(1)")

Asia’s economic rise has reshaped global power dynamics, with profound implications for trade, development, and geopolitics. Dr Kalim Siddiqui analyses the region’s transformation, highlighting how strategic state intervention, industrialisation, and public investment have propelled growth. His study underscores Asia’s central role in shaping a more multipolar and economically diverse world.

I. Introduction

This article examines the rapid economic growth experienced in Asia in recent decades. While development has been uneven across the region, Asia as a whole has become increasingly prosperous, with its share of global output and trade rising sharply. This transformative shift warrants careful analysis due to its profound implications for global development and policy.

Within Asia, East Asia has demonstrated the most remarkable economic success. This achievement can be attributed to a combination of historical, institutional, and strategic factors. Notably, several East Asian countries experienced relatively short periods of Japanese colonial rule which, although often harsh, had different long-term consequences compared to European colonization. Despite national variations, several commonalities underpinned the region’s development: comprehensive land reforms, significant public investment in education and healthcare, a strong emphasis on industrialization, and a commitment to export-oriented economic strategies (Siddiqui, 2022; Glawe and Wagner, 2021).

Geopolitical dynamics also played a critical role. During the Cold War, particularly in the aftermath of the Korean and Vietnam wars, the US was determined to promote economic stability and development in East Asia as a bulwark against communism. This strategic interest led to preferential access to Western markets, inflows capital, and technologies. East Asian governments had built institutions and implemented policies that balanced market incentives with state-led planning. Over the past seven decades, this hybrid approach has resulted in industrialization, rising productivity, improved living standards, and higher income levels across the region (Asian Development Bank, 2020).

Meanwhile, other regions in Asia—particularly South Asia and Central Asia—are also showing signs of economic growth. Over the past decades, these regions have experienced steady growth in income, industrial output, and integration into global markets. In South Asia, India has emerged as a key driver of regional growth, supported by a large domestic market, a thriving service sector, and expanding technological capabilities. Bangladesh and Sri Lanka have also achieved notable progress, particularly in textiles and manufacturing (Bhattacharjee and Haldar, 2015).

In Central Asia, countries such as Kazakhstan and Uzbekistan have benefited from resource wealth—particularly oil, gas, and minerals—as well as increasing economic diversification and regional connectivity initiatives like China’s Belt and Road Initiative. These efforts have begun to reduce their historical dependence on commodity exports. Southeast Asia, too, deserves mention as a dynamic region contributing to Asia’s economic ascent. Countries like Vietnam, Indonesia, and the Philippines have seen rising foreign direct investment, exports, improving infrastructure, and growing manufacturing sectors, particularly in electronics, and consumer goods.

From antiquity until around 1820, China and India were the world’s two largest economies, measured by their share of global GDP. The dominance of the West—first Europe, then the United States (US) – emerged only in the past three centuries. In this historical perspective, the economic dominance of the West can be seen as a temporary divergence, or even an aberration, from a long-standing global norm. Like all historical aberrations, it is now coming to an end (Mahbubani, 2022).

The Western share of global output is gradually shrinking, while Asian countries have been catching up through rising productivity, industrialization, innovation, and investment. This shift coincides with stagnating real wages and rising income and wealth inequalities in many Western countries—particularly for the bottom 50% of the population—over the past four decades (Siddiqui, 2019).

The rise of Asian economies also coincides with the collapse of European colonial empires. Despite winning the Second World War, European powers emerged from the war economically and militarily weakened. They were increasingly unable to maintain control over their colonies and became heavily reliant on US financial assistance, particularly through the Marshall Plan.

However, this US led global order is rapidly declining and the resurgence of Asia is taking place, especially China and India (Siddiqui, 2025a). Technological advances and the growing interdependence of the global economy are accelerating this transition, making the influence of Asian economies increasingly central to the global order (Mahbubani, 2022).

The contemporary global order, though still largely shaped by Western institutions, has its roots in centuries of European and American dominance—established through colonial expansion, the transatlantic slave trade, and geopolitical control. The US, in many ways, represents a continuation of European influence, both politically and economically, as a settler-colonial society built by European migrants. Over the past five centuries, this Euro-Atlantic axis has held a dominant role in shaping global systems of power. That epoch, however, may now be giving way to a more multipolar world, with Asia at its core (Siddiqui, 2020).

The establishment of the Bretton Woods institutions—the International Monetary Fund (IMF) and the World Bank—further entrenched this asymmetrical global power structure. Although created with the stated goal of fostering global economic stability and development, these institutions have often reinforced patterns of dependency and underdevelopment, especially in the Global South. Financial assistance and development loans extended through the IMF and World Bank typically come with stringent conditionalities. These conditions frequently limit recipient countries’ economic sovereignty, compel the adoption of neoliberal reforms, prioritize debt repayment over social investment.

II. Industrialization: Lessons from the Experiences of Developed Economies

A historical comparison between the industrialization of the US and Germany in the 19th centuries reveals important policy measures undertaken such as state-led initiatives and public investment played a pivotal role in driving economic transformation. Significant investments were made in infrastructure, education systems, urban housing, and banks played important role in financing industrialisation – measures that not only modernized national economies but also helped to dismantle various forms of economic rent, particularly land rents and transport monopolies, which otherwise could have obstructed industrial expansion.

In Germany, for example, banks functioned less as instruments of speculative finance and more as facilitators of industrial development. Financial institutions were closely aligned with national economic goals, providing long-term capital for manufacturing and infrastructure projects. Similarly, in the US, federal and state governments took deliberate steps to make infrastructure widely accessible and affordable. Housing markets were also regulated to suppress excessive land speculation and ensure broad access to urban development opportunities. These interventions reduced overall economic overheads, thereby lowering production costs and enhancing global competitiveness. As a result of these developmental strategies, both Germany and the US were able to accumulate financial surpluses over time, positioning themselves as creditor nations and industrial leaders on the global stage.

