")

In this article, Dr. Kalim Siddiqui examines the multifaceted factors contributing to the deepening economic crisis in the United States. The article delves into how policies like globalization and financial deregulation, while initially boosting short-term growth, ultimately introduced structural vulnerabilities, leading to stagnation and unprecedented levels of trade deficit and government debt.

I. Introduction

The United States’ (US) economic crisis has deepened despite efforts to address it through globalization, trade liberalization, and capital mobility. While these policies initially spurred short-term growth and boosted corporate profits, they also introduced structural vulnerabilities. The influx of cheap imports from China and East Asia helped to keep inflation low in the US and other Western economies. However, financial deregulation—a key component of liberalization—culminated in the 2008 financial crisis, severely contracting economic output and ushering in nearly a decade of stagnation. As a result, the US trade deficit and government debt reached unprecedented levels (Siddiqui, 2019a).

In response, the US government implemented measures in 2010 to stimulate investment and employment, including substantial tax cuts for corporations and the wealthy. However, these policies failed to generate the desired economic revival, exposing the limitations of supply-side interventions in a post-crisis economy.

A similar pattern of crisis and recovery can be traced historically. The “thirty-year crisis” of capitalism, marked by two world wars and the Great Depression, eventually gave way to what many economists describe as the ‘Golden Age of Capitalism’. During the postwar era, state intervention through Keynesian demand management fostered sustained growth, low unemployment, rising labour productivity, and increasing wages. However, this prosperity was underpinned by substantial US military spending, particularly during the Korean and Vietnam Wars, financed by issuing dollars. Under the Bretton Woods system, these dollars were pegged to gold, forcing the rest of the world to hold US dollars, which, coupled with excessive US demand, led to inflationary pressures. This shift ultimately contributed to the collapse of the Bretton Woods system (Siddiqui, 2024a).

Over the past four decades, the US and other advanced economies have undergone profound structural shifts in output, employment, and revenue composition. The onset of neoliberal globalization in the 1980s, particularly in the US, triggered massive outflows of capital and technology to developing economies, especially in East Asia and China. Consequently, the share of manufacturing in the US economy declined sharply, and a significant number of industrial jobs were lost as industries relocated to countries offering lower wages and higher returns on investment. This structural transformation resulted in widespread job losses, while employment growth in the services sector has been more limited, and largely for short terms (Siddiqui, 2025a).

II. Financial Deregulation and the 2008 Crisis

With the recession of the early 1970s, the US began dismantling its earlier policy of state intervention in demand management, ushering in the era of neoliberal globalization. This shift promoted financial deregulation and the liberalization of capital and goods markets. Development strategies centered on attracting foreign investment and pursuing export-led growth became regarded as the only viable paths to economic expansion (Siddiqui, 2022a).

The globalization of finance created a paradox: while financial capital became increasingly international, political authority remained confined within the framework of nation-states. As a result, individual states were compelled to align their policies with the demands of global finance to avoid the threat of capital flight. Monetary policy, emphasizing low inflation and currency stability, was prioritized over fiscal policy, which since early 1980s had been used to stimulate economic activity (Patnaik, 1997).

This emphasis on “sound finance”—a principle favoured by global finance capital—led to an obsessive focus on controlling fiscal deficits and reducing the tax burden on capitalists. Together, these changes severely curtailed the state’s ability to intervene in managing aggregate demand. Efforts to stimulate economic activity through running fiscal deficits were increasingly portrayed as irresponsible. Austerity measures in government spending were celebrated as virtues, under the argument that public “profligacy” would crowd out private investment (Patnaik, 1997).

III. Deindustrialization and the Structural Crisis of US Capitalism

Since the 1980s, US corporations have increasingly found it more profitable to invest in low-wage countries such as China and other East Asian economies. These countries offered a disciplined and highly skilled labour force, low wages, inexpensive raw materials, and higher returns on investment. As a result, many industries relocated abroad, leading to massive deindustrialization within the US. The consequent loss of manufacturing jobs was further exacerbated by China’s entry into the World Trade Organization (WTO), which accelerated the offshoring trend.

Despite these shifts, the US dollar has remained the world’s reserve currency. Given the declining domestic growth rate, this dynamic increasingly strains the US economy’s ability to uphold the dollar’s global dominance, signalling a deepening structural crisis (Siddiqui, 2024b). Currently, US capitalism is once again enmeshed in a crisis with far-reaching consequences. Since the mid-1970s, the economy has been marked by slower average growth, and the crisis initiated by the collapse of the housing bubble in 2007–2008 has only intensified existing problems. And by 2024, rising prices, low productivity growth, high unemployment, and increasing inequality have all become more pronounced (Siddiqui, 2025c).

Rosa Luxemburg argued that a capitalist economy requires exogenous stimuli—external sources of demand or expansion—for its sustained growth. Endogenous stimuli, or internal drivers that arise from the economy’s momentum, are often insufficient to prevent stagnation. Exogenous stimuli, therefore, are necessary to avoid prolonged stagnation and to explain periods of long-term growth (Siddiqui, 2024c).

