A federal judge has ruled that the Trump administration violated the law by deploying California’s National Guard to Los Angeles without the state’s approval, siding with Governor Gavin Newsom in a high-profile legal battle over executive authority.

U.S. District Judge Charles Breyer issued the decision Thursday, declaring that former President Donald Trump acted unlawfully by bypassing the governor’s consent. The order mandates a return of control to California, though it will not take effect until Friday afternoon to allow time for the administration’s appeal, which was filed immediately.

“His actions were illegal,” Breyer wrote in his opinion, adding that Trump must “return control of the California National Guard to the Governor… forthwith.”

The dispute centers on Trump’s decision to send more than 4,000 National Guard troops and 700 Marines to Los Angeles amid large-scale protests against his immigration policies. The administration said the deployment was necessary to maintain public order and protect federal immigration agents. However, state officials argued the protests, while disruptive at times, did not warrant federal military involvement.

Governor Newsom welcomed the ruling, stating on social media, “The court just confirmed what we all know — the military belongs on the battlefield, not on our city streets.”

In court, Justice Department attorney Brett Shumate argued that the president had the authority to act without Newsom’s consent, stating, “There is one commander-in-chief of the U.S. armed forces.” Judge Breyer disagreed, noting constitutional limits on presidential power.

“The president isn’t the commander-in-chief of the National Guard,” he said, emphasizing the separation of powers outlined in the Constitution.

This is the first time in over half a century that a president has deployed the Guard without a governor’s approval, recalling tactics last used during the civil rights movement.

California’s lawsuit argued that the conditions in Los Angeles did not meet the threshold of “rebellion” required under the law used by the administration. Over the course of the protests, authorities recorded more than 300 arrests and the closure of major roads but said the unrest remained manageable.

As the legal fight continues, the case raises broader questions about presidential authority, states’ rights, and the role of the military in domestic affairs.

President Donald Trump is drawing sharp criticism after suggesting he may deploy American troops across the country to support immigration crackdowns, casting unrest in Los Angeles as a national threat requiring military intervention.

In a fiery speech at Fort Bragg, North Carolina, Trump framed parts of Los Angeles as being under siege from gangs and criminal groups. He vowed to “liberate” the city, warning that similar actions could be taken in other areas, especially those led by Democratic governors.

“We’re not going to wait for a governor to call,” Trump said. “We’ll act where there’s chaos.”

His remarks followed a series of escalations, including the deployment of National Guard units and 700 active-duty Marines to Los Angeles. The move came despite objections from California Governor Gavin Newsom, who accused the president of undermining democracy and overstepping constitutional limits.

“Democracy is under assault before our eyes,” Newsom said in a televised address. “There are no longer any checks and balances.”

The administration has leaned heavily into a narrative of domestic disorder, portraying immigration protests and localized unrest as justification for potential military action under the Insurrection Act. Critics argue this amounts to political theater aimed at rallying Trump’s base ahead of the election, rather than a necessary response to public safety threats.

At Fort Bragg, Trump linked immigration enforcement to national security, invoking imagery more often used in foreign combat. “We will use every asset at our disposal to restore order,” he declared. “We’re going to have troops everywhere.”

California’s senators, Adam Schiff and Alex Padilla, condemned the troop deployments in a letter to the Pentagon, calling them “unjustifiable.” Senator Susan Collins of Maine also raised concerns, stressing that active-duty forces are not typically used for domestic policing.

While protests in Los Angeles have included instances of vandalism and clashes with law enforcement, local officials maintain the unrest has been largely contained. Mayor Karen Bass said the city may be serving as a “test case” for wider federal action.

The Department of Homeland Security confirmed a memo from Secretary Kristi Noem requesting military assistance for arrests, though officials later clarified it was written before discussions with Trump.

For now, active-duty troops remain limited to guarding federal buildings, though the Defense Department disclosed the operation is already costing $134 million.

As Trump ramps up rhetoric and pressure, concerns grow that this latest strategy echoes authoritarian tactics — using the language of security to justify domestic crackdowns. Still, many of his supporters see it as fulfilling promises of strength and order.

“The only flag that will wave triumphant over the streets of Los Angeles is the American flag,” Trump told troops. “So help me God.”

As the West Bank is being annexed to Israel through blood and violence, many Israeli and international businesses and financials are tacitly supporting the ethnic cleansing with their business operations in the Israeli-occupied Palestinian territories.

Recently, The Norwegian parliament rejected efforts to tighten rules on its huge sovereign wealth fund investing in companies operating in the West Bank. Despite Norway’s central role in the initiation of the two-state peace process in the 1990s, the Norwegians lawmakers voted by 88 to 16 against a proposal that would have ordered the fund to withdraw from companies “that contribute to Israel’s war crimes and the illegal occupation” of the West Bank.

Fueled by vast revenue from Norway’s abundant oil and gas exports, Norway’s sovereign wealth fund is the biggest in the world and has some $1.8 trillion invested around the globe. Its precedence-setting example matters, especially as it prides itself over the fact that many companies are excluded from its portfolios “on ethical grounds.”

Why then the vote for continued war crimes, illegal occupation and ethnic cleansing?

Double standards

According to its ethical guidelines, the Fund cannot invest money in companies that directly or indirectly contribute to killing, torture, deprivation of freedom or other violations of human rights in conflict situations or wars. But in practice, the fund is allowed to invest in a number of arms-producing companies, as only some kind of weapons, such as nuclear arms, are banned by the ethical guidelines as investment objects.

The fund is allowed to invest in a number of arms-producing companies, as only some kind of weapons, such as nuclear arms, are banned by the ethical guidelines as investment objects.

In the past two decades, the Fund has excluded some Israeli companies, but in a highly restrictive manner, including Elbit Systems (Sep. 2009), due to supply of surveillance systems for the Israeli West Bank barrier; Africa Israel Investments and Danya Cebus (Aug. 2010), and Shikun Uvinui (Jun. 2012), due to violation of international humanitarian law in occupied Palestinian territory by being involved in developing settlements.

Such exclusions create an impression of token concern because there are dozens and dozens of both Israeli and international companies operating in the West Bank, even as its Palestinian residents are under constant threat of violence and ethnic cleansing.

In Norway, the government was under pressure to use its financial clout to influence Israel’s policies in Gaza and the West Bank, where its settlement policy has long been deemed illegal under international law. Some 50 Norwegian NGOs, spearheaded by the country’s main union, called on the Labor government to ensure that the fund’s investments were in line with the country’s legal obligations.

Meanwhile, UN special rapporteur on the Palestinian territories, Francesca Albanese, urged Oslo to “fully and unconditionally divest from all entities linked to Israel’s unlawful presence in the occupied Palestinian territory.” In his reply of May 30, Norway’s finance minister Jens Stoltenberg said the Norwegian government was deeply concerned by developments in Palestine, both in Gaza and in the West Bank. Then he proceeded to defend the “legality” of the Fund’s controversial investments in the Israeli-occupied Palestinian territories. Stoltenberg is the former chief of NATO.

Business operations in the West Bank

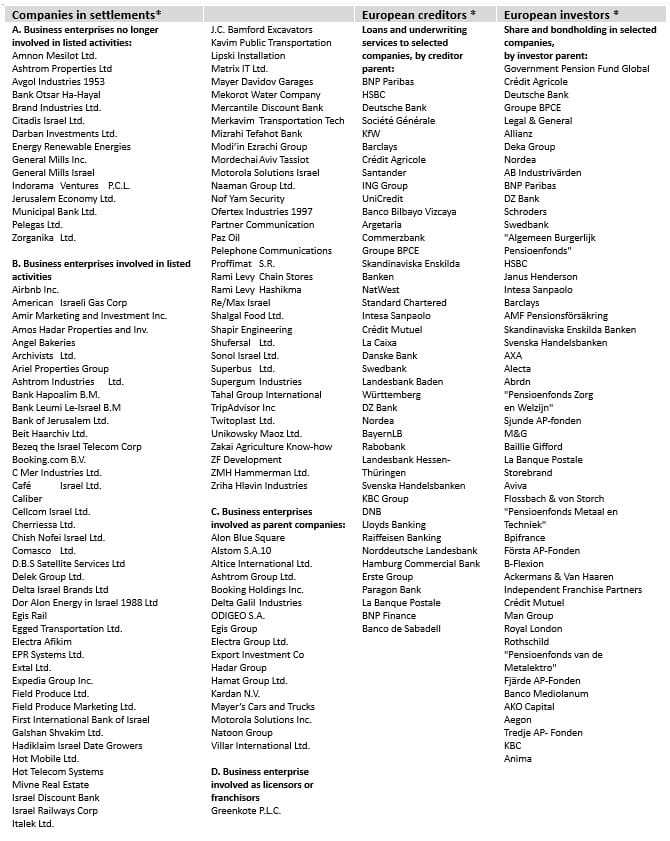

Since the late 2010s, the UN Human Rights Office of the High Commissioner (OHCHR) has used independent international fact-finding missions to investigate the implications of the Israeli settlements on the civil, political, economic, social and cultural rights of the Palestinian people throughout the occupied territories, including East Jerusalem. These reports do not cover all companies operating in the occupied territories. However, they do include the major ones that play the most critical roles (see Table).

Table: Israeli and International Companies in the Occupied Territories

* OHCHR update, UN Human Rights Office of the Commissioner, June 30, 2023. ** European Financial Institutions’ Continued Complicity in the Illegal Israeli Settlement Enterprise, Don’t Buy into Occupation, Dec., 2023.

The overwhelming majority of these firms are headquartered in Israel. There are more than 110 such companies. Since the first OHCHR report in 2020, some are no longer involved in the listed activities, such as General Mills and its Israeli subsidiary, which likely divested following a campaign to get the company to stop manufacturing its Pillsbury products on stolen Palestinian land. In addition to a broad variety of Israeli companies making money on the illicit territories, several international companies prevail in these areas, including Airbnb and Expedia (U.S.), Booking.com and Tahal Group (Netherlands), J.C. Bamford Excavators and Opodo (UK).

Still others operate through their parent organizations, including Motorola and Booking Holdings (U.S.), Egis (France), and Altice (Luxembourg), and licensors or franchisors, such as Greenkote (UK).

