The US–Iran war reshaped the Middle East, exposing US dysfunction and highlighting regional security vulnerabilities. Dr Kalim Siddiqui argues that economic fallout and rising global living costs have intensified criticism of Israeli policies, while many regional states seek greater economic engagement with Iran. The conflict also created opportunities for China to expand Belt and Road partnerships and strengthen regional ties through economic and trade cooperation.

I. Introduction

The Trump administration’s approach to Iran was characterised by a combination of maximalist rhetoric and a preference for rapid, decisive military action. President Trump reportedly sought a swift regime-change operation, anticipating that the Iranian government would collapse under sustained pressure. According to various sources, Israeli officials assured him that the campaign could be concluded within days—a surgical strike that would decapitate Iran’s leadership and trigger a domestic uprising (The Guardian, 2026).

This assessment proved profoundly mistaken. Four months after the outbreak of major hostilities between US, Israel and Iran, the anticipated quick victory has failed to materialise. Instead, the conflict has deepened and expanded, drawing much of the region into a broader war. The closure of the Strait of Hormuz—through which roughly one-fifth of global oil supplies and substantial volumes of liquefied natural gas had passed before the crisis—has severely disrupted global energy markets. Ships traffic through the strait has fluctuated between just two and sixteen ships per day, a dramatic decline from the more than one hundred ships that typically transited daily before the conflict. The resulting disruption has driven up oil and gas prices, fuelled global inflation, and imposed significant economic costs on billions of consumers worldwide.

Rather than securing a rapid victory, the United States (US) has become entangled in a prolonged and costly conflict. The enhanced influence of the Islamic Revolutionary Guard Corps (IRGC) in Iran’s post-war political order has heightened anxieties among Gulf states. With many of the IRGC’s more pragmatic leaders killed during the war, the likelihood of more radical and confrontational factions gaining influence has increased. Far from collapsing, the Iranian regime has consolidated its position by mobilizing anti-imperialist and nationalist sentiment, adopting an even more defiant and militarised posture (Siddiqui, 2026a).

Contrary to the aggressive expansionism that many critics argue has characterised Israeli policy for decades, Iran has not sought regional hegemony through conventional military conquest. Instead, Iran’s strategy of cultivating and supporting regional resistance networks has largely functioned as a form of forward defence—a deterrent posture designed to safeguard its borders and strategic interests rather than a project of territorial expansion. Assertions that Iran’s regional activities constitute a covert campaign of imperial domination are often analytically problematic and insufficiently supported by the available evidence (Siddiqui, 2026a).

Among the Gulf Cooperation Council (GCC) states, a more pragmatic approach is emerging. Although these governments remain reluctant to accept overt Iranian political predominance, they have shown an increasing willingness to accommodate and engage with Iran’s growing economic influence. This gradual rapprochement reflects a strategic calculation that economic interdependence offers a more sustainable foundation for regional stability than perpetual zero-sum competition. Scholarly studies suggest that economic integration, institutional cooperation, and pragmatic mediation—particularly by states such as Qatar and Oman—provide viable mechanisms for reducing tensions and preserving economic stability in a region increasingly shaped by sanctions, energy market volatility, and asymmetric warfare.

This regional transformation is further complicated by the evolving nature of the US’ commitment to the Middle East. US foreign policy in the region remains highly susceptible to pressure from organized interest groups, with lobbying networks serving as important channels of influence. If US’s primary objective is to attract investment and promote economic growth, the Gulf monarchies already make a substantial positive contribution to US power (Siddiqui, 2025a). They are significant investors in emerging US high tech and represent lucrative markets for the US corporations. Moreover, the operating costs of US military installations in the Gulf are largely borne by host governments, effectively subsidizing US force projection across the region (The Economist, 2022).

By contrast, the economic rationale underpinning the US–Israeli alliance remains more contested. Supporters argue that US assistance to Israel should be viewed as a strategic investment rather than conventional foreign aid. The annual $3.3 billion in military assistance is often described as modest relative to overall US defence spending, with most of the funds returning to the US through purchases of US military equipment, thereby supporting domestic defence industries and employment. Israel is also credited with contributing significant innovations in areas such as avionics, cybersecurity, and missile defence, leading proponents to characterize the relationship as mutually beneficial rather than one-sided.

From a political economy perspective, however, the net benefits of this asymmetrical partnership remain subject to debate. Critics argue that the strategic and diplomatic costs associated with unconditional support for Israel—including recurrent demands for diplomatic backing and the geopolitical tensions generated by regional conflicts—may outweigh the economic and technological gains. These costs become particularly salient when such tensions contribute to instability in global energy markets and impose broader economic burdens on the international system.

II. The Global Economic Fallout

Beyond these geopolitical realignments among states, the human and economic toll of this conflict has been devastatingly universal. Over the past three months, the war has inflicted severe economic pain across the globe, with the cost of living surging precipitously in virtually every nation. Consumers worldwide have borne the brunt of this shock, as sharp spikes in oil and gas prices have cascaded through supply chains, driving up the prices of food, transport, and essential goods (The Guardian, 2026).

The crisis surrounding the Strait of Hormuz has been particularly consequential. Prior to the latest escalation, the strait carried approximately one-fifth of global oil supplies—around 20 million barrels per day—as well as substantial volumes of liquefied natural gas. During the conflict, maritime traffic fluctuated between just two and sixteen vessels per day, a dramatic decline from the more than one hundred ships that typically transited the waterway each day before the crisis. This disruption drove up oil and gas prices, strained global supply chains, and significantly increased transportation and insurance costs worldwide.

The broader economic repercussions have been severe. Global growth projections have been revised downward, with the United Nations Conference on Trade and Development (UNCTAD) forecasting growth of just 2.5 per cent in 2026, well below pre-pandemic trends. Across Asia, the economic outlook has deteriorated rapidly as inflationary pressures have intensified. In Pakistan, inflation rose from 7.3 per cent in March to more than 12.6 per cent in May. At the same time, several Asian currencies weakened against the US dollar, while borrowing costs increased as investors reassessed geopolitical and economic risks.

