By Justin Yifu Lin & Volker Treichel

Four years after the beginning of the global financial crisis, the protracted sovereign debt crisis in the eurozone is a looming threat to the recovery of the world economy and could lead to a renewed global financial crisis. While fiscal profligacy on the part of periphery countries has been viewed by many analysts as the root of the ongoing crisis, this paper argues that the impact on capital flows within the eurozone of financial deregulation and liberalization and of the adoption of the common currency was critical in exacerbating a growing competitiveness gap between core and periphery countries and explaining the evolution of the crisis.

The collapse of Lehman Brothers about four years ago marked the beginning of the most severe economic crisis since the Great Depression. While the sluggish recovery in 2010 and 2011—driven primarily by growth in emerging markets—seemed to promise a silver lining on the horizon, stubbornly high unemployment and weak housing markets in many advanced countries have dampened demand and underscore risks to achieving a self-sustained recovery. Most importantly, the protracted sovereign debt crisis in the eurozone is a looming threat to the recovery of the world economy and could lead to a renewed global financial crisis. What have been the root causes of the crisis in Europe? How important has the global financial crisis been for the evolution of the crisis relative to factors internal to Europe, especially the adoption of the Euro?

The crisis in Europe began when financial markets lost confidence in the creditworthiness of Greece and other periphery countries and interest rates on government bonds soared to levels that forced the governments of these countries to seek bailouts from the international community, including the European Community and the IMF. Rising risk premia on government bonds reflected the reaction of financial markets to over-borrowing by private households, the financial sector and governments in periphery countries of the eurozone. As fears of government default were the main trigger of the crisis, many analysts came to the conclusion that the crisis itself was caused by fiscal profligacy in periphery countries, driven by the construction of an elaborate welfare state and rising public sector wages. Consequently, these analysts argue, periphery countries’ commitment to fiscal discipline will allow Europe’s currency to regain strength, without further need for fiscal stimulus. Among European countries, Germany is a particularly strong proponent of the view that fiscal austerity is crucial to addressing the crisis, and under its influence, the G20 Toronto summit in June 2010 established fiscal consolidation as the new policy priority.

Yet, a deeper analysis of the dynamics underlying the current Euro crisis shows that financial deregulation and liberalization was a major cause of the crisis in periphery countries in the eurozone. Much like in the United States, financial deregulation and liberalization encouraged the development of new financial instruments and derivatives and allowed banks in core eurozone countries to increase leverage and boost loanable funds, spurring a real estate and consumption boom. This boom was also made possible by the adoption of the Euro in the context of greater European financial and economic integration, which lowered the currency risk in periphery countries and permitted interest rates to converge towards the much lower level in core countries. Both financial deregulation and the fall in interest rates contributed to large inflows of capital from core countries into periphery countries and led to housing bubbles and excess consumption. Increased lending from core eurozone countries also occurred in countries outside the eurozone, such as Iceland, Hungary and other countries in Eastern Europe. Abundant credit from core countries triggered an economic boom in the periphery countries, driven largely by rising consumption. Given that the boom initially helped increase fiscal revenue, deficits could remain in line with the Maastricht criteria (except for Greece), in spite of the fact that government expenditure rose rapidly due to increasing government wage bills and social transfers. Yet, with rising wages and growth increasingly driven by unsustainably high domestic consumption, periphery countries lost export competitiveness and the manufacturing sector declined. At the same time, core countries’ competitiveness and their external surpluses improved, as a result of wage restraint and the relative undervaluation of the Euro compared to the earlier national currencies.

The global financial crisis since September 2008 led to a recession in Europe and triggered the burst of the real estate bubble. Both the recession and the adoption of fiscal stimulus packages to counteract it as well as the burst of the real estate bubble resulted in a ballooning of fiscal deficits and a massive deterioration of debt indicators that set the stage for the sovereign debt crisis in the eurozone that began with the Greek crisis in early-2010.

