Nobel Peace Prize winner Muhammad Yunus has been appointed to lead Bangladesh’s interim government after the resignation of longtime Prime Minister Sheikh Hasina, who fled the country amid violent unrest. Yunus, an 84-year-old economist and microcredit pioneer, is widely respected for his efforts to lift millions out of poverty through Grameen Bank. His appointment followed demands from student protest leaders, marking a significant shift in Bangladesh’s political landscape. As the nation faces a political crisis, Yunus is tasked with restoring order and guiding the country towards free and fair elections.

Convenience is crucial in the dynamic landscape of modern commerce in India. From bustling marketplaces to digital stores, the ease of transactions has transformed how customers interact with businesses. Among the technological marvels driving this change are UPI payment gateways. According to data provided by the RBI, UPI transactions reached ₹139.2 trillion in FY 2022-23. These amount for 73% of all non-cash transactions during that year.

These gateways have revolutionised the way customers navigate payments, offering a seamless and user-friendly experience. UPI payment gateways embody this convenience, bridging the gap between traditional commerce and digital innovation.

This blog explores how these gateways are reshaping customer experiences and empowering businesses in the digital age.

What is a UPI Payment Gateway?

A UPI payment gateway facilitates transferring funds between parties through the Unified Payments Interface (UPI) platform. UPI, developed by the National Payments Corporation of India (NPCI), allows users to connect multiple bank accounts to one mobile app. Businesses and individuals use UPI gateways to accept payments from customers using UPI-enabled apps, ensuring secure and convenient transactions.

This gateway acts as an intermediary for the payer’s and payee’s banks, ensuring safe and efficient fund transfers. UPI’s feature of linking multiple bank accounts to a single mobile app makes it a convenient and efficient digital payment method.

Payment gateways serve as a crucial component in modern business operations, enabling swift and secure transactions.

Their role extends beyond processing transactions; they enhance customer trust and satisfaction by ensuring a smooth, secure, and adaptable payment experience. This foundational support is essential for businesses looking to thrive in a competitive market landscape.

Essential Features to Enhance User Experience

UPI payment gateways offer customers unmatched ease and flexibility. To elevate the overall customer experience, certain essential features are necessary. Incorporating these features can significantly enhance the functionality and appeal of UPI payment gateways.

1. Enhanced Checkout Experience

The checkout process is a pivotal moment in any online shopping journey, where the effectiveness of a payment gateway is most evident. A user-friendly interface is essential at this stage. When the payment process is intuitive and straightforward, customers are more likely to complete their purchases, leading to increased satisfaction and higher conversion rates.

An easy and smooth checkout experience significantly increases the likelihood of customers finalising their orders, effectively bridging the gap between browsing and buying.

2. Wider Customer Reach

UPI has achieved widespread adoption across India, with millions of users regularly utilising UPI-enabled apps for their transactions. By integrating UPI as a payment option, businesses can effectively reach this large and diverse user base.

Offering UPI as a preferred payment method aligns with customer preferences, potentially increasing conversion rates and fostering customer loyalty by providing a convenient and trusted payment solution.

3. Offering Diverse Payment Options

Customers have varied preferences when it comes to payment methods. By integrating a payment gateway that offers multiple payment options—such as credit cards, debit cards, and digital wallets—businesses can cater to a wide range of customer needs.

This flexibility not only simplifies the payment process for customers but also demonstrates a business’s commitment to accommodating diverse preferences, thereby enhancing the overall user interface and experience.

4. Ensuring Mobile Responsiveness

With the widespread use of smartphones, the importance of mobile-friendly payment interfaces cannot be overstated. A good payment gateway ensures that the payment process is seamless and responsive across all devices, including desktops, tablets, and smartphones.

Efficient mobile payment functionality is now essential for businesses aiming to capture and retain the growing number of mobile shoppers. By providing a consistent and accessible payment experience across devices, businesses can significantly improve customer satisfaction.

5. Strengthening Security Measures

Security is crucial in online transactions, and payment gateways play a vital role in protecting customer information. Implementing strong security features, such as encryption and fraud prevention measures, is essential.

Customers need assurance that their financial information is safe, which builds trust and confidence in the payment process. Secure transactions are vital for establishing and maintaining customer loyalty and encouraging repeat business.

6. Speeding up Transactions

Transaction speed matters a lot in our fast-paced world. Payment gateways that enable quick transactions can greatly enhance the user interface by reducing wait times. This not only meets the expectations of modern consumers but also positively impacts their perception of a business’s efficiency. Fast transaction processing creates a positive user experience, leading to higher customer retention rates and satisfaction.

7. Personalising Payment Experience

Recognising that each customer is unique, payment gateways are increasingly adopting personalisation strategies. Customising the payment experience based on individual customer profiles and preferences makes interactions more engaging and relevant.

This personal touch improves the customer experience and enhances the overall perception of the brand. In a market where consumers seek tailored experiences, personalised payment processes can significantly enhance the user interface.

8. Providing Real-Time Notifications

Effective communication is crucial in financial transactions. Payment gateways that offer real-time updates contribute to a transparent and reliable payment experience. Whether confirming a successful payment or alerting customers to an issue, timely notifications help reduce uncertainty and build trust.

Transparent communication throughout the payment process is key to creating a positive customer experience and maintaining customer trust.

Finding the Perfect UPI Gateway for Your Business

When it comes to finding the perfect UPI payment gateway for your business, it’s essential to consider features such as ease of integration, security protocols, and the ability to support various UPI functionalities. The right UPI gateway should offer comprehensive solutions. Leveraging UPI payment gateways can transform the way customers interact with your business, offering a superior payment experience.

If you are looking for an efficient payment gateway, consider solutions such as Plural by Pine Labs. Plural provides a comprehensive UPI Suite, including a UPI payment gateway, UPI Switch, and UPI Deeplinks for WhatsApp. It adopts all-new UPI features instantly and helps increase your revenue, making it the ideal choice for businesses looking to optimise their payment processes.

Visit Plural’s website now and discover the wide range of features available in their UPI Suite.

A highly anticipated debate between former President Donald Trump and Vice President Kamala Harris is set for September 10 on ABC. This debate marks a pivotal moment in an already extraordinary campaign, as both candidates vie for the presidency. Trump, who reversed his decision to debate, is grappling to regain momentum after Harris and her running mate, Tim Walz, energized the Democratic base. The upcoming debate could serve as a historic turning point, with both candidates facing intense scrutiny as they prepare to address the nation’s most pressing issues on a global stage.

Striving for a world free from emissions is a noble ambition, but how can this be achieved amid rising market volatility and litigation risks?

This is the central question for the Malaysian-based global energy giant Petronas as it marks its 50th anniversary this month.

Environmentalism is deeply ingrained in Malay culture, where nature preservation is a core value. This cultural reverence for the environment is reflected in Petronas’s commitment to environmental stewardship, driving its business model to “create better solutions that benefit people, partners, and the planet.”

