")

Critical raw materials (CRMs) such as lithium, cobalt, rare-earth elements, and copper are central to the green and digital transitions. Dr Kalim Siddiqui emphasises that their economic significance lies not only in enabling technologies—batteries, electric vehicles, renewable energy, and microchips—but also in the concentration of supply chains. China controls about 70 percent of global rare-earth output and 80–90 percent of processing capacity, creating systemic dependencies.

I. Introduction

Critical minerals—especially rare earth elements—are increasingly essential to reducing pollution, lowering carbon emissions, and driving technological innovation toward a more sustainable future. Their significance, however, extends beyond environmental benefits. For advanced economies, secure access to these materials has become a strategic priority, shaping industrial competitiveness and reinforcing corporate power, while simultaneously intensifying geopolitical rivalries over control of critical supply chains. Consequently, rare earth elements have emerged as both a foundation of technological progress and a source of global tension, fuelling new forms of geopolitical rivalry.

These critical raw materials are essential for renewable energy technologies, high-tech manufacturing, and advanced military systems, including electric vehicles, wind turbines, fighter jets, missiles, and radar. As economic historian from Columbia university Adam Tooze (2025) notes, “if fossil fuels heralded the industrial revolution with the West leading it, the green energy transition is clearly being led by Asia, with China as its global leader.” This shift underscores the growing strategic importance of rare earths in shaping global power dynamics.

Critical raw materials (CRMs) are indispensable for 21st-century economies, particularly in mitigating global warming and reducing pollution. The green and digital transitions rely heavily on resources such as lithium, cobalt, rare-earth elements, and copper, which are integral to batteries, electric vehicles, renewable energy systems, and microchips. This growing dependence on CRMs has generated new geopolitical vulnerabilities and dependencies, prompting strategies such as the European Union’s Critical Raw Materials Act, which seeks to diversify supply chains through domestic extraction, processing, and recycling (Brown, et al 2024).

This study examines the importance of CRMs in the coming decades, with a focus on their role in global production and supply. It also considers potential counterstrategies for reducing reliance on CRMs, including material substitution, reduced consumption, recycling, and re-use. The adoption of environmentally sustainable technologies (Siddiqui, 2025a) and new energy systems depends fundamentally on securing access to these materials. Yet the supply of CRMs remains heavily concentrated in the Global South and within a handful of large corporations, fuelling tensions among the developed countries.

Under capitalism, development is driven primarily by private corporations, where private investments play an important role in the overall grow. Most of the developing countries lack funds and modern technology to mine and processes the CRMs and convert them into finished products. The current energy transition is likely to reproduce the contradictory socio-spatial dynamics that characterized the carbon-based industrial revolution. These dynamics would likely exacerbate inequality while delivering transformative benefits primarily to the Global North.

The designation of CRMs as “critical” stems from their strategic significance across multiple sectors. They are essential not only to electronics and defence industries but also to renewable energy technologies such as solar panels, wind turbines, and electric vehicles. For instance: Lithium is crucial for batteries used in electric vehicles and renewable energy storage. Cobalt is a vital component in advanced batteries and other emerging technologies (Brown, et al 2024).

Many countries remain heavily dependent on a limited number of suppliers of CRMs—particularly China—for the processing and supply of critical raw materials, creating significant strategic vulnerabilities. In response, the European Union (EU) and the United States (US) have introduced policy initiatives, such as the EU Critical Raw Materials Act, aimed at strengthening supply chain security by enhancing domestic capabilities in mining, processing, and recycling. The availability of rare earths and other CRMs has become indispensable for the US, the EU, Japan, and other advanced economies, particularly given the global expansion of renewable energy technologies, digitalisation, and the proliferation of artificial intelligence–embedded devices.

For most CRMs, many countries are structurally import-dependent, with limited or no viable substitutes. Supply is further constrained by low recycling rates, technological challenges in recovery, and the concentration of production within a few dominant suppliers. This scarcity, combined with rising demand, has intensified global competition to secure access to key materials such as lithium, cobalt, copper, nickel, and other CRMs. Control over these resources is increasingly seen as essential for maintaining technological leadership in the 21st century (OECD, 2023).

According to the International Energy Agency (IEA), China’s dominance in the processing and refining of these minerals’ ranges from 80 to over 90 percent of global capacity, positioning it as a central actor in emerging technology and energy supply chains.

The US–China dispute over rare earths illustrates this vividly. During Trump administration’s tariff war (Siddiqui, 2025b), China temporarily suspended certain rare earth exports to the US because China produces about 70 percent of global output and controls roughly 90 percent of processing capacity, this moves exposed the US’s dependence. Alternative suppliers were unable to compensate for China’s dominance, forcing the US to negotiate for the resumption of supplies. This episode crystallized the geopolitical stakes of resource dependence: securing access to CRMs is now treated by the West as a matter of national security and technological survival.

The US now has sought to diversify its supply base, including exploring opportunities in Greenland and other territories rich in strategic minerals. Yet such alternatives cannot fully replace China’s dominance, since it possesses nearly half of known global reserves of rare earth elements (REEs). The REEs are a group of 17 metallic chemical elements—the 15 lanthanides, plus yttrium and scandium—that share similar properties, such as high conductivity, magnetism, and fluorescence. They are indispensable for high-performance magnets in wind turbines, electric motors, and other advanced applications. They are essential for modern technologies like wind turbines, electric vehicle motors, and consumer electronics, as well as for green energy initiatives (Goodenough, et al 2018).

II. Imperialism, Foreign Markets, and the Struggle for Critical Minerals

This reality resonates with the broader insight of Marxist scholar Rosa Luxemburg that imperialism functions not merely as a project of market expansion, but also as a means of securing indispensable resources beyond the reach of metropolitan capitalism itself. In the twenty-first century, this dynamic is exemplified by the struggle for critical minerals—lithium, cobalt, nickel, rare earths—which has become a defining axis of contemporary imperial rivalries. This phenomenon aligns with Lenin’s analysis of capitalist imperialism, which he theorized as a definitive, high-stage development of capitalism. In this stage, fundamental characteristics like free competition mutate into their opposites: monopoly. Lenin observed this transition as the concentration of production and capital inevitably displaces free competition with monopoly, creating large-scale industry that eliminates smaller competitors. This economic shift fosters a global hierarchy wherein monopolistic powers export capital to less developed countries in pursuit of higher profits, exploiting these regions and ultimately generating the international conflicts that characterize the imperialist epoch (Siddiqui, 2022).