The International Labour Organization (ILO) has warned that the crisis represents “a slow-moving and potentially long-lasting shock that will gradually reshape labour markets.” Under one scenario modelled by the organization—in which oil prices remain approximately 50 per cent above their early-2026 average—global working hours could decline by 0.5 per cent this year and by 1.1 per cent in 2027, equivalent to the loss of roughly 14 million and 38 million full-time jobs, respectively. Real wages could also fall by as much as US$3 trillion globally by 2027.

The implications for food security are equally alarming. According to the World Food Programme, if oil prices remain near US$100 per barrel through mid-2026, an additional 45 million people worldwide could fall into acute food insecurity, adding to the nearly 320 million people already experiencing hunger since the beginning of the year. In Somalia alone, approximately 6 million people are currently facing severe food shortages, with children under the age of five among the most vulnerable. By the end of 2026, a further 2.5 million people are expected to be unable to afford basic food necessities.

Trump political appeal is closely tied to economic performance and economic nationalism; such developments represent a serious political challenge. Rising energy prices and the resulting cost-of-living pressures are eroding household purchasing power and fuelling public dissatisfaction. Viewed in this context, the administration’s apparent recalibration of its Middle East policy may be understood less as an ideological shift than as a pragmatic response to mounting economic costs and strategic constraints.

III. The Strategic Logic of Israeli Objectives

An important but frequently overlooked dimension of the relationship is the asymmetry of power between the US and Israel. Israel remains heavily dependent on US military assistance, economic support, intelligence cooperation, and diplomatic backing. Its military advantages are reinforced by a continuous flow of US weapons systems, technological assistance, and logistical support.

The US, by contrast, possesses substantially greater economic, military, and diplomatic resources. Its economy is many times larger than Israel’s, its military capabilities are global in scope, and its diplomatic reach remains unmatched. This disparity suggests that US possesses significant leverage should it choose to employ it. The central question is therefore not whether the US has the capacity to influence Israeli behaviour, but whether domestic political considerations permit the full exercise of that influence.

Potential instruments of leverage include conditioning military assistance, reducing diplomatic protection in international forums, limiting intelligence cooperation, or signalling that political support is not unconditional. The relative absence of such measures reflects political calculations and institutional constraints rather than a lack of material capability.

For decades, Iran has been viewed by analysts as the sole regional actor capable of imposing meaningful constraints on Israeli military superiority and limiting its strategic flexibility. By leveraging a constellation of resistance forces—including Hezbollah, Hamas, and the Houthis—Iran has built a layered network of influence that grants it strategic depth and repeatedly complicates Israeli regional calculations (Siddiqui, 2026a).

From this vantage point, neutralizing Iran’s deterrent capabilities has become a central pillar of Israeli regional strategy. Critics contend, however, that this push is driven less by immediate security concerns than by a broader ambition for uncontested regional supremacy—an aspiration some associate with expansionist visions linked to the concept of a “Greater Israel.”

For these critics, Israel’s objective extends far beyond degrading Iran’s military infrastructure or halting its nuclear progress. The ultimate aim, they argue, is to fracture Iran as a coherent state—reducing it to a condition reminiscent of post-invasion Iraq, post-Gaddafi Libya, or war-torn Sudan: riven by ethnic and sectarian divisions, paralyzed by internal strife, and incapable of projecting power beyond its borders. Such a weakened Iran would pose no threat to Israeli dominance and would serve as a stark warning to any regional actor considering resistance to the US-led order

This vision has been articulated with increasing clarity by Israeli officials. Defence Minister Israel Katz, for instance, stated in February 2026 that Israel was “determined” to ensure Iran never recovers, advocating for a “Libya model” in which Iran would be “completely destroyed, without a central government, weakened, disintegrated, with no capability to threaten the region or the world”.

Crucially, Israel has consistently sought to position the US as the executor of this project. Rather than bearing the full cost of a direct confrontation, Israeli strategy has been to leverage The US military and financial power to achieve its objectives. The logic is straightforward: the US possesses the military capacity to effect regime change and the economic heft to sustain a prolonged campaign, while Israel, constrained by its smaller population and geographic vulnerability, cannot absorb the same level of casualties or international opprobrium.

IV. The Divergence of US and Israeli Interests

For Trump, the political calculus has shifted. A prolonged war with mounting casualties and economic costs does not serve his domestic agenda. The promised quick victory has not materialized, and the electoral implications of a quagmire are becoming impossible to ignore.

Israel, however, views the situation through an entirely different lens. For Israeli decision-makers, the current window of opportunity—in which the US is militarily engaged and Iran is under maximum pressure—represents a historic chance to achieve the long-sought objective of permanently neutralizing the Iranian threat. Israel therefore seeks to prolong the conflict, to deepen the destruction, and to ensure that Iran emerges not merely defeated but destroyed as a functional state. As Defence Minister Katz has made clear, the Israeli goal is not a negotiated settlement but the complete disintegration of Iranian statehood (The Guardian, 2026).

This divergence creates a dangerous dynamic. The US, seeking an exit, finds itself constrained by its alliance commitments and the inertia of military engagement. Israel, seeking escalation, continues to press for more aggressive action, knowing that it lacks the capacity to achieve its objectives without The US support. The result is a protracted conflict that serves Israeli strategic interests while imposing mounting costs on the US and the global economy—a classic case of a smaller ally exploiting a larger patron’s commitments to pursue its own maximalist agenda.

Perhaps the most notable recent development has been the administration’s changing rhetoric toward Israel. President Trump has moved from near-unconditional support toward a more openly critical posture, while Vice President JD Vance has emerged as one of the administration’s most prominent voices advocating a reassessment of the relationship. Vance has questioned aspects of Israeli regional policy, criticised the continuation of certain military deployments, and argued for a more balanced approach to regional diplomacy.

This position carries considerable political risks. For decades, strong support for Israel has been a defining feature of mainstream Republican foreign policy. Any departure from that consensus is likely to encounter resistance from influential political constituencies and lobbying organizations. Vance’s willingness to embrace such a position therefore suggests that elements within the administration view the broader economic and strategic consequences of regional instability as increasingly serious.

The speed of this rhetorical shift has been striking. Positions that would have been politically difficult to imagine within a Republican administration only months earlier are now being voiced publicly by senior officials. Expressions of frustration with Israeli policy and suggestions that US support may not be limitless indicate a growing reassessment of long-standing assumptions. Moreover, economic pressures and strategic considerations are playing an increasingly important role in shaping the administration’s approach to the region.

