")

Dr. Kalim Siddiqui analyzes Donald Trump’s aggressive trade strategies, exploring how the US’s tariff policies are contributing to an emerging global trade war. The article highlights the geopolitical and economic consequences for the US, China, and the broader global landscape.

I. Introduction

The United States (US) perceives China’s economic rise as a challenge to its global dominance. As a hegemonic power, the US is reluctant to accept a rival capable of undermining its influence. In response, it has imposed tariffs and restrictions on China’s access to the high-tech sector, where the US maintains a near-monopoly.

Historically, China was an impoverished country in the 1970s, characterized by a predominantly agrarian population, low productivity, minimal industrialization, and limited investment. During the Cold War, the US sought to divide the Soviet Union and China by offering China economic incentives, including access to Western capital, technology, and markets. This strategy aimed to weaken the Soviet Union, particularly by drawing it into prolonged conflicts such as the war in Afghanistan—ultimately contributing to its collapse (Siddiqui, 2023a).

Trump’s “Make America Great Again” agenda, which includes imposing tariffs on key trading partners, is unfolding in a global economic environment characterized by stagnating demand. This stagnation is largely driven by globalized finance capital, which resists fiscal deficits and higher taxation on the wealthy. Consequently, Trump’s tariff policies are likely to exacerbate the broader capitalist crisis (Siddiqui, 2025), fuelling rapid inflation and intensifying trade wars—disproportionately impacting the Global South (Siddiqui, 2023b).

Tariffs function as a tax on imports, intended to encourage domestic production, create jobs, and reduce reliance on foreign markets. However, their effectiveness remains a subject of debate. In the current US context, it is doubtful that tariffs alone will lead to meaningful reindustrialization. Over the past four decades, under neoliberal globalization, US industries have relocated to China and other East Asian countries, where wages are lower and labour forces are more disciplined. Beyond tariffs and protectionist measures, successful industrial revitalization also requires competitive wages, a skilled labour force, and high returns on investment to attract capital.

Adam Tooze highlights strong parallels between Trump and Biden in their approach to economic nationalism. While Trump’s first administration pledged to “Make America Great Again” by reshoring industry, it was Biden who implemented concrete policies such as the CHIPS Act. This legislation subsidized semiconductor manufacturers under the condition that they refrain from producing cutting-edge chips in strategic rival nations like China (Tooze, 2018; Siddiqui, 2024a).

II. The US-China Rivalry: A Shift in Global Trade and Power

Barack Obama initiated discussions on China’s rise and strategies for containing it. Donald Trump accelerated this approach during his first term by imposing tariffs on US imports from China. However, despite his criticism of Trump’s trade policies, Joe Biden largely maintained these tariffs while expanding restrictions, particularly on electric vehicles, solar cells, and semiconductor chips. For Biden, China is the primary geopolitical rival, with conflicts in Ukraine and the Middle East viewed as secondary concerns. Trump has proposed trade policies includeing imposing 25% tariffs on goods from Mexico and Canada, 60% tariffs on Chinese imports, and 10% tariffs on imports from all other countries.

The US and European corporations historically viewed China’s abundant, low-cost, and disciplined labour force, as well as its access to inexpensive raw materials, as a means to maximize profitability. By outsourcing production to China and other developing nations, multinational corporations (MNCs) aimed to maintain control over higher-value activities such as product design, innovation, and research and development—securing monopoly profits in the process (Sweezy, 1990). Meanwhile, lower-value segments of the supply chain, characterized by intense competition and minimal profit margins, were left to China and other emerging economies. This strategy aligned with the principles of globalization, benefiting Western consumers through lower prices while allowing corporations to capitalize on cost-efficient production.

However, MNCs sought to restrict technology transfer, fearing that advancements in developing countries would erode their economic advantage. This approach echoed historical colonial structures, in which profitable industries and plantations were concentrated in the hands of European powers, while high-competition, low-margin activities were relegated to the colonies. The assumption underpinning globalization was that China would remain confined to low-value production. However, this strategy has not unfolded as anticipated. China has rapidly advanced its technological capabilities, industrialized at an unprecedented pace, and significantly increased productivity. Consequently, Western elites now perceive a major threat to their long-standing dominance over global resources—a dominance that has persisted for nearly four centuries (Siddiqui, 2022).

