By Kalim Siddiqui

This article attempts to provide a deeper explanation for the United States’ trade imbalances, which U.S. President Donald Trump has cited as a pretext to impose tariffs and catastrophic retaliatory measures while ignoring the structural weakness of the U.S. economy itself. Such unilateral action has a profound impact on the global economy and institutions such as the WTO.

Initially, Trump targeted imports of steel and aluminium from several key trade partners, including the European Union and South Korea, and just recently, he imposed another series of protectionist measures that went beyond any previously seen in the post-war period. The reasoning given for imposing such high tariff duties is the U.S.’ perception of the “unfair” trade practices currently being enacted by China. China responded to this by adopting a tit-for-tat strategy of imposing tariffs on selected U.S. products. Since August this year, both countries have together imposed tariffs on $100 billion worth of goods and which will almost certainly escalate further with increased trade retaliation (Guardian, 2018).

An ongoing trade war between the U.S. and China would adversely affect global economic growth, and their unilateral actions on trade apparently seem to be designed to bypass the rules set by the WTO, and could thus have a serious impact on global trade and governance. It seems clear that the U.S. is purely diverting attention from its own structural problems, and which are ultimately themselves responsible for imbalances in trade. President Trump, however, is attempting to establish a (probably erroneous) link between rising U.S. imports and the decline in its manufacturing industries.

Since August this year, both countries have together imposed tariffs on $100 billion worth of goods and which will almost certainly escalate further with increased trade retaliation.

The recent increase in import tariffs by the U.S. in its steel and aluminium sectors is claimed to be an important step towards helping its domestic steel and aluminium industries. President Trump imposed import duties of 25% on steel and 10% on aluminium by invoking the Trade Expansion Act of 1962 that allows for the protection of domestic industries on the grounds of national security (Guardian, 2018). However, this act is in clear violation of the WTO’s multilateral trade rules – which the U.S. leadership itself help to negotiate – where then U.S. agreed that developing countries could reduce their import tariffs by a small proportion compared to more advanced economies worldwide (Siddiqui, 2016a).

This principle of non-reciprocity was accepted as the basis for tariff cuts at the WTO’s Doha Round negotiations (Siddiqui, 2015a). This unilateralism is seen as discriminatory against a number of countries that includes China, and which is a clear violation of WTO rules. It is inconsistent with the provisions of the WTO’s Dispute Settlement Understanding (DSU). Article 23(a) of the DSU is obligatory for every member, who is advised that rather than make a judgement on other acts, their grievances must instead be taken directly to the DSU. The WTO’s dispute settlement process has sole authority to adjudicate in, and to resolve, any dispute between members (WTO, 2015).

Ironically, it is China that seems to be most interested in restoring and saving the tattered economic order. The U.S. has witnessed a sudden reversal of its fortunes that to a large extent were brought about by a number of factors including its engagement with an open economic order, and also by giving further concessions to its own large corporations and its pursuit of the policy of deregulation, rather than providing incentives to big corporations to invest locally in more productive sectors of the economy and to create jobs.

Economic theory holds that trade surpluses are a sign of an undervalued currency (Siddiqui, 2016b; also see Siddiqui, 1998). During the Presidential election campaign, Trump repeatedly accused China of pursuing unfair trade practices through currency manipulation, subsidies and stealing intellectual property rights from U.S. companies. However, after becoming President, Trump did not speak about the fact that the Chinese yuan has risen 8.6% against the U.S. dollar since January 2017. Indeed, since Trump took over, U.S imports from China have increased from $463 billion in 2016 to $506 billion in 2017. As a result, the trade deficit has widened from $347 billion in 2016 to an all-time high of $375 billion in 2017 (McBride, 2017). That means that China accounts for nearly half (43.6%) of America’s total trade deficit with the entire world.

Concern about China’s trade policy was also apparent during the Obama administration. The U.S. has for some time been reviewing policy options as to how to deal with China’s growing economic power, and questions were raised in Congress about the need for a shift in U.S. policy towards China.

