Europe has world-renowned gambling meccas such as Monte Carlo, Deauville, and of course, London and Paris. Still, not much is known about Macau, despite it being the largest gambling market globally and the second home to some of the world’s biggest gambling brands, including The Venetian, MGM and Sands.

History of Macau and the development of the gambling industry

Macau is a Chinese Island and ex-Portuguese colony; it’s only 33 sq km and has a population of 682,300. It’s also a gambling heaven for Chinese and International tourists, with millions of players visiting the territory and spending billions yearly. Gambling has existed in Macau since the 16th century, but the current gambling regime has been present since 2001-02.

According to the Centre for Gaming Research, games of chance were first legalised by the colonial government of Macau in 1847. Later in the 1930s, the colonial government awarded the monopoly concession for operating all forms of sanctioned casino games, awarding it to the Hou Heng Company, with games of chance like baccarat making their first debut. In 1962 the government then awarded the monopoly to Sociedade de Turismo e Diversões de Macau (STDM), which would retain control of the market for 40 years until 2001/02, when the term expired.

In 1999, the status of Macau changed, and the territory’s sovereignty was ceded to China. Hence, it became a Special Administrative Region, using the one country, two systems policy, with gambling remaining legal in Macau but not in China. In 2001, the Chinese government broke the casino monopoly, splitting it between SJM (a subsidiary of STEM), Wynn Resorts, and a Galaxy Entertainment and Las Vegas Sands partnership (these were later allowed to divide).

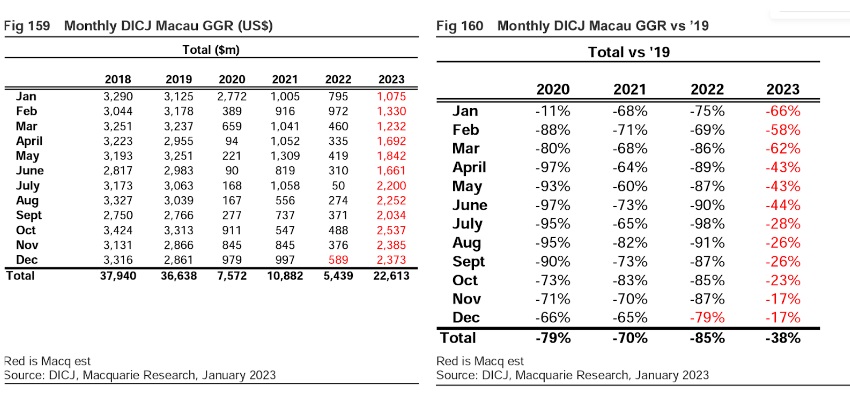

Today, Macau has over 40 casinos regulated and licensed by the Gaming Inspection and Coordination Bureau of Macau. The tax rate for operators is 40%, and regulated gambling accounts for 80% of Macau’s total tax revenue. In terms of revenue, the Macau casino industry was thriving pre-pandemic, far outpacing Las Vegas in revenue and more than earning its title as the “Las Vegas of the East”. In 2019, despite having only one-tenth of the land space of Las Vegas, it generated 5.5 times the USA’s gambling capital pre-pandemic at $36billion vs Vegas’ $6.5billion.

Macau vs Monte Carlo

Rather than comparing Macau to Las Vegas, as is often the case, let’s turn to a more European example – Monte Carlo. Monte Carlo is a world-renowned gambling location; despite being smaller than Macau, with a land size of 0.28 square kilometres, it’s home to four casinos.

Gambling was legalised in 1856 when Monaco’s Prince Charles III granted permission for the city’s most popular casino, Casino De Monte Carlo, to be built, and it opened its doors in 1865. This casino is so iconic it has been the backdrop for 007 movies. Like Macau, Monte Carlo’s casino industry is driven by tourism, and it also draws high rollers, with players opting for Roulette over other games. Although slot games also account for a fair share of the revenue.

Monaco’s Casino Tourism Market is estimated at $4,282m in 2022, with a projected growth rate of 8.5% until 2032. In 2019, 365,000 tourists visited Monaco, compared to Macau’s 39 million, making Macau the larger gambling market both by visitors and spending.

However, unlike Macau, Monte-Carlo’s industry was not affected similarly by COVID restrictions, as local lockdowns and border closures were shorter in duration. Additionally, the ongoing COVID situations in the two countries were vastly different (see the graph below), creating different attitudes and policies regarding sharing public spaces, like casino halls, contributing to differing speeds of industry recovery.

Macau’s gambling industry post-pandemic

Since 2020, the casino industry has suffered dramatically in Macau. China’s zero COVID policy led to three years of continually bottoming-out revenue figures, from which Macau’s casinos are still recovering. Estimated revenue for this year is expected to be down as much as 38% on 2019’s figures, while 2022 was the worst year, with total revenue down 85%.

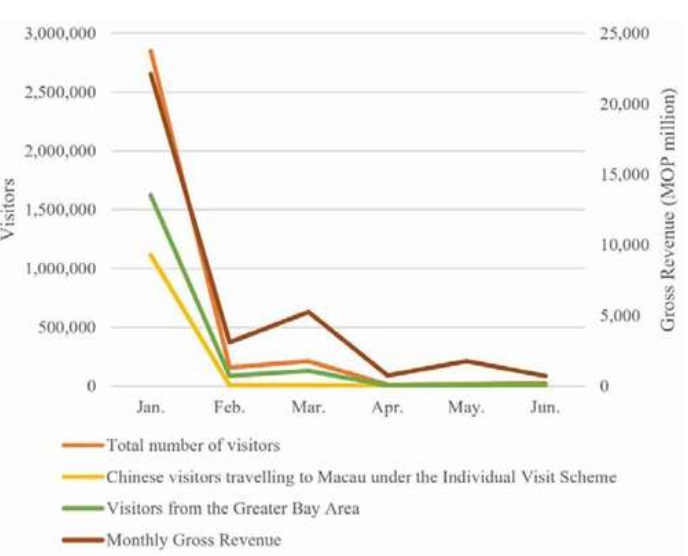

With the Chinese borders closed during pandemic restrictions, visitors to Macau plummeted from 39 million in 2019 to below 6 million for the following three years, with local operators describing it as “an empty shell of what it used to be”.

Since the sudden u-turn on lockdowns and zero COVID policy in relation to nationwide protests from November to December 2022, Macau’s casinos began to benefit from returning customers and increased footfall. Still, at a far slower pace, as the return of consumers brought with it concerns over COVID spreading and the risk of mass infections. Three years of zero COVID policy, internal focus, and critical international media attention have damaged the country’s international reputation affecting the return of international casino tourism.

In other gambling jurisdictions, online gambling participation grew when COVID restrictions caused land-based gambling establishments to close. However, online casino is illegal across most of Asia and in China, and it’s unlikely that this will change anytime soon.

Like most areas where online gambling is illegal, the illegal market is present, and the lack of legal gaming doesn’t stop numerous offshore gambling sites from targeting and accepting Chinese players (even so, there are significant issues with payment processing and legal clampdowns).

While it’s more challenging to find data regarding online gambling in China due to its illicit nature, we can look at the Asian-Pacific region as a whole, which includes China, Japan, South Korea, Malaysia, Singapore, Vietnam and Cambodia. This region has been publicised as one of the fastest-growing gambling markets currently, with IMARC Group charting the size of the online gambling market in the region at $19.5bn in 2022 with a projected growth rate of 11.39% between 2023-2028.

Many Asian affiliates use social media platforms to refer players to offshore gambling operators, such as Weibo or WeChat (China’s most extensive social network) or messaging apps like Tencent/QQ. This contrasts with the operations of traditional gambling affiliates such as Slot Gods, where players are referred to operators licensed in the players’ home country. Secure referrals to licensed gambling sites ensure legitimacy in online gambling regimes as well as increased player safety. Sports advertising also plays a significant role in directing traffic, with Asian English Premier League sponsorship deals securing greater exposure for gambling brands when EPL games are aired in Asia.

Data on the types of games and revenue per game for the online casino industry servicing Chinese clientele is also not readily available. Extrapolating from land-based trends, gamblers in Macau tend to be high rollers who focus on table games, like baccarat and roulette, and VIP gamers account for 43% of revenue. This differs from European online gambling jurisdictions, where online slot games are the most popular type of casino game and generate the most revenue at around 42%.

A slower recovery?