There is a growing and palpable conviction among populations worldwide that Israeli policy is fundamentally misaligned with the broader interests of ordinary people. The widespread, graphic documentation of civilian casualties—particularly the killings of children and non-combatants—has catalysed a moral reckoning. These images, disseminated instantly across digital platforms, have pierced traditional media filters and galvanised public opinion across diverse cultural and political contexts.

Critically, this popular discontent is increasingly reflected within elite intellectual and strategic circles. A significant and growing cohort of academics—including Jeffrey Sachs, John Mearsheimer, Trita Parsi, Ilan Pappé, and others—as well as foreign policy analysts and prominent media figures such as Tucker Carlson and Ana Kasparian, have begun openly challenging prevailing Zionist narratives.

Scholarly analyses increasingly frame the recent Israel–Iran war not as an isolated event, but as “a sharp symptom of long-standing global contradictions” rooted in imperialism, colonialism, and competition within global capitalism (Siddiqui, 2025b). From this perspective, Israel is viewed as “a vehicle of primitive accumulation in Middle East,” advancing the imperatives of global capitalism through settler-colonial expansion and dispossession while simultaneously intensifying the enduring contradictions of imperialist rivalry (Siddiqui, 2018).

V. Implications for Regional Order

The long-term implications of this dynamic are chaos and instability in the region. If Israel succeeds in its objective of reducing Iran to a failed state, the regional balance of power would be fundamentally transformed. The elimination of Iran as a countervailing force would leave Israel as the unchallenged military hegemon in the Middle East, with no regional power capable of constraining its actions. This would likely embolden further Israeli expansionism, whether through settlement construction in the West Bank, annexation of territory, or military action against other perceived threats.

However, the costs of such an outcome would be immense. The disintegration of Iran—a country of over 95 million people with a rich historical heritage and significant economic potential—would create a humanitarian catastrophe on a scale not seen since the wars in Syria and Yemen. It would also generate a power vacuum that extremist groups, regional militias, and external powers would rush to fill, perpetuating instability for decades to come. The refugee flows, the collapse of regional trade, and the continued disruption of energy supplies would impose costs not only on the Middle East but on the entire global economy (The Guardian, 2026).

Moreover, the destruction of Iran would not eliminate resistance to Israeli hegemony. History suggests that the elimination of one adversary merely creates space for others to emerge. The underlying grievances that animate opposition to Israeli policy—the displacement of Palestinians, the occupation of Arab lands (Siddiqui, 2024a), the perceived injustice of the regional order—would persist, finding new expression in different forms. The cycle of violence would continue, albeit in new configurations (Siddiqui, 2024a).

Talks between Iran and the US in Switzerland have stalled. Iran has reaffirmed the closure of the Strait of Hormuz, citing continued Israeli strikes in southern Lebanon as the immediate trigger. The closure—already responsible for disrupted energy markets and global inflationary pressures—is presented by Iran as a direct response to Israeli military actions rather than as unilateral escalation (The Financial Times, 2026).

At the heart of the diplomatic deadlock lies a single, non-negotiable issue for Iran: the withdrawal of Israeli forces from southern Lebanon. This condition is explicitly laid out in the memorandum of understanding underpinning the negotiations. From Iran’s perspective, no meaningful progress—whether on reopening the Strait, reviving the JCPOA, or reconstructing Iran—is possible without a binding commitment to Israeli withdrawal.

The post-war reconstruction of Iran presents a particularly revealing lens through which to examine the political economy of the region. The Memorandum of Understanding (MOU) demands of over $300 billion for reconstruction and economic development of Iran, to be undertaken with regional partners.

The US shares this objective in principle. US would like to see Israeli forces depart southern Lebanon, recognizing that their continued presence obstructs regional stability and complicates US-Iranian relations. However, the gap between US preference and Israeli action has widened. If Israel resists—as its recent rhetoric and military posture suggest—President Trump faces a stark choice: compel Israeli compliance or accept the collapse of negotiations and the perpetuation of a conflict inflicting mounting costs on the global economy.

There is no viable alternative. Maintaining the status quo—Israeli forces entrenched in southern Lebanon, the Strait closed, and Iran under maximum pressure—would be a strategic and economic disaster. The costs are already visible: disrupted energy supplies, soaring inflation, and a global economy teetering on the brink of recession. To allow this to persist is simply not an option.

VI. Trade, Development, and Regional Cooperation

As the US economy grapples with deepening crises—soaring public debt, widening trade and fiscal deficits, rising inequality, and falling profitability (Siddiqui, 2025c) – the US is increasingly ill-positioned to fund developmental projects in the Middle East. The previous US model for the region hinged on exporting arms and luxury goods while strategically maintain conflicts and tensions to drive further weapons sales. This approach has visibly failed (The Economist, 2022).