During the Presidential election campaign, Trump repeatedly accused China of pursuing unfair trade practices through currency manipulation, subsidies and stealing intellectual property rights from U.S. companies.

For instance, in 2017, the U.S. Trade Representative to Congress stated that “It seems clear that the United States erred in supporting China’s entry into the WTO on terms that have proven to be ineffective in securing China’s embrace of an open, market-oriented trade regime”.

The present trading system began to emerge at the end the Second World War when representatives of 44 countries, largely from Europe, North America and Latin America, met in Bretton Woods in the U.S. to lay the foundation of a new international economic order suitable to the new world leader, i.e., the US. Moreover, one of the most important tasks was to create a system, which could reduce the tension between countries by increased trade and economic cooperation among capitalist countries (Siddiqui, 2018a). The governments of the developed economies then prioritised higher levels of employment, and a number of further measures were undertaken to improve the living conditions of the populace. The period between 1950 and 1972 was known as the “Golden Age of Capitalism”, when average incomes in North America, Europe and Japan grew at a faster rate than they had for over the past century.

In the 1980s and the 1990s, trade and investment policies changed radically, and in 1994 the WTO was established. Rather than regulating investment and finance towards productive investments and the creation of employment, as attempted in previous decades, they instead deregulated. Deregulation was also imposed on developing countries by IMF/World Bank-led neoliberal reforms, also known as the “Structural Adjustment Programme” (Girdner and Siddiqui, 2008).

Trade liberalisation has been very good for the United States for the last seven decades or so, but this no longer seems to be the case (Siddiqui, 2018b). The U.S. extended its full support to corporate globalisation in the hope that this would create a new era for U.S. dominance, but since 1990s free trade deals negotiated through the WTO have benefitted U.S. much less than expected, and indeed are currently shrinking. U.S. corporations, rather than investing profits from globalisation into productive and employment-generating areas of the economy, choose instead to shift their capital into speculation.

For the last three decades or more, financialisation of the economy has expanded rapidly in both the U.S. and the rest of the world. This has defined the massive and extensive accumulation of interest-bearing capital, and has profoundly transformed the organisation of economic and social reproduction. These transformations not only include the outcomes but also the structures, processes, agencies and relations through which those outcomes are determined across production and employment.

According to the World Bank, the overall investment level in the United States has fallen from 25% of GDP in 1980 to 19% in 2017. Since the 2008 financial crisis, the U.S. economy, despite some recent signs of improvement, is still far from achieving sustained economic growth.

Financialisation encapsulates the increasing role of globalised finance in ever more areas of economic and social life. In the United States and other advanced economies, Fine and Saad-Filho (2017:692) argue that: “the realisation that the operation of key neoliberal macroeconomic policies, including ‘liberalised’ trade, financial and labour markets, inflation targeting, central bank independence, floating exchange rates and tight fiscal rules, is conditional upon the provision of potentially unlimited state guarantees to the financial system, since the latter remains structurally unable to support itself despite its escalating control of social resources under neoliberalism”. However, soon after the global financial crisis of 2008, as Adam Tooze (2018) explains that in the U.S. and Europe, “The failures of banks forced “scandalous government intervention to rescue private oligopolists” (Cited in Wolf, 2018).

Ten years have passed since the global financial crisis of 2008 which nearly reduced capitalism to bankruptcy. However, it did not lead to the same kind of complete meltdown as happened in the Great Depression of 1930 for the majority of the developed economies. The 2008 crisis affected the global economy adversely, particularly developed economies, with a subsequent decade of slow growth, low investment, and low productivity which has further been marked by increased public debts and current account deficits. According to the World Bank, the overall investment level in the United States has fallen from 25% of GDP in 1980 to 19% in 2017 (McBride, 2017). Since the 2008 financial crisis, the U.S. economy, despite some recent signs of improvement, is still far from achieving sustained economic growth.