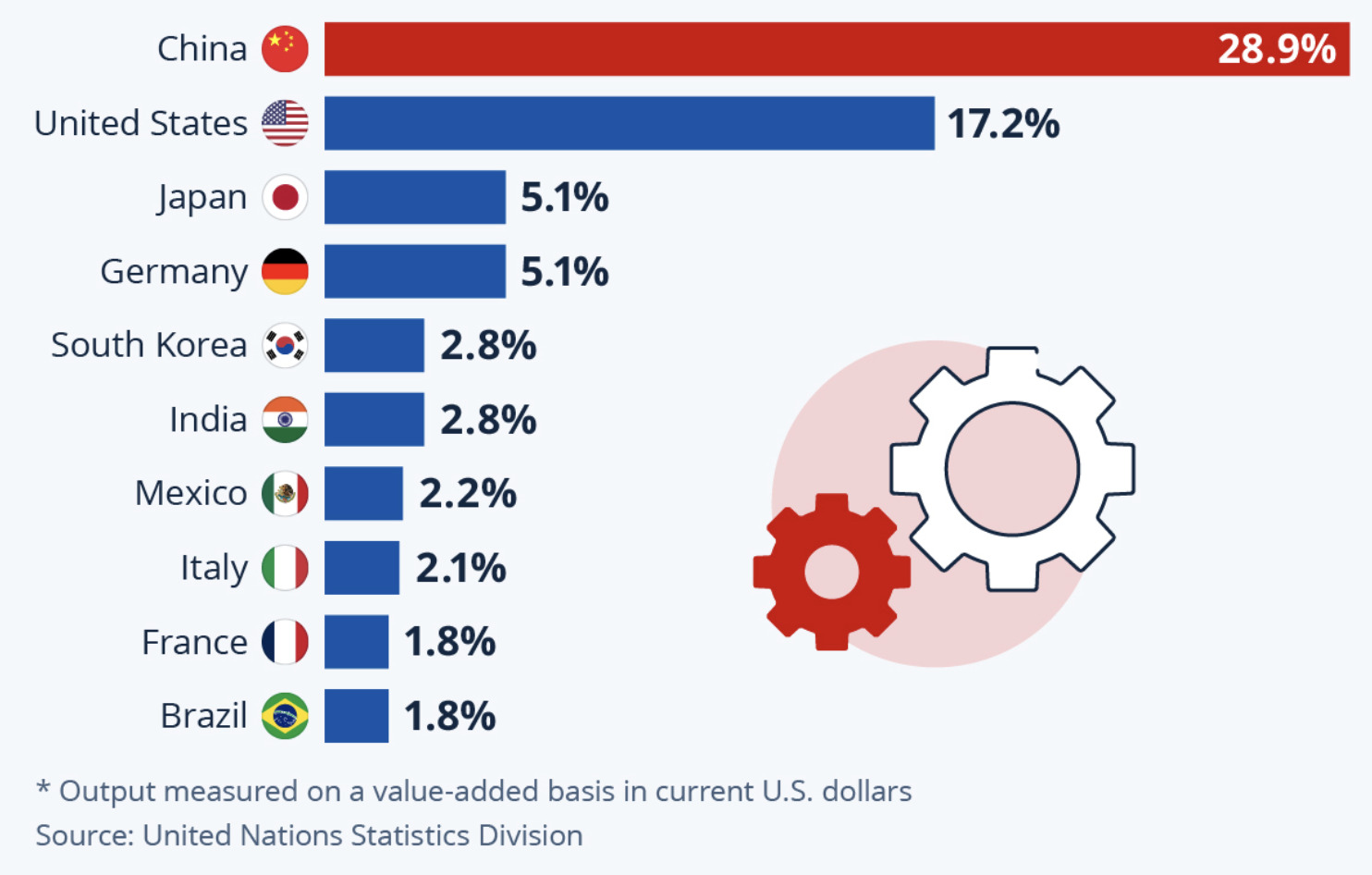

In 2024, the contribution of the manufacturing sector to GDP varied significantly across major economies. China had the largest share of manufacturing output, with the sector accounting for 28.9% of its GDP. The US ranked second in total manufacturing output, though manufacturing comprised only 17.2% of its GDP (see Figure 1). Other economies, such as Germany and Japan, also maintained substantial manufacturing sectors, each contributing around 5.1% to their GDP. In terms of total value added, China’s manufacturing output reached $4.8 trillion in 2024, representing 27% of its GDP. In contrast, manufacturing in the US accounted for just over 10% of value added, making it the least dependent on domestic manufacturing among the top ten manufacturing nations—matched only by France. Outside of China, only Ireland, South Korea, Vietnam, and Thailand reported manufacturing contributions exceeding 25% of GDP.

Figure 1: Share of Manufacturing Output in Selected Countries, 2024.

IV. Neoliberalism, Automation, and the Hollowing Out of the US Labour Market

Neoliberalism emerged as the US economic crisis deepened. This strategy facilitated the construction of the dollar–Wall Street regime, but it failed to address the underlying causes of the country’s economic decline (Siddiqui, 2022b). The US and other Western countries retained a near-monopoly over core technologies and high-value-added sectors within the global value chain. The reintegration of China into the world economy—as a supplier of cheap labour and raw materials and as a vast market for imports.

Since the 1980s, automation aimed at reducing labour costs, coupled with heavy reliance on imported manufactured goods, has led to the hollowing out of US blue-collar factory jobs and low-skilled white-collar office employment. This deindustrialization has fuelled massive discontent among working-class Americans. However, the idea of restoring these jobs by imposing tariffs on exporting countries is largely a pipe dream. While some degree of reshoring may occur, particularly in high-end manufacturing sectors that rely heavily on robotics, it will not reverse the broader trend.

Indeed, industries such as computer production are already almost entirely automated. Any reshoring of high-end manufacturing will likely increase the manufacturing sector’s contribution to US GDP, but it will not generate substantial employment for low- and medium-skilled workers, especially those with only a high school education. Instead, automation and robotization are creating a growing polarization of skills, contributing directly to rising income inequality.

This technological transformation has increased the demand for highly skilled workers—such as managers, engineers, and IT specialists, while simultaneously expanding low-wage service sector jobs that require human interaction. The US labour market thus faces a crucial challenge: the rapid pace of technological advancement is not being matched by the creation of sufficient employment opportunities for workers with lower levels of education. Automation and robotization are driving a deepening skill polarization, which is closely linked to rising income inequality.

The decline of US manufacturing has been largely driven by the emergence of a new international division of labour under neoliberal globalization. This shift opened avenues for productive capital to move to the Global South, where labour is cheaper and natural resources more accessible. Consequently, core manufacturing tasks were retained in the Global North. Although production was geographically dispersed, profits remained concentrated among multinational corporations (MNCs) headquartered in advanced economies, thereby reinforcing global economic inequalities (Siddiqui, 2017).

The US now heavily depends on cheap imports from China, covering a vast range of goods—from consumer electronics and household appliances to toys and bicycles. Domestic production of these goods is not easily or rapidly replaceable, underscoring the country’s deep entanglement in global supply chains. While President Trump aimed to rebuild US manufacturing, many of the imports from China, Vietnam, EU, Canada, and Mexico are produced by US-based MNCs (Siddiqui, 2025a). These firms manufacture overseas to exploit lower costs advantages, then sell back to the US market.

This outsourcing strategy has had profound effects. East and Southeast Asian countries rapidly industrialized, expanding their shares of global manufacturing and exports, while the US economy became increasingly reliant on marketing, finance, and services, leading to a hollowing out of its manufacturing base (Siddiqui, 2021).

During the Clinton administration, US policy aimed to integrate China into the global economy, expecting that economic liberalization would lead to political change. This strategy, including China’s entry into the WTO, failed to produce the anticipated political outcomes. Subsequently, the US strategy shifted toward containment, exemplified by a growing military presence in the South China Sea and strategic support for Taiwan. The Biden administration sought to revitalize US industry through subsidies for technology and manufacturing, but this approach had little success.

V. The Limits of Reindustrialization and the Reality of Globalization

Although the US maintains the second-largest manufacturing sector, employment in the manufacturing sector has sharply declined since the 1970. This decline is primarily attributable to falling profitability and technological advancements that displaced labour, rather than solely to trade liberalization.

The Trump administration proposed expanding domestic manufacturing through increased use of robotics and artificial intelligence, a strategy unlikely to create substantial new employment. In reality, restoring traditional manufacturing jobs is not feasible: globalization has fundamentally dispersed the manufacturing value chain across borders, distributing components, raw materials, and production processes worldwide. Meaningful restoration of US manufacturing would require massive investment, but given low profitability rates, corporations are unlikely to undertake such investments outside of military hardware, where government subsidies remain strong. Despite these structural barriers, Trump has pursued a protectionist strategy focused on tariffs and reshoring efforts. However, this approach risks triggering broader economic contraction, both domestically and globally.

