")

In an era increasingly shaped by trade wars and shifting geopolitical priorities, Kalim Siddiqui explores the United States’ departure from its longstanding commitment to free trade. The article offers a critical analysis of how the world’s leading economy has turned to tariffs, unilateralism, and protectionist measures to reassert its global economic influence.

I. Introduction

President Donald Trump’s imposition of sweeping tariffs—widely regarded as the most significant protectionist measures in over a century—marked a dramatic shift in United States (US) trade policy. Trump called it as a “Liberation Day,” the ensuing trade war disrupted global markets, erasing an estimated US$6.6 trillion in value within just 48 hours worldwide. A large portion of that was from US markets, but it’s not exclusive to the US. It represents a broader global market value loss tied to fears about disrupted trade, uncertainty, and slowed growth due to the trade war. In swift retaliation, China imposed reciprocal tariffs and blacklisted American firms, and tightened export controls on rare earth minerals essential to high-tech industries.

The US is effectively turning its back on a trading system that has long served it well. For nearly eighty years, the US has greatly benefited from trade liberalization. While it has consistently run a trade deficit in goods, but it maintains a surplus in services—an area in which it is the world’s leading exporter.

Trump’s tariff strategy was unlikely to succeed for several reasons. Most importantly, his effort to “stop China” in key sectors such as technology failed to account for the complexities of highly integrated global supply chains. His belief that the US should maintain a bilateral trade balance with every country reveals a fundamental misunderstanding of global economics (Siddiqui, 2025). In today’s interconnected world, trade imbalances naturally arise from comparative advantage and specialization. By attempting to reduce the US trade deficit through broad tariffs—primarily targeting China and the European Union (EU)—Trump inadvertently strengthened the dollar by attracting global capital inflows. This, in turn, will make the US exports less competitive on the global stage (The Guardian (2025a).

Moreover, true structural reform would require challenging the privileged status of the US dollar as the world’s primary reserve currency—a move that would undermine the US financial hegemony (Siddiqui, 2024a). One probable objective of these tariffs was to force China and the EU into a currency revaluation similar to the 1985 Plaza Accord. That agreement led to a significant decline in Japanese exports and contributed to decades of economic stagnation. Yet, unlike 1980s Japan—a US ally with limited geopolitical leverage—China is neither defeated nor dependent. It is an ascendant power with growing influence. The contrast is underscored by the enduring US military presence in Okinawa, where over 53,000 American troops remain stationed, highlighting the historical asymmetry between the two cases.

Rather than adapting to an increasingly multipolar global order, the US appears committed to preserving its hegemonic status. In pursuit of this objective, it has employed a combination of strategic, economic, and diplomatic tools aimed at containing the rise of potential rivals—chiefly China—underscoring the geopolitical motivations behind its recent shift in trade policy (Siddiqui, 2020a).

There are indications that the US seeks to replicate the outcome it achieved with the Soviet Union: internal collapse driven by economic and systemic pressure. While the Soviet Union achieved significant technological and industrial advancements between the 1950s and 1970s, it ultimately failed to increase the production of consumer goods and improve living standards, contributing to its eventual disintegration in 1990. However, the analogy with China is limited. Unlike the Soviet Union, China has actively expanded its trade and investment ties, particularly within East Asia. Since its accession to the World Trade Organization (WTO) in 2001, economic integration between China and its regional neighbours has deepened significantly, creating a resilient and dynamic network that distinguishes China’s position from that of the Soviet Union (Siddiqui, 2024b).

China is unlikely to agree to a significant revaluation of the renminbi (yuan) merely to address the US trade deficit. Trump’s twin objectives—reducing the trade deficit while preserving dollar hegemony—are, in fact, mutually exclusive. Protectionist measures alone are insufficient to correct structural imbalances in the economy. Without a broader overhaul of the international monetary and trading system, such policies are more likely to accelerate a shift away from US economic primacy than reinforce it (Siddiqui, 2020b).

Over the past eight decades, the trajectory of US trade policy has undergone dramatic shifts: from protectionism during the interwar period, to liberalization in the postwar era, and more recently, a return to protectionist tendencies. During the Great Depression, the US President Herbert Hoover signed the Smoot-Hawley Tariff Act of 1930, raising average import duties by approximately 20% in an attempt to shield domestic industries. However, the act provoked retaliatory tariffs from major trading partners, severely disrupting global commerce and exacerbating the global economic downturn.

In contrast, the post–World War II era witnessed a fundamental transformation in US trade policy. With much of Europe and Asia in ruins, the US emerged as the dominant economic power and championed a liberal trade agenda. It spearheaded the creation of multilateral institutions like the General Agreement on Tariffs and Trade (GATT) and, later, the WTO to promote open markets and lower trade barriers. Trade liberalization proved highly beneficial for the US; despite comprising only 4% of the global population, the US produced more than half of the world’s manufactured goods during this period (Siddiqui, 2016).

The dissolution of the Soviet Union in 1991 further solidified US economic leadership and deepened its commitment to globalization, capital mobility, and market integration. However, recent years have seen a resurgence in the US of protectionist sentiment in response to rising trade deficits, industrial decline, and widening income inequality. Today’s economic nationalism unfolds in a very different international environment, as the Global South—especially many East and Southeast Asian nations—has achieved rapid industrialization, with China emerging as a key technological and manufacturing power.

The US was instrumental in initiating the contemporary phase of globalization, driven largely by the goal of maximizing multinational corporations’ profitability. Rising labour costs at home spurred firms to shift production to low-wage countries, notably China, to enhance returns on investment, maintain low production costs, and contain inflation. However, offshoring also brought domestic challenges: it contributed to job losses in the US and eroded the bargaining power of labour unions (Siddiqui, 2012).

Over the past several decades, US-driven globalization—enabled by liberalized capital flows and trade agreements—has not only expanded global trade volumes but also transformed the organization of production. Whereas goods were once manufactured entirely within a single country, modern production is characterized by geographic fragmentation and cross-border interdependence. This evolution has elevated the strategic importance of supply chain management (SCM), which coordinates and optimizes the flow of materials, finances, and information from raw materials to finished products. Effective SCM can drive improvements in efficiency, cost reduction, and customer satisfaction, providing firms a crucial competitive edge in an increasingly interconnected global market.