Despite garnering less attention than Monte Carlo, Paris or London, Macau is still the largest casino gambling jurisdiction in the world. While COVID policies have depleted Macau’s gambling industry, there is hope, and it is expected to recover. Still, due to the Chinese government’s attempts to rain in the sector while diversifying the economy, as well as the territory’s reliance on tourism, it might not be as quick as gambling operators would like.

In today’s ever-changing economic landscape, securing a strong financial future has become more crucial than ever. With uncertainties in traditional investment avenues, more individuals are turning to alternative options such as Gold Individual Retirement Accounts (IRAs) to safeguard their retirement funds.

Gold, known for its stability and long-term value retention, has garnered attention as a reliable asset to include in retirement portfolios. However, navigating the realm of Gold IRA investments requires careful consideration and choosing the right company to partner with. This article delves into the significance of Gold IRAs and provides insights into selecting the best Gold IRA companies to ensure a robust financial future.

Understanding Gold IRAs

A Gold IRA is a specialized retirement account that allows investors to include physical gold and other precious metals within their portfolio.

This type of IRA provides diversification, safeguarding retirement savings from the volatility often associated with traditional investment vehicles like stocks and bonds. Precious metals, particularly gold, have historically acted as a hedge against inflation and economic downturns, making them an attractive option for long-term wealth preservation.

Why Gold IRAs Matter

Diversification: A well-diversified portfolio is key to managing risk. Gold IRAs offer a unique avenue for diversification, as gold often moves inversely to the stock market. This means that when equities are underperforming, gold tends to hold its value or even appreciate, helping to stabilize overall portfolio performance.

Inflation Hedge: Gold’s value has shown resilience during periods of high inflation. As central banks increase money supply, the value of paper currency can decrease. In such scenarios, the value of gold typically rises, providing a hedge against the eroding purchasing power of money.

Long-Term Store of Value: Throughout history, gold has maintained its value over the long term. Unlike paper assets that can become worthless, gold’s intrinsic worth is widely recognized, making it a reliable store of value for future generations.

Portfolio Insurance: Gold serves as a form of insurance within a portfolio. In times of economic uncertainty or geopolitical turmoil, the demand for gold tends to surge, potentially benefiting Gold IRA holders.

Selecting the Best Gold IRA Companies

Choosing the right Gold IRA company is a critical step toward building a strong financial future. You can see a list of top-tier Gold IRA companies, complete with their distinctive features and pricing details, let’s check out this link: https://www.wishtv.com/sponsored/best-gold-ira-companies/

Here are essential factors to consider when evaluating potential companies:

Reputation and Trustworthiness: Research the company’s reputation within the industry. Look for established companies with a history of serving clients well and adhering to ethical business practices. Online reviews, ratings, and independent assessments can provide insights into a company’s reputation.

Experience and Expertise: Opt for companies with experience in the precious metals and retirement account sectors. A knowledgeable company can guide you through the process, answer your questions, and provide valuable advice based on market trends.

Transparency: A trustworthy Gold IRA company should provide clear and transparent information about fees, processes, and the types of assets they offer. Hidden fees or complex terms can lead to unexpected costs and complications down the line.

Storage Options: Physical gold needs secure storage. Ensure the company offers secure storage options, such as insured and segregated storage facilities, to safeguard your precious metals investments.

Customer Service: Excellent customer service is vital, especially in the world of finance. A reputable company should be responsive to your inquiries and provide clear communication throughout the investment process.

Flexibility: Look for companies that offer a range of precious metals options beyond just gold, such as silver, platinum, and palladium. Diversification within precious metals can further enhance your portfolio’s stability.

Conclusion

As individuals seek to build a strong financial future, Gold IRAs have emerged as a compelling option for preserving wealth and mitigating investment risks. With their historical value retention and inflation-hedging capabilities, precious metals like gold can play a crucial role in diversifying retirement portfolios. However, selecting the right Gold IRA company is paramount to ensure a smooth and successful investment journey.

By prioritizing factors such as reputation, experience, transparency, storage options, customer service, and flexibility, investors can make informed choices about the best Gold IRA companies to partner with. With the right guidance and prudent decision-making, individuals can leverage the stability and potential growth offered by Gold IRAs to secure a solid financial foundation for their retirement years.

The automotive industry is undergoing a major transformation, driven by the rise of digital technologies. In order to stay ahead of the curve, automotive companies need to embrace digital transformation and unleash their automotive expertise in the digital realm.The future of the automotive industry lies in the hands of those who are capable of driving, and it is essential that automotive expertise is unleashed in the digital realm.

Digital technology has revolutionised the way we live, work, and do business. From smartphones to social media platforms, the digital world has changed the way we connect, communicate, and consume information.

The automotive industry is no stranger to digital technology, and as vehicles become increasingly connected and autonomous, the industry is poised to undergo a major transformation. Automotive professionals who are able to navigate this change and embrace digital technology will be well-positioned to succeed in the industry of the future.

In this post, we will explore the role of digital technology in the:

Automotive industry digital transformation strategies

The automotive industry is rapidly undergoing a digital transformation, with many companies looking to implement strategies to stay competitive and meet the changing needs of consumers.

These strategies often involve leveraging digital technologies to optimize operations, enhance customer experiences, and develop new business models. By embracing digital tools and technologies, automotive companies can improve their agility, responsiveness, and efficiency, while also gaining new insights into customer behavior and preferences.

Adopting a customer-centric approach

It is essential for driving digital excellence in the automotive industry. In today’s digital age, customers have more power than ever before. They have access to information about products and services, and they can quickly compare prices and read reviews before making a purchase.

By adopting a customer-centric approach, automotive companies can tailor their products and services to meet their customers’ needs, resulting in increased customer satisfaction and loyalty. Ultimately, this leads to a more successful and profitable business in the digital realm.

Building agile digital solutions

Digital transformation is reshaping the automotive industry, and companies that fail to adapt will be left behind. Building agile digital solutions is essential for staying competitive in this rapidly changing landscape and there is digital marketing for car dealers also that proves of immense help. By adopting agile methodologies, automotive companies can quickly respond to market changes, and deliver innovative products and services.

Agile teams work collaboratively, breaking down silos and promoting cross-functional communication to develop flexible and adaptable solutions. This approach promotes continuous improvement, enabling companies to continuously iterate and refine their digital products and services to meet evolving customer needs.

Leveraging data analytics tools

To stay ahead of the competition, companies must leverage data analytics tools to gain valuable insights into customer behaviors, preferences, and market trends. With the right tools and expertise, businesses can gain a competitive edge by making data-driven decisions that improve operational efficiencies, enhance customer experiences, and drive revenue growth. From predictive analytics to machine learning, there are a variety of data analytics tools available to automotive businesses.

By embracing digital transformation, automotive companies can unleash their automotive expertise in the digital realm and stay ahead of the curve in the rapidly changing automotive industry.Here are some specific examples of how automotive companies are using digital technologies to drive innovation:

Volkswagen is using 3D printing to create prototypes of new vehicles more quickly and easily. This allows Volkswagen to test new designs and iterate more quickly, which can lead to better products.

Tesla is using artificial intelligence to improve the performance of its self-driving cars. Tesla’s self-driving cars use AI to constantly learn and improve, which makes them safer and more efficient.

BMW is using big data to optimize its manufacturing processes. BMW collects data from its factories and uses it to identify areas where it can improve efficiency. This has led to significant cost savings for BMW.

Mercedes-Benz is using social media to engage with customers. Mercedes-Benz has a large following on social media, and it uses this platform to connect with customers, share news and updates, and get feedback.

Ford is using telematics to monitor vehicle health. Ford’s telematics system allows the company to monitor the health of its vehicles and provide remote diagnostics. This can help Ford to identify and fix problems before they cause major damage.

These are just a few examples of how automotive companies are using digital technologies to drive innovation. As the automotive industry continues to evolve, we can expect to see even more innovative uses of digital technologies in the years to come.

Automotive companies must invest in the right technologies, build digital talent and capabilities, and create a culture of innovation and collaboration. Only by doing so can they unlock the full potential of digital and stay ahead of the curve in the years to come.

Apple Inc. (NASDAQ:AAPL) is an American tech giant, a real heavyweight in the global corporate scene. The company is known for its innovative gadgets, such as the iPhone, iPad, and Macbook, not to mention their nifty software like the iOS operating system.