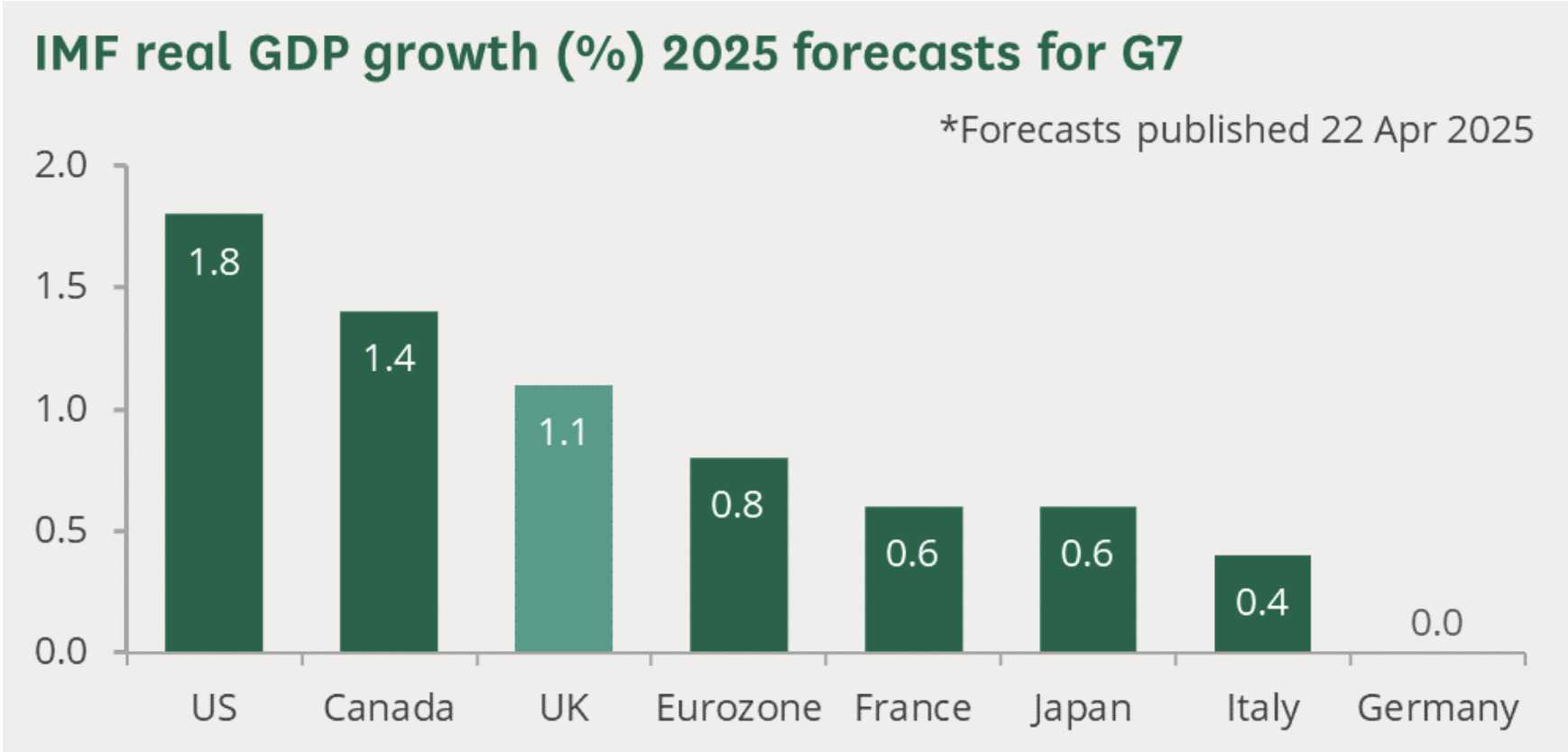

The most recent IMF Report, published in April 2025, projects only modest growth for the US and other advanced economies (see Figure 2). This slowdown is attributed to tariff rates reaching levels not seen since the Great Depression of the 1930s, rising economic uncertainty, and an increasingly volatile global environment. Inflation and elevated unemployment are expected to persist through 2025. Moreover, escalating trade tensions, financial market adjustments, and heightened trade policy uncertainty may further undermine both short- and long-term growth prospects.

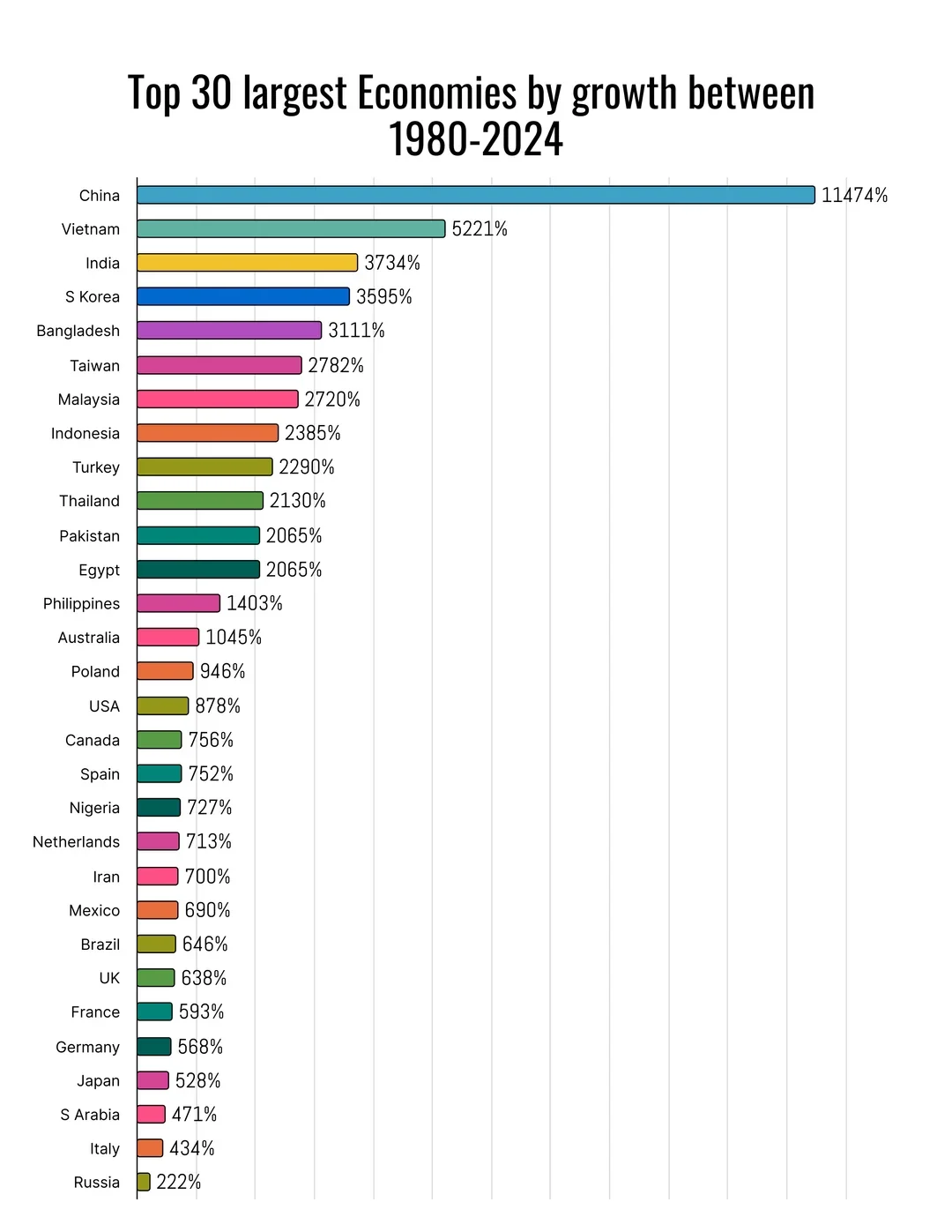

Over the past forty-four years (1980-2024), China has recorded the most significant GDP growth among major economies, while Vietnam, India, Indonesia, Malaysia, and Russia have also experienced substantial expansion, as illustrated in Figure 3. Although US growth was more modest compared to China and India, it outpaced that of the UK, France, and Japan over the same period (Siddiqui, 2020). Between 2021 and 2024, China and India sustained particularly strong performance, with average annual growth rates of 5.5% and 6.4%, respectively. Russia also demonstrated notable growth, averaging over 4% annually during this period (Siddiqui, 2024d).

Figure 2: Real GDP Growth (%), 2025 Forecasts for G7.

Figure 3: Output Growth of the Top 30 Largest Economies between 1980-2024.

VI. Neoliberalism and Rising Inequality

The neoliberal globalization of the past four decades has dramatically increased capital mobility. In this new development model, foreign investment and exports became key drivers of growth, incentivizing governments to offer tax concessions and subsidies to attract multinational corporations. Meanwhile, privatization, austerity measures, and welfare cuts suppressed incomes for lower-income groups. This period also saw a sharp rise in income and wealth inequalities, particularly in the US, with similar patterns observable across other advanced capitalist economies (Siddiqui, 2018).

Thanks to neoliberal policies, the wealthy and large corporations accumulated unprecedented levels of wealth. The number of billionaires surged from 66 in 1990 to 813 by 2024, accompanied by a steep increase in their combined net worth. Forbes reported that the total wealth of US billionaires reached $6.72 trillion in 2024, with several individuals surpassing $100 billion each in personal wealth. The US’s richest 1% increased their share of total wealth from 22.8% in 1989 to 30.8% by 2024. A closer breakdown shows that the top 0.1% alone held 13.8% of the nation’s wealth, while the remaining 0.9% within the top 1% controlled another 17%. In dollar terms, the top 1% commanded an estimated $49.2 trillion in 2024.