III. China’s Path to Industrialization: State and Economic Transformation

China’s rapid industrialization and economic modernization over the past four decades has drawn widespread global attention. In less than two generations, the country transformed from a predominantly agrarian society into the world’s second-largest economy. This extraordinary transition was not the product of unregulated market liberalization, but rather the outcome of a strategically managed mixed economic model in which state and private sectors played mutually reinforcing roles. Crucially, the Chinese government retained control over key sectors—including banking, education, infrastructure, and communications—ensuring that essential services remained both accessible to the public and aligned with national development priorities (Siddiqui, 2025b).

A central pillar of China’s development strategy was the state’s decision to preserve sovereign control over money creation and the banking system. By keeping financial institutions largely within the public domain, the Chinese government curtailed the growth of a speculative, profit-driven domestic financial sector. Instead, credit and investment were channelled into productive areas such as housing, transportation, energy, and industrial infrastructure—projects that were delivered at low cost and often supported by public subsidies. This approach minimized production overheads and allowed Chinese industries to maintain competitive pricing in international markets (Siddiqui, 2025b).

China’s experience thus illustrates the effectiveness of a coordinated developmental state in achieving industrial modernization while avoiding some of the destabilizing effects associated with financial liberalization and speculative capital flows. It presents a compelling alternative to neoliberal economic orthodoxy and raises important questions about the role of state intervention in late-industrializing economies. In addition, sustained public investment in education and infrastructure has played a critical role in China’s economic transformation by fostering a skilled labour force and developing an efficient logistical network (Siddiqui, 2024a).

These developments underscore the broader importance of financial sovereignty and strategic public investment in driving industrial development. For many developing countries, capital outflows and the extraction of financial surpluses by advanced economies—often through mechanisms such as external debt servicing, capital flight, or profit repatriation—pose significant obstacles to sustainable growth. To mitigate these challenges, governments in the Global South must adopt policies that prioritize the retention, mobilization, and reinvestment of financial surpluses within their domestic economies. Redirecting financial resources toward domestic investment—particularly in education, research and development, and infrastructure—can substantially enhance productivity, and reduce production costs.

IV. Industrialization and Economic Growth

Rapid industrialization has played a pivotal role in enabling the export of higher-value commodities to global markets. The opportunities created by globalization, increased access to Western markets, and substantial inflows of foreign capital have collectively transformed many developing economies. Between 1970 and 2024, measured in current prices at market exchange rates, the share of industrialized countries in global GDP declined significantly—from 70% to 36%—while the share of developing countries rose sharply from 10% to 48%. Asia’s share alone increased from 4% to 44%, accounting for nearly the entire growth in the developing countries’ portion; by contrast, the combined shares of Latin America and Africa increased by less than two percentage points over the same period.

By 2024, Asian countries accounted for 35% of global income, 44% of world manufacturing output, and over one-third of global trade, with income per capita converging towards the global average. Asia now represents half of the world’s twenty fastest-growing economies, generates two-thirds of global economic growth, and contributes 44% of global GDP (IMF, 2025).

Table 1 presents the world’s largest economies and their shares of global GDP in 1995. At that time, the US held the top position, with a GDP of $7.6 trillion, accounting for 25.4% of global output. Of the ten largest economies, eight were developed nations. Only two—Brazil and China—were classified as developing countries, ranking sixth and eighth, respectively.

Nearly thirty years later, as shown in Table 2, the global economic landscape has shifted significantly. China surged from eighth to second place, and India entered the ranks of the world’s top ten economies (Siddiqui, 2018). The US remains a dominant economic power, contributing 24.1% of global GDP despite comprising just over 4.5% of the world’s population. Meanwhile, China’s economic rise has been striking: its GDP has grown to $17.78 trillion, representing 18.6% of global GDP—a substantial increase over the past three decades (see Table 2).

Over this period, Asia experienced a dramatic rise in industrial production and exports. The region underwent significant structural transformation, with a growing share of its workforce employed in industry and services. And proportion of manufactured goods in exports have also risen sharply. However, the growth in manufactured exports has not been evenly distributed across Asia’s sub-regions. From 1995 to 2024, Asia’s share of global exports increased by more than 22 percentage points. Of this growth, East Asia accounted for over three-quarters, while Southeast Asia, South Asia, and West Asia together contributed less than one-quarter.

Table 1: The World’s Largest Economies, Sized by GDP (1995)

| Rank | Country | GDP in US$ (1995) | Share of Global GDP |

| 1 | US | 7.6 trillion | 25.4% |

| 2 | Japan | 5.5 trillion | 17.7% |

| 3 | Germany | 2.6 trillion | 8.3% |

| 4 | France | 1.6 trillion | 5.1% |

| 5 | UK | 1.3 trillion | 4.3% |

| 6 | Italy | 1.2 trillion | 3.8% |

| 7 | Brazil | 778 billion | 2.5% |

| 8 | China | 734 billion | 2.4% |

| 9 | Spain | 615 billion | 2.0% |

| 10 | Canada | 606 billion | 1.9% |

Source: https://www.visualcapitalist.com/cp/the-worlds-largest-economies-1970-2020/

Table 2: The Top 10 Largest Economies in the World, Sized by GDP (2023)

| Rank | Country | GDP in US$ (2023) | Share of Global GDP |

| 1 | US | 26.95 trillion | 24.1% |

| 2 | China | 17.78 trillion | 18.6% |

| 3 | Germany | 4.43 trillion | 7.3% |

| 4 | Japan | 4.23 trillion | 5.1% |

| 5 | India | 3.73 trillion | 4.6% |

| 6 | UK | 3.33 trillion | 3.5% |

| 7 | France | 3.05 trillion | 2.5% |

| 8 | Italy | 2.19 trillion | 2.4% |

| 9 | Brazil | 2.13 trillion | 2.0% |

| 10 | Canada | 2.12 trillion | 1.9% |

Source: https://www.visualcapitalist.com/cp/the-worlds-largest-economies-1970-2020/

