By Dan Steinbock

Despite China’s success in containment, the novel coronavirus is exploding outside China, due to complacency and inadequate preparedness. The contraction will compound human risks and economic damage. It will shake economies, politics and governments worldwide.

Although the epicenter of the outbreak is now Europe, only a few major economies have launched effective battles against the virus.

Since complacency and inadequate preparedness prevailed outside China until recently, the consequent global pandemic casts a dark shadow over the global economy. It, too, shall pass, but only with effective global cooperation.

Worldwide infection rates

With the novel coronavirus (Covid-19), the number of accumulated confirmed cases worldwide continues to soar toward 300,000 and beyond. In the absence of adequate testing, even these official figures are just the tip of the iceberg. Most likely, 15% to 25% of the real figure.

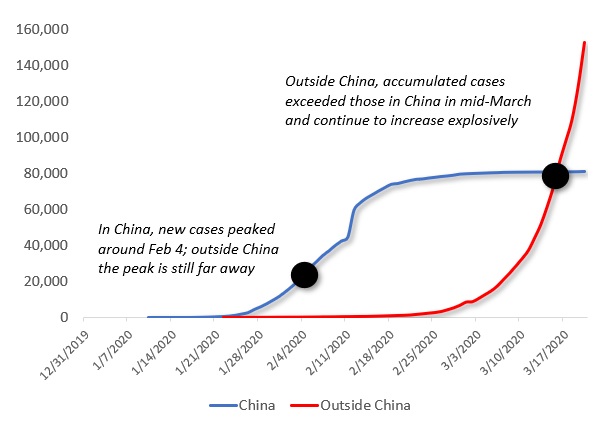

In China, the turnaround came a month after the first novel coronavirus cases were diagnosed, thanks to strong containment measures. Outside China, the first cases were reported after mid-January. Two months later, they soared beyond those in China and continue to accelerate (Figure 1).

Figure 1 Accumulated confirmed cases in and outside China (until March 18)

In China, the impact of the coronavirus is already easing, though complacency is no option. Outside China, epidemiologists currently anticipate a peak around June. If that’s the case, economic damage in China would be largely limited to the first quarter, but international economic damage would endure well into the second quarter, and in the most affected countries well beyond.

Due to the uncertainty of current data in Europe and particularly the United States, one plausible scenario is that the battle against the coronavirus may last through the ongoing year and possibly through 2021.

After mid-January, I projected three probable virus impact scenarios, which can now be reassessed. In the “SARS-like impact” scenario, a sharp quarterly effect, accounting for much of the damage, would be followed by a rebound. The broader impact would be relatively low and regional. Although China has been successful in containment, advanced economies in Europe and North America failed to respond in time. So, this scenario is no longer in the cards.

In the “extended impact” scenario, the adverse impact would last two quarters. The broader impact would be more serious and have a significant impact on global prospects. That’s where the world economy is now heading to, rapidly.

In the “accelerated impact” scenario, the damage would be steeper and broader with severe consequences on the global economy. If the containment measures continue to fail outside China, this risky scenario can no longer be excluded.

In early March, the International Monetary Fund (IMF) projected global growth to fall 0.1 percentage points from the expected 3.3%. The estimate was too optimistic. Even the OECD expects global GDP growth to drop to 2.4% in 2020, with possibly negative growth in the first quarter. But that was a month ago. Now a global contraction could cause economic growth prospects to plunge closer to 2%.

China toward rebound

Thanks to China’s draconian measures, reported cases peaked and plateaued between January 23 and 27, and have largely declined since then (Figure 2).

Figure 2 Epidemic curves for confirmed COVID-19 cases in China

Before the crisis, Chinese economy was benefiting from a mild recovery, which was expected to result in GDP growth of 5.8% to 6.1%. In early March, IMF projected China’s growth to fall to 5.6% in 2020. Now some estimates in the West anticipate baseline growth of less than 5%, with significant downside risk of less than 3%.

In January, factory activity did contract at the fastest pace on record as the Purchasing Managers’ Index (PMI) fell to a record low of 35.7 from 50.0. The same goes for the services activity. While the anxiously awaited initial data was significantly worse than anticipated, both plunges were only to be expected. Economic shocks translate to contractions.