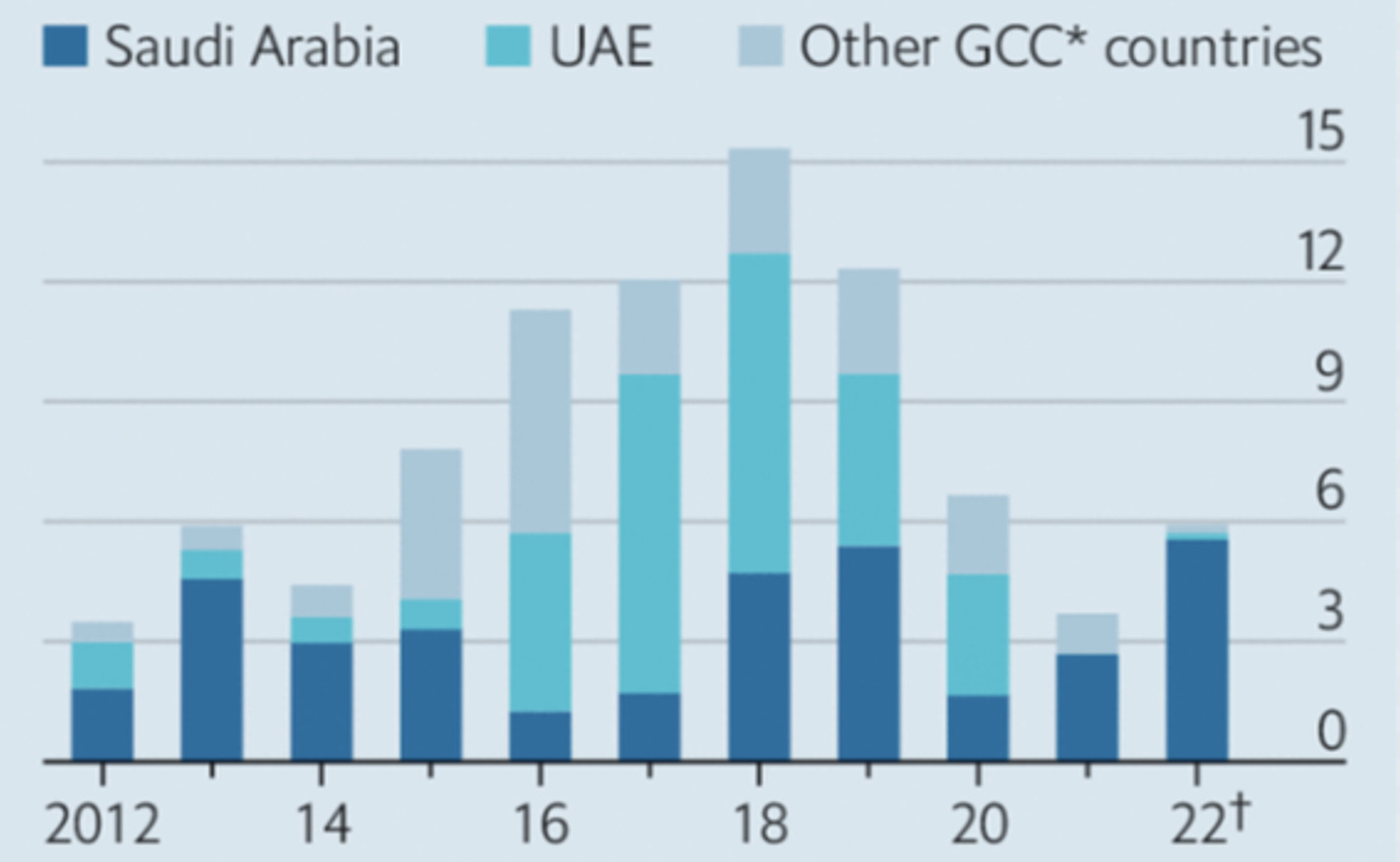

China’s Built and Road Initiative (BRI), by contrast, has grown sharply. Figure 1 tracks the steady rise in Chinese investments and construction projects over the years. Saudi Arabia and the UAE have been key partners throughout, but after 2020, Saudi Arabia clearly emerged as the dominant hub for Chinese companies in the region.

Over a recent 12-month period, Chinese investments and construction contracts in the region totalled $39.4 billion, heavily concentrated in energy and resource-backed infrastructure deals, particularly in Saudi Arabia and the UAE. A central BRI objective is the promotion of regional trade and economic development. Rather than pursuing bilateral arrangements, China deploys the BRI as a hedging instrument, engaging the region collectively. Since 2009, China has surpassed the US as the largest exporter to the Middle East—a telling indicator of its growing economic footprint (Kamel, 2018).

China’s engagement in the Middle East differs from the Western development model that has shaped the region since the 1960s. Rather than emphasizing political influence, China has focused on trade, infrastructure development, and regional economic integration. Through the BRI, China has generated positive economic spillovers for both developing and developed countries without pursuing a strategy of containment. BRI infrastructure and development projects have transformed previously neglected regions by improving connectivity, investment opportunities, and economic capacity (Siddiqui, 2019).

Figure 1: Investment and Construction Projects in the Middle East by China, 2012-2022 (billion $).

The development of energy, trade, investment, and digital infrastructure enables countries to address their economic challenges according to their own priorities. Drawing on more than four decades of economic reform and opening-up, China has developed a distinctive model of political economy that offers valuable lessons for other developing nations. In the Middle East, the BRI has helped unlock economic potential and strengthen local capacities. As demands for new approaches to development intensify, China’s growing role in the region provides an important case for reassessing conventional development paradigms and the geopolitical implications of great-power competition. Xi Jinping’s 2022 visit and the Gulf states’ embrace of the BRI offer particularly useful examples of these evolving dynamics.

The 2008–2009 global financial crisis marked a turning point in China-Gulf relations. As the Financial Times notes, the symbiotic relationship between Gulf oil producers and fast-growing Asian economies—led by China—is increasingly displacing the Western-dominated business landscape of the Middle East.

The Industrial and Commercial Bank of China established its presence in the Dubai International Financial Centre in 2008, followed by the Agricultural Bank of China—China’s second-largest bank—in November 2012. Between 2013 and 2019, Chinese investment in the Middle East reached US$93.3 billion, concentrated in energy (US$52.8 billion), real estate (US$18.4 billion), transport (US$18.6 billion), and utilities (US$5.9 billion).

President Xi Jinping’s visit to Saudi Arabia in 2022 marked a significant milestone in China–Gulf relations. As a result of the visit, 34 agreements covering green energy, information technology, and infrastructure were signed between Chinese and Saudi companies. At the broader China–GCC level, bilateral trade reached US$230 billion, and both sides agreed to pursue a free trade area and establish a joint investment council to deepen economic cooperation. Key outcomes of the inaugural China–GCC Summit included support for the Global Development Initiative, the Global Security Initiative, and the 2023–2027 Action Plan for Strategic Dialogue.