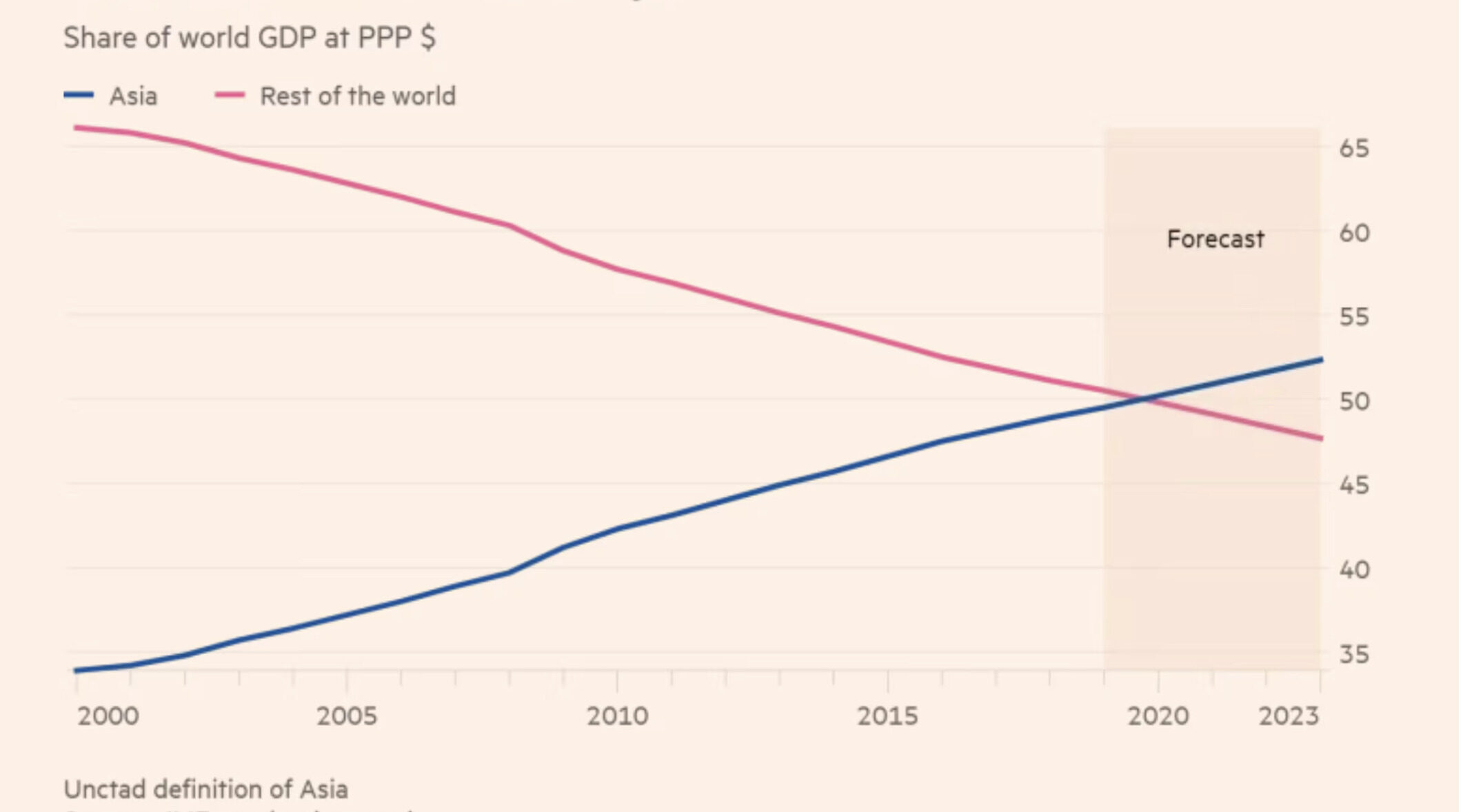

From a relatively modest share of global GDP in the early 2000s, Asian economies have surged ahead, accounting for more than half of global output (measured in PPP) by 2023. This dramatic rise marks a pivotal shift in the global economic landscape. The rapid economic ascent of Asia is unprecedented in modern history. In 2000, Asia’s contribution to global gross domestic product was relatively minor. However, driven by the economic dynamism of countries such as China, India, (Siddiqui, 2016) and the ASEAN nations, the region’s share of global output has grown significantly. By 2023, Asia accounted for over 50% of global GDP in PPP terms, outperforming other regions in both growth rates and aggregate output (Figure 1).

Projections to 2050 indicate that Asia will continue to expand its global economic presence. According to long-term forecasts by international institutions, Asia is expected to not only maintain but also strengthen its leadership in global output, innovation, and trade. This shift is often interpreted as a restoration of historical balance—a “return to normalcy” after a relatively brief period of Western dominance (IMF, 2025; Mahbubani, 2022).

