installed with polycarbonate side walls but a polyethylene roof.

3. Shade Structures and Screen Houses

Shade structures are used to cool temperatures and limit the sunlight a crop receives. Shade structures are beneficial for fast-growing greens, such as lettuce or baby salad greens, susceptible to sweltering weather. Shade structures are covered with a woven material that blocks sunlight. Because the material doesn’t tear as plastic does, it can be built over hoop frames or frames with more angular edges. Screen houses are helpful in areas with serious pest problems or with high-value crops susceptible to pest pressure.

Greenhouse technology helps farmers maximize land space for food production, especially in vertical farming systems. Having learned the benefits of greenhouse farming, these concepts are important to know if you intend to adopt greenhouse technology.

By Marcelina Horrillo Husillos, Journalist and Correspondent at The World Financial Review

President Donald Trump said the U.S. will “go as far as we have to go” to get control of Greenland.

However, Greenland is not terra nullius ripe for American colonisation. The island is part of Denmark (a NATO member) and indigenous Greenlanders possess a right of self-determination. Moreover, any use of US military force to take Greenland would be in violation of both the 1949 North Atlantic Treaty on which NATO is founded and the 1945 United Nations Charter.

In recent weeks, Trump also said that the 2.1 million Palestinians should be moved out from Gaza to Arab states like Egypt and Jordan following Israel’s war with Hamas, controversially proposing that the US take control of the Strip and turn it into a Middle Eastern “Riviera.”

Although presented as a supposed gesture of generosity, global public opinion has rightly pointed out that permanently forcing Palestinians to leave Gaza would constitute ethnic cleansing, and the acquisition of Gaza by the US or Israel would amount to annexation. Both actions are profoundly illegal under international law.

International humanitarian law unequivocally prohibits the forced transfer or deportation of populations under occupation. Article 49 of the Fourth Geneva Convention states: “Individual or mass forcible transfers, as well as deportations of protected persons from occupied territory to the territory of the Occupying Power or to that of any other country, occupied or not, are prohibited, regardless of their motive.” Articles seven and eight of the Rome Statute of the International Criminal Court defines forcible transfer as a crime against humanity and a war crime. Moreover, such displacement undermines the foundational norms of international law.

The Declaration on Principles of International Law declares that “no territorial acquisition resulting from the threat or use of force shall be recognized as legal.” Trump’s Greenland and Gaza Statements clashes with the Declaration on Principles of International Law, which declares that “no territorial acquisition resulting from the threat or use of force shall be recognized as legal.” Furthermore, indigenous peoples also have a right to self-determination as part of their collective human rights.

Gaza

The Trump Organization’s growing real estate business interests in the region revived an idea previously touted by both him and his son-in-law, Jared Kushner. Both Trump and Kushner are clearly keen on the idea of developing Gaza in terms of a real estate project, rather than as a home for the more than 2 million Palestinians who currently live there.

In the last few years, The Trump Organization, the real estate and hospitality conglomerate currently run by Trump’s sons Eric and Donald Junior, have struck several agreements with Saudi Arabian real estate company Dar Global, the international arm of Saudi Arabia’s Dar Al Arkan Real Estate Development Company.

A luxury Trump-branded hotel and golf resort in Oman is in development, while The Trump Organization and Dar Global have announced plans for two Trump Tower projects, in Jeddah, Saudi Arabia and in Dubai, United Arab Emirates.

A previous Trump Tower for Dubai, comprising of a hotel and apartments, was announced in October 2005. However, the project was cancelled in 2011 due to the global financial crisis.

Trump already owns a golf club in Dubai, which was opened in 2017. The Dubai golf club was built in partnership with DAMAC Properties, run by Hussain Sajwani. In January 2025, Sajwani appeared alongside Trump at a press conference where it was announced that DAMAC would invest “at least” $20 billion (€19.39 billion) to build new data centres across the US.

Following World War II, the international community adopted the four Geneva Conventions of 1949, which form the cornerstone of international humanitarian law, regulating the laws of war and occupation. Today, 196 states – including the US and Israel – have ratified the Geneva Conventions.

Article 49 of the Geneva Conventions prohibits an occupying power from forcibly transferring or removing people from a territory. This is one of the foundations of international law since the creation of the United Nations. Forced displacement is recognized as an unacceptable consequence of wars, and its prohibition is meant to remove any political incentives for an acquisitive power to cleanse part or all of an indigenous population from its homeland.

Hence the US could only take control of Gaza with the consent of the sovereign authority of the territory. Israel can’t cede Gaza to the US. The International Court of Justice has ruled that Gaza is an occupied territory – and that this occupation is illegal under international law.

Greenland

Trump’s interest in Greenland is framed around US security. The island is strategically located in the GIUK (Greenland-Iceland-United Kingdom) Gap. The gap gained prominence during the Cold War as an area where Soviet nuclear submarines could operate in the Atlantic Ocean proximate to the US and its NATO partners. Denmark’s limited naval capacity meant these Soviet submarine incursions were uncontested.

Washington has always appreciated the strategic significance of Greenland. It was used during the second world war as a US military staging point due to its relative safety from the European theatre of war and its capacity as a stopover for aircraft to refuel.

Later, during the Cold War, the Thule US Airbase was constructed on its northwest coast, later becoming the Pituffik Space Base.

Trump is particularly concerned about Russian and Chinese ships operating offshore near Greenland in the Arctic Ocean, and with ensuring US access to rare earth minerals on the island.

The island is recognised as Danish territory. Any dispute over a Danish claim to the island was resolved by an international court in 1933, and since that time Denmark has overseen Greenlandic affairs without challenge. Any suggestion Denmark’s sovereignty over Greenland is contested has no foundation.

While Denmark has been a colonial power, there has been an active process underway to grant the 57,000 Greenlanders increased autonomy from Copenhagen. Home rule has been granted, a legislature has been created, and a road map exists for self-determination that may eventually see the emergence of an independent Greenland.

All five parties in Greenland‘s parliament have united to reject US President Donald Trump’s calls to take over the strategically important Arctic Island. Seeking to honour the responsibility Copenhagen feels for ushering Greenlanders through this process, Denmark has made clear that Greenland is not for sale.

International Law

International law prohibits annexation for several key reasons, including: use of force; violation of a state’s sovereignty and of a peoples’ right to self-determination; national security concerns, and violations of jus cogens norms—fundamental principles of international law that cannot be overridden.

In addition, the Organization of American States deemed the use of coercive economic measures as an illegal use of force. Article 20 of its Charter notes that “no State may use or encourage the use of coercive measures of an economic or political character in order to force the sovereign will of another State and obtain from its advantages of any kind.”

In 1932, the United States also adopted the Stimson Doctrine, which declared that territorial changes achieved through forceful annexation would not be acknowledged as legitimate. In other words, the United States refused to recognize such actions as lawful territorial claims.

When a state declares annexation on its own, the international community usually doesn’t recognize the act. The annexing state often faces legal consequences like sanctions or global condemnation.