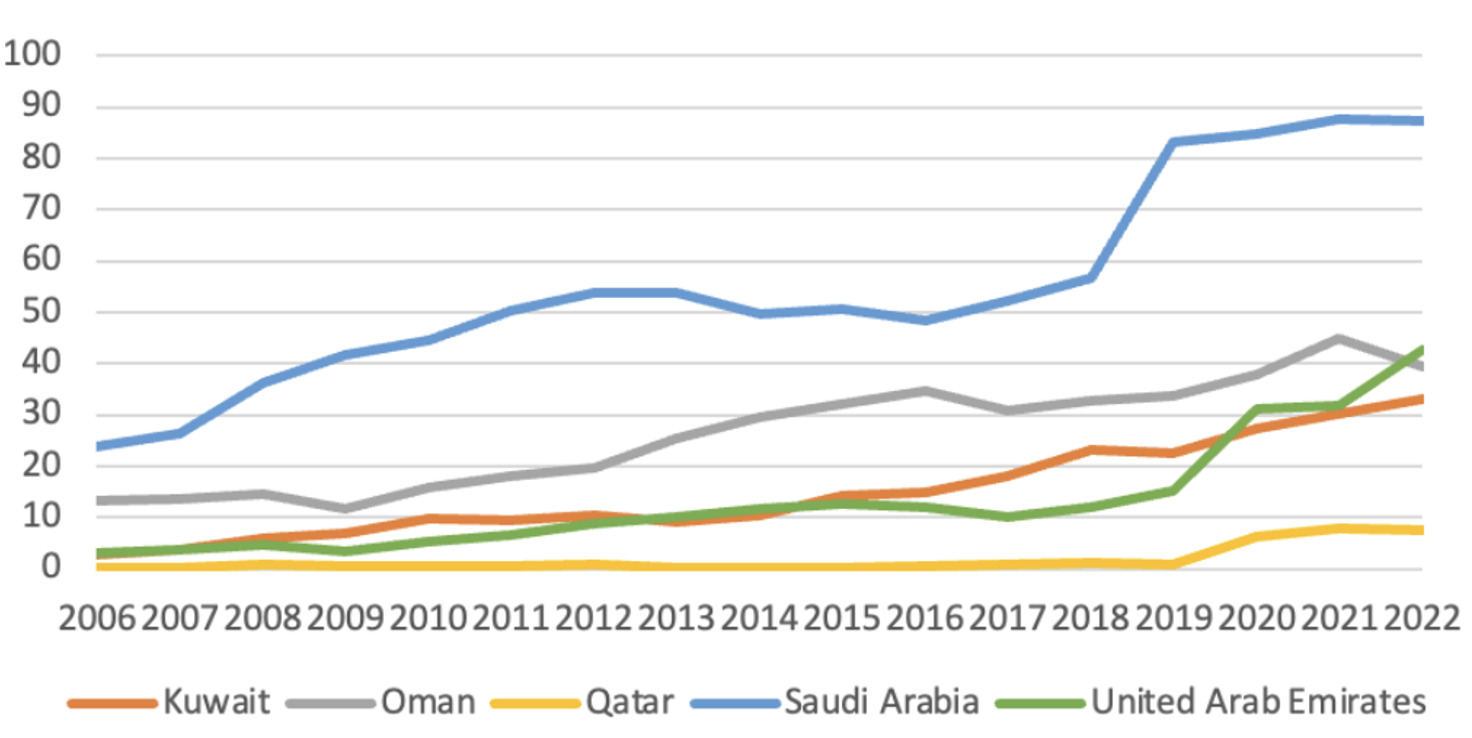

Figure 2 charts the trajectory of crude oil exports from Gulf Cooperation Council countries to China between 2006 and 2022. The trend is unmistakably upward, underscoring the deepening energy relationship. Saudi Arabia, the UAE, and Kuwait emerge as the pivotal suppliers, together dominating China’s Gulf oil imports across the entire decade.

Figure 2: Gulf Countries’ Crude Oil Exports to China, 2006–2022 (Million Tons).

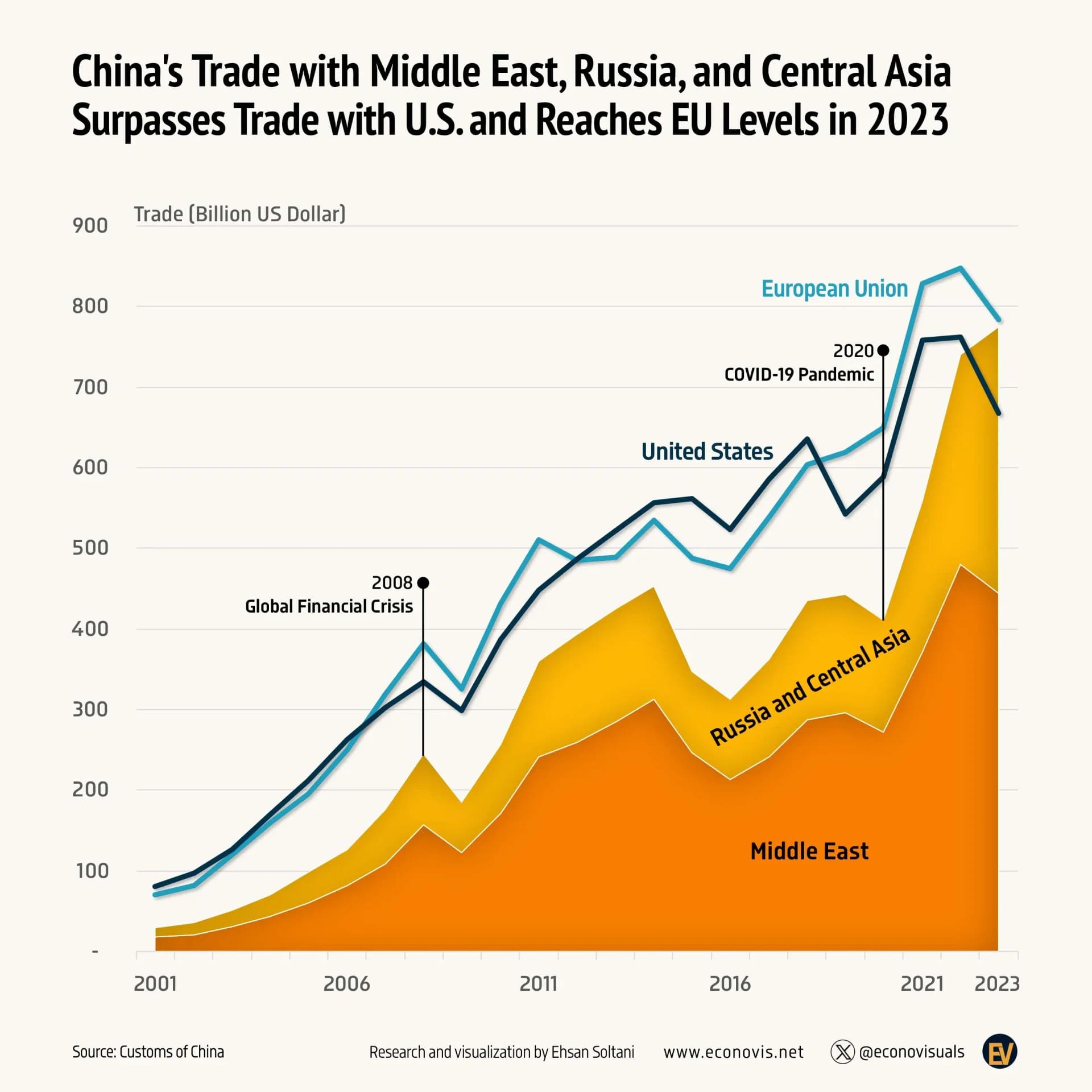

Figure 3: China’s Trade with the Middle East, Russia and Central Asia, US and EU, 2001-2023 (billion$).