The Industrial Revolution began in Britain, particularly in Manchester’s cotton textile industry, during the second half of the eighteenth century. Cotton manufacturing was driven by the application of new technologies that dramatically increased productivity. However, Britain neither cultivated the raw cotton required for textile production nor initially possessed the necessary expertise to establish large-scale cotton industries. To overcome these limitations, Britain relied heavily on its colonies—India, Egypt, and later the US—for the supply of raw materials. This reliance had devastating consequences for colonized economies. India’s flourishing textile industries, for example, were systematically dismantled, forcing the country to specialize in the production of raw cotton for British industry.

As British factories began producing textiles in bulk, the demand for foreign markets to absorb this output intensified. This demand was met through the deliberate destruction of India’s indigenous textile industry, which had long exported high-quality cotton and silk to global markets. Consequently, India was transformed from a leading exporter of textiles into a captive importer of British-manufactured goods. In short, the rise of industrial capitalism was predicated on the metropolis securing cheap raw materials from its colonies and dismantling their existing industries.

This dynamic has persisted into the present. While the composition of industrial output in advanced capitalist economies has changed over time—with new products replacing old ones—the structural dependence on external sources of raw materials remains. Many of these essential resources lie outside the territorial domain of metropolitan capitalism, yet their reliable supply remains crucial. Ensuring such access has historically provided, and continues to provide, a powerful motive for imperialist control over resource-rich regions.

In teaching political economy, I emphasize to my students that mainstream economics typically treats the supply of raw materials as if it occurs through “normal” commodity exchange in free markets. The assumption is that these resources are acquired voluntarily and without coercion. Historical reality, however, tells a different story. The extraction and trade of raw materials have long been shaped by colonial domination, coercion, and asymmetrical power relations. Mainstream economists, by ignoring these imperialist dimensions, erases the role of force and dependency in the global supply of raw materials (Siddiqui, 2018a).

A second argument often advanced by mainstream economists against the claim that capitalism drives imperialism concerns the relative insignificance of raw materials in the value composition of metropolitan output. Since the share of such inputs from the “outside” world appears small in quantitative terms, many mainstream economists dismiss the idea that advanced capitalist countries would undertake the immense costs and risks of imperialist expansion simply to secure resources that constitute a minor fraction of total output value.

Marxist scholars, however, have long challenged this reasoning. Harry Magdoff, in The Age of Imperialism (1969), argued that securing vital raw materials and other inputs from colonies has been a paramount necessity for metropolitan capitalism. Agricultural commodities and food crops have historically been central to this logic, as metropolitan powers sought to reorganise land use across the globe to serve both industrial needs and domestic consumption. For the purposes of this discussion, however, the focus is on minerals. The strategic dependence of metropolitan capitalism on external mineral supplies is starkly illustrated by recent US experiences with rare earth elements.

The economic ascent of Western Europe from the 16th to the 19th centuries was not an isolated phenomenon. It was fundamentally predicated on the large-scale extraction of wealth and resources from the global South. This presentation will argue that European capital accumulation and industrialization were directly fuelled by the systematic plunder of Latin America, Africa, and Asia, often through coercive and violent means.

For example, European powers, led by Spain, extracted thousands of tons of silver and significant quantities of gold. A primary source was the Potosí mines in modern-day Bolivia. This extraction is more accurately characterized as plunder rather than equitable trade. The immense influx of precious metals generated massive wealth for colonial powers but also triggered profound economic shifts in Europe, notably the so-called “Price Revolution,” a period of widespread inflation. Historical evidence demonstrates that European industrialization created an insatiable demand for raw materials, which was met through the coercion of African and Asian societies (Siddiqui, 2021).

This exploitative process culminated in the late 19th century with the “Scramble for Africa.” This period of intense imperial competition was fundamentally a race to claim and directly administer African territory and its vast resources, formalizing and intensifying patterns of extraction. This systematic transfer of wealth is central to explaining the “Great Divergence”—the period where Western Europe’s economic power dramatically outpaced the rest of the world. The capital and resources acquired through these practices were not merely supplemental; they were a critical precondition for European industrialization and global economic dominance (Siddiqui, 2018b).

During the Trump administration’s tariff disputes with China, China responded by temporarily suspending certain rare earth exports to the US. Given that China produces around 70 percent of global rare earth output and controls approximately 90 percent of processing capacity, this move left the US in a precarious position. Alternative suppliers could not compensate for China’s dominance, as no other country possessed comparable production capacity. As a result, the US was compelled to negotiate with China, linking the resumption of rare earth supplies to broader trade concessions.

This episode underscores the strategic vulnerability of advanced economies and highlights how access to critical minerals fuels imperialist expansion. In an effort to reduce reliance on Chinese supply, the US has pursued alternative sources, including Greenland, which is rich in a range of mineral resources. While American interest in Greenland predates the rare earth dispute, China’s temporary suspension of exports sharpened US strategic focus on the territory. Yet even these efforts cannot fully replace Chinese dominance, as China controls nearly half of the world’s known reserves of rare earths. This case encapsulates a central motivation for contemporary capitalist imperialism: the drive to secure and control indispensable raw materials, regardless of their proportionate share in the total value of metropolitan output.

Rosa Luxemburg is her book The Accumulation of Capital (1919) highlighted the importances of markets for imperialism, arguing that sustained capital accumulation within the metropolis was impossible without penetrating pre-capitalist markets abroad. For this reason, annexations and interventions in “outside” territories became a structural necessity. While other external stimuli for metropolitan capitalism can be identified—such as demand generated by the capitalist state—these have limited scope, especially in the era of globalization. By contrast, there are no substitute sources within the metropolis for the raw materials it requires. The quest for raw materials, and especially minerals, thus remains a permanent and indispensable motive for capitalist imperialism (Siddiqui, 2022).

The intensity of imperialist intervention has historically escalated whenever countries in the Global South have sought to assert sovereign control over their natural resources. After political decolonization, many states attempted economic decolonization by reclaiming authority over mineral wealth. These efforts often provoked violent backlash from metropolitan powers. The US- and Europe-backed coups against Mossadegh in Iran, Arbenz in Guatemala, Allende in Chile, and Lumumba in Congo were all directly tied to attempts at resource nationalization (Siddiqui, 2021).

With the consolidation of neoliberal globalization, direct coups became less frequent as structural adjustment programs, debt conditionalities, and trade liberalization restored metropolitan capital’s control over resource flows (Siddiqui, 2018a). This institutionalized dependency, embedding neocolonial relations in international financial and legal frameworks. Yet as the neoliberal order falters, US imperialism has sought to manage global imbalances by compelling Global South economies to specialize in raw material exports in order to earn foreign exchange and service external debts. These pressures have, in turn, reignited calls for a new international economic order and renewed struggles for resource sovereignty (Siddiqui, 2025a).