At the same time, the Chinese economy was, at least initially, adversely hit by the global financial crisis, (Siddiqui, 2015b) but the country was able to recover in only a short period; a decade later, the country had emerged as a major economic power. In China, state capitalism was seen as an important policy tool with which to assist the economy and state-owned enterprises were not abandoned, as happened in the early 1990s in Russia. As a result, since the crash China has emerged as the world’s second-largest economy and the world’s biggest manufacturer and exporter of goods (Siddiqui, 2015c). During the same period, the U.S. economy has, relatively speaking, weakened, and consequently Trump considers China to represent a serious threat U.S. trade hegemony (Wolf, 2018).

Between 2009 and 2017, the Chinese economy tripled in size, and by 2012 had overtaken Japan as world’s second largest economy. Its economic growth continued at a rate of around 10% until 2011, and thereafter by nearly 7% per annum, which is above the worlds’ average economic growth of 3.9%. China’s per capita income had risen from $3,500 in 2009 to $8,800 in 2017. In 2017, China created 11 million jobs compared to just 1 million in India.

In recent years, China has begun to move away from low-cost, export-led growth towards a gradual increase in domestic consumption and the acquisition and development of a high-tech base. As a result, the trade to GDP ratio has fallen from 37% in 2008 to 20% in 2017, while the domestic consumption of GDP has increased steadily since 2012. There is further evidence that China has been undergoing a structural change in recent years. For example, between 2011 and 2017, the share of earlier key industries such as cement, steel, coal and iron declined from 75% to 60%, while for the same period the share in other sectors such as energy, healthcare, entertainment and high-tech has risen and service sector employment has increased from 33% to 45% over the same period. Moreover, in 2017, China had 109 companies in Fortune Global 500, which has risen from 10 in 2001 to 30 in 2008 (McBride, 2017).

Between 2009 and 2017, the Chinese economy tripled in size, and by 2012 had overtaken Japan as world’s second largest economy.

The recent initiative by Chinese President Xi Jinping, “Made in China 2025”, sets out plans to develop Chinese technology in key industries such as aircrafts, robotics, pharmaceuticals and defence. This has further antagonised the U.S.; the U.S. Trade Representative described it as an attempt at “seizing economic dominance of certain advanced technology secto rs” (McBride, 2017).

Moreover, China is challenging the advanced economies monopoly in robotics and 3D printing. The Chinese government has undertaken a huge investment drive in aviation engines, electronic chips and set a target to become the largest investor in R&D in the world. Despite all these changes, the United States wants to keep the U.S. dollar as the de facto global currency, even at the expense of huge trade deficits.

The question arises as to whether the United States’ protectionism is justified. Therefore, in order to assess this, we will attempt to take a somewhat long-term view regarding the external payments situation of the U.S. Figure 1 provides a summary of the external sector of the country from just before the breakdown of the Bretton Woods System in 1971.

To understand the situation more clearly, we need to analyse the U.S. trade in goods and services and its current account situation on the basis of available statistics. Figure 1 shows the external sector payments of the US from 1970 to 2016. Apart from few exceptions, most of the time its current account was negative in goods. However, the late 1980s service sector gained a surplus and is steadily rising. Despite these changes, the rise in service export was unable to fill the gap created by the general trade imbalance in goods. Moreover, since 2014, service export has stagnated, which has thus become a real problem for the U.S. The United States trade deficit kept on rising, and has grown remarkably over the last two decades. This was coincidental with the period when China joined WTO, all of which appears to have given the U.S. the excuse to blame China for raising its trade deficits.