In 2020, Petronas became the first energy company in Asia to set a net-zero goal. This ambitious commitment is particularly noteworthy in Malaysia, and Petronas is making significant strides toward it. By 2023, the company had reduced its annual greenhouse gas emissions by 1.8 million tonnes, established nearly 570 charging points, and deployed over 2,500 electric vehicles worldwide.

But achieving net zero is an expensive and increasingly challenging endeavour. That is why Petronas has focused on financial resilience amid market volatility, striving to balance reducing emissions while remaining competitive.

Economic conditions have exacerbated these challenges, with enduring inflation, high interest rates, and stagnant energy prices in 2024 making profitability difficult.

Additionally, there is a growing threat from litigation, especially through international arbitration. The UN recently highlighted the rise of profit-driven enterprises exploiting the investor-state dispute settlement process, posing significant obstacles to urgent environmental actions.

Arbitration cases have surged, with Asia-Pacific becoming the second most popular jurisdiction for disputes, accounting for a quarter of all cases filed last year. This trend puts over a quarter of a trillion dollars at stake.

Companies are compelled to reserve more funds for costly litigation, diverting resources needed for green initiatives. The rise in litigation has led to over $113 billion in public money being paid to private investors, with claims exceeding $856 billion, squeezing both private enterprises and national budgets and impacting green agendas.

Petronas has not been immune from this challenge. It is currently embroiled in a legal battle with the alleged heirs of the lapsed Sultanate of Sulu in the Philippines. While Petronas looks forward to the 21st century, investing in green solutions and striving for a sustainable future, the Sulu claimants are stuck in a 19th century mindset, seeking to profit from outdated colonial agreements at the expense of ordinary Malaysians and environmental welfare.

The Sulus base their claim on a treaty signed between the Sultanate and the British Empire in 1878, with the former ceding the resource-rich province of Sabah—now part of Malaysia—in exchange for an annual payment. Although Malaysia did not exist at the time of the agreement, or for more than 75 years thereafter, the Sulus argue that their agreement is still valid, demanding over $15 billion in damages from Malaysia’s domestic assets.

Yet, the Sulus never really controlled Sabah, and the Sultanate ceded any remaining sovereignty to the United States in 1915. This raises serious doubts about their authority to seek compensation for a non-existent country, from an agreement Malaysia had no part in, for territory they never truly governed.

This dubious claim has been reviewed by multiple jurisdictions in France, Spain, and the Netherlands – countries that often preach at the developing world and its duty to pursue green transitions while supporting cases that hinder their economic capacity for such transitions.

The forces supporting the Sulu plaintiffs are clearly driven not by an environmental ethos but by profit. To launch their challenge, the Sulu plaintiffs secured in excess of $20 million from British litigation funder Therium, exploiting third-party litigation funding laws that allow corporations to finance a case in exchange for a share of the award.

While this approach is quickly becoming a crucial tool for financing climate action, it’s also facing a growing risk of being hijacked for profit. This could seriously undermine the very environmental goals these claims aim to achieve. Take, for instance, Therium’s support for the UK-based Victoria Oil & Gas against Kazakhstan. Despite numerous charges against the company’s environmental practices, Therium’s backing seemed indifferent to the potential harm of providing financial support to the company.

Though Therium has not disclosed the stake they stand to gain in the Sulu case, many see this as a troubling re-emergence of colonialism, with the case threatening to siphon off resources equivalent to nearly triple the cost of Malaysia’s energy transition plan launched last year.

The case culminated in the freezing of Petronas assets in Europe although the company is not a party to the arbitral proceedings. The enforceability of the award, however, remains contested after Malaysia appealed to annul it, and the Spanish courts slapped a criminal conviction on the arbitrator for refusing to comply with a court order annulling his appointment. His motivations are unclear, but his extraordinarily high fee raises suspicions that financial incentives may have influenced both the arbitrator and the Sulu backers, undermining the legal process.

This uncertainty about the final award’s future continues, as the Sulu plaintiffs persist with a range of appeals across Europe. The lingering threat of a such a huge $15bn payout undermines both Petronas’ commitment to reduce emissions by 25% by 2030, and Malaysia’s ambitious goal of implementing the UN’s 2030 Agenda for Sustainable Development.

Despite ongoing legal wrangling and billions in frozen assets, Petronas deserves praise for sticking to its green commitments, even with stakes approaching their annual profits. Their dedication to a sustainable future is vital, especially as the green transition in developing countries depends heavily on private enterprises.

To achieve a sustainable future, the limited resources available in the developing world should be channelled towards realizing net-zero goals, rather than enriching a few dynastic opportunists and a British corporation with no green vision.

For most farmers, tractors are an indispensable part of daily operations. However, the high cost of purchasing a tractor outright can be a significant barrier. This is where tractor leasing comes into play, offering a cost-effective alternative to owning. In this guide, we’ll explore how tractor leasing works, its benefits, and tips for making the most of this financing option.

What is Tractor Leasing?

Tractor leasing allows farmers to use a tractor for a specified period while making regular lease payments. Unlike purchasing, leasing does not require a large upfront payment. Instead, you pay for the tractor’s use over the lease term, which typically ranges from two to five years. At the end of the lease, you can either return the tractor, extend the lease, or purchase the tractor at its residual value. Read more at ride on lawn mower finance.

How Tractor Leasing Works

Choose a Tractor: Select the tractor that best fits your farm’s needs. Leasing companies often have a range of options, including the latest models with advanced technology.

Apply for Lease: Submit a lease application to the leasing company. You’ll need to provide financial documents and details about your farm’s operations.

Lease Agreement: Once approved, you’ll sign a lease agreement outlining the terms, including monthly payments, lease duration, and maintenance responsibilities.

Regular Payments: Make regular lease payments as per the agreement. These payments are usually fixed, making budgeting easier.

End of Lease Options: At the end of the lease, decide whether to return the tractor, extend the lease, or purchase the tractor.

Benefits of Tractor Leasing

Lower Initial Costs: Leasing requires a smaller initial outlay compared to purchasing, preserving your farm’s cash flow for other expenses.

Access to Latest Equipment: Leasing allows you to use the newest models with the latest technology, enhancing productivity and efficiency.

Tax Benefits: Lease payments are often tax-deductible as a business expense, reducing your taxable income.

Flexibility: At the end of the lease term, you have the flexibility to upgrade to a new model, continue leasing, or purchase the tractor.

Maintenance Packages: Some leasing agreements include maintenance packages, reducing the hassle and cost of upkeep.

Tips for Successful Tractor Leasing

Evaluate Your Needs: Assess your farm’s requirements and choose a tractor that matches your operational needs.

Understand Lease Terms: Carefully read the lease agreement, paying attention to terms related to maintenance, mileage limits, and end-of-lease options.

Budget for Payments: Ensure that you can comfortably afford the monthly lease payments without straining your cash flow.

Maintenance Plan: Check if the lease includes maintenance services. If not, budget for maintenance costs separately.

Plan for the End of Lease: Consider your options at the end of the lease. If you plan to purchase the tractor, start setting aside funds for the residual value payment.