European financial institutions behind settler expansion

According to Don’t Buy into Occupation (DBIO), a coalition of 25 Palestinian, regional and European organizations, in the early 2020s almost 800 European financial institutions, including banks, asset managers, insurance companies, and pension funds, had financial relationships with more than 50 businesses that were actively involved with Israeli settlements.

All of these companies were involved in activities that raise particular human rights concerns, which constitute the basis for inclusion in the UN database of business enterprises.

The list had almost 40 major European creditors, including BNP Paribas, HSCBC and Barclays, and 50 European investors, including Crédit Agricole, Deutsche Bank and Allianz.

In addition to Israeli companies, defense contractors, financial institutions and universities that have been targeted in boycott and sanction campaigns for years, recent boycott efforts have increasingly centered on companies that play a critical role in the occupied territories, especially in the West Bank and East Jerusalem.

Under international law, Israeli settlements, their maintenance and expansion are illegal activities, which give rise to individual criminal liability as war crimes and crimes against humanity under the Rome Statute of the International Criminal Court. Israeli, European, and international business enterprises, operating with or providing services to Israeli settlements, play a critical role in the functioning, sustainability and expansion of illegal settlements.

Israelis for boycotts

In the past decade, the Israeli government has invested hundreds of millions of dollars in PR struggles against the international boycott movement. Though controversial, the latter has attracted some Israeli Jews. Despite different political motivations, they are united by the quest for peace and the view that international pressure is necessary to achieve change in Israel.

Despite different political motivations, they are united by the quest for peace and the view that international pressure is necessary to achieve change in Israel.

In 2012, Avraham Burg, the former chair of the Knesset and interim president of Israel, endorsed a boycott of Israeli settlement products. Personally, he boycotted all products produced in the settlements, refusing to cross the Green Line; that is, the pre-1967 borders. Such products were not “made in Israel” and should not be mislabeled that way. Colonizing Palestinian lands has made Israel “the last colonial occupier in the Western world.”

Burg’s views were echoed by Ha’aretz journalist Gideon Levy, who also supported boycotting Israel, stressing that it was “the Israeli patriot’s final refuge.” As far he was concerned, “the change won’t come from within.”

International boycotts are painful, but they cost less than human massacres and economic expenditures associated with forever wars. They are neither antisemitic nor anti-Israel. They target the occupation, the settlers and their allies in Israel and elsewhere, and their violence.

Yet, the likelihood that most Israelis would adopt Gideon Levy’s view of Israeli boycotts is currently minimal, thanks to the parallel universe created by decades of massive U.S. military aid and money flows by American Jewry to Israel.

If the status quo is untenable and change won’t come from within, then change can only come from without.

The original version was released by Informed Comment on June 11, 2025.

In the first 90 days of a new U.S. administration, one thing is certain: uncertainty. Markets react. Investors speculate. And political shifts, whether real or rumored, ripple through portfolios. For wealth managers and their clients, these early months are less about prediction and more about preparation.

According to Jeffrey Fratarcangeli, founder and managing principal of Fratarcangeli Wealth Management, the key to navigating this kind of economic environment isn’t timing the market, it’s building habits that outlast it.

“Be patient. Be prepared. And don’t overreact,” Jeffrey Fratarcangeli said. “That’s the formula. It’s not flashy, but it works.”

Here are four takeaways Jeffrey Fratarcangeli and his team are focusing on as markets adjust to a new presidential administration:

Volatility is Inevitable and Patience is Critical

Stock markets typically experience turbulence during administrative transitions, and this year is no exception. From foreign policy shifts to new regulations and trade uncertainty, early policy changes can spark emotional responses in the market.

“Every time a new administration comes in, there’s uncertainty, and the markets don’t like uncertainty,” Jeffrey Fratarcangeli said. “But you’ve got to remember, worst-case scenarios usually don’t play out the way people fear in the moment.”

That’s why his advice to clients hasn’t changed: stay patient. “You can’t make emotional decisions during a dip and expect long-term results,” he added. “Ride it out with a solid strategy.”

Liquidity Isn’t a Luxury, It’s a Requirement

One of the biggest vulnerabilities investors face during volatile periods? Lack of liquidity. Those who aren’t properly positioned may be forced to sell long-term investments at inopportune times just to cover short-term needs.

“If you don’t have cash on hand or an emergency buffer, you’re putting yourself in a bad spot,” Jeffrey Fratarcangeli said. “Markets can drop 15% in a matter of days, and if you need liquidity right then, you’re selling low.”

The lesson? Build an allocation strategy that includes enough short-term reserves to avoid panic selling, especially during times of political transition.

Disruption Creates Opportunity For The Disciplined

While the market often reacts harshly to early policy speculation, such as tariff changes or tax reforms, those reactions can also create opportunity. Valuations can dip well below fundamentals, offering long-term investors a chance to layer in.

“People assume the worst and price it in like it’s guaranteed. It rarely is,” said Jeffrey Fratarcangeli. “Let the market react. You stick to your strategy.”

That strategy, he says, might include dollar-cost averaging and periodic rebalancing, but always with a focus on long-term growth. “If you stay calm, stay intentional and follow a plan that’s built to weather volatility, you’re going to come out stronger,” he added.

Communication Builds Confidence

For wealth managers, the early days of a new administration are a crucial time to reinforce trust. The Fratarcangeli Wealth Management team has leaned into that by ramping up direct communication with their clients and internally, sharing regular market updates, making one-on-one calls, and scheduling daily team huddles to align messaging.

“We’re on the phones all day,” Jeffrey Fratarcangeli said. “Not because we’re chasing the news, but because clients want to know their plans still hold. And if you’ve done the work up front, it does.”

Frequent touchpoints, he says, are less about predicting policy outcomes and more about reinforcing strategy. “This is when people need leadership. You’ve got to show them you’re looking ahead — not reacting.”

Stay Prepared and Grounded

Transitions in Washington will always come with noise. But smart investors, and the advisors guiding them, know that success comes not from sidestepping disruption, but from staying grounded through it.

“You can either put your head in the sand, or you can use this moment to educate and strengthen habits,” said Jeffrey Fratarcangeli. “This administration, like the last, will bring change. But if your financial foundation is solid, you don’t have to flinch.”

Jeffrey Fratarcangeli regularly shares no-nonsense market updates that cut through the noise to offer a grounded perspective on what matters and what doesn’t. To follow his latest commentary, visit https://fratarcangeliwealth.com/videos/.

At Experian, where data forms the lifeblood of both consumer and business services, integrating generative AI was never a matter of following trends. It was a deliberate, strategic decision to amplify the value of one of the most significant consumer data sets on the planet. Shri Santhanam, Executive Vice President and General Manager of Platforms, Software, and AI at Experian, has been at the forefront of this transformation. In an era where the pace of innovation accelerates with breathtaking speed, Santhanam told me in our interview about how Experian crafted a structured, four-pronged approach to Gen AI integration: Products, Productivity, Platform and Governance, and Education and Adoption.

Experian seized the moment not with scattered pilots but with a clear-eyed, enterprise-wide strategy that positioned the company to move at scale rather than get trapped in endless proofs of concept

Their AI journey did not start with ChatGPT’s 2022 debut. Long before the world took notice, Experian’s innovation labs were already exploring advanced machine learning, transformers, and natural language applications. Yet, the public awakening to Gen AI’s potential marked a pivotal inflection point. Experian seized the moment not with scattered pilots but with a clear-eyed, enterprise-wide strategy that positioned the company to move at scale rather than get trapped in endless proofs of concept.

Products and Productivity: AI That Enhances Human Potential

On the product front, Experian focused sharply on creating tangible, high-impact outcomes for both its consumer and business segments. For consumers, the major breakthrough was a virtual assistant. Designed to offer personalized, sophisticated financial guidance, it moves beyond basic chatbot functionality. It mirrors the insights and professionalism of top-tier credit advisors, answering questions about credit scores and financial management with accuracy and nuance. Already interacting with 16 million consumers, this assistant is strengthening Experian’s mission to empower financial health at scale.

Meanwhile, on the B2B side, Experian’s leadership identified a persistent challenge: how to democratize access to their deep well of proprietary data expertise. The solution came in the form of a 24/7 digital data advisor, branded as the Experian Assistant. This agentic AI framework provides clients with on-demand insights that previously required direct interaction with top data scientists. Not only has it dramatically improved client engagement, but it has also earned multiple innovation awards, underscoring its transformative impact.

Productivity gains within the organization have also been substantial. Experian embedded Gen AI tools across engineering, customer service, and knowledge work teams, unleashing measurable efficiency improvements. Whether through code generation or customer query resolution, Experian’s approach to productivity is proving that AI is less about replacing workers and more about empowering them to focus on higher-value tasks.

Platform and Governance: Scaling with Trust

From the outset, Experian recognized that the rush to deploy Gen AI would expose companies to significant risks—ethical, regulatory, and reputational. Many organizations have found themselves mired in fragmented pilots, unable to cross the chasm to scaled, trusted applications. Experian avoided that fate by committing early to building a robust internal platform for AI services, coupled with rigorous governance structures.

A dedicated risk council reviews every AI use case against strict data privacy, compliance, and ethical standards. This system ensures that innovations align with Experian’s deeply entrenched values around responsible data stewardship. By creating this strong backbone, Experian has been able to confidently move AI initiatives from proof-of-concept to production, maintaining the integrity of its brand while capitalizing on the advantages of technological advancement.

Education and Adoption: Building a Grassroots Innovation Culture

No matter how powerful the platform or how sophisticated the product, without widespread adoption, AI initiatives stagnate. Recognizing this, Experian’s leadership made education and grassroots empowerment central pillars of its strategy. Rather than relegating Gen AI experimentation to a handful of experts, Experian launched organization-wide hackathons, established weekly AI seminars, and created interactive training agents to facilitate personalized upskilling.

No matter how powerful the platform or how sophisticated the product, without widespread adoption, AI initiatives stagnate.

This democratization of innovation is already bearing fruit. New ideas and applications are not only emerging from corporate leadership but also bubbling up from Experian’s 20,000 employees worldwide. The company’s internal forums and collaborative exercises have fostered a sense of shared ownership over AI’s future, helping to reduce anxieties about job displacement. As Santhanam emphasized, Experian’s core message to employees has been one of amplification, not replacement: AI is here to empower human creativity, not to eliminate it.