III. China’s Strategic Dominance: Processing as Power

In global supply chains for critical minerals, control over processing—not raw production—determines strategic power. China has secured dominance by investing heavily in refining and processing capacity, even when it is not the largest holder of reserves. China dominates the global rare earth supply chain, controlling roughly 70% of mining and over 90% of refining capacity. It produces around 92% of high-strength permanent magnets, critical for civilian and military applications. China has also strategically invested abroad, partnering with countries in Africa, Latin America, and Southeast Asia, including the Congo, Bolivia, Chile, and Myanmar, often linking mineral extraction with infrastructure under the Belt and Road Initiative (Siddiqui, 2019).

This dominance allows China to exercise leverage over global technology and defence sectors. Even countries rich in raw materials, such as Australia and Vietnam, remain dependent on Chinese refining capabilities, illustrating the structural asymmetry in global mineral supply chains. For example, in the case of natural graphite—vital for batteries, lubricants, and industrial applications—China accounts for about 72% of global production but controls 100% of processing capacity. All graphite destined for global markets must therefore pass through Chinese facilities. While China holds roughly 28% of global reserves, Brazil follows closely with 26%. New suppliers, such as Mozambique (10% of production) and Madagascar (8%), have entered the market, but without processing plants they remain dependent on external technology and investment, leaving China’s dominance intact.