The spectre of Trump’s earlier defiance of international norms looms large, fuelling concerns that legal frameworks may again be swept aside. In his first term, Trump unilaterally recognised Israeli sovereignty over occupied East Jerusalem and the Golan Heights, sweeping moves that directly contravened decades of international consensus. Both actions were rejected by the United Nations General Assembly, the Security Council and the International Court of Justice, as well as by a majority of states, which deemed the annexations to be violations of international law. If Trump’s Gaza scheme is anything to go by, he seems utterly unperturbed and ready to flout international law entirely if it suits him.

In what respects to Trump’s plans for Greenland, assuming Denmark agrees, the US can’t simply buy Greenland now. Especially not without the consent of the Greenlanders. Anything else would violate their right to self-determination. You can no longer sell off parts of a state territory. While the right to self-determination under international law is a more recent development, it goes back to the idea of popular sovereignty emerging during the Enlightenment. Accordingly, a monarch could no longer dispose of parts of his territory at will, even if this understanding was initially limited to European territory. The 20th century then saw the development of a general right to self-determination under international law, which is mentioned in the UN Charta and in the first article of both UN Human Rights Covenants. It provided the basis for decolonization during the postwar period. In 2019, the International Court of Justice reaffirmed its validity.

The Nasdaq Composite looked set to confirm a bear market Friday, plunging more than 20% from its record high in December, as an escalating tariff war between the U.S. and China sent shockwaves through global markets and threatened to derail the AI-driven tech boom.

The tech-heavy index, which hit a record close of 20,173.89 on December 16, was last down 3.6% Friday following China’s announcement of 34% tariffs on U.S. imports. The move was a retaliatory strike against sweeping levies imposed by President Donald Trump earlier in the week. The Nasdaq’s decline now marks its worst stretch since the Covid era.

“The tech sector is staring down the barrel of a recession,” said Wedbush analyst Dan Ives. “If these tariffs stand, we’re looking at a 15% hit to tech earnings and a supply chain nightmare rivaling 2020.”

The pain extended across Wall Street. The Dow Jones Industrial Average was on track to confirm a correction—down 10% from its high—while the S&P 500 has slumped 15.3% from its record.

The market’s most influential tech names—Apple, Amazon, Alphabet, Meta, Microsoft, Nvidia, and Tesla—are taking the hardest hits. An ETF tracking these so-called “Magnificent Seven” has cratered 27.6% since December.

Apple, with its vast manufacturing base in China, has fallen 12% since Wednesday, facing the brunt of a 54% combined tariff rate. Meta and Tesla are down 12.4% and 13.1%, respectively, while Nvidia, the face of the AI revolution, has slid 13.6% amid worries of a slowdown in data center investment.

“Big tech is now in a triple bind—regulatory scrutiny, supply chain disruption, and global economic uncertainty,” said Michael Ashley Schulman of Running Point Capital. “A 34% tariff from China forces companies to rework pricing, margins, and even where they make their products.”

Tesla also faces growing public backlash in Europe over Elon Musk’s increasing political involvement as a senior advisor in Trump’s administration. Meanwhile, PC makers and server suppliers have been hammered by soaring electronics tariffs. Dell and HP are down 22.3% and 19.1% this week, while Hewlett Packard Enterprise has lost nearly 22%.

Ives called the tariffs a “bad science experiment,” warning they could crush the AI revolution and cause an “economic Armageddon.”

As the world’s two largest economies dig in for a prolonged trade fight, investors are bracing for more volatility—and an uncertain future for the tech sector that has powered markets for the past decade.

As geopolitical tensions rise, Dr. Kalim Siddiqui examines the shifting power dynamics between the United States and Europe, particularly in the context of the Ukraine conflict. This article explores how the U.S. might be abandoning Europe in favor of a multipolar world order, with significant implications for global security and cooperation.

I. Introduction

This article explores the origins of recent conflicts, particularly Ukraine in the context of the declining dominance of the Western world, particularly the United States (US). It argues that contemporary geopolitical tensions arise from this power shift, driven by technological advancements and economic convergence. Advocating for a transition to multipolarity and multilateralism, this paper highlights the limitations of the US’s continued pursuit of hegemony and underscores the benefits of global cooperation (Siddiqui, 2020a). It contends that a future characterized by peace and shared development can only be achieved through international collaboration and respect for diversity.

Donald Trump’s policy toward Ukraine is expected to differ from that of the Biden administration. This shift is not merely a reflection of Trump’s personal views but rather an acknowledgment by US policymakers that the US has manoeuvred itself into a precarious position. The US now faces a difficult choice: either escalate the war in Ukraine—potentially to the point of nuclear confrontation—or gradually retreat from its hegemonic ambitions. Efforts to force Russia into submission have largely failed. Ukraine has steadily lost territory to Russian forces, and the economic sanctions imposed by the US and the European Union (EU), which were intended to “reduce the rubble to rubble,” have not had their intended effect. The rubble has regained its value against the dollar, surpassing pre-sanction levels.

Russia’s legitimate demands for the recognition of its sovereignty have been largely disregarded, while the US has shown little concern for Russia’s strategic interests.

More than three years have passed since Russian troops invaded Ukraine on February 24, 2022. The war has resulted in over 50,000 deaths, countless injuries, and the displacement of millions (Siddiqui, 2022a). However, the notion of a unified European foreign policy on Ukraine remains unrealistic. A sustainable resolution would require Ukraine to undergo de-Nazification, democratization, and the formation of a neutral government that is acceptable to the US, the EU, and Russia. Russia’s legitimate demands for the recognition of its sovereignty have been largely disregarded, while the US has shown little concern for Russia’s strategic interests. The roots of Russophobia can be attributed to two key factors: Russia’s vast natural resources, which position it as a potential rival to the West, and the US’s broader objective of maintaining a unipolar world order in which no dissent is tolerated. Notably, in 2007, President Vladimir Putin proposed a framework for a peaceful Europe at the Munich Security Conference, but Western leaders dismissed his initiative.

II. NATO Expansion and the Geopolitical Consequences of US Influence in Europe

NATO was established in 1949 as a military alliance against the Soviet Union, making it a Cold War institution. However, following the Soviet Union’s collapse in 1991, NATO was not dismantled. Instead, it expanded eastward toward Russia’s borders, directly contradicting assurances given to Soviet leader Mikhail Gorbachev on February 7, 1990, when the US explicitly promised that NATO would not expand. In response to this commitment, the Soviet Union agreed to the reunification of Germany, and the Warsaw Pact was dissolved. The Warsaw Treaty Organization, established on May 14, 1955, by the Soviet Union and seven other Eastern Bloc countries, was originally intended as a counterbalance to NATO.

Despite its initial assurances, the US proceeded with NATO expansion, incorporating former Eastern Bloc countries into a US-dominated neoliberal order (Siddiqui, 2024a). It openly supported and financed colour revolutions, particularly in Ukraine, to weaken democratically elected governments that did not align with Western interests. Through these efforts, the US facilitated the rise of a Ukrainian government that was sympathetic to American geopolitical objectives in the region (Foy, 2024; Siddiqui, 2022a).

On February 28, 2025, during a meeting in the Oval Office of the White House, US President Donald Trump and Vice President J.D. Vance humiliated Ukrainian President Volodymyr Zelensky, refusing to provide any security guarantees. Regarding the Ukraine crisis, Europe remains divided, lacking a unified stance. Historically, European countries have managed to maintain cohesion under US leadership, but without American influence, sustaining unity on major international issues becomes significantly more challenging (Chotiner, 2025; Sabbagh, 2025).