Measuring Success and Anticipating the Future

Experian’s disciplined approach to measuring ROI ensures that their Gen AI investments remain tightly aligned with strategic objectives. On the consumer side, metrics like the number of monthly active users, conversation volumes, and rising NPS scores reveal a strong trajectory of engagement and satisfaction. In the B2B space, the Experian Assistant is delivering tangible efficiency gains, cutting time spent on key tasks by as much as 75 percent in some cases.

Internally, productivity metrics, usage growth rates, and adoption rates among employees serve as KPIs that inform ongoing refinement. The company is not resting on early wins; it is continuously calibrating its programs to ensure sustained momentum.

Looking ahead, Santhanam envisions a future shaped by “trusted agents”—AI systems that not only perform complex tasks but also operate with transparency, ethics, and reliability. He predicts that while the last two decades were defined by how fast technology could move, the next phase will demand a new focus: ensuring that trust in AI keeps pace with its technical capabilities.

At Experian, the foundations for this future are already in place. With a four-pronged Gen AI strategy that balances ambition with responsibility, Experian stands as a model for how enterprises can harness the transformative power of AI—deliberately, thoughtfully, and with an unwavering commitment to both innovation and trust.

The United States and China have reached a tentative trade agreement following two days of negotiations in London, officials from both countries confirmed on Wednesday.

Chinese trade envoy Li Chenggang announced the development during a press briefing, saying both delegations had settled on a basic structure for enacting the consensus previously reached by President Donald Trump and Chinese leader Xi Jinping during recent discussions.

“This framework reflects the understanding achieved during the June 5 call and last month’s Geneva meetings,” Li stated, according to Chinese state broadcaster CGTN.

U.S. Commerce Secretary Howard Lutnick, speaking separately to reporters, said the framework would be presented to both President Trump and President Xi for final approval. “The idea is we’ll now consult our leaders. If they sign off, we’ll move forward with implementation,” Lutnick said, according to Reuters.

The agreement follows recent tensions sparked after an initially positive deal in Geneva. That May agreement had included a temporary reduction in tariffs for 90 days, but optimism quickly faded due to disputes over China’s export controls on rare earth materials and limits on its access to American semiconductor technology.

Lutnick confirmed that China’s restrictions on exporting rare earths and magnets to the U.S. would be addressed as a key part of the new framework. In turn, the U.S. may lift certain trade barriers it imposed in response to those limits. “You should expect those to come off,” Lutnick said, adding that any changes would be reciprocal, in line with President Trump’s guidance.

Both sides are expected to finalize the details pending approval from their respective heads of state.

Top officials from the United States and China have gathered in central London this week in a renewed attempt to resolve escalating trade tensions that have rattled global markets and threatened economic growth.

US Commerce Secretary Howard Lutnick and Treasury Secretary Scott Bessent are leading the American delegation at Lancaster House, where they are meeting Chinese Vice Premier He Lifeng and other senior officials. The discussions mark the most significant talks since a temporary truce was struck in May in Switzerland.

Central to the agenda are disputes over rare earth exports from China and American restrictions on advanced technology sales to Beijing. The US accuses China of delaying shipments of key minerals used in electronics and electric vehicles. In return, Beijing says Washington has unfairly limited access to semiconductors and software critical to artificial intelligence development.

The current standoff stems from earlier tariff battles that began when President Donald Trump introduced sweeping import duties. China retaliated, sparking tit-for-tat hikes that reached a peak of 145 percent. Although both sides agreed to lower tariffs temporarily, they now accuse each other of violating the terms of that agreement.

US National Economic Council Director Kevin Hassett said on Monday he expects a brief but productive round of talks. “We’re hopeful that once we shake hands, export controls will be eased and China will resume large-scale rare earth shipments,” he told CNBC.

Lutnick’s presence signals Washington’s serious stance on safeguarding high-tech industries. He has played a key role in crafting the current export restrictions. Meanwhile, fund manager Swetha Ramachandran told the BBC that rare earths remain a strong bargaining chip, given China’s control of nearly 70 percent of the global supply.

Trade Representative Jamieson Greer, also attending the London talks, criticized Beijing for not lifting restrictions on rare earth magnets. China, in turn, claims the US is blocking software sales and revoking student visas, undermining cooperation.

Beijing confirmed over the weekend that it had approved some export licenses for rare earth materials but provided few details.

Separately, Vice Premier He met UK Chancellor Rachel Reeves to discuss deeper economic collaboration. The meeting comes as China plans to build a new embassy near London’s financial center, a project that has raised US concerns over national security.

The stakes remain high. Without a deal by July 9, British steel exports to the US could face steep tariffs, and further disruption to global supply chains looms. Meanwhile, new trade data from China revealed weaker-than-expected exports and a significant drop in imports, reflecting mounting pressure on the world’s second-largest economy.

The Organization for Economic Co-operation and Development has lowered its global growth forecast to 2.9 percent, blaming rising protectionism and prolonged trade friction.

As negotiations continue behind closed doors, officials on both sides are under mounting pressure to strike a lasting deal before the truce expires.

By Marcelina Horrillo Husillos, Journalist and Correspondent at The World Financial Review

The Donald Trump administration stated that “using Huawei Ascend chips anywhere in the world violates US export controls.” The logic is that even if it’s a Chinese-made semiconductor, if it contains US technology, it is subject to US export regulations, a measure to prevent Chinese AI chips from expanding their presence in the global market.

The US Department of Commerce’s Bureau of Industry and Security (BIS) provided the industry with a notice containing this information, specifying Huawei Ascend 910B, 910C, and 910D series as chips with a high possibility of violating export control regulations. Recently, these have been widely used in China for AI training and inference and have been noted as alternatives to NVIDIA products.

Additionally, BIS plans to warn companies and consumers about the consequences when US AI chips are used for AI model training and inference in China. The plan is to block China’s strategy of indirectly securing advanced US AI chips through third countries.

Nvidia’s CEO Jensen Huang warned that export controls on its highest-end chips, as part of US government initiatives to restrict China’s access to AI technology that began under Joe Biden, could cost the company $50 billion.

This is probably the first time we have seen mention of the AI chips in official documents, and this shows how far Huawei has come with its Ascend AI lineup. It is revealed that the use of Ascend accelerators anywhere in the world will be considered a violation of US export control, which shows that the Trump administration doesn’t want these chips to end up anywhere apart from China, limiting their scope of influence.

Also, the use of US AI chips, particularly from NVIDIA, to train Chinese AI models will now be much more scrutinized. This could be done by integrating “tracking features” into NVIDIA chips to see where they end up. This is very much a possibility now, given that a bill to implement this is now with the US Senate, so it won’t be long before we see AI chips coming with location tracking features or even a kill switch.

NVIDIA Challenged Monopoly

Amazon unveiled its latest AI chips last month in a bid to reduce its dependence on market leader Nvidia and take a share of a multibillion-dollar market.

Central to this effort is the introduction of Trainium 2, Amazon’s newest chip built for training massive AI models. Amazon is hardly alone. A growing cohort of Big Tech companies are eager to challenge the commanding lead of Nvidia in designing cutting-edge AI chips.

Nvidia has been at the forefront when it comes to supplying chips that power large language models, such as the one used by OpenAI’s ChatGPT. Nvidia’s near monopoly has propelled the company’s valuation past $3.4 trillion, leaving competitors including AMD scrambling to close the gap.

In November, Nvidia reported an impressive 94 per cent annual revenue growth for the third quarter, reaching a record $35.1 billion. Questions remain, however: how long can Nvidia stay on top? And how can it do so? As Nvidia’s chief executive Jensen Huang stated: how can the company keep growing when it already has the largest market share of AI chips?

Some of Nvidia’s biggest customers, including Amazon, Microsoft and Google, are spending billions of dollars to build their own custom chips. In many ways, Big Tech’s push to unseat Nvidia is a familiar story: develop in-house hardware to reduce reliance on outside suppliers, cut costs and achieve tighter control over one’s own technology.

Butoverthrowing Nvidia is no small feat, even for these tech giants. They all rely on the same manufacturing partner: Taiwan Semiconductor Manufacturing Company (TSMC), the world’s largest chip manufacturer. Because TSMC produces chips for so many companies, no single rival gains a manufacturing edge over Nvidia. Furthermore, TSMC’s pricing structure favours those placing larger orders. Companies such as Nvidia benefit from lower per-unit costs, reinforcing an already sizeable advantage.

HUAWEI’s Towards Independence

China’s race for technological independence gains momentum as Huawei develops a new AI processor designed to challenge Nvidia’sdominance. Huawei is developing its own AI semiconductors to replace NVIDIA’s high-performance AI semiconductors. It is showing moves to solve all processes, including semiconductor design, production, and packaging, in China. Recently, satellite images of a semiconductor factory Huawei is building in Shenzhen were reported by the Financial Times (FT).

According to tech industry and company data, the performance of Huawei’s latest semiconductor ‘Ascend 910C’ has reached 60-80% of NVIDIA’s flagship product ‘H100.’ The price is 70-80% cheaper than the H100.

DeepSeek, a Chinese AI startup gaining attention in the global AI market, used low-spec NVIDIA semiconductors in the AI development process but used Huawei products in the AI service process.

It remains to be seen if big AI chip players will be affected by Huawei’s new launch. But if DeepSeek taught us anything, it is that any new platform can be disruptive, costly and may cause a shift in perception on US tech, the argument being it is possible to create something good for cheaper.

The launch of R1 DeepSeek AI updated model in January sent tech shares outside China plummeting and challenged the view that scaling AI requires vast computing power and investment. Since R1’s release, Chinese tech giants like Alibaba and Tencent have released models claiming to surpass DeepSeek’s.

US pushing for exports in the Middle East

Coinciding with President Trump’s Middle East tour, NVIDIA decided to supply 18,000 of its latest AI chips, the GB300 Blackwell, to Humane, a company owned by the Saudi sovereign wealth fund. It plans to supply hundreds of thousands of advanced chips over the next few years. These chips will be used in data centers being built by Saudi Arabia to foster AI.

Bloomberg reported that the Trump administration is pushing a deal to allow the United Arab Emirates (UAE) to import more than 1 million of NVIDIA’s advanced semiconductors. This is about four times more than what was allowed under the AI semiconductor export controls of the previous Joe Biden administration.