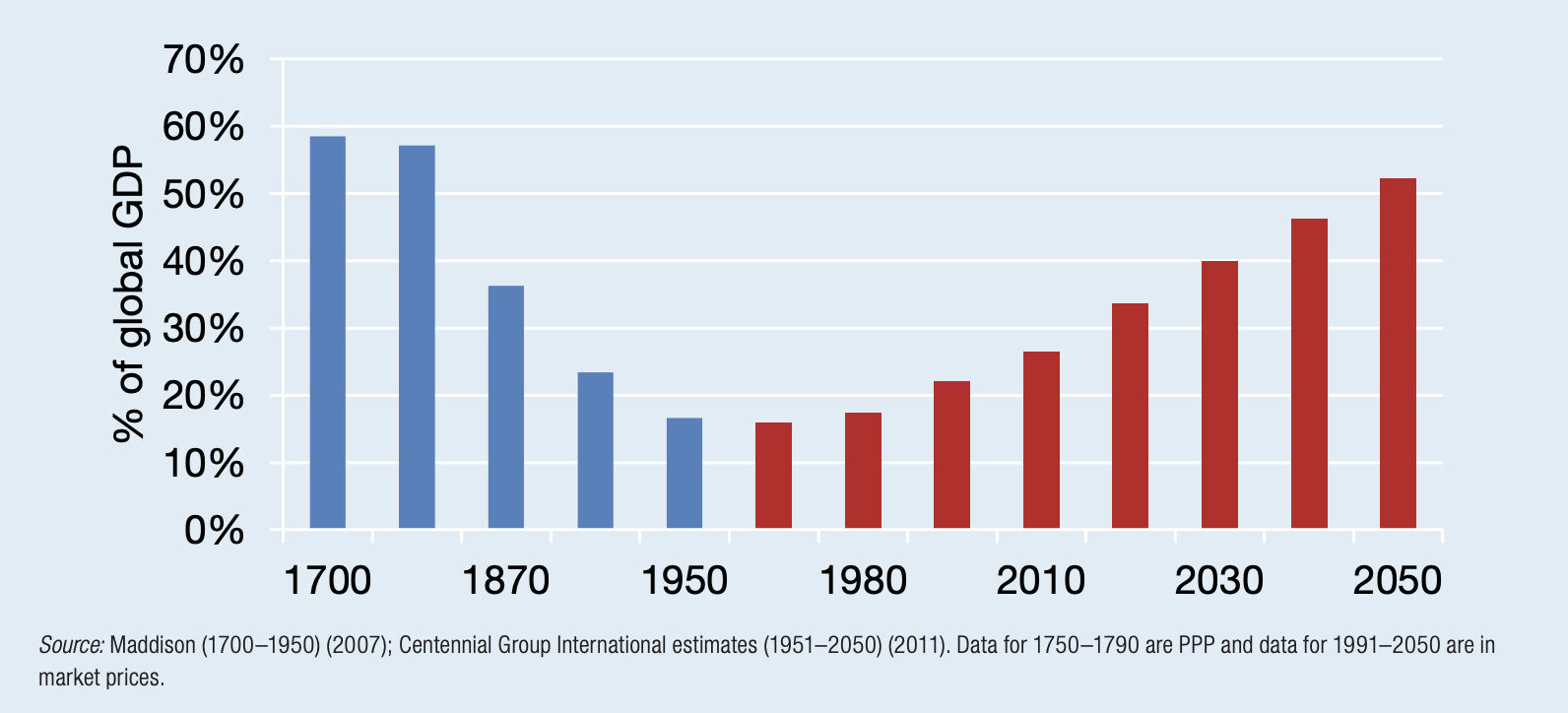

A historical perspective on Asia’s share of global gross domestic product (GDP) from 1700 to 2050 reveals that, prior to colonization, Asian economies—particularly those of China and India—dominated global output. Projections indicate that by 2050, Asia is poised to regain this leading position in the world economy, marking a restoration of its historical economic prominence (see Figure 2)

Figure 1: Share of World Gross Domestic Product (PPP, US$) from 2000 to 2023.

Figure 2: Asia’s Share of Global Gross Domestic Product, 1700-2050.

