Europe has world-renowned gambling meccas such as Monte Carlo, Deauville, and of course, London and Paris. Still, not much is known about Macau, despite it being the largest gambling market globally and the second home to some of the world’s biggest gambling brands, including The Venetian, MGM and Sands.

History of Macau and the development of the gambling industry

Macau is a Chinese Island and ex-Portuguese colony; it’s only 33 sq km and has a population of 682,300. It’s also a gambling heaven for Chinese and International tourists, with millions of players visiting the territory and spending billions yearly. Gambling has existed in Macau since the 16th century, but the current gambling regime has been present since 2001-02.

According to the Centre for Gaming Research, games of chance were first legalised by the colonial government of Macau in 1847. Later in the 1930s, the colonial government awarded the monopoly concession for operating all forms of sanctioned casino games, awarding it to the Hou Heng Company, with games of chance like baccarat making their first debut. In 1962 the government then awarded the monopoly to Sociedade de Turismo e Diversões de Macau (STDM), which would retain control of the market for 40 years until 2001/02, when the term expired.

In 1999, the status of Macau changed, and the territory’s sovereignty was ceded to China. Hence, it became a Special Administrative Region, using the one country, two systems policy, with gambling remaining legal in Macau but not in China. In 2001, the Chinese government broke the casino monopoly, splitting it between SJM (a subsidiary of STEM), Wynn Resorts, and a Galaxy Entertainment and Las Vegas Sands partnership (these were later allowed to divide).

Today, Macau has over 40 casinos regulated and licensed by the Gaming Inspection and Coordination Bureau of Macau. The tax rate for operators is 40%, and regulated gambling accounts for 80% of Macau’s total tax revenue. In terms of revenue, the Macau casino industry was thriving pre-pandemic, far outpacing Las Vegas in revenue and more than earning its title as the “Las Vegas of the East”. In 2019, despite having only one-tenth of the land space of Las Vegas, it generated 5.5 times the USA’s gambling capital pre-pandemic at $36billion vs Vegas’ $6.5billion.

Macau vs Monte Carlo

Rather than comparing Macau to Las Vegas, as is often the case, let’s turn to a more European example – Monte Carlo. Monte Carlo is a world-renowned gambling location; despite being smaller than Macau, with a land size of 0.28 square kilometres, it’s home to four casinos.

Gambling was legalised in 1856 when Monaco’s Prince Charles III granted permission for the city’s most popular casino, Casino De Monte Carlo, to be built, and it opened its doors in 1865. This casino is so iconic it has been the backdrop for 007 movies. Like Macau, Monte Carlo’s casino industry is driven by tourism, and it also draws high rollers, with players opting for Roulette over other games. Although slot games also account for a fair share of the revenue.

Monaco’s Casino Tourism Market is estimated at $4,282m in 2022, with a projected growth rate of 8.5% until 2032. In 2019, 365,000 tourists visited Monaco, compared to Macau’s 39 million, making Macau the larger gambling market both by visitors and spending.

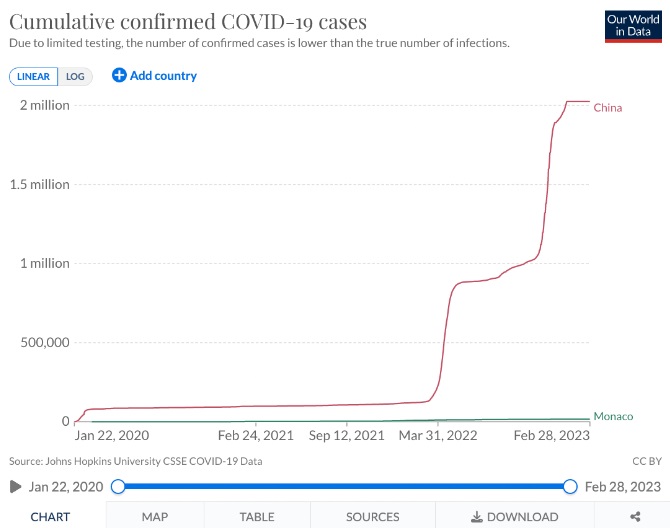

However, unlike Macau, Monte-Carlo’s industry was not affected similarly by COVID restrictions, as local lockdowns and border closures were shorter in duration. Additionally, the ongoing COVID situations in the two countries were vastly different (see the graph below), creating different attitudes and policies regarding sharing public spaces, like casino halls, contributing to differing speeds of industry recovery.

Macau’s gambling industry post-pandemic

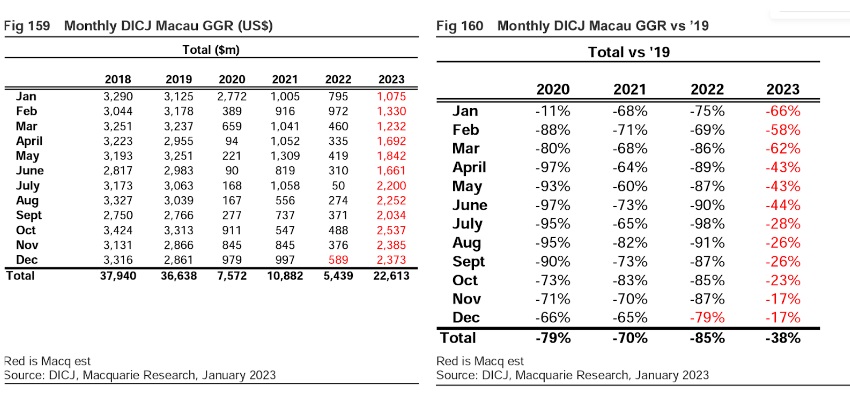

Since 2020, the casino industry has suffered dramatically in Macau. China’s zero COVID policy led to three years of continually bottoming-out revenue figures, from which Macau’s casinos are still recovering. Estimated revenue for this year is expected to be down as much as 38% on 2019’s figures, while 2022 was the worst year, with total revenue down 85%.

