Introduction

Investment planning is crucial to ensure a solid financial future. The decisions you make today can significantly impact your financial well-being in the future. Investing wisely and planning for the long term, such as with Chocolate Finance, is essential to achieve financial security.

Investment planning can initially seem overwhelming, but with the right approach and guidance, anyone can achieve their financial goals. This article will outline three key steps to sound investment planning, providing the necessary tools to make informed decisions about your financial future.

Step 1: Assess Your Financial Goals and Risk Tolerance

Before investing your hard-earned money, assessing your financial goals and risk tolerance is vital. This means understanding what you want to achieve with your investments and how much risk you will take to achieve those goals.

Start by defining your financial goals. Do you want to save for retirement, pay for your children’s education, or buy a house? Whatever your goals are, they will determine how much money you need to save and how long to invest to reach them.

It’s important to be specific about your goals and create a plan to achieve them. This will help you stay focused and motivated as you work towards your financial objectives.

Investing involves risk, and it’s essential to understand your risk tolerance before you start investing. Some investors are comfortable taking on more risk to potentially earn higher returns, while others prefer lower-risk investments offering more stability.

To determine your risk tolerance, consider your investment goals, time horizon, and financial situation. If you have a longer time horizon and are investing for retirement, you may be able to take on more risk. But if you’re saving for a short-term goal, such as buying a house, you may want to focus on lower-risk investments.

Step 2: Diversify Your Portfolio and Avoid Emotional Decisions

Once you clearly understand your financial goals and risk tolerance, the next step is to create a diversified investment portfolio that aligns with those goals and tolerance levels. The diversification approach aims to lessen the risk by investing in a range of different assets, including stocks, bonds, real estate, and commodities. With portfolio diversification, you can avoid putting all your resources into one investment and reduce the impact of any individual investment’s performance on your entire portfolio.

When you diversify your portfolio, it is crucial to evaluate the various asset types you are investing in and their performance under varying economic circumstances. For instance, stocks may perform better during economic growth, while bonds may excel during economic uncertainty. Conversely, real estate could be an attractive long-term investment but may necessitate a substantial upfront investment.

In addition to portfolio diversification, avoiding making emotional investment decisions is essential. Emotional decisions may lead to buying high and selling low, which can be detrimental to your portfolio’s performance. Instead, focus on your long-term investment strategy and avoid reacting to short-term market fluctuations.

One way to avoid emotional investment decisions is to set up automatic contributions to your investment accounts. By automating your contributions, you can avoid the temptation to time the market and instead focus on your long-term investment strategy.

Regularly checking and adjusting your portfolio’s balance is crucial to maintain diversification and alignment with your financial goals. Since various investments perform differently, your portfolio might become imbalanced over time, resulting in more risk than anticipated. By consistently reviewing and rebalancing your portfolio, you can minimize this risk and guarantee that your investments remain in line with your goals and risk tolerance.

Step 3: Monitor Your Investments and Maintain Liquidity

After assessing your financial goals, risk tolerance, and portfolio diversification, the next step is to monitor your investments and maintain liquidity. It is crucial to take these steps to maintain the coherence of your investments with your objectives, and prevent any damages that may jeopardize your financial plan in the long run.

Regularly Monitor Your Investments

One way to keep track of your investments is to review your portfolio at least once a year or when there are significant changes in the market. During these reviews, assess the performance of your investments and compare them to your goals. You can use online tools or work with a financial advisor to track your investments.

Another essential step is to stay informed about economic and market developments that could impact your investments. Keep an eye on news and trends that affect the sectors in which you have invested. By staying informed, you’ll be better equipped to make informed decisions when the time comes.

Maintain Liquidity

Maintaining liquidity means having enough cash on hand to meet your short-term financial obligations, including unexpected expenses or emergencies. Without adequate liquidity, you may be forced to sell your investments at a loss to access cash quickly, which can hurt your long-term financial plan.