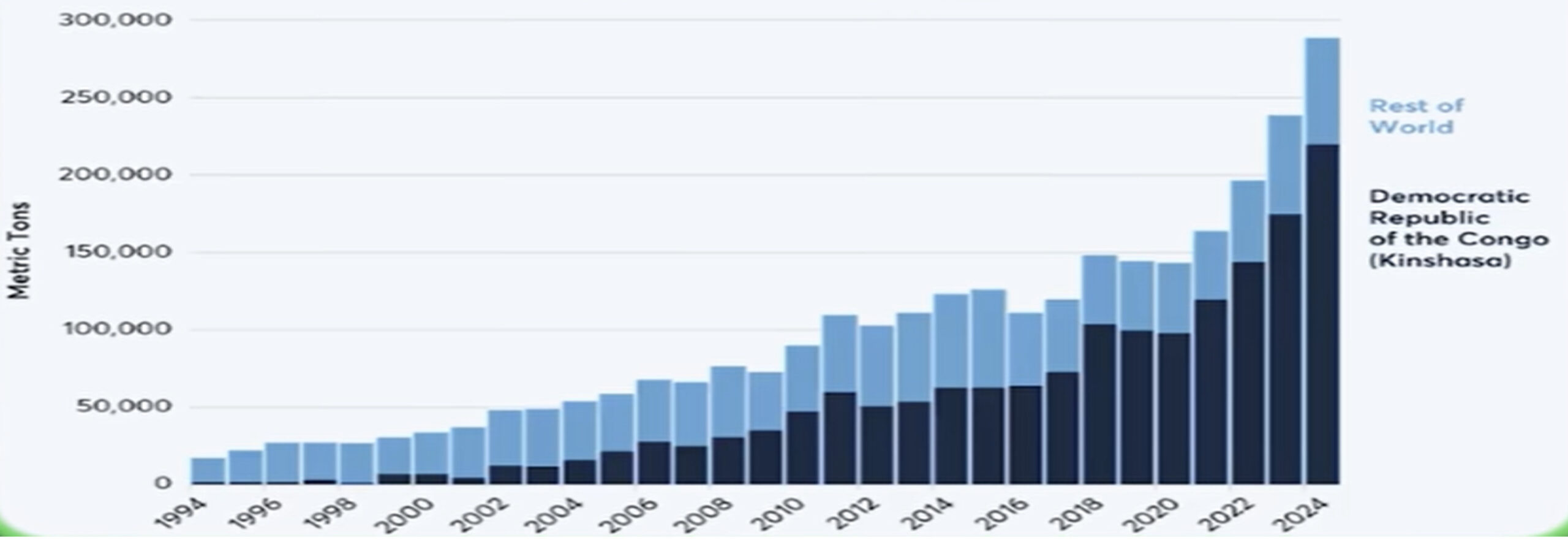

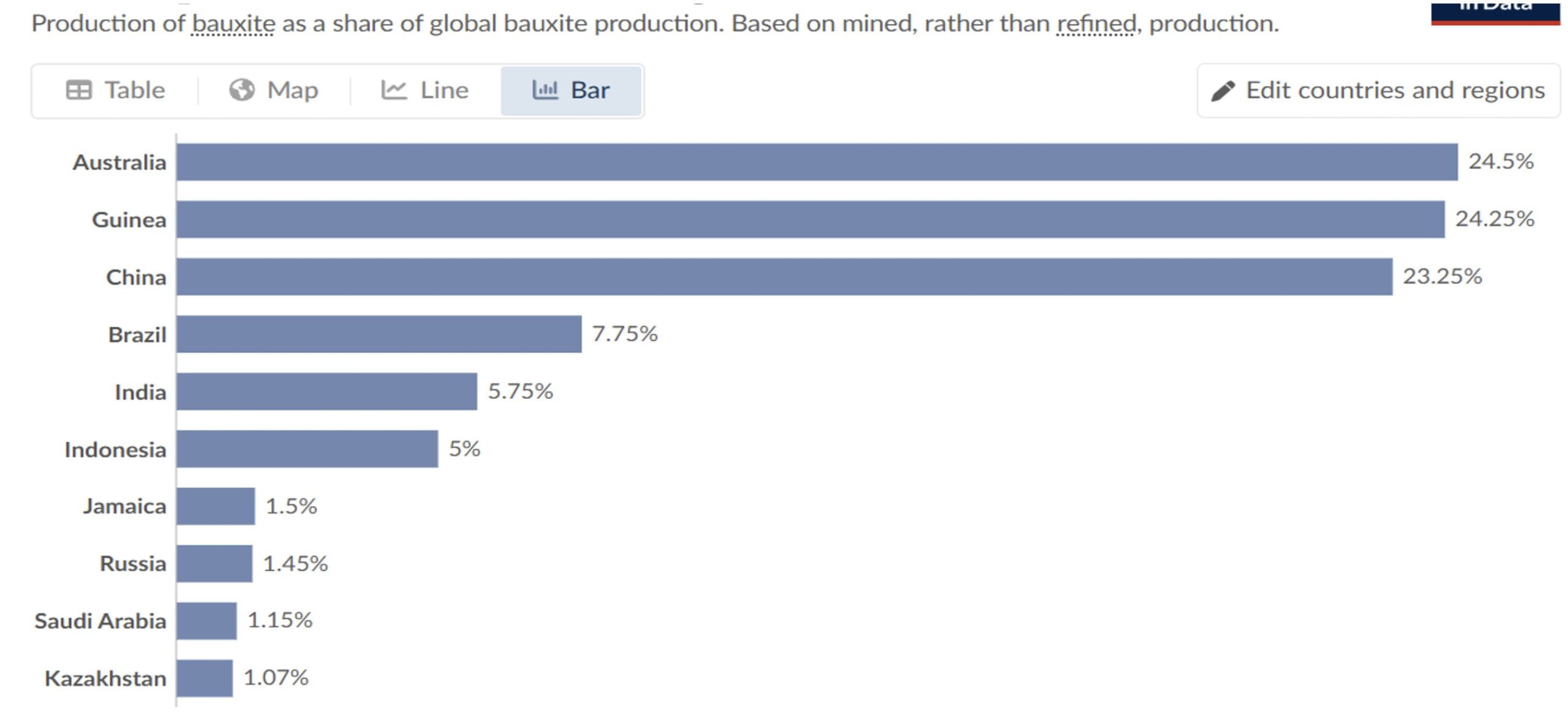

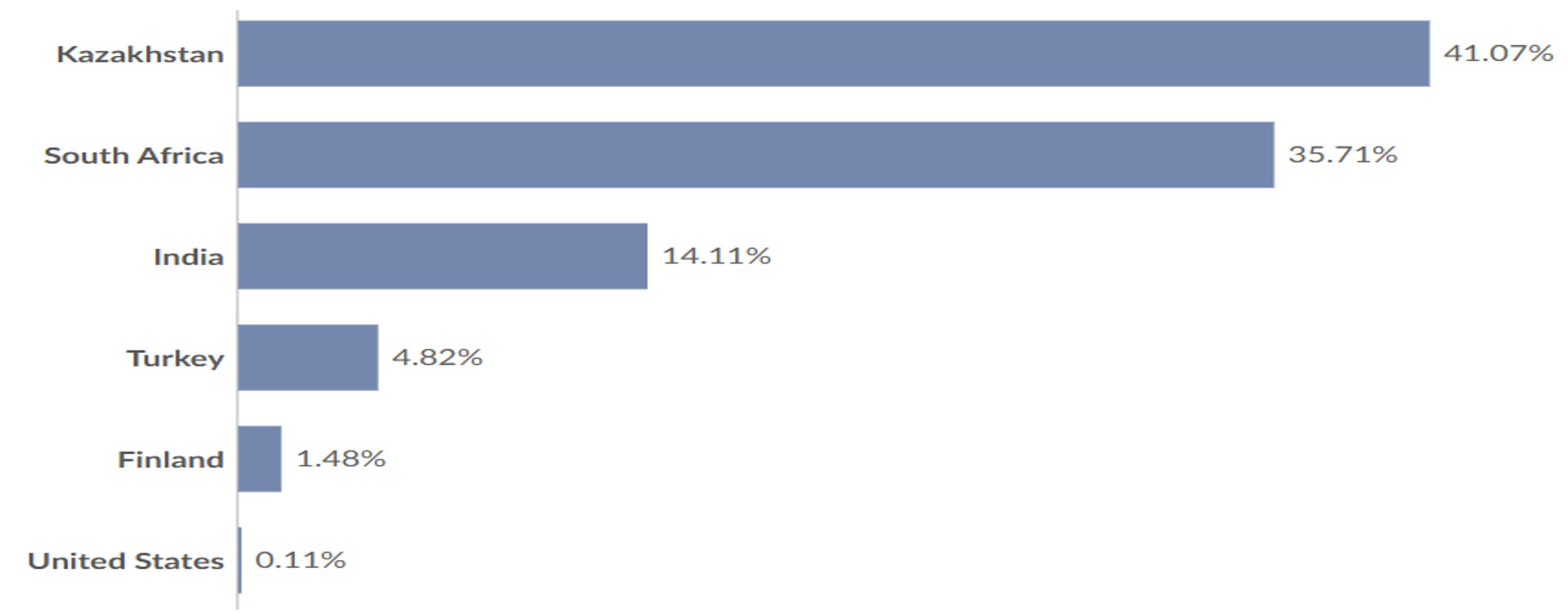

This enduring dynamic is starkly visible in contemporary struggles over CRMs. Reserves are highly concentrated in particular regions: China dominates rare earth production and processing; Congo is the world’s largest cobalt producer (see Figure 1); Chile, Argentina, and Australia hold major lithium reserves; Australia and Indonesia lead in nickel; Brazil and Mozambique in natural graphite; and Australia, Guinea, China, Brazil, India and Indonesia in bauxite (as illustrated in Figure 2). Large reserves of chromium deposits are found in Kazakhstan, South Africa, and Turkey (see Figure 3). Hence, such geographical concentration underpins metropolitan capitalism’s structural vulnerabilities.

Figure 1: Production of Cobalt, 1994-2024.

Figure 2: Production of Bauxite as the Global Share, 2023.

Figure 3: Countries Global Share of Chromium Reserves, 2023.

Rare earth elements (REEs) illustrate this dynamic even more clearly. Despite accounting for around 70% of REEs mining and 90% of processing, China’s leverage derives primarily from its refining capacity rather than from reserves alone (as shown in Figures 4a and 4b). The US (14% of production) and Australia (6%) contribute to extraction but continue to rely heavily on China for processing, highlighting the structural asymmetry of the supply chain.