Common Pitfalls to Avoid

Overestimating Needs: Leasing a tractor larger or more advanced than necessary can result in higher costs without proportional benefits.

Ignoring Total Costs: Focus not just on monthly payments but also on the total cost of the lease, including any additional fees or charges.

Neglecting Maintenance: Ensure that regular maintenance is performed to avoid penalties or additional charges at the end of the lease.

Final Thoughts

Tractor leasing can be a valuable option for farmers looking to enhance their operations without the financial strain of purchasing new equipment. By understanding how leasing works, evaluating your needs, and carefully reviewing lease terms, you can make informed decisions that benefit your farm in the long run.

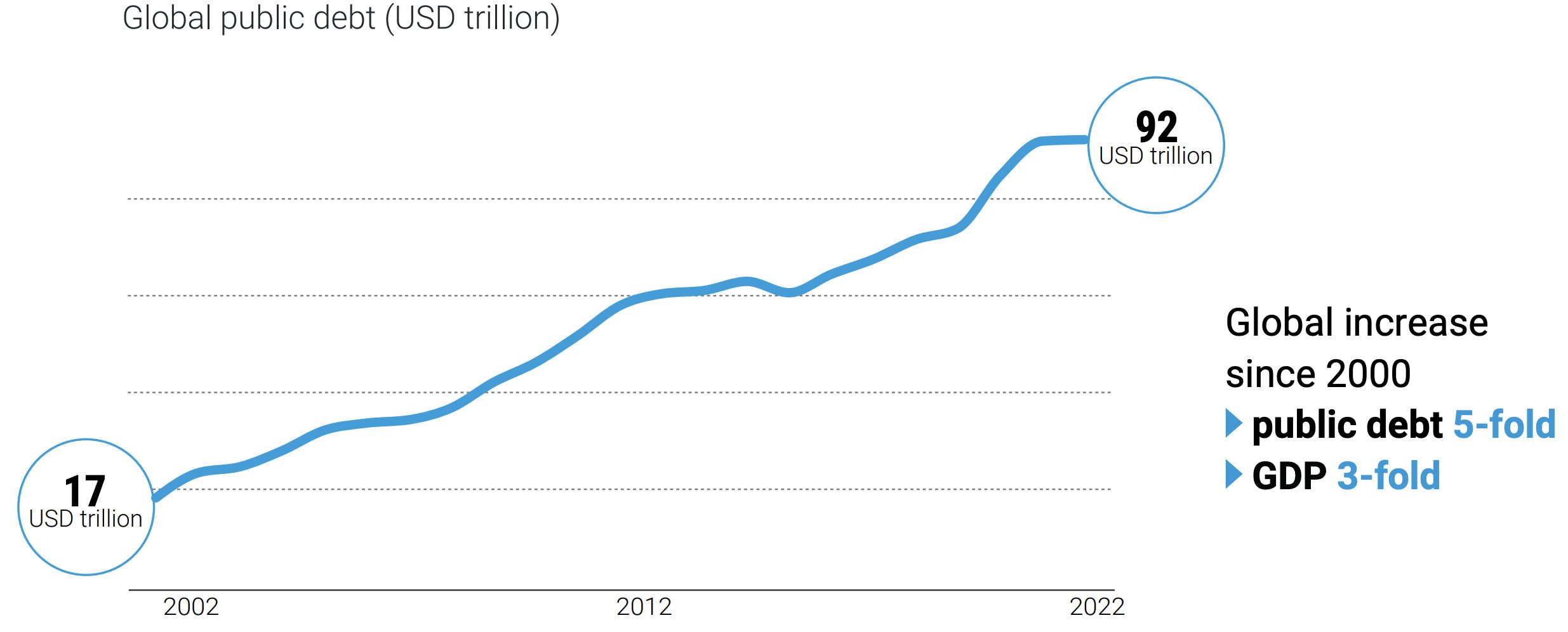

The exponential rise in external debts poses a significant threat to the prosperity and economies of developing countries. Nearly half of the world’s population lives in countries where foreign debt servicing exceeds government spending on education and health. For example, in 2023, global sovereign debt reached very high levels, i.e., US$92 trillion, with poor countries carrying 30 percent of the total debt burden. Moreover, around 40 percent of developing countries experience serious debt repayment challenges. These unsustainable debt levels adversely affect long-term investment in Sustainable Development Goals and addressing environmental challenges (UN, 2023).

Regarding the gravity of the situation with very high levels of external debt in developing countries, UN Secretary-General António Guterres stated that, on average, borrowing costs are four times higher for African countries than for the US and eight times higher than for the richest EU countries. Poor nations increasingly rely on private creditors who charge “sky-high” interest rates. These countries have little choice but to borrow to revive their economies. Guterres noted that, for poor countries, debt has become “a trap that simply generates more debt” (UN, 2023).

The UN Report (2023) proposes a number of urgent remedies, including an “effective debt workout mechanism” that supports payment suspensions, longer lending terms, and lower rates, “including for vulnerable middle-income countries.” The report also calls for a “massive” scale-up of affordable long-term financing by transforming the way that Multilateral Development Banks function, re-engineering them to support sustainable development.

In 2020, the average total debt burden (both public and private) of poor countries rose by 9 percentage points, compared with an annual increase of 1.9 percent in the previous decade. In the same year, fifty-one countries experienced a downgrade in their sovereign debt rating, making borrowing more expensive. Global inflation, spurred by the Russian invasion of Ukraine in early 2022, created upheaval in global markets for food, fuel, and fertilizer. The sudden decrease in the supply of these essentials caused high prices, hurting many developing countries dependent on imports of these basics even more deeply than they had already been by the COVID-19 pandemic. These two external factors affected price hikes and multiplied public and private debt (Stiglitz and Rashid, 2020).

In early 2022, the United States Federal Reserve and European Union Central Banks raised interest rates rapidly to curb high inflation after decades of low inflation and low interest rates. Thanks to globalization and financial liberalization over the last four decades, most countries are integrated into Western financial markets, promoted by the International Monetary Fund (IMF) and World Bank. Higher interest rates caused investors to withdraw capital from developing countries and move to United States (US) and European Union (EU) (Siddiqui, 2024).

