")

Introduction

The exponential rise in external debts poses a significant threat to the prosperity and economies of developing countries. Nearly half of the world’s population lives in countries where foreign debt servicing exceeds government spending on education and health. For example, in 2023, global sovereign debt reached very high levels, i.e., US$92 trillion, with poor countries carrying 30 percent of the total debt burden. Moreover, around 40 percent of developing countries experience serious debt repayment challenges. These unsustainable debt levels adversely affect long-term investment in Sustainable Development Goals and addressing environmental challenges (UN, 2023).

Regarding the gravity of the situation with very high levels of external debt in developing countries, UN Secretary-General António Guterres stated that, on average, borrowing costs are four times higher for African countries than for the US and eight times higher than for the richest EU countries. Poor nations increasingly rely on private creditors who charge “sky-high” interest rates. These countries have little choice but to borrow to revive their economies. Guterres noted that, for poor countries, debt has become “a trap that simply generates more debt” (UN, 2023).

The UN Report (2023) proposes a number of urgent remedies, including an “effective debt workout mechanism” that supports payment suspensions, longer lending terms, and lower rates, “including for vulnerable middle-income countries.” The report also calls for a “massive” scale-up of affordable long-term financing by transforming the way that Multilateral Development Banks function, re-engineering them to support sustainable development.

In 2020, the average total debt burden (both public and private) of poor countries rose by 9 percentage points, compared with an annual increase of 1.9 percent in the previous decade. In the same year, fifty-one countries experienced a downgrade in their sovereign debt rating, making borrowing more expensive. Global inflation, spurred by the Russian invasion of Ukraine in early 2022, created upheaval in global markets for food, fuel, and fertilizer. The sudden decrease in the supply of these essentials caused high prices, hurting many developing countries dependent on imports of these basics even more deeply than they had already been by the COVID-19 pandemic. These two external factors affected price hikes and multiplied public and private debt (Stiglitz and Rashid, 2020).

In early 2022, the United States Federal Reserve and European Union Central Banks raised interest rates rapidly to curb high inflation after decades of low inflation and low interest rates. Thanks to globalization and financial liberalization over the last four decades, most countries are integrated into Western financial markets, promoted by the International Monetary Fund (IMF) and World Bank. Higher interest rates caused investors to withdraw capital from developing countries and move to United States (US) and European Union (EU) (Siddiqui, 2024).