The real question involves the strength of the post-shock rebound between mid-March and April, given the low starting-point. It is these assumptions of the first scenario that fueled the bold projections by J.P. Morgan that the Chinese first quarter could go down to -4%, but second quarter would go up to +15%.

The rebound story is possible, if fiscal and monetary support is adequate and if small- and mid-size firms, which account for more than four-fifths of nationwide employment and over half of the GDP, can jumpstart production.

In China, economic development is seen as critical to the country’s future. But ultimately, Chinese leaders are not accountable to GDP. People come first. It is thanks to that mindset that China is now busy getting back to business, working to bolster the economy with accommodative monetary and fiscal policies, reopening schools and trying to contain the remaining chains of transmission.

As the populous country is moving from containment to the mitigation stage, the challenge will be to contain new imported cases in the borders, while quickly extinguishing potential new virus clusters at home.

In economic terms, China must prepare for the negative feedback effect from the world economy starting in the second quarter.

Contraction, stagnation, debt in US…

Despite elevated warnings since mid-January, uncertainty began to grip the rest of the world only at the end of February. Instead of mobilizing against the virus, complacency in advanced economies led to a series of missteps, including faulty and belated local testing, failures in evacuations and quarantines, lax enforcement of self-quarantines. Hence the consequent multi-trillion-dollar market corrections.

In the US, the S&P 500 equity market has plunged more than 20% since January 1, as evidenced by Shiller’s cyclically adjusted PE ratio. Volatility spiked as it last did in fall 2008. Liquidity stress has spread rapidly across firms and households. Oil prices almost halved to less than $30 per barrel, which could be further penalized by a misguided and ill-timed price war.

Prior to the virus outbreak, the IMF expected US growth to moderate from 2.3% in 2019 to 2% in 2020 and 1.7% in 2021, due to waning support of fiscal and financial conditions. Those estimates are now history and the same goes for IMF projections in early March. In the second quarter, the US could face a significant contraction before the expected recovery, which may prove more challenging than expected.

Recently, the IMF projected US growth to suffer a slowdown from 2.0% to 1.6%. But the estimate is too optimistic. If the second quarter carnage proves limited, U.S. growth could still stay close to 0.2%-5%. But the risks are on the downside and, after a series of policy mistakes, the margin of error is slim.

After the White House’s delays of outbreak management, the Fed cut interest rates close to zero, coupled with a new round of $700 billion for quantitative easing. In the short-term, the move is understandable. But in the long-term, it compounds new risks. Moreover, the Fed’s rate cut will be coupled with fiscal stimulus, which is not likely to suffice.

Yet central banks in Europe, the UK and Japan will follow US footprints into more monetary and fiscal accommodation. But that may fail to quell virus fears, if infection rates continue to soar.

… Eurozone and Japan

In the Eurozone, recessionary pressures come in a particularly bad time. Before the virus, quarterly growth was 0.1%; the weakest in seven years. Now things will get a lot worse. German GDP will stall further, France and Italy will remain in contraction. In the UK, annualized growth is likely to fall fast from 1% closer to contraction territory. With tourism in shambles, soaring infection rates will reverse Spain’s growth pickup. Italy, the Eurozone’s most indebted major economy is struggling with infections and deaths that are soaring faster than in any other major economy

If the virus cases continue to increase in the Eurozone, regional growth prospects are likely to end near contraction territory. In the most affected countries, the failure of timely containment is likely to foster a recession through the first half of the year. And if the virus cases continue to climb in the second quarter, the contraction will prove steeper. A potential protracted appreciation of the euro – a déjà vu of the sovereign debt crisis in the early 2010s – could penalize growth even into 2021.

In both the United States and the Eurozone/UK, the first quarter damage will only be the prelude to the second quarter carnage. And if the virus is not managed appropriately, the consequent hit will cast a shadow over the hoped-for rebound in the second half of 2020 as well, possibly into 2021.

Prior to the coronavirus, Japanese growth contracted 0.7% in the fourth quarter of 2019. After last fall’s consumption tax and the consequent economic turmoil, contraction prevailed in January, while great uncertainty overshadows the 2020 Olympics. Many major Japanese companies must cope with heavy damage in the first half of 2020; in the second half, they face Olympic repercussions, with or without the Olympics. Both scenarios will further weaken the world’s most rapidly aging major economy that’s been in secular stagnation for several decades.

