This paper examines how Indian merchants such as Parsi, Marwari, Baghdadi Jewish and others accumulated capital as junior partners in the colonial opium trade (1773–1900). Dr Kalim Siddiqui argues that operating within the East India Company’s monopoly system, they profited from smuggling opium into China. As the trade faced scrutiny, they diversified into cotton textiles, and other industries leveraging their wealth and networks to lay foundations for Indian industrial capitalism.

I. Introduction

The historiography of Indian capitalism has long been framed within a narrative of de-industrialization and colonial exploitation—a perspective powerfully articulated by nationalist economists such as Dadabhai Naoroji, R.C. Dutt, A.K. Bagchi, Irfan Habib and others. Their influential “drain theory” illuminated the mechanisms through which British rule systematically extracted wealth from the subcontinent, impoverishing its people while enriching the metropole (Siddiqui, 2024a; Habib, 2022). Yet this interpretive framework, for all its analytical power, has inadvertently obscured a parallel history: the accumulation strategies, and complex collaborations of indigenous merchant capital within the colonial political economy. This study addresses this lacuna by examining the critical—and under-theorised—role of Indian merchant communities as active participants in the opium trade that underwrote Britain’s imperial expansion in Asia.

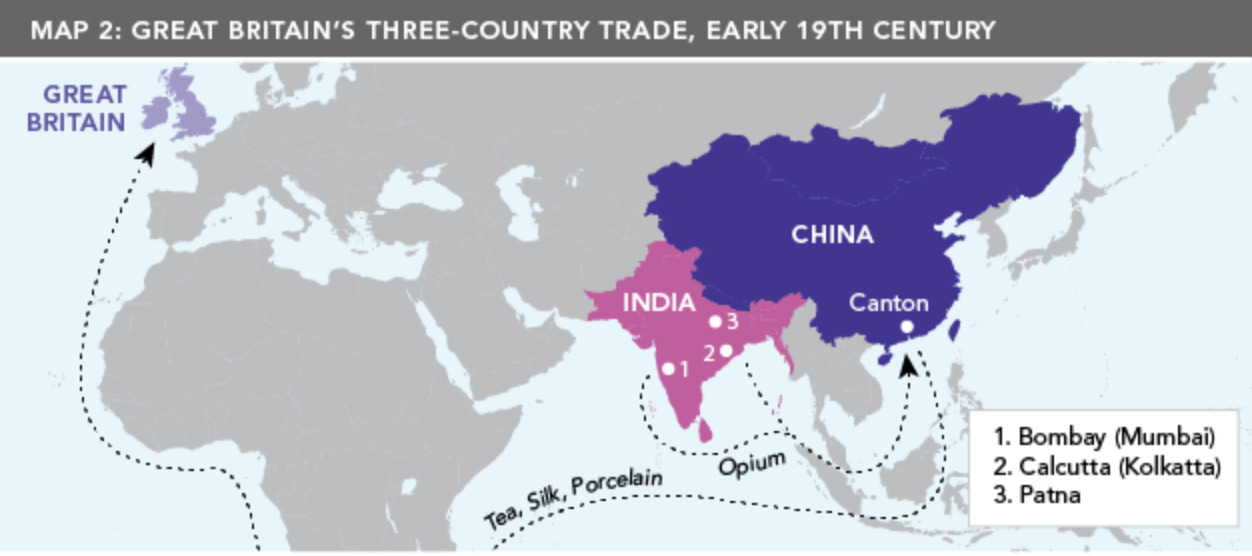

The trade in Chinese commodities, particularly tea and silk, posed significant financial challenges for the East India Company (EIC), a corporation owned entirely by British shareholders, which struggled to finance imports due to the absence of a cost-effective medium of exchange acceptable to the authorities of Qing China. At the time, Britain faced a persistent trade deficit with China, driven by strong European demand for Chinese commodities such as tea, silk, and porcelain, while Chinese consumers showed little interest in British manufactured goods. In response to this imbalance, British merchants increasingly relied on the export of opium to China. Following the Company’s victory at the Battle of Plassey in 1757, it secured political and economic control over key opium-producing regions in India and consolidated a monopoly over its production. Indian peasants were compelled to cultivate opium under this system, and the drug was subsequently smuggled into China, where its sale financed Britain’s purchases of Chinese commodities (Siddiqui, 2024b).

In 1773, Warren Hastings, Governor-General of Bengal, declared opium production in Bengal a monopoly of the EIC. The Company subsequently developed inexpensive and large-scale methods of cultivating opium poppies across its Indian territories. Under this system, the Bengal colonial administration controlled both the production and sale of opium, which soon emerged as a highly effective commodity of exchange. Opium not only generated its own demand but also helped offset the mounting costs associated with importing Chinese goods.

However, because the authorities of Qing China had imposed a ban on opium imports, the EIC could not ship the drug directly to China. Instead, it devised an indirect system: opium was auctioned in Calcutta to private merchants, who assumed the considerable risks—and potential profits—of smuggling it into China. This arrangement allowed the Company to avoid directly violating Chinese law while still capturing the bulk of the production surplus generated by the trade (Siddiqui, 2024a).

The opium trade that flourished under this system was among the most profitable and consequential enterprises of the nineteenth century. It resolved Britain’s chronic trade deficit with China, financing the burgeoning national appetite for tea while simultaneously creating a vast, dependent consumer population for opium in the Qing Empire. The trade’s illicit nature did not diminish its scale or sophistication; by the 1820s, opium had become the single largest commodity in world trade, valued at more than tea and coffee combined. Its geopolitical ramifications were equally profound: Chinese efforts to suppress the trade precipitated the Opium Wars (1839–1842; 1856–1860), which culminated in China’s forced opening under unequal treaties and the cession of Hong Kong to Britain.

Less recognized in this familiar imperial narrative is the trade’s transformative impact on economic development within India itself. In Bombay (now known as Mumbai), the opium trade provided an unparalleled avenue for capital formation among indigenous merchant communities. As early as 1803, private Indian enterprises were actively engaged in opium smuggling, often resisting British monopolistic controls through ingenious evasion. This covert commercial resistance contributed significantly to Bombay’s emergence as the preeminent center of economic activity in western India. More importantly, the fortunes accumulated through opium—by Parsi shipowners, Marwari financiers, and Baghdadi Jewish merchants like the Sassoons—would later seed the subcontinent’s industrial transformation. By the end of the nineteenth century, these merchants were leveraging their opium-derived wealth and global commercial networks to establish control over the cotton textile industry, laying the groundwork for modern Indian industrial capitalism (Siddiqui, 1996).

This paper traces that trajectory: from junior partners in an empire of illicit trade to pioneers of indigenous industrialization. In doing so, it offers not only a more nuanced account of Indian agency within colonial political economy but also a case study in the entangled moral economies of empire, where the profits of addiction financed the foundations of national capital.

Mainstream economists, focused on formal institutions and industrial development, have often failed to account for the primary sources of capital accumulation that later fuelled Indian industrial enterprise. They have also neglected the complex, ambivalent relationship between Indian merchant capital and the dominant British mercantile and colonial state. This paper argues that understanding the evolution of Indian industrial capitalism requires rigorous examination of the origins of this capital and the mechanisms of its accumulation during early colonial rule. The opium trade, despite its subsequent notoriety, served as a crucial—if morally fraught—crucible for this process.