To maintain liquidity, consider keeping a portion of your investments in cash or cash equivalents, such as savings accounts, money market funds, or short-term certificates of deposit (CDs). Keeping enough cash to cover three to six months of living expenses is generally recommended.

Rebalance Your Portfolio

Over time, market fluctuations and changes in your financial situation may cause your investments to become unbalanced. For example, if one of your holdings has performed exceptionally well, it may now represent a larger proportion of your portfolio than you intended.

To address this issue, it’s essential to rebalance your portfolio periodically. Rebalancing involves selling investments that have become overrepresented in your portfolio and buying more of those that have become underrepresented. This helps you maintain your desired asset allocation and manage risk exposure.

Rebalancing can be done annually, semi-annually, or when there are significant changes in the market or your financial situation. Consider working with a financial advisor to determine the appropriate frequency and strategy for rebalancing your portfolio.

Conclusion

Building a solid financial future through sound investment planning requires time, effort, and discipline. It’s not a one-time task, but a continuous process that needs to be monitored and adjusted regularly to ensure your investments align with your financial goals and risk tolerance.

Remember to be patient, disciplined, and focused on your objectives, and always seek the advice of a financial professional when making investment decisions. Proper planning and approach can create a stable and prosperous financial future for yourself and your loved ones. So start today and take control of your financial future!

U.S. Banking Crisis in a New Stage of Contagion

By Dr. Dan Steinbock

In view of the Fed, American banking crisis is over. Yet, US and European banks face the most acute stress since 2008 and 2011, respectively. Global economy is exposed to new headwinds.

Last week, as the Federal Reserve pushed ahead with its 10th rate hike since last March, its chairman Jerome Powell declared that the period of U.S. bank failures had come to an end. That’s why Powell assured Americans, “There were three large banks, really from the very beginning, that were at the heart of the stress that we saw in early March — the severe period of stress. Those have now all been resolved, and all the depositors have been protected.”

In other words, the failures of Silicon Valley Bank, Signature Bank and First Republic Bank mark the end, not the spread of the banking crisis. As Powell added, the most recent failure of First Republic, and its subsequent sale to JPMorgan Chase, “kind of draws a line under that period.”

Obviously, such ideas are plain silly. U.S. banking crisis is not over; it has entered a new stage. And it continues to spread.

As dominoes fall

Nearly half (48%) of Americans are concerned about the safety of their bank deposits, according to a Gallup poll last week. Distressingly, the survey results resemble the aftermath of the Lehman Brothers’ collapse.

Recently, Lawrence McDonald, former vice-president at Lehman Brothers, projected that the banking crisis could derail another 50 regional lenders in America if the US fiscal and monetary authorities fail to take steps to resolve structural challenges.

In the U.S. and European banking sector, the rollercoaster ride began in early March, with three weeks of substantial volatility. First, two major US regional banks (Silicon Valley Bank [SVB] and Signature Bank) failed. Then, one of the 30 global systemically important banks, the Switzerland-based Credit Suisse, lost its autonomy after a government-facilitated takeover by UBS.

In the process, market and depositor confidence dissipated in key parts of the sector, with adverse repercussions in investor and consumer confidence.

To prevent the situation from affecting more banks, global industry regulators – including the Federal Reserve, the Bank of Canada, Bank of England, Bank of Japan, European Central Bank, and Swiss National Bank – were compelled to intervene and provide extraordinary liquidity.

How could it all happen – again?

Bank analysts would say that the lead-up period saw many banks invest their reserves in US Treasury securities. So, when the Fed sharply tightened financial conditions last year to rein in surging inflation, companies found it challenging to raise cash, which triggered deposit outflows.

To meet those outflows, SVB sold its long-term Treasuries at great loss. As a capital raise to cover the losses fell apart, a huge run on deposits ensued leading to the largest bank failure since the 2008 financial crisis. What compounded challenges was several banks’ exposure to the bursting cryptocurrency bubble. These events sparked a broad migration of deposits from the banking sector to money market funds while migrating to global systemically important banks, thus forcing some banks to source liquidity from the Fed – the mistakes of which had compounded the challenges in the first place.