Rising External Debts

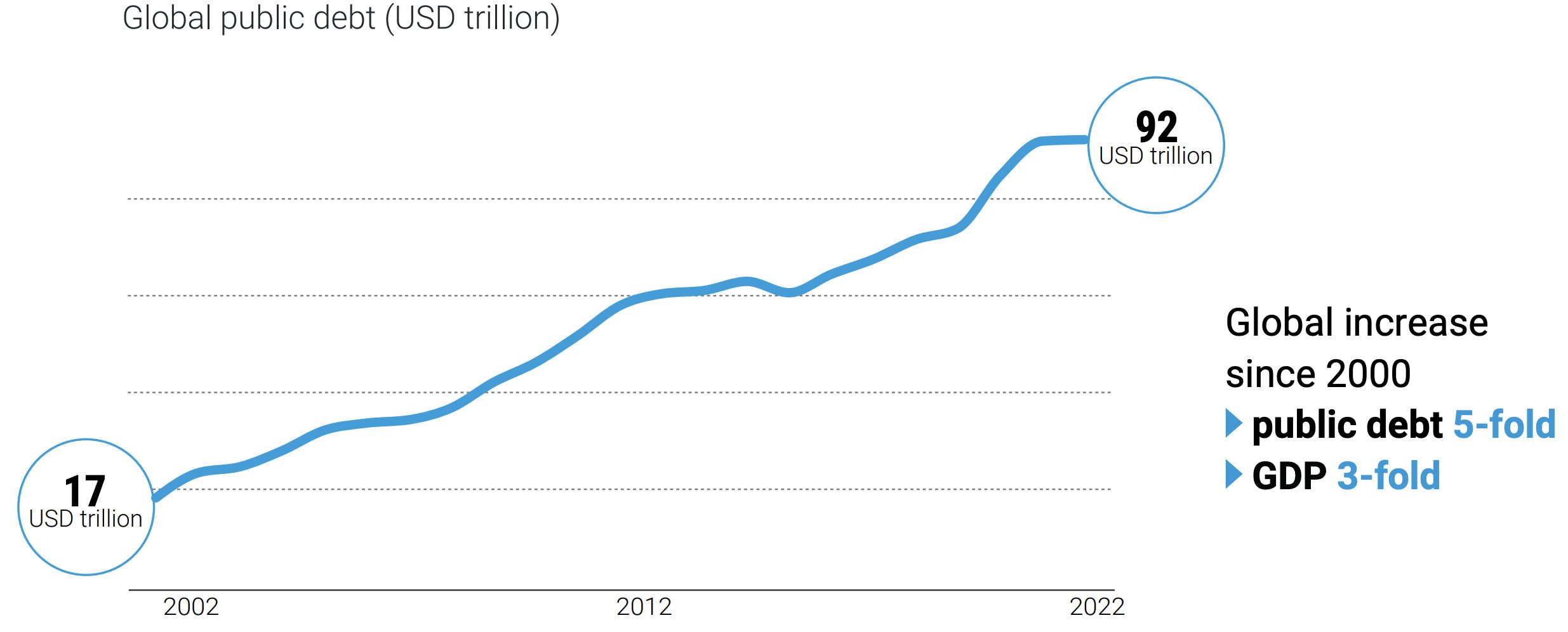

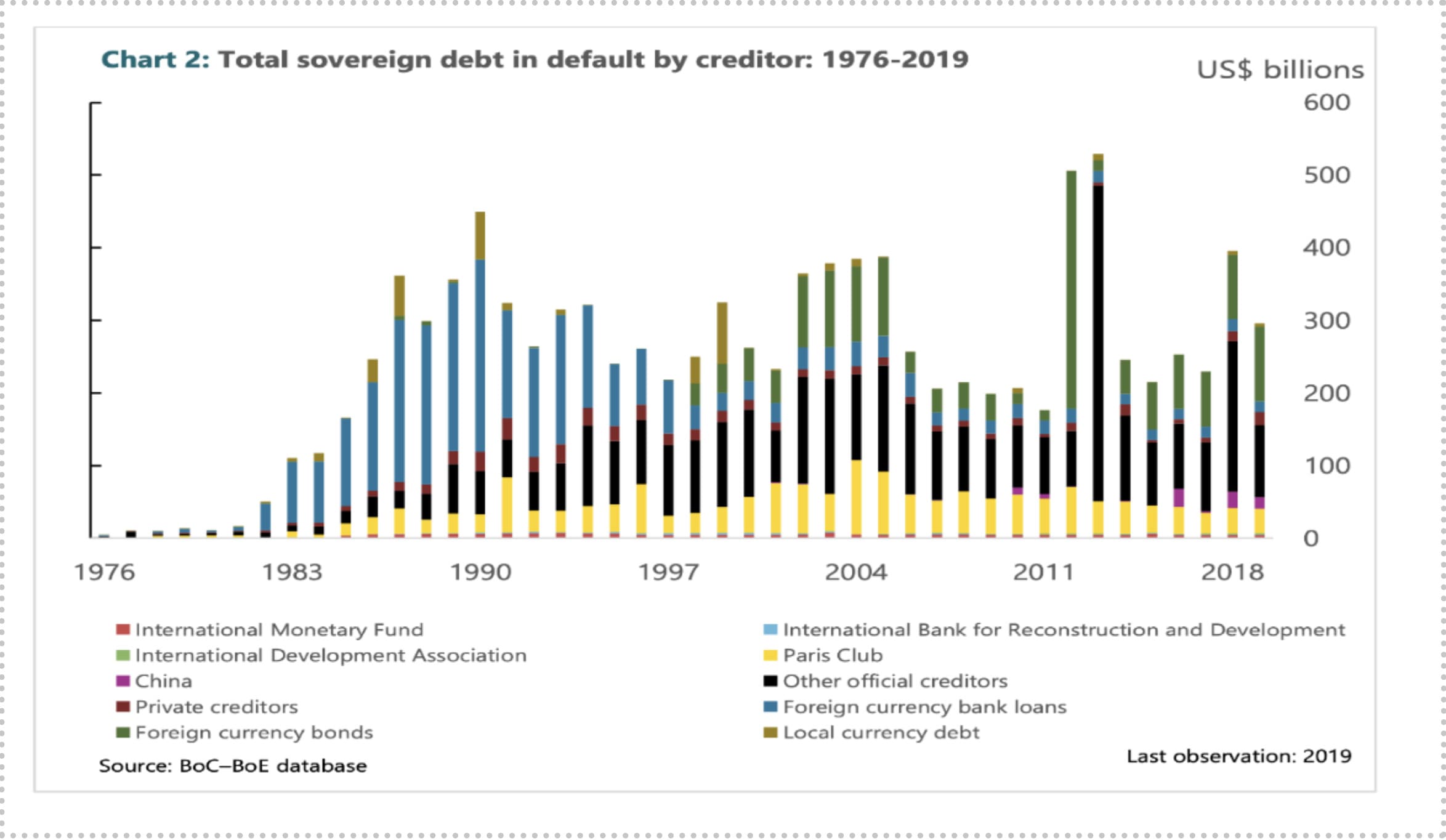

Public debt around the world has been on the rise over the last few decades, and the prevailing economic crisis in most developing countries has triggered a sharp acceleration of this trend. Between 2002 and 2022, global public debts rose dramatically from US$17 trillion to US$92 trillion (as shown in Figure 1). However, prior to 1980, sovereign debts were at very low levels, and the incidence of sovereign debt defaults by creditors rose only after the mid-1980s, as indicated in Figure 2a. According to the data, global public debt has increased more than fivefold since the year 2000, clearly outpacing global GDP, which tripled over the same period.