The prevailing historical narrative often relegates Indian merchants to the role of passive intermediaries or compradors, mere cogs in the wheel of the British imperial enterprise. This perspective, however, obscures a more complex and dynamic reality. A critical examination of the primary sources of capital accumulation during the British colonial period reveals a foundational, yet fraught, phase in the growth of Indian capitalism. This was an era in which prominent merchant families did not simply serve as junior partners, but actively forged their own paths to wealth and influence, navigating the constraints and opportunities of colonial hegemony. By strategically operating within foreign markets, leveraging colonial trade networks, and selectively adopting new technologies, these business communities laid the groundwork for modern Indian enterprise, all while remaining fundamentally shaped by the unequal power dynamics of the Raj (Siddiqui, 2020a).

This study examines the paradox of Indian capital accumulation under colonial rule, moving beyond the simplistic comprador thesis to argue that Indian merchants functioned as proto-industrial capitalists who devised sophisticated strategies to build their fortunes. Their reliance on the colonial regime for protection and market access signified not passivity, but pragmatic adaptation within a structurally disadvantaged system. Those merchant communities that benefited from British imperialism and its wider Asian markets, recognised that aligning with British capital could facilitate global expansion while offering security, financing, and access to new technologies.

Paradoxically, the very technologies and legal frameworks imposed by the British—including telegraphs, railways, and contract law enforcement—became tools that these enterprising business families could, within limits, leverage to their advantage. Wealth accumulation thus unfolded as a dual process: collaboration with colonial power generated substantial profits, even as a quieter, parallel process built indigenous financial, commercial, and industrial capacity that would ultimately outlast the empire itself (Habib, 2022).

By focusing on specific merchant communities and family dynasties, such as the Parsis of Bombay (like the Tatas and Wadias), the Marwaris of Calcutta (like the Birlas), or the Chettiars of Madras, we can trace the diverse trajectories of this capital formation. Their stories reveal a pattern of beginning as traders, financiers, or collaborators with British capitalists, and then strategically diversifying into nascent industries like textiles, mining, and banking (Habib, 2022). They utilized capital accumulated through trade to challenge British monopolies in certain sectors, demonstrating that the “junior partner” was often learning the business with the intent of one day becoming a competitor. This complex interplay of collaboration and competition, dependence and defiance, constitutes the essential dialectic of Indian capitalism’s formative years. To understand the post-colonial economic might of India, one must first look to this crucial, and often misrepresented, period of gestation under colonial hegemony.

This study challenges this view by analysing their multifaceted involvement in the opium monopoly. From procuring raw opium in Malwa and Benares to its processing, transport, and sale in Calcutta, Indian merchant houses—such as the famous trading firms of Bombay and Calcutta—were indispensable. They operated not as simple agents but as crucial nodes in a complex commodity chain, managing credit networks, supply logistics, and market intelligence that the EIC could not easily replicate. This was not a relationship of pure subordination but one of asymmetrical interdependence. The Company relied on the capital, expertise, and infrastructure of Indian merchants to make the opium enterprise viable, while Indian merchants leveraged this partnership to generate substantial profits and accumulate capital on an unprecedented scale (Farooqui, 2021).

The role of Indian merchants in the opium trade thus demands scholarly attention for reasons extending beyond the history of a single commodity. First, it illuminates the significant agency of a non-European group within the international drug trade, demonstrating that the victims of imperialism could also, under constrained conditions, serve as its intermediaries and beneficiaries. Second, Parsi, Marwaris and other Indian involvement in opium constituted an important component in the rise of profits, the development of the Indian and imperial economies, and the growth of Bombay and other colonial commercial centres. Third, and most significantly, this history reveals the capacity of an illicit commodity to serve the material interests of non-European groups under imperialism. Opium provided not only profits but also the economic foundation for the subsequent social and political development of an Indian merchant class that would, in time, transform itself into a national bourgeoisie (Guha, 1984).

II. Opium, Empire, and Indian Merchants: Production, Exports, and Political Economy

Before examining the role of Indian merchants in the opium trade, it is essential to first understand the scale and expansion of opium exports to China, as well as the political economy of this trade that culminated in the Opium Wars and stiff resistance from the Chinese government. Under Mughal rule, India already possessed a sophisticated money market and complex credit instruments, such as the hundi, which challenge any notion of a passive or underdeveloped merchant class. By the late seventeenth century, merchant-bankers had become integral to the empire’s fiscal machinery, managing tax collection and facilitating the transmission of revenue across vast distances. Prominent financiers like the Jagat Seths of Bengal were not mere moneylenders but diversified capitalists whose financial backing could determine succession battles and the viability of provincial administrations (Farooqui, 2021).

However, the relationship between merchant-financiers and political power, though deeply embedded, remained personal and contingent. The prosperity of merchants rested on an “alliance between the businessman and the state,” but this dependence on individual patronage inhibited the development of institutional mechanisms capable of systematically aligning state authority with commercial interests. The Mughal state met its substantial credit requirements largely through agricultural revenues and loans from prominent bankers, creating a relationship characterized simultaneously by state dependence and the precarious privilege of the financier. This precolonial legacy—of sophisticated commerce operating within politically contingent frameworks—would profoundly shape how Indian merchants navigated the very different political economy of British rule.

The opium trade fundamentally reshaped the economic and political landscape of nineteenth-century China. Britain’s growing national obsession with tea created a chronic trade deficit, as China demanded payment in silver, not British goods. Following its decisive victories at Plassey (1757) and Buxar (1764), the EIC gained control over India’s most fertile regions. From 1773 onward, it established a state monopoly on opium production, compelling peasants in Bengal and Bihar to cultivate poppies for cheap and abundant export to China. While this system generated enormous revenues for the British, it also entrenched economic backwardness in regions such as the Bihar and Eastern Uttar Pradesh, distorting local economies and entrenching dependency.

Although the EIC monopolised British trade with South and East Asia, private ventures operated under its license through “country ships”—vessels chartered to sail between India and China, distinct from the Company’s own ships. Between 1764 and 1800, six of every ten country ships originated from Bombay, with two each from Bengal and Madras. Key Opium exporters were predominantly Englishmen resident in India, alongside a smaller number of Indians namely Parsis and Marwaris (Subramanian, 2017).

Opium occupied a central position in the political economy of British colonialism in India. At its peak, it constituted one-third or more of India’s total exports by value, serving simultaneously as an indispensable source of revenue for the colonial administration and as a primary conduit for remitting the imperial tribute—including the private fortunes amassed by EIC officials and British merchants. Beyond its fiscal functions, the trade financed Britain’s larger imperial commerce: opium sold in China provided the silver necessary to purchase Chinese tea, silk, and porcelain, which yielded enormous profits upon resale in Britain and Europe. The trade thus formed a lynchpin connecting the exploitation of India, the penetration of China, and the enrichment of the metropolitan economy (Farooqui, 2021).

Alongside moneylending, the opium trade served as a critical source of capital accumulation for Indian merchants. During the colonial period, land ownership underwent profound transformation, marked by sharply rising peasant indebtedness, landlessness, rising land rents, and the rise of absentee landlordism. Although cultivation of cash crops—jute, cotton, indigo, and opium—expanded, peasant incomes deteriorated. The agricultural surplus generated was largely siphoned off as tribute to Britain. Unlike in the precolonial era, this surplus was not reinvested in agriculture, contributing to long-term productivity decline and recurrent famines—phenomena largely unknown in the preceding period. The resulting rural impoverishment and mass mortality led to population stagnation over two centuries of British rule. (Siddiqui, 2020b).