Rising External Debts

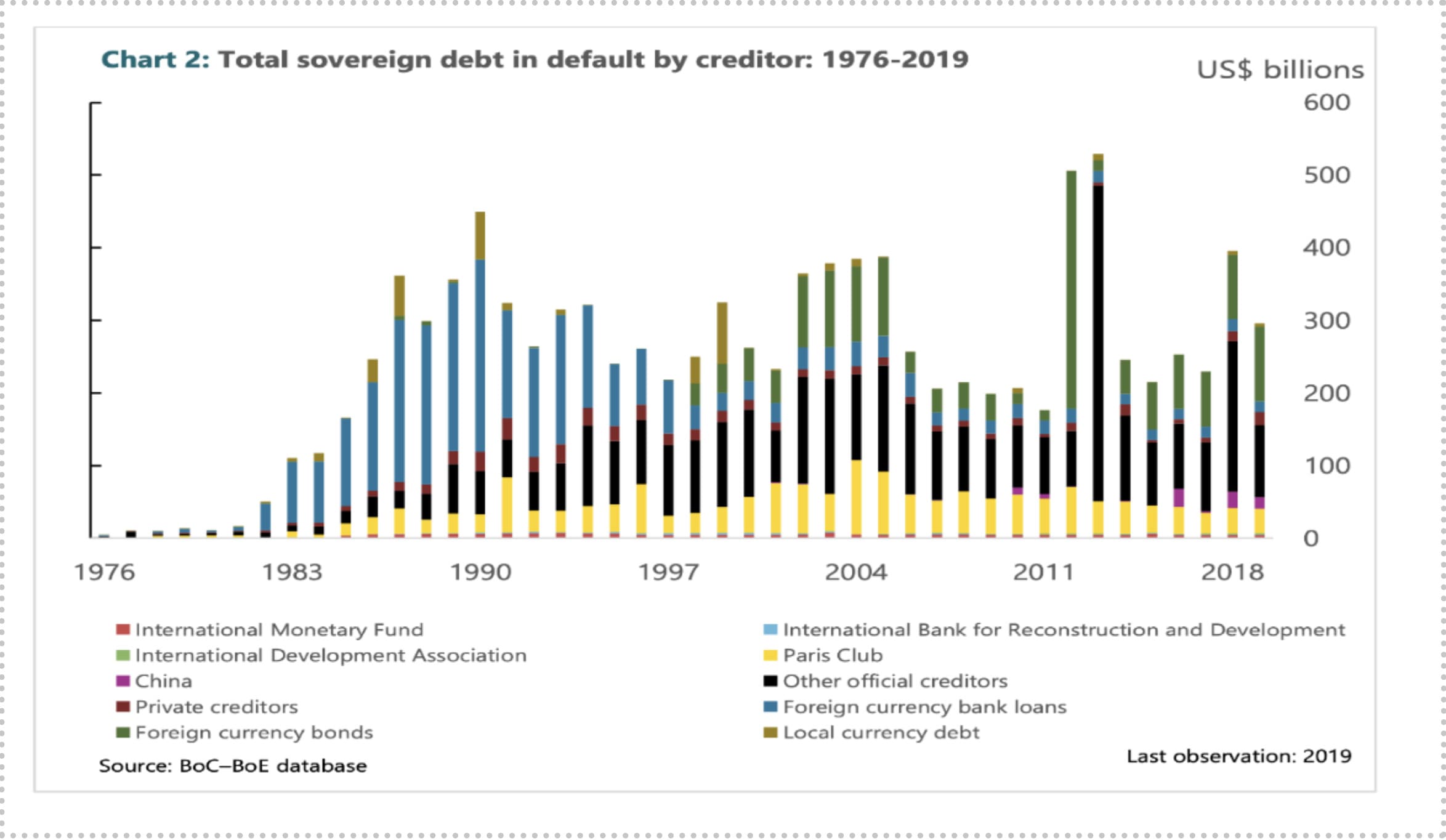

Public debt around the world has been on the rise over the last few decades, and the prevailing economic crisis in most developing countries has triggered a sharp acceleration of this trend. Between 2002 and 2022, global public debts rose dramatically from US$17 trillion to US$92 trillion (as shown in Figure 1). However, prior to 1980, sovereign debts were at very low levels, and the incidence of sovereign debt defaults by creditors rose only after the mid-1980s, as indicated in Figure 2a. According to the data, global public debt has increased more than fivefold since the year 2000, clearly outpacing global GDP, which tripled over the same period.

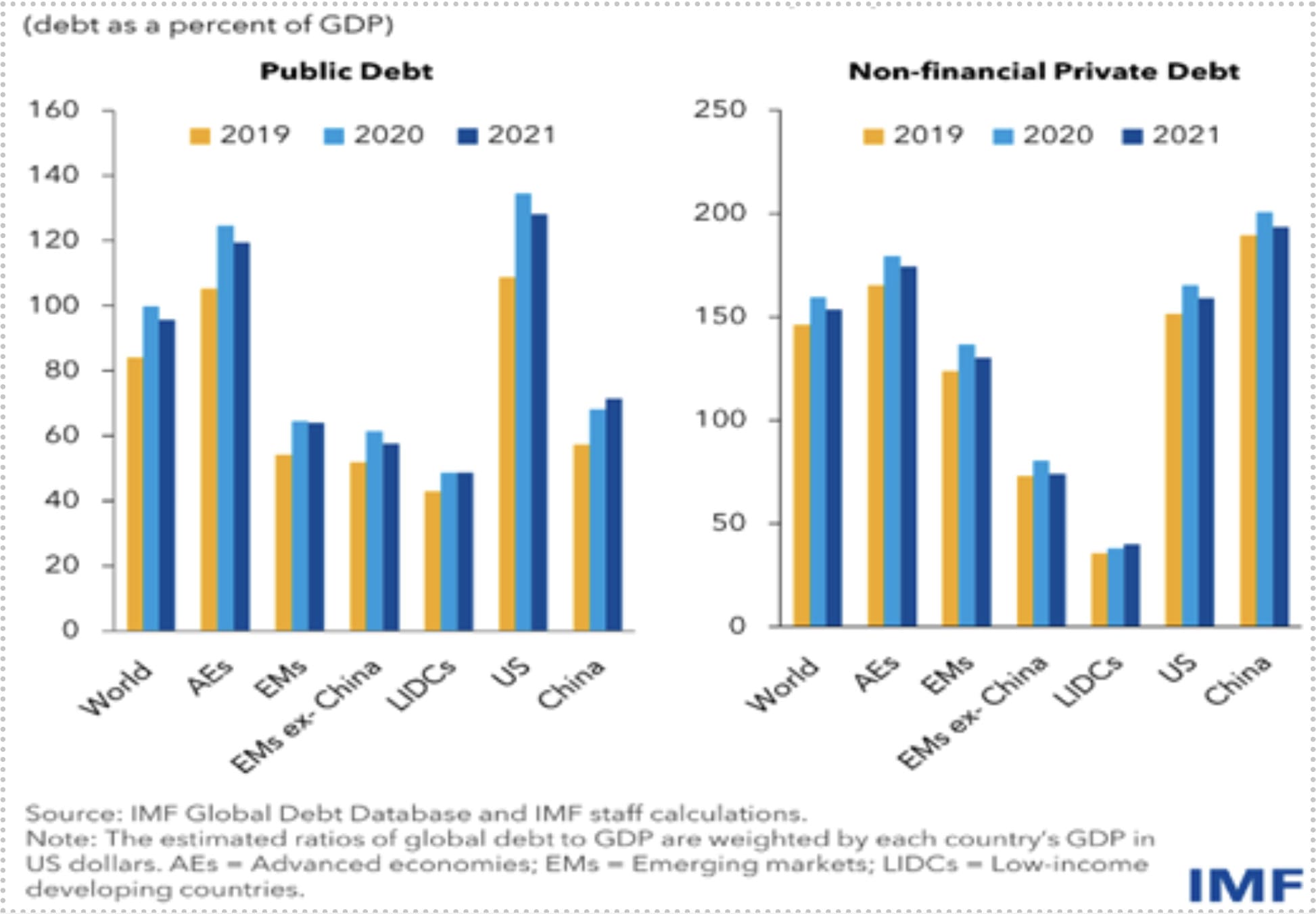

Figure 2b shows that during the COVID-19 pandemic, public and non-financial private debt rose significantly between 2019 and 2021. Despite external debts being at low levels for less developed countries, low incomes and high levels of poverty mean that debt repayments could cause severe socio-economic crises.