With some 9,000 confirmed cases, South Korea has been worst hit by the coronavirus in non-China Asia. As the decline in exports will be coupled by the decline of domestic demand, South Korea may contract in the first quarter, despite rate cuts and efforts at fiscal support.

Additionally, Australia and the regional financial hubs Singapore and Hong Kong are on their way or in contraction. Since these countries are significant investors in Southeast Asia, their challenges will reverberate across emerging Asia.

Early damage limited in emerging economies, but risks rising

In December, the Asian Development Bank (ADB) still maintained 4.7% for ASEAN economies in 2020, mainly based on mild recovery in China and the US. Now even countries that have strong structural growth potential, including Indonesia, Vietnam and the Philippines, are not immune to indirect short-term hits as their trade, investment, migration and remittance flows depend on the international environment.

The same goes for South Asia, particularly India, Pakistan and Bangladesh. In India, the growth rate decelerated from 7.7% to 4.7% in January and 5.3% in 2020. That was before the global pandemic, which will compound such threats. While virus cases have so far been low in Russia, it will be penalized by oil prices, just as Brazil’s growth has been harmed by the fall of commodities.

Until recently, the Middle East and Latin America had not witnessed sustained case growth. Now, local transmissions have begun, and cases are rising in the Gulf, Egypt and Northern Africa’s Maghreb economies. Iran has suffered a dramatic rise in infections and deaths. Prior to the pandemic, US withdrawal from the nuclear deal, drone assassinations and intensified efforts at regime change caused growth to decrease to close to 1%, while the virus will significantly deepen economic erosion.

Sub-Saharan Africa is already struggling with a lingering Ebola crisis in the West and locust plagues in the East. Official virus cases are still low (South Africa, Nigeria, Senegal), but tests have only begun. In simulations, the highest importation risk involves countries (South Africa) that have moderate to high capacity to respond to outbreaks, whereas countries at moderate risk (Nigeria, Ethiopia, Sudan, Angola, Tanzania, Ghana, and Kenya) have variable capacity and high vulnerability.

While struggling to restore their potential output level, emerging economies will have to absorb the economic tsunami from the West. That will cause new pressures in countries that depend on capital inflows and commodity reliance (Indonesia, Mexico and South Africa) or carry excessive debt (Turkey).

While oil exporters from Gulf to Russia will suffer from collateral damage and price wars, lower prices will benefit emerging Asia in the short term.

Inadequate preparedness

Unlike markets, the novel coronavirus cannot be “talked down” as the Trump administration has tried. Eager to disguise its utter failure in containment and local testing, it is appealing to the worst racial instincts by calling the virus “Chinese”, even against the reprimand of the WHO, thereby contributing to hate speech, stigmatization, as well as anti-Chinese and anti-Asian incidents in America.

On March 16, the New York Times released a balanced investigative report about the Trump administration’s mishandled virus response. A day later, the administration shared with the Times its pandemic report. Ostensibly, the White House hoped to show it was in control. But timelines revealed tell a different story.

Even though the government’s leading health executives had been monitoring the crisis since early January and the first COVID-19 case was confirmed in the state of Washington on January 20, followed by WHO alerts, White House failed to act upon pressing evidence. Until recently, Trump’s has said publicly that any danger would pass by April 1. When he finally understood the risks, he botched his error-ridden Oval Office virus address and the subsequent mistake-ridden Rose Garden address. Until mid-March, the infection enjoyed a relatively free ride in America.

The pandemic report was clear about the consequences: “A pandemic will last 18 months or longer and could include multiple waves of illness… Increasing COVID-19 suspected or confirmed cases in the U.S. will result in increased hospitalizations among at-risk individuals, straining the health care system.” Shortages would ensue.

In the UK, comparable stumbling has caused a similar debacle, which Prime Minister Boris Johnson has tried hard to express in optimistic terms: “We can turn the tide within the next 12 weeks.” Yet, that cannot be achieved without restrictive measures, which could have been launched weeks ago. In contrast, German Chancellor Angela Merkel has been blunt: “Not since World War II has our country faced a challenge that has required such a high degree of common and united action. We can succeed as long as everyone truly understands what’s needed.”