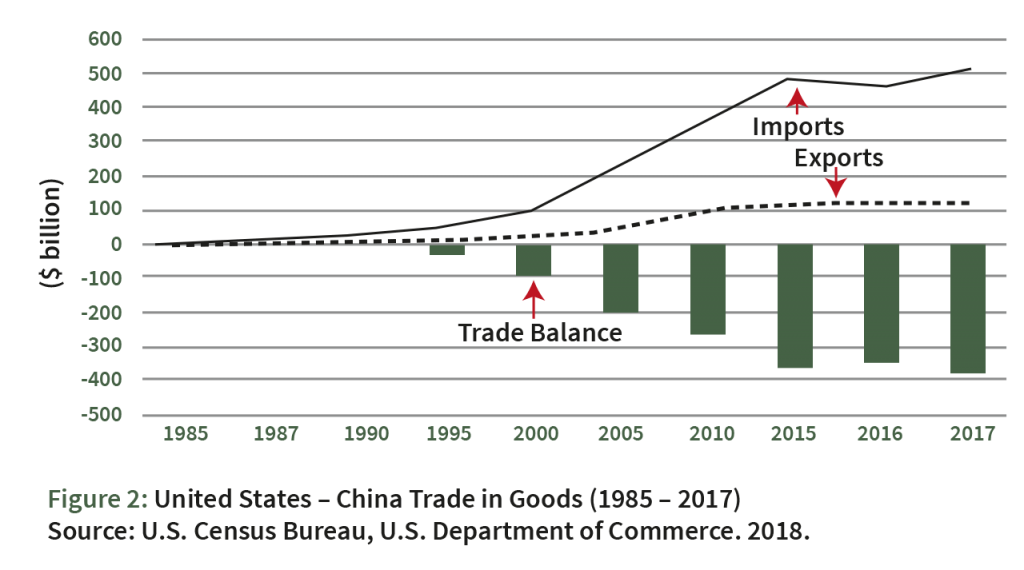

Figure 2, which shows the trade in goods between the U.S. and China, indicates that the U.S. had trade deficits in goods with China since the early 1990s, which has grown up sharply. For example, the deficit was only $10 billion in 1990, but by 2000 had reached $100 billion; by 2005 it had risen further to $200 billion, by 2012 it rose to $315 billion, and by 2017 it had reached $376 billion. The sharpest rise was since 2001, which also coincided with China joining the WTO. For example, China’s exports to the U.S. increased from $125 billion to $505 billion, while U.S. exports to China rose from merely $19 billion to about $130 billion for the same period.

The question arises as to the extent to which China is responsible for the U.S.’ rising trade deficit. To answer this, we need to examine the US trade performance with the other major trading partners.

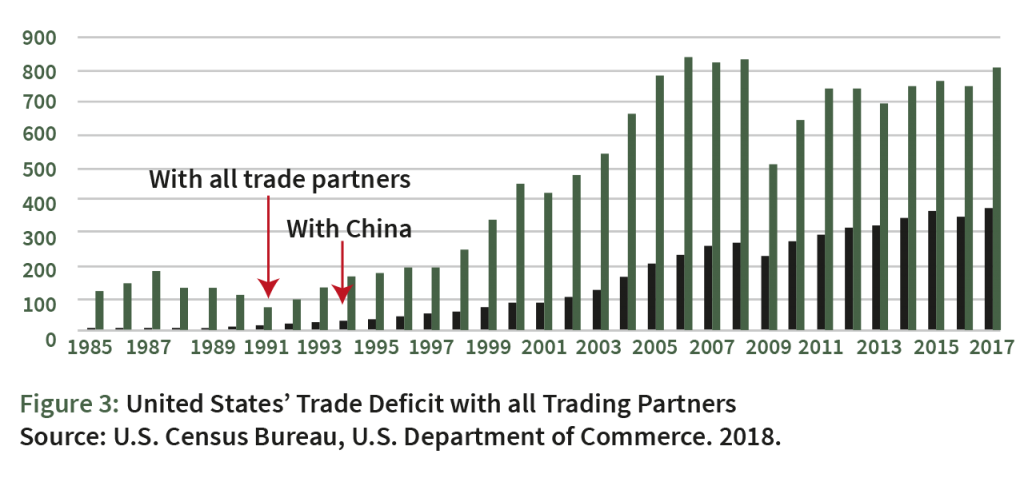

Figure 3 indicates that China is an important trading partner for the U.S., but that China still has less than half of the U.S.’ overall trade deficits. For example, according to the statistics, in 2017 the U.S.’ trade deficit with China was $375 billion, however, its overall trade deficit was $775 billion. This means that even if the U.S. were to eliminate its trade deficit with China, its trade imbalance problems would still exist.