The current geopolitical situation in Central Europe presents risks even more severe than those of the Cold War, as the threat of nuclear confrontation could have catastrophic consequences (Siddiqui, 2023a). Furthermore, a potential US withdrawal from Europe could cause the continent to regress into a pre-1940 era of political rivalries and conflicts. Historical precedent suggests that, in the absence of US influence, European nations may once again descend into internal tensions, competition, and instability. For over 500 years, the rise of European powers has been marked by wars, slavery, indentured labour, colonialism, resource exploitation, and famines in the Global South (Siddiqui, 2020b).

III. Brzezinski’s Geopolitical Strategy and the Implications of European Rearmament

Zbigniew Brzezinski’s (1997) strategy for restoring and extending US dominance appears to align with the views presented in Samuel Huntington’s Clash of Civilizations (1993). While Brzezinski addresses global geopolitical challenges, his analysis devotes relatively little attention to Africa and Latin America, instead focusing primarily on Europe and Asia. He strongly advocates for further European integration and the eastward expansion of NATO, emphasizing that maintaining US hegemony requires strategic control over the Eurasian landmass (Brzezinski, 1997).

However, Brzezinski’s study (1997) overlooks several critical developments, particularly the rising economic power of emerging economies and their growing influence on global geopolitics. His perspective is primarily shaped by US strategic military considerations, particularly how the US can expand its dominance over Eurasia and the Global South. He supported NATO’s eastward expansion under the assumption that Russia would not respond militarily. However, this assumption proved flawed, as demonstrated by the 2014 US-backed overthrow of Ukrainian President Viktor Yanukovych during the so-called Revolution of Dignity, which followed months of protests against his administration.

The rearmament of Germany is likely to have significant consequences, including a rise in authoritarianism, a deepening economic crisis, and the growing influence of the far right. Increased military expenditures will necessitate drastic reductions in social spending, exacerbating inequality and fuelling domestic tensions. Furthermore, rearmament across Europe may weaken the European economy, as higher defence spending will lead to further budget cuts and austerity measures (Siddiqui, 2017). These policies will disproportionately affect the majority of the population, while benefiting a small elite through tax cuts and corporate subsidies (Siddiqui, 2024a).

Historically, whenever capitalism encounters economic stagnation, centre-left political parties often shift toward the political centre in an attempt to preserve stability. However, such compromises frequently open the door to authoritarianism and the resurgence of far-right movements, resulting in heightened attacks on minorities and other marginalized groups.

The current socio-economic crisis in Europe has already contributed to the rise of far-right parties such as the neo-Nazi Alternative for Germany (AFfD), alongside similar movements across the continent. Many of these groups express hostility not only toward refugees from outside Europe but also toward immigrants from within Eastern Europe. The emergence of neo-fascism in advanced capitalist countries has been marked by increased repression and a reallocation of public funds from welfare to military spending. At the same time, the United States has sought to reassert its control over the natural resources of the Global South under the neoliberal order. Notably, figures such as Donald Trump have made overt claims about acquiring territories like Greenland, exploiting Ukraine’s natural resources, and even developing Gaza for real estate and tourism purposes—highlighting the imperialist ambitions behind such rhetoric.

Furthermore, the US and the UK played a significant role in undermining the Minsk Agreement, a diplomatic effort between Russia and Ukraine that could have averted the ongoing war. NATO’s broader strategy appears aimed at subordinating Russia and gaining access to its vast natural resources, reminiscent of the Western alignment with Russian President Boris Yeltsin during the post-Soviet 1990s. The Western narrative that Russia seeks to conquer Europe mirrors the propaganda of the Cold War era, when similar claims were made about the Soviet Union. These assertions lack a factual basis and serve to justify militarization and geopolitical confrontation rather than peaceful diplomacy (Siddiqui, 2022a).

IV. The Decline of the Welfare State and the Burden of Military Spending in Europe

In the post-war period, communist parties emerged as the second-largest political forces in many European countries. In response to the geopolitical landscape of the time, the US agreed to provide military protection for Europe, allowing European governments to focus their resources on social welfare spending rather than defence expenditures. This arrangement was part of a broader Keynesian economic strategy, in which increased US military spending functioned as a stimulus for economic growth (Siddiqui, 2022b).

However, the current geopolitical landscape is shifting. European unity is weakening, and the US is facing financial constraints, unable to sustain the rising costs of military expenditures. As a result, the US has pressured European nations to increase their own defence budgets. The failure of the US and Europe to defeat Russia in Ukraine has led countries like the United Kingdom (UK) and France to assert that they can achieve this objective independently. To do so, they plan to significantly increase their military budgets (Siddiqui, 2024b).

Currently, in the EU, higher education and healthcare remain freely accessible to citizens. However, expanding military budgets will require significant cuts to social spending, mirroring recent policies in the UK, where reductions in higher education funding, healthcare services, and workers’ benefits have been implemented to finance defence expenditures. This shift threatens to dismantle the welfare state, undermining workers’ rights that were won through decades of political and social struggle.

Following World War II, much of Europe lay in ruins. However, rapid reconstruction was facilitated by free access to US markets and technology, along with Marshall Plan aid. Even former adversaries such as Germany and Japan benefited from this economic assistance. At the time, the US was keen to foster European prosperity, improving living standards while ensuring that European countries remained loyal junior partners to the US. Today, however, Europe allocates between 20% and 40% of its GDP to social spending, benefiting from relatively low defence expenditures—a model that is now under threat.

John Mearsheimer, in his book (2001) The Tragedy of Great Power Politics, argues that the Ukraine conflict is the result of US provocations. His perspective, rooted in realist international relations theory, asserts that the best guarantee of a state’s survival is to achieve hegemony, as no rival power can then pose a serious threat. However, history has shown that when all major powers seek hegemonic dominance, it results in endless conflicts. According to Mearsheimer, true global hegemony is unattainable, meaning that the world is perpetually condemned to great power competition and recurrent wars (Mearsheimer, 2001).

V. Global Economic Changes

To understand the significance of economic factors in security considerations, it is essential to examine the evolving economic dynamics between the US and the European Union (EU). Since 2020, the US has experienced real economic growth of approximately 10%—three times the average growth rate of other G7 countries. In addition to prioritizing competition with China, the Trump administration has sought to reduce military spending on European security (Sabbagh, 2025). The relatively weak economic performance of European economies compared to the US appears to be another reason for Trump’s inclination to sideline European countries in negotiations with Russia over Ukraine. Among G20 nations, including BRICS countries, the US stands alone in exceeding pre-pandemic projections for both economic output and employment (Siddiqui, 2016). According to the most recent IMF Report (2025), US economic output per capita is now approximately 40% higher than that of the EU and Canada and 60% higher than that of Japan—roughly double the gaps observed in 1990. The US benefits from its vast natural resources, large consumer base, and deep capital markets, allowing businesses to scale efficiently and distribute products across the country.

The relatively weak economic performance of European economies compared to the US appears to be another reason for Trump’s inclination to sideline European countries in negotiations with Russia over Ukraine.