Following the conquest of Bengal, the EIC established a monopoly over the opium produce of Bihar, initially through the private dealings of Company servants and later as an official colonial monopoly by the end of the eighteenth century. This monopoly was extended to Banaras, Ghazipur, and other opium-producing districts of the Ganga region as they came under the EIC control. In 1797, a formal policy was introduced under which all opium produced in Company territories in eastern India was directly appropriated from peasant cultivators. (Ghosh, 2008).

Once the EIC assumed control over the opium-growing districts of Bengal and Bihar, British shipping dominated the export of Bengal opium through Calcutta. Despite the Chinese edict of 1729 prohibiting opium smoking, consumption of Bengal opium in China increased fivefold in less than forty years, rising from 200 chests annually in 1729 to 1,000 chests by 1767. Even in the face of illegality, Chinese officials collected tariffs on the trade, reflecting the entanglement of commerce, imperial control, and local governance (Siddiqui, 2020a).

By 1819, confronting the persistent failure of its earlier prohibitionist measures to curb the flow of contraband opium from central India, the EIC adopted a new strategic approach. The objective was to bring the Malwa opium crop under its regulatory and commercial control in a manner analogous to its established monopoly in Bengal. The new policy mandated that the Company purchase the entirety of the Malwa opium harvest, which would then be officially auctioned at the ports of Bombay and Calcutta. From these auctions, merchants could legally (from the British perspective) ship the commodity to the Chinese market. This strategy represented an attempt to transform an uncontrollable illicit trade into a state-managed monopoly that could capture its revenues (Brown, 2002).

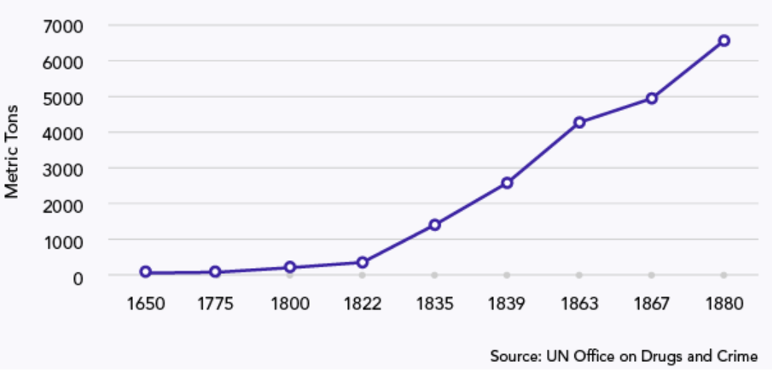

However, this attempt to assert control proved largely unsuccessful, encountering robust resistance from the entrenched commercial networks of Malwa. The region’s sahukars (merchant-bankers) and opium cultivators responded to the Company’s intervention with strategies of evasion and market defiance (Ghosh, 2008). They increased overall production, deliberately cultivated surplus opium to be sold outside official Company channels, and effectively circumvented the EIC’s purchasing mechanism by continuing to smuggle their product. The result was not a decline in the trade but its dramatic acceleration. Official exports of Malwa opium to China surged: from 1,715 chests in 1821–22, they nearly tripled to 4,000 chests the following year, a high volume that was sustained through most of the 1820s. The sharp increase in opium trade due to the Company’s policy is starkly illustrated in Figure 1. While the graph shows a general upward trend in total opium exports to China beginning after 1775—a period coinciding with the EIC’s consolidation of its monopoly over production and exports in Bengal—the curve becomes markedly steeper after 1822. This sharp inflection point visually captures the explosion in trade driven by the unregulated and officially-supplied Malwa opium, underscoring how the Company’s attempt to monopolize the crop inadvertently catalysed an even greater volume of opium entering China (Siddiqui, 2020a).

Figure 1: Opium Imports into China, 1650-1880.

While much attention focuses on the Company’s military and political activities after 1757, it is important to remember that the EIC remained fundamentally a private commercial enterprise. Its primary objective was to earn profits for shareholders, who received dividends throughout the Company’s rule and even after its dissolution. The Company was formally dissolved in 1874, without loss to its shareholders.

The final commercial privileges surrendered by the Company—most notably the monopoly of the China trade in 1834—did not diminish shareholder returns. On the contrary, the guaranteed dividend payable to shareholders increased slightly, from 10 to 10.5 percent, funded from the Company’s political revenues rather than commercial profits. As Karl Marx observed in 1858, the EIC’s transition from commercial to political revenue effectively maintained shareholder income: “The commercial existence of the East India Company was terminated in 1834, when its principal remaining source of commercial profits, the monopoly of the China trade, was cut off. Consequently, the holders of East India stock, having derived their dividends nominally from trade profits, required a new financial arrangement. The payment of dividends, previously chargeable upon commercial revenue, was transferred to its political revenue. The proprietors of East India stocks were to be paid out of revenues enjoyed by the Company in its governmental capacity” (New-York Daily Tribune, 9 February 1858).

The opium trade not only served imperial interests but also nurtured certain forms of indigenous capitalism in Asia, a dynamic noted by Karl Marx, who examined the broader Asian opium economy encompassing India, China, and Southeast Asia. Subsequent scholarship has highlighted the particularly Indian dimension of this trade, emphasizing the role of local merchants and intermediaries in sustaining the flow of opium to China. This arrangement highlights the inseparable link between colonial governance, commercial monopoly, and shareholder profit, illustrating how the Company’s political authority was leveraged to secure financial returns from its imperial dominions (Siddiqui, 2020a).

The drug that poisoned China enriched Bombay, and the fortunes made in its traffic funded the cotton mills that became symbols of Indian industrial aspiration. As Farooqui (1996:2746) notes: “Bombay as a great commercial and industrial centre was born of its becoming an accomplice in the drugging of countless Chinese with opium, a venture in which the Indian business class showed great zeal alongside the British. This is the sordid underside of Bombay’s colonial past. Towards the end of the 18th century Bombay, having been drawn into the vortex of capitalist relations, was assigned its role in the world capitalist system. Through colonial manipulation Bombay was made the main spatial regulator, in western and central India, for the transfer of tribute to the metropolis. In the process the hegemony of capitalism was fomented in the city. In the case of an advanced capitalist country like Britain establishing a colonial relationship with regions in which the capitalist mode of production is not sufficiently developed, or not dominant, problem of transition to capitalism is complicated by the fact that the colonial power seeks to create a mechanism for tribute realisation which as loot/plunder/drug- trafficking may form a part of the prehistory of capitalism.”

The rise of Bombay as India’s premier commercial centre in the nineteenth century was closely intertwined with the colonial opium trade. British opium policy created divergent conditions in eastern and western India. While the EIC maintained a strict monopoly over opium produced in Bengal, Bihar, and Awadh, Malwa and Rajasthan were subject to a more flexible, non-monopolistic system. This allowed private Indian merchants to participate directly in trade and linked the Malwa hinterland to Bombay’s port economy. Between 1821 and 1833, exports of Malwa opium from Bombay rose sharply, from fewer than 5,000 chests to nearly 40,000, reflecting the city’s emergence as a central transshipment hub. Indian merchants’ opium trade financed British purchases of Chinese tea while generating revenue for colonial authorities, forming a triangular system of trade linking India, China, and Britain. This mechanism underscored opium’s centrality to early global commerce and imperial finance.

The Chinese government, recognising the escalating social damage caused by narcotic addiction, had formally banned both the production and importation of opium in 1800. Despite this prohibition, the EIC and the private British merchants who succeeded it persisted in systematically smuggling the drug into China. The scale of this illicit trade grew exponentially. Between 1810 and 1838, annual opium imports surged from approximately 4,500 chests to a staggering 40,000 chests.