Apple has recently reported its third quarter results of fiscal year 2023. Revenue reached a record high of $21 billion, which is a solid 8.2% rise. Such growth is attributed to more than a billion of paid subscriptions to music and TV streaming services, plus software sales through the Apple Store. However, it is alarming that the segment’s growth rate has taken a bit of a dive: in 2021, they were growing at a whopping 27.3%, in 2022 this number was almost half as big – 14.2%, and by the end of the first half of 2023 the rate diminished to mere 6.7%. Experts think it might pick up again to around 14%, but it’s a bit too early to say for sure.

The company managed to reach the $3 trillion mark of capitalization. Nevertheless, for the second week in a row, the company’s been seeing a drop in their stock price. With the profit report released on August 3, this trend got more pronounced. It got so intense that the trend line got broken, and sellers began to act pretty aggressively.

The main factor for the current slide is the decline in the smartphone market along with increased competition, especially from Asian companies, and the tightening of antitrust regulation, which has become a priority in the US. Speaking of the smartphone market, we can observe a certain correlation. After the boost triggered by the pandemic, the market had to slow down and saturate itself with new gadgets and tech, a people need time to adjust to new systems before they’re ready to embrace the next ones. The market has been flooded with options. Therefore, the purchasing power has decreased. After Covid, most smartphone manufacturers, tried to regain their pre-pandemic production rates as quickly as possible. Some companies managed it, some didn’t, but overall the market started gaining momentum.

Apple is one of those companies that sells the same candy in a different wrapper, presenting it as something as revolutionary. Though most are aware of this trick, they still fall for it sometimes. Nevertheless, the sales data hasn’t been great, and the company is forced to prematurely suspend production of less popular models, which consequently affects the indicators and revenue. A good example is the Mini lineup models, which posted the worst sales results in the company’s history. The global appetite for electronics is kind of weak, which led to a 2.4% drop in iPhone revenue and a 7.3% slump in Mac sales. Still, the number of active Apple devices hit a new high during the June quarter.

However, there’s a bunch of investors who still have faith in Apple stock, and here’s why. The current decline slowed down right around the critical support level of $177. This level is a mirror one – previously, it acted as a strong resistance and restrained growth but after a previous drop and then a surge, the price finally managed to break through it. Thus, a rollback is regarded as an expected correction, and the level itself is a zone of interest for major players. Although, most often, after a stop, a slight lateral movement follows to accumulate volumes. Accumulation helps establish a balance between supply and demand. And the presentation of new devices this fall is likely to give things a boost. Roughly speaking, the market froze in anticipation of the following “breakthrough” technologies to keep the growth going.

The probability that the level will give way remains, but in this case, sellers will have to face the historical accumulation that formed back when the level was a resistance. If that happens, all eyes would be on it and around the $150 area.

Major players are already showing confidence in continued growth. For example, Berkshire Hathaway, whose investment portfolio includes Apple stock worth $177.6 billion.

And there’s another thing messing with Apple’s sales figures: the almighty dollar. You see, a good chunk of their revenue comes from abroad. Apple’s CEO, Tim Cook, and its CFO, Luca Maestri, have mentioned that if the exchange rate of the US currency doesn’t change, their sales should still show some year-on-year growth.

From all of the above, it seems reasonable to say that the chances of the shares continuing to drop are notably lower than the continuation of growth after a rebound from the current support. The stability in the reported figures and the upcoming presentation of new devices are hold key importance in stirring up the market.

In addition, the company plans to continue investing in AI and augmented reality related developments. The projects that didn’t quite hit the mark, like the Apple Vision Pro, haven’t been entirely abandoned, and we have yet to see the real revolution. After all, Apple is not the sort of company that gives up on its projects, especially expensive ones, but squeezes as much as possible out of them.

When you put all these pieces together, it’s a strong indication that Apple maintains its status as a leader and one of the most triumphant companies in the realm of technology, both nationally and across the globe. Their achievements owe a great deal to their products and the strategic path they’ve chosen.

This is part 2 of this series of articles on the New Cold War. (Link to Article Part 1) Kalim Siddiqui concludes his analysis of the global geopolitical situation, with reference in particular to the US, China, and Russia, comparing and contrasting it with the Cold War period of the late twentieth century.

IV. Economic and Trade Rivalry

US post-war military strategy was based on the view that a rise in military expenditure would have more than proportionate effects on growth rates, jobs, consumption, and investments, i.e., the well-known Keynesian multiplier effect. A National Bureau of Economic Research study (2019) found that defence spending of US$1 billion raised the economy by US$1.5 billion.

The US has always maintained superiority in defence to enhance its industrial, financial, and technological power. Cypher notes, “to conserve global ‘primacy’, US grand strategy requires a ‘core commitment’ to (1) maintenance and enhancement of US military power projection capabilities; (2) preservation and expansion of the structural dominance of the laissez-faire economic ‘order’; and (3) protection and revision of the post-war global institutional configuration” (Cypher, 2016: 800).

But compared to the earlier Cold War, in the new Cold War, we find that, while the US is very critical of the ideas of the Chinese Communist Party, the Chinese official media refrains from denouncing American values. China and the US, unlike the former Soviet Union, have engaged deeply in trade, investment, the supply chain of vital products, and student exchanges. This is the reason that the new Cold War is quite different and will involve tremendous economic and social costs for both sides. We do not see any direct military confrontation between the countries and have no proxy war. There is a potential flashpoint in the South China Sea.

China’s unprecedented opening of its markets through trade and investment, while keeping its national strategic industries firmly under the public sector, in the presence of the massive availability of cheap labour, made China the most important destination of the global supply chain after the country joined the WTO.

Deng Xiaopeng in 1992 visited the southern region of China and extended his full support to the “market reforms” in China. Soon after, President Clinton granted China most-favoured-nation treatment and said that his administration would continue to support pro-market reforms in China. He said that China was a huge market and it was very important for US companies to engage with China. As Lixin writes, “The engagement strategy includes three aspects. First, support for China’s Reform and Opening-up and modernisation, a relaxation of technology transfers to China, granting China permanent most-favoured-nation status and encouraging American businessmen to invest in China. Second is the promotion of extensive exchanges and cooperation in culture, education, academics, and science between the two countries, and the promotion of the spread of Western values in China. Third, support for and acceptance of China’s accession to the World Trade Organisation and other international organisations and increasing China’s voting rights in the World Bank, the International Monetary Fund, and other international institutions” (Lixin, 2021:8).

China’s unprecedented opening of its markets through trade and investment, while keeping its national strategic industries firmly under the public sector, in the presence of the massive availability of cheap labour, made China the most important destination of the global supply chain after the country joined the WTO. By investing in China, MNCs attained economies of scale and became internationally competitive in terms of reducing costs and thus raising returns (Stiglitz, 2015).

However, indigenous manufacturing was generally located at the low end of the value chain and hence operated with low profit margins and faced a few challenges in acquiring and upgrading advanced technologies. From 2006 onwards, the Chinese government introduced a new policy to facilitate indigenous innovation with the target to achieve increased high-tech innovation by 2022. The policy targeted mainly unexploited areas such as energy, environment, high-tech manufacturing, and services.

For more than three decades, China’s labour productivity rose faster than wages in the manufacturing sector and thus rates of profits were much higher than in the US. China produces more goods than the US used to produce. And we find that the rapid development of communication technology and the fact that China can compete with the US have alarmed US leaders.

The rapid rise of high-tech Chinese companies poses a major challenge to the US manufacturing sector and that was the reason that then-President Obama put forward the slogan “Bringing manufacturing back to America”. The Trump administration took it forward but forgot to see that implementing such a policy is not an easy task. The US does not have a comparative advantage in the manufacturing sector; one reason could be that US wages are higher compared to China. The other reason is the US financial sector, which is built on various forms of derivatives and its size has grown enormously since, in the mid-1990s, it acquired financial freedom in the name of efficiency and high returns, while China’s financial sector is strictly government-controlled and regulated (Yao, 2021).

Since the 2008 global financial crisis, China has narrowed its income and technological gaps with the US, and this is seen as a threat to the US that China is challenging US technological and economic supremacy. China’s catch-up with the US was staggering. For instance, in 2008, China’s GDP was only 31.2 per cent of the US GDP but, 12 years later, the number has more than doubled. In 2008, there were only 35 Chinese companies in the Fortune Global 500 list of the world’s largest companies based on revenues, which was far below the number of US companies. But in 2021, China had 124 companies in the Fortune List, which was more than the US. Such development has given Chinese leaders more confidence in their economic policy. Academics also in recent years began debating China’s success and it was said that the dramatic rise of China was due to its authoritarian government policy with active state involvement in the economy, i.e., state capitalism (Li, 2020).