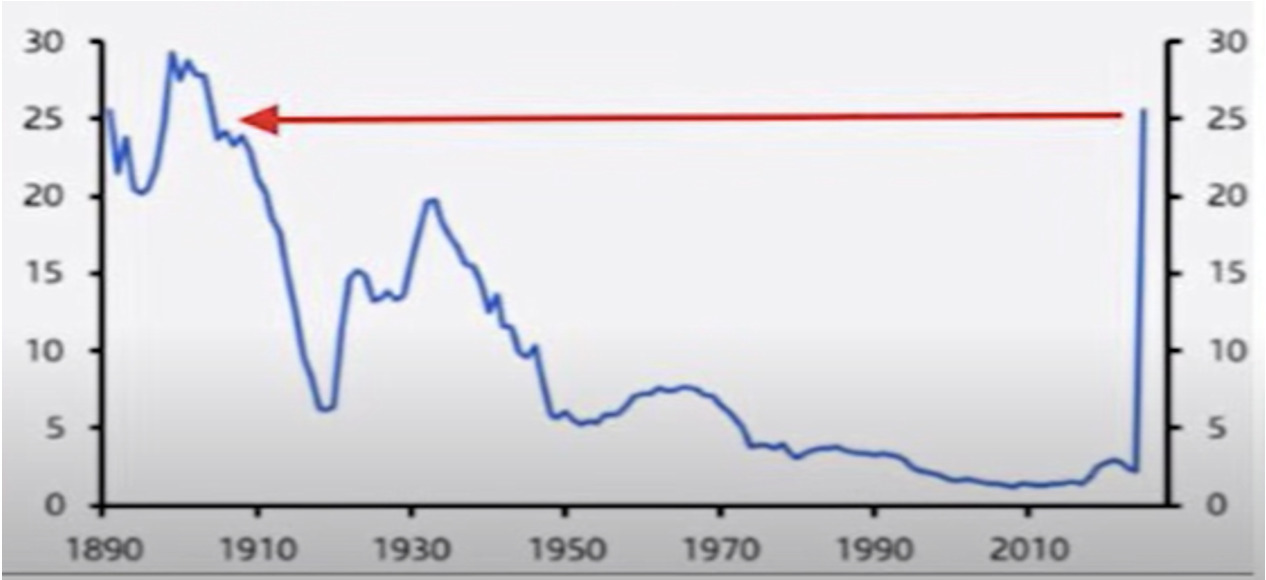

Despite the sophistication of today’s supply chains, President Donald Trump’s recent imposition of tariffs on US imports (see Figure 1) underscores a policy approach aimed at correcting trade imbalances and generating federal revenue. However, such measures overlook the potential for retaliatory actions by key trading partners, thereby risking further disruption of global trade systems and undermining the intended economic benefits (The Guardian (2025b).

II. The Limits and Complexities of Tariff-Based Industrial Revival

Rather than engaging in direct economic competition with China, the US appears to be adopting a strategy to disrupt China’s economic ascent. This strategy includes punitive tariffs, restrictions on Chinese access to advanced technologies, and an assertive military posture intended to encircle China. At the same time, the US has provided both rhetorical and material support to dissident groups among China’s minorities. Collectively, these measures signal a broader strategic objective: preventing China from emerging as a serious rival to US global hegemony (Siddiqui, 2018a).

The recent US-led trade war is emblematic of this approach. Rather than constituting a conventional trade dispute, it is designed to destabilize the global economy, reverse the momentum of globalization, and introduce inflationary pressures and uncertainty into international markets. Such a policy, however, carries significant risks and unintended consequences—not only for China but for the global economy and the US itself.

Tariffs can yield short-term benefits by shielding domestic industries from foreign competition, but this protection often comes at a cost. When firms are insulated from competitive pressures, they may have fewer incentives to innovate, improve efficiency, or diversify consumer offerings, ultimately undermining long-term productivity and economic dynamism. While many nations, including the US, have historically used tariffs to nurture infant industries, such strategies rely on careful implementation and are limited in scope (Siddiqui, 2018b).

The current US turn toward protectionism represents a stark departure from its longstanding commitment to free trade—a system it once helped establish and promote. Today, however, the US criticizes this system as inherently unfair. This pivot adversely impacts developing countries, which are forced to purchase higher-priced American goods, thereby deepening debt burdens and exacerbating economic hardship across the Global South.

Historically, manufacturing was the backbone of the US economy, generating substantial profits during the 1950s (Siddiqui, 1995). By the 1980s, however, rising labour costs and declining industrial profitability spurred a shift toward high-value sectors such as banking, finance, information technology, and digital services. This economic transformation has persisted into the present; in 2024, the US exported over US$1 trillion in services—more than any other country—underscoring its dominance in high-value industries.

Figure 1: The United States Effective Tariff Rate from 1890 to April 5, 2025 (%).