The EU, by contrast, faces structural economic limitations. Politically fragmented and lacking independent oil and gas resources, its economic potential remains constrained. Although the EU operates under a so-called single market, significant intra-EU trade barriers persist due to national differences in taxation, professional regulations, and legal frameworks. Additionally, the fragmentation of European capital markets limits investment opportunities. Furthermore, demographic challenges—including an aging population and increasingly restrictive immigration policies—exacerbate labour shortages. Europe’s heavy reliance on energy imports also leaves it vulnerable to fluctuations in oil and gas prices (Chotiner, 2025).

The collapse of the Soviet Union briefly allowed the US to assert unparalleled global hegemony. However, China’s accession to the World Trade Organization (WTO) in 2001 profoundly altered the global economic landscape (Siddiqui, 2015). The implementation of Structural Adjustment Programs (SAPs), a cornerstone of neoliberal economic policy, has had divergent effects on economies worldwide. While these policies disproportionately harmed weaker economies in the Global South, they also reshaped economic structures in the West. Measures such as wage suppression, industrial restructuring, reduced investment in domestic manufacturing, and the strategic offshoring of production—particularly to China—helped sustain profit rates in major capitalist economies (Siddiqui, 2019a).

The global economy has undergone significant transformations in recent decades. Between 1990 and 2010, Brazil, India, and China doubled their share of global GDP, while the share of Western economies declined. The 2008 global financial crisis accelerated this shift (Siddiqui, 2023b). In response, China implemented a massive US$ 600 billion post-crisis stimulus package, solidifying its position as a key driver of global demand (Siddiqui, 2019b). The expansion of Chinese steel, cement, and aluminium production integrated raw material exporters into its regional economic orbit and fuelled the growth of South-South trade. Consequently, China surpassed the US as the world’s largest recipient of foreign direct investment, emerged as the leading source of merchandise trade, and contributed to over a third of global growth during the post-crisis period. By 2030, the World Bank projects that China and India will account for 38% of global investment and nearly half of total investment in manufacturing (Lavery, 2024).