Unfortunately, the US, the Eurozone, and the UK are mobilizing with an unwarranted delay of 4 to 8 weeks. Today, accumulated confirmed cases worldwide exceed 250,000. But that’s only a prelude to more.

Let’s assume that cases in China will remain low and imported cases can be quarantined. So, cases in China would remain less than 85,000 even in late April. Let’s also assume that other countries and regions – not just US and Europe but those in the Middle East, Latin America and Africa that will suffer collateral damage, due to complacency in the West – will still increase. Let’s also be conservative and use polynomial rather than exponential trendlines. Even then, cases outside China could more than triple in the period, even in a benign scenario.

Avoiding nightmare scenarios requires multipolar cooperation

Obviously, the early economic defense has been by the major central banks to cut down the rates, inject liquidity and re-start major asset purchases. But as the post-2008 decade has shown, monetary responses cannot resolve fiscal challenges.

The early damage has focused on a set of key sectors, such as healthcare, transportation, retail, tourism, among others. In turn, ultra-low rates, liquidity injections and asset purchases will be coupled with targeted fiscal stimuli in affected economies. Yet, current measures to restrict the infection and economic damage will contribute to further debt erosion in many major advanced and emerging economies.

As the US national debt now exceeds $23.5 trillion (107% of GDP), Washington’s debt burden is at par with Italy just before its 2010 European Union (EU) sovereign debt crisis. In Italy, that level is now significantly higher (135%) and in Japan alarming (240%). In Europe, the Maastricht Treaty deems that member states should not have excessive government debt (60%+ of GDP). Today, no major European economy fulfills that criteria.

In advanced economies, the coronavirus contraction has potential to wipe out much of the recovery. Meanwhile, as a result of the US tariff wars, developing countries, which have weaker healthcare systems, already suffer from financial and debt vulnerabilities and may not be able to withstand still another external shock.

Furthermore, old supply-side measures cannot resolve pandemic challenges. If containment measures fail, or subsequent mitigation proves inadequate, or new virus clusters emerge after containment and mitigation, markets will remain volatile and economies will suffer further damage, particularly with multiple waves of secondary infections after the current restrictive measures.

The way to the normality requires the defeat of the virus. Following China’s response, most countries do seek to contain the virus, then mitigate it and finally to deter secondary infection crises. China had to develop its stance almost overnight in mid-January. Other major economies had weeks to mobilize, yet many missed the opportunity, due to complacency and inadequate preparedness. Containment will be only partial in these countries, which will compound their mitigation challenges.

So, when restrictive measures are phased out in major economies, some countries are likely to record odd spikes in death rates, particularly in the virus risk groups. It is a discrete modern-day version of the old eugenics, which permits certain policymakers in the West to bury their mistakes, literally. At home, virus carriers may or may not gain adequate immunity. As poorly-enforced quarantines are phased out, flows of people, many of which may be infected or carriers, will show up in the borders of countries that have successfully managed the crisis – as already evidenced by the spikes of imported cases in China, Singapore and Hong Kong.

What is desperately needed to avoid further nightmare scenarios is multipolar cooperation among major economies and across political differences. In this quest, China, where containment measures have been successful, can show the way, along with major advanced and emerging powers.

About the Author

Dr. Dan Steinbock is an internationally recognized strategist of the multipolar world and the founder of Difference Group. He has served at the India, China and America Institute (USA), Shanghai Institutes for International Studies (China) and the EU Center (Singapore). For more, see https://www.differencegroup.net

After mid-January, Dr Steinbock argued that China had adopted pioneering standard-setting measures to contain the novel coronavirus outbreak.

In late January, he said that the COVID-19 politicization, the associated “infodemic” and battle against the WHO and its chief were misguided and would undermine the international crisis response.

In the first week of February, he predicted the virus cases would decelerate in China as Beijing was containing the outbreak, but were accelerating outside China.

In late February, he predicted that delays and mistakes in the US and Europe would prove costly in terms of infection rates, human lives and economic damage.

At the turn of March, he projected a shift toward global economic contraction, due to containment failures in the West. In the longer-term, the spillovers could prove costly in the developing world.

{kind=link}