This dramatic rise in consumption precipitated a severe economic crisis for the Qing Empire. The massive volume of opium imports reversed China’s traditional trade surplus, leading to a crippling outflow of silver, the country’s monetary standard. The drain intensified rapidly: from an estimated loss of two million ounces of silver annually in the early 1820s, the outflow skyrocketed to over nine million ounces per year by the early 1830s. This monetary haemorrhage destabilised the imperial economy, depleting state reserves and causing severe deflation that burdened the general populace (Siddiqui, 2024b).

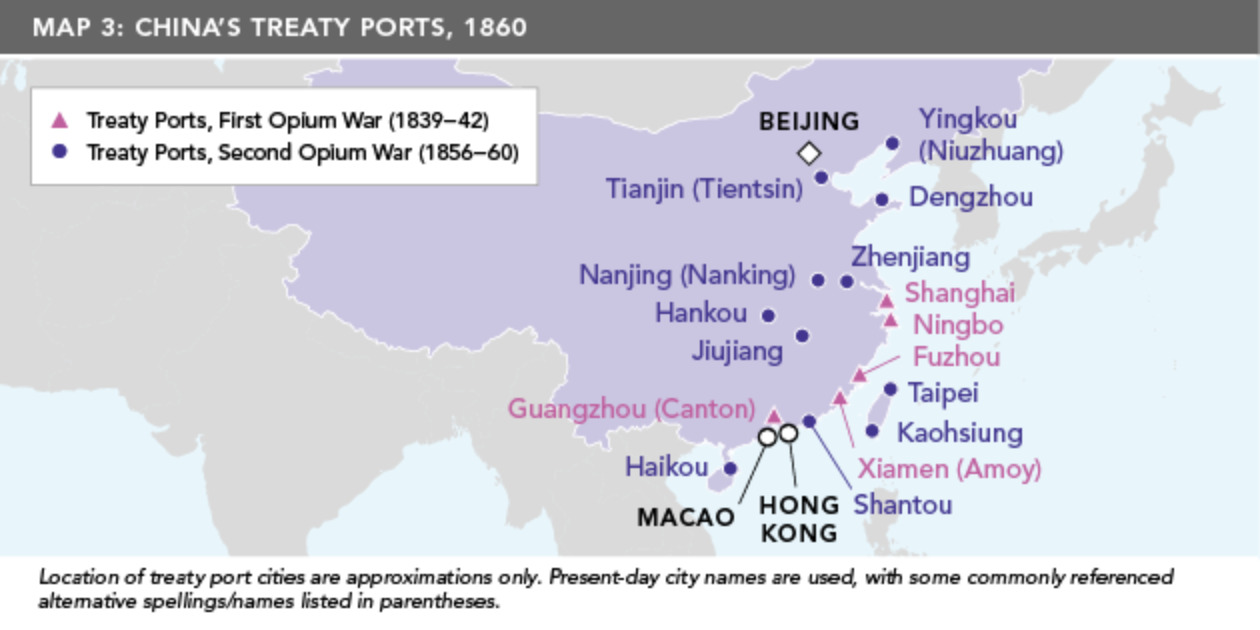

The Qing court’s decisive attempt to halt opium trade by confiscating and destroying over 20,000 chests of opium at Canton (Guangzhou) in 1839 provided the catalyst for armed conflict. In June 1840, a British naval expeditionary force arrived off the Chinese coast, initiating the First Opium War (1839–1842). After bombarding coastal forts and capturing key cities, Britain compelled a preliminary settlement. The conflict formally ended with the Treaty of Nanjing (1842), the first of the “unequal treaties” that would define a century of Chinese subjugation. The terms were entirely one-sided and offered no benefit to China. They forced the Qing to open five treaty ports (including Shanghai and Canton) to foreign trade, grant British citizens extraterritorial rights (exemption from Chinese law), pay a substantial indemnity, and cede the island of Hong Kong to Britain in perpetuity. Crucially, China was forced to halt its enforcement of the anti-opium laws.

Dissatisfied with the commercial access gained and seeking to expand the trade, Britain, allied with France, launched the Second Opium War (1856–1860). And in 1860, British and French troops looted and burned the Old Summer Palace (Yuanmingyuan) in Beijing. Prior to the fire, the forces seized thousands of artifacts, including porcelain, silk, pearl and gold ornaments. In China, this event is regarded as a symbol of national humiliation and imperialist aggression.

This conflict concluded with the humiliating Anglo-French capture and occupation of Beijing. The resulting treaties (the Treaties of Tianjin) imposed even harsher terms on China. Among the most significant provisions was the legalisation of the opium trade itself, albeit subject to a nominal import tax. This effectively forced the Chinese government to abandon its moral and public health stance and accept the drug’s influx as a legitimate article of commerce. The agreements also opened eleven additional treaty ports, imposed further indemnities, and permitted increased Christian missionary activity across the interior.

The consequences of these wars were catastrophic for the Qing Dynasty and Chinese society. The “unequal treaties” crippled the state’s legitimacy, demonstrating its military and diplomatic weakness to its own subjects and the world. Economically, the legalized opium trade continued to drain China’s silver reserves for decades; imports peaked at a staggering 87,000 chests in 1879, exacerbating the very social damage—widespread addiction and poverty—that the original ban had sought to prevent (Siddiqui, 2019). The volume of imports only began to decline by the end of the 19th century and the trade largely ceased during World War I.

The opium economy had permanently reshaped the trajectory of India and China. China’s defeat in these mid-century conflicts signalled the terminal decline of the Qing state, setting the stage for internal rebellions, the fall of the monarchy in 1911, and a “Century of Humiliation.” For Britain, the wars secured a lucrative commodity that helped balance its trade with China and finance its imperial administration in India. The Opium Wars thus mark a pivotal turning point in modern history, where the forces of British imperial capitalism, operating under the banner of ‘free trade’, forcibly dismantled China’s sovereignty and integrated it into a global economic system on profoundly unequal and destructive terms.

Map: China’s Treaty Ports after the Opium Wars.

III. The ascent of Parsi and Jewish Merchants in the Opium Trade

The Parsis were distinct from the village-based Hindu caste society of Gujarat. Even if they had integrated with Hindu artisans, intra-village jajmani production relations would likely have remained tenuous. This structural separation, however, allowed Parsi small producers to bring larger marketable surpluses than their Gujarati caste-based counterparts, particularly during the commercialisation of Mughal India.

Under British rule, Parsis who adopted new business practices—working as brokers, agents, and intermediaries for Europeans—were well positioned to succeed financially, provided their ambitions remained within colonial limits. Their skills in carpentry enabled some to establish manufactories producing horse coaches and bullock carts. Yet such activities, though cultivating small-scale capitalists and a capitalist outlook, accounted for only a fraction of the wealth the community had accumulated by 1840 (Guha, 1984).

The Parsis, descendants of Zoroastrians who migrated from Iran to India in the eighth century, constitute one of the country’s smallest communities. As migrants, they settled in urban areas, rapidly adopting the Gujarati language and leveraging their commercial skills. They enjoyed a special status in western India as enterprising traders, and were quick to appreciate the advantages of the British connection in the Indian Ocean trade, specifically with China, from the latter half of the 18th century. Parsis participation in the opium trade represents an important non-European contribution to imperial commerce, facilitating the accumulation of wealth in western India while supporting the expansion of both the Indian and imperial economies. Under British India, however, they transformed from a relatively insular group into one of the subcontinent’s most prosperous, educated, and influential communities. From their ranks emerged prominent merchants whose participation in the opium trade with Qing China generated substantial capital, much of which was reinvested in other profitable ventures (Palsetia, 2008).