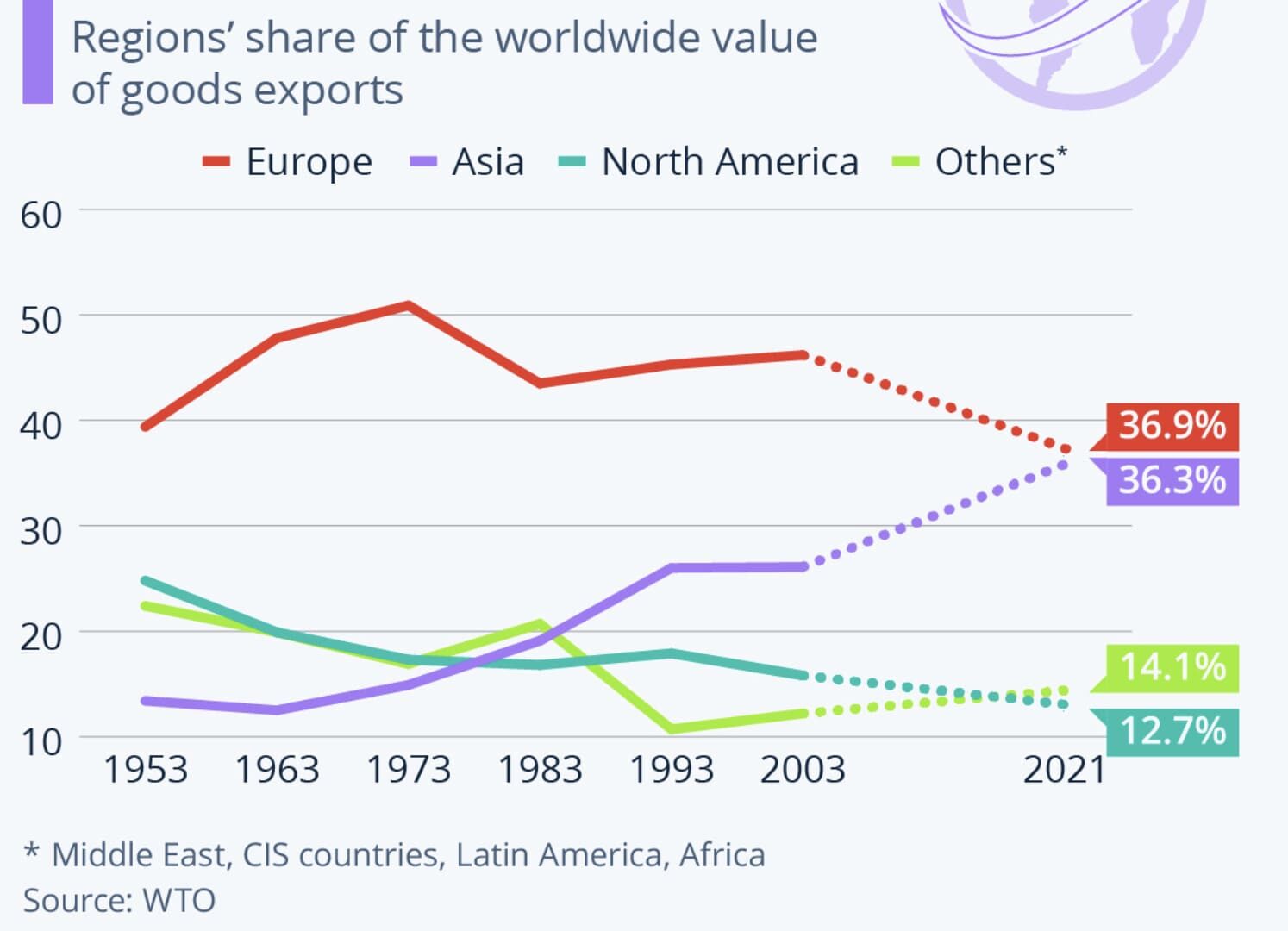

Figure 3: Share of Asian Exports of Goods to the Global Markets, 1953-2023.

Between 1970 and 2023, Asia’s share of global GDP, measured in constant 2010 US dollars, rose dramatically—from less than one-twelfth to over one-fourth, marking an increase of nearly 20 percentage points. However, growth in GDP per capita, relative to that of industrialized countries, increased at a much slower pace. This divergence highlights the uneven nature of Asia’s economic catch-up, both across and within countries. Nevertheless, the region experienced significant structural transformation: the share of the primary sector in Asia’s GDP declined from 27% to just 8%, reflecting a shift toward industry and services.

The recent rapid growth of South Asia is due to several factors including greater integration into the global economy, driven by trade liberalization, globalization, and accession to the World Trade Organization (WTO). Since the 1990s, countries such as India, Bangladesh, and Sri Lanka have pursued a range economic reforms aimed at attracting foreign capital, and encouraging exports. India’s accession to the WTO in 1995 marked a pivotal moment in its economic trajectory. The liberalization of trade and investment regimes enabled Indian firms to participate more actively in global value chains, particularly in high-growth sectors such as information technology (IT), pharmaceuticals, and automotive manufacturing. The rapid expansion of the IT and services sectors has since emerged as a major engine of GDP growth and urban employment, especially in cities such as Bengaluru, Hyderabad, and Chennai.

Similarly, Bangladesh has emerged as one of the world’s leading exporters of ready-made garments (RMG), leveraging its competitive labour costs, preferential trade access to Western markets, and targeted government support. The RMG sector has not only driven substantial export earnings but has also generated millions of jobs—particularly for women—thereby contributing to broader socio-economic development and poverty reduction. Additionally, remittances from overseas workers have played a crucial role in strengthening foreign exchange reserves and raising household incomes across South Asia (Sachs, 2009).

Moreover, South Asian economies have increasingly diversified their export portfolios to include higher-value goods and services. Investments in infrastructure, skills development, and digital connectivity have further enhanced their industrial capacities. These structural transformations have underpinned sustained economic growth, reductions in poverty, and gradual improvements in living standards throughout the region. While significant challenges remain—including income inequality, poor infrastructures, and environmental sustainability.

Historically, Asia’s socio-economic achievements have been remarkable. According to Maddison’s PPP statistics, Asia’s share of world GDP reached its lowest point of 14.9% in 1962, while its GDP per capita as a proportion of that in Western Europe and North America also hit a nadir of 9.2% in the same year. It is important to note that these proportions cannot be directly compared with income shares and levels expressed in current prices at market exchange rates, due to differences in valuation methods (Maddison, 2007).

The Maddison database, recently extended through 2016, estimates that Asia’s share of world GDP, measured in 1990 international (Geary–Khamis) dollars, stood at 43.1% in 2016—up from 36.1% in 1870 and 56.5% in 1820. Furthermore, GDP per capita in Asia as a proportion of that in Western Europe, North America, and Oceania was estimated at 26.4% in 2016, closely resembling the 26.6% recorded in 1870. These figures suggest that Asia’s share of global output has returned to levels last seen around the mid-19th century, while per capita income relative to industrialized countries has reverted to its 1870 benchmark (Maddison, 2007).

During the 1980s, the export-led growth model was widely promoted as the ideal development strategy for developing countries, inspired by the extraordinary economic performance of the Four East Asian Tigers—South Korea, Taiwan, Hong Kong, and Singapore. These economies demonstrated rapid growth rates significantly exceeding those of countries like India, which pursued more dirigiste, or state-led, development strategies. Consequently, international institutions such as the World Bank advocated for abandoning ‘inward-looking’ policies in favour of export orientation (Glawe and Wagner, 2021).

This neoliberal prescription gained further momentum in the aftermath of the foreign debt crisis of the 1990s, when many developing countries were compelled to adopt export-led growth strategies. However, the apparent success of export-led growth, particularly in China and Southeast Asia, is more nuanced than often portrayed. Much of this growth was facilitated by easy access to foreign capital, especially from the US, Japan, and multinational corporations that relocated labour-intensive industries to low-wage Asian countries to produce goods for Western markets (Siddiqui, 2012).

V. Asian Economic Transformation

Asia has emerged as a global economic powerhouse, with a rapidly increasing share of global output, manufacturing, and trade. Over the past several decades, many Asian economies have undergone significant structural transformations. Improvements in demographic, social, and economic indicators reflect this progress, and several countries in the region have successfully transitioned to high-income or industrialized status.