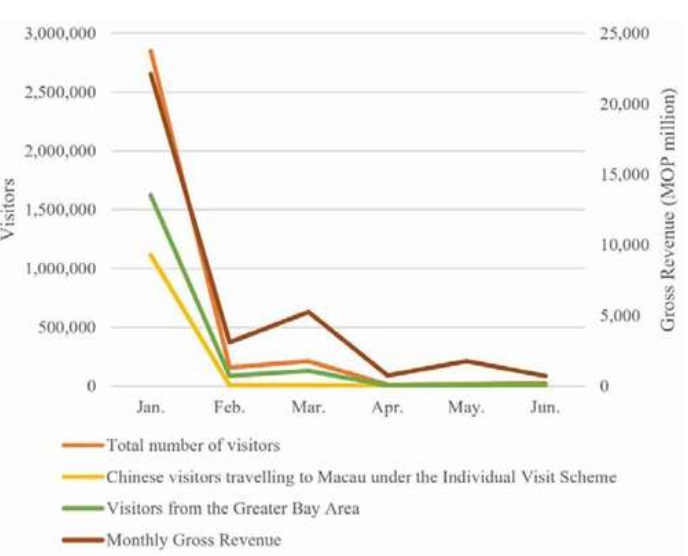

With the Chinese borders closed during pandemic restrictions, visitors to Macau plummeted from 39 million in 2019 to below 6 million for the following three years, with local operators describing it as “an empty shell of what it used to be”.

Source: https://www.tandfonline.com/doi/full/10.1080/1528008X.2021.1897920

Since the sudden u-turn on lockdowns and zero COVID policy in relation to nationwide protests from November to December 2022, Macau’s casinos began to benefit from returning customers and increased footfall. Still, at a far slower pace, as the return of consumers brought with it concerns over COVID spreading and the risk of mass infections. Three years of zero COVID policy, internal focus, and critical international media attention have damaged the country’s international reputation affecting the return of international casino tourism.

While the Macau industry is struggling to return to its former days, the Chinese government has also implemented new reforms that have halved the duration of casino licenses from 20 to 10 years and increased the tax rate from 39 to 40%, further hitting the newly recovering industry.

How does Macau relate to online gambling?

In other gambling jurisdictions, online gambling participation grew when COVID restrictions caused land-based gambling establishments to close. However, online casino is illegal across most of Asia and in China, and it’s unlikely that this will change anytime soon.

Like most areas where online gambling is illegal, the illegal market is present, and the lack of legal gaming doesn’t stop numerous offshore gambling sites from targeting and accepting Chinese players (even so, there are significant issues with payment processing and legal clampdowns).

While it’s more challenging to find data regarding online gambling in China due to its illicit nature, we can look at the Asian-Pacific region as a whole, which includes China, Japan, South Korea, Malaysia, Singapore, Vietnam and Cambodia. This region has been publicised as one of the fastest-growing gambling markets currently, with IMARC Group charting the size of the online gambling market in the region at $19.5bn in 2022 with a projected growth rate of 11.39% between 2023-2028.

Many Asian affiliates use social media platforms to refer players to offshore gambling operators, such as Weibo or WeChat (China’s most extensive social network) or messaging apps like Tencent/QQ. This contrasts with the operations of traditional gambling affiliates such as Slot Gods, where players are referred to operators licensed in the players’ home country. Secure referrals to licensed gambling sites ensure legitimacy in online gambling regimes as well as increased player safety. Sports advertising also plays a significant role in directing traffic, with Asian English Premier League sponsorship deals securing greater exposure for gambling brands when EPL games are aired in Asia.

Data on the types of games and revenue per game for the online casino industry servicing Chinese clientele is also not readily available. Extrapolating from land-based trends, gamblers in Macau tend to be high rollers who focus on table games, like baccarat and roulette, and VIP gamers account for 43% of revenue. This differs from European online gambling jurisdictions, where online slot games are the most popular type of casino game and generate the most revenue at around 42%.

A slower recovery?

Despite garnering less attention than Monte Carlo, Paris or London, Macau is still the largest casino gambling jurisdiction in the world. While COVID policies have depleted Macau’s gambling industry, there is hope, and it is expected to recover. Still, due to the Chinese government’s attempts to rain in the sector while diversifying the economy, as well as the territory’s reliance on tourism, it might not be as quick as gambling operators would like.

Disclaimer: This article contains sponsored marketing content. It is intended for promotional purposes and should not be considered as an endorsement or recommendation by our website. Readers are encouraged to conduct their own research and exercise their own judgment before making any decisions based on the information provided in this article.

{kind=link}