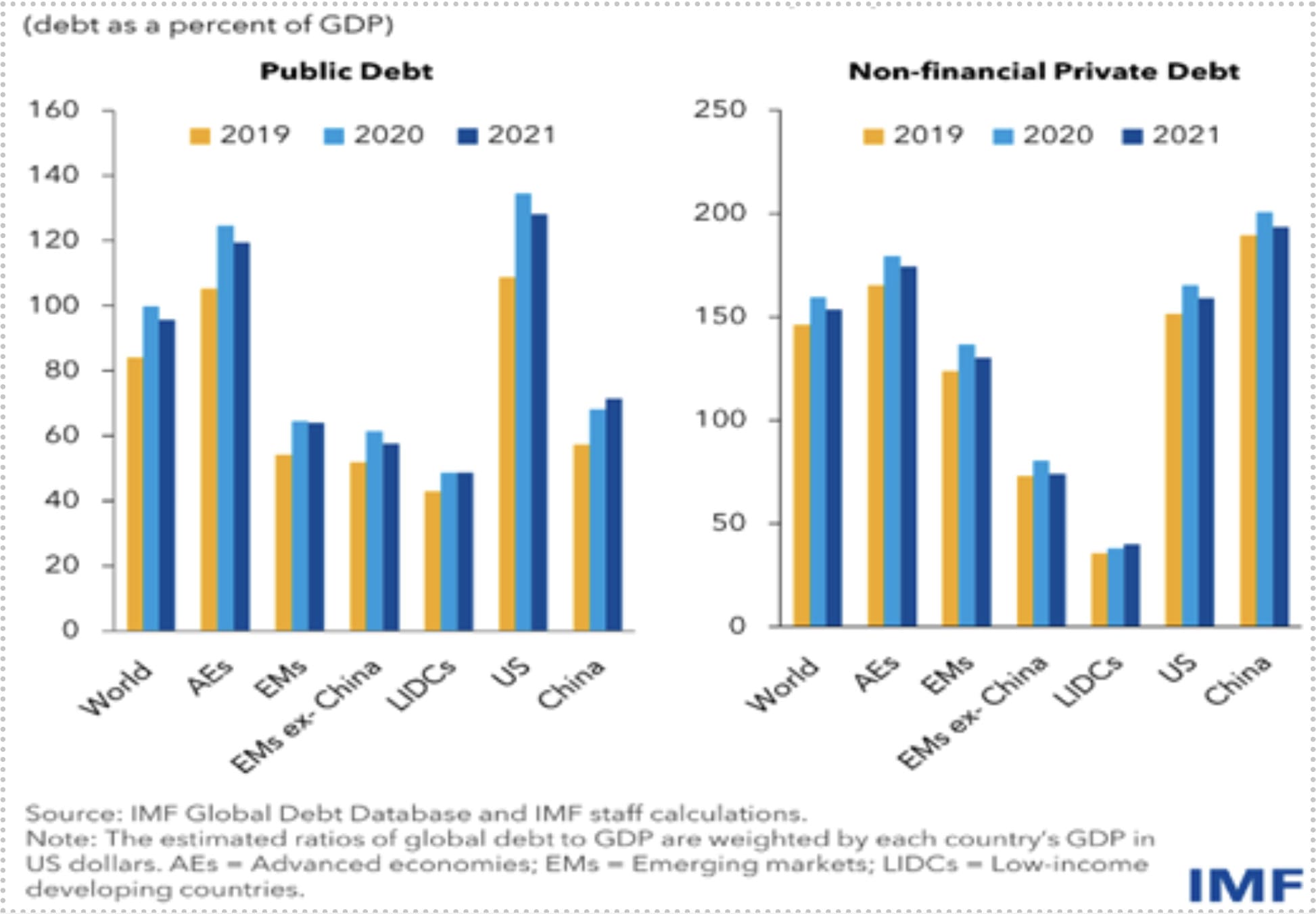

Figure 2b shows that during the COVID-19 pandemic, public and non-financial private debt rose significantly between 2019 and 2021. Despite external debts being at low levels for less developed countries, low incomes and high levels of poverty mean that debt repayments could cause severe socio-economic crises.

In 2022, global public debt—comprising general government domestic and external debt—reached a record US$92 trillion. Developing countries owe almost 30 percent of the total, of which roughly 70 percent is attributable to China, India, and Brazil (UN, 2023).

Figure 1: Global Public Debt, 2000-2022 (US$ trillion)

Figure 2a: Total Sovereign Debt in Default by Creditors, 1976-2019

Figure 2b: Public and Non-Financial Private Debt, 2019-2021.

The IMF estimates that about 60 percent of low-income developing countries were experiencing debt distress or were close to it in 2021 and 2022. Additionally, the IMF noted that more than 70 developing countries had public debt exceeding 60 percent of GDP in 2020, and almost 60 countries remained at that level in 2022 despite following austerity programs (IMF. 2023).

The socio-economic consequences of a debt crisis have been devastating for low-income groups in poor countries. Latin America’s and Africa’s negative performance is generally attributed to the regions’ debt crises. A full-blown debt crisis inevitably leads to cuts in public spending in areas like education, health, and other social sectors. This can result in years of slow economic growth and high unemployment. Stagnation and higher unemployment increase poverty, breeding discontent and instability, and ultimately erasing gains in development (Dymski, 2003).

Over the past decade, external debts of developing countries have more than doubled, with most of these countries highly dependent on commodity exports. Developing countries’ total external debts, also known as public-guaranteed debts, rose from US$600 billion in 2008 to over US$1.3 trillion in 2020. Developing countries were forced to pay US$130 billion in debt service payments in 2021, which squeezed incomes soon after the COVID-19 pandemic. Moreover, private corporations’ borrowing from foreign banks, which were non-guaranteed, rose from US$520 billion in 2008 to nearly US$900 billion in 2021. Almost all of the developing countries’ debt is in US dollars, and they greatly rely on export earnings and remittances to service or repay their loans (Arellano; Bai, and Mihalache, 2024).

Mainstream economists’ advice on debt restructuring revolves around cuts in public spending and improving fiscal balance. Fiscal spending cuts are often given as universal solutions to avoid debt crises (Siddiqui, 1996). As a debtor country reduces fiscal spending and tightens its belt to minimize its ‘payment problems,’ this can improve credit ratings and encourage creditors to lend more, helping the government service its existing debts. However, in the real world, this seldom works, as Greece’s experience clearly demonstrates. Austerity usually exacerbates debt crises. Attempts to solve debt crises through restructuring, as many developing countries have done in the past, have often proved to be too little and less effective.