China is largely facilitating the final assembly stages of global production networks of vertically integrated high-tech industries. To explore the magnitude and patterns of trade arising from cross-border production networks, it is necessary to separate parts and components from final assembled products traded within global production networks. The U.S. trade war, if broadened, will adversely affect U.S. corporations as well.

Exports of global production network (PN) exports from China rose from $47 billion in 1993 to $1.3 trillion in 2015, where these products accounted for more than 70% of China’s total manufacturing exports as indicated in Figure 4. This pattern shows China’s dominant role as an assembly centre within global production networks. In 2015, China accounted for 27% of the total global network product exports worldwide, compared with an 18% share in total world manufacturing exports (see Figure 5). This means the shares of both final assembly and components were notably higher than the aggregate global export share.

In fact, U.S. trade imbalances are largely self-inflicted. The U.S. needs to address factors within its economy rather than blaming others, especially China. Trade deficits (i.e., imports more than export), reflects the saving-investment gap in terms of national income, which is associated with low levels of domestic saving rates (Siddiqui, 2016c). Most economists and policy makers have barely touched on this important issue, namely that consumption has risen while saving rates have declined, or otherwise remained low. For example, the U.S. domestic savings rate was never higher than 24% in the 1950–60s, but for the last two decades it has steadily declined and is now below 17% (McBride, 2017).

In conclusion, the article indicated that there are serious structural weaknesses in the U.S. economy which needs to be addressed. Blaming its trading partners might help the U.S. in the short term, but will certainly not be effective in the long term. Trump, rather than addressing structural crisis, has taken the initiative to cut corporation tax and increase tariffs, which seems to give short-term relief and will at the same time increase imports. In 2002, during the Bush administration, higher tariffs were imposed on imported steel and aluminium, but rather than helping, this adversely affected the automotive and construction industries, which are amongst the largest employers in the U.S.

The United States has witnessed a decade of slow growth, low investment, and low productivity, all of which has been further marked by increased public debts. All of these factors have contributed towards higher levels of current account deficits. Further, by raising import tariffs, the U.S. has violated the WTO’s multilateral trade rules, which ironically were negotiated earlier under the United States’ leadership.

About the Author

Dr. Kalim Siddiqui teaches International Economics at University of Huddersfield, UK. He is an economist, specialising in Development Economics and has written extensively on development economics, economic reforms as well as on the political economy of development. He may be reached at [email protected].

Dr. Kalim Siddiqui teaches International Economics at University of Huddersfield, UK. He is an economist, specialising in Development Economics and has written extensively on development economics, economic reforms as well as on the political economy of development. He may be reached at [email protected].

References

1. Fine, B. and A. Saad-Filho. (2017). “Thirteen Things You Need to Know about Neoliberalism”, Critical Sociology, 43(4-5): 685-706.

2. Girdner, E.J. and Kalim. Siddiqui. (2008). “Neoliberal Globalization, Poverty Creation and Environmental Degradation in Developing Countries”, International Journal of Environment and Development 5(1):1-27, January-June.

3. Guardian. (2018). “US on Brink of Trade War with EU, Canada and Mexico s tit-for-tat Tariff begins”, 31 May. https://www.theguardian.com/business/2018/may/31/us-fires-opening-salvo-in-trade-warwith-eu-canada-and-mexico.

4. McBride, J. (2017). “The US Trade Deficit: How Much Does it Matter?” Council on Foreign Relations, 17 October. https://www.cfr.org/backgrounder/us-trade-deficit-how-much–does-it-matter.

5. Siddiqui, Kalim. (2018a). “Imperialism and Global Inequality: A Critical Analysis”, Journal of Economics and Political Economy, 5(2): 266-291.

6. Siddiqui, Kalim. (2018b). “David Ricardo’s Comparative Advantage and Developing Countries: Myth and Reality”, International Critical Thought, 8(3): 1-28, September.

7. Siddiqui, Kalim. (2017). “Financialization and Economic Policy: The Issues of Capital Control in the Developing Countries”, World Review of Political Economy 8 (4): 564-589, winter, Pluto Journals. DOI: 10.13169/worlrevipoliecon.8.4.0564.