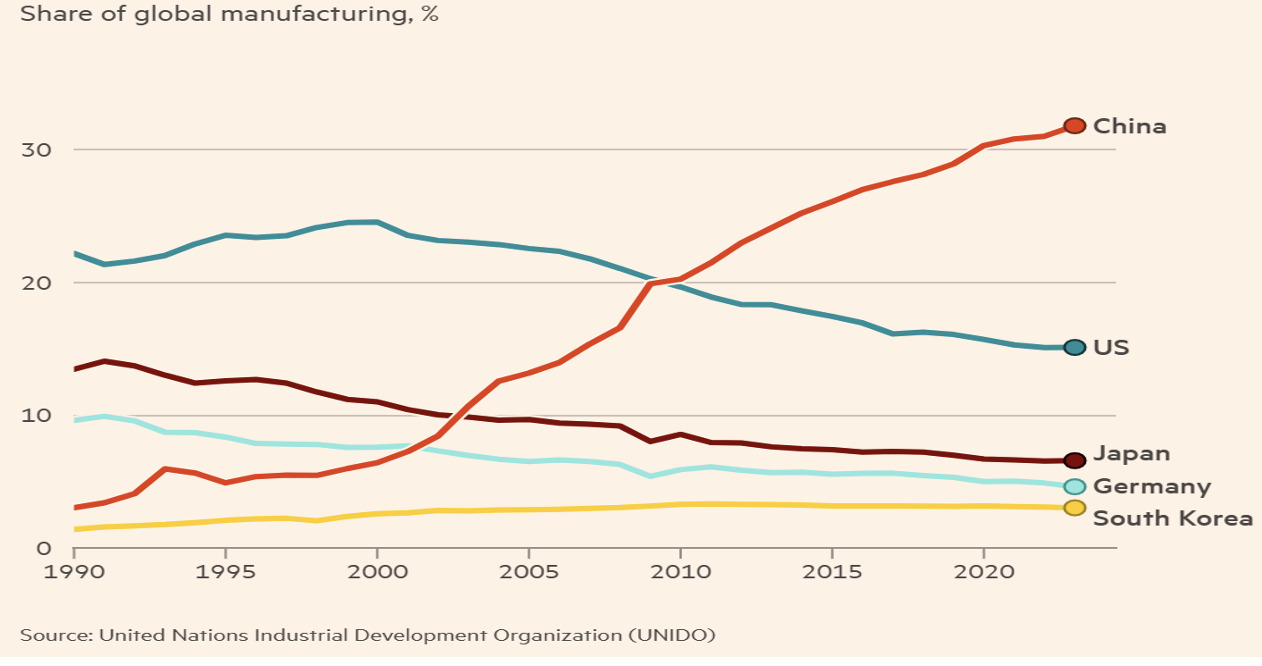

Figure 2: Share of Global Manufacturing by Major Economies from 1990 to 2024 (%).

Significant structural changes have reshaped the US economy over the past several decades. In 2024, only 9% of the American workforce was employed in the manufacturing sector—a stark contrast to 1980, when manufacturing accounted for approximately 39% of total employment. Similarly, manufacturing now constitutes just 10.2% of the US GDP, amounting to $2.3 trillion. When considering both direct and indirect contributions, manufacturing accounts for 17.1% of total GDP. While this remains a substantial component of the economy, its relative importance has declined in comparison to dominant sectors such as services, healthcare, education, and finance.

The erosion of the US manufacturing base is not limited to employment and output; it has also had profound implications for industrial capacity and supply chain sovereignty. For instance, the production of complex consumer electronics like the iPhone depends on components such as batteries, semiconductors, and rare earth elements—none of which are manufactured at scale within the US. Instead, these components are sourced from international supply chains, particularly in East and Southeast Asia. Decades of offshoring have not only displaced industries and skilled labour, but also undermined domestic entrepreneurship, manufacturing ecosystems, and technical expertise.

As illustrated in Figure 2, the share of global manufacturing attributable to the US has declined sharply over time. In contrast, China’s share has surged—from negligible levels in 1990 to over 30% in 2024, making it the world’s largest manufacturer. Japan and Germany have experienced gradual declines in their manufacturing shares over the same period, while South Korea has seen modest growth.

Furthermore, in recent decades, US corporations have increasingly prioritized short-term shareholder value over long-term productivity and innovation. Over the past thirty years, many US firms have directed the majority of their profits toward dividend payments and stock buybacks, often at the expense of capital reinvestment, research and development, and workforce training. This short-termism has contributed to a weakening of industrial competitiveness and a diminished capacity for technological leadership.

III. Historical Precedents of Protectionism and Industrial Policy

Historically, virtually all now-developed countries employed protectionist policies during their early stages of industrialization. In the US, for instance, Alexander Hamilton championed the use of tariffs in the early 19th century to promote domestic industries. Similar strategies were implemented earlier in Britain, and later adopted in Germany and Japan, as integral components of broader industrial development agendas. Effective industrialization typically requires more than just shielding select sectors from foreign competition. It also demands comprehensive policy support, including investments in education and skill development, the cultivation of a capable labour force, access to affordable credit, favourable interest rates, and coordinated industrial planning. Building a robust and competitive industrial base necessitates long-term strategic commitment—sporadic factory investments or isolated policy interventions are insufficient to generate sustained growth and technological advancement.

Moreover, the imposition of tariffs does not automatically lead to industrial revival. The relocation of manufacturing operations is costly, time-consuming, and often infeasible unless firms are assured that such tariffs will be maintained over the long term. If viewed as temporary or politically unstable, tariff regimes may discourage companies from reshoring production. Poorly conceived protectionist measures can also lead to higher operational costs and reduced global competitiveness. At the macroeconomic level, tariffs frequently result in elevated consumer prices, contributing to inflationary pressures. When combined with rising inequality and stagnant wages, this can suppress aggregate demand and, in severe cases, trigger economic slowdowns or recessions.

Contemporary economic discourse remains heavily dominated by neoclassical paradigms that prioritize market efficiency while neglecting structural inequality. This intellectual orthodoxy bears a resemblance to the role played by the Catholic clergy in the Middle Ages—when natural disasters were often attributed to the moral failings of the poor, thereby absolving elites and rulers of responsibility. Similarly, modern economic narratives tend to individualize poverty and underdevelopment, often framing them as consequences of personal failings rather than systemic injustices. This tendency obscures the structural advantages enjoyed by economic elites and impedes critical engagement with wealth concentration, inequality, and the status quo (Siddiqui, 1989).

Historically, the consequences of free trade in colonial contexts have often been devastating. One of the most tragic examples is the Irish Famine of 1846–1848, precipitated by a potato blight that decimated the staple food crop. The humanitarian crisis was exacerbated by several structural factors, including overreliance on a single crop, a deeply exploitative system of absentee landlordism, and the inadequate relief efforts of the British colonial administration. Despite the mass starvation, substantial quantities of food—such as wheat and livestock—continued to be exported from Ireland, primarily to England. This paradox of food exports amid widespread famine intensified the suffering, ultimately claiming over a million lives and forcing another million to emigrate, mainly to North America and Australia.