Unsurprisingly, Chinese experts characterize the United States’ Middle East policy under Trump as transactional and commercially driven, mostly in negative terms. More bluntly, Liu Zhongmin, professor at the Middle East Studies Institute of Shanghai International Studies University (SISU), characterized Trump’s visit as “a blatant money-making trip,” adding that:

“Trump aggressively leveraged the United States’ advantages to extract wealth from the Gulf states, even blatantly enriching himself and his family, a rare and overt display of greed rarely seen in previous U.S. presidents.”

The Trump administration is blocking Chinese AI chips while increasing exports of US AI chips. This aligns with what CEO Huang and other US big tech CEOs have recently said, that the US must supply more AI chips to the global market to win the AI competition with China.

On the other hand, the Founder of Huawei Technologies, Ren Zhengfei believes that AI is becoming unstoppable. It is creating turning points for many firms. If Huawei uses AI in the best ways, it could achieve more success in the time ahead. However, the company needs to put more effort into being at the top in the AI race.

Conclusion

Earlier this year DeepSeek upended beliefs that US export controls were holding back China’s AI advancements after the startup released AI models that were on a par with or better than industry-leading models in the United States at a fraction of the cost.

In the meantime, and as per the claimed performance of DeepSeek R1, Nvidia suffered the biggest one-day loss in sharemarket history, other tech giants – Microsoft, Alphabet and Amazon, who are investing heavily in competing AI tools including ChatGPT and Gemini – were also hit. Almost A$1 trillion (US$600 billion) was wiped off the value of artificial intelligence microchip maker Nvidia overnight, when a little-known Chinese startup, DeepSeek, threatened to upend the US tech market.

Stock prices are driven by market expectations. Investors have rapidly incorporated the news of a low-cost Chinese AI competitor into stock prices, anticipating this new entrant could disrupt the market and erode the competitive advantage of existing leaders.

An analogy can be found in the present situation between NVIDIA and Huawei Ascend chips, moreover the reliance that the first has on TSMC, reaffirms the US multinational vulnerability to navigate and seek fast sales in a highly competitive market.

Investors’ role – who are closely watching these vertiginous changes – is betting on the most advantageous and competitive deals taking place in the global market. NVIDIA’s tricky position is being globally exposed, while China tech advancements, which by all means, seem unstoppable, keep challenging the traditional US tech hegemony.

Asia’s economic rise has reshaped global power dynamics, with profound implications for trade, development, and geopolitics. Dr Kalim Siddiqui analyses the region’s transformation, highlighting how strategic state intervention, industrialisation, and public investment have propelled growth. His study underscores Asia’s central role in shaping a more multipolar and economically diverse world.

I. Introduction

This article examines the rapid economic growth experienced in Asia in recent decades. While development has been uneven across the region, Asia as a whole has become increasingly prosperous, with its share of global output and trade rising sharply. This transformative shift warrants careful analysis due to its profound implications for global development and policy.

While development has been uneven across the region, Asia as a whole has become increasingly prosperous, with its share of global output and trade rising sharply.

Within Asia, East Asia has demonstrated the most remarkable economic success. This achievement can be attributed to a combination of historical, institutional, and strategic factors. Notably, several East Asian countries experienced relatively short periods of Japanese colonial rule which, although often harsh, had different long-term consequences compared to European colonization. Despite national variations, several commonalities underpinned the region’s development: comprehensive land reforms, significant public investment in education and healthcare, a strong emphasis on industrialization, and a commitment to export-oriented economic strategies (Siddiqui, 2022; Glawe and Wagner, 2021).

Geopolitical dynamics also played a critical role. During the Cold War, particularly in the aftermath of the Korean and Vietnam wars, the US was determined to promote economic stability and development in East Asia as a bulwark against communism. This strategic interest led to preferential access to Western markets, inflows capital, and technologies. East Asian governments had built institutions and implemented policies that balanced market incentives with state-led planning. Over the past seven decades, this hybrid approach has resulted in industrialization, rising productivity, improved living standards, and higher income levels across the region (Asian Development Bank, 2020).

Meanwhile, other regions in Asia—particularly South Asia and Central Asia—are also showing signs of economic growth. Over the past decades, these regions have experienced steady growth in income, industrial output, and integration into global markets. In South Asia, India has emerged as a key driver of regional growth, supported by a large domestic market, a thriving service sector, and expanding technological capabilities. Bangladesh and Sri Lanka have also achieved notable progress, particularly in textiles and manufacturing (Bhattacharjee and Haldar, 2015).

In Central Asia, countries such as Kazakhstan and Uzbekistan have benefited from resource wealth—particularly oil, gas, and minerals—as well as increasing economic diversification and regional connectivity initiatives like China’s Belt and Road Initiative. These efforts have begun to reduce their historical dependence on commodity exports. Southeast Asia, too, deserves mention as a dynamic region contributing to Asia’s economic ascent. Countries like Vietnam, Indonesia, and the Philippines have seen rising foreign direct investment, exports, improving infrastructure, and growing manufacturing sectors, particularly in electronics, and consumer goods.

From antiquity until around 1820, China and India were the world’s two largest economies, measured by their share of global GDP. The dominance of the West—first Europe, then the United States (US) – emerged only in the past three centuries. In this historical perspective, the economic dominance of the West can be seen as a temporary divergence, or even an aberration, from a long-standing global norm. Like all historical aberrations, it is now coming to an end (Mahbubani, 2022).

The Western share of global output is gradually shrinking, while Asian countries have been catching up through rising productivity, industrialization, innovation, and investment. This shift coincides with stagnating real wages and rising income and wealth inequalities in many Western countries—particularly for the bottom 50% of the population—over the past four decades (Siddiqui, 2019).

The rise of Asian economies also coincides with the collapse of European colonial empires. Despite winning the Second World War, European powers emerged from the war economically and militarily weakened. They were increasingly unable to maintain control over their colonies and became heavily reliant on US financial assistance, particularly through the Marshall Plan.

However, this US led global order is rapidly declining and the resurgence of Asia is taking place, especially China and India (Siddiqui, 2025a). Technological advances and the growing interdependence of the global economy are accelerating this transition, making the influence of Asian economies increasingly central to the global order (Mahbubani, 2022).

The contemporary global order, though still largely shaped by Western institutions, has its roots in centuries of European and American dominance—established through colonial expansion, the transatlantic slave trade, and geopolitical control. The US, in many ways, represents a continuation of European influence, both politically and economically, as a settler-colonial society built by European migrants. Over the past five centuries, this Euro-Atlantic axis has held a dominant role in shaping global systems of power. That epoch, however, may now be giving way to a more multipolar world, with Asia at its core (Siddiqui, 2020).

The establishment of the Bretton Woods institutions—the International Monetary Fund (IMF) and the World Bank—further entrenched this asymmetrical global power structure. Although created with the stated goal of fostering global economic stability and development, these institutions have often reinforced patterns of dependency and underdevelopment, especially in the Global South. Financial assistance and development loans extended through the IMF and World Bank typically come with stringent conditionalities. These conditions frequently limit recipient countries’ economic sovereignty, compel the adoption of neoliberal reforms, prioritize debt repayment over social investment.

II. Industrialization: Lessons from the Experiences of Developed Economies

A historical comparison between the industrialization of the US and Germany in the 19th centuries reveals important policy measures undertaken such as state-led initiatives and public investment played a pivotal role in driving economic transformation. Significant investments were made in infrastructure, education systems, urban housing, and banks played important role in financing industrialisation – measures that not only modernized national economies but also helped to dismantle various forms of economic rent, particularly land rents and transport monopolies, which otherwise could have obstructed industrial expansion.

In Germany, for example, banks functioned less as instruments of speculative finance and more as facilitators of industrial development. Financial institutions were closely aligned with national economic goals, providing long-term capital for manufacturing and infrastructure projects. Similarly, in the US, federal and state governments took deliberate steps to make infrastructure widely accessible and affordable. Housing markets were also regulated to suppress excessive land speculation and ensure broad access to urban development opportunities. These interventions reduced overall economic overheads, thereby lowering production costs and enhancing global competitiveness. As a result of these developmental strategies, both Germany and the US were able to accumulate financial surpluses over time, positioning themselves as creditor nations and industrial leaders on the global stage.

III. China’s Path to Industrialization: State and Economic Transformation

China’s rapid industrialization and economic modernization over the past four decades has drawn widespread global attention. In less than two generations, the country transformed from a predominantly agrarian society into the world’s second-largest economy. This extraordinary transition was not the product of unregulated market liberalization, but rather the outcome of a strategically managed mixed economic model in which state and private sectors played mutually reinforcing roles. Crucially, the Chinese government retained control over key sectors—including banking, education, infrastructure, and communications—ensuring that essential services remained both accessible to the public and aligned with national development priorities (Siddiqui, 2025b).

By keeping financial institutions largely within the public domain, the Chinese government curtailed the growth of a speculative, profit-driven domestic financial sector.

A central pillar of China’s development strategy was the state’s decision to preserve sovereign control over money creation and the banking system. By keeping financial institutions largely within the public domain, the Chinese government curtailed the growth of a speculative, profit-driven domestic financial sector. Instead, credit and investment were channelled into productive areas such as housing, transportation, energy, and industrial infrastructure—projects that were delivered at low cost and often supported by public subsidies. This approach minimized production overheads and allowed Chinese industries to maintain competitive pricing in international markets (Siddiqui, 2025b).

China’s experience thus illustrates the effectiveness of a coordinated developmental state in achieving industrial modernization while avoiding some of the destabilizing effects associated with financial liberalization and speculative capital flows. It presents a compelling alternative to neoliberal economic orthodoxy and raises important questions about the role of state intervention in late-industrializing economies. In addition, sustained public investment in education and infrastructure has played a critical role in China’s economic transformation by fostering a skilled labour force and developing an efficient logistical network (Siddiqui, 2024a).

These developments underscore the broader importance of financial sovereignty and strategic public investment in driving industrial development. For many developing countries, capital outflows and the extraction of financial surpluses by advanced economies—often through mechanisms such as external debt servicing, capital flight, or profit repatriation—pose significant obstacles to sustainable growth. To mitigate these challenges, governments in the Global South must adopt policies that prioritize the retention, mobilization, and reinvestment of financial surpluses within their domestic economies. Redirecting financial resources toward domestic investment—particularly in education, research and development, and infrastructure—can substantially enhance productivity, and reduce production costs.