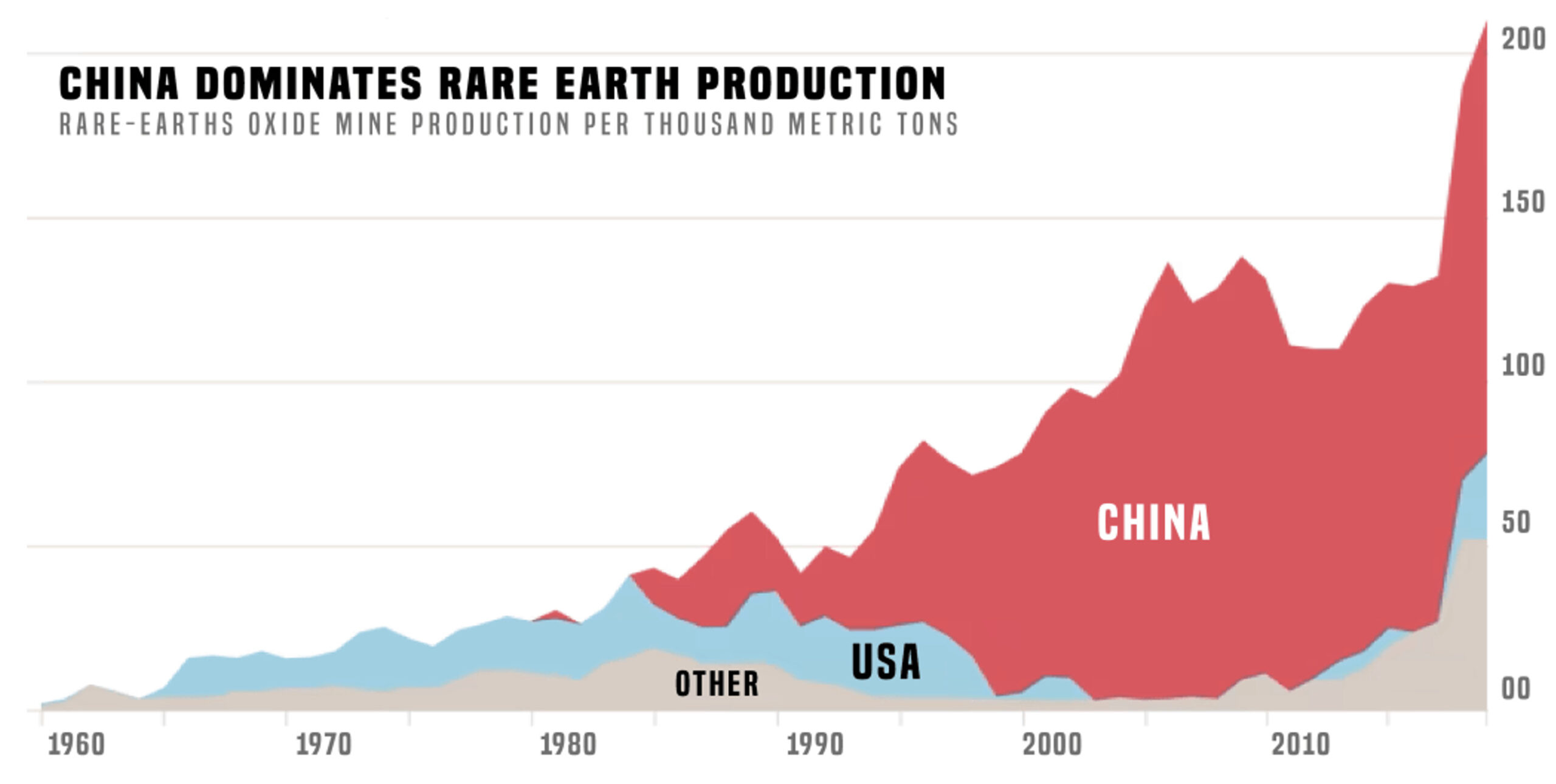

Over the years China has invested heavily in both production and processing of rare earth elements (as illustrated in Figure 5). Hence, this dominance is not accidental. Processing rare earths and other strategic minerals is technologically complex, capital-intensive, and environmentally costly. China’s willingness to absorb these costs—backed by long-term state support—has allowed it to capture a near-monopoly over the most value-added segment of the supply chain.

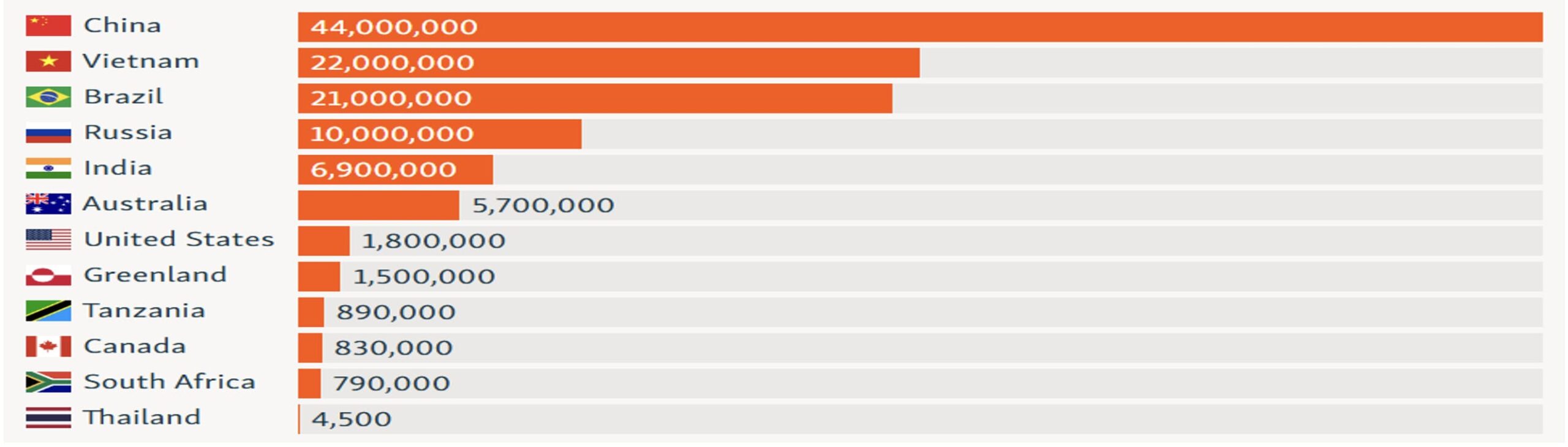

Figure 4a: Known Rare Earth Elements Reserves by Country (metric tons), 2024.