China produces more goods than the US used to produce. And we find that the rapid development of communication technology and the fact that China can compete with the US have alarmed US leaders.

In the past, virtually all the now-advanced economies had adopted interventionist industrial policies to promote domestic industries, exports, and investments. They also supported industrialisation in their take-off stage of economic development and structural change. It means that industrialisation must precede liberalisation. But to say that China did the opposite by liberalising its economy before industrialisation from the mid-1980s onwards is incorrect.

In December 2017, the Trump administration unveiled the US National Security Strategy Report, which proposed that the US was entering into a new era of power competition. The report portrayed China as a “strategic competitor” that wants to shape a world antithetical to US values and interests. US elites were alarmed by China’s fast upgrading of its advancements in the telecommunications sector. The US ban on Chinese access to high-tech would affect innovation because it needs markets to meet the costs. China is the largest market for US products and cutting off US companies from the Chinese markets would adversely affect their global expansion and would ultimately slow down their innovation.

According to statistics, the total volume of services trade between the US and China was US$120 billion in 2017 and the volume of goods trade in 2018 reached US$633.5 billion. By December 2018, the US’s total investment reached US$85.2 billion in China. And in 2017, the number of Chinese students studying in US higher academic institutions was more than 350,000, which then accounted for nearly 33 per cent of the total number of international students in the US. In 2019, five million people travelled between the two countries.

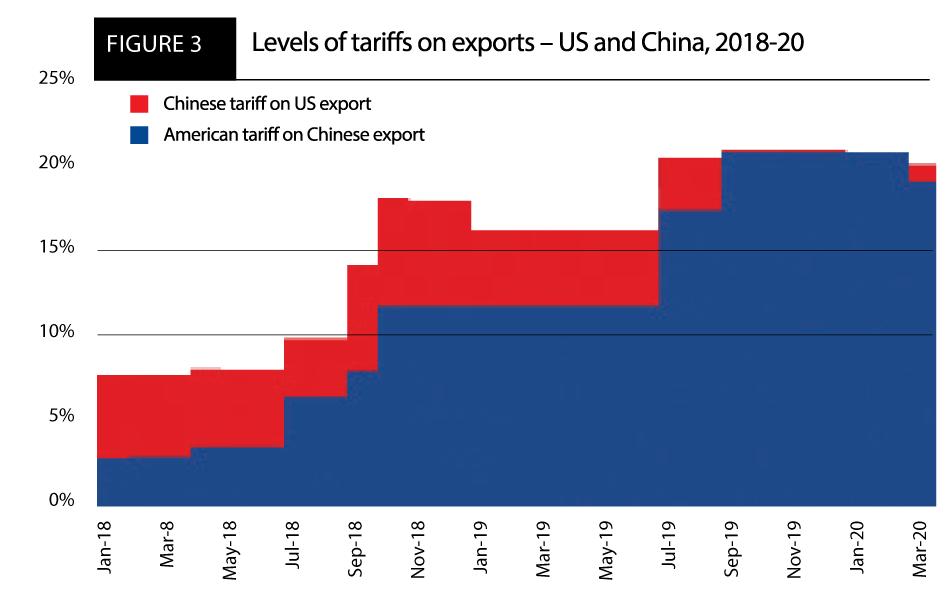

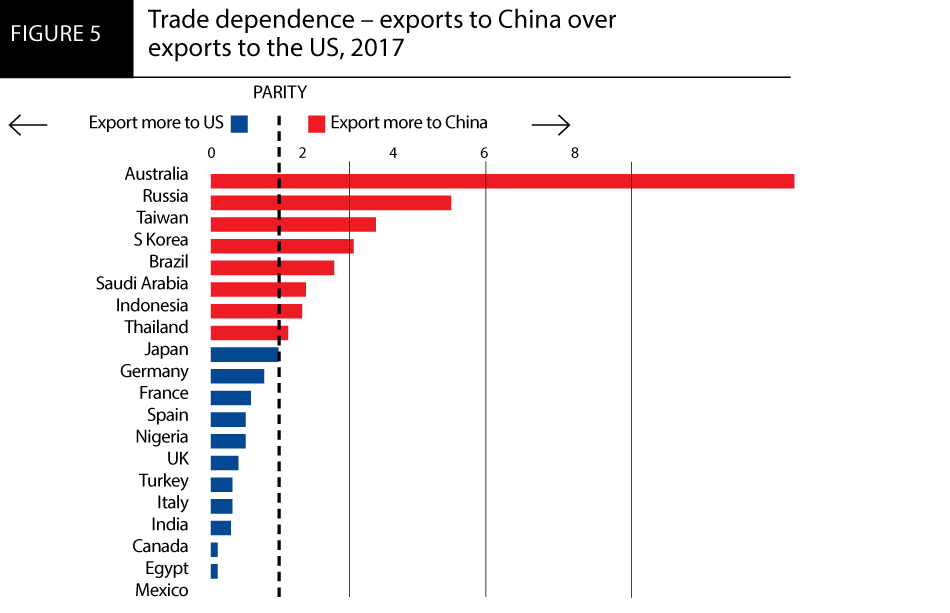

In July 2018, President Trump imposed tariffs on several goods imported from China, which continued after Biden became president. Due to this rising trade conflict, imports from China to the US have been reduced (see figures 2 and 3). Imports from China declined further from March 2020 as global trade collapsed due to the COVID-19 pandemic and have since then recovered gradually. Only recently, US imports from China have returned to pre-trade-war levels, while imports from the rest of the world are above the pre-war level. China is now the source of only 18 per cent of total US goods imports, down from 22 per cent at the onset of the trade war. In contrast to this, at present, US imports from the rest of the world have risen to 38 per cent compared to pre-trade-war levels and are even above that level (blue line). With a few exceptions, these imports were not hit with new US tariffs.

The world has entered a new age of intra-core rivalry and US and Chinese competition will shape the trajectory of the capitalist world order for decades to come.

In fact, President Trump under Section 301 of the Trade Act of 1974 imposed a tariff of 25 per cent on products of nearly US$34 billion of US imports from China in July 2018. China retaliated, the trade war continued, and the US imposed 10 per cent tariffs on an additional US$200 billion of imports in September 2018, increasing the rate of those duties to 25 per cent in June 2019.

Moreover, the goods that were affected by 25 per cent tariffs by the US were largely intermediate inputs and capital equipment which, because they were used by firms to make other consumer goods or to provide services, were less visible to consumers. Imports of some products were lower, despite rising demand in the US during the pandemic, contributing to shortages, and costs for firms using these imported inputs rose sharply. As a result, such companies were forced to either continue importing from China even with the tariff or find new suppliers from other countries. Other examples, such as IT hardware and electronics, were in higher demand during the COVID-19 lockdown, i.e. modems, routers, network servers, smart watches, and wireless headphones. In fact, US imports from China of such goods declined from 62 per cent after the imposition of 25 per cent tariffs. In contrast, US imports from the rest of the world are now 60 per cent higher. China’s share of US imports of IT hardware and consumer electronics has declined from 38 per cent to 13 per cent.

Other important products imported were vehicle parts from China, which was seen by the US car industry as a threat. Imports from China and the rest of the world fell sharply during COVID-19, as the car industry in the US stopped production due to the COVID-19 pandemic. After the end of the pandemic, US imports from the rest of the world have recovered and at present it is 20 per cent higher, but imports from China due to the tariffs have only just returned to pre-trade-war levels. However, China’s share of US vehicle parts imports has only dropped from 15 per cent to 13 per cent.

The US sees China under President Xi Jinping as becoming more assertive and stronger, both economically and militarily, with its boosting economy not even deterred by the recent adverse impact of COVID-19 and backing its Belt and Road Initiative (BRI) (Siddiqui, 2019b). It seems that any return to the pre-2017 world of “strategic engagement” with China is unlikely.

The Chinese economic policy of advancing its technological capability, particularly “Made in China 25”, is certainly seen by the US as direct competition with the US global companies in the services and knowledge sectors. This Chinese attempt is taken as competition rather than complementary and seems to be a threat to US global technological hegemony. Thus, new development has created a rift between the US and China since 2018.