A key factor behind this transformation has been sustained public investment in education and healthcare, coupled with strategies focused on employment creation and export-oriented growth. While openness to trade, foreign investment, and technology transfer has been crucial, successful industrialization has often required the guidance of deliberate and adaptive industrial policies.

The region’s economic growth has been accompanied by a dramatic structural shift. In the 1960s, over two-thirds of Asia’s labour force was employed in subsistence agriculture. By 2024, more than 65% of workers were employed in the industrial and services sectors and Asia accounted for 30.7% of global merchandise exports, 29.3% of global imports, and attracted 35.9% of global inward foreign direct investment.

In the early postcolonial period, particularly in the 1960s, Asian exports were largely composed of agricultural and primary commodities, along with light manufacturing goods such as textiles and garments. Today, the region is widely recognized as production of high-tech goods, including automobiles, computers, smartphones, machine tools, and robotics. The region now boasts an electrification rate of over 90% and operates approximately 75% of the world’s high-speed rail network.

Exports of goods from Asia have risen sharply over the past several decades, reflecting the region’s deepening integration into the global economy. In 1953, Asia accounted for approximately 12% of global merchandise exports. By 2023, this share had increased to 36.3%, as shown in Figure 3. A major inflection point occurred around 2003, when many Asian economies—benefiting from WTO membership and greater access to global markets—accelerated their export-led growth strategies.

By 2023, Asia’s share of global exports slightly exceeded that of Europe, reaching 37% compared to Europe’s 36.9%. China, in particular, has played a pivotal role in this transformation. Since its accession to the WTO in 2001, China has emerged as the world’s leading manufacturing hub, with its share of global trade reaching nearly 16% by 2023. Intra-regional trade has also grown significantly (Siddiqui, 2023a). By 2023, approximately 58% of Asia’s trade occurred within the region, making it the second-most integrated trade bloc globally, after the European Union (Siddiqui, 2023b).

In terms of overall economic output, Asia’s share of global GDP (measured in PPP) reached approximately 55% in 2023—surpassing the combined share of Europe and North America. This growth has been driven primarily by the rapid expansion of China and India, but also supported by the performance of other emerging Asian economies. In 2023, Asia’s GDP was estimated at $41.36 trillion, making it the world’s largest economic region. China alone accounted for 19.2% of global GDP in 2024.

VI. Demographic Changes in Asia

The demographic transformation of Asia over the past seven decades has been profound. By 2023, Asia’s population had nearly tripled compared to its 1965 level, reflecting one of the most significant demographic expansions in modern history. This growth occurred alongside far-reaching social and economic transformations. Most notably, the region underwent a major demographic transition characterized by sharply declining birth and fertility rates, rising life expectancy, and improved education and health outcomes (Siddiqui, 2024b).

Fertility rates in Asia declined to roughly one-third of their 1965 levels, while birth rates fell by more than half. Life expectancy at birth rose dramatically, from 49 years in 1965 to 79 years in 2023. Infant mortality saw a striking decline—from 160 deaths per 1,000 live births to just 23. At the same time, literacy rates increased from 43% to 94%, underscoring major improvements in public education and healthcare systems. These gains were largely the result of sustained public investment in human capital, effective population policies, and broader economic modernization (Siddiqui, 2024c).