A deeper look at the dynamics between core countries, especially Germany, and non-core countries in the eurozone shows a certain analogy to that between East Asian surplus economies and the United States in the run-up to the global financial crisis. Excess consumption in the United States brought about by a real estate boom and low interest rates allowed East Asian countries to expand their exports, until the burst of the real estate bubble and the ensuing crisis of the financial sector triggered a global recession. The consumption boom in the United States went hand in hand with a decline in the competitiveness of the US economy, particularly in the manufacturing sector.

Financial integration and deregulation in the eurozone

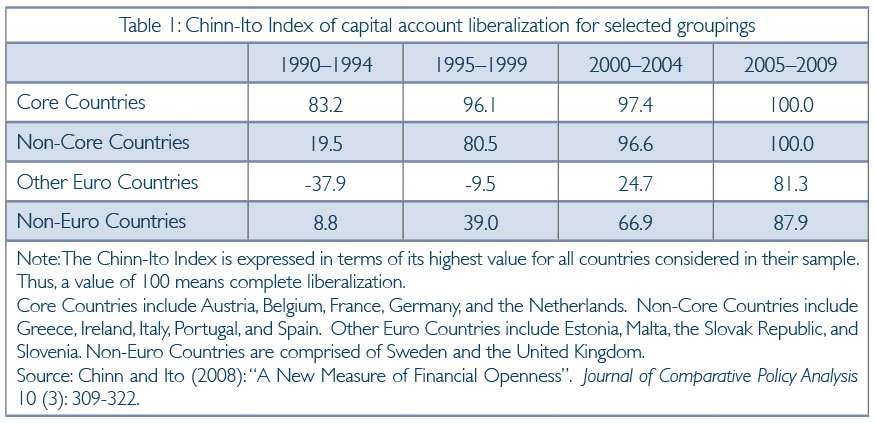

Europe has pursued greater financial integration since 1957, but these efforts gained significant steam in 1999 with the adoption of a five-year financial harmonization program—the Financial Services Action plan (FSAP). The Chinn-Ito index in the table below shows that both core and non-core countries reached the status of full liberalization after the adoption of the Euro in 2002 (Table 1), spurring an increase in capital flows across Europe.

But like in the United States, capital flows also benefited from financial deregulation and liberalization, and mostly occurred from core to periphery countries. Total claims by core countries on non-core countries increased by 433 percent from 1999 to the peak in 2008. Demonstrating the importance of financial deregulation, countries outside the eurozone were also significant recipients of lending from core countries. In two striking cases, core bank claims on Iceland increased by 1113 percent over the same period, while core bank claims on Hungary increased by 603 percent.

Increased lending by core country banks was made possible by the dramatic rise in leverage ratios, measured as total assets over total equity, for these lending institutions, peaking in 2007 at 33 to 1. Like in the United States, this increase in leverage was encouraged by the creation of derivatives whose risk profile could not be properly assessed. At the same time, risk management was weakened through the shadow banking system that was only marginally under the supervision of bank regulatory authorities.

In fact, off-balance sheet bank leverage increased rapidly and significantly contributed to the buildup of financial leverage prior to the crisis of 2007. Many segments of the asset-backed commercial paper markets, such as structured investment vehicles, collateralized debt obligations, single-sell ABCP conduits, and securities arbitrage programs grew exponentially during this timeframe in both the United States and Europe. Covered bonds played an important role in increasing leverage, especially in Spain, where the amount outstanding increased from less than €10 billion in 2000 to more than €125 billion in 2005. Crucial to this increase in volume was legislation allowing for low risk weighting for this class of assets, permitting to take on greater exposure to liquidity risk. These higher leverage ratios amplified the rate of return to assets for core countries during the run–up to the crisis.

But it was not only financial deregulation and liberalization that brought about a boom in lending from core to periphery countries. Crucial in intensifying these capital flows was also the adoption of the common currency. The importance of the Euro can be demonstrated by differences in financial indicators between eurozone countries on the one hand and European countries on the other hand that did not use the Euro: Among eurozone countries, bilateral bank holdings and transactions increased by roughly 40 percent following the adoption of the Euro. In contrast, bank holdings and transactions only increased by 25 to 30 percent if the three countries that did not adopt the Euro (the United Kingdom, Denmark and Sweden) are included with the eurozone countries. The increase in transactions was thus significantly smaller in countries not using the Euro, underscoring the impact of the common currency.