In 2022, global public debt—comprising general government domestic and external debt—reached a record US$92 trillion. Developing countries owe almost 30 percent of the total, of which roughly 70 percent is attributable to China, India, and Brazil (UN, 2023).

Figure 1: Global Public Debt, 2000-2022 (US$ trillion)

The IMF estimates that about 60 percent of low-income developing countries were experiencing debt distress or were close to it in 2021 and 2022. Additionally, the IMF noted that more than 70 developing countries had public debt exceeding 60 percent of GDP in 2020, and almost 60 countries remained at that level in 2022 despite following austerity programs (IMF. 2023).

The socio-economic consequences of a debt crisis have been devastating for low-income groups in poor countries. Latin America’s and Africa’s negative performance is generally attributed to the regions’ debt crises. A full-blown debt crisis inevitably leads to cuts in public spending in areas like education, health, and other social sectors. This can result in years of slow economic growth and high unemployment. Stagnation and higher unemployment increase poverty, breeding discontent and instability, and ultimately erasing gains in development (Dymski, 2003).

Over the past decade, external debts of developing countries have more than doubled, with most of these countries highly dependent on commodity exports. Developing countries’ total external debts, also known as public-guaranteed debts, rose from US$600 billion in 2008 to over US$1.3 trillion in 2020. Developing countries were forced to pay US$130 billion in debt service payments in 2021, which squeezed incomes soon after the COVID-19 pandemic. Moreover, private corporations’ borrowing from foreign banks, which were non-guaranteed, rose from US$520 billion in 2008 to nearly US$900 billion in 2021. Almost all of the developing countries’ debt is in US dollars, and they greatly rely on export earnings and remittances to service or repay their loans (Arellano; Bai, and Mihalache, 2024).

Mainstream economists’ advice on debt restructuring revolves around cuts in public spending and improving fiscal balance. Fiscal spending cuts are often given as universal solutions to avoid debt crises (Siddiqui, 1996). As a debtor country reduces fiscal spending and tightens its belt to minimize its ‘payment problems,’ this can improve credit ratings and encourage creditors to lend more, helping the government service its existing debts. However, in the real world, this seldom works, as Greece’s experience clearly demonstrates. Austerity usually exacerbates debt crises. Attempts to solve debt crises through restructuring, as many developing countries have done in the past, have often proved to be too little and less effective.

In developed economies, after fiscal expansion averted the worst of the 2009 financial crisis, unconventional monetary policies, mainly ‘quantitative easing,’ took over. The European Central Bank (ECB) followed the US Federal Reserve’s lead in implementing quantitative easing for over a decade. Quantitative easing’s lower interest rates encouraged more borrowing as more credit became available at lower costs (Stiglitz and Rashid, 2020).

Debt has become unsustainable when a government is forced to make cuts in areas that hurt its people, such as education or healthcare, just to keep up with payments. In 2021, Zambia’s debt servicing accounted for 39 percent of its national budget, with more spent on paying debts than on education, health, water, and sanitation combined. This undermines a country’s ability to invest in developmental projects. For instance, debt servicing costs in Sri Lanka have heavily burdened the government’s finances, leading the central bank to suspend external debt payments in April 2022 to buy essential goods like fuel. Coupled with unfavourable foreign exchange and high-interest rates, debt is seen as riskier for smaller economies (World Bank, 2023).