IV. Industrialization and Economic Growth

Rapid industrialization has played a pivotal role in enabling the export of higher-value commodities to global markets. The opportunities created by globalization, increased access to Western markets, and substantial inflows of foreign capital have collectively transformed many developing economies. Between 1970 and 2024, measured in current prices at market exchange rates, the share of industrialized countries in global GDP declined significantly—from 70% to 36%—while the share of developing countries rose sharply from 10% to 48%. Asia’s share alone increased from 4% to 44%, accounting for nearly the entire growth in the developing countries’ portion; by contrast, the combined shares of Latin America and Africa increased by less than two percentage points over the same period.

By 2024, Asian countries accounted for 35% of global income, 44% of world manufacturing output, and over one-third of global trade, with income per capita converging towards the global average. Asia now represents half of the world’s twenty fastest-growing economies, generates two-thirds of global economic growth, and contributes 44% of global GDP (IMF, 2025).

Table 1 presents the world’s largest economies and their shares of global GDP in 1995. At that time, the US held the top position, with a GDP of $7.6 trillion, accounting for 25.4% of global output. Of the ten largest economies, eight were developed nations. Only two—Brazil and China—were classified as developing countries, ranking sixth and eighth, respectively.

Nearly thirty years later, as shown in Table 2, the global economic landscape has shifted significantly. China surged from eighth to second place, and India entered the ranks of the world’s top ten economies (Siddiqui, 2018). The US remains a dominant economic power, contributing 24.1% of global GDP despite comprising just over 4.5% of the world’s population. Meanwhile, China’s economic rise has been striking: its GDP has grown to $17.78 trillion, representing 18.6% of global GDP—a substantial increase over the past three decades (see Table 2).

Over this period, Asia experienced a dramatic rise in industrial production and exports. The region underwent significant structural transformation, with a growing share of its workforce employed in industry and services. And proportion of manufactured goods in exports have also risen sharply. However, the growth in manufactured exports has not been evenly distributed across Asia’s sub-regions. From 1995 to 2024, Asia’s share of global exports increased by more than 22 percentage points. Of this growth, East Asia accounted for over three-quarters, while Southeast Asia, South Asia, and West Asia together contributed less than one-quarter.

Table 1: The World’s Largest Economies, Sized by GDP (1995)

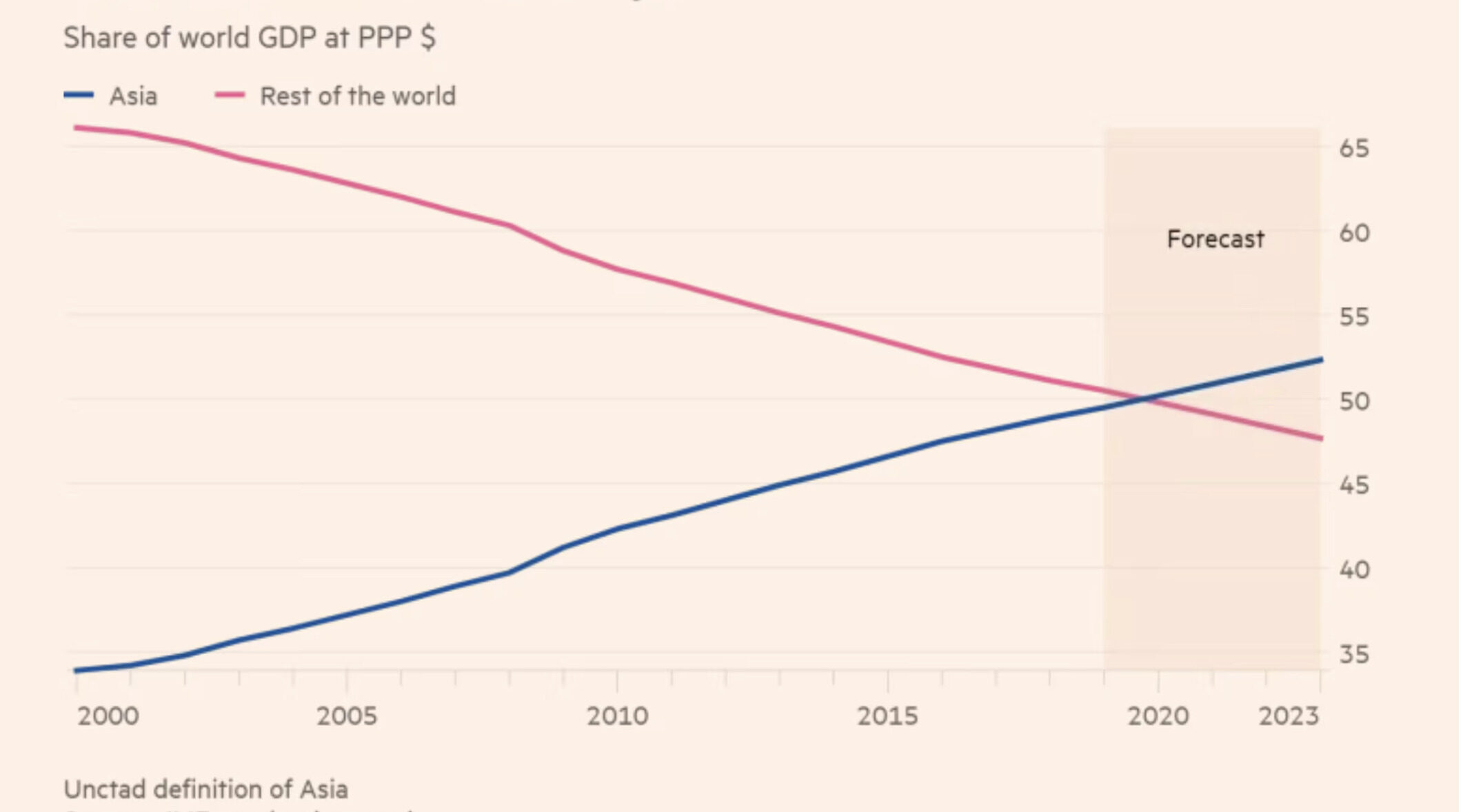

From a relatively modest share of global GDP in the early 2000s, Asian economies have surged ahead, accounting for more than half of global output (measured in PPP) by 2023. This dramatic rise marks a pivotal shift in the global economic landscape. The rapid economic ascent of Asia is unprecedented in modern history. In 2000, Asia’s contribution to global gross domestic product was relatively minor. However, driven by the economic dynamism of countries such as China, India, (Siddiqui, 2016) and the ASEAN nations, the region’s share of global output has grown significantly. By 2023, Asia accounted for over 50% of global GDP in PPP terms, outperforming other regions in both growth rates and aggregate output (Figure 1).

Projections to 2050 indicate that Asia will continue to expand its global economic presence. According to long-term forecasts by international institutions, Asia is expected to not only maintain but also strengthen its leadership in global output, innovation, and trade. This shift is often interpreted as a restoration of historical balance—a “return to normalcy” after a relatively brief period of Western dominance (IMF, 2025; Mahbubani, 2022).

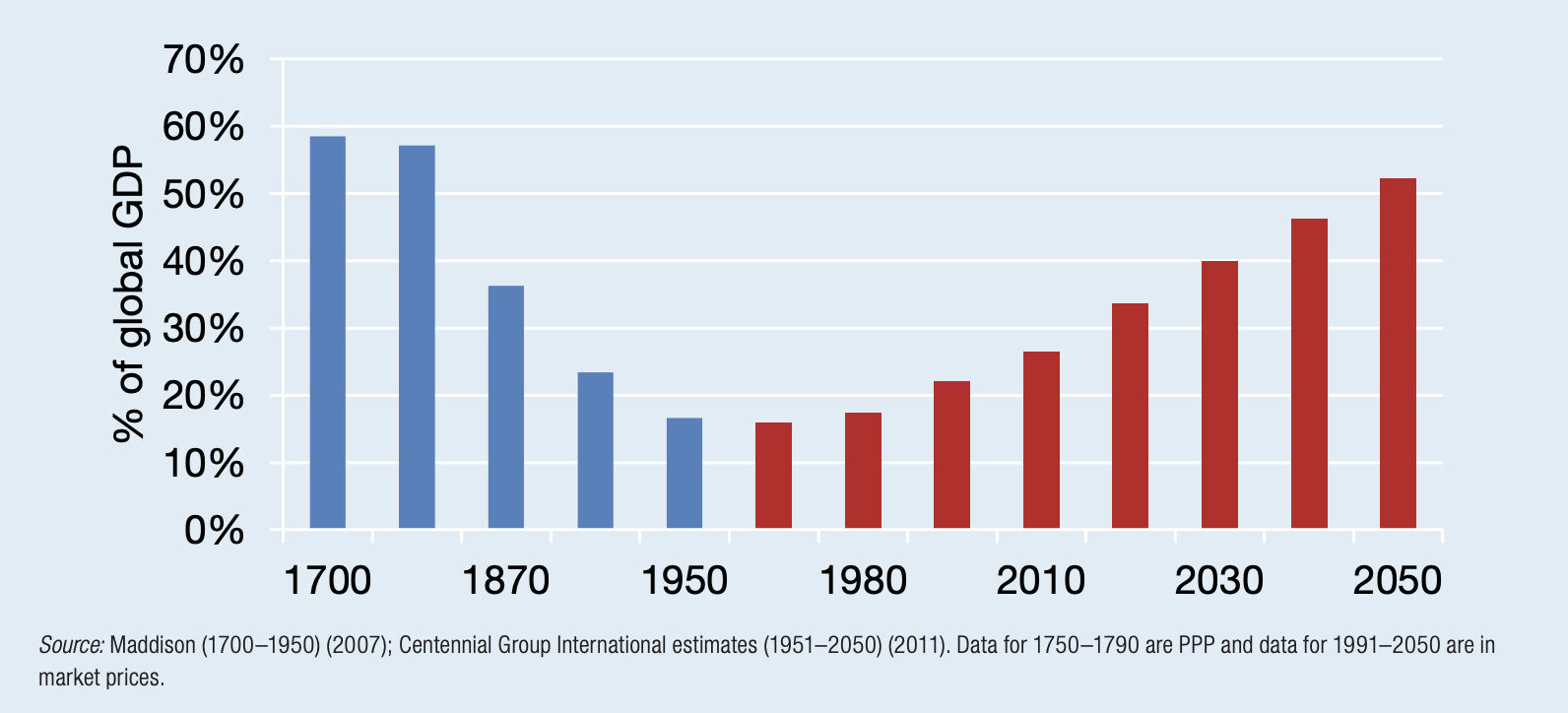

A historical perspective on Asia’s share of global gross domestic product (GDP) from 1700 to 2050 reveals that, prior to colonization, Asian economies—particularly those of China and India—dominated global output. Projections indicate that by 2050, Asia is poised to regain this leading position in the world economy, marking a restoration of its historical economic prominence (see Figure 2)

Figure 1: Share of World Gross Domestic Product (PPP, US$) from 2000 to 2023.