As the world shifts toward multipolarity, the US is actively working to curtail China’s access to cutting-edge technology and prevent its emergence as an independent economic powerhouse.

III. The Self-Defeating Nature of US Protectionism

It appears that US protectionism will ultimately backfire. China’s economy remains in a strong position, as it is a low-cost producer of cutting-edge technology that the world increasingly relies on. Chinese firms such as BYD in electric vehicles, DeepSeek in AI, and advancements in 5G technology exemplify China’s growing dominance in key industries. Ironically, rather than weakening China, US protectionist policies may have the opposite effect—strengthening China’s economy while pushing it closer to the rest of the world.

Historically, open trade between the US and China has been mutually beneficial. However, the US strategy to contain China is unlikely to succeed. In terms of purchasing power parity (PPP), China’s economy is already larger than that of the US with a population of 1.4 billion—nearly four times larger than the US population of 330 million—China has a significant long-term economic advantage. Moreover, China’s annual economic growth continues to outpace that of the US, ensuring that its economy will expand further in the years to come.

China’s strength lies in its ability to produce advanced technology at lower costs, making it an attractive partner for developing countries. As a result, many countries in the Global South seek closer economic ties with China, benefiting from its innovation and manufacturing capabilities. This undermines the US strategy of containment, which lacks widespread support outside of its traditional Western allies.

Furthermore, the rise of artificial intelligence (AI) presents both opportunities and risks. AI should serve humanity rather than replace human labour. However, there is a growing danger that AI will contribute to the centralization of corporate power, increasing surveillance and control in the hands of a few private firms. This concentration of power could also accelerate the militarization of AI through autonomous weapons, reducing human oversight in warfare—an alarming prospect.

Unlike the Soviet Union, which was never an economic competitor to the US, China has emerged as a true economic powerhouse. While the Soviet Union’s challenge to the US was primarily military, China’s strength lies in its economic and technological advancements. After World War II, the European economies were devastated, allowing the US to rise as the dominant global economic power without any real rivals. However, China’s rapid industrialization and technological progress have now positioned it as a formidable economic force, even though it remains militarily weaker than the US. The US is waging a new Cold War against China. While US military bases encircle China, China has no military presence in Mexico or Canada. Meanwhile, China has even developed an alternative to the US-led SWIFT international payment system, providing emerging economies with new options for financial transactions.

One of the US’s key claims is that China is attempting to “take over” Taiwan. However, this contradicts historical US policy. When President Nixon visited China in 1972, the US formally recognized the One China Policy, acknowledging Taiwan as part of China—similar to Hong Kong. Even under President Clinton, when China was invited to join the World Trade Organization (WTO), Taiwan was not a point of contention. However, as China’s rapid economic growth and technological advancements have increased its share in high-tech industries, the US now perceives China as a threat to its global hegemony. A fundamental difference between the two economic systems is that in the US, capitalist-controlled banks allocate investments based on private interests. In contrast, China’s government exerts control over its central bank and plays a direct role in guiding investment decisions. This political advantage allows China to implement long-term economic strategies.

IV. The Reciprocal Tariff Dilemma

The US is also pursuing aggressive tariff policies, but these could have unintended economic consequences. Mexico, for instance, is highly dependent on trade with the US, exporting 80% of its goods to American markets. In 2024, the US imported $558 billion worth of goods from Mexico while exporting $334 billion, creating a $178 billion trade deficit in Mexico’s favour. If the US imposes tariffs on Mexican imports, Mexico has already threatened reciprocal measures that would particularly impact American agriculture, the automotive industry, and electronics. In response, US automakers and agricultural lobby groups have strongly opposed these tariffs, fearing that higher consumer prices will fuel inflation.