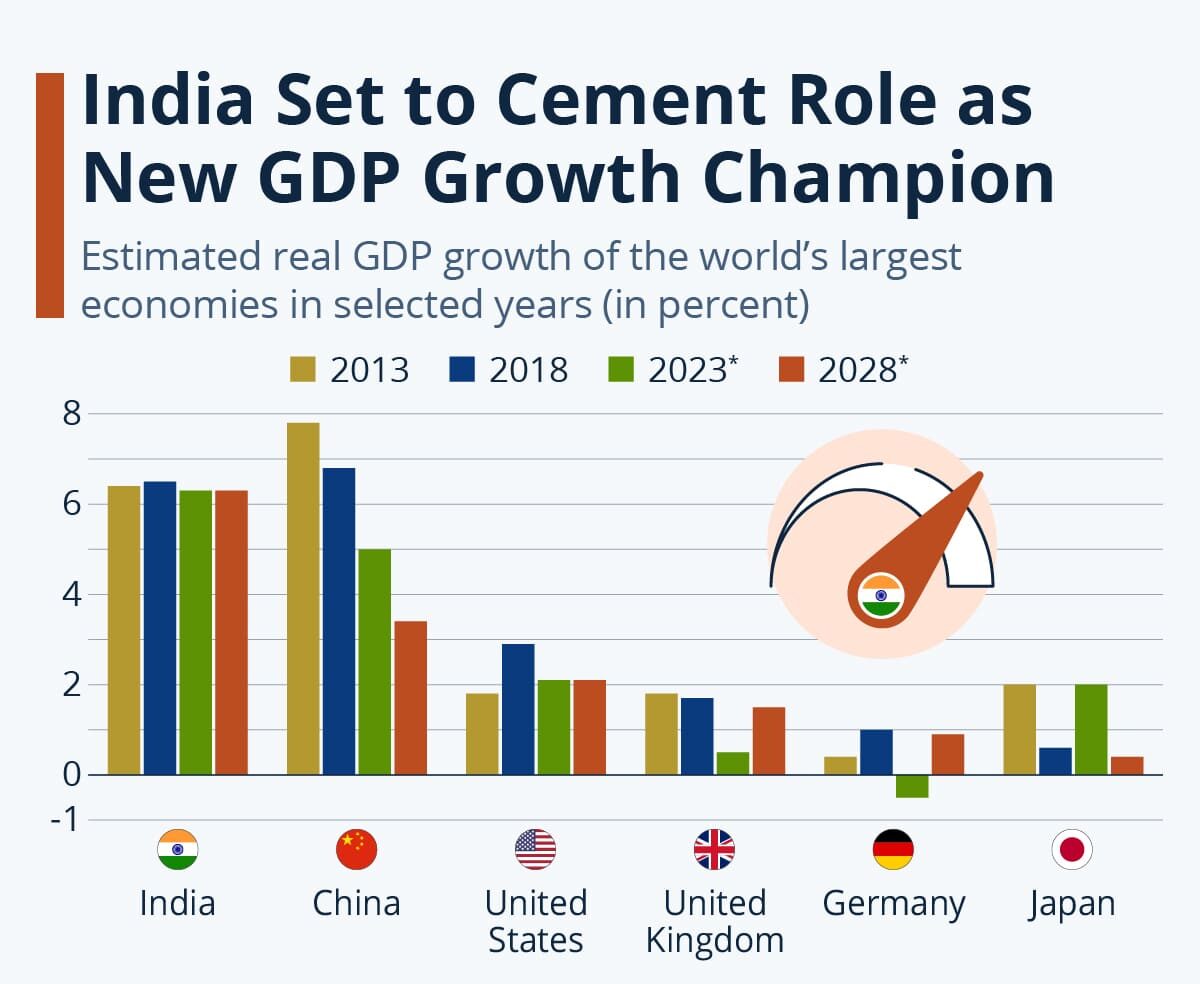

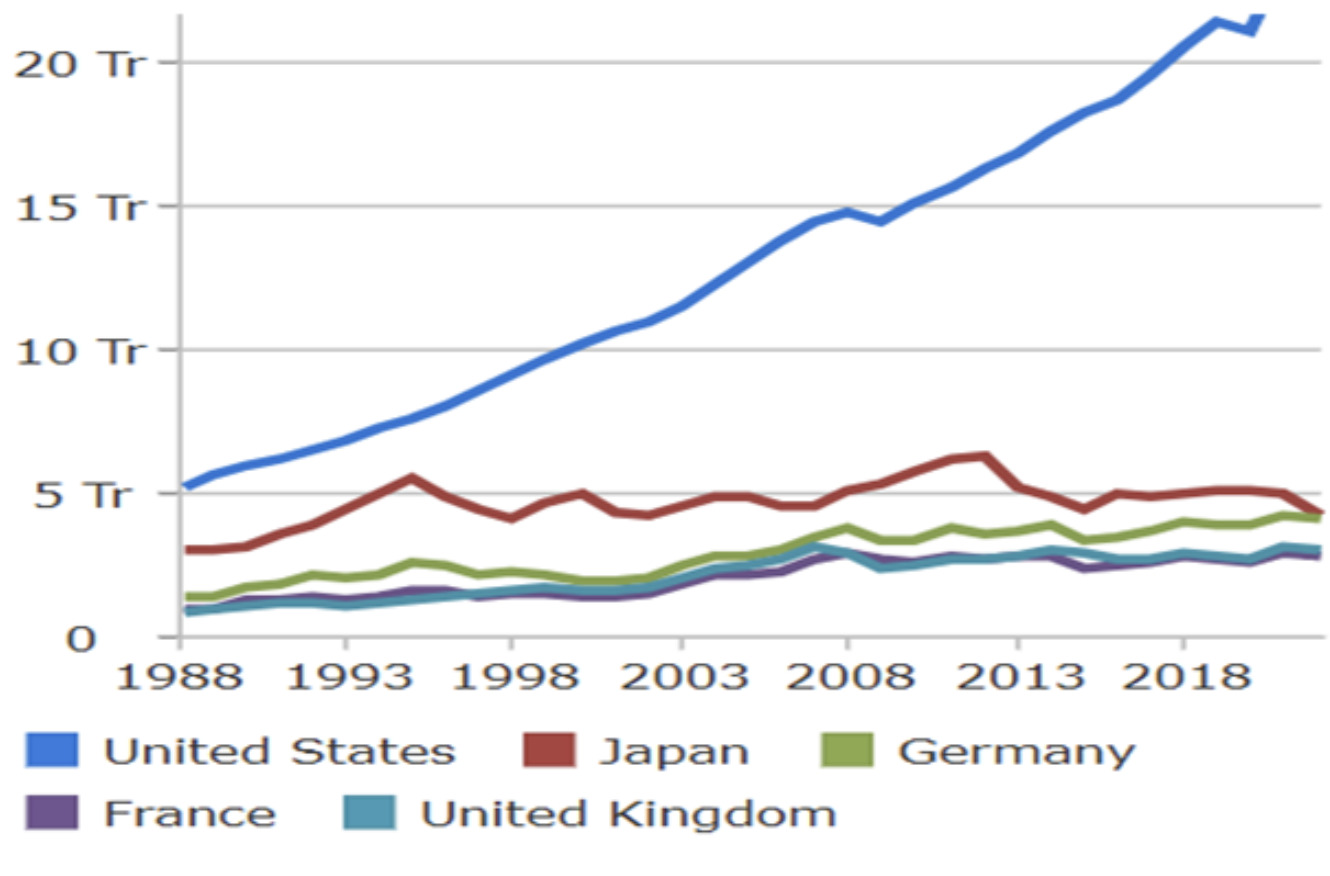

Figure 1 illustrates the real GDP growth of the world’s largest economies between 2013 and 2023, as well as projections by the IMF. The data clearly indicate that India and China have sustained growth rates more than double those of advanced capitalist economies. Within the advanced economies, the US has demonstrated significantly stronger GDP growth than its counterparts. In terms of nominal GDP at current US dollar prices, Figure 2 shows that the US economy has expanded at a faster rate than other advanced economies.

Figure 1: Real GDP Growth of the World’s Largest Economies in Selected Years (in%).

In recent decades, an analysis of the world’s top six economies by their share of global GDP from 1985 to 2024 (IMF, 2025) reveals significant fluctuations, particularly in the case of the United States (see Figure 1). While the US has consistently remained the world’s largest economy, its share of global GDP has undergone notable shifts over time.

The IMF’s projections for the world’s ten largest economies in 2025 highlight a clear trend: major developed capitalist economies are experiencing significantly lower real growth rates compared to emerging economies such as China and India (see Table 1). In the 1950s, the US alone accounted for over 50% of global GDP, but this share has declined sharply, falling below 25% by 2024.

After reaching a low of 22.6% in 2010, the US economy rebounded, increasing its relative share by several percentage points. According to IMF estimates, the US will account for 26.3% of global GDP in 2024. In contrast, China and India have steadily expanded their share of global GDP over the past three decades, while the relative contributions of the US, the EU, and Japan have declined (see Table 2).

Despite the EU’s expansion as new countries have joined over the past thirty years, its global output share has sharply declined, making it less economically significant than in the 1990s. In recent decades, the EU has become increasingly reliant on the US not only for security but also for economic stability. This dependency explains why former US President Donald Trump was less concerned about the EU’s reaction to the Ukraine issue. This broader trend also highlights the US’s relatively strong recovery from the COVID-19 pandemic, as evidenced by its rising share of global GDP since 2020 (See Table 2). Meanwhile, the EU, and Japan have experienced relative declines during the same period.

Table 1: Top 10 Largest Economies in the World in 2025.

Rank & Country

GDP (trillions of US$)

2025 Projected Real GDP (% Change)

GDP Per Capita at Current Prices (in 0000’s) (US$)

1. US

30.34

2.2

89.68

2. China

19.53

4.5

13.87

3. Germany

4.92

0.8

57.91

4. Japan

4.39

1.1

35.61

5. India

4.27

6.5

2.94

6. UK

3.73

1.2

54.28

7. France

3.28

1.1

49.53

8. Italy

2.46

0.8

41.71

9. Canada

2.33

1.3

55.89

10. Brazil

2.31

2.5

10.82

Source: IMF, World Economic Outlook, 2025.

Table 2: Share of Global GDP of the World’s Top Five Economies from 1985 to 2024 at current prices (%).

VI. Technological Convergence, Hegemony, and the Geopolitical Landscape

Another significant study is by Professor Jeffrey Sachs in his 2020 book The Ages of Globalization: Geography, Technology, and Institutions. Sachs argues that technological and institutional changes have interacted to produce long-term global economic shifts. During the colonial period, technological divergence occurred, with more technologically advanced countries gaining decisive advantages over less advanced nations. This disparity led to wars, occupation, and exploitation. However, since the period of independence for many former colonies, technological convergence has emerged, with poorer countries progressively catching up to wealthier ones. As poorer nations narrow the technological gap, they pose a growing challenge to the hegemonic power of dominant states. This technological convergence has given rise to new and potentially tragic hegemonic conflicts (Sachs, 2020).

As poorer nations narrow the technological gap, they pose a growing challenge to the hegemonic power of dominant states.

This fear of being overtaken by rising powers is not a new phenomenon. Japan had similar concerns in 1941, and Germany shared the same anxiety in 1914. Today, China faces the same challenge, with the US explicitly seeking to contain China’s rise. This situation mirrors the concept of Thucydides’s Trap, an analogy drawn from fifth-century BCE Athens, where the rise of Athens as a dominant power led to a hegemonic contest with Sparta, the leading military power at the time. According to Thucydides, the fear of Athens’ rise led to inevitable conflict—a situation echoed in modern international relations as emerging powers challenge incumbent hegemonic states.

In 2014, the US played a pivotal role in the overthrow of the Ukrainian government. Evidence suggests that much of the violence, including shooting into crowds, originated from protesters rather than the security forces under President Viktor Yanukovych. At the time, Yanukovych had pursued a neutral foreign policy and was opposed to NATO expansion. However, after his removal, the US supported the rise of a Russophobia, nationalist government, which quickly abandoned Ukraine’s neutrality and even passed laws banning the Russian language. In response, Russia annexed Crimea, and many pro-Russian factions within the Ukrainian military defected, initiating an insurrection in Eastern Ukraine (the Donbas region).