Charles Edward Trevelyan, then British Secretary to the Treasury, notoriously remarked that “God’s judgment sent the calamity to teach the Irish a lesson… Plague is an effective mechanism to control the population.” His comments encapsulated a broader colonial mindset that dehumanized colonized populations and rationalized state inaction. A similar pattern played out decades earlier during the Bengal Famine of 1770 under the rule of the British East India Company. Roughly one-third of Bengal’s population—over 10 million people—perished as colonial authorities failed to provide meaningful relief. In both instances, British officials invoked Malthusian theories to justify neglect, framing mass death as a natural corrective rather than acknowledging the structural causes and administrative failures that exacerbated the disasters (Siddiqui, 2020c).

IV. Economic Size, Growth Trajectories and Trade Flows

As of January 2025, the US boasts a Gross Domestic Product (GDP) of approximately US$25.5 trillion, compared to China’s US$18 trillion. On a per capita basis, the US leads with an income of US$82,800, while China’s per capita income stands at about US$12,600. Looking ahead, forecasts for 2025 expect the US GDP to grow at an annual rate of approximately 2.4%, whereas China’s economy is anticipated to expand by 4.8%. Collectively, these two economic giants account for nearly one-third of global trade, highlighting their central roles in the international economic order.

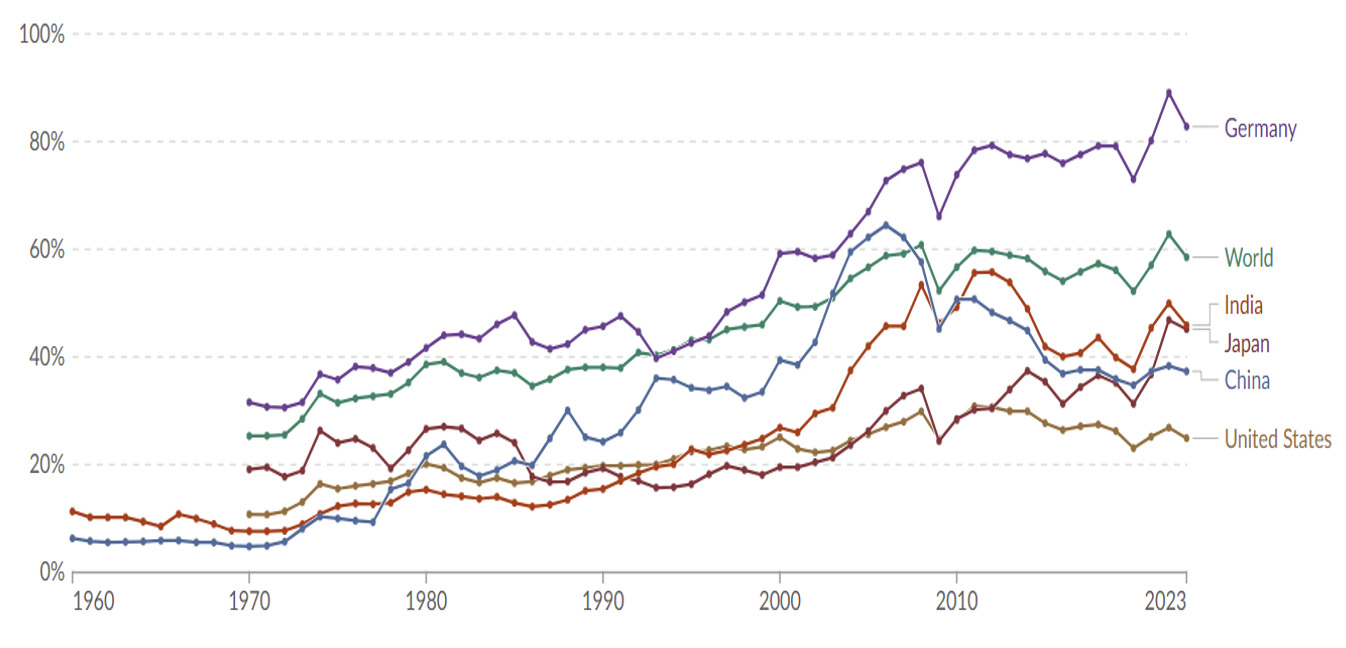

International trade expressed as a percentage of the GDP (sum of exports and imports of goods and services, divided by gross domestic product). Trade has expanded markedly over the past few decades, as illustrated by Figure 3. However, since the onset of the global financial crisis in 2008, there has been a notable decline in the share of trade relative to GDP, particularly in China. In response to the crisis, China adopted an inward-focused economic strategy, investing heavily in domestic infrastructure and services to stimulate internal markets and boost employment (World Bank, 2025; Dadush, 2022).

Figure 3: Trade as a Share of GDP from 1960 to 2023 (%).