China, too, has decided to retaliate against US tariffs, which could further harm the American economy. The US seeks to eliminate competition in industries where it holds near-monopoly power (Siddiqui, 2019a). However, China’s participation in BRICS, a bloc representing 50% of the world’s population, challenges US economic dominance (Siddiqui, 2016). In contrast, the US accounts for only 4% of the global population.

India also has significant trade ties with the US, with bilateral trade reaching $125 billion. If tariffs are imposed on Indian goods, prices are expected to rise by 4.9%. Currently, US imports from India face an average tariff rate of 2.8%, whereas US exports to India are subject to a 7.7% tariff. If India were to impose reciprocal tariffs, the additional cost to Indian goods entering the US would be around 4.9%. The impact of tariffs varies across sectors. The US farm sector would suffer if Indian agricultural imports awere allowed to enter at lower tariffs, undercutting American producers. Meanwhile, US imports of auto parts, processed foods, meat, diamonds, gold and jewellery, chemicals, and pharmaceuticals from India would be significantly affected by rising tariff rates.

V. The Economic Fallout of US Tariffs and Changing Global Dynamics

An increase in tariffs raises the cost of US imports. Since many of these products are price-sensitive or elastic, higher prices will lead to a decline in import demand. In the agricultural sector, the US benefits from heavy government subsidies, allowing its agro-food processing giants to compete aggressively in global markets. If US agribusinesses gain unrestricted access to the Indian market, they could undermine small and family farms, leading to widespread displacement. Currently, about 45% of India’s population is employed in agriculture, and removing protective measures against global agribusiness would cause massive impoverishment in rural areas (Siddiqui, 2023c).

The US appears to be shifting its economic narrative. While neoliberalism once championed unrestricted trade as beneficial to all parties, a new discourse has emerged—one defined by protectionism and echoes of colonial economic dominance. The notion of exerting control over Panama, Greenland, and even Canada reflects a broader trend of US economic and geopolitical assertiveness. Imposing tariffs raises production costs, which are inevitably passed on to consumers. Additionally, global supply chains are becoming increasingly uncertain, disrupting production structures and trade relations worldwide.

For decades, the US operated under the assumption that its companies would maintain dominance over the upper segments of the value chain—including product design, research and development, and innovation—allowing them to sustain monopoly profits and economic rents (Sweezy, 1990). Meanwhile, it was believed that the lower-value segments, such as mass production, would remain in China and other developing countries. Intense competition at this lower end of the value chain was expected to keep costs low, ensuring higher returns on investment for Western companies (Siddiqui, 2021).

This strategy closely resembled colonial-era economic divisions, where the core (the colonizers) controlled profitable sectors like plantations and mining, while manufacturing was concentrated in European hands. The periphery (the colonies) was relegated to low-value production, which was highly competitive and, therefore, unattractive to Western investors. This colonial mindset persisted into the era of globalization, as the US sought to maintain a similar structure. However, this strategy did not unfold as planned (Siddiqui, 2022).

China has successfully developed advanced technology, modernized its industrial base, and increased productivity, challenging Western dominance in key industries (Siddiqui, 2018). In response, the West now perceives China as an existential threat to its four-century-long control over global resources. As economic power shifts and multipolarity takes hold, the US is facing the reality that its era of unchallenged global supremacy is coming to an end (Siddiqui, 2020)