In developed economies, after fiscal expansion averted the worst of the 2009 financial crisis, unconventional monetary policies, mainly ‘quantitative easing,’ took over. The European Central Bank (ECB) followed the US Federal Reserve’s lead in implementing quantitative easing for over a decade. Quantitative easing’s lower interest rates encouraged more borrowing as more credit became available at lower costs (Stiglitz and Rashid, 2020).

Debt has become unsustainable when a government is forced to make cuts in areas that hurt its people, such as education or healthcare, just to keep up with payments. In 2021, Zambia’s debt servicing accounted for 39 percent of its national budget, with more spent on paying debts than on education, health, water, and sanitation combined. This undermines a country’s ability to invest in developmental projects. For instance, debt servicing costs in Sri Lanka have heavily burdened the government’s finances, leading the central bank to suspend external debt payments in April 2022 to buy essential goods like fuel. Coupled with unfavourable foreign exchange and high-interest rates, debt is seen as riskier for smaller economies (World Bank, 2023).

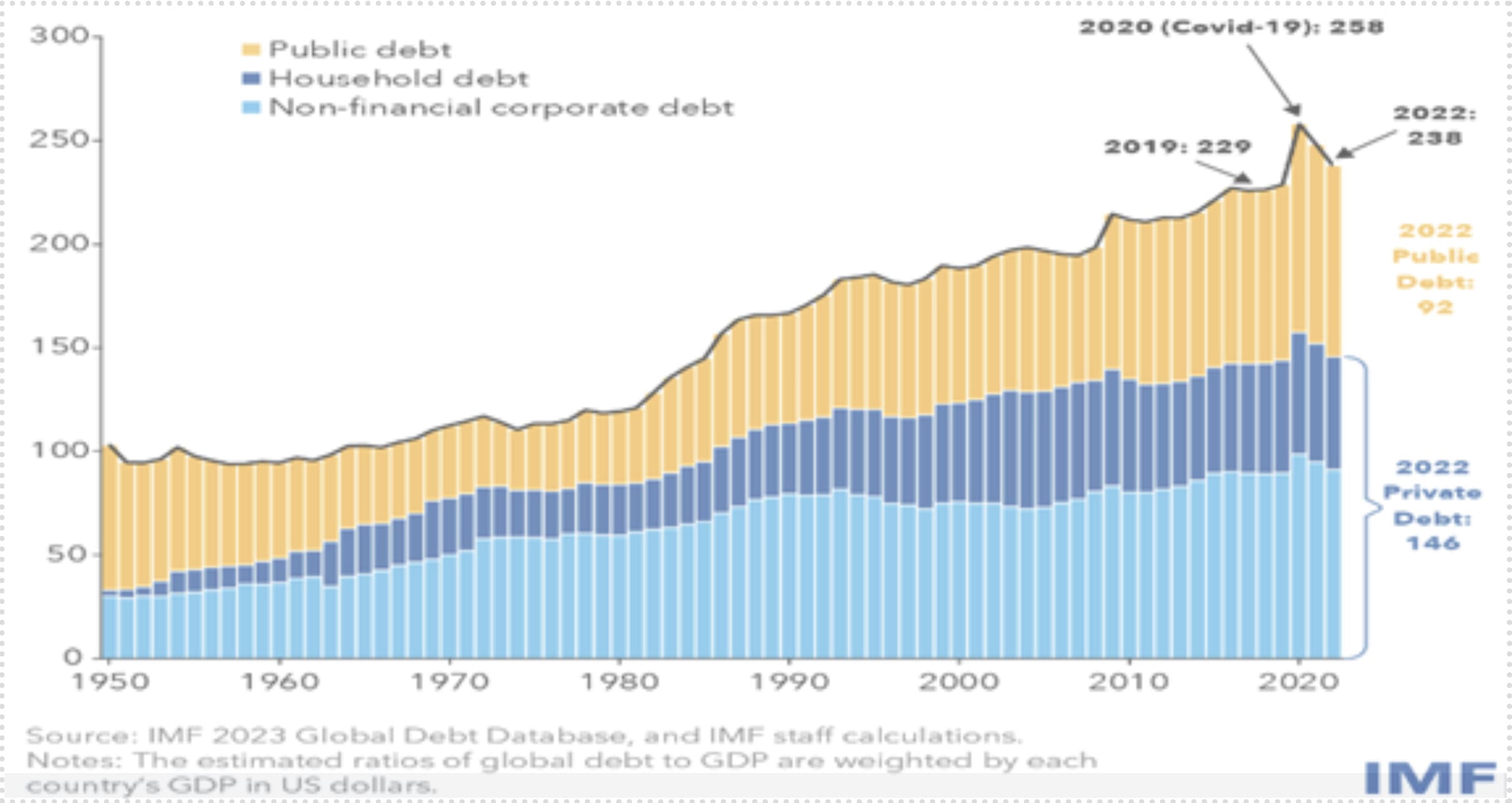

Developed countries face entirely different challenges, with some exceptions. For example, Japan, the world’s fourth-largest economy, is also one of the world’s most indebted countries, with total debt sitting above 600 percent of GDP. While the bulk of Japan’s debt is public, in recent years, it has been the financial sector piling on debt, not the government. Around two-thirds of the US$315 trillion owed originates from mature economies, with Japan and the United States contributing the most to that debt pile. However, the debt-to-GDP ratio for mature economies has generally been coming down. Figure 3a indicates that over the last seven decades since 1950, global debts (public and household) have consistently increased. During the COVID-19 pandemic, global debts as a percentage of GDP rose sharply, as shown in Figure 3b (IMF. 2023).

Figure 3a: Global Debt, 1950-2020 (% of GDP).

Figure 3b: Total Global Debts, 2015-2022 (in trillion US$)

On the other hand, emerging markets held $105 trillion in debt, with the debt-to-GDP ratio hitting a new high of 257 percent—pushing the overall ratio up for the first time in three years. China, India, and Mexico were the biggest contributors.

Mainstream economics claims that the path to economic growth for developing countries is achieved through the implementation of neoliberal policies, which include economic openness, market deregulation and liberalization, and privatization of public enterprises. Despite the lack of empirical evidence supporting these policies’ effectiveness, they continue to be imposed (Wade, 2023).