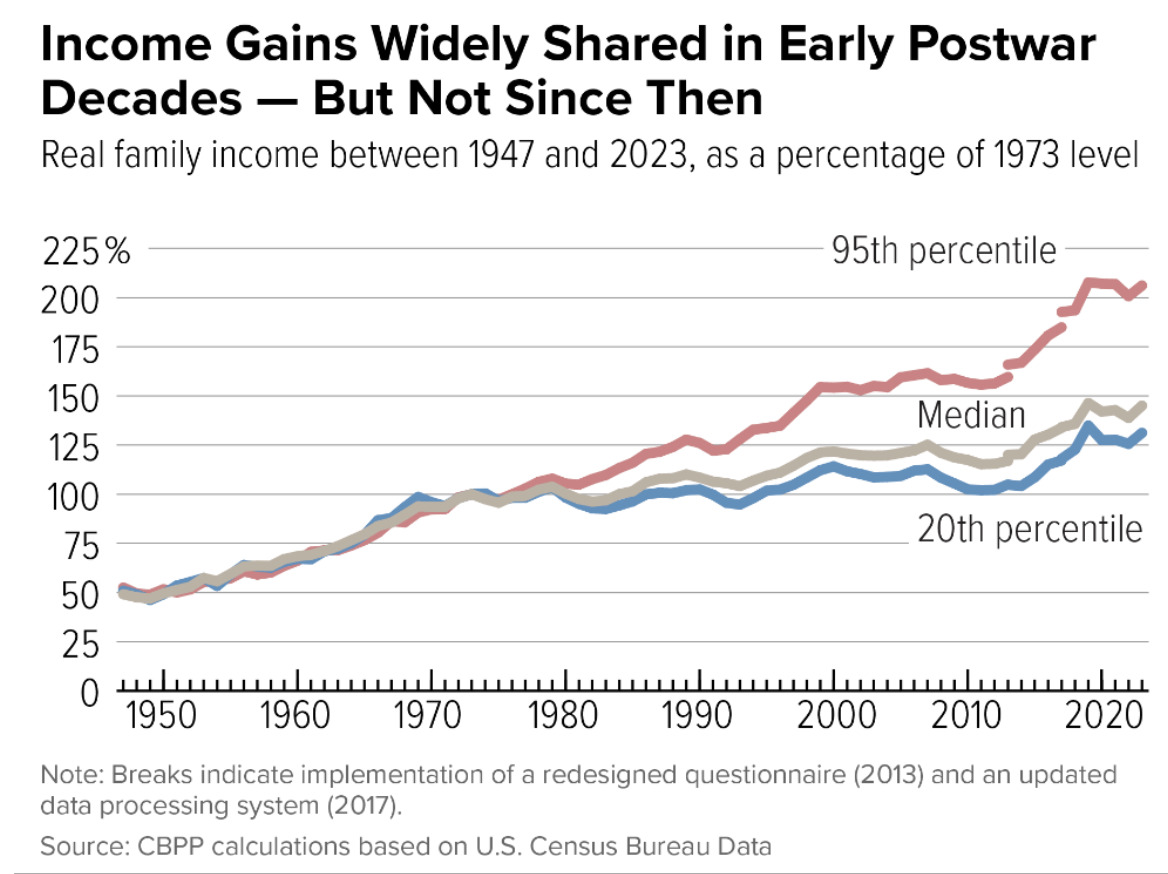

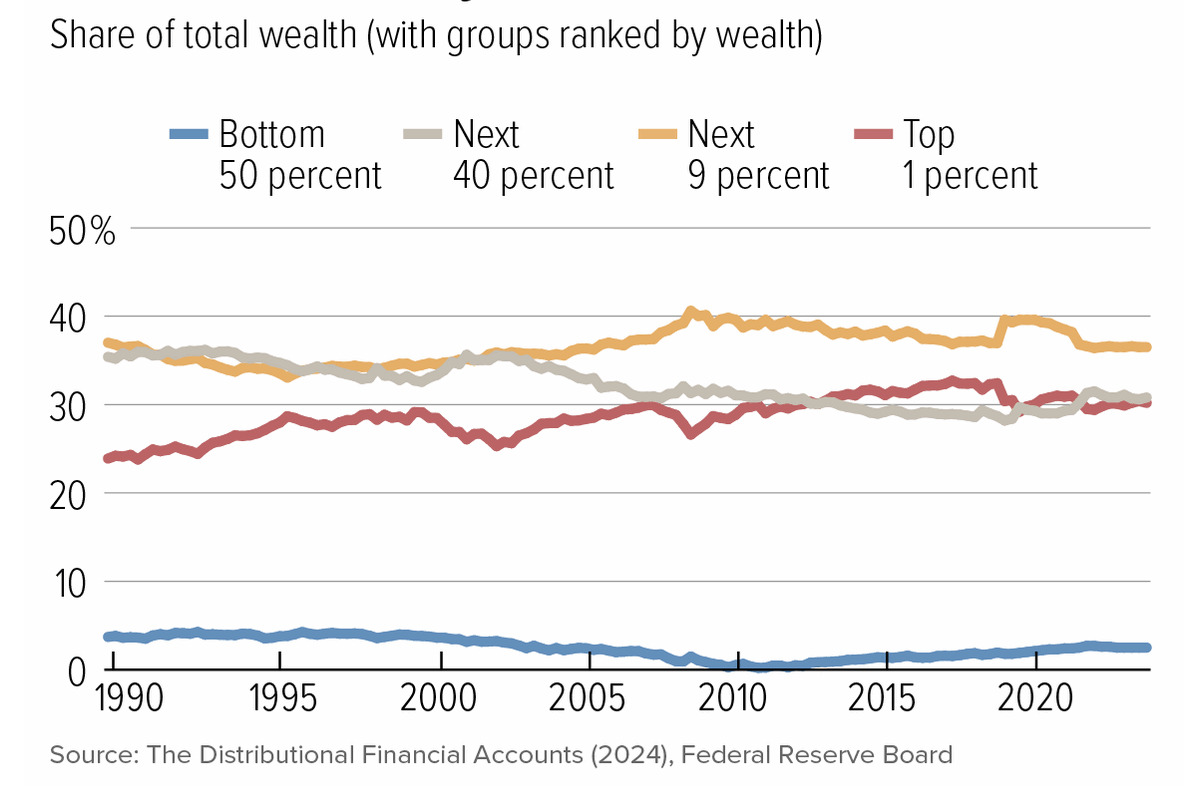

In contrast, the bottom 50% of the population saw their share of national wealth shrink from 3.5% in 1989 to just 2.8% in 2024—reflecting deepening wealth inequality. The US GINI coefficient, a measure of inequality, rose from 34.8 in 1980 to 41.3 in 2024, signalling an alarming trend. Between 1983 and 2016, the share of wealth held by upper-income families increased from 60% to 79% (see Figure 4a), while middle-income families’ share declined from 32% to 17%. From 1990 to 2023, the top 20% of earners expanded their wealth share from 61% to 71%, while the bottom 20% remained stagnant at around 3% (See Figure 4b).

The most recent Federal Reserve data on wealth distribution are presented in its Distributional Financial Accounts of the US. These accounts, which begin in 1989 and are updated quarterly, provide detailed information on the share of wealth held by households across four groups: the bottom 50%, the next 40%, the next 9%, and the top 1%. The data reveal that households in the bottom 50% consistently hold no more than 4% of total wealth, while households in the top 10% control over two-thirds. Moreover, the Distributional Financial Accounts show that wealth concentration at the very top has steadily increased since 1989, reflecting a deepening inequality within the US economy.

Figure 4a: Real Family Income Between 1947 and 2023 as a percentage of 1973 level.

Figure 4b: Share of Total Wealth from 1990 to 2024 (with groups ranked by wealth in %).