China’s economic rise is underlined by its growth model, which is perceived to have the desire to re-divide the world and expand its sphere of influence. Therefore, it is predicted that the US and China will continue to be strategic rivals, shaped by external and internal forces (see figures 4 and 5). The world has entered a new age of intra-core rivalry and US and Chinese competition will shape the trajectory of the capitalist world order for decades to come.

In 2010, China began to show its financial ambitions by using the Renminbi in international transactions and as a part of projecting the Renminbi as a global currency. The reason for China’s global financial desire was due to the fact that its economic share of global GDP had almost quintupled from 4 per cent to 18 per cent, and its share of global trade had quadrupled to 15 per cent in the last two decades. In recent human history, no other economy in the world has grown so fast and in such a sustained way for so many years. Moreover, China’s stock market has been performing well compared to other developed economies, and the Renminbi raised its share of global central bank reserves to 3 per cent in 2021, up from 1 per cent in 2016 (Sharma, 2022).

During the past decade, China has printed a lot of money to stimulate growth. But capital control has been imposed to prevent capital flight and this may hinder capital from fleeing the country when given the chance. Sharma notes, “Since 2015, the Renminbi share of payments through the Swift network for international bank transactions has fallen by a fifth, from an already negligible level under 3 per cent. A widely followed index that ranks 165 nations by capital account openness puts China at 106th… While Chinese investors are restricted from investing abroad, foreigners are scared away from China by erratic government attempts to control the market. That helps explain why unlike in other nations, stocks in China do not rise and fall with economic growth” (Sharma, 2022).

In fact, at present in China, foreign companies own only 5 per cent of stocks, while nearly 28 per cent in other emerging markets, and about 3 per cent of bonds in China, compared to around 20 per cent in other developing nations (Sharma, 2022). However, nearly 90 per cent of global foreign exchange transactions take place in US dollars, and only 5 per cent are in Renminbi.

During the Japanese economic boom of the 1980s, the country emerged as both a financial and economic power. The Japanese yen and stocks reflected that strength and Tokyo emerged as a global financial centre. However, at present, the Chinese Renminbi is not considered by investors a safe destination. China is still a long way from becoming a financial superpower.

US President Joe Biden, in a joint speech to the US Congress, declared that the US is in competition with China “to win the 21st century”, as he put it. However, the US government under Biden, and of course before, under Trump, has imposed several rounds of sanctions on Russia and China. So, while on the one hand, he is continuing the nationalistic trade policies of the Trump administration, Biden is escalating the new Cold War against Russia and China, in the belief that the US can impose sanctions and isolate them, which will lead to the fall of their governments (Kovalik, 2017).

There is a serious threat of escalation beyond Ukraine, not to mention the danger of nuclear war.

The US attempted to isolate Russia, so that it can recapture the resources and resume the sale of Russia’s national resources and public utilities to the US-based MNCs. This is unlikely to be repeated. The actual effect of the sanctions on Russia and China has been to drive them together, rather than isolate them.

The question in this is, what about Europe? In the last few weeks, there has been a lot of discussion about cutting Russia off from the SWIFT bank clearing system, and of other sanctions against Russia. Russia has already worked with China to develop its own alternative to the SWIFT banking clearing system. So Russian domestic payments are not going to be that disrupted, after the week or two that they say it will take to put the new system in. But certainly, cutting off Russia from the SWIFT system does block its trade and its economic relations with Europe. The US would like to see Europe more dependent on the it for the supply of vital resources.

In the US, money is not made by its companies investing in industry and in production. But its big companies can make huge profits, largely via monopoly rents, resource rents, or other forms of rent extraction. And 90 per cent of corporate income in the US is spent on share buybacks and dividend pay-outs, not on investing in new industries and it is no longer expected that any dramatic increase in private investment in manufacturing will occur in the US, while China is trying to avoid the rentier policies, as well as the financialisation and privatisation that has made America so high-cost and so ineffective. And the US is blaming China for over-regulating and supporting its businesses (Siddiqui, 2021).

For the classical economists, the whole concept of free markets, from Adam Smith to John Stuart Mill, was to free industrial capitalism from the rentier class, from the landlords, and from banking and the monopolies that banks created in organising trusts. So, the US realises that the economy has been transformed in the last 40 years, since the 1980s, since Ronald Reagan and Margaret Thatcher, when Margaret Thatcher said, “There is no alternative.” Of course, there were many alternatives. But the US would like to create the “rules-based order” of free markets, meaning no government power to regulate or tax the corporate and rules-based order that supports the rentier class – a hereditary, financial, small minority of rich corporates of the population, which could hold the rest of the population in debt, or keep them in permanent dependency and job insecurity.

The US has often used its military power to enhance its political, industrial, and financial base. As Brooks et al. emphasised, “Deep engagement allows the United States to institutionalise its alliances and wrap its hegemonic rule in its rules-based order. The result is to make the US alliance system – especially among its core liberal members – far more robust and harder to challenge than if the United States were to disengage” (cited in Cypher, 2016:801).

On Ukraine’s current crisis, Professor John Mearsheimer (2022) argues, “The West, and especially America, is principally responsible for the crisis which began in February 2014. It has now turned into a war that not only threatens to destroy Ukraine but also has the potential to escalate into a nuclear war between Russia and NATO. The trouble over Ukraine started at NATO’s Bucharest summit in April 2008… Russian leaders responded immediately with outrage, characterising this decision as an existential threat to Russia and vowing to thwart it. According to a respected Russian journalist, Mr Putin “flew into a rage” and warned that “if Ukraine joins NATO, it will do so without Crimea and the eastern regions… America ignored Moscow’s red line, however, and pushed forward to make Ukraine a Western bulwark on Russia’s border… These efforts eventually sparked hostilities in February 2014, after an uprising (which was supported by America) caused Ukraine’s pro-Russian president, Viktor Yanukovych, to flee the country… The next major confrontation came in December 2021 and led directly to the current war. The main cause was that Ukraine was becoming a de facto member of NATO… Unsurprisingly, Moscow found this evolving situation intolerable and began mobilising its army on Ukraine’s border last spring to signal its resolve to Washington. But it had no effect, as the Biden administration continued to move closer to Ukraine.” He further states, “America and its allies may be able to prevent a Russian victory in Ukraine, but the country will be gravely damaged, if not dismembered. Moreover, there is a serious threat of escalation beyond Ukraine, not to mention the danger of nuclear war” (Mearsheimer, 2022).

China’s phenomenal growth over the last four decades has had no comparison in human history. China has done quite well so far in terms of growth and has been able to reduce poverty significantly in the last less than four decades.

Russian President Putin appears to be concerned about the security threat to his country. But due to this security threat, he opposes the IMF policy not because the IMF is basically a promoter of international finance capital but because the IMF is promoting US foreign policy. Putin is concerned with the role of the IMF in facilitating the US hegemony over Ukraine. But in the case of the confrontation between Russia and Ukraine, there seems to be a close intermingling of the US foreign policy interests with the IMF. Therefore, it is not only the question of the role of the IMF but here in this instance, keeping Ukraine under IMF control. Moreover, the IMF insists that to borrow more, Ukraine has to meet certain conditionalities including a reduction in real wages and cuts in welfare spending, particularly in the healthcare and education sectors.

Putin has presided over the growth of tremendous inequality in Russia. However, it began with the collapse of the Soviet Union and then, under President Boris Yeltsin, Russia witnessed a huge rise in inequality.

In the name of efficiency and competition, the IMF would like to eliminate the role of the government to intervene in the economy. It means the removal of subsidies to small and medium producers and their role to keep essential goods prices low and remove its role to provide education, healthcare, and employment.

There is a general objective of the MNCs that all countries should be open to the free movement of capital and finance and even commodities. In fact, that is the essence of the neoliberal economic policy that fundamentally economies should be opened. It is not just for capital to come in and set up industries or capital to come in and buy up industries. But capital must come in also to take control of the sources of raw materials (Siddiqui, 2022).

V. Conclusion

During the Cold War with the Soviet Union, there was an ideological confrontation between communism and capitalism. It was generally believed that the hegemony of international finance capital was thwarted by the Soviet Union and East European countries, as these countries were part of the centrally planned economies and not integrated with the US and EU markets. Under it, the state played a very important role in generally directing the way in which the economy was to develop. Therefore, that was a regime in which the Soviet Union was opposed to the free operation of the market and the free operation of international finance capital.