The growing debt of poor countries is alarming and brings back harsh memories of the debt crises of the late 1970s and early 1980s (Siddiqui, 1996). That period ended with a monetary tightening policy in the US, triggering a wave of debt crises in developing countries, especially in Latin America and Africa. During this period, neoliberalism was imposed, and austerity programs, known as Structural Adjustment Programs (SAPs), were enforced on debtor developing countries as a supposed solution (World Bank, 2023).

External Debt Crisis in Latin America

In Latin America and Africa, IMF loans are structured around two main programs: Stand-By Arrangements (SBAs) and Extended Fund Facility (EFF) or Extended Credit Facility (ECF) Arrangements. The former is most frequently used by member countries and is typically for relatively short periods, lasting between twelve and twenty-four months but rarely exceeding thirty-six months. Generally, these agreements involve constant monitoring of the country’s economic policies by the IMF but have few conditionalities regarding structural reforms focused on meeting certain set objectives.

The second type of agreement, the Extended Credit Facility, is applied to countries that not only experience a temporary balance of payments problem but are considered to have structural imbalances. With this type of agreement, the IMF proposes to intervene in the country’s economic structure, imposing fiscal austerity, exchange rate liberalization, and interest rate guidelines; it usually also includes a range of measures related to privatizations, labor reforms, and changes in social security. These plans were not genuinely meant to help debtor countries resolve their economic and financial problems; on the contrary, the IMF appears intent on intervening in their internal politics, imposing neoliberal market policies under the guise of “unconditional” assistance, thereby assuring their compliance with the demands of international capital markets.

To understand the relationship between the IMF and Latin America, we must examine the role that the United States has historically assigned to the region. For the most powerful country in the world, Latin America primarily serves as a supplier of raw materials and cheap natural resources. This is vastly different from the role that Europe, for example, has had for the US. In the framework of Europe’s reconstruction after the Second World War, the US faced the dilemma of how to lend money to its allied European countries. The central objective of the US in the postwar period was to maintain the full employment achieved through public investment and ensure a trade surplus in US relations with the rest of the world.