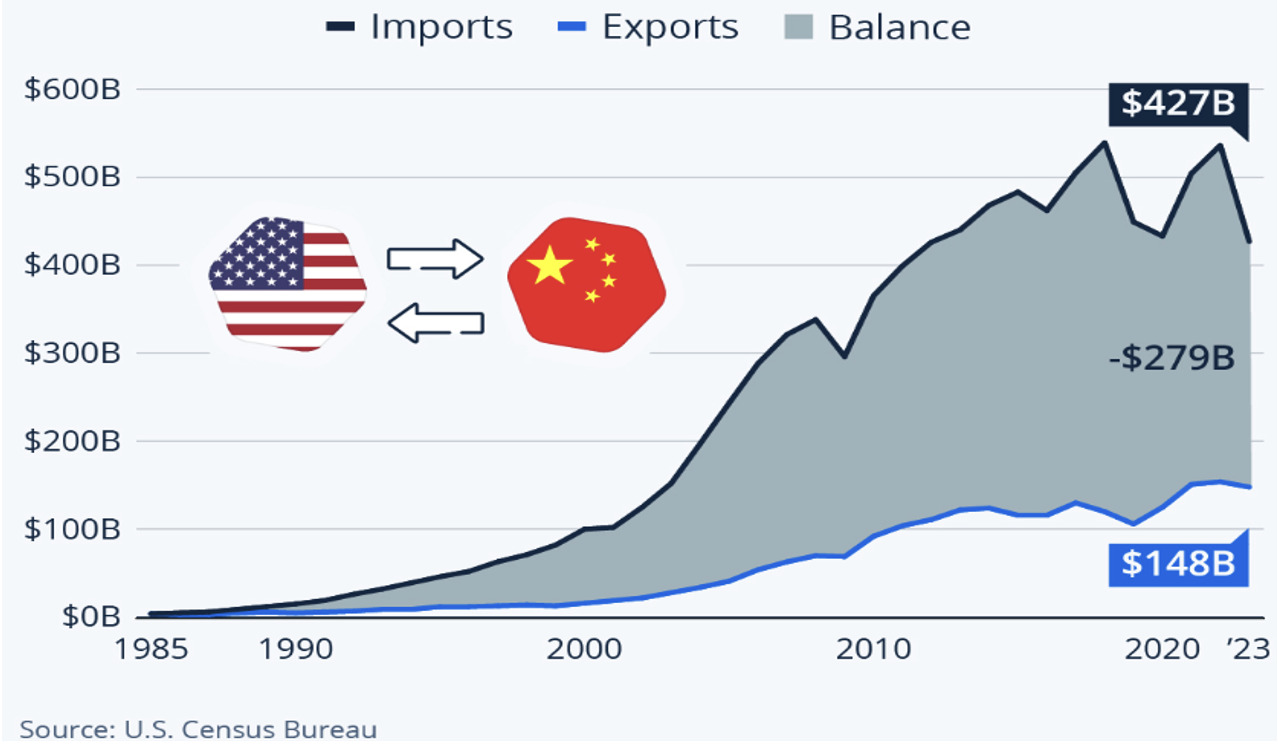

Trade between the US and China remains substantial. In 2024, bilateral trade totalled US$582.4 billion. US exports to China reached US$143.5 billion, while imports from China climbed to US$438.9 billion, resulting in a US trade deficit of US$295.4 billion. Comparatively, in 2023, US exports to China amounted to US$147.7 billion, with imports totalling US$426.8 billion, yielding a trade deficit of US$279.1 billion (see Figure 4). These figures underline the persistent imbalance between US exports and imports with China.

The structure of trade between the two nations reflects their distinct economic profiles. In 2024, US exports to China were primarily dominated by agricultural products—such as soybeans—and energy commodities like crude petroleum and petroleum gas. Conversely, US imports from China were centred on manufactured goods, including broadcasting equipment, computers, and office machine parts. This product composition underscores the differing competitive advantages: while the US excels in high-value agricultural and energy sectors, China maintains strength in the manufacturing of electronics and other consumer goods.

Figure 4: United States Trade Deficit with China from 1985 to 2023.