China’s trade with the Middle East, Russia, and Central Asia expanded rapidly, reaching approximately US$774 billion in 2024. As Figure 3 illustrates, China’s trade with the Middle East has surged since 2001—from near-negligible levels to surpassing both the US and EU by 2023—making the region a vital trading partner. This growth reflects deepening ties driven by strategic initiatives, complementary economic interests, and shifting geopolitics.

China has overtaken the US as the Middle East’s largest trading partner. While bilateral trade between China and the region has grown steadily—bolstered by the Belt and Road Initiative and rising energy demand—US trade has remained stagnant at roughly half that volume. The Gulf relationship is particularly significant: by 2025, China-GCC trade had reached approximately US$300 billion, with China as the Gulf’s top crude oil buyer and a growing source of investment as Gulf states diversify beyond hydrocarbons (The Economist, 2022; Siddiqui, 2019).

Recent US-Iran tensions have delivered a major shock to the Gulf, challenging two pillars of regional stability. The first is the Gulf’s economic model—built on stability, favourable tax regimes, flexible regulations, and a dynamic business environment. The second is the traditional oil-for-security arrangement, underpinned by the US military presence. Missile and drone attacks during the conflict exposed vulnerabilities in this security architecture, prompting Gulf states to reassess the reliability of the US as their principal security guarantor.

China economic footprint in the Gulf countries has expanded substantially through trade, investment, and infrastructure development, creating a level of engagement that is difficult for regional governments to ignore. Following President Xi Jinping’s visit to Riyadh and the China–GCC Summit, relations evolved into a broader strategic partnership. Although Chinese investments initially focused on energy and port infrastructure, the changing geopolitical environment is encouraging both sides to pursue deeper economic integration across a wider range of sectors (The Economist, 2022).

The future of China–Gulf economic relations is likely to centre on three key areas where Chinese technological capabilities complement Gulf capital and development ambitions. The first is green energy. China dominates global solar manufacturing, accounts for the majority of electric vehicle production, and has rapidly expanded exports of renewable energy technologies. For Gulf states pursuing economic diversification and energy transition strategies, partnerships with Chinese firms such as BYD, Geely, and Changan offer access to advanced technologies for modernising power grids and transportation systems (Siddiqui, 2024b).

China’s approach in the Middle East emphasises stability, development, and economic cooperation. Its role in facilitating the 2023 restoration of diplomatic relations between Iran and Saudi Arabia demonstrated its growing diplomatic influence and preference for dialogue-based conflict management. Alongside its 25-year cooperation agreement with Iran, China has expanded economic partnerships with Saudi Arabia, the United Arab Emirates, Qatar, Kuwait, Oman, and Bahrain, particularly in energy, telecommunications, infrastructure, and technology. Chinese companies have also played a prominent role in major development projects in Egypt. Through the BRI, China has strengthened economic ties across the region while supporting national development and reform agendas (Cheung, 2023).

The Gulf states’ Western political-economic model rested on an oil-for-security bargain with the US: security guarantees and military protection in exchange for oil exports, Western arms purchases, luxury goods, and substantial investments in Western financial markets and real estate.

This arrangement is now under mounting pressure. Geopolitical shifts and regional conflicts have eroded trust in external security commitments (Siddiqui, 2025d), driving Gulf states to broaden their strategic and economic partnerships. The recent US-Iran war has been a particular catalyst, prompting a fundamental reassessment of the security architecture.

Concurrently, Gulf governments have recognized that hydrocarbon dependence, arms imports, and overseas asset accumulation cannot sustain long-term prosperity. Industrialization, infrastructure development, and economic diversification have accordingly risen to the top of policy agendas.

Economic vulnerabilities have compounded these pressures. While oil wealth once reduced the imperative for diversification, the post-2014 oil price slump exposed the risks of overreliance on a single commodity. Fiscal strains have since compelled several Gulf states to draw on sovereign wealth funds and fast-track economic reforms.

Saudi Arabia’s Vision 2030 became the clearest expression of this shift. Rather than relying primarily on oil exports and overseas investments, Gulf states increasingly sought to diversify their sources of income through industrialisation, infrastructure development, technology, renewable energy, tourism, and manufacturing. In this context, China emerged as an attractive partner. Through trade, investment, technology transfer, and the Belt and Road Initiative (BRI), China offered a development-oriented model focused on infrastructure, industrial capacity, and long-term economic transformation (Cheung, 2023).

As a result, Gulf states are gradually transitioning from an economic model centred on oil exports and financial investment abroad toward one emphasising domestic development, economic diversification, and strategic cooperation with emerging partners in the East. China’s expanding role in this process reflects broader changes in the regional and global balance of economic power.

A key feature of the BRI is its focus on regional connectivity. Historically, colonial powers concentrated on controlling maritime trade routes while leaving many neighbouring states poorly connected by land-based infrastructure. As a result, economic integration across parts of the Middle East remained limited despite geographical proximity. China’s infrastructure strategy seeks to address these gaps through transport corridors, ports, railways, industrial zones, and digital networks that facilitate trade and regional cooperation.

The emergence of a more multipolar regional order has further strengthened China’s position. Unlike the US, whose regional engagement has often been closely linked to security concerns, China’s interests are primarily economic. China maintains extensive energy, trade, and investment relationships with both Gulf states and Iran and therefore has strong incentives to promote stability rather than regional confrontation. Improved relations between Iran and its Gulf neighbours create favourable conditions for trade, infrastructure development, and cross-border investment, all of which support China’s long-term economic interests (Cheung, 2023).