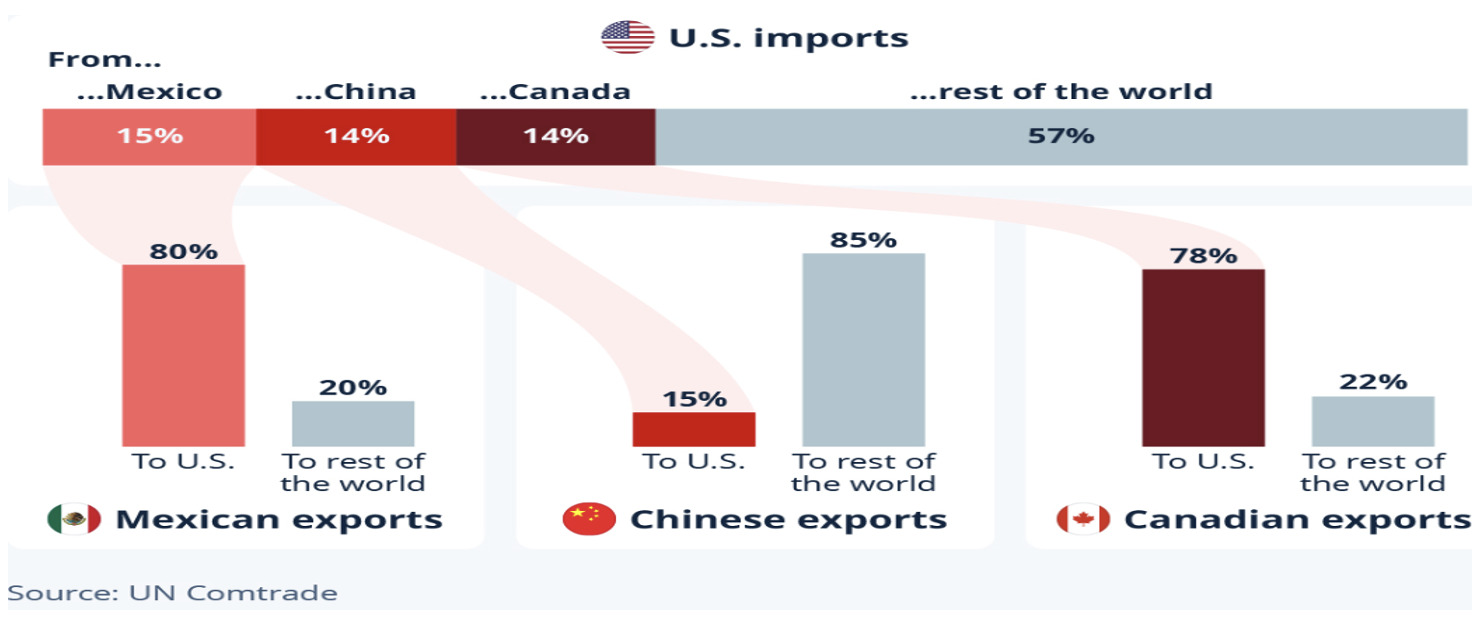

Figure 1 shows that in 2024, the US imports from Mexico, Canada, and China accounted for 15%, 14%, and 14% of its total imports, respectively—nearly half of the country’s total imports. For Mexico, the US market is crucial, with approximately 80% of its total exports destined for the US. Similarly, 78% of Canada’s total exports go to the US, making it a vital trade partner.