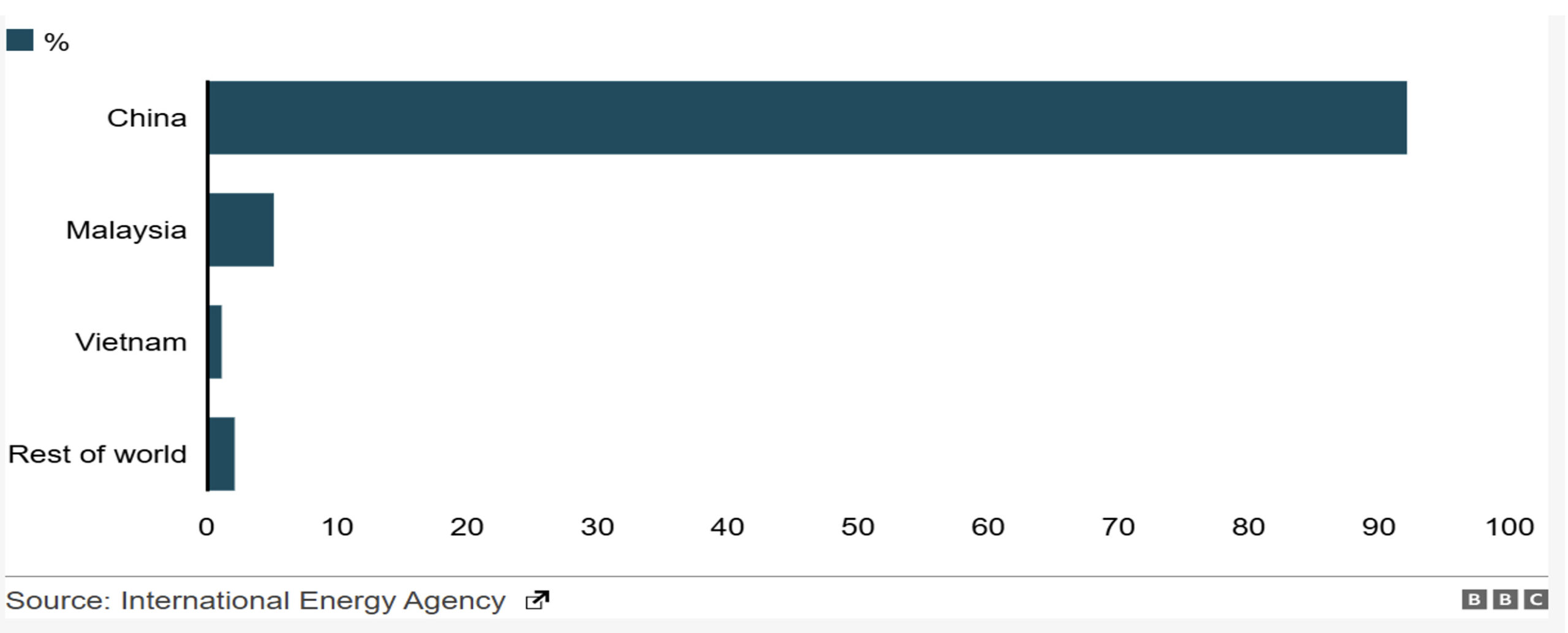

Figure 4b: Refined Production of Rare Earth Elements, 2023 (%).

Figure 5: China’s Production of Rare Earth Elements, 1960-2024.

The US and the EU have begun to respond. In 2023, three US-based recycling facilities for strategic minerals became operational, aiming to reduce dependence on imports and diversify supply chains. Similar initiatives in Australia, Canada, and the EU mark an important shift, though they remain in their early stages.

Overall, China’s overwhelming control of processing capacity reveals the central paradox of the critical minerals’ economy: resource abundance alone does not confer strategic advantage; control over processing does. By dominating refining capacity, China has positioned itself as the indispensable hub of global supply chains, securing both economic leverage and geopolitical influence in the transition to clean energy and advanced technologies.

IV. The United States Dependence

The US depends heavily on rare raw materials on China for its strategic industries, including defence, renewable energy, and high-tech manufacturing. Estimates suggest that the US relies on China for roughly 70% of its rare earth compound and metal imports. This dependence is compounded by the fact that China dominates both mining volumes and, more importantly, the processing capacity required to transform raw materials into usable inputs. Over 50% of another 29 critical minerals are imported by the US. It plans to reduce this dependence include developing domestic mining and processing capabilities, recycling initiatives, and partnerships with allied countries such as Australia and Canada (OECD, 2023).

Policy measures across administrations highlight the growing strategic importance of mineral supply chains. Executive Order 14017 under Biden and the use of the Defence Production Act under Trump demonstrate recognition of the vulnerabilities posed by reliance on foreign refining capacity (Siddiqui, 2025c). However, building a complete, resilient supply chain remains a long-term challenge, requiring investments in extraction, refining, manufacturing, and recycling. Recognizing these vulnerabilities, US has increasingly sought to diversify its supply chains and reduce reliance on China. Efforts include expanding domestic mining and processing capabilities and forging partnerships with resource-rich allies such as Australia and Canada. These measures by the US aims to develop alternative supply chains that are both secure and resilient.

US policy responses have evolved across administrations. The Trump administration first designated rare earths as critical to national security but notably exempted them from the 2018 tariffs imposed on Chinese goods. The Biden administration adopted a more structured approach, issuing Executive Order 14017 on America’s Supply Chains and allocating dedicated funding for critical minerals. Under Biden, multilateral initiatives such as the Minerals Security Partnership were also launched to coordinate supply chain diversification with allied countries. The second Trump administration has since intensified these efforts, invoking Section 232 of the Trade Expansion Act, activating the defence Production Act, and proposing major funding increases for domestic mining and processing in the upcoming fiscal year.

These measures underscore a growing recognition in the US that reducing dependence on China requires more than securing raw materials—it requires investment in processing, recycling, and international partnerships. Still, given China’s entrenched dominance, US efforts remain in the early stages and face significant challenges in scaling to match the strategic risks (Kuo, 2021).

V. Critical Minerals as Geopolitical Competition

Critical minerals have emerged as central instruments of geopolitical power. China illustrates this most clearly: it accounts for roughly 70% of global rare earth mining and more than 90% of refining capacity. It also produces around 92% of the world’s high-strength permanent magnets, which are indispensable for technologies ranging from electric vehicles to advanced military systems such as submarines, fighter jets, missiles, and radar (Brown, et al 2024).

China also moved early to secure resources abroad. Through investments in Africa and Latin America—particularly in the Congo, Bolivia, and Chile—China has paired mineral extraction with infrastructure projects under the Belt and Road Initiative (Siddiqui, 2024b), including ports, railways, and industrial facilities. This integration has given China not only access to raw materials but also influence over the logistics and trade routes that move them.

In contrast, the US has only recently begun to frame critical minerals not merely as commodities but as strategic assets central to national security. Escaping China’s grip will require more than expedited mine permits or short-term funding. It demands a coherent, long-term strategy to construct a resilient supply chain that encompasses domestic capabilities, reliable alliances, and investments across the full spectrum: mining, refining, magnet production, and recycling. This will require targeted investment, permitting reform, and close coordination with trusted partners.

The strategic stakes are high and the REEs underpin a wide range of defence technologies, including modern fighter aircraft, submarines, Tomahawk missiles, radar systems, and advanced communications equipment. Yet the US is already on the back foot: China is rapidly expanding munitions production and fielding advanced weapons systems at a faster pace. Ultimately, critical minerals are no longer simply inputs to industry—they are levers of geopolitical influence. China recognized this early, while the US and its allies are only beginning to respond. The struggle for control over these supply chains will shape the balance of power in both the global energy transition and the future of warfare.

Rare earth elements form the foundation of renewable energy technologies, especially through their use in high-efficiency permanent magnets. These magnets power mobile phones, wind turbines, electric vehicles, and aerospace applications, while also serving critical military functions in drones, missiles, and radar systems. Just as the US has imposed export controls on semiconductors, China has used its dominance in rare earths to restrict flows abroad. Export licensing requirements for certain REE products highlight the asymmetric leverage China holds in today’s technology wars.