VII. The Rise of Public Debt, Foreign Holdings, and Trade Imbalances

Rising trade deficits and growing public debt have further deepened the crisis in the US economy. Tax cuts for the wealthy, intended to stimulate investment, have instead contributed to reduced federal revenue and a sharp increase in public borrowing. US government debt, largely issued in the form of Treasury bonds and securities, has expanded significantly since the 2008 financial crisis. These securities are widely regarded as safe investments and play a critical role in financing federal expenditures.

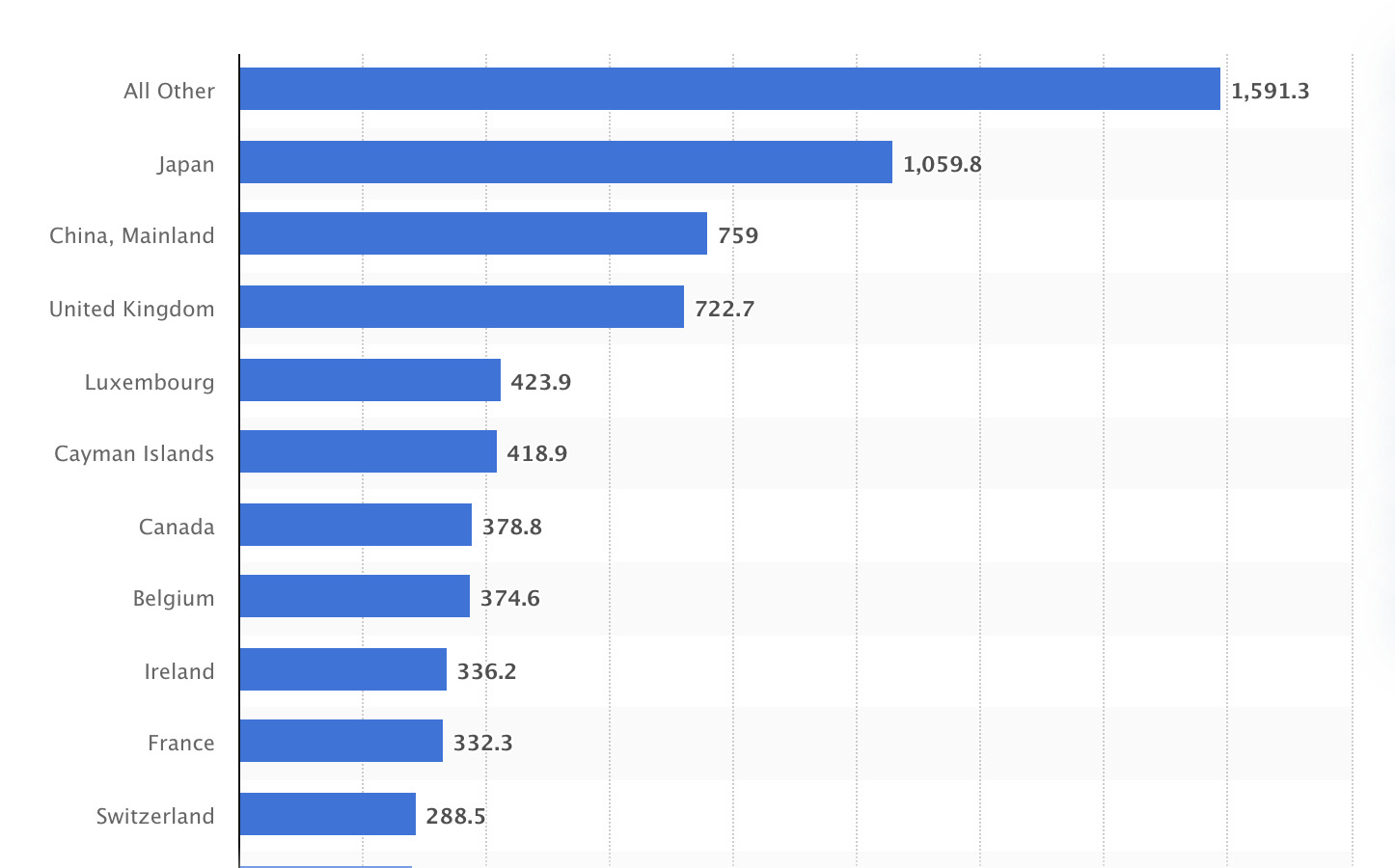

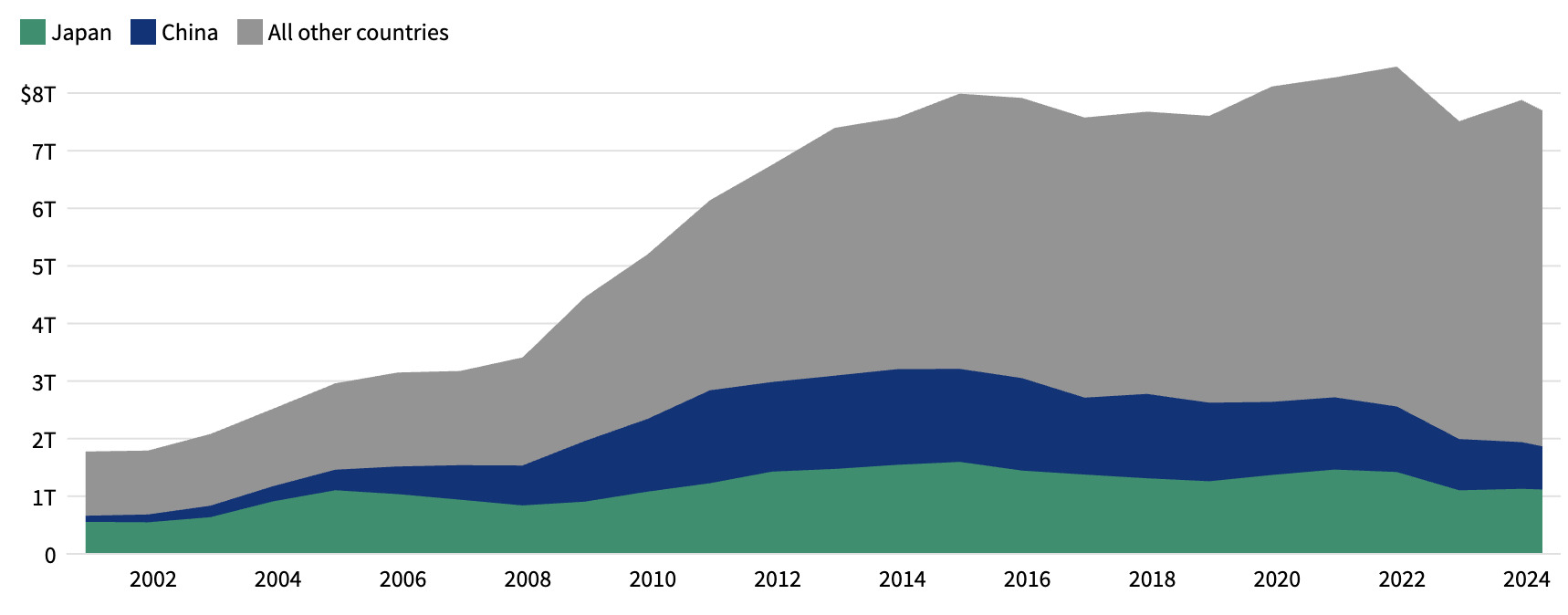

As of December 2024, foreign entities collectively held approximately $8.5 trillion in US Treasury securities. Japan remained the largest individual holder, with over $1 trillion, followed by China at around $759 billion, and the UK at $723 billion. In recent years, both Japan and China have reduced their holdings. Foreign investment in US debt reflects not only US’s borrowing needs but also the central role of the US dollar as the world’s primary reserve currency.