In a shift in US foreign policy, Defence Secretary Pete Hegseth stated that the US planned to reduce its military presence in Europe. He emphasized that the US was no longer “primarily focused” on European security and that Europe would need to take the lead in defending Ukraine. Hegseth also acknowledged that restoring Ukraine’s pre-2014 borders was unrealistic. He noted that the US was shifting its military priorities to focus on deterring China and called on European NATO members to increase their defence budgets to 5% of GDP to better defend the continent.

VII. Conclusion

Since around 2017, the world has transitioned from a unipolar order dominated by the US to a multipolar world, driven by global economic shifts. This shift has seen the emergence of three major global powers: the US, China, and Russia. Amid a deepening crisis in the US economy, the US is seeking to disengage from Europe and resolve the conflict in Ukraine, redirecting its resources towards reviving its domestic economy while focusing on the growing threat from China. The US has also pressured the EU to increase its defence spending, with a target of at least 5% of GDP, up from the current 2%.

Economically, under Trump, despite some shifts in policy, there remain key continuities with previous administrations. The neoliberal economic framework is expected to persist. In response to inflationary pressures, central banks will likely follow the neoclassical model, raising interest rates to constrain wages and limit consumer spending, in the hope of slowing down price increases. The neoliberal policies—including deregulation and austerity—may be pursued to unleash entrepreneurial activity. Trump’s policies are expected to focus on reducing taxes, particularly corporate taxes, while imposing tariffs on imports. This approach could trigger inflationary pressures, prompting the Federal Reserve to raise interest rates again, potentially risking recession due to the economy’s reliance on cheap credit and the growing burden of US government debt.

In contrast, an alternative European policy should prioritise ending the war in Ukraine and rejecting Trump’s predatory stance on Ukraine’s natural resources. This would involve removing sanctions, returning the $300 billion of Russian frozen assets, and restoring trade relations with Russia. Europe should pursue a comprehensive strategic partnership with Russia, China, India, and other emerging economies. Investment in green technology should be a priority, with a combined focus on de-growth to address the environmental challenges ahead. Fiscal policy should be revitalized, with increased public investment playing a central role in reducing inequality and driving long-term growth and prosperity. To restore peace and trust, demilitarising the 400 km border on both sides of Ukraine could be a crucial step. This model could draw inspiration from Austria’s post-war success, where the country emerged as a sovereign, democratic state and integrated with the rest of Europe. Ukraine could adopt similar policies to those Austria implemented during the Cold War, serving as a neutral buffer between the West and Soviet Union.

Dr. Kalim Siddiquiis an economist specializing in International Political Economy, Development Economics, Trade and Economic Policy. Since 1989, he has been teaching economics at various universities in Norway and the UK. Dr. Siddiqui’s research interests encompass a wide range of topics, including political economy, international trade, and economic history, South Asia, and emerging economies. He has presented papers at international conferences across numerous countries, reflecting his global engagement in the field. His scholarly pursuits span six broad domains: Political Economy, Development Economics, Economic History, Economic Policy, Globalization, and International Trade. Dr. Siddiqui has made significant contributions to research in areas such as trade policy, globalization, and political economy. His work has been published in chapters of edited books and articles published in peer-reviewed journals. For inquiries, Dr. Siddiqui can be reached at: [email protected]

References

Brzezinski, Z. (1997) The Grand Chessboard: American Primacy and Its Geostrategic Imperatives, New York: Basic Books.

Chotiner, I. (2025) “What Could Happen if the U.S. Abandons Europe” New Yorker, February 21.

Foy, H. (2024) “The untold story of the most chaotic Nato summit ever” Financial Times, July 4, London.

IMF (International Monetary Fund) (2025) World Economic Outlook – Growth on divergent paths amid elevated policy uncertainty, January, Washington DC: IMF.

Lavery, S. (2024) “Rebuilding the fortress? Europe in a changing world economy” Review of International Political Economy 31(1): 330–353.

Mearsheimer, J. (2001) The Tragedy of Great Power Politics, New York: WW Norton.

Sachs, J. (2020) The Ages of Globalisation: Geography, Technology, and Institutions, Columbia: Columbia University Press.

Sabbagh, D. (2025) “US no longer “primarily focused” on Europe’s Security” TheGuardian, February 12, London.

Siddiqui, K. (2024a) “The Decline of the West and Global Political Economy” World Financial Review, December.

Siddiqui, K. (2024b) “Political Economy of Globalisation and Issues of Global Governance” World Financial Review, September.

Siddiqui, K. (2023a). “The New Cold War: Struggle for Global Domination” (Part I & Part 2) World Financial Review, June and August.

Siddiqui, K. (2023b) “Marxian Analysis of Capitalism and Crises”, International Critical Thought, 13(4): 525-545.

Siddiqui, K. (2022a) “Ukraine-Russia War and the Impact on the Global Economy” World Financial Review, November-December.

Siddiqui, K. (2022b) “Capitalism, Imperialism, and Crisis”, European Financial Review, June-July.

Siddiqui, K. (2020a) “Prospects of a Multipolar World and the Role of Emerging Economies” World Financial Review, November-December.

Siddiqui, K. (2020b). “The Political Economy of the Slave Trade, Capital Accumulation and the Rise of Britain” World Financial Review, January-February

Siddiqui, K. (2019a). “The US Economy, Global Imbalances under Capitalism: A Critical Review” Istanbul Journal of Economics 69(2): 175 – 205, December.

Siddiqui, K. (2019b). “Financialization, Neoliberalism and Economic Crises in the Advanced Economies” World Financial Review, May-June, pp.22 – 30.

Siddiqui, K. (2017). “Austerity as a Tool of Fiscal Consolidation: Theoretical and Empirical Perspective” (Edi) S. Owsiak, Public Finance, and the New Economic Governance in the European Union, 116 – 166, Warsaw: Wydawnictwo Naukowe.

Siddiqui, K. (2016). “Will the Growth of the BRICs Cause a Shift in the Global Balance of Economic Power in the 21st Century?” International Journal of Political Economy 45(4): 315 – 338.

Siddiqui, K. (2015). “Trade Liberalisation and Economic Development: A Critical Review” International Journal of Political Economy 44(3): 228 – 247.

Your credit report is one of the most important documents when it comes to managing your financial health. It helps determine everything from your ability to secure loans to the interest rates you’ll pay. That’s why it’s crucial to stay on top of your credit report and ensure everything is accurate. The problem is, errors can happen—and when they do, they can have a significant impact on your credit score. So, how do you spot these errors and what should you do if you find them? Let’s break it down in simple terms so you can protect your credit and your financial future.

The Importance of Checking Your Credit Report

Before we dive into how to spot errors, it’s important to understand why checking your credit report is so essential. Your credit report includes information about your credit history, such as your current loans, credit cards, payment history, and public records like bankruptcies or tax liens. This information is used by lenders to assess your creditworthiness, meaning an inaccurate report can result in higher interest rates, rejected loan applications, or even issues like being denied for a job.

Additionally, if you’re struggling with debt, like many people are, errors on your report can make it harder to access tools like a debt settlement in Washington or other financial relief options. Regularly reviewing your credit report can help you spot these issues early and avoid any unexpected surprises.