The opium trade provided a vital opportunity for capital formation, allowing the community to evolve from petty traders and contractors in the 18th century to major shipbuilders, brokers, and merchants by the 19th century. From the early eighteenth century, Bombay emerged as the primary centre for the Parsi community. Migrating from Gujarat and surrounding regions, Parsis capitalised on the security offered by the EIC and the growing opportunities from trade and urban expansion. They played a key role in transforming Bombay into a thriving commercial hub, distinct from entrenched port cities like Surat. Their economic rise in western India, particularly in Bombay and Ahmedabad, coincided with the arrival of European traders, laying the foundation for mutually beneficial commercial ties. Parsis worked as hawkers, interpreters, contractors, and intermediaries for European merchants, gradually embedding themselves in colonial trade networks (Subramanian, 2017).

The China opium trade proved instrumental in elevating Parsis from small-scale traders to influential merchants and founders of prominent families. Hirji Jivanji and his brother Maneckji are recorded as the first Parsis to establish a trading firm in Canton in 1756—then the only Chinese port open to foreign trade. Owning seven ships, half of which were dedicated to the China route, the Jivanji exemplified how maritime commerce underpinned the rise of the Parsi mercantile elite. Even master shipbuilders, such as the Wadias, faced structural limits: the docks they used were owned by the EIC, and much of the working capital—raw materials and other inputs—was not their own (Guha, 1984).

By the nineteenth century, many Parsis had become agents for British firms, guarantee brokers, and shipbuilders, securing their position within imperial economic structures. Their engagement extended beyond commerce: during the First Opium War (1840–42), Parsi merchants actively supported British military operations by lending their ships to transport troops, an act for which several were imprisoned by Chinese authorities. This collaboration underscores the depth of the comprador relationship; wherein Indian capital not only coexisted with British power but also enabled its aggressive expansion across South and East Asia (Palsetia, 2008).

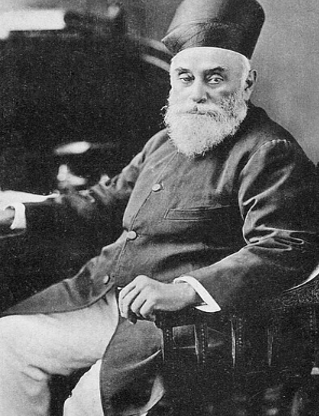

The foremost Parsi merchant in China, Jamsetjee Jejeebhoy (1783–1859), exemplified this ascent. His firm, established in 1818 and renamed Jamsetjee Jejeebhoy Sons & Co. in 1836, partnered across religious lines with Motichund Amichund and Mahomed Ali Rogay, creating a vast trading network capable of handling large-scale commerce. By the 1830s, Jejeebhoy’s firm held a near-monopoly over Malwa opium shipments from Bombay, managing both personal and third-party consignments. Parsi involvement in opium facilitated the community’s rise from hawkers and interpreters to merchant princes and leaders, providing the wealth that later funded diversified commercial ventures and philanthropic foundations (Guha, 1984).

The Tata family exemplifies this trajectory. Nusserwanji Tata broke from his family’s priestly tradition to establish an export business in Bombay (Harris, 1958). Following the First Opium War (1839–42), when the EIC allowed exports from the Malwa region, he began shipping opium to China. His son, Jamsetji Tata, was sent to Hong Kong in 1859 to manage the family’s opium interests, including Tata & Co., an importing firm run by his relative Ratanji Dadabhoy Tata (1856–1926). During his time in China, Jamsetji recognised the greater potential in cotton and pivoted the family enterprise accordingly—a strategic shift that enabled the Tatas to survive the cotton crash of 1865 and eventually build a diversified industrial empire. Although later renowned for steel, hydroelectric power, and philanthropy, the family’s early fortune was rooted in the lucrative, state-sanctioned opium trade centred in British-controlled Bombay (Harris, 1958).

Source: https://dailypioneer.com/news/jamsetji-tata-and-the-power-of-purpose

The transformation of Bombay’s Parsi community continued through several phases from 1750 to 1918, coinciding with the British Industrial Revolution and the consolidation of colonial rule in India. Between 1750 and 1850, Parsis gradually accumulated wealth and commercial experience, often serving as brokers, agents, and intermediaries for European merchants. This period laid the foundations for a limited and highly constrained form of industrialisation, which gained momentum in its third phase (1850–1918), when the Parsi bourgeoisie led whatever, private industrial initiatives were possible under colonial constraints. The Parsis thus represent a striking example of how a non-European community could, under imperialism, leverage participation in the drug trade to transform its economic and social standing (Subramanian, 2017).

Parsis almost monopolised the China trade in opium until 1809. By 1812–13, twenty-nine large ships traded from Bombay, nineteen of which exceeded 600 tons; of these, twelve were Parsi-owned and seventeen belonged to British traders. Several Parsi-owned ships also traded from Calcutta. By 1823, opium had far surpassed raw cotton in importance within the China trade. Initially, the Company attempted to restrict Malwa opium exports, but this proved impractical. From 1830 onward, it implemented a pass system allowing Malwa opium to transit Bombay for export to China upon payment of a heavy excise duty. The Parsis, collaborating with British private traders such as Beale & Magniac, Jardine Matheson, and Company, maintained dominance in the opium trade from 1810 to 1842. Their share began to decline thereafter, challenged by the entry of Jews and other Gujarati trading communities.

Parsis similarly leveraged the China-opium trade to ascend socially, politically, and economically. Pestonjee Cowasjee Sethna established Cowasjee Pallanjee & Co. in Canton in 1794, and other families, such as the Banajis, traded timber, silk, and opium with China and Burma. The opium trade provided a financial foundation for major Parsi business houses and elevated the community as a leadership group within western India. By the mid-nineteenth century, Bombay had become the principal Parsi hub, offering security under British rule and freedom from the competitive pressures of older cities such as Surat. Parsi merchants such as Jamsetjee Jejeebhoy and Jewish merchants such as David Sassoon were among the most prominent exporters of opium to China (Sassoon, 2022).

Within this process, the Parsi community occupied a particularly prominent position in the opium trade between India and China during the late the eighteenth and nineteenth centuries. Their participation highlights the role of non-European intermediaries in the expansion of imperial commerce. Opium trade contributed to the rapid expansion of Bombay as a major colonial centre. At the same time, the opium economy demonstrates how certain colonial actors were able to advance their own interests within imperial structures. Profits from the trade facilitated the economic consolidation and social mobility of the Parsi community, illustrating how a global commodity could significantly reshape the fortunes of a small but influential group within the broader political economy of empire (Palsetia, 2008).

The opium trade not only fuelled the British Empire and transformed China but also served as a powerful engine for the rise of specific merchant communities in India, especially Jewish families from Iraq, who settled in Western towns and soon involved in new profit venture such as opium exports to China. And the most prominent examples are the Baghdadi Jewish Sassoons of which leveraged this lucrative commerce to build enduring commercial empires in 19th-century Bombay.