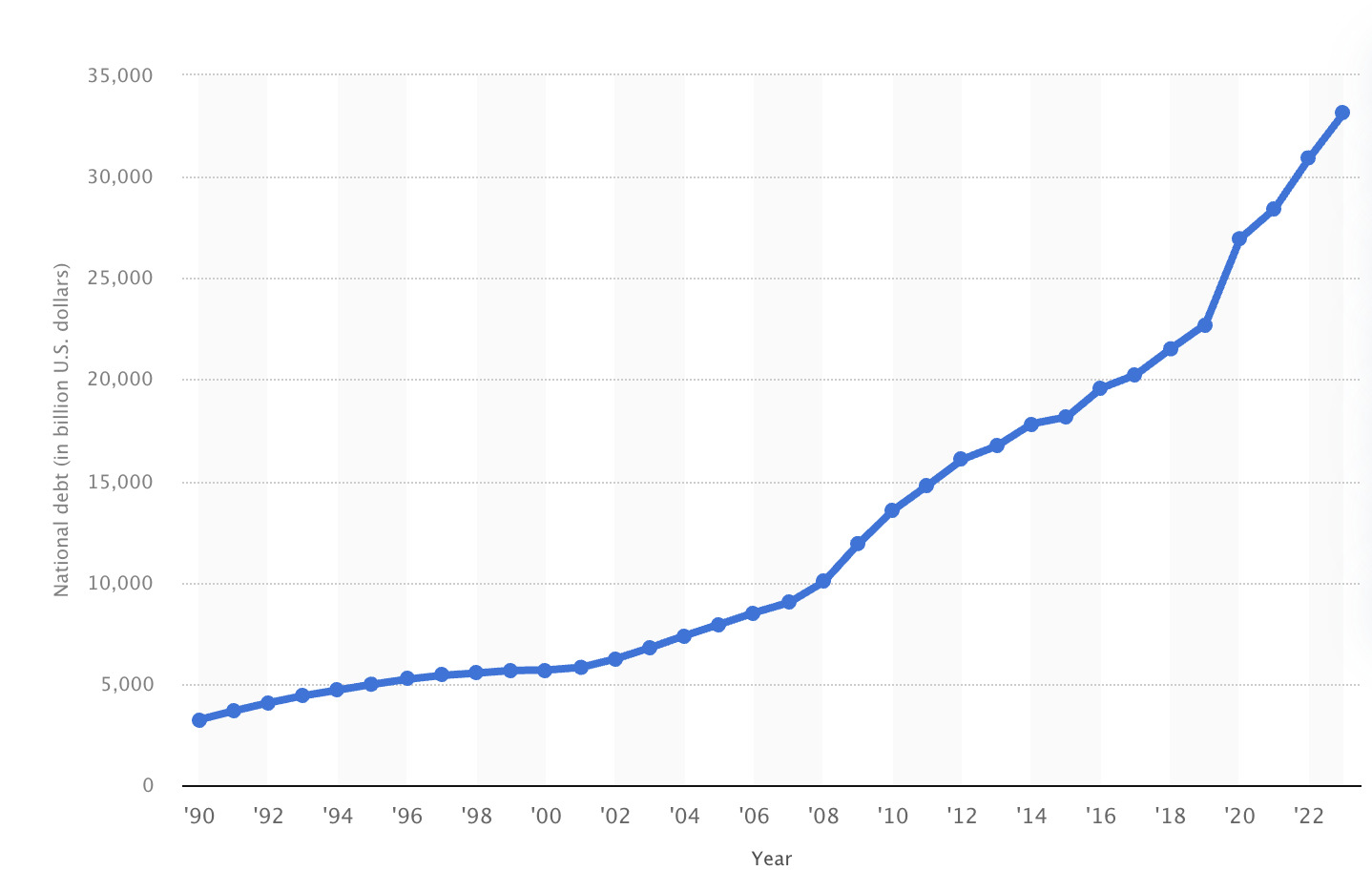

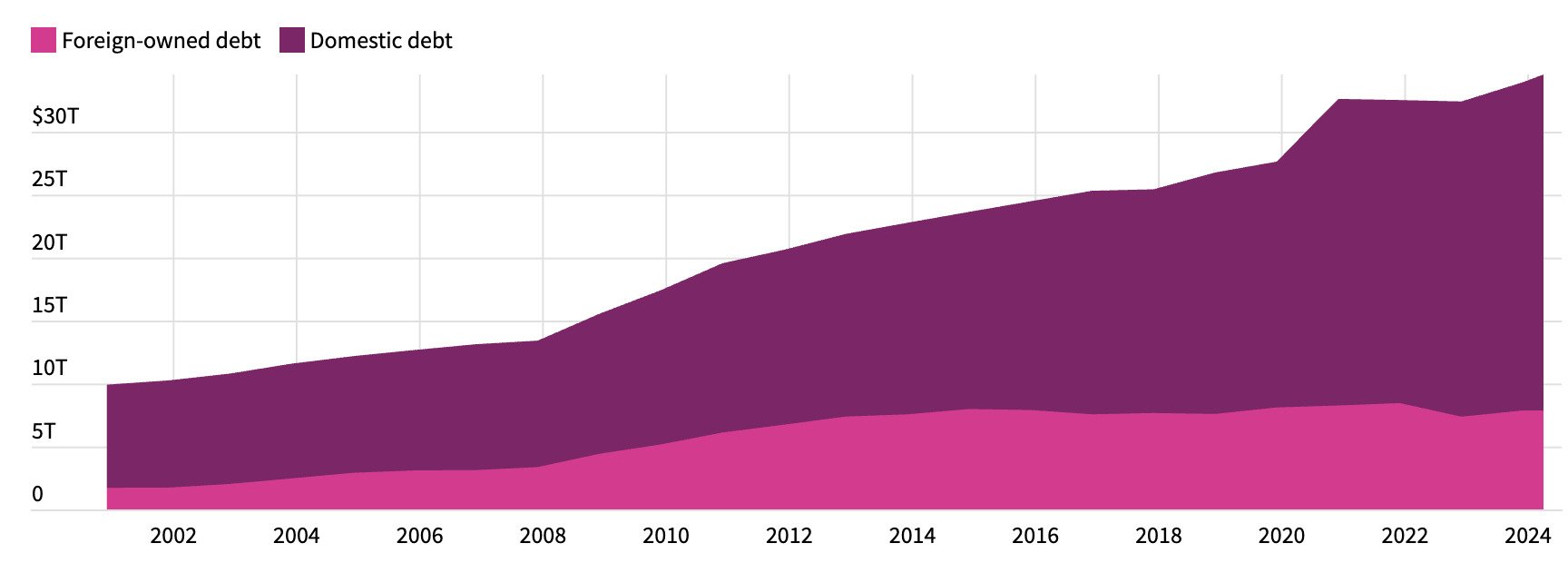

By February 2025, total US federal debt had reached $35.4 trillion (See Figure 5). Although China was long the largest foreign holder of US Treasury securities, it has since been overtaken by Japan (see Figure 6). The continued growth of US debt, and the reliance on foreign financing underscore the structural vulnerabilities in the US economy. Domestic and foreign debts both have risen for the last two decades (See Figure 7a).

Figure 5: Public Debt of the US from 1990 to 2023 (in billions of US$).

Figure 6: Major Foreign Holders of the US Treasury Securities, December 2024 (in US$ billion).

Figure 7a: Total US National Debt, Separated by Ownership, adjusted for inflation, 2000-2024.

Figure 7b: Foreign-owned US Debt, adjusted for inflation, 2000-2024.

In 2000, foreign ownership of US government debt stood at $1.8 trillion, or 17.9% of total debt. By 2014, this share had risen to $8.0 trillion, or 33.9%, the highest percentage in US history. Over the past two decades, Japan and China have consistently been the largest foreign holders of US Treasury securities. From December 2000 to April 2024, Japan’s holdings grew from $556.3 billion to just over $1.1 trillion, while China’s holdings increased from $105.6 billion to $749.0 billion (as illustrated in Figure 7b).

The US currently runs a trade deficit, meaning that the value of its imports exceeds that of its exports. The US policymakers often attribute this imbalance to unfair trade practices by other countries and have responded with tariffs aimed at correcting the deficit. However, this perspective overlooks structural issues within the US economy itself. The trade deficit is not solely the result of external factors, but rather reflects domestic economic behaviour—specifically, the tendency to consume more than is produced.