Between 1970 and 2023, Asia’s share of global GDP, measured in constant 2010 US dollars, rose dramatically—from less than one-twelfth to over one-fourth, marking an increase of nearly 20 percentage points. However, growth in GDP per capita, relative to that of industrialized countries, increased at a much slower pace. This divergence highlights the uneven nature of Asia’s economic catch-up, both across and within countries. Nevertheless, the region experienced significant structural transformation: the share of the primary sector in Asia’s GDP declined from 27% to just 8%, reflecting a shift toward industry and services.

The recent rapid growth of South Asia is due to several factors including greater integration into the global economy, driven by trade liberalization, globalization, and accession to the World Trade Organization (WTO). Since the 1990s, countries such as India, Bangladesh, and Sri Lanka have pursued a range economic reforms aimed at attracting foreign capital, and encouraging exports. India’s accession to the WTO in 1995 marked a pivotal moment in its economic trajectory. The liberalization of trade and investment regimes enabled Indian firms to participate more actively in global value chains, particularly in high-growth sectors such as information technology (IT), pharmaceuticals, and automotive manufacturing. The rapid expansion of the IT and services sectors has since emerged as a major engine of GDP growth and urban employment, especially in cities such as Bengaluru, Hyderabad, and Chennai.

Similarly, Bangladesh has emerged as one of the world’s leading exporters of ready-made garments (RMG), leveraging its competitive labour costs, preferential trade access to Western markets, and targeted government support. The RMG sector has not only driven substantial export earnings but has also generated millions of jobs—particularly for women—thereby contributing to broader socio-economic development and poverty reduction. Additionally, remittances from overseas workers have played a crucial role in strengthening foreign exchange reserves and raising household incomes across South Asia (Sachs, 2009).

Moreover, South Asian economies have increasingly diversified their export portfolios to include higher-value goods and services. Investments in infrastructure, skills development, and digital connectivity have further enhanced their industrial capacities. These structural transformations have underpinned sustained economic growth, reductions in poverty, and gradual improvements in living standards throughout the region. While significant challenges remain—including income inequality, poor infrastructures, and environmental sustainability.

Historically, Asia’s socio-economic achievements have been remarkable. According to Maddison’s PPP statistics, Asia’s share of world GDP reached its lowest point of 14.9% in 1962, while its GDP per capita as a proportion of that in Western Europe and North America also hit a nadir of 9.2% in the same year. It is important to note that these proportions cannot be directly compared with income shares and levels expressed in current prices at market exchange rates, due to differences in valuation methods (Maddison, 2007).

The Maddison database, recently extended through 2016, estimates that Asia’s share of world GDP, measured in 1990 international (Geary–Khamis) dollars, stood at 43.1% in 2016—up from 36.1% in 1870 and 56.5% in 1820. Furthermore, GDP per capita in Asia as a proportion of that in Western Europe, North America, and Oceania was estimated at 26.4% in 2016, closely resembling the 26.6% recorded in 1870. These figures suggest that Asia’s share of global output has returned to levels last seen around the mid-19th century, while per capita income relative to industrialized countries has reverted to its 1870 benchmark (Maddison, 2007).

During the 1980s, the export-led growth model was widely promoted as the ideal development strategy for developing countries, inspired by the extraordinary economic performance of the Four East Asian Tigers—South Korea, Taiwan, Hong Kong, and Singapore. These economies demonstrated rapid growth rates significantly exceeding those of countries like India, which pursued more dirigiste, or state-led, development strategies. Consequently, international institutions such as the World Bank advocated for abandoning ‘inward-looking’ policies in favour of export orientation (Glawe and Wagner, 2021).

This neoliberal prescription gained further momentum in the aftermath of the foreign debt crisis of the 1990s, when many developing countries were compelled to adopt export-led growth strategies. However, the apparent success of export-led growth, particularly in China and Southeast Asia, is more nuanced than often portrayed. Much of this growth was facilitated by easy access to foreign capital, especially from the US, Japan, and multinational corporations that relocated labour-intensive industries to low-wage Asian countries to produce goods for Western markets (Siddiqui, 2012).

V. Asian Economic Transformation

Asia has emerged as a global economic powerhouse, with a rapidly increasing share of global output, manufacturing, and trade. Over the past several decades, many Asian economies have undergone significant structural transformations. Improvements in demographic, social, and economic indicators reflect this progress, and several countries in the region have successfully transitioned to high-income or industrialized status.

A key factor behind this transformation has been sustained public investment in education and healthcare, coupled with strategies focused on employment creation and export-oriented growth. While openness to trade, foreign investment, and technology transfer has been crucial, successful industrialization has often required the guidance of deliberate and adaptive industrial policies.

While openness to trade, foreign investment, and technology transfer has been crucial, successful industrialization has often required the guidance of deliberate and adaptive industrial policies.

The region’s economic growth has been accompanied by a dramatic structural shift. In the 1960s, over two-thirds of Asia’s labour force was employed in subsistence agriculture. By 2024, more than 65% of workers were employed in the industrial and services sectors and Asia accounted for 30.7% of global merchandise exports, 29.3% of global imports, and attracted 35.9% of global inward foreign direct investment.

In the early postcolonial period, particularly in the 1960s, Asian exports were largely composed of agricultural and primary commodities, along with light manufacturing goods such as textiles and garments. Today, the region is widely recognized as production of high-tech goods, including automobiles, computers, smartphones, machine tools, and robotics. The region now boasts an electrification rate of over 90% and operates approximately 75% of the world’s high-speed rail network.

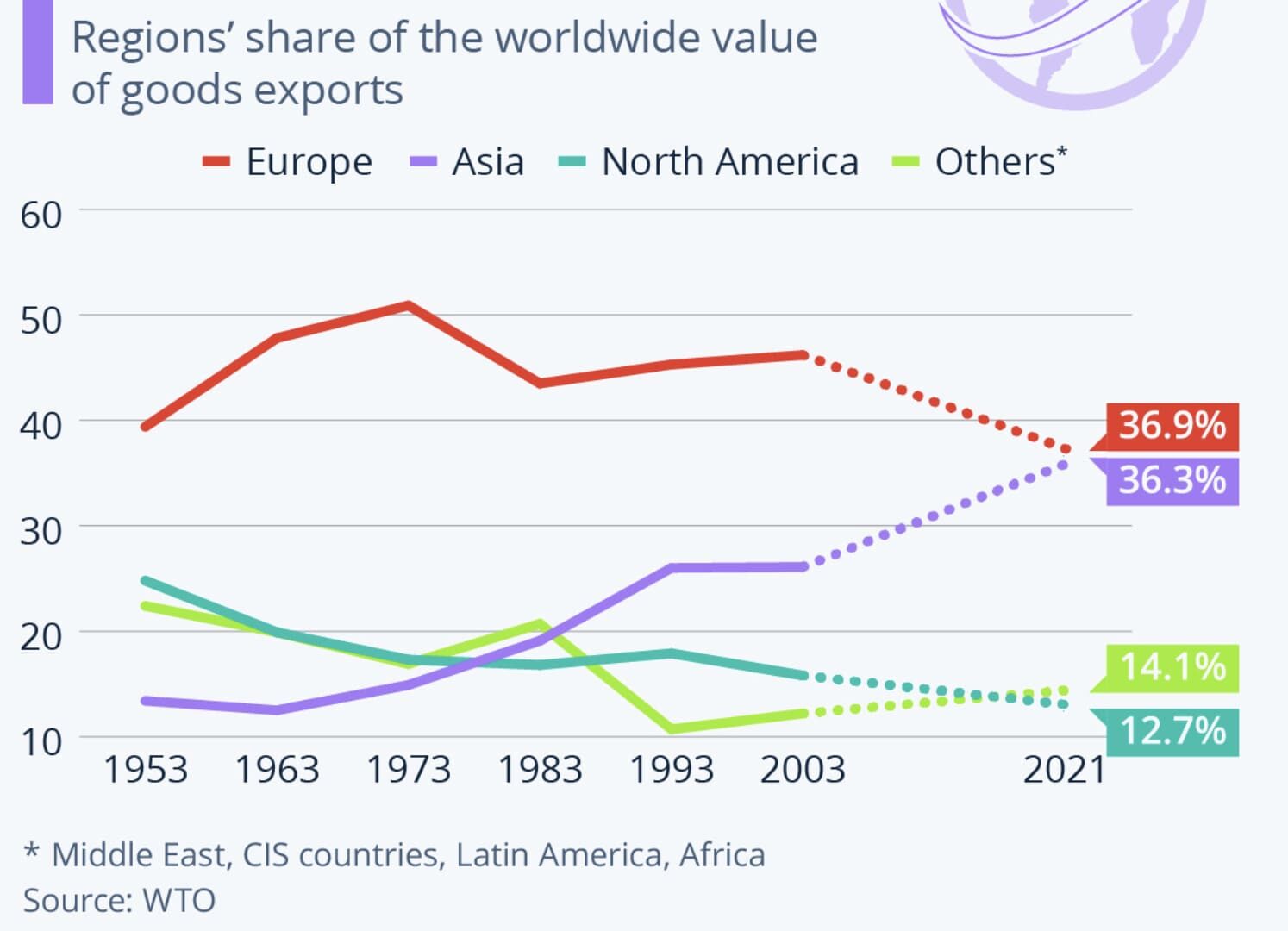

Exports of goods from Asia have risen sharply over the past several decades, reflecting the region’s deepening integration into the global economy. In 1953, Asia accounted for approximately 12% of global merchandise exports. By 2023, this share had increased to 36.3%, as shown in Figure 3. A major inflection point occurred around 2003, when many Asian economies—benefiting from WTO membership and greater access to global markets—accelerated their export-led growth strategies.