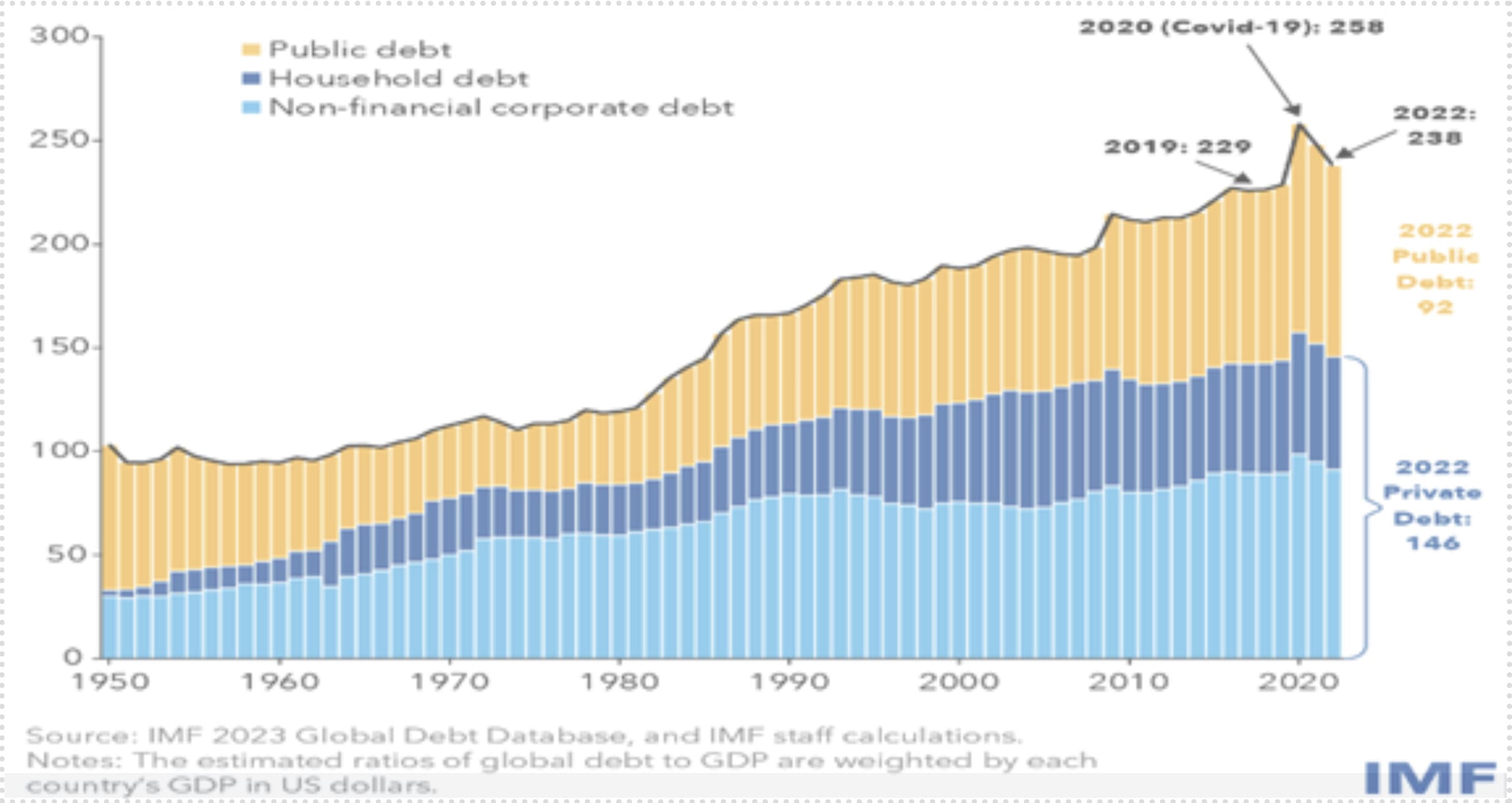

Developed countries face entirely different challenges, with some exceptions. For example, Japan, the world’s fourth-largest economy, is also one of the world’s most indebted countries, with total debt sitting above 600 percent of GDP. While the bulk of Japan’s debt is public, in recent years, it has been the financial sector piling on debt, not the government. Around two-thirds of the US$315 trillion owed originates from mature economies, with Japan and the United States contributing the most to that debt pile. However, the debt-to-GDP ratio for mature economies has generally been coming down. Figure 3a indicates that over the last seven decades since 1950, global debts (public and household) have consistently increased. During the COVID-19 pandemic, global debts as a percentage of GDP rose sharply, as shown in Figure 3b (IMF. 2023).

Figure 3a: Global Debt, 1950-2020 (% of GDP).

Source: IMF, Global debt is on the rise, 2023.

Figure 3b: Total Global Debts, 2015-2022 (in trillion US$)

On the other hand, emerging markets held $105 trillion in debt, with the debt-to-GDP ratio hitting a new high of 257 percent—pushing the overall ratio up for the first time in three years. China, India, and Mexico were the biggest contributors.

Mainstream economics claims that the path to economic growth for developing countries is achieved through the implementation of neoliberal policies, which include economic openness, market deregulation and liberalization, and privatization of public enterprises. Despite the lack of empirical evidence supporting these policies’ effectiveness, they continue to be imposed (Wade, 2023).

The growing debt of poor countries is alarming and brings back harsh memories of the debt crises of the late 1970s and early 1980s (Siddiqui, 1996). That period ended with a monetary tightening policy in the US, triggering a wave of debt crises in developing countries, especially in Latin America and Africa. During this period, neoliberalism was imposed, and austerity programs, known as Structural Adjustment Programs (SAPs), were enforced on debtor developing countries as a supposed solution (World Bank, 2023).

External Debt Crisis in Latin America

In Latin America and Africa, IMF loans are structured around two main programs: Stand-By Arrangements (SBAs) and Extended Fund Facility (EFF) or Extended Credit Facility (ECF) Arrangements. The former is most frequently used by member countries and is typically for relatively short periods, lasting between twelve and twenty-four months but rarely exceeding thirty-six months. Generally, these agreements involve constant monitoring of the country’s economic policies by the IMF but have few conditionalities regarding structural reforms focused on meeting certain set objectives.

The second type of agreement, the Extended Credit Facility, is applied to countries that not only experience a temporary balance of payments problem but are considered to have structural imbalances. With this type of agreement, the IMF proposes to intervene in the country’s economic structure, imposing fiscal austerity, exchange rate liberalization, and interest rate guidelines; it usually also includes a range of measures related to privatizations, labor reforms, and changes in social security. These plans were not genuinely meant to help debtor countries resolve their economic and financial problems; on the contrary, the IMF appears intent on intervening in their internal politics, imposing neoliberal market policies under the guise of “unconditional” assistance, thereby assuring their compliance with the demands of international capital markets.

To understand the relationship between the IMF and Latin America, we must examine the role that the United States has historically assigned to the region. For the most powerful country in the world, Latin America primarily serves as a supplier of raw materials and cheap natural resources. This is vastly different from the role that Europe, for example, has had for the US. In the framework of Europe’s reconstruction after the Second World War, the US faced the dilemma of how to lend money to its allied European countries. The central objective of the US in the postwar period was to maintain the full employment achieved through public investment and ensure a trade surplus in US relations with the rest of the world.

However, the major European countries capable of importing goods from the US had no money to pay for their imports. To enable them to buy US-manufactured products, large quantities of dollars had to be provided. There were three ways to do this: (a) lend money and have the recipients pay in kind; (b) lend them money and require them to pay their debts in dollars; and (c) donate the money until they got back on their feet.

The risk of entering an uncontrollable cycle of indebtedness combined with the risk evoked in the first possibility. Therefore, the option chosen was to donate the dollars in what was known as the Marshall Plan, where Europeans would use them to buy goods and services, ensuring an outlet for U.S. exports and consequently full employment. The Marshall Plan was also part of the Cold War strategy of rebuilding Western Europe in opposition to the Soviet Union.

The debt crisis in Latin America lasted for ten years, until the early 1990s, despite several unsuccessful attempts at resolution. The last effort to resolve the debt problem came with the Brady Plan, the plan proposed exchanging old external debt bonds for new ones backed by the US. Mexico was the first to adopt the plan in 1989, and in the following years, ten countries in the region signed on: Argentina, Brazil, Costa Rica, Ecuador, Mexico, Panama, Peru, the Dominican Republic, Uruguay, and Venezuela. Debt reduction fluctuated between 35 percent and 45 percent, reducing the debt-to-GDP ratio from 54 percent in 1987 to 32 percent in 1997. The consequences of the crisis were dramatic in economic and social terms for most countries in the region, as debt levels increased and degrees of autonomy in sovereign decisions were forever lost

In the mid-1990s, Latin America faced a new debt crisis, a crisis concerning the Mexican peso, led to a “bank run” that threatened the stability of private banks. This crisis was the predictable result of an unsustainable program to maintain an artificially fixed exchange rate during President Carlos Salinas’ administration, an attempt to enhance his international reputation. With the change in administrations in 1995, the financial community forced a major devaluation, leading to a dramatic increase in inflation and rising interest rates. This pushed millions into bankruptcy, destroyed small businesses, and led to significant segments of the population losing their homes as banks foreclosed on them due to mortgage defaults.

The IMF intervened with a US$50 billion loan, supporting Mexico’s decision to “socialize” the unpayable debts of the private banking system through the poorly named “Banking Fund for Savings Protection,” totalling over 500 billion pesos. The clear purpose was to save private foreign banks, providing them with liquidity and absorbing their unpayable debts at the expense of a public burden that the Mexican people would be paying for many decades. This severely limited the public sector’s ability to finance essential public works and services (UN, 2023).

This stage marks the peak influence of neoliberalism in the region, with policies causing structural transformations and a rise in imports. Argentina, for instance, during the 1990s, promptly implemented all the recommendations of the Washington Consensus. This led to a process of over-indebtedness and capital flight that culminated in 2001 with the worst economic and social crisis in the country’s history. At the end of 2001, Argentina declared a partial default on its external debt of over US$100 billion, one of the largest sovereign debt defaults in world history (Dymski, 2003). The IMF continues to play a crucial role in restructuring and extending international financial capital’s dominion over local productive resources, arbitrating disputes between social classes within countries, and furthering the consolidation of a local capitalist class subordinate to the dictates and power of international capital (Siddiqui, 2022).