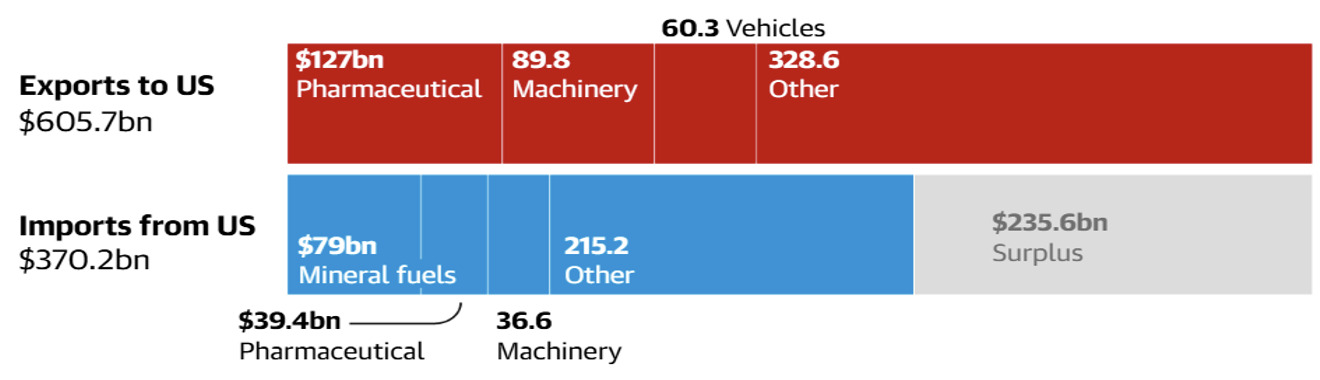

In contrast, the US market is less significant for China, which sends only 15% of its total exports to the US, while 85% of Chinese exports are directed to other global markets. This indicates that China has successfully diversified its export destinations, reducing its dependence on US trade. Figure 2 highlights US-EU trade dynamics in 2024, showing that the European Union exported US$ 605.7 billion worth of goods to the US, while US exports to the EU amounted to US$ 370.2 billion. This results in a trade surplus in favour of the EU.

Figure 1: US Trade with Mexico, Canada, and China in 2024 (%).

Figure 2: Trade between the EU and US in 2024. (US$ billion).

In 2023, Canada’s global agricultural exports totalled approximately $69.2 billion, while agricultural imports amounted to $48.2 billion, based on the WTO’s definition of “agricultural products” applied to Canadian trade statistics. The US is Canada’s largest agricultural trading partner, accounting for 60.3% of Canada’s agricultural exports and supplying 56.8% of its agricultural imports. In 2023, Canada represented 16.3% of US agricultural exports and 20.6% of US agricultural imports, highlighting the deep trade relationship between the two countries. Nearly half of all US imports-over US$ 1.3 trillion-come from Canada, China, and Mexico. While the tariffs could generate an additional US$ 100 billion annually in federal tax revenue, they will also impose significant costs on the broader economy. These include disrupting supply chains, raising business costs, eliminating hundreds of thousands of jobs, and ultimately driving up consumer prices in the US (The Guardian, 2025).

This strong integration between the US and Canadian agricultural sectors is due to the North American Free Trade Agreement (NAFTA) in 1994. NAFTA eliminated nearly all tariff and quota barriers to Canada-US agricultural trade, with a few exceptions. The US maintained restrictions on imports of dairy products, peanuts, peanut butter, cotton, sugar, and sugar-containing products, while Canada continued to impose restrictions on imports of dairy products, poultry, eggs, and margarine. In November 2018, Canada, Mexico, and the US signed the US-Mexico-Canada Agreement (USMCA), it preserved NAFTA’s provisions for tariff- and quota-free agricultural trade between the US and Canada while expanding market access for US dairy, poultry, and egg exports to Canada. In 2023, US agricultural exports to Canada and US agricultural imports from Canada grew at compound annual rates of 5.7% and 6.9%, respectively, reflecting the continued strength of the trade partnership under USMCA (The Guardian, 2025).

VI. US-China Economic Relations: From Cooperation to Containment

The US welcomed China into the WTO, recognizing the immense economic opportunities China presented. With its vast market and abundant low-cost labour, China helped keep inflation low in the US, boost corporate profits, and enhance US competitiveness. Geopolitically, integrating China into the global capitalist system was seen as a way to reduce its potential as a strategic threat (Siddiqui, 2015).

However, recent US opposition to China stems from a desire not only for relative economic and military dominance but for absolute power. Militarily, China remains weaker than the US and has not exhibited expansionist tendencies. In contrast, the US maintains approximately 750 military bases worldwide, including 200 in Asia, while China has no overseas military bases. Despite this disparity, the US seeks to contain China both militarily and technologically, but without fully “decoupling” from its economy.

China has mitigated the loss of the American market by significantly expanding its domestic economy. Unlike other countries, China has managed this because, despite market-oriented reforms, it remains fundamentally a command economy. The Chinese government retains significant influence over economic decisions, supported by a strong public sector and state-owned enterprises that allow for strategic investment.

By contrast, the US economy heavily relies on government deficits to absorb surplus capital. The combination of large fiscal deficits and slow economic growth has led to rising debt-to-GDP ratios, raising concerns about long-term sustainability (Siddiqui, 2019b). Meanwhile, China’s economy has primarily relied on private-sector investment, but its overinvestment has lowered returns on new capital, presenting its own set of economic challenges.