The Sassoon family, often called “the Rothschilds of the East,” built one of the world’s wealthiest business empires on the foundations of the opium trade. The family’s rise began when David Sassoon (1792–1864) migrated from Baghdad and settled in Bombay in 1832. Capitalizing on the city’s explosive growth as a British trade hub, he established a trading firm that dealt in commodities like silver, gold, and silk. However, the company’s primary vehicle for immense wealth was the trafficking of Indian opium to China. Operating as major shippers and consignment merchants, the Sassoons perfected a triangular trade: they purchased Indian opium, exported it to China, used the proceeds to buy Chinese goods like tea and silk, and then sold those goods for a profit in Britain (Sassoon, 2022).

By the 1870s David Sassoon’s sons, particularly Albert Abdullah David Sassoon (1818-1896), founded his own rival firm in 1867 and the family had come to dominate the opium trade. Their shipment volume expanded from roughly 30,000 chests in 1836 to a staggering 105,508 chests by 1880, surpassing established British firms like Jardine Matheson. The colossal wealth generated allowed the Sassoons to diversify massively. They capitalized on the American Civil War-era cotton boom, becoming major cotton mill owners with seven mills under the Sassoon Spinning and Weaving Company. They also ventured into banking, real estate, and built Bombay’s first commercial wet docks, the Sassoon Docks. Their legacy was cemented through extensive philanthropy, funding landmarks such as the David Sassoon Library, the Knesset Eliyahoo Synagogue, and various hospitals. The Sassoons’ success was built on their close ties to the British Empire and their ability to adapt to global trade demands, transforming Bombay into a major commercial center in the process (Sassoon, 2022).

IV. Marwaris and Other Merchant Communities in the Opium Trade

Within this trading network, indigenous merchant groups such as Marwari played vital intermediary roles in opium trade during the mid-19th century. Originating from the arid regions of Rajasthan (particularly Shekawati and Bikaner), they migrated to burgeoning commercial centres like Calcutta and Bombay in the 19th and early 20th centuries to seek livelihood. They leveraged community networks and kinship ties to establish themselves. Although Parsis and Jewish merchants dominated the direct export of opium to China, Marwaris were deeply involved in the trade’s financial and speculative dimensions. Merchants such as Swarupchand Hukumchand, Sevaram Ramrikhdas, Devibaksh Jivanram, and Ghanshyam Das Birla accumulated considerable wealth through opium speculation. By the early nineteenth century, Malwa opium accounted for nearly 40 percent of the Chinese market, underscoring the scale and importance of this trade (Calangutcar, 2007).

Many Marwari firms established strong connections with opium markets in central and western India. Initially operating as brokers and agents for established Bombay merchants, they gradually expanded their role within the trade. Evidence from the official account indicates that several Marwari firms were involved in opium trade, these transactions were recorded as early as 1791. These official trade records demonstrate the early participation of Marwari merchants in the opium trade and later on by mid-19th century their involvement increased sharply in commercial networks linking major trading ports in China.

The opium trade provided the foundation for the accumulation of indigenous merchant capital for Marwaris. Initially as brokers and agents for established Bombay merchants, Marwaris gradually expanded their networks, facilitating inland trade, finance, and speculation. Figures such as Shivnarain Birla, Swarupchand Hukumchand, and Ghanshyam Das Birla amassed substantial wealth through these activities. Although Marwaris entered direct export relatively late, their early capital accumulation allowed them to consolidate a strong position in Bombay’s commercial economy and, by the twentieth century, diversify into industry and finance. Over time, several Marwari merchants accumulated substantial capital through brokerage, speculation, and inland trade. The opium trade thus played an important role in the formation of Marwari merchant capital during the nineteenth century (Calangutcar, 2007).

The profitability of the opium trade attracted a wide range of merchant communities to Bombay. According to Amar Farooqui (2021), by the 1820s Parsis, Marwaris, Gujarati Banias, and Konkani Muslims had all entered the opium trade in the city. These groups played different but complementary roles within the commercial network that connected opium-producing regions in India with markets in China. Although Marwaris entered the direct export trade in opium relatively late—at a time when international pressure to suppress the trade was increasing—the profits they had already accumulated enabled them to establish a strong presence in Bombay’s commercial economy. Despite occasional losses caused by market fluctuations and political restrictions, the capital generated through opium trading remained substantial.

The divergent policies adopted toward opium produced in eastern and western India had significant consequences for the development of Bombay. While the EIC established a strict monopoly over opium produced in Bengal, Bihar, and Awadh, it was unable to impose the same system on Malwa and Rajasthan. Instead, a more flexible, non-monopolistic policy emerged in western India. This arrangement allowed private merchants to participate more directly in the trade and effectively opened up a vast hinterland for Bombay’s commercial expansion. Through the Malwa opium trade, Bombay developed strong economic links with interior regions, integrating them into global trading networks.

During the nineteenth century, Bombay rose to prominence as India’s leading commercial centre. Its early commercial fortunes were closely tied to the opium and cotton trade with China. Although cotton exports formed an important component of Bombay’s commerce, they were insufficient to finance the growing demand for Chinese tea within the British Empire. Opium provided the crucial means of balancing this trade. The expansion of the opium trade therefore coincided with—and significantly contributed to—the rise of Bombay as one of the principal port cities of the British Empire during the first half of the nineteenth century. The profitability of this commerce attracted a wide range of merchant communities to the city, all seeking to participate in the flourishing opium economy.

British opium policy in India played a decisive role in shaping the commercial expansion of Bombay in the nineteenth century. While the EIC maintained a strict monopoly over opium produced in eastern India—particularly in Bengal, Bihar, and Awadh—it was unable to impose similar control over opium produced in western India, especially in Malwa and Rajasthan. As a result, a more flexible and largely non-monopolistic system developed in western India. This allowed private merchants to participate actively in the trade and linked the Malwa hinterland to Bombay’s port economy.

The China trade, and opium as a core component, was central to the economic and social transformation of Bombay’s Indian merchant communities. Together, Marwaris and Parsis drove the city’s phenomenal growth as a commercial hub in the nineteenth century. Opium profits not only financed industrial expansion but also shaped the moral, social, and philanthropic infrastructure of these communities, leaving a lasting imprint on the commercial and civic life of Bombay. As Amar Farooqui (1996) argues, “the destiny of Bombay as a great commercial centre was born of it becoming an accomplice in the drugging of countless Chinese with opium, a venture in which the Indian business class showed great zeal. The wealth accumulated through this trade allowed many Marwari business families to diversify their investments. By the late nineteenth and early twentieth centuries, they increasingly moved into banking, finance, and modern industry. This transition marked the transformation of Marwari merchant capital into industrial entrepreneurship, positioning them as leading figures in India’s industrial economy during the twentieth century.”

The Marwaris, a mercantile community originating from the arid region of Marwar in Rajasthan, represent a distinctive archetype of commercial and political agency in Indian history. Their economic ascendancy was initially built upon a foundation of traditional financial practices. As indigenous bankers and moneylenders (sahukars), they were instrumental in the pre-colonial and early colonial rural economy, extending credit to nobles, feudal intermediaries, and, crucially, to peasants who relied on them as a vital source of liquidity (Calangutcar, 2007).

Belonging predominantly to traditional Hindu trading castes (such as Maheshwari, Agarwal, and Oswal), the Marwaris specialized in the procurement and circulation of agricultural commodities. This commercial role was inextricably linked to the political structures of their time. They cultivated and maintained close, symbiotic relationships with the Maharajas and large feudal estates (jagirdars) that dominated the Indian subcontinent. This proximity to royal courts and feudal magnates was not merely a business strategy but a defining feature of their social and political identity, embedding them deeply within the established power matrix.