Putin is by no means against the hegemony of international finance capital. He is not in an ideological battle against the domination of a neighbouring country by an organisation that acts in the interests of international finance capital. His concern is only with Russian security. He is, in other words, concerned only with the role of the IMF as a promoter of US geostrategic interests, not with the role of the IMF as a promoter of neoliberalism in general. In fact, the gross inequality and even absolute destitution that a neoliberal regime created is not too far from what Putin himself has achieved. We should not forget that after the collapse of the Soviet Union, the IMF’s neoliberal reforms were adopted by Russia and resulted in a huge drop in the country’s GDP, a huge fall in the national income, and a massive increase in unemployment.

In the 1980s, when China opened its economy for foreign capital and technology with its low unit costs attracted foreign capital, China became a new “workshop of the world”. Due to the availability of cheap labour and good infrastructure, China was able to retain a large proportion of surplus value generated in the case of most developing countries and successfully created joint ventures and partnerships with global businesses and access to acquire new technology from Western companies.

In the 1990s, when China opened to international trade and was admitted to the WTO in 2001, this opened a huge market to foreign companies and investors where MNCs based in the West could sell their products and get rid of the overproduction crisis. And also, taking advantage of a huge pool of educated and low-cost workers and earning higher profits under such circumstances, China became the “workshop of the world”. During the 1990s, China’s exports enjoyed low-tariff access to the US market, which encouraged China to join WTO in 2001. In February 2020, the US and China kept the same level of tariffs. Compared to the pre-trade-war period, US tariffs on Chinese products increased 2.5 times (Yao, 2021).

China’s phenomenal growth over the last four decades has had no comparison in human history. China has done quite well so far in terms of growth and has been able to reduce poverty significantly in the last less than four decades.

This study has discussed the rising tension on economic and strategic issues, especially between the US, China, and Russia, and it seems that following the end of the Cold War, the US in its quest to consolidate its global hegemony has attempted to redraw the imperialist spheres of influence globally.

At present, the US economy is performing poorly in terms of growth, productivity, and investments compared to China. The challenger, i.e., China, has to figure out in which areas the US is weak and how to strengthen its economy and global influence. This is the same strategy the US adopted a century earlier when it was trying to replace Britain. Recently, China has made an alliance with Russia.

Until recently, the US was motivated by the hope that Chinese elites would become a countervailing force against the military and Communist Party establishment. It seems that the present criticism against China is built on its economic success rather than its ideology. China’s success is based on a careful application of state capitalism through gradually promoting and enhancing industrialisation by taking advantage of low-cost production and access to global markets.

This study concludes that the US has long applied economic sanctions as a means to try to undermine the governments that oppose US policies. The US-China economic rivalry could generate a “sphere of influence” in which countries could be drawn into the sphere of influence and thus, could possibly divide the world. So, we are seeing an intensification of economic warfare, especially against China and Russia, and the US is hoping that somehow this will weaken and divide them.

Dr. Kalim Siddiqui is an economist specialising in International Political Economy, Development Economics, International Trade, and International Economics. His work, which combines elements of international political economy and development economics, economic policy, economic history and international trade, often challenges prevailing orthodoxy about which policies promote overall development in less-developed countries. Kalim teaches international economics at the Department of Accounting, Finance and Economics, University of Huddersfield, UK. He has taught economics since 1989 at various universities in Norway and the UK.

References

Arrighi, G. (2007) Adam Smith in Beijing: Lineages of the Twenty-First Century, Cambridge: Verso.

Christensen, T.J. (2021) “There will not be a New Cold War”, Foreign Affairs, 24 March.

Cypher, J.M. (2016) “Hegemony, military power projection and US structural economic interests in the periphery”, Third World Quarterly, 37(5):800-16.

Fukuyama, F. (1992) The End of History and the Last Man, Free Press, New York.

Girdner, E.J. and Siddiqui. K. (2008). “Neoliberal Globalization, Poverty Creation and Environmental Degradation in Developing Countries”, International Journal of Environment and Development 5(1):1-27, January-June.

Holloway, S.K. (1983) “Relations among the Core Capitalist States: The Kautsky-Lenin Debate Reconsidered”, Canadian Journal of Political Science, 16(2): 321-33.

Kennan, G.F. (1995) “Fateful Error”, New York Times, New York, 5 February.

Kennedy, Paul (1987) The Rise and Fall of the Great Powers: Economic Change and Military Conflict from 1500 to 2000, Random House: New York.

Kindleberger, C. (1973) The World in Depression, 1929-1939, University of California Press: USA.

Kovalik, D. (2017) The Plot to Scapegoat Russia: How the CIA and the Deep State Have Conspired to Vilify Russia, Skyhorse Publishing: New York.

Leffler, M.P. (2019) “China isn’t the Soviet Union: confusing the two is dangerous”, Atlantic, December.

Lenin, V.I. (2010) Imperialism: The Highest Stage of Capitalism, Penguin: UK. [First published in 2017].

Li, X. (2020) “The rise of China and its impact on the world economy stratification and re-stratification”, Cambridge Review of International Affairs, 34(4): 530-50.

Lixin, W. (2021) “What can history reveal about the future of Sino-American relations? – Retrospect, reflections, and prospects”, Chinese Studies in History, 54(1):5-18.

Mazur, O.A. (2009) Development of the Workforce of Contemporary Russia, St Petersburg University Publication, St Petersburg.

Mearsheimer, J. (2022) “Why the West is principally responsible for the Ukrainian crisis”, The Economist, London, 11 March.

National Bureau of Economic Research (2019) “Local Fiscal Multipliers and Fiscal Spill overs in the United States”, Working Paper No. 25457, January.

Politi, J. (2022) “The U.S. Pours Cold Water on Hopes of Diplomatic Solution in Ukraine,” Financial Times, London, 17 March.

Sharma, R. (2022) “Why China is not rising as a financial superpower”, Financial Times, 20 June, London.

Siddiqui, K. (2009). “The Political Economy of Growth in China and India”, Journal of Asian Public Policy 1(2):17-35, March.

Siddiqui, K. (2018a). “U.S. – China Trade War: The Reasons Behind and its Impact on the Global Economy”, World Financial Review, November/December, p. 62-8.

Siddiqui, K. (2018b). “David Ricardo’s Comparative Advantage and Developing Countries: Myth and Reality”, International Critical Thought, 8(3):1-28, September.

Siddiqui, K. (2019a). “Economic Transformation of China and India: A Comparative Political Economy Perspective”, Asian Profile, 47(3):243-59.

Siddiqui, K. (2019b). “One Belt and One Road, China’s Massive Infrastructure Project to Boost Trade and Economy: An Overview”, International Critical Thought. 9(2):214-35.

Siddiqui, K. (2020a). “Prospects of a Multipolar World and the Role of Emerging Economies”, World Financial Review, November/December, 65-77.

Siddiqui, K. (2020b). “The Rise of the Chinese Economy and Growing Concerns in the United States”, World Financial Review, September October, p. 40-9.

Siddiqui, K. (2020c). The Impact of COVID-19 on the Global Economy, World Financial Review, May-June 25-31.

Siddiqui, K. (2020d). “The US Dollar and the World Economy: A critical review”, Athens Journal of Economics & Business 6(1):21-44, January.

Siddiqui, K. (2021a). “Can the 21st Century be an Asian Century?” Asian Profile, 49(1):1-19, March.

Siddiqui, K. (2021b) “The Import Substitution Policy in the Post-Colonial Countries”, World Financial Review, November-December, p. 76-84.

Siddiqui, K. (2021c). “The Political Economy of Industrial Policy”, World Financial Review, May-June, p. 58-66.

Siddiqui, K. (2021d) “The Importance of Industrialisation in Developing Countries”, World Financial Review, January February, 60-73.

Siddiqui, K. (2022). “Capitalism, Imperialism, and Crisis”, European Financial Review, June/July, p.16-32.

Stiglitz, Joseph (2003) “The ruin of Russia”, Guardian, 9 April, London.

Stiglitz, Joseph (2015) “The Chinese Century”, Vanity Faire, January, p. 38-42.

Taylor, I. & Cheng, Z. (2022) “China as a ‘rising power’: why the status quo matters”, Third World Quarterly, 43 (1):244-58.

The Economist. (2020) “Is Wall Street Winning in China?” 3 September, London.

Wallerstein, I. (1983) “The three instances of hegemony in the history of the capitalist world economy”, International Journal of Comparative Sociology, 24(1-2): 100-8.