Global Debt Build-Up and Rising Interest Rates

Despite the fact that more than 80 percent of the 2023 debt build-up has come from the developed world—with the US, Japan, the UK, and France registering the largest increases—emerging markets have also seen significant rises, particularly in China, India, and Brazil. Rising prices and high inflation have led central banks to increase interest rates to try and contain inflation. Higher interest rates, in turn, mean higher loan repayments. Moreover, the increasing reliance on private creditors, who offer more expensive debt with shorter maturities than official sources, has further complicated debt restructuring for developing countries. Currently, private creditors hold 62 percent of external public debt, up from 47 percent a decade ago. This disparity in interest rates highlights the inherent inequality in the international financial system, burdening developing countries disproportionately. Today, half of all developing nations spend a minimum of 7.4 percent of their export revenues on servicing external public debt (Siddiqui, 2018).

Conclusion

Nearly one hundred years ago, J.M. Keynes warned about the dangers of an unsustainable debt burden imposed on Germany by the victorious powers at Versailles. The aftermath of World War I left many European countries, particularly the defeated ones, grappling with unsustainable war debt. The US emerged as the largest creditor nation, lending money to Germany so it could repay its war debt to the UK, France, and the Netherlands (Siddiqui, 2019). These countries then used German debt payments to pay down their own war debts to the US. This intricate web of debt payments kept tensions high and contributed to the economic crisis that led to the Great Depression in 1929. In 1933, a conference in London aimed at economic recovery failed, further deepening the crisis and contributing to the tensions that led to World War II.

In 2022, developing countries paid an unprecedented $443.5 billion to service their external public and publicly guaranteed debt, according to the World Bank’s International Debt Report 2023. When low-income developing countries face debt distress, it often leads to “protracted recessions, high inflation, and fewer resources going to essential sectors like health, education, and social safety nets, with a disproportionate impact on the poor,” according to the World Bank. Debt distress occurs when a country cannot fulfil its financial obligations, such as debt repayments. The IMF and World Bank believe that 60 percent of low-income developing countries have reached a critical point, which significantly hampers developmental programs.

As of May 2024, global debt has reached a total of US$305 trillion, increasing due to compounding shocks such as COVID-19 and the war in Ukraine. Developing countries, in particular, saw external debt levels grow by over 15% last year compared to pre-pandemic levels, according to the UN Report. This increase has driven up debt servicing costs, straining less developed countries and international financial lending institutions.

The study finds that international financial institutions like the IMF and World Bank continue to play a crucial role in restructuring debt, often extending international financial capital’s control over local resources. There is increasing pressure on developing countries to favor trade and financial liberalization, which can prevent them from strengthening and diversifying their economies. These countries need “degrees of freedom” to develop their economies according to local needs, free from the constraints of international finance.

Today, the challenge for progressive forces in the Global South is to promote regional economic cooperation and organize a countervailing opposition that can limit the IMF and World Bank’s influence. This would allow these countries to pursue development paths that are more aligned with their unique economic and social contexts.

Dr Kalim Siddiqui is an economist specialising in International Political Economy, Development Economics, International Trade, and International Economics. His work, which combines elements of international political economy and development economics, economic policy, economic history and international trade, often challenges prevailing orthodoxy about which policies promote overall development in less-developed countries. Kalim teaches international economics at the Department of Accounting, Finance and Economics, University of Huddersfield, UK. He has taught economics since 1989 at various universities in Norway and the UK.

References

Arellano, C.; Bai, Y. and Mihalache, G. (2024) “Deadly Debt Crises: COVID-19 in Emerging Markets”, Review of Economic Studies, 91 (3): 1243–1290.

Dymski, G. (2003) “The International Debt Crisis”, in Edi by J. Michie, The Handbook of Globalisation, London: Edward Elgar.

IMF. (2023) World Economic Outlook updated, Washington DC.

Siddiqui, K. (2024) “Neocolonialism: An analysis of international factors on the development of the Global South” World Financial Review, December-January. pp.2-12.

Siddiqui, K. (2022) “Capitalism, Imperialism, and Crisis”, European Financial Review, June/July, p.16 – 32.

Siddiqui, K. (2019). “Government Debts and Fiscal Deficits in the UK: A Critical Review” World Review of Political Economy, 10(1): 40 – 68.

Siddiqui, K. (2018). “Capitalism, Globalisation and Inequality” World Financial Review, November-December, p.72 – 77.

Siddiqui, K. (1996) “The Debt Crisis – Need for a New Strategy”, The News, 17th May.

Stiglitz, J. and Rashid, H. (2020) “Averting Catastrophic Debt Crises in Developing Countries”, Centre for Economic Policy Research, July, Columbia University.

Wade, R. (2023) “The World Development Report 2022: Deepening Economic Crisis Recovery in the Context of the International Debt Crisis”, Development and Change 2023; 54(5): 1354–1373.

Companies operating in the life sciences sector must navigate a complex landscape of rules and guidelines to ensure they comply with standards set by regulatory bodies. Failing to comply can result in severe consequences, including hefty fines, legal action, and reputational damage. To mitigate these risks, life sciences companies need to adopt robust compliance monitoring practices. This blog will explore best practices for global compliance monitoring and highlight the importance of investing in the right tools for effective risk management.

Despite rigorous efforts, compliance-related violations continue to rise. Understanding the underlying reasons can help companies address these issues more effectively:

Integration Gaps: Risk identification and coverage might not be fully integrated into the organization’s processes, leading to overlooked risks.

Ineffective Mitigation Plans: Plans may lack clear definitions or a holistic approach, making them less effective in managing identified risks.

Disconnected Monitoring Activities: Monitoring activities may not be well-aligned with mitigation plans, resulting in gaps in risk management.

Resource Constraints: Limited resources can restrict a company’s ability to address identified risks effectively, compromising overall compliance.

Best Practices for Global Compliance Monitoring

To navigate this complex regulatory landscape, life sciences companies must implement effective compliance monitoring practices. Here are some best practices to consider in 2024:

1. Conduct Regular Risk Assessments

Conducting regular risk assessments is a cornerstone of effective compliance monitoring. These assessments help companies identify potential areas of risk and prioritize their compliance efforts accordingly. By systematically evaluating processes, transactions, and business practices, companies can pinpoint vulnerabilities that may lead to noncompliance. Regular risk assessments should include:

Identifying Potential Risks: Mapping out all possible compliance risks, including regulatory, operational, and reputational risks.

Evaluating Impact and Likelihood: Assessing the severity and probability of each identified risk to prioritize mitigation efforts.

Implementing Mitigation Strategies: Developing and deploying strategies to address high-risk areas, reducing the likelihood of noncompliance.