At the same time, countries such as Iran have shown increasing interest in deeper economic and technological cooperation with China, viewing Chinese expertise in infrastructure, manufacturing, and advanced technologies as valuable for their own development goals. As US influence in the region faces growing challenges, China has gained additional opportunities to expand its economic role. The result is the gradual emergence of a new regional framework in which economic integration, infrastructure connectivity, and development cooperation increasingly complement, and in some areas reshape, the traditional security-centred order that dominated the Middle East for decades.

VII. Historical Foundations of the Chinese Relations with the Middle East

Historically, Arab countries maintained close cultural, technical, and trade links with China, facilitating a rich exchange of goods, ideas, and technologies that benefited both regions. The Tang Dynasty (c. 670–750)—often regarded as China’s golden age—exemplified this interconnectedness. During this period, papermaking reached unprecedented sophistication, while the capital, Chang’an (modern Xi’an), emerged as the world’s largest city, with a population estimated between 800,000 and one million. With China’s total population approaching 50 million, the empire’s economic and demographic strength enabled it to project influence deep into Central Asia and secure key sections of the Silk Road—routes that likewise connected it to the Arab world and beyond.

At the same time, the Umayyad Caliphate (661–750) expanded from the Iberian Peninsula in the west to Transoxiana and the Indus River in the east. Following the Abbasid takeover in 750, the Chinese and Islamic empires met on the frontiers of Central Asia. Traditional accounts of the Battle of Talas (751), fought in present-day Kyrgyzstan, claim that Chinese prisoners—including papermakers—were captured by Muslim forces. However, as Jonathan Bloom notes, this connection may be more legend than established fact (Bloom, 2001).

A more consequential episode in Sino-Islamic relations came during the An Lushan Rebellion (755–763). After rebels seized Chang’an in 756, forcing Emperor Xuanzong to flee, the Tang court reportedly sought assistance from the Abbasid Caliph Abu Ja’far al-Mansur. Muslim sources state that thousands of Arab troops helped the Tang recapture the capital. Some are said to have settled in China, contributing to the origins of the Hui Muslim community. During this period, Muslim merchants continued to travel to China, where Islam was generally tolerated by the Tang authorities (Friedrichs, 2019).

While the Umayyads relied heavily on Egyptian papyrus for administration, paper gradually replaced it under the Abbasids, particularly after Baghdad was founded by al-Mansur in 762. The first major paper mill was established there in 794 during the reign of Harun al-Rashid, followed by others in Basra, Raqqa, and Hama. By the ninth and tenth centuries, Baghdad and Basra had become major centres of book production and trade, with many scholars also working as booksellers, copyists, and translators. (Friedrichs, 2019).

Under Caliph al-Ma’mun (r. 813–833), Baghdad emerged as the leading center of scientific and philosophical inquiry. Through the House of Wisdom, manuscripts from across the known world were collected, translated, studied, copied, and disseminated. This institution preserved and expanded knowledge from Greek, Persian, Indian, and other intellectual traditions.

The spread of paper and the growth of Silk Road networks accelerated an extraordinary era of cultural and scientific exchange. At the House of Wisdom, Muhammad ibn Musa al-Khwarizmi combined Greek mathematics with Indian numerals, laying the foundations of algebra and giving rise to the term “algorithm.” Medical works from Greece and Persia were translated and expanded by scholars such as Ibn Sina (Avicenna), whose Canon of Medicine remained a standard text throughout the Islamic world and medieval Europe for centuries. Advances in cartography likewise integrated Greek, Persian, and Chinese traditions (Friedrichs, 2019).

China’s relations with the Middle East are deeply rooted in history. The ancient Silk Road facilitated extensive trade, cultural exchange, and scientific collaboration between both communities. Many Arab traders settled in China, and a significant number of Chinese converted to Islam, some of whom contributed to Chinese military and administration.

Bloom (2001) provides a comprehensive analysis about introduction of paper and immense impact on Islamic civilization. It traces paper’s journey from its invention in China to its spread through the Islamic lands and eventual transmission to Europe, arguing that paper was a crucial agent for the dissemination of information and transformed medieval life.

The Abbasid world’s largest library was founded in Baghdad in 991 by the Persian minister Sabur ibn Ardashir and contained more than 10,000 volumes. Yet the most celebrated library of the age stood in Córdoba under the Umayyad Caliph al-Hakam II (r. 961–976). According to Bloom, it housed some 400,000 books, with a catalogue filling forty-four volumes. Even if these figures are exaggerated, the collection far exceeded any contemporary library in Christian Europe. Open to Muslim, Jewish, and Christian scholars alike, it became a vibrant center of learning and debate. Similar institutions later emerged in Fatimid Egypt (Bloom, 2001).

This history challenges modern theories of an inevitable “clash of civilizations.” The intellectual exchanges linking China, the Islamic world, and Europe demonstrate that civilizations can coexist, cooperate, and enrich one another. Despite periods of political conflict and instability, medieval Muslim societies generally regarded knowledge as a source of power, progress, and human flourishing—a principle championed by thinkers such as al-Farabi.

The transmission of papermaking from China to the Islamic world, and later to Europe, was one of history’s most transformative developments. As Jonathan Bloom’s Paper Before Print illustrates, paper became the medium through which ideas travelled, knowledge accumulated, and a global renaissance took shape.

At present, scholars attribute China’s popularity in the Middle East to a combination of historical and social factors. The region’s fraught legacy with Western colonialism contrasts sharply with China’s self-presentation as “an all-time friend and development partner.” Simultaneously, China’s remarkable economic trajectory offers “a welcome alternative to the so-called US consensus.” Its non-interventionist stance has been instrumental in making the Belt and Road Initiative broadly acceptable across the Middle East.

VIII. Conclusion

The US–Iran confrontation and Israel’s ongoing war on Gaza—now in its third year—have laid bare Western double standards for the world to see. The devastation in Gaza has severely undermined the perceived legitimacy of the Western-led international order. The contrast is stark: swift, decisive Western action to uphold international law in Ukraine stands in sharp relief against a hesitant, muted response to the humanitarian catastrophe in Gaza. Despite rhetorical condemnations, the West continues to enable Israel’s territorial expansion. Words alone are insufficient; economic and military cooperation with the genocidal Israeli regime must end. Without the credible exercise of leverage, Israel has no reason to alter its course.