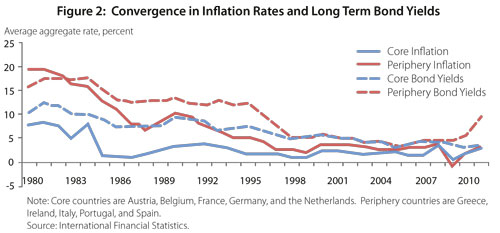

Why did the adoption of the Euro have such a significant impact on the volume of financial transactions? Mainly, because it eliminated the currency risk and led to the convergence of interest rates in periphery countries to the much lower level of core countries (Figure 2). No other effect of the adoption of the Euro was more consequential for the structure of European economies than this rapid fall of interest rates.

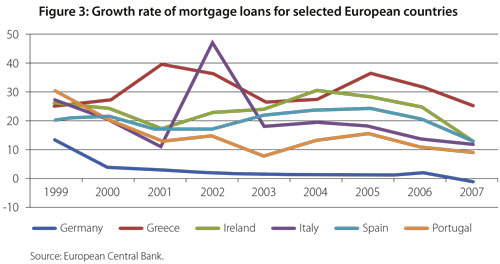

The sharp increase of bank funds and the fall in interest rates led to a very significant increase in the volume of consumer lending; and in Greece, Ireland and Spain, much of it was channeled into real estate (Figure 3). As a result, from 1997 to 2007, housing prices rose at an average annual rate of 12.5 percent in Ireland, 9 percent in Greece, and 8 percent in Spain. Even in the United States where the real estate bubble was at the origin of the global financial crisis housing prices increased by an average of only 4.6 percent per year.

Over the same period, construction as a share of gross output rose from 9.8 to 13.8 percent in Spain, and from 7.9 to 10.4 percent in Ireland. In Greece, construction as a share of gross output rose from 6 percent in 2000 to 7.1 percent in 2006. In the United States, the share of construction in gross output only increased from 4.6 to 4.9 percent. The channeling of funds into real estate allowed bubbles to emerge whose burst was at the core of the economic crisis.

The housing investment and consumption boom were not without (temporary) benefits. For example in Greece, after averaging an annual GDP growth rate of 1.1 percent from 1980 through 1997—the slowest in eventual eurozone countries—Greece’s economy expanded at an average rate of 4 percent over the next ten years, the third-fastest rate in the eurozone. In Spain, economic growth averaged 3.8 percent between 1997 and 2007, 1.3 percentage points higher than the average for the years between 1980 and 1997. Ireland had the highest growth during 1997 and 2007, achieving an average rate of 6.8 percent, an improvement over its already impressive growth rates of 4.6 during the years of 1980 and 1997. Only Portugal experienced slower average growth rates in the later period, with an average rate of 2.3 percent during 1997-2007, and an average rate of 3 percent for the period 1980-97. This is due to the country’s poor competitiveness. In fact, there is much evidence that Portugal’s business climate is especially weak and further deteriorated following the adoption of the Euro.

But the large increase in financial flows throughout Europe, substantially lower borrowing costs, easy access to liquidity via leveraging and as a result of growing lending from core banks to noncore banks, and the elimination of the exchange rate risk provided an illusionary sense of prosperity in a low-risk environment. The sense of prosperity was illusionary because it was not matched by improvements in productivity or the business environment that would have laid the foundation for sustained long-term growth. In fact, the sudden abundance of financial flows in non-core countries resulting from the financial deregulation and adoption of the euro exacerbated weak competitiveness that had already adversely affected these countries before the adoption of the common currency.

Why and how did periphery countries lose competitiveness so quickly?

One of the primary factors behind the loss of competitiveness in periphery countries was the sharp rise in wages. Between 2001 and 2011 per-unit labor costs in Greece rose by 33 percent, 31 percent in Italy, 27 percent in Spain and 20 percent in Ireland, while they grew by only 11 percent in the United States and by only 0.9 percent in Germany (Table 4). This increase in wages was driven both by the private sector reflecting the higher demand for labor due to accelerated growth and by rises in wages in the public sector. Expenditure increases were considered to be manageable, though, owing to the substantially lower borrowing costs for sovereigns in the aftermath of the adoption of the Euro and rapidly rising revenue reflecting the increase in economic activity and the real estate boom.