8. Siddiqui, Kalim. (2016a). “Will the Growth of the BRICs Cause a Shift in the Global Balance of Economic Power in the 21st Century?” International Journal of Political Economy 45(4):315-338, Routledge Taylor & Francis.

9. Siddiqui, Kalim. (2016b). “A Study of Singapore as a Developmental State” in edited by Young-Chan Kim. Chinese Global Production Networks in ASEAN, pp.157-188, London: Springer.

10. Siddiqui, Kalim. (2016c). “International Trade, WTO and Economic Development”, World Review of Political Economy, 7(4):424-450, winter, Pluto Journals.

11. Siddiqui, K. (2015a). “Economic Policy: Sate versus Market Controversy” in edited by Adam P. Balcerzak. Contemporary Issues in Economy: Market or Government, pp.39-63, Torun: European Regional Science Association, Poland.

12. Siddiqui, Kalim. (2015b). “Trade Liberalisation and Economic Development: A Critical Review”, International Journal of Political Economy 44(3):228-247.

13. Siddiqui, Kalim. (2015c). “Perils and Challenges of Chinese Economic Development”, International Journal of Social and Economic Research 5 (1): 1-56.

14. Siddiqui, Kalim. (1998). “The Export of Agricultural Commodities, Poverty and Ecological Crisis: A Case Study of Central American Countries”, Economic and Political Weekly 33(39): A128-A137, 26th September.

15. Wolf, Martin. 2018. “What Really Went Wrong in the 2008 Financial Crisis”, Financial Times, 17 July, London. (accessed on 10 September, 2018.http://www.Wolf,Martin.FT.com.

16. World Trade Organisation (WTO). 2015. Ministerial Declaration Adopted on 4 December. https://www.southcentre.int/wp…/2015/12/AN_MC10_4_Ministerial-Declaration.pdf. Also see the dispute settlement system of the WTO – legal text.https://www.wto.org/english/tratop_e/dispu_e/dsu_e.htm

European Union (EU) Security technology background")

Global Economic Outlook after Trump-Xi Timeout

By Dan Steinbock

As many hoped, the highly anticipated Trump-Xi meeting in the Buenos Aires G20 Summit resulted in a truce. The devil is in the details.

As the G20 Summit ended in Buenos Aires, the G20 official summit statement acknowledged flaws in global commerce, called for reforming the World Trade Organization (WTO) and deleted the word “protectionism” after U.S. resistance.

The statement was completed only after hours of diplomatic bargaining over the night. As far as the European Union (EU) was concerned, the U.S. was the lone holdout on almost every issue in Buenos Aires, particularly in climate change.

The G20 economies preferred a diluted final statement to further G20 division.

Tango in Buenos Aires

Following the summit’s close, Presidents Trump and Xi and their top aides met in a highly-anticipated dinner, which lasted longer than expected. Either there was magic dust in their grilled sirloin steaks paired with a malbec from the Argentine winery Catena Zapata. Or perhaps, just perhaps, reason finally prevailed.

Before Buenos Aires, Trump threatened to impose tariffs on an additional $267 billion in Chinese goods. He also indicated he would raise the existing tariff rate on $250 billion in Chinese imports from 10% to 25% on January 1.

According to early reports, U.S. and China agreed to put on hold new tariff increases. Following Buenos Aires, the White House said that, after a “highly successful meeting”, Trump had agreed to leave tariffs on U.S. products at a 10% rate after January 1, while China agreed to buy a substantial amount of products from the U.S.

The White House also said that China has agreed to start purchasing substantial U.S. agricultural, energy, industrial and other products from the U.S. to reduce the trade imbalance; and that the US and China agreed to try to reach an agreement on several trade issues “within the next 90 days.”

The first impression is that the Trump-Xi Summit may have achieved a critical truce, de-escalation of tensions, and possibly a path toward a long-term compromise.

The timeout came at the 11th hour.

Three trade-war scenarios

Last October, Roberto Azevêdo, Director of the World Trade Organization (WTO), said that the trade war between the U.S. and China was far from over. The speech preceded the release of the WTO Indicator, which suggested that trade growth is likely to slow further into the fourth quarter of 2018 and below-trend trade growth in the coming months.