However, the major European countries capable of importing goods from the US had no money to pay for their imports. To enable them to buy US-manufactured products, large quantities of dollars had to be provided. There were three ways to do this: (a) lend money and have the recipients pay in kind; (b) lend them money and require them to pay their debts in dollars; and (c) donate the money until they got back on their feet.

The risk of entering an uncontrollable cycle of indebtedness combined with the risk evoked in the first possibility. Therefore, the option chosen was to donate the dollars in what was known as the Marshall Plan, where Europeans would use them to buy goods and services, ensuring an outlet for U.S. exports and consequently full employment. The Marshall Plan was also part of the Cold War strategy of rebuilding Western Europe in opposition to the Soviet Union.

The debt crisis in Latin America lasted for ten years, until the early 1990s, despite several unsuccessful attempts at resolution. The last effort to resolve the debt problem came with the Brady Plan, the plan proposed exchanging old external debt bonds for new ones backed by the US. Mexico was the first to adopt the plan in 1989, and in the following years, ten countries in the region signed on: Argentina, Brazil, Costa Rica, Ecuador, Mexico, Panama, Peru, the Dominican Republic, Uruguay, and Venezuela. Debt reduction fluctuated between 35 percent and 45 percent, reducing the debt-to-GDP ratio from 54 percent in 1987 to 32 percent in 1997. The consequences of the crisis were dramatic in economic and social terms for most countries in the region, as debt levels increased and degrees of autonomy in sovereign decisions were forever lost

In the mid-1990s, Latin America faced a new debt crisis, a crisis concerning the Mexican peso, led to a “bank run” that threatened the stability of private banks. This crisis was the predictable result of an unsustainable program to maintain an artificially fixed exchange rate during President Carlos Salinas’ administration, an attempt to enhance his international reputation. With the change in administrations in 1995, the financial community forced a major devaluation, leading to a dramatic increase in inflation and rising interest rates. This pushed millions into bankruptcy, destroyed small businesses, and led to significant segments of the population losing their homes as banks foreclosed on them due to mortgage defaults.

The IMF intervened with a US$50 billion loan, supporting Mexico’s decision to “socialize” the unpayable debts of the private banking system through the poorly named “Banking Fund for Savings Protection,” totalling over 500 billion pesos. The clear purpose was to save private foreign banks, providing them with liquidity and absorbing their unpayable debts at the expense of a public burden that the Mexican people would be paying for many decades. This severely limited the public sector’s ability to finance essential public works and services (UN, 2023).

This stage marks the peak influence of neoliberalism in the region, with policies causing structural transformations and a rise in imports. Argentina, for instance, during the 1990s, promptly implemented all the recommendations of the Washington Consensus. This led to a process of over-indebtedness and capital flight that culminated in 2001 with the worst economic and social crisis in the country’s history. At the end of 2001, Argentina declared a partial default on its external debt of over US$100 billion, one of the largest sovereign debt defaults in world history (Dymski, 2003). The IMF continues to play a crucial role in restructuring and extending international financial capital’s dominion over local productive resources, arbitrating disputes between social classes within countries, and furthering the consolidation of a local capitalist class subordinate to the dictates and power of international capital (Siddiqui, 2022).

Global Debt Build-Up and Rising Interest Rates

Despite the fact that more than 80 percent of the 2023 debt build-up has come from the developed world—with the US, Japan, the UK, and France registering the largest increases—emerging markets have also seen significant rises, particularly in China, India, and Brazil. Rising prices and high inflation have led central banks to increase interest rates to try and contain inflation. Higher interest rates, in turn, mean higher loan repayments. Moreover, the increasing reliance on private creditors, who offer more expensive debt with shorter maturities than official sources, has further complicated debt restructuring for developing countries. Currently, private creditors hold 62 percent of external public debt, up from 47 percent a decade ago. This disparity in interest rates highlights the inherent inequality in the international financial system, burdening developing countries disproportionately. Today, half of all developing nations spend a minimum of 7.4 percent of their export revenues on servicing external public debt (Siddiqui, 2018).