Walt, Stephen M. (2018) “US Grand strategy after the Cold War: Can realism explain it? Should realism guide it?” International Relations, 32(1): 3–22.

Wolf, M. (2018) “The US must avoid a new cold war with China”, Financial Times, 30 October, London.

Yao, Y. (2021) “The New Cold War: America’s new approach to Sino-American relations”, China International Strategy Review, 3:320-33. World Bank (2016) Russian Economic Report, 3 March, Washington DC, World Bank.

Bingo, a game cherished for its simplicity and cherished for the sense of community it fosters, is not just about matching numbers on cards – it’s a world rich with its own vocabulary, a symphony of terms that seasoned players wield with ease.

Whether you’re a newcomer looking to dive into the world of bingo or a seasoned player seeking to brush up on your linguistic prowess, this guide will be your companion in navigating the colorful lexicon that accompanies this beloved pastime. From the iconic call-outs that prompt exuberant shouts of “Bingo!” to the jargon that’s woven into the fabric of bingo culture, we’ll explore it all, ensuring you’re not left feeling like you’re in the dark on bingo night.

Whether you play at your neighborhood bingo hall, casino or play bingo online, and the game has its very own vocabulary or ‘lingo’ commonly used by players. Some terms may be familiar to you. Others, however, may be new; especially if you are new to playing online bingo or participating in the chat rooms. Below is a list of the most common terms used in bingo.

The most common terms used in bingo game

Admission Packet – The number of cards that a player must purchase before being able to play. Both physical bingo halls and those online will have admission packets.

Bingo Balls – Bingo balls come in a count of either 75 or 90 balls. These are drawn from the hopper at random.

Bingo Caller – The bingo caller acts as an announcer and referee for the game The bingo caller draws bingo balls randomly from the bingo hopper and calls them out to the players.

Cover All – An alternative name used for a blackout bingo game.

Daubers –Bottles filled with water-soluble ink which comes in several different colors. These are used to mark off called bingo numbers on bingo sheets. In online bingo, this is done virtually with a computer mouse or touch screen.

Early Bird- Also known as ‘warm up bingo’. Early bird games are 2 -10 games held before the official bingo games. They help players warm up and can ease new people into the game.

Free Space – the square located in the middle of each bingo card or sheet.

Game Pattern – Usually consisting of the five numbers in a row; up, down, across, or diagonal, Game patterns may make up other things such as shapes, an ‘X’, or four corners, for example

Late Bird – Also known as a ‘wrap up game’. Similar to early bird games, there are between 2 -10 bingo games after the regular bingo session.

Nite Owl – Both at the bingo hall and online, nite owl sessions are for hardcore bingo players.

Progressive Jackpot – A prize where the amount of money continues to grow until the final game.

Winner Takes All – Held after the main session where the winner receives all money raised in the sales of bingo sheets or cards for the game.

Bingo etiquette basics

The lingo used in bingo chatrooms is similar to that found in any chatroom, social media or texting on a phone. When in chat, there are just a couple of things to remember: First, be friendly! You can make new friends through online bingo. It is also important to remember, NO SHOUTING. Shouting is anytime someone types in all capital letters. Just as it’s considered rude to shout in the bingo hall, it’s not a good idea to shout in an online bingo chatroom.

Bingo lingo online shortenings

Below are some of the most common abbreviations which you may see and use while playing, no matter whether it’s an offline or online bingo game:

LOL – Laughing Out Loud

OMG – Oh My God

WD – Well Done

AFK – Away From the Keyboard

BRB – Be Right Back

BBL – Be Back Later

FYI – For Your Information

IMO – In My Opinion

TY – Thank You

NN – Nickname

GG – Good Game

GF – Good Fight

GJ – Good Job

GL – Good Luck

GLA – Good Luck All

BLNG – Better Luck Next Game

HB – Hurry Back

CA – Cover All

CH – Chat Host

TG – To Go – (how many are left)

SAC – Sorry A$$ Cards

BOGOF – Buy One Get One Free

F2P – Free to play

P2P – Pay to play

Final Thoughts

As you step into bingo halls or join online communities, armed with this newfound understanding of bingo lingo, you’re not just a player – you’re a participant in a time-honored tradition that transcends generations. The phrases, numbers, and call-outs are more than mere words. They’re the bonds that unite players in excitement and anticipation, turning each round into a unique and thrilling adventure.

Of course, it is just a small part of bingo therminology. Every site is different and you may find that there are different terms used where you play. The best way to learn the terms is to practice. If there are any terms you aren’t sure about, fellow players are often more than happy to explain them. After a few sessions, they’ll become second nature.

Let the lingo infuse your experience with a sense of camaraderie and shared tradition, turning each game into a delightful journey of numbers, words, and community.

When gambling online for real money, you need to make a deposit at the online casino or sportsbook. You can play some casino games for free as a demo but if you want the thrill of playing for real money, you must deposit funds at the online casino.

That means choosing a payment method from those available at your gambling website or app of choice. All payment methods offered by fully licensed online gambling sites come with their own security to keep your money safe but what can you do to increase your online payments security?

SSL Encryption

Checking for SSL encryption is perhaps the easiest security measure you can take when making payments online. If you look at the beginning of the website URL in the address bar of your internet browser, you should see a small padlock icon. You can click on the padlock icon and this will allow you to view the connection security. You will be able to see if the website has a valid certificate from a trusted authority. By having a valid certificate, it means any financial information sent to the website will be secure and cannot be intercepted. In many cases, the information is changed to a code and that code alone is no use to anyone.

Check Your Financial Statements

The best way to see if there has been any suspicious activity on your account having made a payment online, such as a gambling deposit, is to regularly check your financial statements.

It is possible to check bank statements online and many people now choose to do all their banking using a mobile application. You can quickly login to your financial accounts and view all the transactions from your account. You know where and when you have spent money and how much money you have spent when paying for entertainment online. If there is a payment you do not recognize, you can immediately contact your bank and ask them to check the payment details. Usually, a bank will quickly recognize if there has been suspicious activity and will block the payment method being used until you confirm if the payment was made by you or if it was fraudulent. However, it is wise to take a few seconds out of each day to quickly check your financial statements.

Two-Factor Authentication

Two-factor authentication has become one of the best ways to protect accounts online. It does not matter if it is an email account, Amazon account, eBay account, or online gambling account, if you have the option to turn on two-factor authentication, you should aways use it.

The beauty of two-factor authentication is that if your password gets stolen and someone tries to login to your account, it will ask for a further form of authentication. This is usually a code that is sent to the mobile phone of the account holder. So, unless the hacker has both your password and mobile phone, which is highly unlikely, they will not gain access to your account. For those who like to gamble online, you could have an account with funds and you do not want a hacker entering your account and stealing the money. There are several mobile casinos available in NJ that have two-factor authentication and it is a great way to increase online payments security.

Never Use the Same Password

It is extremely tempting to use the same password for every online account you create. This is based solely on convenience because it is easier to remember just one password than it is to remember ten different passwords. However, if a criminal gets hold of your password for one account, they will immediately try and use it for all your other accounts and within a matter of minutes, they have access to multiple online accounts. Even when you have set up two-factor authentication, you should never reuse the same password because it only encourages hackers to keep trying to steal account information.

So, there are several things you can do to increase your online payments security. They are all straightforward and take only a matter of minutes to complete. Just one of them could be the difference between keeping your finances safe and having your details stolen.

Financial planning is both a science and an art. When choosing effective strategies for creating and preserving wealth, you’ve got to understand the numbers — not just the figures in your own family budget, but the vast amounts of data that provide a glimpse into where the overall economy is headed.

Beyond that, there’s a special skill that’s required, a certain type of intuition. After all, if numbers alone told the whole story, we could all turn our financial worries over to an algorithm. Not even leading-edge artificial intelligence has reached the point where it has made its creators perpetual winners in the stock market.

With that in mind, certified financial planners such as Canada’s Nathan Garries point to an iron law of physics to explain the road ahead for North American economic activity — the principle that every action has an equal and opposite reaction. According to the Edmonton-based wealth preservation professional, the progressive monetary tightening by central banks worldwide has and will continue to have significant effects that are being felt at both macro and micro levels.

When you make money more expensive, ultimately you reduce and restrict economic activity. Interest rates of auto loans go up, dissuading families from buying a new car. Interest rates of credit cards go up, taking a large chunk out of the discretionary power of the average family.