The US has persistently run current account deficits because it spends more than its national income, borrowing the difference from abroad. For instance, in 2024, the US federal government spent approximately $2 trillion more than it collected in revenue. Contributing to this fiscal imbalance is a reluctance to raise taxes on high-income earners, partly due to concerns that they might relocate to countries with lower tax rates.

In addition to domestic policy factors, geopolitical considerations also influence trade policy. Tensions with China, for example, are often framed in economic terms, though they are also driven by the perception of China as a rising global competitor. China’s economic growth and increasing global influence have positioned it as a formidable rival to the US, exacerbating existing trade tensions.

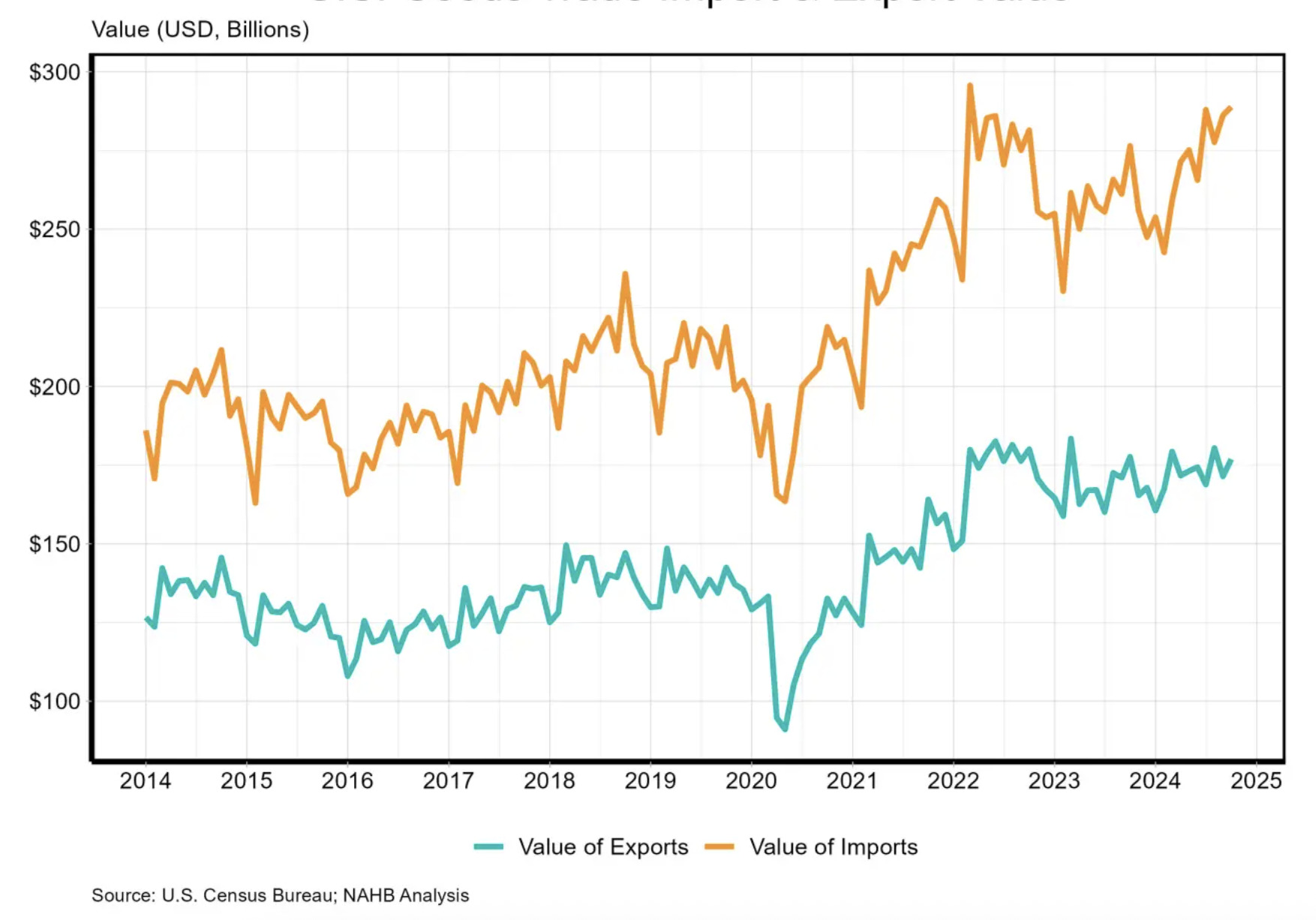

As of April 2025, the US trade deficit in goods and services reached $140.5 billion, up from $123.2 billion in February. The goods trade deficit alone rose to $163.5 billion in March 2025, marking a record high. These figures underscore a sustained trend: over the past decades, the US has frequently experienced trade deficits, with varying intensity. Countries contributing significantly to the US trade deficit include China, Ireland, France, and Switzerland. While trade deficits can signal strong domestic demand, they may also negatively impact GDP by increasing reliance on imported goods and reducing domestic production.