Conclusion

Nearly one hundred years ago, J.M. Keynes warned about the dangers of an unsustainable debt burden imposed on Germany by the victorious powers at Versailles. The aftermath of World War I left many European countries, particularly the defeated ones, grappling with unsustainable war debt. The US emerged as the largest creditor nation, lending money to Germany so it could repay its war debt to the UK, France, and the Netherlands (Siddiqui, 2019). These countries then used German debt payments to pay down their own war debts to the US. This intricate web of debt payments kept tensions high and contributed to the economic crisis that led to the Great Depression in 1929. In 1933, a conference in London aimed at economic recovery failed, further deepening the crisis and contributing to the tensions that led to World War II.

In 2022, developing countries paid an unprecedented $443.5 billion to service their external public and publicly guaranteed debt, according to the World Bank’s International Debt Report 2023. When low-income developing countries face debt distress, it often leads to “protracted recessions, high inflation, and fewer resources going to essential sectors like health, education, and social safety nets, with a disproportionate impact on the poor,” according to the World Bank. Debt distress occurs when a country cannot fulfil its financial obligations, such as debt repayments. The IMF and World Bank believe that 60 percent of low-income developing countries have reached a critical point, which significantly hampers developmental programs.

As of May 2024, global debt has reached a total of US$305 trillion, increasing due to compounding shocks such as COVID-19 and the war in Ukraine. Developing countries, in particular, saw external debt levels grow by over 15% last year compared to pre-pandemic levels, according to the UN Report. This increase has driven up debt servicing costs, straining less developed countries and international financial lending institutions.

The study finds that international financial institutions like the IMF and World Bank continue to play a crucial role in restructuring debt, often extending international financial capital’s control over local resources. There is increasing pressure on developing countries to favor trade and financial liberalization, which can prevent them from strengthening and diversifying their economies. These countries need “degrees of freedom” to develop their economies according to local needs, free from the constraints of international finance.

Today, the challenge for progressive forces in the Global South is to promote regional economic cooperation and organize a countervailing opposition that can limit the IMF and World Bank’s influence. This would allow these countries to pursue development paths that are more aligned with their unique economic and social contexts.

About the Author

Dr Kalim Siddiqui is an economist specialising in International Political Economy, Development Economics, International Trade, and International Economics. His work, which combines elements of international political economy and development economics, economic policy, economic history and international trade, often challenges prevailing orthodoxy about which policies promote overall development in less-developed countries. Kalim teaches international economics at the Department of Accounting, Finance and Economics, University of Huddersfield, UK. He has taught economics since 1989 at various universities in Norway and the UK.

References

- Arellano, C.; Bai, Y. and Mihalache, G. (2024) “Deadly Debt Crises: COVID-19 in Emerging Markets”, Review of Economic Studies, 91 (3): 1243–1290.

- Dymski, G. (2003) “The International Debt Crisis”, in Edi by J. Michie, The Handbook of Globalisation, London: Edward Elgar.

- IMF. (2023) World Economic Outlook updated, Washington DC.

- Siddiqui, K. (2024) “Neocolonialism: An analysis of international factors on the development of the Global South” World Financial Review, December-January. pp.2-12.

- Siddiqui, K. (2022) “Capitalism, Imperialism, and Crisis”, European Financial Review, June/July, p.16 – 32.

- Siddiqui, K. (2019). “Government Debts and Fiscal Deficits in the UK: A Critical Review” World Review of Political Economy, 10(1): 40 – 68.

- Siddiqui, K. (2018). “Capitalism, Globalisation and Inequality” World Financial Review, November-December, p.72 – 77.

- Siddiqui, K. (1996) “The Debt Crisis – Need for a New Strategy”, The News, 17th May.

- Stiglitz, J. and Rashid, H. (2020) “Averting Catastrophic Debt Crises in Developing Countries”, Centre for Economic Policy Research, July, Columbia University.

- UN (2023) A World of Debt: A Growing Burden to Global Prosperity, July, New York: United Nations. 2023_07-A-WORLD-OF-DEBT-JULY_FINAL.pdf (un.org)

- Wade, R. (2023) “The World Development Report 2022: Deepening Economic Crisis Recovery in the Context of the International Debt Crisis”, Development and Change 2023; 54(5): 1354–1373.

- World Bank (2023) World Development Indicators. Washington DC. https://databank.worldbank.org/source/world–development–indicators#

{kind=link}