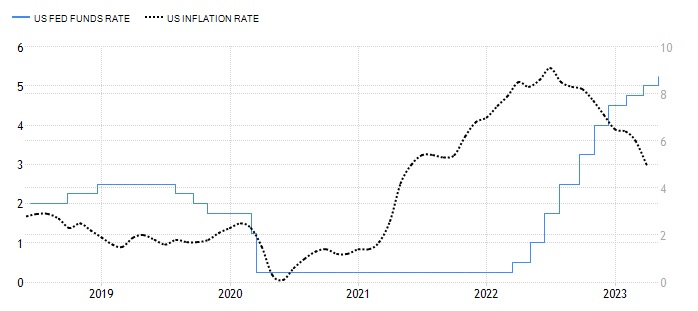

After mid-year 2021, when inflation started to climb rapidly, the Fed shunned a timely response. Instead, its chairman downplayed the threat of soaring prices calling them “transitionary.” The stunning complacency proved costly. By mid-2022, US inflation peaked at 9.1%; a four-decade high. And it remains around 5%, more than twice the 2% target. That’s too why the Fed raised the fed funds rate by 25bps to a range of 5%-5.25% in its May meeting.

If the Fed’s monetary pain wasn’t enough, the White House’s foreign policy has contributed to runaway inflation and elevated uncertainty. After years of trade protectionism, the global pandemic and depression, the net effect of the high-cost US/NATO-led proxy war against Russia in Ukraine has been a lethal mix of a global energy crisis and the meltdown of the global food system.

The spread effects

The elusive calm until the demise of First Republic Bank did not reflect the end of the crisis, but its steady progress. As Mohamed El-Erian, chief economic advisor at Allianz, put it last week. “Now we have stage two, where banks that are not particularly badly managed they have issues but they’re not particularly badly managed – are suddenly vulnerable.” In other words, “the cancer within [these banks] is starting to spread.”

As credit conditions are tightening, the risks of further contraction rise with banking contagion. Structural vulnerabilities remain huge. In parallel with the demise of SVB in March, one consequential study indicated that almost 200 more banks may be vulnerable to the type of risk that caused the collapse of SVB. These banks across the US could fail if half of their depositors quickly withdraw their funds. Even insured depositors — those with $250,000 or less in the bank — could have problems getting their cash if these institutions face the kind of run that SVB experienced.

According to the co-author of the study, a banking expert at Stanford University, half of US lenders are underwater: “Let’s not pretend that this is just about Silicon Valley Bank and First Republic,” he said recently. “A lot of the US banking system is potentially insolvent.” Presumably, some 2,315 banks across the US are currently sitting on assets worth less than their liabilities.

Still worse, the lingering banking crisis occurs at a time, when the White House is engaged in the largest war funding in decades and the Congress has wasted half a year failing to agree on a debt limit.

U.S. default risk as an “economic and financial catastrophe”

A week ago, US Treasury Secretary Janet Yellen warned that the US will run out of cash by June 1 if Congress fails to raise or suspend the debt ceiling. She urged Congress to act “as soon as possible” to address the $31.4 trillion limit. President Biden has called a meeting of congressional leaders on the matter on May 9.

The US hit the statutory limit already last December. Since then, Yellen has repeatedly warned that “failure to raise U.S. debt ceiling would lead to “economic and financial catastrophe.” Unsurprisingly, the Biden administration is under mounting pressure to reconcile the conflicting demands.

Historically, the debt ceiling has been raised, extended or revised 78 times since 1960. If this time is different, it will have significant and adverse global repercussions. If, however, a new debt limit arrangement will be achieved, it can only happen by taking more debt. In this case, Washington will delay its default by buying time, which will make the eventual US debt crisis worse.

The economic fundamentals and safety nets that prevailed in 2008 have been largely exhausted. The West is navigating in perilous waters with leaking lifeboats.

About the Author