Although China holds an estimated 44% of global rare earth reserves—followed by Vietnam (22%), Brazil and Russia (21% each), India (6.9%), and Australia (5.7%)—its real power lies not in geology but in processing. China controls nearly 90% of global refining capacity, including material mined elsewhere, such as in Australia, Myanmar, and Vietnam. Since the 1980s, when REEs were primarily used in colour televisions, glassmaking, and oil refining, China has steadily built a near-monopoly across the rare earth supply chain. Today, these materials are indispensable to rapidly growing industries such as wind energy, electric vehicles, robotics, and advanced aerospace, as well as in military systems ranging from lasers and tanks to precision-guided missiles (Tooze, 2025).

This dependency is rooted not only in China’s rise but also in the long-term decline of US industrial capacity. In pursuit of cheap labour and higher profits, American firms offshored critical sectors, hollowing out domestic processing industries. In the 1950s, the US led the world in zinc refining; today it accounts for only 6% of global output, compared to China’s 33%. The US was once the top uranium producer; now it imports its entire supply, including from strategic rivals such as Russia. These structural vulnerabilities illustrate that the rare earth struggle is not just about resources, but about the long-term erosion of industrial and technological sovereignty.

The pursuit of critical minerals has become a focal point of geopolitical competition. The US, seeking to secure access to strategic resources, has pursued agreements with mineral-rich countries. For example, on April 30, the US signed a mineral deal with Ukraine, which possesses 117 of the 120 most-used industrial minerals. However, much of these resources are located in territories contested or occupied by Russia, illustrating the inherent geopolitical and logistical challenges of such projects.

Developing mineral resources is neither simple nor guaranteed. Projects require enormous capital investment, and many involve constructing new mines in regions where resource estimates remain unconfirmed. In Greenland, for instance, harsh climatic conditions and icy terrain present significant obstacles. In the US, mining development is notoriously slow, with an average of 29 years required to bring a mine from exploration to production.

Environmental sustainability often remains secondary in the pursuit of strategic resources. For instance, Canada’s Ring of Fire—a wetland and forest serving as an important carbon sink—contains an estimated $67 billion in rare earth minerals. Exploiting these resources could release substantial greenhouse gases, illustrating the environmental trade-offs inherent in mineral extraction under current economic systems.

These dynamics reveal the structural tensions inherent in the global mineral economy: strategic competition, environmental degradation, and economic instability are interlinked outcomes of the current system. Addressing these challenges requires approaches that prioritize long-term sustainability, equitable resource management, and careful consideration of the geopolitical implications of critical mineral development.

VI. Rare Earth Critical Minerals: Geopolitics, Supply Chains, and Capitalist Power

The US President Donald Trump expressed interest in acquiring Greenland, an autonomous territory under Danish sovereignty, citing its strategic value and vast resource potential. The proposal was widely interpreted as motivated, at least in part, by Greenland’s significant reserves of REEs, which have attracted growing international attention. Both Denmark and Greenland firmly rejected the idea, emphasizing that Greenland is not for sale and asserting their sovereignty over resource management. While Greenland is estimated to hold approximately 1.5 million metric tons of rare earth elements, the island does not currently produce these metals. Nevertheless, it hosts two major projects with substantial reserves—the Tanbreez project and the Kvanefjeld project—which could position Greenland as a significant supplier in the future (Goodenough, et al 2018).

The US interest in Greenland reflects broader geopolitical competition over critical minerals essential to renewable energy technologies and defence industries. China currently dominates the global processing of rare earths, accounting for the vast majority of refining capacity, and has in the past signalled its willingness to use this dominance as a strategic tool. From a US perspective, securing alternative sources of rare earths, such as those potentially available in Greenland, is therefore not only an economic issue but also a national security concern. Greenland, situated in the Arctic—a region of increasing strategic importance due to climate change and emerging shipping routes—thus represents both a potential resource frontier and a geopolitical flashpoint in the contest between great powers (Tooze, 2025).

The case of Greenland reflects a broader geopolitical dilemma: the location of mineral reserves does not necessarily translate into supply chain power. For example, cobalt—an essential input for lithium-ion batteries that power electric vehicles (EVs) and renewable energy technologies—is overwhelmingly concentrated in the Congo, as it accounts for about 73% of global cobalt mine output and holds roughly 57% of the world’s reserves, giving it an unparalleled role as a supplier. Yet the strategic value of these reserves is diminished by the fact that China controls approximately 74% of global cobalt processing. Because processing is the stage that transforms raw materials into battery-grade components, China ultimately wields leverage over the downstream supply chain (Goodenough, et al 2018).

Lithium, another indispensable mineral for EV batteries, demonstrates a similar asymmetry. While Australia produces around 51% of global lithium output and Chile 26%, China—despite being a relatively minor producer—dominates refining, with 65% of global processing capacity. This control over processing capacity, rather than raw production, grants China disproportionate influence over global supply chains.

Taken together, these cases illustrate a central paradox: resource-rich states such as the Congo, Chile, or potentially Greenland may command geological abundance, yet their strategic position is weakened when processing and technological capacities are concentrated elsewhere. China’s dominance in mineral processing highlights a structural vulnerability for countries seeking to secure supply chains for clean energy technologies. It also underscores a shift in geopolitical competition: from traditional control over raw resources to control over the value-added stages of the supply chain.

The US, in contrast, is heavily dependent on imports for critical minerals. It relies on China for roughly 70% of its rare earth imports and is entirely dependent on imports for 12 of 50 critical minerals, while over 50% of another 29 come from foreign sources. US efforts to diversify supply chains and develop domestic capabilities include mining initiatives, recycling programs, and strategic partnerships with allies like Australia and Canada. Policy measures across administrations—ranging from Executive Order 14017 under Biden to invoking the defence Production Act under Trump—illustrate the growing recognition that supply chain security is central to national security. Yet building a complete domestic or allied supply chain remains a long-term challenge, requiring investment not only in extraction but also in refining, manufacturing, and recycling.

Under colonialism, the extraction and control of rare earth minerals were intrinsically linked to capitalist imperialism, facilitating the exploitation of labour and natural resources. This process established enduring neocolonial economic structures that primarily benefit dominant powers and their multinational corporations. Despite being essential for modern technology and defence, the mining of these minerals often exacerbates global inequalities rather than generating broad societal benefit (Siddiqui, 202016).

Marxist theory frames the extraction of rare earth minerals as a form of capitalist exploitation. Natural resources are privatized and extracted primarily for profit, frequently at the expense of local communities and the environment. Workers in mines are often subjected to low wages, unsafe conditions, and alienating labour, reflecting the separation of labour from the products of their work.