VII. Manufacturing Decline in the US: The Limits of Protectionism

Employment in US manufacturing peaked in June 1979. Since then, the most recent data from January 2025 indicate a 35% decline in manufacturing employment, amounting to a loss of more than a third of the workforce. While offshoring has played a role, the primary reasons for this decline are productivity gains, automation, and the adoption of labour-saving technologies.

By imposing tariffs on imports from China, India, and the EU will help revitalize US industries. However, this claim is misleading. Several key points must be considered: Protectionism without financial regulation is Ineffective. Despite his rhetoric, Trump has never proposed restricting the free flow of international finance capital, a core element of the neoliberal economic order. Without such measures, corporations will continue prioritizing offshore investments, seeking higher returns in countries with lower production costs. Tariffs may reduce dependence on foreign imports and marginally boost domestic production, but they do not inherently expand the overall size of the US market. For meaningful economic growth, the government must increase state expenditures, which can only be financed through higher fiscal deficits or increased taxation on the wealthy. Ultimately, while protectionism may shift production patterns, it cannot reverse decades-long trends in deindustrialization without complementary policies such as industrial investment, workforce retraining, and fiscal stimulus.

VIII. Conclusion

Donald Trump’s mercantilist trade strategy, aimed at reviving US manufacturing, is unlikely to succeed. Imposing tariffs alone cannot restore the manufacturing sector, as it overlooks other crucial factors such as industrial policy, wages, productivity, exchange rates, and the availability of a skilled workforce. By attempting to restrict imports, Trump risks triggering retaliation, sharp rise in prices, supply chain disruptions, and a deeper economic crisis. This approach could spiral into full-scale trade wars, further exacerbating the global capitalist crisis (Siddiqui, 2024b). Additionally, capital inflows have surged, and both trade and financial movements have become increasingly sensitive to geopolitical tensions.

The internationalization of capital has further complicated relationships between states, corporations, and financial markets—realms over which governments have limited control. The immense concentration of capital has strengthened the dominance of multinational corporations (MNCs), particularly in key industries where they continue to consolidate power. As Karl Marx observed, the “concentration and centralization” of capital is accelerating, deepening economic inequalities and reinforcing global capitalist structures.

For capitalism, the era of boom-and-bubble cycles has ended, giving way to long-term economic stagnation. Since the 2008 financial crisis, economic growth has remained sluggish, unemployment persistent, and wages stagnant, while income and wealth inequality have widened dramatically. Over a century ago, Rosa Luxemburg warned that capitalism’s trajectory would ultimately force humanity to choose between socialism and barbarism. Today, her warning has become disturbingly relevant. Neoliberal capitalism—the latest phase of the system—has not only reached a dead end but has also fuelled the rise of pervasive neo-fascism. The only viable path forward is to reverse the growing income and wealth inequality, create employment, and boost productivity through a transition toward publicly owned enterprises with greater democratic accountability. Controlling multinational corporations (MNCs) and financial oligarchies is crucial to addressing this systemic crisis.

With no significant investment drivers—such as transformative innovations like the automobile or computers, or large-scale government spending—modern capitalist economies have increasingly relied on financialization to generate profits. While financial markets provided a temporary reprieve from stagnation, they have ultimately contributed to declining growth rates and employment. Instead of being reinvested into productive industries, economic surpluses are increasingly funnelled into speculative financial instruments, exacerbating inequality and deepening economic instability.

The contradictions of the global financial order are particularly evident in the selective enforcement of economic principles by institutions like the IMF, World Bank, and WTO. These institutions have remained conspicuously silent on Trump’s protectionist policies while continuing to pressure the Global South to adhere to free trade doctrines, preventing them from implementing similar measures. At the same time, they advocate for strict fiscal deficit limits while opposing higher taxation on the wealthy, claiming that such policies would deter capital inflows. This hypocrisy underscores the deep structural biases that serve the interests of financial elites rather than fostering equitable global economic development.