People buy less in general, and as a result manufacturers produce fewer goods and service industries such as restaurants employ fewer workers. Soon, every consumer begins to feel the effects of tighter monetary policy.

Most significantly, mortgage rates go up, which leaves housing units sitting on the market without many buyers willing to pay high rates. In the worst case, this may lead to a cratering of home prices, similar to what happened during the housing crisis of 2008 to 2009. In various markets in Canada and across the U.S., softening of housing demand and a dip in prices have already been seen, although prices have not dropped off the cliff in any major region.

“What this means for investors is that caution is warranted, but not timidity,” says Garries. “We all know the famous adage by Warren Buffet, ‘Be greedy when others are fearful, and fearful when others are greedy.’ I’d refine that a bit to say: ‘Be especially alert for opportunities when others are showing irrational levels of fear.’”

Right now, the trick is gauging whether greed or fear is ruling the day. There’s certainly a large segment of the market that remains on the sidelines, fearing a dramatic decline in equities may be on the horizon. Nonetheless, major indexes, including the Dow Jones Industrial Average and the NASDAQ, have been holding up well. It’s not exactly greed, but there does seem to be an element of euphoria involved, especially with some of the AI-centric stocks.

For optimists, there are statistics that suggest that even the interest rate environment is not as gloomy as some observers believe. For example, in Canada the key interest rate set by the Bank of Canada was much higher in the 1980s. Even in the early part of the twentieth century it was about 10 times higher than the current rate. Of course, many Canadians and Americans alike remember how difficult it was to buy a house or even find steady employment in 1981 or 1982.

“It’s the age-old quandary, is the glass half empty or half full?” notes Certified Financial Planner Nathan Garries. “And yet, sometimes there’s a third option, a much more practical choice. It may be that the glass is simply twice as big as it needs to be.”

In the dynamic and fast-paced world of startups, networking is not just a strategy but a lifeline, fueling growth, fostering innovation, and shaping success stories. The power of building connections within the startup community can never be underestimated, as it provides entrepreneurs with unique opportunities for learning, mentorship, partnership, and investment.

This article aims to explore the significance of networking in the startup community, illustrating how meaningful connections can ultimately lead to entrepreneurial success.

What is business networking, and how does it work?

Business networking is the process of connecting with other entrepreneurs, business owners, and professionals who can help you achieve your startup goals. It involves forming mutually beneficial relationships through social events, professional organizations, online platforms such as LinkedIn and Meetup.com, and traditional face-to-face meetings.

When done right, networking can be highly effective in opening up new pathways and connections that were previously inaccessible. Through these interactions, entrepreneurs can access industry knowledge, resources, and potential investors. Moreover, when you partner with leading digital marketing companies like EZ Rankings, they will help you improve your visibility so that your business can get more exposure in the digital world.

Types of business networking

Professional networking

This type of networking is all about making valuable connections with professionals who may be able to help you in the long term. This means attending events and trade shows, participating in online forums, or joining professional organizations such as chambers of commerce. Through these interactions, entrepreneurs can gain valuable industry knowledge, find mentors and potential customers, and, most importantly, build relationships that can help their businesses grow.

Social networking

Social networking events are more casual, informal entrepreneurs’ and business owners’ gatherings. These events focus less on making deals and more on building relationships. They usually involve networking over drinks or dinner, attending local classes, or joining startup-focus groups like Mentor Mob. Through these interactions, entrepreneurs can get to know each other’s business and build valuable relationships that may lead to future opportunities.

Online networking

Online networking is a growing trend that allows entrepreneurs to build virtual networks using social media, online forums, and other digital platforms. This type of networking enables entrepreneurs to reach out to industry contacts in faraway places or access valuable resources from around the world. Through these interactions, entrepreneurs can access the latest trends, gain insights into their customers’ behavior, and find new partners and potential customers.

Importance of networking events

No matter what type of networking entrepreneurs engage in, it’s essential to understand how powerful it can be for their businesses. By building relationships and gaining access to valuable resources, entrepreneurs can gain invaluable insights into their markets, increase visibility for their companies, and get the word out about the products or services the offer.

Additionally, entrepreneurs can use networking to find potential investors or partners and build relationships with customers, leading to more sales and repeat business.

Ultimately, the power of networking lies in its ability to bring people together and open up possibilities for collaboration that wouldn’t have been possible before. Whether through social events or online forums, entrepreneurs should take advantage of every opportunity to make meaningful connections with others in the startup community. It would be good to take their business to the next level.

Effective networking strategies for entrepreneurs

1. Understanding the Power of First Impressions

Your first impression can often get the one for future interactions with someone. As an entrepreneur, you must understand and leverage this concept. Dress appropriately, maintain contact and exhibit positive body language. These may seem like minute details, but they’re crucial in establishing a good rapport immediately. Remember, you never get a second chance to make a first impression.

2. Adopting a Value-Giving Mindset

Networking isn’t just about what you can gain from others. It’s also about what you bring to the table. Successful entrepreneurs understand the importance of offering value to their connections. This might be in knowledge, resources, or even introductions to other valuable contacts. A mindset focused on giving rather than receiving can help establish lasting, mutually beneficial relationships.

3. Leveraging Social Media Platforms

In our digital age, social media platforms have invaluable networking tools. LinkedIn, Twitter, Facebook, and Instagram, among others, offer numerous opportunities to connect with like-minded entrepreneurs, potential clients, and industry leaders. However, it’s not enough to create profiles on these platforms. Check the top social media marketing agencies in India for actively engage with your connections by sharing relevant content, commenting on their posts, and participating in discussions. Attending Networking Events and Conferences:

While online networking is crucial, don’t underestimate the power of face-to-face interactions. Attending networking events and conferences allows you to meet and interact with people in your industry. Prepare for these events by researching attendees and speakers. Have your elevator pitch ready, and ensure you follow up with the connections you make.

4. Practicing Active Listening

Effective networking isn’t just about talking; it’s also about listening. When conversing, make sure you’re not just waiting for your turn to speak. Show genuine interest in what others are saying. Ask insightful questions that demonstrate your understanding and interest in their ideas. This will not only help you learn more but will also make your connections feel valued and respected.

5. Mastering the Art of Follow-up

Networking doesn’t end when the conversation or event does. The most successful networkers understand the importance of follow-up. Send a thank-you note or email expressing gratitude for the person’s time. Refer to a highlight of the conversation to show that you were attentive and interested. Regularly touch base with your connections to keep the relationship alive.

6. Building a Personal Brand

Last but certainly not least, building a personal brand is a powerful networking strategy. Your brand is essentially how you market yourself to the world. It includes your values, skills, passions, and unique selling proposition. A solid personal brand can help you attract connections and opportunities that align with your entrepreneurial goals.

To summarize, networking in the startup community is all about connecting with others, practicing active listening, mastering the art of follow-up, and building a personal brand. These strategies can help you gain access to resources, knowledge, and new opportunities that can jumpstart your business success.

As global demand for sustainable energy solutions continues to grow, the demand for copper, a crucial component in many green technologies, has grown along with it. Importantly, this increase in demand for copper is taking place during a macro environment of relatively cheap valuations for mining companies, especially for those in the exploration and development stages.

Many industry observers now believe that the current M&A cycle is only beginning to gain momentum. With commodity prices driving an uptick in Free Cash Flow (FCF), there is a higher propensity for M&A activities, especially within the developer space which has been the largest laggard in the past year.

The Changing Face of M&A in the Mining Sector

Over the past five years, larger mining companies have predominantly been interested in Tier 1 assets, but now, a shift in focus is noticeable. Large mining companies are willing to consider any copper asset, especially those with potential operational synergies in unpopular jurisdictions.

Recent transactions reveal a striking departure from the no-premium mergers of 2020. Over the past two years, the median M&A premium is about 40%. Most of the larger miners appear to have fairly limited internal growth opportunities in ESG-friendly commodities, particularly in copper, which suggests that M&A will likely be a large part of the solution. Larger players are also signalling a new openness to investing in higher-risk jurisdictions given the dearth of quality opportunities elsewhere.

Solaris Resources (TSX:SLS) (OTCQB:SLSSF): A High-Grade Copper Machine

Solaris Resources, with a market capitalization of US$730 million, stands out in the exploration and development copper sector with its growing 1.5 billion-tonne copper project in southeastern Ecuador. The upcoming 43-101 resource update around year-end is expected to push the total tonnage towards 2.5 billion tonnes of copper.