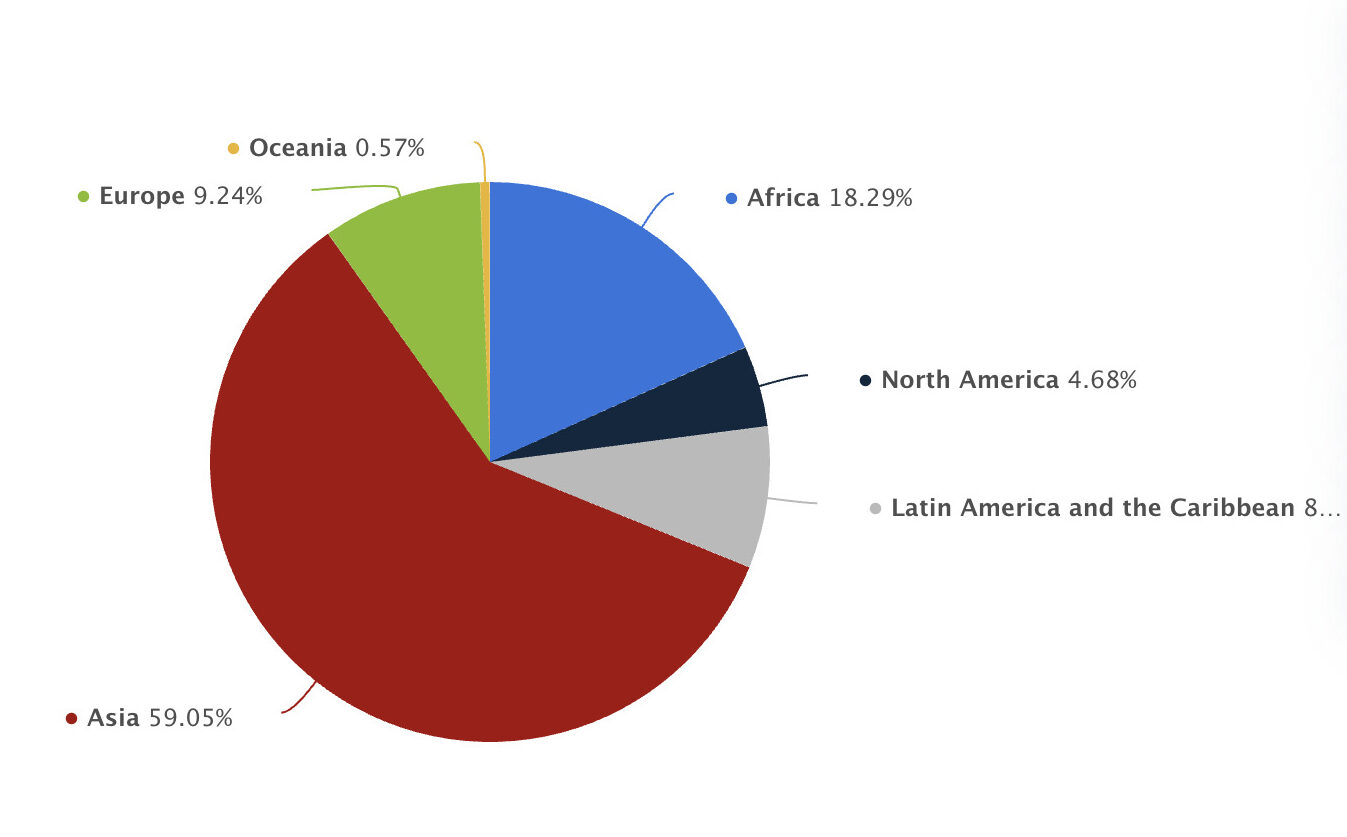

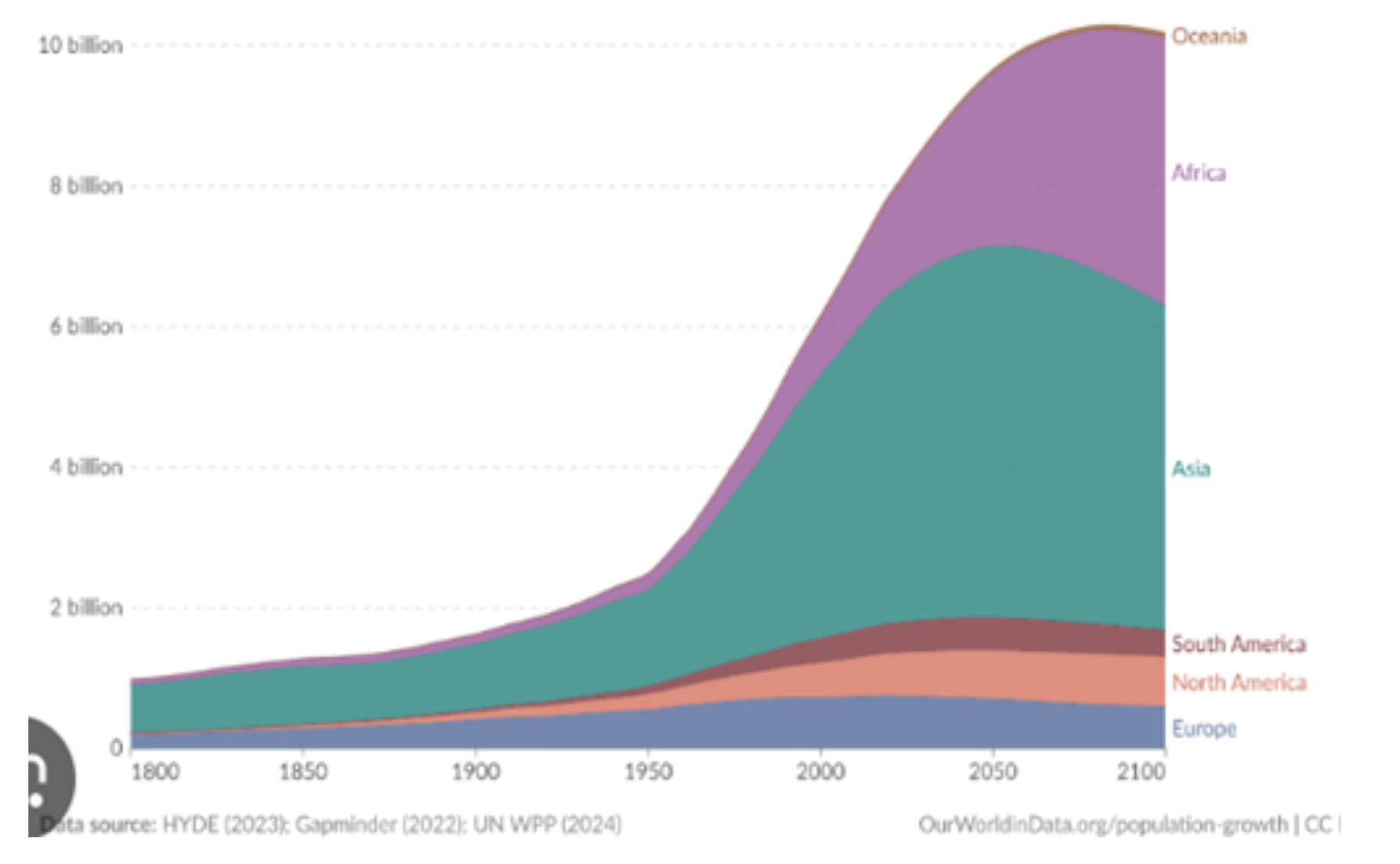

As of May 2025, Asia remains the most populous continent, home to approximately 4.8 billion people—or 58.8% of the world’s total population (see Figure 4). Over the past half-century, the region has experienced rapid population growth (see Figure 5), but this trajectory is expected to shift in the coming decades. By 2050, Asia’s population is projected to peak at around 5.3 billion, followed by a gradual decline in the second half of the century.

In contrast, Africa’s share of the global population is set to rise significantly. In 2024, Africa accounted for about 18% of the world’s population; by 2100, this figure is projected to reach 38%. Meanwhile, Asia’s relative share is expected to fall from nearly 60% today to approximately 45% by the end of the century. These shifts in global population distribution will have far-reaching implications for labour markets, economic development, migration patterns, and geopolitical dynamics.