V. China’s Evolving Trade Network and Economic Diversification

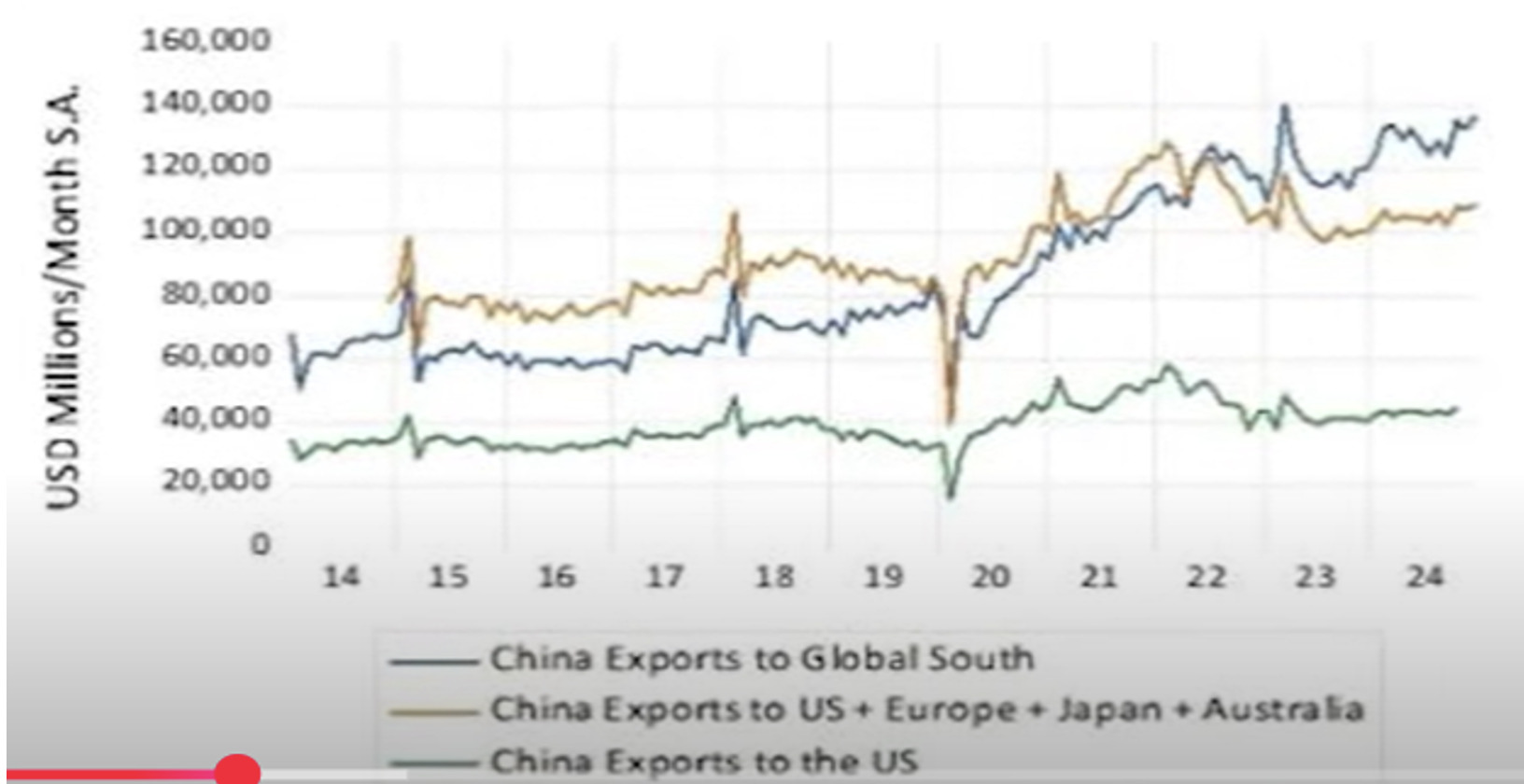

It is important to note that the global economic landscape has shifted considerably since 2018. In 2024, China’s trade strategy has evolved, with the nation diversifying its economic ties and increasingly relying on partners from the Global South. Contrary to earlier years when the US was China’s largest trading partner, recent data indicate that East Asian countries now dominate China’s trading relationships (see Figures 5a and 5b) Furthermore, China has broadened its trade network by expanding economic cooperation with Russia and other BRICS nations, leading to an export portfolio that now favours markets in the Global South over those in the Global North (Siddiqui, 2024c).

Under the auspices of the Belt and Road Initiative (BRI), China has sought to boost its export capacity globally. As a result, in 2024, 47% of China’s exports were directed to markets outside of the US (See Figure 6). In stark contrast, only 13% of China’s total exports were destined for the US market in 2024—down from 23% in 2018. Despite this diversification, however, certain product categories—particularly electronics and raw materials crucial for manufacturing—remain heavily reliant on access to the US market. This dual strategy of diversification combined with selective dependency underscores China’s efforts to rebalance its international trade relationships while maintaining competitive strengths in key sectors (Siddiqui, 2021).

Figure 5a: China to US Trade, April 5, 2025.

Figure 5b: China’s Exports to the world from 2014 to 2024.

Figure 6: China’s Key Exports Destinations in 2023.

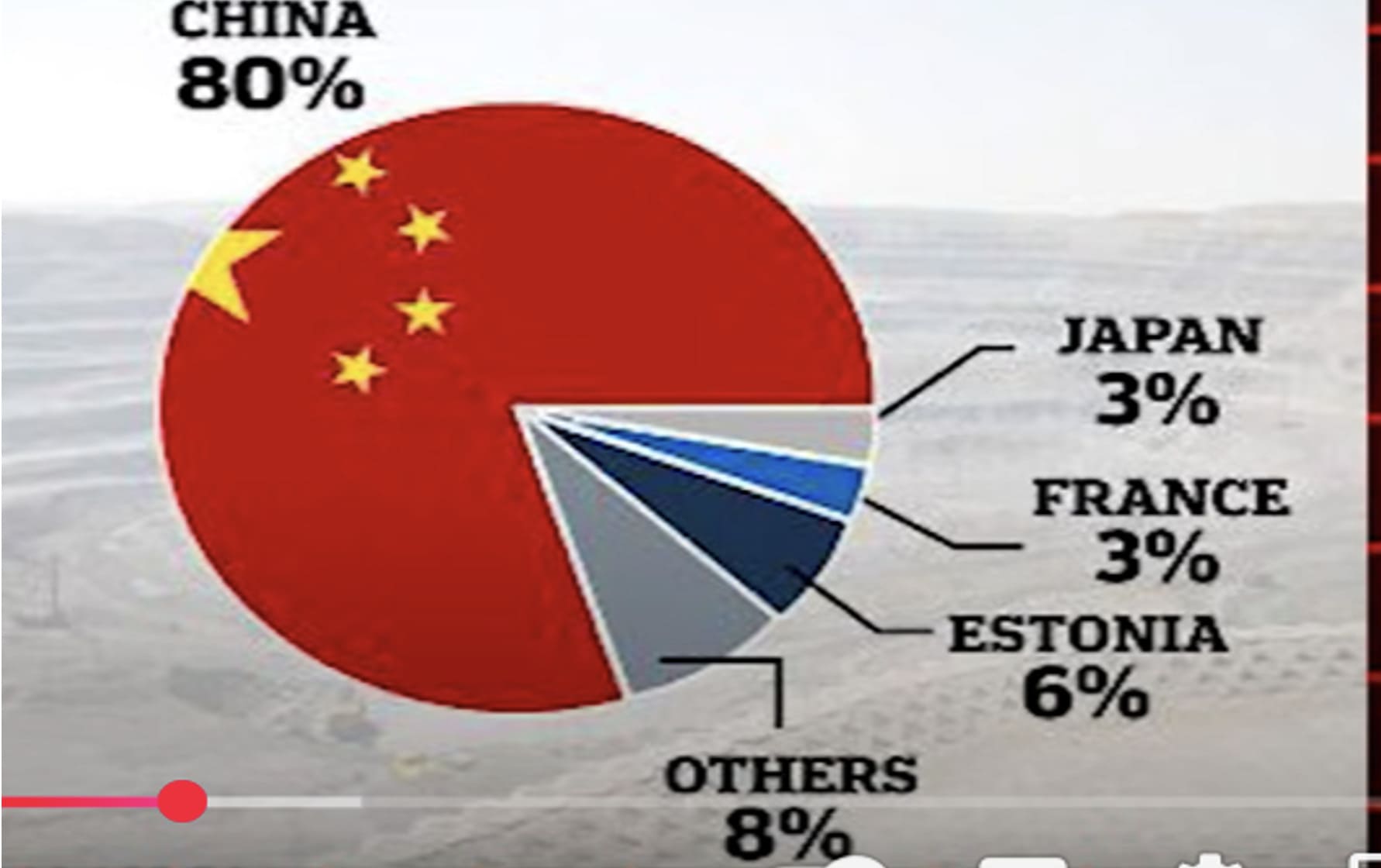

Figure 7: Rare Earth Materials Suppliers to the United States, April 5, 2025.