After a sharp upswing in 2017, both exports and imports in Asia had held up very well year-to-date, with continued double-digit growth in many economies. But since the onset of Trump’s tariff wars in spring, elevated uncertainty has haunted the global economy.

According to WTO, merchandise trade volume growth was expected to reach 4.4% in 2018, which is still below the 2017 level. But as Trump’s tariffs have escalated tensions, a fall in business confidence and revised investment decisions may soften the outlook. Moreover, a full trade war could derail trade recovery for years.

According to the UN, global investment flows were projected to resume growth in 2017 and surpass $1.8 trillion in 2018. Thanks to U.S. neo-protectionism, they fell to $1.5 trillion last year. The current status quo looks even gloomier; especially with the trade tensions and central banks’ planned normalization.

Three scenarios illustrate the rising economic stakes of Trump’s tariff wars that have rapidly expanded from a bilateral trade conflict to a potential global trade war.

Last July, U.S. and China imposed 25% tariffs on $34 billion of the other’s imports and levies on another $16 billion. In this $50 billion Muddling Through Scenario, the tariff’s economic impact would have been limited to 0.1% of Chinese GDP and 0.2% of U.S. GDP, respectively.

Recently, Trump has threatened with further tariff escalation. In the ‘America First’ Scenario, the stakes will quadruple to $200 billion, with soaring collateral damage. In China, it could shave off 0.4% of GDP; in the U.S., 0.8% of GDP.

If the stakes of the White House’s tariff war would escalate to $500 billion – Trump’s pre-Buenos Aires goal – the potential collateral damage would increase tenfold from the first scenario. In this Global Trade War Scenario, China’s GDP could take a hit of 1%, but the U.S. GDP would suffer a 2% impact.

How will these trade war scenarios impact global growth prospects?

Three global scenarios

As the global economy has passed its peak, thanks to rising interest rates and global trade tensions, each trade war scenario implies different growth prospects (Figure).

Sources: Difference Group (WEO/IMF growth data)

In the Muddling Through Scenario, both full trade war and ‘America First’ prospects are avoided. A good start would be a bilateral tariff truce starting in early 2019. But it is predicated on successful bilateral diplomacy that will lead to positive prospects in the second half of 2019. In this case, global growth prospects would remain close to the OECD/IMF baselines at around 3.5%-3.9% – possibly even higher.

In the ‘America First’ Scenario, neither truce nor diplomacy would prevail. After spring 2019, continued friction would result in progressive escalation and spillovers in global economy. As a result, global prospects would dampen as world GDP growth in 2019 would sink to 3% or worse.

In the Global Trade War Scenario, diplomacy would fail, while ‘America First’ escalation would spread across the world economy. Risks to global outlook would overshadow world GDP growth, which would plunge to 2%-2.5% for several years to come – which would translate to plunging world trade and investment, and new geopolitical conflicts.

High stakes

After Buenos Aires, the Global Trade War scenario has been temporarily suspended. Yet, the ‘America First’ scenario has not been fully reversed.

We’ve been there before. After the Trump-Xi Florida summit in April 2017, U.S. and China announced a 100-day action plan to improve strained trade ties. Yet, only two weeks later, Trump issued a memorandum, which directed Commerce Secretary Wilbur Ross to investigate the effects of steel imports on national security – and that became the first shot in the bilateral trade war last spring.

With the truce, the Muddling Through scenario prevails momentarily but it can easily reverse back toward escalation, even global trade war.

If the White House and the Congress fail to achieve a decent compromise in the Trump trade wars, the complications would degrade global economic outlook for years to come.

The stakes are historical. Failure should not be an option.

Based on Dr. Steinbock’s briefing on the Trump-Xi meeting and its impact on global growth prospects on December 2, 2018.

About the Author

Dan Steinbock is the founder of Difference Group and has served as research director of international business at the India, China and America Institute (US) and a visiting fellow at the Shanghai Institute for International Studies (China) and the EU Center (Singapore). For more, see http://www.differencegroup.net/