The stakes could hardly be higher—not merely prolonged conflict, but a potential global downturn marked by surging energy prices, broken supply chains, and rising food insecurity. For a president focused on economic growth, this calculus is increasingly impossible to ignore.

Durable peace requires accountability under international law, equal rights, and dignity for both Jewish and Palestinian peoples. These are not optional ideals but essential prerequisites for long-term stability. The status quo—entrenching discrimination, denying Palestinian rights, and relying on military force over diplomacy—is unsustainable. A just settlement demands an end to asymmetrical power relations and a commitment to human rights, democracy, and self-determination for all (Siddiqui, 2024a).

Yet the current trajectory is one of deepening entanglement. The US depends on Gulf countries for military and economic partnership; while propping up an Israel whose policies generate recurrent global crises. As Gulf states deepen ties with Iran and international criticism mounts, the US faces a stark choice: continue alienating key partners while absorbing mounting costs, or adopt a balanced approach that respects regional autonomy, reflects shifting realities, and prioritises broader stability. Only the latter offers a sustainable path.

Global economic crisis is already visible—higher energy costs, inflation, and supply-chain strains affecting billions. International bodies warn of a 1973-style cost-of-living crisis, threatening vulnerable economies (Siddiqui, 2026b).

Compounding this, Israel aims to eliminate Iran as a regional counterweight, using US power to do so, while the Trump administration’s hope for rapid regime change in Iran has failed. US and Israeli interests have rarely diverged so sharply: the US seeks an exit; Israel pursues a decisive victory. That dynamic is unsustainable. With rising Chinese economy, and better performance of other emerging economies, the US faces new challenges as in the form of multipolarity.

The US cannot indefinitely bear substantial economic and geopolitical costs for policies that increasingly serve Israel’s agenda. A fundamental reassessment—weighing strategic benefits against mounting liabilities—is overdue. Without it, the cycle of conflict will persist, and the opportunity for a more resilient, equitable regional order in the Middle East will slip away. The choice is clear: continue toward deeper instability, or recalibrate US influence to pursue de-escalation and a more resilient regional order.

About the Author

Dr. Kalim Siddiqui is an economist specializing in International Political Economy, Development Economics, Trade and Economic Policy. Since 1989, he has been teaching economics at various universities in Norway and the UK. Dr. Siddiqui’s research interests encompass a wide range of topics, including political economy, international trade, and economic history, South Asia, and emerging economies. He has presented papers at international conferences across numerous countries, reflecting his global engagement in the field. His scholarly pursuits span six broad domains: Political Economy, Development Economics, Economic History, Economic Policy, Globalization, and International Trade. Dr. Siddiqui has made significant contributions to research in areas such as trade policy, globalization, and political economy. His work has been published in chapters of edited books and articles published in peer-reviewed journals. For inquiries, Dr. Siddiqui can be reached at: [email protected]

Dr. Kalim Siddiqui is an economist specializing in International Political Economy, Development Economics, Trade and Economic Policy. Since 1989, he has been teaching economics at various universities in Norway and the UK. Dr. Siddiqui’s research interests encompass a wide range of topics, including political economy, international trade, and economic history, South Asia, and emerging economies. He has presented papers at international conferences across numerous countries, reflecting his global engagement in the field. His scholarly pursuits span six broad domains: Political Economy, Development Economics, Economic History, Economic Policy, Globalization, and International Trade. Dr. Siddiqui has made significant contributions to research in areas such as trade policy, globalization, and political economy. His work has been published in chapters of edited books and articles published in peer-reviewed journals. For inquiries, Dr. Siddiqui can be reached at: [email protected]

References

- Bloom, J.M. (2001) Paper Before Print: The History and Impact of Paper in the Islamic World, Yale University Press.

- Cheung, G.C.K. (2023) “China’s Belt and Road Initiative: The Economic Footprints in the Middle East vs. Geopolitical Dimensions with the United States” East Asian Policy 15(01): 60-73, April.

- Friedrichs, J. (2019) “Explaining China’s Popularity in the Middle East and Africa” Third World Quarterly, 40 (9).

- Kamel, M.S. (2018) “China’s Belt and Road Initiative: Implications for the Middle East” Cambridge Review of International Affairs, 31(1).

- Siddiqui, K. (2026a) “US-Iran Conflict: Oil Volatility and Global Economic Crisis”, World Financial Review, May.

- Siddiqui, K. (2026b) “The United States, the Petrodollar, and Multipolarity: Strategic Intervention in an Age of Monetary Decline” World Financial Review, January.

- Siddiqui, K. (2025a) “The United States’ Future in an Imperial Mirror: Lessons from Britain, Spain, Abbasids, Rome, and Beyond” World Financial Review, November.

- Siddiqui, K. (2025b) “Decolonisation and Economic Sovereignty: The Bandung Conference and the Making of the Global South” World Financial Review, June.

- Siddiqui, K. (2025c) “The Reasons Behind the Decline of the United States Economy” World Financial Review, May.

- Siddiqui, K. (2025d) “Geopolitics and the Persistence of Global Uneven Development: A Critical Analysis” World Financial Review, July.

- Siddiqui, K. (2024a) “Palestine, Imperialism and the Settler Colonial Project” World Financial Review, February/March.

- Siddiqui, K. (2024b) “China’s Growth Miracle and Development Strategy Since the 1980s” World Financial Review,

- Siddiqui, K. (2019). “One Belt and One Road, China’s Massive Infrastructure Project to Boost Trade and Economy: An Overview” International Critical Thought. 9(2):214-235.

- Siddiqui, K. (2018). “Imperialism and Global Inequality: A Critical Analysis” Journal of Economics and Political Economy, 5(2): 266-291.

- The Economist (2022) “The Gulf Looks to China”, 7 December, London.

- The Financial Times (2026) “US and Iran conduct tense peace talks in Switzerland” 22 June, London.

- The Guardian (2026) “What lessons will Iran’s new leadership draw from the 110-day war?” 20 June, London.

Dr. Dan Steinbock

Dr. Dan Steinbock