What to Look for When Reviewing Your Credit Report

When you review your credit report, it’s crucial to pay attention to several key areas: your personal information, account details, and any unfamiliar accounts. Here’s how to break it down:

Personal Information

Your credit report should include your name, address, and other identifying details. While this may seem straightforward, it’s essential to verify that everything is spelled correctly and up to date. Even small errors—like a misspelling of your name or an outdated address—can cause problems, especially if they’re linked to incorrect credit information. If you spot any inconsistencies, it’s important to correct them right away, as they can lead to issues like a mix-up with another person’s credit profile.

Account Information

Next, look at the details of your open accounts—this includes credit cards, loans, mortgages, and other forms of credit. Check the following:

Credit Limits: Are the credit limits listed correct? If you’ve had a limit increase, make sure it’s reflected.

Balances: Double-check that your account balances are accurate and match what you owe. If you’ve made payments recently, the balance should reflect that.

Payment History: Ensure your payment history is accurate. Look for any late payments that you know didn’t happen, or payments that were missed even though you paid on time. Missing payments on your report can negatively impact your credit score.

Any discrepancies in these details could signal an error or a potential case of identity theft.

Unfamiliar Accounts

One of the biggest red flags on a credit report is an account that doesn’t belong to you. If you see accounts you don’t recognize, it’s important to investigate them immediately. These could be the result of fraudulent activity or mistakes by the credit bureau. Sometimes, a mix-up can occur where another person’s account is listed under your name, particularly if you have a similar name or share an address.

Inconsistencies and Mistakes to Look Out For

Errors can show up in many different forms. Here are a few to keep an eye out for:

Incorrect Dates: For example, a missed payment might be reported with the wrong date, which could lead to a false negative impact on your credit score.

Wrong Amounts: If the amounts listed on your credit accounts don’t match what you know you owe, this could be a sign of an error.

Duplicate Accounts: Sometimes, accounts can be listed twice on your report by mistake, which can affect your credit score. Make sure to check for any duplicate accounts and get them removed if needed.

How to Dispute Errors on Your Credit Report

If you find an error or discrepancy, the next step is to dispute it. Disputing errors is relatively simple, but it’s important to take action as soon as you spot something wrong.

Step 1: Contact the Credit Bureau

The first thing you need to do is contact the credit bureau that issued the report. There are three major credit bureaus—Equifax, Experian, and TransUnion. You can dispute errors directly with them by either filing an online dispute or sending a letter. Make sure to include all relevant details, such as the error you’ve found and any supporting documentation that proves your case.

Step 2: Provide Documentation

To back up your dispute, include copies of any documentation that proves the error. For example, if a payment is being listed as late, provide a bank statement or confirmation of the payment to show that it was made on time.

Step 3: Follow Up

Once you’ve submitted your dispute, the credit bureau is legally required to investigate the issue, usually within 30 days. They’ll inform you of the results of their investigation, and if the dispute is successful, they’ll update your credit report accordingly. If the error isn’t resolved in your favor, you can appeal the decision and escalate the issue if necessary.

Why It’s Important to Keep Checking Your Credit Report

Even after you’ve fixed any errors, it’s crucial to continue reviewing your credit report regularly. Errors can crop up at any time, and by checking your report often, you can catch issues before they snowball into bigger problems. This is especially important if you’re working toward improving your credit score, getting approved for loans, or pursuing debt relief options like debt settlement.

You’re legally entitled to one free credit report per year from each of the three bureaus, which you can request through AnnualCreditReport.com. Checking your credit report every few months can help you stay on top of any changes or errors.

Asian stock markets experienced a dramatic sell-off on Monday, intensifying a global market downturn fueled by escalating trade tensions between the U.S. and China. Japan’s Nikkei 225 index closed down 7.9%, while Hong Kong’s Hang Seng plummeted nearly 12%, and the Shanghai Composite fell over 7%. The widespread losses reflect growing fears of a damaging trade war and its potential to trigger a global economic slowdown.

The market turmoil was triggered by President Trump’s implementation of new tariffs and China’s forceful retaliation, which included imposing 34% tariffs on all U.S. goods. Analysts point to “forced liquidations” and “full-blown panic” as trading volumes surged.

Tech giants like Sony, Alibaba, and Tencent saw significant declines, along with major automakers Toyota and Honda. Taiwan’s Taiex index also suffered a steep 9.7% drop, with key exporters like TSMC and Foxconn triggering circuit breakers.

“Washington’s shock decision to impose a 34% tariff on Chinese goods dealt a direct blow to core export sectors like semiconductors and EVs (electric vehicles), triggering a sharp and broad-based repricing across Asian markets,” stated Dilin Wu, a research strategist at Pepperstone.

The market downturn follows a brutal two-day stretch on Wall Street, where over $5.4 trillion in market value was wiped out. U.S. stock futures continued to decline Sunday evening, indicating further losses.

China, through its state-run media, has signaled its resolve to withstand U.S. pressure, stating it has “plenty of countermeasures at hand.” Ronald Temple, chief market strategist at Lazard, predicts further retaliation from other countries, exacerbating the economic damage.

Even traditionally safe-haven assets like gold saw sell-offs, and oil prices continued to slide. The S&P 500 is on the verge of a bear market, raising concerns about a broader economic downturn.

Billionaire investor Bill Ackman warned that Trump is “losing the confidence of business leaders around the globe” and called for a “timeout” to avoid an “economic nuclear war.”

President Trump, while acknowledging market volatility, defended his trade policies, stating he aims to address trade deficits with China and the European Union. He also revealed that he had received calls from technology executives and world leaders over the weekend regarding the tariffs.

Japan and Taiwan have expressed their intent to negotiate with the U.S. to reduce tariffs and address trade imbalances. However, economists at Barclays have adopted a “cautious view” on the success of these negotiations and have begun revising economic growth forecasts for the region.

After a decade of deglobalization and US geopolitics, globalization is no longer at crossroads, but unraveling. The longer this plunge prevails, the greater will be its costs.

After divisive debates and conflicting reports, President Trump announced his trade plan: a 10% baseline tariff on all imports; “discounted reciprocal tariff” on “bad actors”: 24% on Japan, 20% on EU, respectively; and a new 34% tariff on China.

As expected, it is a protectionist plan building on both reciprocal and universal tariffs, but devoid of an economic rationale. As fears of a recession mount and mass protests in the US have begun, the loss of over $6 trillion on Wall Street in only two days is just a prelude of what’s to come. Along with China’s strike of all US imports with 34% tariff, Europe, Japan and South Korea, India and Brazil and the rest of the world are positioning to counter the Trump tariffs.

Half a decade ago, Trump tariffs on imports from China accounted for $400 billion, or more than 90% of the trade affected. Today, in what appears to be the first round of US tariffs with Canada, Mexico and China alone could add up to more than $1.3 trillion; that is, over 3.5 times more than half a decade ago.

But with the new tariff rounds, international plus universal tariffs and the expected retaliations, which may prove more aggressive than anticipated, there is far, far worse ahead. Thanks to decades of postwar globalization, these inter-dependencies will take longer to fragment. But the process of unraveling has begun.