By 2023, Asia’s share of global exports slightly exceeded that of Europe, reaching 37% compared to Europe’s 36.9%. China, in particular, has played a pivotal role in this transformation. Since its accession to the WTO in 2001, China has emerged as the world’s leading manufacturing hub, with its share of global trade reaching nearly 16% by 2023. Intra-regional trade has also grown significantly (Siddiqui, 2023a). By 2023, approximately 58% of Asia’s trade occurred within the region, making it the second-most integrated trade bloc globally, after the European Union (Siddiqui, 2023b).

In terms of overall economic output, Asia’s share of global GDP (measured in PPP) reached approximately 55% in 2023—surpassing the combined share of Europe and North America. This growth has been driven primarily by the rapid expansion of China and India, but also supported by the performance of other emerging Asian economies. In 2023, Asia’s GDP was estimated at $41.36 trillion, making it the world’s largest economic region. China alone accounted for 19.2% of global GDP in 2024.

VI. Demographic Changes in Asia

The demographic transformation of Asia over the past seven decades has been profound. By 2023, Asia’s population had nearly tripled compared to its 1965 level, reflecting one of the most significant demographic expansions in modern history. This growth occurred alongside far-reaching social and economic transformations. Most notably, the region underwent a major demographic transition characterized by sharply declining birth and fertility rates, rising life expectancy, and improved education and health outcomes (Siddiqui, 2024b).

Fertility rates in Asia declined to roughly one-third of their 1965 levels, while birth rates fell by more than half. Life expectancy at birth rose dramatically, from 49 years in 1965 to 79 years in 2023. Infant mortality saw a striking decline—from 160 deaths per 1,000 live births to just 23. At the same time, literacy rates increased from 43% to 94%, underscoring major improvements in public education and healthcare systems. These gains were largely the result of sustained public investment in human capital, effective population policies, and broader economic modernization (Siddiqui, 2024c).

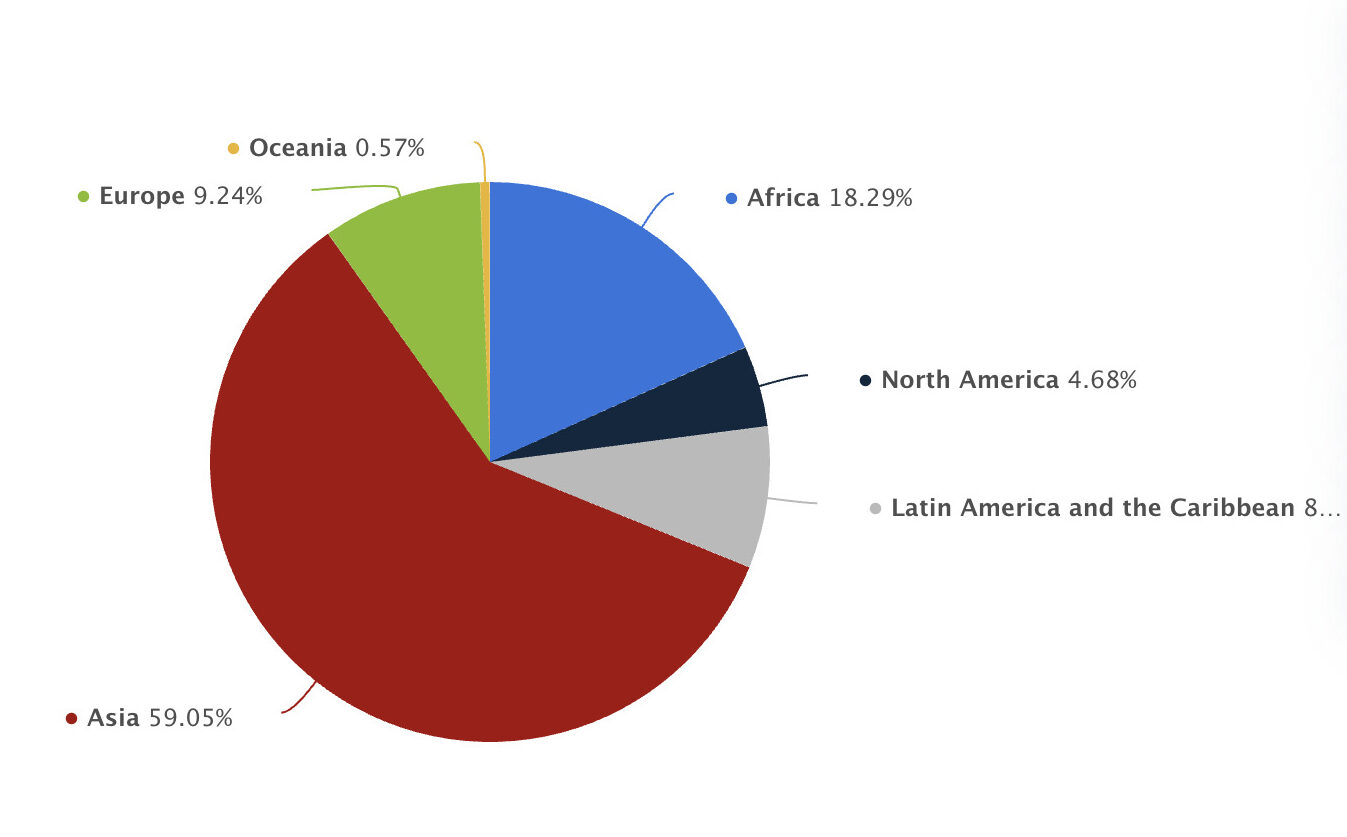

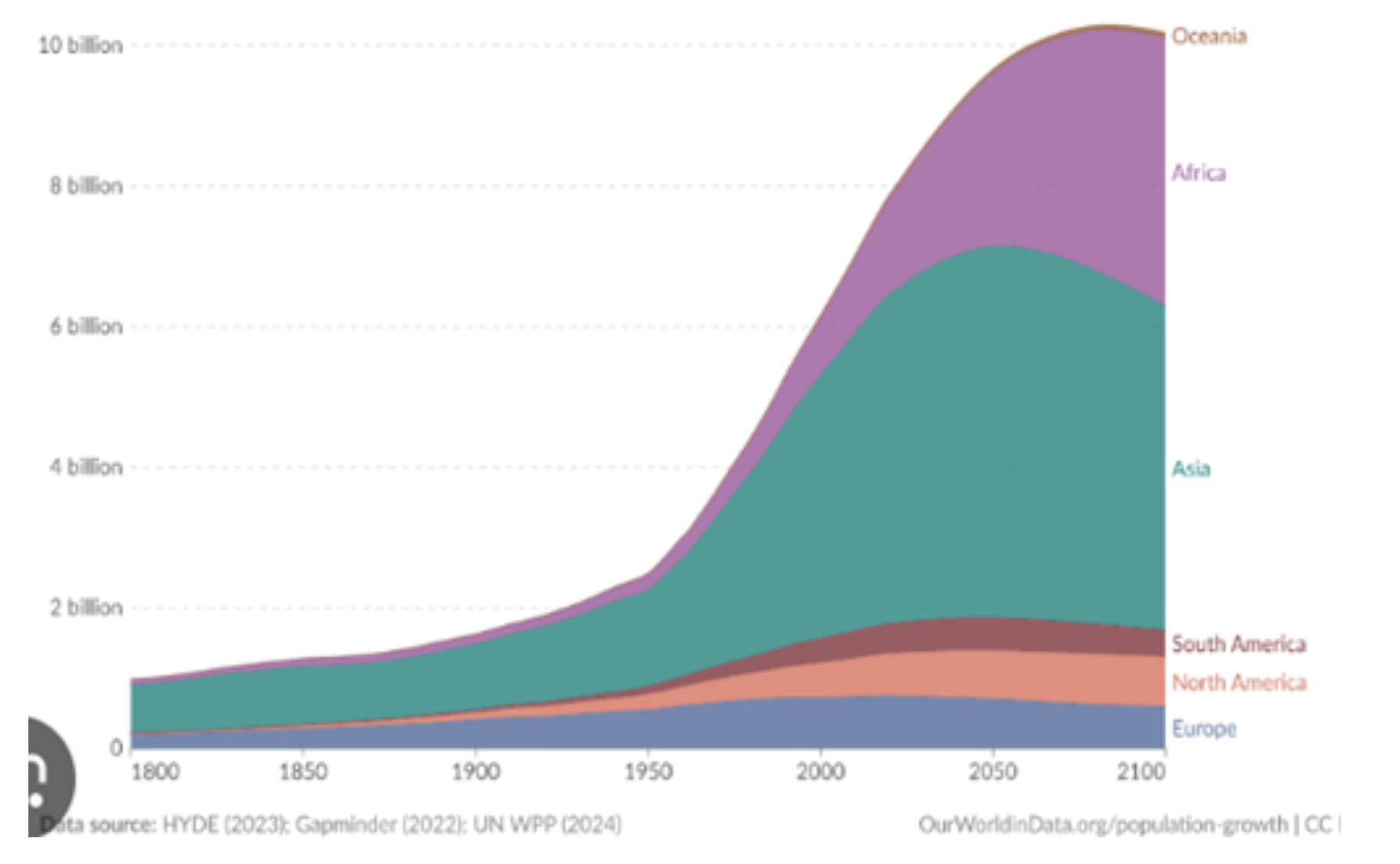

As of May 2025, Asia remains the most populous continent, home to approximately 4.8 billion people—or 58.8% of the world’s total population (see Figure 4). Over the past half-century, the region has experienced rapid population growth (see Figure 5), but this trajectory is expected to shift in the coming decades. By 2050, Asia’s population is projected to peak at around 5.3 billion, followed by a gradual decline in the second half of the century.

In contrast, Africa’s share of the global population is set to rise significantly. In 2024, Africa accounted for about 18% of the world’s population; by 2100, this figure is projected to reach 38%. Meanwhile, Asia’s relative share is expected to fall from nearly 60% today to approximately 45% by the end of the century. These shifts in global population distribution will have far-reaching implications for labour markets, economic development, migration patterns, and geopolitical dynamics.

Figure 4: Distribution of the Global Population by Continent, 2024.