Figure 4: Distribution of the Global Population by Continent, 2024.

Figure 5: Population by World Region, 1800-2100.

VII. Concluding Remarks

Over the past seven decades, Asia has undergone a remarkable economic transformation. From widespread poverty and post-colonial stagnation in the mid-20th century, the region has emerged as a global engine of growth, investment, trade, and innovation. Many Asian countries have successfully transitioned from agrarian economies to dynamic industrial and service-based systems, lifted hundreds of millions out of poverty, and significantly improved human development indicators (IMF, 2025).

This unprecedented success has been underpinned by strategic state intervention, investment in human capital, industrialization, and the pragmatic use of global integration to serve national development goals. The Asian experience demonstrates that rapid development in the Global South is possible—if supported by effective state institutions, active public investment, and inclusive economic strategies.

Looking ahead, building a resilient and equitable economy in the Global South requires reclaiming economic sovereignty from the constraints of neoliberal orthodoxy. This involves a more assertive role for the state—not only in regulating markets but also in driving public investment, expanding domestic demand, and addressing inequality. Key policy measures include increasing rural incomes through agricultural development, public investments in education, health, and infrastructure. Asia’s development trajectory offers not a singular model, but vital lessons: long-term planning, key role of the state, industrialisation and social inclusion are essential to achieving broad-based and sustainable growth.

About the Author

Dr. Kalim Siddiqui is an economist specializing in International Political Economy, Development Economics, Trade and Economic Policy. Since 1989, he has been teaching economics at various universities in Norway and the UK. Dr. Siddiqui’s research interests encompass a wide range of topics, including political economy, international trade, and economic history, South Asia, and emerging economies. He has presented papers at international conferences across numerous countries, reflecting his global engagement in the field. His scholarly pursuits span six broad domains: Political Economy, Development Economics, Economic History, Economic Policy, Globalization, and International Trade. Dr. Siddiqui has made significant contributions to research in areas such as trade policy, globalization, and political economy. His work has been published in chapters of edited books and articles published in peer-reviewed journals. For inquiries, Dr. Siddiqui can be reached at: [email protected]

Dr. Kalim Siddiqui is an economist specializing in International Political Economy, Development Economics, Trade and Economic Policy. Since 1989, he has been teaching economics at various universities in Norway and the UK. Dr. Siddiqui’s research interests encompass a wide range of topics, including political economy, international trade, and economic history, South Asia, and emerging economies. He has presented papers at international conferences across numerous countries, reflecting his global engagement in the field. His scholarly pursuits span six broad domains: Political Economy, Development Economics, Economic History, Economic Policy, Globalization, and International Trade. Dr. Siddiqui has made significant contributions to research in areas such as trade policy, globalization, and political economy. His work has been published in chapters of edited books and articles published in peer-reviewed journals. For inquiries, Dr. Siddiqui can be reached at: [email protected]

References

- Asian Development Bank (2020) 50 Years of Asian Development, Manila, Philippines.

- Bhattacharjee, J. and Haldar, S. (2015) “Economic Growth in South Asia: Binding Constraints for the Future” Journal of South Asian Development, 10(2).

- Glawe, L. and Wagner, H. (2021) The Economic Rise of East Asia – Development Paths of Japan, South Korea, and China, London: Springer.

- IMF (2025) World Economic Outlook, Washington DC: IMF.

- Maddison, A. (2007) Contours of the World Economy 1-2030 AD: Essays in Macro-Economic History. New York: Oxford University Press.

- Mahbubani, K. (2022) The Asian 21st Century, Springer: Singapore.

- Sachs J. (2009) South Asia story of development: Opportunities and risks. In Ghani E., Ahmed S. (Eds), Accelerating growth and job creation in South Asia (pp. 42–49). New Delhi: Oxford University Press

- Siddiqui, K., (2025a) “Indian Economy at 75: Transformation and Challenges”, American Review of Political Economy 19(1).

- Siddiqui, K. (2025b) “Understanding the Rise of High Technology in China” World Financial Review, April.

- Siddiqui, K. (2024a) “China’s Growth Miracle and Development Strategy Since the 1980s”, World Financial Review, December.

- Siddiqui, K. (2024b) “Impact of Population Changes and Economic Growth in China and India” World Financial Review, November.

- Siddiqui, K. (2024c) “The BRICS Expansion and the End of Western Economic and Geopolitical Dominance” World Financial Review, November.

- Siddiqui, K. (2023a) “Developmental Challenges: Export vs Import-Substitution in Industrialisation in Developing Countries” World Financial Review, October-November.

- Siddiqui, K. (2023b) “The Political Economy of Shanghai Cooperation Organisation (SCO) and the Growing Regional Multilateral Ties” World Financial Review, February-March.

- Siddiqui, K. (2022) “Comparing the Economic Performance of East Asian and Latin American Countries: The Role of Agricultural Reforms in the Economic Transformation” World Financial Review, July-August.

- Siddiqui, K. (2020) “Prospects of a Multipolar World and the Role of Emerging Economies” World Financial Review, November-December.

- Siddiqui, K. (2019) “The Political Economy of Global Inequality: An Economic Historical Perspective” Argumenta Oeconomica Cracoviensia 21(2):11 – 42.

- Siddiqui, K. (2018). “The Political Economy of India’s Economic Changes since the last Century” Argumenta Oeconomica Cracoviensia 19: 103 – 132.

- Siddiqui, K. (2016) “Will the Growth of the BRICs Cause a Shift in the Global Balance of Economic Power in the 21st Century?” International Journal of Political Economy 45(4): 315 – 338.

- Siddiqui, K. (2012) “Malaysia’s Socio-Economic Transformation in Historical Perspective”, International Journal of Business and General Management 1(2):1-50.

{kind=link}