A key point of distinction from their European counterparts lies in this very integration. Unlike the emerging bourgeoisie in Europe, whose economic interests often placed them in opposition to the landed aristocracy and absolute monarchies, the Marwaris’ capital accumulation was profoundly aligned with the pre-existing feudal and imperial order. Their wealth was not deployed to fundamentally challenge these structures. Instead, during the colonial period, this alignment evolved into a complex collaboration with British imperial capital. They operated as key intermediaries in the colonial economy, facilitating the extraction of raw materials and the distribution of imported manufactured goods, thereby consolidating their position as compradors within the imperial system.

Furthermore, Marwari identity was profoundly shaped by deeply rooted religious orthodoxy and engagement with sectarian politics. Their commercial world was often governed by community-specific religious and social norms. This religiosity extended beyond personal piety to include active patronage and organizational support. The Marwari community served as a significant financial backbone for Hindu extremist organisations in the late nineteenth and early twentieth centuries, providing funding and support to groups like the Hindu Mahasabha and the Rashtriya Swayamsevak Sangh (RSS) illustrate a conscious fusion of commercial interests with a specific, Hindu majoritarian political vision (Siddiqui, 2016). Consequently, for the Marwaris, the realms of commerce, religion, and politics were not discrete but were interwoven, with sectarian politics being a consistent and practiced dimension of their public life. This unique combination—of feudal loyalty, collaboration with imperialism, and patronage of religious nationalism—distinguishes the Marwari mercantile class from the classical model of the liberal, revolutionary bourgeoisie (Siddiqui, 2024c).

V. The Dialectic of Dependency and Development

The rise of capitalism was characterized by the expansion of commodity production and the gradual displacement of production oriented solely toward subsistence. In colonial contexts, this transformation took the form of production for distant markets and exchange within imperial trading networks. However, colonial capitalism developed under structural constraints that distinguished it from the trajectory of metropolitan economies. Through political and economic intervention, the imperial centre extracted colonial surpluses and redirected them to the metropolis. This asymmetrical relationship of control and appropriation limited the emergence of autonomous capitalist development within the colony.

With the colonisation of the Indian economy, however, the relationship between Indian merchant capital and British imperial power cannot be understood simply in terms of subordination. Rather, it unfolded as a dynamic and transformative process. In the early colonial phase, Indian merchants who partnered with the British—in opium, indigo, and other export commodities—often operated in a comprador capacity, performing functions that were complementary rather than competitive. The opium trade of the late eighteenth and early nineteenth centuries illustrates this arrangement clearly: Indian merchants supplied local knowledge, capital, and extensive credit networks, while the EIC provided monopoly authority, military protection, and privileged access to global markets. The result was a system of “collusion to exploit,” in which the profits of imperial commerce were shared, though on markedly unequal terms.

Despite these constraints, certain commodities created opportunities for indigenous accumulation. Opium was one of the most significant among them. For Indian merchants, the opium trade became a major source of capital accumulation, generating substantial profits within the commercial networks of western and central India. These resources, combined with an already strong indigenous presence in regional trade, were later redirected into industrial investment, particularly in Bombay.

This comprador phase, however, contained the seeds of its own transcendence. Unprecedented capital accumulation within the opium trade created a class increasingly aware of its own power. This “class-in-itself”—defined by its objective economic position—gradually evolved into a “class-for-itself,” defined by subjective awareness of its collective interests and its growing conflict with foreign capital. The pivotal moment was the First World War and its aftermath.

The war weakened British capitalism, disrupted global markets, and opened new opportunities for indigenous enterprise. Simultaneously, the international stigmatization of the opium trade made that avenue of accumulation less viable. At this conjuncture, the Indian capitalist class decisively began to assert itself as a national bourgeoisie. Utilizing profits accumulated from decades of trade—including vast fortunes from the opium bazaars—capitalists, most notably Marwari firms, diversified out of the “bazaar” trade and into the organized industrial sector. They moved from being complementary to foreign capital to directly competitive with it. The Great Depression, while a global catastrophe, accelerated this process by eroding the foundations of expatriate British managing agencies and the European banks that controlled industrial finance.

The relationship between Indian merchant capital and British imperialism, however, was not static. It evolved in response to shifts in the global and colonial political economy. The end of EIC rule in 1858 and the establishment of direct Crown administration marked an important institutional transition, but a more decisive transformation occurred around the First World War. The war weakened British capitalism, disrupted global supply chains, and opened new opportunities for indigenous enterprise. At the same time, the opium trade faced growing international criticism, as well as increasing opposition from social reform movements within India. A commerce that had once underpinned imperial finance gradually became a moral and political liability (Brown, 2002).

VI. The Shifting Terrain of Empire and Capital: From Opium to Industry

British colonial rule pursued a dual strategy toward indigenous capital. It suppressed sections of the native bourgeoisie that could not serve colonial interests, while remould elements of the old merchant class and actively cultivating a new intermediary bourgeoisie to act as its agents. This policy unfolded within a deeper structural transformation: colonialism dismantled much of India’s incipient industry—including early manufactories in iron and steel, saltpetre, textiles, handlooms, and shipping where capitalist relations had begun to emerge—and ruptured the traditional link between agriculture and industry. Urban populations declined, traditional manufacturing centres decayed, and devastating famines became increasingly frequent under colonial rule (Siddiqui, 2018).

As British industrial capitalism gained ascendancy, earlier mercantilist priorities gave way to the demands of industrial capital. Under the new international division of labour consolidated in the nineteenth century, India was reconfigured primarily as a supplier of raw materials and a market for British manufactured goods, and as a region for British capital investment.

The domination of India’s external and internal trade by the British bourgeoisie accelerated the transformation of big Indian merchants into a comprador bourgeoisie, a process that had commenced long before colonial rule. Under these conditions, India’s transition toward capitalism confronted two formidable obstacles instead of one: the forces of colonialism combined with those of the pre-capitalist society to block the path of independent industrial development (Siddiqui, 2025a). Far from laying the material foundations for progress, British rule actively retarded India’s economic evolution. The stunted, lop-sided industrialization that did occur was not achieved by overcoming British opposition; rather, it was guided and fostered by British capital on terms favourable to imperial interests. Industrial capitalism in India did not emerge through the normal development of industry as it had in the Western Europe and Japan.

A second distinguishing feature of Indian industrial capitalism was that it grew not by defeating feudalism but by accommodating itself to it. A significant source of capital for Indian industries derived from the vast rents extracted from the peasantry by two parallel feudal formations: the despotic princely states (such as Gwalior, Mysore, Baroda, Indore, Travancore, Maharaja of Darbhanga, and others), which were responsible only to the British rulers. The rule of a foreign bourgeoisie and the persistence of a semi-feudal economy thus became the twin determinants shaping the course, character, and limits of Indian industrial development (Siddiqui, 2025b).

Thus, Indian colonial history reveals a crucial paradox at the heart of Indian industrial capitalism. The collaboration with the British bourgeoisie that enabled Indians to accumulate the capital for setting up cotton mills was many-sided and long-standing. The relationship was one of subordination, yet it generated the very resources that would later fund enterprises capable of competing with British capital (Siddiqui, 1996).

VII. Conclusion

The opium economy of the eighteenth and nineteenth centuries was not merely a sordid chapter in colonial history but a fundamental, if deeply controversial, engine of global commerce and primary capital accumulation. As this study has demonstrated, the trade formed the linchpin of a triangular system linking India, China, and Britain. Britain’s chronic trade deficit with China, driven by imperial demand for tea, was largely settled through the export of opium from India. In turn, these profits helped finance India’s colonial “tribute” to Britain, integrating the subcontinent into a global financial network on profoundly unequal terms. The expansion of this trade through Bombay was crucial to the city’s transformation into a leading imperial port.