Over the past seven decades, Asia has undergone a remarkable economic transformation. From widespread poverty and post-colonial stagnation in the mid-20th century, the region has emerged as a global engine of growth, investment, trade, and innovation. Many Asian countries have successfully transitioned from agrarian economies to dynamic industrial and service-based systems, lifted hundreds of millions out of poverty, and significantly improved human development indicators (IMF, 2025).

This unprecedented success has been underpinned by strategic state intervention, investment in human capital, industrialization, and the pragmatic use of global integration to serve national development goals. The Asian experience demonstrates that rapid development in the Global South is possible—if supported by effective state institutions, active public investment, and inclusive economic strategies.

Looking ahead, building a resilient and equitable economy in the Global South requires reclaiming economic sovereignty from the constraints of neoliberal orthodoxy. This involves a more assertive role for the state—not only in regulating markets but also in driving public investment, expanding domestic demand, and addressing inequality. Key policy measures include increasing rural incomes through agricultural development, public investments in education, health, and infrastructure. Asia’s development trajectory offers not a singular model, but vital lessons: long-term planning, key role of the state, industrialisation and social inclusion are essential to achieving broad-based and sustainable growth.

Dr. Kalim Siddiquiis an economist specializing in International Political Economy, Development Economics, Trade and Economic Policy. Since 1989, he has been teaching economics at various universities in Norway and the UK. Dr. Siddiqui’s research interests encompass a wide range of topics, including political economy, international trade, and economic history, South Asia, and emerging economies. He has presented papers at international conferences across numerous countries, reflecting his global engagement in the field. His scholarly pursuits span six broad domains: Political Economy, Development Economics, Economic History, Economic Policy, Globalization, and International Trade. Dr. Siddiqui has made significant contributions to research in areas such as trade policy, globalization, and political economy. His work has been published in chapters of edited books and articles published in peer-reviewed journals. For inquiries, Dr. Siddiqui can be reached at: [email protected]

References

Asian Development Bank (2020) 50 Years of Asian Development, Manila, Philippines.

Bhattacharjee, J. and Haldar, S. (2015) “Economic Growth in South Asia: Binding Constraints for the Future” Journal of South Asian Development, 10(2).

Glawe, L. and Wagner, H. (2021) The Economic Rise of East Asia – Development Paths of Japan, South Korea, and China, London: Springer.

IMF (2025) World Economic Outlook, Washington DC: IMF.

Maddison, A. (2007) Contours of the World Economy 1-2030 AD: Essays in Macro-Economic History. New York: Oxford University Press.

Mahbubani, K. (2022) The Asian 21st Century, Springer: Singapore.

Sachs J. (2009) South Asia story of development: Opportunities and risks. In Ghani E., Ahmed S. (Eds), Accelerating growth and job creation in South Asia (pp. 42–49). New Delhi: Oxford University Press

Siddiqui, K., (2025a) “Indian Economy at 75: Transformation and Challenges”, American Review of Political Economy 19(1).

Siddiqui, K. (2025b) “Understanding the Rise of High Technology in China” World Financial Review, April.

Siddiqui, K. (2024a) “China’s Growth Miracle and Development Strategy Since the 1980s”, World Financial Review, December.

Siddiqui, K. (2024b) “Impact of Population Changes and Economic Growth in China and India” World Financial Review, November.

Siddiqui, K. (2024c) “The BRICS Expansion and the End of Western Economic and Geopolitical Dominance” World Financial Review, November.

Siddiqui, K. (2023a) “Developmental Challenges: Export vs Import-Substitution in Industrialisation in Developing Countries” World Financial Review, October-November.

Siddiqui, K. (2023b) “The Political Economy of Shanghai Cooperation Organisation (SCO) and the Growing Regional Multilateral Ties” World Financial Review, February-March.

Siddiqui, K. (2022) “Comparing the Economic Performance of East Asian and Latin American Countries: The Role of Agricultural Reforms in the Economic Transformation” World Financial Review, July-August.

Siddiqui, K. (2020) “Prospects of a Multipolar World and the Role of Emerging Economies” World Financial Review, November-December.

Siddiqui, K. (2019) “The Political Economy of Global Inequality: An Economic Historical Perspective” Argumenta Oeconomica Cracoviensia 21(2):11 – 42.

Siddiqui, K. (2018). “The Political Economy of India’s Economic Changes since the last Century” Argumenta Oeconomica Cracoviensia 19: 103 – 132.

Siddiqui, K. (2016) “Will the Growth of the BRICs Cause a Shift in the Global Balance of Economic Power in the 21st Century?” International Journal of Political Economy 45(4): 315 – 338.

Siddiqui, K. (2012) “Malaysia’s Socio-Economic Transformation in Historical Perspective”, International Journal of Business and General Management 1(2):1-50.

The Bandung Conference marked a turning point in the postcolonial world’s pursuit of political and economic independence. Dr Kalim Siddiqui explores how this historic gathering laid the foundation for South-South cooperation and economic sovereignty, examining its enduring relevance to today’s Global South amid shifting geopolitical and economic power structures.

I. Introduction

In April 1955, representatives from 29 newly independent Asian and African countries convened in Bandung, Indonesia, for the landmark Asian-African Conference—widely known as the Bandung Conference. This historic gathering marked a watershed moment in the political awakening of former colonies in what is now commonly referred to as the Global South.

Seventy years later, the legacy of the Bandung Conference endures as a powerful symbol of the shared aspirations of postcolonial states to forge a world order based on solidarity, mutual respect, and economic cooperation. The struggle for independence not only dismantled colonial rule (Siddiqui, 2019a) but also paved the way for envisioning alternative models of economic development. Bandung Conference thus signalled the beginning of a transformative era aimed at reshaping global power dynamics and advancing South-South economic cooperation (Siddiqui, 1985).

One of the conference’s most enduring contributions was its resolution on economic collaboration, which emphasized the importance of mutual support among developing countries. This initiative sought to promote regional integration and strengthen intra-South economic ties as a pathway toward greater autonomy and equity within the global economic system.

The economic ascent of the Global South—a term broadly encompassing developing countries—has been one of the most significant global transformations since the end of World War II. This evolution can be traced through five interrelated phases: decolonisation, non-aligned movement, Third World’s debt crisis, globalisation, and the emergence of new economic powers.

The globalisation model rests on policies such as market liberalisation, trade and capital deregulation, and the reduction of state intervention in the economy.

Globalisation, initiated by the United States and other developed capitalist countries in the 1980s, was once heralded as a pathway to shared prosperity. The globalisation model rests on policies such as market liberalisation, trade and capital deregulation, and the reduction of state intervention in the economy. Rather than promoting a more equitable global order, globalisation has exacerbated socio-economic disparities, particularly in the Global South—and has undermined the traditional role of the state as a mediator of economic and social tensions (Siddiqui, 2019a).

The Global South—typically referring to developing countries, often characterized by lower GDP per capita—accounted for approximately 44% of global GDP in 2024. Despite this already substantial share of the world economy, these countries contributed an even more striking 80% to global economic growth, underscoring their increasing influence in shaping the trajectory of global development.

However, regions formerly subjected to imperial rule continue to face significant setbacks and challenges. A striking example is Israel, which has functioned as an outpost of imperialism and has played a destabilizing role in the broader Middle East. The creation of Israel can be traced back to imperial agreements such as the Sykes-Picot Agreement (1916) between Britain and France and the Balfour Declaration (1917). Israel was officially established in 1948 as part of a settler-colonial project facilitated by British support. Its founding involved the violent displacement of approximately 760,000 Palestinians and the destruction of hundreds of towns and villages in ethnic cleansing (Kaplan, 2025).

Since its inception, Israel has pursued policies aimed at the appropriation of Palestinian land and water resources while systematically displacing the indigenous Palestinian population to enable the expansion of Jewish settlements. Over time, this process has developed into a system of institutionalized segregation and discrimination. In the occupied territories, Israel has enforced policies that physically and legally separate Palestinians from Israeli settlers, maintaining parallel legal systems that significantly disadvantage Palestinians in terms of rights, freedom of movement, and access to essential resources (Siddiqui, 2024a).

II. Colonialism and Marx’s Critique of Imperial Power

From the late 15th century onward, European imperial powers established colonies that came to dominate nearly all of Asia, Africa, and the Americas (Siddiqui, 2020a). These colonial powers systematically stripped regions of the Global South of their sovereignty, plundered their natural resources, disrupted indigenous cultures, destroyed self-sufficient economies, and dismantled longstanding social and political institutions (Siddiqui, 2020b).

Although Karl Marx’s primary analytical focus was on Europe and the development of capitalism in 19th-century Britain, he also engaged with colonialism, particularly in the contexts of Ireland, India, and China (Siddiqui, 1990; also see 1996). In a New York Daily Tribune article dated June 5, 1857, Marx asserted: “One thing is certain, that the death-hour of Old China is rapidly drawing nigh… before many years pass away, we shall have to witness the death struggles of the oldest empire in the world, and the opening day of a new era for all Asia.” (Marx and Engels, 1968)

Marx’s reflections on India were notably ambivalent. While he acknowledged the devastating consequences of British colonial rule, he also viewed it as a possible—albeit violent—catalyst for historical transformation (Siddiqui, 2018). He lamented the “terrible havoc” inflicted on Indian society but argued that colonialism might inadvertently undermine stagnant social structures and facilitate progress (Siddiqui, 2024b). Karl Marx in his article, The British Rule in India (1853) which was published in the New-York Daily Tribune on June 25, 1853. Here in particular, Marx identified the Indian village community—often idealised by others—as a fundamental pillar of what he termed “Oriental despotism.” Further in The British Rule in India (1853), he wrote: “[Village communities], inoffensive though they may appear, had always been the solid foundation of Oriental despotism… restraining the human mind within the smallest possible compass… enslaving it beneath traditional rules, depriving it of all grandeur and historical energies.” (Marx and Engels, 1968)

Karl Marx argued that Britain’s transformation of India into a “reproductive country” for British industry—supplying raw materials in exchange for manufactured goods—necessitated the development of modern infrastructure, including railways, roads, and irrigation systems. This process of economic integration, he believed, would also undermine hereditary divisions of labour and, by extension, weaken the caste system, which he regarded as a central impediment to India’s social and political progress (Marx and Engels, 1968).