VI. Strategic Economic Interdependencies and Supply Chain Vulnerabilities

In 2024, China continued to consume 14% of total US agricultural exports—valued at approximately US$27 billion. However, recent months have witnessed a marked shift: China has increasingly sourced food from Argentina, Brazil, and Russia, as it pursues a dual strategy of diversifying its import partners and bolstering domestic production. This strategy includes significant investments in domestic food cultivation, initiatives to reclaim unproductive desert and coastal lands for agriculture, and the development of a comprehensive food safety policy.

Beyond agriculture, critical sectors such as pharmaceuticals remain intertwined with Chinese supply chains. The US pharmaceutical industry, for instance, relies heavily on China for vital active pharmaceutical ingredients (APIs), with India serving as a secondary supplier. Without this crucial input from China, production of many essential medicines could face severe disruption. Similarly, China plays a key role in supplying rare earth materials to the US—a dependency underscored in Figure 7—with tariff impositions likely to adversely affect American companies that depend on these raw materials.

Regarding US tariffs, Elliott (2025) observes: “It is not only the multilateral economic system that is under assault, but every single pillar of the rules-based order, from respect for the law to the self-determination of nations and historic commitments to humanitarian aid. Indeed, we are seeing a simultaneous breakdown in economic and geopolitical orders … The US exports less to China than its imports from China, and this gap has widened since China joined the WTO in 2001. China now exports products such as electronics and machinery to the US market, earning its reputation as the ‘world’s factory.’ Trump seeks to reverse these trends by imposing tariffs on Chinese imports. However, in recent years, China has significantly reduced its dependence on the US market by redirecting trade toward other emerging economies. The overall result, some argue, will be higher consumer prices, slower economic growth, and potentially a recession in the US, as its trade deficit with China accelerated post-2001. In 2024, China exported only 13% of its goods to the US—a decline from 23% in 2018.”

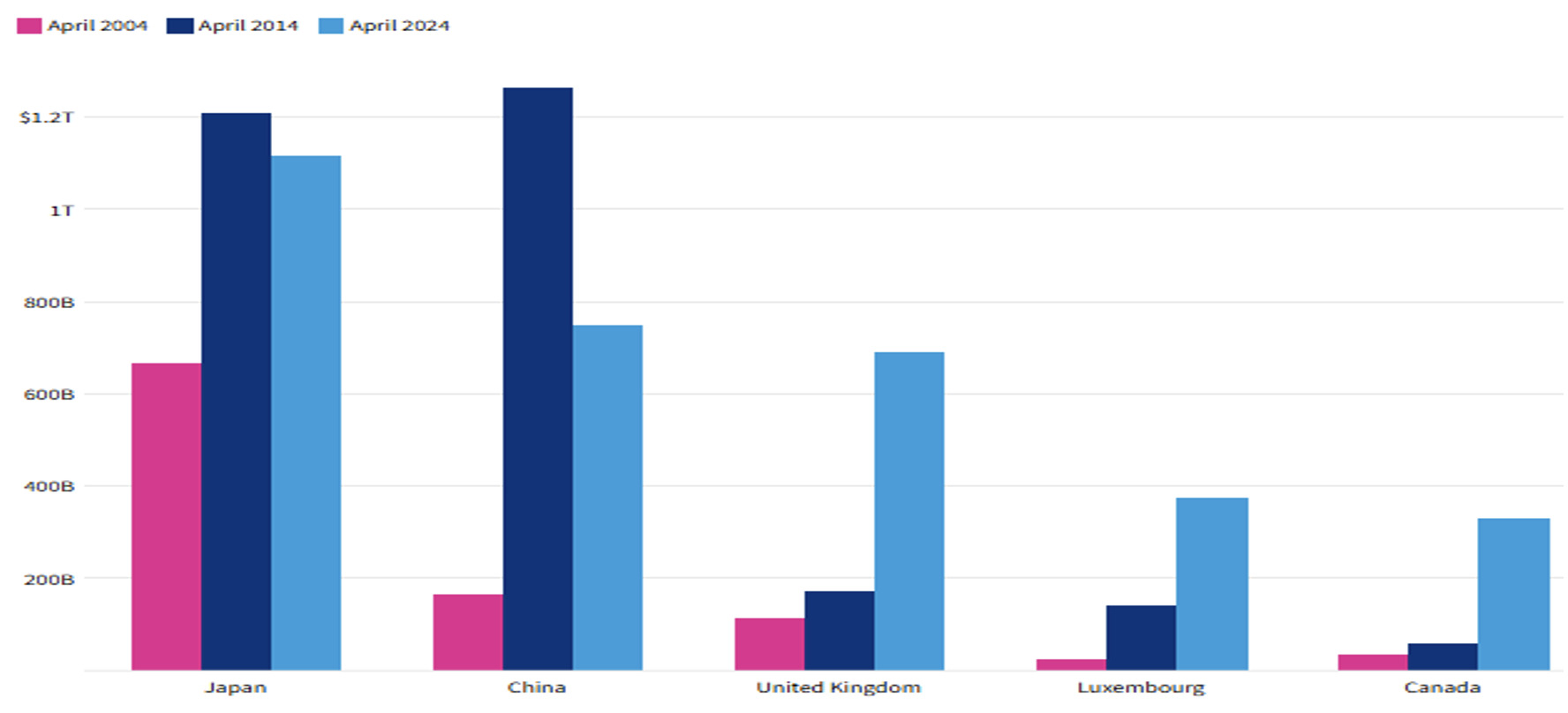

China has long reinvested its export surpluses into US assets, particularly Treasury bonds, helping to finance US fiscal deficits, support the dollar, and fuel import growth. As of April 2024, foreign entities hold about US$7.9 trillion in US Treasurys—22.9% of total US debt. The top five holders are Japan ($1.1 trillion), China ($749 billion), the UK ($690.2 billion), Luxembourg ($373.5 billion), and Canada ($328.7 billion). In the early 2000s, China’s rapid growth and foreign investment led to massive foreign reserves, peaking at $1.3 trillion in US Treasurys in 2013 (see Figure 8). Recently, China has reduced its holdings, reallocating funds toward initiatives like the Belt and Road Initiative (BRI), into which it invested about $50 billion in 2023 to deepen global economic ties.