As a result of this loss of competitiveness, the structure of economies shifted away from the manufacturing sector towards service and non-tradable sectors. Between 2000 and 2007, the share of manufacturing in GDP fell by 10 percent in Ireland, 3 percent in Italy, 4 percent in Spain, 3 percent in Portugal and 1 percent in Greece (from its already low level of 10 percent). Yet, the share of the manufacturing sector rose by 1 percentage point of GDP in Germany. This increase in the relative size of Germany’s manufacturing sector (from its already very high level) was also reflected in a rise of Germany’s overall surplus position with the eurozone member countries.

Overall, at the heart of the crisis in the eurozone is a balance of payments crisis caused by the large and growing gap in competitiveness between core and periphery countries. And as discussed above, the large increase in lending to non-core countries made possible by rising bank leverage and the common currency was central to this outcome with its impact on interest rates (both for sovereigns and for credit to the private sector), financial integration and the encouragement of export-led growth in core countries and consumption-led growth in non-core countries.

In the aftermath of the global financial crisis, most European countries entered a recession and the bubble in the real estate market burst, leading to sharp increases in non-performing loans and subsequent government-financed bailouts for the financial sectors. The increase in public debt resulting from these bailouts was further compounded by the ballooning of government deficits resulting from the sharp fall in revenue as a result of the drop in output and the adoption of stimulus packages to counteract the impact of the crisis. Figure 5 and 6 show the evolution of the public debt burden following the crisis.

Conclusions

As in the United States, financial deregulation increased bank leverage and availability of funds in the core eurozone countries. The adoption of the Euro catalyzed financial flows to periphery countries and convergence of interest rates in periphery countries to the levels in core countries. The sharp increase in low-interest funds set off a consumption and real estate boom in periphery countries, leading to higher growth and increases in government revenue and spending. The resulting real appreciation led to a loss of competitiveness in periphery countries, adversely affecting export performance and causing current account imbalances. While the fiscal position remained manageable before the crisis owing to rising revenue, the recession following the global financial crisis led to the burst of the real estate bubble and a financial sector crisis, as well as to sharply increased budget deficits and worsened debt indicators: this triggered the sovereign debt crisis. Core countries, in particular Germany, maintained a competitive edge through wage restraint allowing them to increase exports to periphery countries, while their banks profited from increased lending to non-core countries.

In sum, increases in lending from core countries to periphery countries, facilitated by the adoption of the Euro but caused mainly by rising bank leverage in the core countries as a result of financial deregulation, contributed to the real estate bubble and consumption boom in periphery countries. Its unsustainability became evident in the aftermath of the global financial crisis and triggered the current sovereign debt crisis.

About the Authors

Justin Yifu Lin is the former World Bank Chief Economist and Senior Vice President, Development Economics. In his capacity, Mr. Lin guided the Bank’s intellectual leadership and played a key role in shaping the economic research agenda of the institution. Building on a distinguished career as one of China’s leading economists, Mr. Lin is undertaking an ambitious research program that examines the industrialization of rapidly developing countries and sheds new light on the causes of lagging growth in poor regions. He took up his World Bank position on June 2, 2008, after serving for 15 years as Professor and Founding Director of the China Centre for Economic Research (CCER) at Peking University.

Volker Treichel has been a Lead Economist in the Office of the Chief Economist and Senior Vice President of the World Bank since December 2010. During this time, he published several Working Papers with Justin Lin, including on growth strategies for Nigeria and Latin America, the unexpected global financial crisis and the Euro crisis. From 2007, he was the Lead Economist for Nigeria. During this time, he published the book Putting Nigeria to Work – a Strategy for Employment and Growth. He also led the first subnational Development Policy Operation in sub-Saharan Africa in Lagos State as well as the initial engagement with the Niger Delta. Prior to 2007, Volker was at the IMF in positions including mission chief for Togo and resident representative in Albania.

{kind=link}