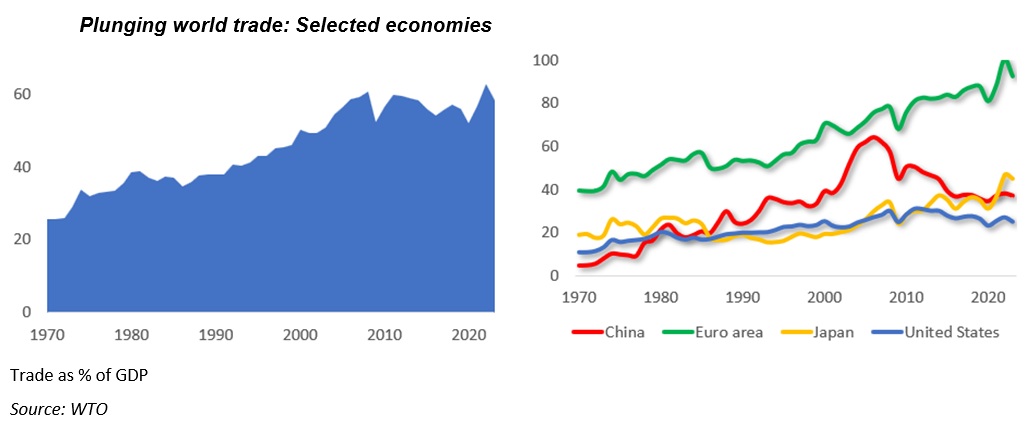

Plunging world trade

Global economic integration is often measured by world trade and investment. The postwar wave of globalization benefited mainly the advanced economies. It was only after 1980 that some developing countries, spearheaded by China, broke into world markets for manufactured goods and services, while attracting foreign capital.

This era of globalization eclipsed with the global recession in 2008. As the G20 cooperation subsequently dimmed, so have the global growth prospects diminished. After 2019, the brief gains of the U.S.-Sino trade truce were derailed by the COVID-19 pandemic and the dire international economic landscape. As percentage of world GDP, world trade during the first term of President Trump (“Trump 1.0”) fell back to the level where it had been over 15 years before.

After the first round of trade wars focusing on Mexico, Canada and China, the trendline is falling rapidly, faster than in 2018. With the onset of the second round – the launch of unilateral “reciprocal tariffs” and/or “universal tariffs” – that fall will escalate and is likely to boost mounting inflation and growth stagnation; a corrosive mix of stagflation.

But disaggregate these totals and there are differences. When tariff wars grow international, the trading economies, measured by trade as percentage of GDP, are the first in the firing line. The Euro area economies are major traders, but since they trade mainly among other European countries, it is their transatlantic trade that’s under fire.

Japan benefited from Trump 1.0, which hit mainly China. But as Tokyo is not immune to an international tariff war, the downhill has started. Since 2008, Beijing has shifted its growth model from exports and investment toward consumption and innovation. As a result, China’s trade ratio has steadily decreased from over 60% to 37% of GDP, or the level it first reached around 2000.

In the US, the trade ratio has been relatively lowest, around 20% to 25%. In the past, Washington considered international multilateral cooperation too important to risk. But those times are now gone.

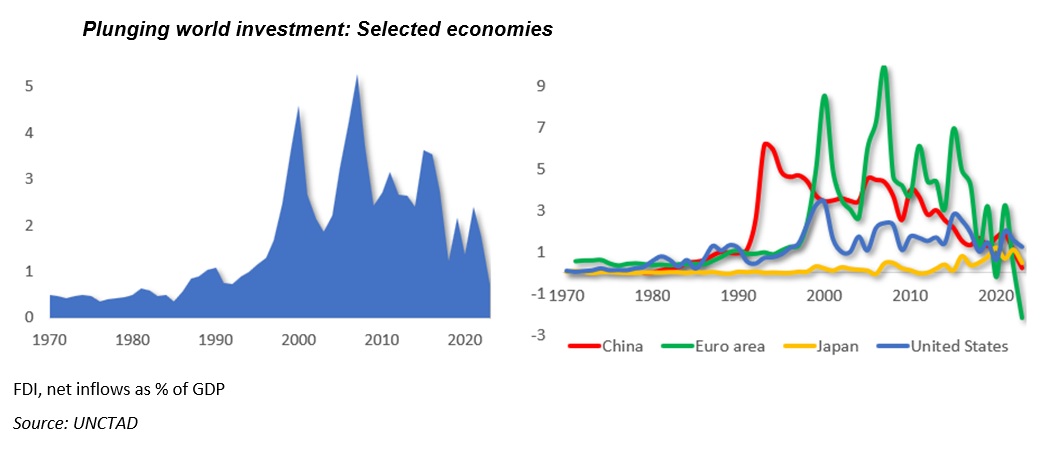

Plunging world investment

Before the 2008 global crisis, world investment soared to almost $2 trillion, with foreign direct investment (FDI), rising to 5.3% of world GDP, measured by net inflows as percentage of GDP. Following the severe 2008 recession, the FDI ratio more than halved to 2.4%. In 2017, the fundamentals were aligned for global recovery. Yet, the hoped-for rebound of world investment failed, due to the Trump 1.0 tariff wars. In 2020, the FDI ratio had plunged to 1.4%; a level that was first reached 30 years ago.

Since then, this failure has been compounded by the coronavirus depression, the US/NATO-led proxy war against Russia in Ukraine and the US-armed and financed proxy war of Israel against Gaza, not to mention a set of new Cold Wars. With the end of Trump 1.0, the FDI ratio climbed back to 2.4%. The expectation was that the Biden administration would reverse most of the unwarranted tariffs. Instead, it not only coopted the Trump tariffs but broadened them. So, the ratio has plunged to barely 0.7% – a level that world investment had first reached in 1981, that is over 44 years ago.

But here, too, there are intriguing differences between economies. In Europe, foreign investment, measured by net inflows (% of GDP), has long been volatile. But gone are the glory days of globalization, when the ratio was still 10%, or even the mid-2010s, prior to the Brexit, the pandemic and wars, when it hovered around 7%. If Trump 1.0 caused it to plunge to red, Trump 2.0 begins at a historical moment when it is -2.2%.

In China, the FDI ratio had its high in 1994, when it exceeded 6.2%. Thanks to US coercive pressure on allies and geopolitics, it now hovers below 0.3%. Similarly, Japan’s benefits during Trump 1.0 have now diminished and the ratio lingers at below 0.5%.

In the US, the ratio was its highest at 3.4% in 2000, after the Internet revolution. Before Trump 1.0 trade wars, it still hovered around 2.5% in 2015. Today, it is only half of that. Thanks to the unwarranted tariff frictions and geopolitical conflicts, the net inflows are now at a level the US reached already in the late 1980s; that is, over four decades ago.

With Trump 2.0, the first signs of a new plunge, a far more severe one, are looming.

Global costs of fragmentation

Essentially, deglobalization reflects the retrenchment of economic flows between countries, whether measured by world trade or investment. Until recently, it still prevailed.

During Trump 1.0, deglobalization ensued from policy choices, such as tariff wars, and the waning of structural forces. The latter used to spur rapid integration of economies until 2008, thanks to technological progress, reduced transport costs, and offshoring of value activities across countries.

A few years ago, I reviewed these costs that were then still largely focused on the US-China trade friction. With the internationalization of the US trade wars and the broadening of their scope, both of which are now the reality, the attendant losses are likely to prove far higher, both in terms of economic and human costs.