The profits accumulated through this collaboration were immense and would prove foundational for subsequent Indian industrial development. Prominent business houses that would later lead India’s industrialisation—most notably the Tatas, Sassoons and, subsequently, the Birlas—amassed their initial fortunes through active participation in the opium trade. This pattern was widespread: the first Indian cotton mill companies in Bombay were floated by Parsi families such as the Davars and Petits, who had long been associated with British capital as brokers, sahukars, and agents. The textile magnates who dominated Bombay’s industrial landscape—the Sassoons (a Baghdadi Jewish family that emigrated to Bombay in the early 1830s before later settling in England), the Currimbhoys, the Petits, the Wadias, and the Tatas—were all intimately tied to British commercial and financial interests. Jamsetji Tata, for instance, established his first cotton mill not as a break from this collaborative past but as its logical extension, capitalising on the fortunes, networks, and expertise acquired through decades of intermediary commerce (Harris, 1958).

Crucially, profits from opium were not simply consumed but strategically reinvested by Indian merchants. The EIC’s monopoly created a protected, highly profitable environment that communities like the Parsis, Marwaris, and Baghdadi Jews learned to navigate. By securing contracts and managing complex supply chains, they amassed fortunes that funded their later transformation from traders into industrialists. The houses of the Sassoons, for instance, directly reinvested opium wealth into cotton textiles, steel, and hydroelectric power.

This paradox lies at the heart of colonial capitalism: the same illicit commodity that drained China and enriched the British Empire also underwrote the emergence of indigenous capitalist enterprise in India. The merchants who entered this trade were not novices but heirs to a sophisticated commercial tradition. Yet they operated within a system in which the colonial state functioned simultaneously as partner and master.

As the opium trade came under mounting pressure in the late nineteenth century, these merchants strategically pivoted toward new industries. Their ascent, however, was not entirely autonomous. The networks forged with foreign capital during the opium trade remained indispensable, providing privileged access to technology and global markets. Profits accumulated under empire thus paradoxically financed an industrial base that would later challenge British economic dominance.

Seen in this light, the opium trade appears not as a peripheral vice but as a central—if morally fraught—pillar in the making of modern Indian capitalism. To overlook this is to miss how Bombay emerged as a global commercial center, its industrial foundations seeded, in part, in the poppy fields of Malwa, Ghazipur, Banaras, and Bengal.

About the Author

Dr. Kalim Siddiqui is an economist specializing in International Political Economy, Development Economics, Trade and Economic Policy. Since 1989, he has been teaching economics at various universities in Norway and the UK. Dr. Siddiqui’s research interests encompass a wide range of topics, including political economy, international trade, and economic history, South Asia, and emerging economies. He has presented papers at international conferences across numerous countries, reflecting his global engagement in the field. His scholarly pursuits span six broad domains: Political Economy, Development Economics, Economic History, Economic Policy, Globalization, and International Trade. Dr. Siddiqui has made significant contributions to research in areas such as trade policy, globalization, and political economy. His work has been published in chapters of edited books and articles published in peer-reviewed journals. For inquiries, Dr. Siddiqui can be reached at: [email protected]

Dr. Kalim Siddiqui is an economist specializing in International Political Economy, Development Economics, Trade and Economic Policy. Since 1989, he has been teaching economics at various universities in Norway and the UK. Dr. Siddiqui’s research interests encompass a wide range of topics, including political economy, international trade, and economic history, South Asia, and emerging economies. He has presented papers at international conferences across numerous countries, reflecting his global engagement in the field. His scholarly pursuits span six broad domains: Political Economy, Development Economics, Economic History, Economic Policy, Globalization, and International Trade. Dr. Siddiqui has made significant contributions to research in areas such as trade policy, globalization, and political economy. His work has been published in chapters of edited books and articles published in peer-reviewed journals. For inquiries, Dr. Siddiqui can be reached at: [email protected]

References

- Brown, R.H. (2002) “The Opium Trade and Opium Policies in India, China, Britain, and the United States: Historical Comparisons and Theoretical Interpretations” Asian Journal of Social Science 30(3):623-656.

- Calangutcar, A. (2007) “Marwaris in Opium Trade: A Journey to Bombay in the 19th Century” Proceedings of the Indian History Congress, 67:745-753

- Farooqui, A. (2021) “The Opium Trade” Oxford Research Encyclopaedia of Asian History, Oxford.

- Farooqui, A. (1996) “Urban Development in a Colonial Situation: Early Nineteenth Century Bombay” Economic and Political Weekly 31(40):2746-2759

- Ghosh, A. (2008) Sea of Puppies, New Delhi, Viking Press.

- Guha, A. (1984) “More about the Parsi Seths: Their Roots, Entrepreneurship and Comprador Role, 1650-1918” Economic and Political Weekly, January 21.

- Habib, I. (2022) Indian Economy Under Early British Rule, 1757-1857, New Delhi : Tulika Books.

- Harris, F.R. (1958) Jamsetji Nusserwanji Tata, Bombay.

- Palsetia, J. (2008) “The Parsis of India and the opium trade in China”, Contemporary Drug Problems 35, pp.647-678, Winter.

- Sassoon, J. (2022) The Global Merchants: The Enterprise and Extravagance of the Sassoon Dynasty, London: Allan Lane.

- Siddiqui, K. (2025a) “Decolonisation and Economic Sovereignty: The Bandung Conference and the Making of the Global South” World Financial Review, June.

- Siddiqui, K. (2025b) “Geopolitics and the Persistence of Global Uneven Development: A Critical Analysis” World Financial Review, July.

- Siddiqui, K. (2024a) “The Multinational Corporations, Capitalism, and Imperialism: The Case Study of East India Company” World Financial Review, July.

- Siddiqui, K. (2024b) “Economic Drain from India during the British Rule” World Financial Review, December.

- Siddiqui, K. (2024c) “Hindu Nationalism and the Rise of RSS in India” World Financial Review, September.

- Siddiqui, K. (2020a) “Britain’s Trade with China in the Eighteenth and Nineteenth Century: A Review of the Opium Wars” Asian Profile, 48(3):206-221, September.

- Siddiqui, K. (2020b) “The Political Economy of Famines under Colonial India: A Critical Analysis” World Financial Review, July/August.

- Siddiqui, K. (2019) “The Political Economy of Global Inequality: An Economic Historical Perspective” Argumenta Oeconomica Cracoviensia, 21(2):11-42.

- Siddiqui, K. (2018) “The Political Economy of India’s Economic Changes since the last Century” Argumenta Oeconomica Cracoviensia, 19:103-132.

- Siddiqui, K. (2016) “The Economics and Politics of Hindu Nationalism in India” Asian Profile 44(6):497-507. ISBN: 03048675.

- Siddiqui, K. (1996) “Growth of Modern Industries under Colonial Regime: Industrial Development in British India between 1900 and 1946”, Pakistan Journal of History and Culture 17(1):11 – 59, January.

- Subramanian, L. (2017) “Parsi Traders in Western India, 1600–1900” Oxford Research Encyclopaedia of Asian History, Oxford.

Dr. Dan Steinbock

Dr. Dan Steinbock Dr. Gleb Tsipursky

Dr. Gleb Tsipursky Dražen Kapusta

Dražen Kapusta