The environmental consequences of rare earth extraction further illustrate capitalist priorities. The mining and refining processes consume large amounts of water and chemicals, produce hazardous waste, and disrupt ecosystems. From a Marxist viewpoint, under capitalism, these impacts are not incidental but stem from the systemic drive for short-term profit over long-term ecological sustainability.

At present, the rare earth minerals have also become instruments of geopolitical power. Control over these strategic resources’ fuels technological supremacy and military capabilities, enabling certain states and corporations to maintain economic and political dominance. China’s near-monopoly in rare earth processing exemplifies the concentration of economic power within a specific national capital, resulting from historical developments and the global division of labour. This concentration creates dependency for other nations, deepening global inequality as wealth, technological capacity, and strategic advantage are disproportionately held by a few actors.

VII. Conclusion

Rare earth minerals are at the nexus of technology, geopolitics, and capitalism. China’s dominance in processing and strategic investments abroad has created a structural dependency that challenges the US and EU (Siddiqui, 2025d). Meanwhile, the extraction and use of these minerals often exacerbate environmental and social inequalities, reflecting the systemic priorities of profit-driven economies.

Addressing these challenges requires a multi-faceted approach: building resilient domestic and allied supply chains, investing in processing and recycling capabilities, and incorporating ecological and social considerations into resource management. Ultimately, control over rare earth elements and critical minerals is not just an economic or technical issue—it is a central determinant of geopolitical power and industrial sovereignty in the 21st century.

The global competition for REEs exemplifies a convergence of strategic, economic, and environmental imperatives. This contest exposes critical supply chain vulnerabilities and technological dependencies, which are exacerbated by severe ecological consequences—including hazardous waste, water contamination, and widespread ecosystem disruption.

Within the capitalist world-system, rare minerals are predominantly privatized and extracted for profit by major corporations, a process that frequently occurs at the expense of local communities and ecosystems. Labour exploitation is endemic, with mine workers often subjected to harsh conditions and low wages, while the industry’s logic prioritizes short-term gain over long-term ecological stewardship. Consequently, the extraction and control of these critical minerals are not merely economic activities; they function as structural mechanisms through which capitalist systems reproduce social and environmental exploitation, consolidate corporate and state power, and reinforce entrenched international hierarchies.

From this critical perspective, rare earth minerals are thus revealed not as neutral commodities, but as central instruments of geopolitical power. Control over the entire value chain—from processing to manufacturing—enables dominant powers such as the US, the EU, and China to consolidate technological, economic, and military advantages. This dynamic perpetuates global core-periphery inequalities, as even countries endowed with significant mineral reserves remain constrained by a lack of downstream refining capabilities and technological sovereignty. Ultimately, the rare earth economy illustrates how economic and strategic power remains concentrated within a select group of core nations and their corporate entities.

About the Author

Dr. Kalim Siddiqui is an economist specializing in International Political Economy, Development Economics, Trade and Economic Policy. Since 1989, he has been teaching economics at various universities in Norway and the UK. Dr. Siddiqui’s research interests encompass a wide range of topics, including political economy, international trade, and economic history, South Asia, and emerging economies. He has presented papers at international conferences across numerous countries, reflecting his global engagement in the field. His scholarly pursuits span six broad domains: Political Economy, Development Economics, Economic History, Economic Policy, Globalization, and International Trade. Dr. Siddiqui has made significant contributions to research in areas such as trade policy, globalization, and political economy. His work has been published in chapters of edited books and articles published in peer-reviewed journals. For inquiries, Dr. Siddiqui can be reached at: [email protected]

Dr. Kalim Siddiqui is an economist specializing in International Political Economy, Development Economics, Trade and Economic Policy. Since 1989, he has been teaching economics at various universities in Norway and the UK. Dr. Siddiqui’s research interests encompass a wide range of topics, including political economy, international trade, and economic history, South Asia, and emerging economies. He has presented papers at international conferences across numerous countries, reflecting his global engagement in the field. His scholarly pursuits span six broad domains: Political Economy, Development Economics, Economic History, Economic Policy, Globalization, and International Trade. Dr. Siddiqui has made significant contributions to research in areas such as trade policy, globalization, and political economy. His work has been published in chapters of edited books and articles published in peer-reviewed journals. For inquiries, Dr. Siddiqui can be reached at: [email protected]

References

- Brown, D., Zhou, R. and Sadan, M. (2024) “Critical minerals and rare earth elements in a planetary just transition: An interdisciplinary perspective” Extractive Industries and Society, 19, September.

- Goodenough, K.M., Wall, F. & Merriman, D. (2018) “The Rare Earth Elements: Demand, Global Resources, and Challenges for Resourcing Future Generations” Natural Resources Research, 27:201–216.

- Kuo, J. (2021) ‘Geopolitical Risks in the Rare Earth Supply Chain’, Strategic Studies Quarterly, 15(2), pp. 59–83.

- Organisation for Economic Co-operation and Development (OECD). (2023)Critical Materials Outlook. Paris: OECD.

- Siddiqui, K. (2025a) “Challenges for Degrowth, Sustainability, and Long-Term Economic Development” World Financial Review, March.

- Siddiqui, K. (2025b) “Donald Trump’s Tariffs: A Prelude to Global Trade Wars?” World Financial Review, April.

- Siddiqui, K. (2025c) “The Reasons Behind the Decline of the US Economy” World Financial Review, May.

- Siddiqui, K. (2025d) “Understanding the Rise of High Technology in China” World Financial Review,

- Siddiqui, K. (2024a) “Political Economy of Globalisation and Issues of Global Governance” World Financial Review, September.

- Siddiqui, K. (2024b) “China’s Growth Miracle and Development Strategy Since the 1980s” World Financial Review,

- Siddiqui, K. (2022) “Capitalism, Imperialism, and Crisis” European Financial Review, June/July.

- Siddiqui, K. (2021) “Trade Liberalisation, Comparative Advantage, and Economic Development: A Historical Perspective” World Financial Review, May/June.

- Siddiqui, K. (2019). “One Belt and One Road, China’s Massive Infrastructure Project to Boost Trade and Economy: An Overview”.

- Siddiqui, K. (2018a). “David Ricardo’s Comparative Advantage and Developing Countries: Myth and Reality” International Critical Thought, 8(3):1-28, September.

- Siddiqui, K. (2018b). “Capitalism, Globalisation and Inequality” World Financial Review, November/December

- Siddiqui, K. (2016). “International Trade, WTO and Economic Development” World Review of Political Economy 7(4):424 – 450.

- Tooze, A. (2025) “Trouble Transitioning: What energy transition?” London Review of Books, 47(1), January 23.

{kind=link}