Figure 8: The United States Foreign-owned Debts in trillions of US dollars, April 10, 2024.

V. Conclusion

The US efforts to hinder China’s technological rise have largely fallen short. Despite banning key companies—such as those in 5G, semiconductors, and electric vehicles—China has become a global leader in 57 of 64 critical technologies by 2025, driven by its “Made in China 2025” strategy and strong government support that fostered domestic innovations like BYD and DeepSeek.

Globalization over the past forty years has produced integrated supply chains that rely on cost-effective international production. Companies like Boeing source components worldwide, making the prospect of recreating a complete domestic supply chain unrealistic given the specialized competencies developed abroad. US tariffs now risk disrupting these networks, leading to higher costs and inefficiencies.

Moreover, such tariffs hurt workers in both developed and developing countries. In the US, they can increase consumer prices and fuel inflation, while in the Global South, reduced exports and depreciated currencies tend to lower wages and exacerbate unemployment. Rather than rely on protectionism—which mainly shifts costs onto consumers and destabilizes trade—policymakers should consider economic decoupling from an overreliance on the US market. Strengthening trade cooperation and diversifying supply chains among major Global South economies (such as China, India, Indonesia, Iran, Malaysia, Russia, Brazil, Nigeria, and South Africa) can help mitigate tariff-induced disruptions and promote a more resilient, equitable global trading system.

About the Author

Dr. Kalim Siddiqui is an economist specializing in International Political Economy, Development Economics, Trade and Economic Policy. Since 1989, he has been teaching economics at various universities in Norway and the UK. Dr. Siddiqui’s research interests encompass a wide range of topics, including political economy, international trade, and economic history, South Asia, and emerging economies. He has presented papers at international conferences across numerous countries, reflecting his global engagement in the field. His scholarly pursuits span six broad domains: Political Economy, Development Economics, Economic History, Economic Policy, Globalization, and International Trade. Dr. Siddiqui has made significant contributions to research in areas such as trade policy, globalization, and political economy. His work has been published in chapters of edited books and articles published in peer-reviewed journals. For inquiries, Dr. Siddiqui can be reached at: [email protected]

Dr. Kalim Siddiqui is an economist specializing in International Political Economy, Development Economics, Trade and Economic Policy. Since 1989, he has been teaching economics at various universities in Norway and the UK. Dr. Siddiqui’s research interests encompass a wide range of topics, including political economy, international trade, and economic history, South Asia, and emerging economies. He has presented papers at international conferences across numerous countries, reflecting his global engagement in the field. His scholarly pursuits span six broad domains: Political Economy, Development Economics, Economic History, Economic Policy, Globalization, and International Trade. Dr. Siddiqui has made significant contributions to research in areas such as trade policy, globalization, and political economy. His work has been published in chapters of edited books and articles published in peer-reviewed journals. For inquiries, Dr. Siddiqui can be reached at: [email protected]

References

- Dadush, U. (2022) “Deglobalisation and Protectionism” Bruegel Working Paper, No. 18/2022, Bruegel, Brussels.

- Elliott, L. (2025) “I’ve seen many phoney trade wars come and go: This is the real thing” The Guardian, April 9, London.

- Siddiqui, K. (2025) “Donald Trump’s Tariffs: A Prelude to Global Trade Wars?” World Financial Review, April.

- Siddiqui, K. (2024a) “Trends and Prospects of De-Dollarization in the Rapidly Changing Global Economy” World Financial Review, Part One & Part Two, December.

- Siddiqui, K. (2024b) “China’s Growth Miracle and Development Strategy Since the 1980s” World Financial Review, December, pp.11-25.

- Siddiqui, K. (2024c) “The BRICS Expansion and the End of Western Economic and Geopolitical Dominance” World Financial Review, November.

- Siddiqui, K. (2021) “Trade Liberalisation, Comparative Advantage, and Economic Development: A Historical Perspective” World Financial Review, May.

- Siddiqui, K. (2020a) “Prospects of a Multipolar World and the Role of Emerging Economies” World Financial Review, November.

- Siddiqui, K. (2020b). “The US Dollar and the World Economy: A critical review” Athens Journal of Economics and Business. 6(1): 21 – 44.

- Siddiqui, K. (2020c) “The Political Economy of Famines under Colonial India: A Critical Analysis” World Financial Review, July.

- Siddiqui, K. (2018a). “US – China Trade War: The Reasons Behind and its Impact on the Global Economy” World Financial Review, November.

- Siddiqui, K. (2018b). “David Ricardo’s Comparative Advantage and Developing Countries: Myth and Reality” International Critical Thought 8(3): 1-28, September.

- Siddiqui, K. (2016). “International Trade, WTO and Economic Development” World Review of Political Economy, 7(4): 424 – 450.

- Siddiqui, K. (2012). “Malaysia’s Socio-Economic Transformation in Historical Perspective”, International Journal of Business and General Management 1(2): 1 – 50.

- Siddiqui, K. (1995) “The Myth of the Free Trade”, The Nation, January 13.

- Siddiqui, K. (1989) “Neo-Classical Economic Theory: A critical perspective” Klassekampen (in Norwegian) August 31& September 1, Oslo, Norway.

- The Guardian (2025a) “US-China trade war intensifies as Beijing’s tariffs come into effect after Trump pause” April 10, London.

- The Guardian (2025b) “Fundamentally wrong, brutal and paranoid’: how will the world respond to Donald Trump’s tariffs?” April 5, London.

{kind=link}