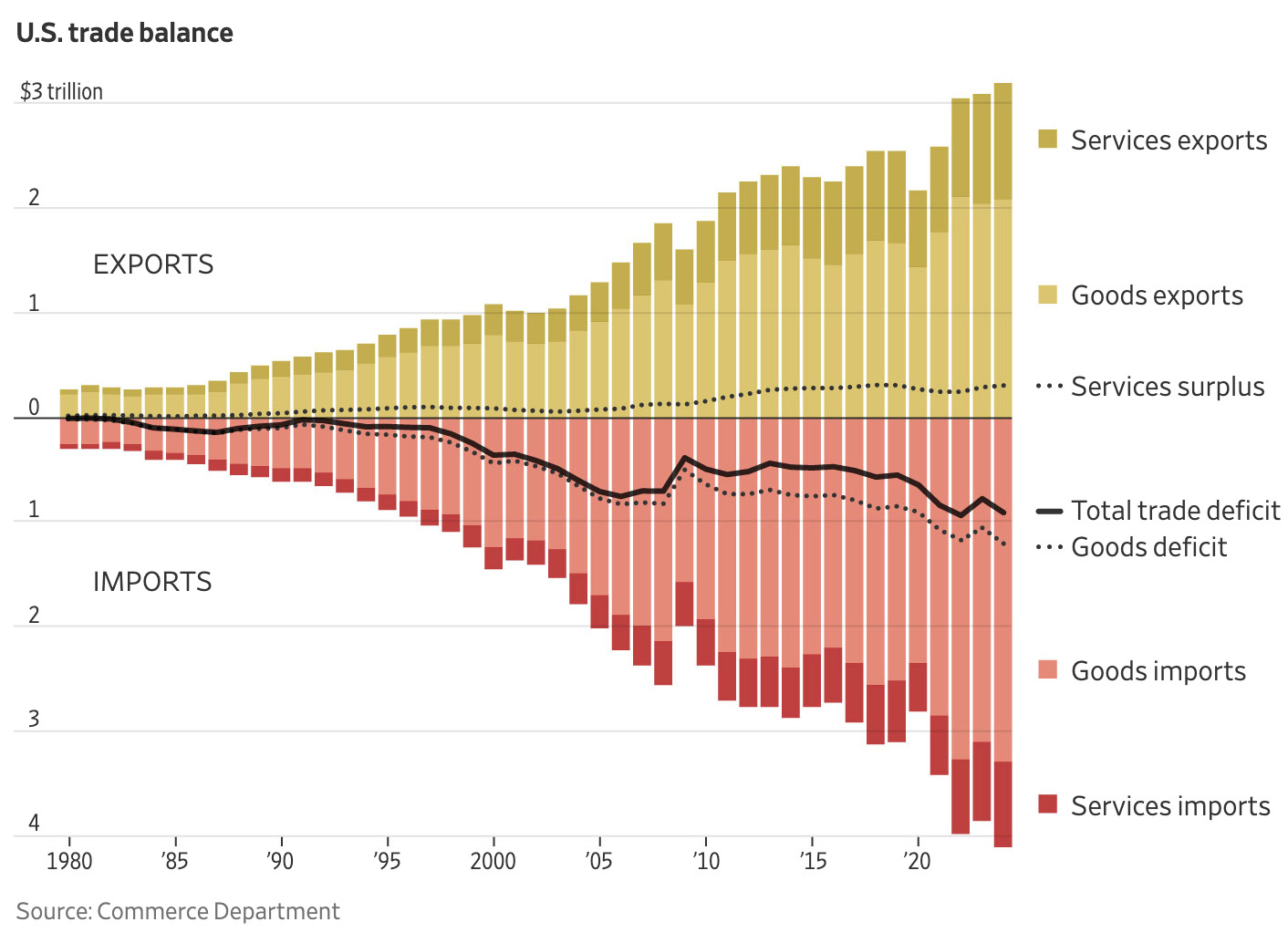

These trends are further illustrated in Figure 8a, which presents the US trade balance from 1980 to 2024, highlighting cyclical periods of deficits and surpluses. Figure 8b shows the value of US goods imports and exports from 2014 through April 2025, offering a visual representation of the growing disparity between imports and exports in recent years.

Figure 8a: The United States Trade Balance, 1980-2024.

Figure 8b: The United States Goods Trade: Imports and Export Values, 2014 – April 2025.

VIII. Conclusion: The Long-Term Crisis of US Capitalism

The US capitalist system is undergoing a deepening and long-term crisis (Siddiqui, 2023). While neoliberalism’s ideological hegemony and the dominance of finance capital remain strong, the systemic unsustainability of the US-led order is becoming increasingly evident. The crisis of liberal democracy and the erosion of the postwar international order reflect the broader decline of US imperialism, though a strong alternative systemic challenge has yet to emerge (Cheng and Baolin, 2021).

Over the past four decades of neoliberal globalization, the US economy has undergone a profound transformation. This era has been marked by de-industrialization, job insecurity, rising income and wealth inequality, falling aggregate demand, and sharply rising public debt (Siddiqui, 2019b). As the US economy shifted toward a monopoly-capitalist model, where financial expansion increasingly overshadowed production, the system became not only more unequal but also more fragile. Financial markets, inherently unstable and driven by the unpredictable credit cycle, came to dominate. As the financial sector grew disproportionately large relative to stagnant production, the economy became more susceptible to risk, ultimately resulting in greater economic inequality and frequent state interventions, including massive infusions of capital by central banks (Cheng and Baolin, 2021).

Karl Marx had argued that the state in capitalist societies is ultimately controlled by the capitalist class. However, he recognized that historical conditions might lead to variations in how this control manifests. In The Eighteenth Brumaire of Louis Bonaparte, Marx discussed instances where the capitalist class did not directly rule, allowing for semi-autonomous governance, as long as it did not challenge the economic interests of capital. He also acknowledged that the state could be dominated by different factions within the capitalist class. Central to Marx’s theory was the concept of the state’s relative autonomy from capitalist interests, a crucial idea in Marxist theories of the state.

In recent years, with the onset of global crises, there has been a resurgence of interest in Marx’s analysis of capitalism’s instability. This “Marx renaissance” reflects his enduring ability to explain contemporary economic issues, especially in the context of US capitalism in the early twenty-first century. Scholars have increasingly turned to Marx’s economic writings to critique the challenges facing developed capitalist economies today.

The parasitic stage of capitalism has strengthened the dominance of finance capital across capitalist countries. The global network of finance capital now supports the US political-military strategy, with bourgeois states increasingly relying on security measures to suppress dissent. However, US allies are struggling with internal discontent and the consequences of economic stagnation and political dependency. (Siddiqui, 2023). While the US retains political and military hegemony, the erosion of its economic base is likely to hasten the decline of US capitalism.

About the Author

Dr. Kalim Siddiqui is an economist specializing in International Political Economy, Development Economics, Trade and Economic Policy. Since 1989, he has been teaching economics at various universities in Norway and the UK. Dr. Siddiqui’s research interests encompass a wide range of topics, including political economy, international trade, and economic history, South Asia, and emerging economies. He has presented papers at international conferences across numerous countries, reflecting his global engagement in the field. His scholarly pursuits span six broad domains: Political Economy, Development Economics, Economic History, Economic Policy, Globalization, and International Trade. Dr. Siddiqui has made significant contributions to research in areas such as trade policy, globalization, and political economy. His work has been published in chapters of edited books and articles published in peer-reviewed journals. For inquiries, Dr. Siddiqui can be reached at: [email protected]

Dr. Kalim Siddiqui is an economist specializing in International Political Economy, Development Economics, Trade and Economic Policy. Since 1989, he has been teaching economics at various universities in Norway and the UK. Dr. Siddiqui’s research interests encompass a wide range of topics, including political economy, international trade, and economic history, South Asia, and emerging economies. He has presented papers at international conferences across numerous countries, reflecting his global engagement in the field. His scholarly pursuits span six broad domains: Political Economy, Development Economics, Economic History, Economic Policy, Globalization, and International Trade. Dr. Siddiqui has made significant contributions to research in areas such as trade policy, globalization, and political economy. His work has been published in chapters of edited books and articles published in peer-reviewed journals. For inquiries, Dr. Siddiqui can be reached at: [email protected]

References

- Cheng, Enfu, and Baolin, Lu (2021) “Five Characteristics of Neo-imperialism” Monthly Review 73(1) May, New York.

- IMF (2025) World Economic Outlook Update. April.

- Patnaik, P. (1997) Accumulation and Stability under Capitalism, Oxford: Oxford University Press.

- Siddiqui, K. (2025a) “Understanding the Rise of High Technology in China” World Financial Review, March.

- Siddiqui, K. (2025b) “Donald Trump’s Tariffs: A Prelude to Global Trade Wars?” World Financial Review, April.

- Siddiqui, K. (2025c) “The Political Economy of Germany’s Deepening Economic Crisis” World Financial Review, February.

- Siddiqui, K. (2024a) “Trends and Prospects of De-Dollarization in the Rapidly Changing Global Economy” Part One and Part Two, World Financial Review, December.

- Siddiqui, K. (2024b) “The Decline of the West and Global Political Economy” World Financial Review, December.

- Siddiqui, K. (2024c) “Deepening Economic Crisis in the Advanced Capitalism” World Financial Review, June.

- Siddiqui, K. (2024d) “China’s Growth Miracle and Development Strategy Since the 1980s” World Financial Review, December.

- Siddiqui, K. (2023) “Marxian Analysis of Capitalism and Crises” International Critical Thought 13(4): 525-545.

- Siddiqui, K. (2022a) “Is a Global Economic Recession Looming” World Financial Review, September.

- Siddiqui, K. (2022b) “Capitalism, Imperialism, and Crisis” European Financial Review, July.

- Siddiqui, K. (2021). “Can the 21st Century be an Asian Century?” Asian Profile 49(1): 1-19, March.

- Siddiqui, K. (2020) “Prospects of a Multipolar World & the Role of Emerging Economies” World Financial Review, November.

- Siddiqui, K. (2019a). “The US Economy, Global Imbalances under Capitalism: A Critical Review” Istanbul Journal of Economics 69(2):175 – 205, December.

- Siddiqui, K. (2019b). “Financialisation, Neoliberalism and Economic Crises in the Advanced Economies” World Financial Review, May.

- Siddiqui, K. (2018). “Capitalism, Globalisation and Inequality” World Financial Review, November.

- Siddiqui, K. (2017) “Financialization and Economic Policy: Issues of Capital Control in the Developing Countries” World Review of Political Economy 8 (4):564 – 589.

- World Bank (2024) “World Bank Open Data.” World Bank Open Data. August 12. https://data.worldbank.org

{kind=link}