About the Author

Dr. Kalim Siddiqui is an economist specializing in International Political Economy, Development Economics, Trade and Economic Policy. Since 1989, he has been teaching economics at various universities in Norway and the UK. Dr. Siddiqui’s research interests encompass a wide range of topics, including political economy, international trade, and economic history, South Asia, and emerging economies. He has presented papers at international conferences across numerous countries, reflecting his global engagement in the field. His scholarly pursuits span six broad domains: Political Economy, Development Economics, Economic History, Economic Policy, Globalization, and International Trade. Dr. Siddiqui has made significant contributions to research in areas such as trade policy, globalization, and political economy. His work has been published in chapters of edited books and articles published in peer-reviewed journals. For inquiries, Dr. Siddiqui can be reached at: [email protected]

Dr. Kalim Siddiqui is an economist specializing in International Political Economy, Development Economics, Trade and Economic Policy. Since 1989, he has been teaching economics at various universities in Norway and the UK. Dr. Siddiqui’s research interests encompass a wide range of topics, including political economy, international trade, and economic history, South Asia, and emerging economies. He has presented papers at international conferences across numerous countries, reflecting his global engagement in the field. His scholarly pursuits span six broad domains: Political Economy, Development Economics, Economic History, Economic Policy, Globalization, and International Trade. Dr. Siddiqui has made significant contributions to research in areas such as trade policy, globalization, and political economy. His work has been published in chapters of edited books and articles published in peer-reviewed journals. For inquiries, Dr. Siddiqui can be reached at: [email protected]

References

- The Guardian (2025) “Canada announces retaliatory tariffs on nearly $30bn worth of US imports”, March 13, London.

- Siddiqui, K. (2025) “The Political Economy of Germany’s Deepening Economic Crisis” World Financial Review, February.

- Siddiqui, K. (2024a) “Trends and Prospects of De-Dollarization in the Rapidly Changing Global Economy”, Part One and Part Two, World Financial Review, December.

- Siddiqui, K. (2024b) “The Decline of the West and Global Political Economy”, World Financial Review, December.

- Siddiqui, K. (2024c) “Revisiting the Japan’s Economic Stagnation”. World Financial Review, February.

- Siddiqui, K. (2023a). “The New Cold War: Struggle for Global Domination” (Part I & Part 2) World Financial Review, June, p.6 – 17 & August.

- Siddiqui, K. (2023b). “World Trade Organization” p. 631 – 637, Elgar Encyclopaedia of Development, Edward Elgar.

- Siddiqui, K. (2023c) “Marxian Analysis of Capitalism and Crises”, International Critical Thought, 13(4): 525-545.

- Siddiqui, K. (2022) “Capitalism, Imperialism, and Crisis”, European Financial Review, June-July.

- Siddiqui, K. (2021) “Trade Liberalisation, Comparative Advantage, and Economic Development: A Historical Perspective” World Financial Review, May-June.

- Siddiqui, K. (2020) “Prospects of a Multipolar World and the Role of Emerging Economies” World Financial Review, November-December.

- Siddiqui, K. (2019a). “The US Economy, Global Imbalances under Capitalism: A Critical Review” Istanbul Journal of Economics 69(2): 175 – 205, December.

- Siddiqui, K. (2019b). “Financialisation, Neoliberalism and Economic Crises in the Advanced Economies” World Financial Review, May-June

- Siddiqui, K. (2018). “US – China Trade War: The Reasons Behind and its Impact on the Global Economy” World Financial Review, November-December.

- Siddiqui, K. (2016). “Will the Growth of the BRICs Cause a Shift in the Global Balance of Economic Power in the 21st Century?” International Journal of Political Economy 45(4): 315 – 338.

- Siddiqui, K. (2015). “Trade Liberalisation and Economic Development: A Critical Review” International Journal of Political Economy 44(3): 228 – 247.

- Sweezy, P.M. (1990) “Monopoly Capitalism”, Marxian Economics, (Eds) John Eatwell, Murray Milgate and Peter Newman, London: Macmillan.

- Tooze, A. (2018) Crashed: How a decade of financial crises changed the world. New York: Viking.

")

{kind=link}