2. Foster Cross-Functional Collaboration

Effective compliance monitoring requires collaboration between various departments, including:

Legal and Compliance: Ensuring that all activities adhere to current regulations and guidelines.

MedicalAffairs: Ensuring the accuracy and integrity of medical information and promotional activities.

Sales and Marketing: Aligning promotional strategies with regulatory requirements to avoid misleading information.

Finance and Operations: Monitoring financial transactions for compliance with anti-bribery and corruption laws.

Cross-functional collaboration ensures that compliance considerations are integrated into business decisions and that compliance risks are identified and addressed early on. By fostering a culture of collaboration, companies can enhance their ability to manage compliance risks comprehensively.

3. Implement Monitoring and Auditing

Regular monitoring and auditing of business practices and transactions are essential for identifying potential compliance issues early on. Monitoring and auditing ensure that corrective actions are taken promptly, preventing minor issues from escalating into significant compliance breaches. This proactive approach to compliance helps maintain the integrity of business operations and regulatory adherence.

4. Provide Regular Training and Education

Providing regular training and education on compliance is vital for ensuring that employees understand the requirements and consequences of noncompliance. Training programs should be tailored to the specific roles and responsibilities of employees, emphasizing the importance of compliance and ethical behaviour. Regular training helps foster a culture of compliance within the organization, making it an integral part of its operations.

5. Ensure Oversight with Designated Roles

Designating a compliance officer and establishing a compliance committee is critical for overseeing the compliance program. These roles provide assurance that key risks have been identified and managed. They also offer support and guidance to ensure that the compliance program is adequately designed and supported. Effective oversight helps maintain the integrity and effectiveness of the compliance program.

6. Focus on Continuous Improvement

Continuous improvement is essential for keeping compliance programs effective over time. This includes regular review and updating of internal policies and procedures, ongoing training and education for employees, and regular assessment of program effectiveness. Continuous improvement ensures that the compliance program evolves to address new risks and regulatory changes, maintaining its relevance and effectiveness.

Leveraging Technology for Global Compliance Monitoring

Incorporating technology into a compliance monitoring plan can significantly enhance the effectiveness and efficiency of compliance programs. Compliance monitoring software can automate and streamline various compliance-related tasks, reducing the risk of human error and ensuring consistent adherence to regulations.

qordata’s global compliance monitoring solution offers comprehensive coverage and leverages AI and machine learning to streamline your monitoring process.

Key features:

Create and track your risk mitigation plan

Prioritizes risk by data sciences techniques

GenAI chatbot to quickly access policies and procedures

Live monitoring with preset, yet customizable checklist

Automated expense monitoring and auditing with full coverage

Computer vision and OCR technology to detect anomalies in sign-in sheets

Remediation with custom workflows

Accessible by external monitors as part of role-based security

Comprehensive analytics with executive dashboards

Integration with Concur, Veeva and other systems

Impact Of These Best Practices For Life Sciences Companies

Implementing robust compliance monitoring best practices can lead to several positive outcomes for life sciences companies. Enhanced risk mitigation is achieved by regularly assessing risks and fostering cross-functional collaboration, allowing companies to reduce their overall risk profile. Strengthened regulatory compliance is another benefit, as consistent monitoring and auditing help ensure adherence to regulatory requirements, minimizing the likelihood of fines or legal actions. Moreover, improved operational efficiency is realized through automation via compliance monitoring software, which streamlines processes and enables better resource allocation, allowing companies to focus on high-risk areas without overextending their workforce.

Building a compliance culture, ongoing training and designated roles for compliance oversight promote ethical behavior among employees at all levels. Access to comprehensive analytics enhances informed decision-making. Additionally, a commitment to continual adaptability ensures that compliance programs remain relevant in a rapidly changing regulatory environment, allowing organizations to quickly address new challenges.

Finally, increased stakeholder confidence is achieved by demonstrating a strong compliance program, which builds trust with investors, partners, and regulatory bodies, enhancing reputation and market position. Adopting these best practices safeguards life sciences companies against compliance risks and positions them for sustainable growth in a highly regulated industry.

Understanding your customers is the key to any successful business. But what if your data is incomplete or inaccurate? This is where a top-ranked data append service comes in. The Data Group, specializing in customer data list appending and enhancing, offers solutions that improve your data quality, leading to better customer insights.

What is Data Append Service?

Data append service is a process of adding new data to your existing customer records. Imagine having a customer list with just names and addresses. With data append services, you can enrich this list with additional details like email addresses, phone numbers, and demographic information. This comprehensive data helps you understand your customers better, allowing for more targeted and effective marketing campaigns.

Why Choose a Data Append Service?

The benefits of using a data append service are numerous. Firstly, it enhances the quality of your customer data, making your marketing efforts more precise. Secondly, it saves time and resources by automating the data enrichment process. Lastly, it improves your customer engagement and retention rates, as you can tailor your communications to meet their specific needs.

How Data Append Service Improves Your Marketing

Marketing is all about reaching the right people with the right message. With The Data Group’s data append service, you can ensure your marketing campaigns hit the mark every time.

Personalized Marketing Campaigns

With more detailed customer information, you can personalize your marketing messages. Personalized emails and targeted ads resonate better with customers, increasing engagement and conversion rates. By knowing more about your customers, you can send them relevant offers and information, making them feel valued and understood.

Improved Decision Making

Having accurate and comprehensive data allows you to make better business decisions. You can identify trends, understand customer behavior, and predict future needs more accurately. This strategic advantage helps you stay ahead of the competition and continuously meet your customers’ expectations.

Higher Return on Investment (ROI)

Better data means better marketing decisions, leading to higher ROI. When you know who your customers are and what they want, your marketing efforts become more efficient and effective. This reduces wasted spend on ineffective campaigns and increases the profitability of your marketing investments.

Why The Data Group is the Best Choice for Data Append Services

When it comes to choosing a data append service, you want to go with a professional and authoritative provider. The Data Group stands out in this field for several reasons.

Industry-Leading Match Rates

The Data Group boasts industry-leading match rates, ensuring you get the most accurate and up-to-date data. This precision is crucial for enhancing your customer database and improving your marketing efforts.

Superior Data Quality

Data quality is at the core of The Data Group’s services. Their continuous testing and refinement processes ensure you always receive top-notch data. This superior quality data leads to more effective marketing and better customer engagement.

Affordable and Efficient Services

Despite offering high-quality services, The Data Group provides affordable solutions. They understand that businesses need to manage costs without compromising on data quality. Their efficient processes and competitive pricing make them a community favorite among marketers and advertisers.

Choosing The Data Group for Your Data Append Needs

Selecting the right data append service is crucial for your business’s success. The Data Group not only provides top-ranked services but also ensures that the data you receive is secure and compliant with all regulations.

Trusted by Many

Many businesses trust The Data Group for their data enhancement needs. Their reliable services and excellent customer support make them a go-to choice for marketers looking to improve their customer data.

Seamless Integration

The Data Group offers seamless integration of their data append services into your existing systems. Whether through their real-time API or batch processing, you can easily enhance your data without disrupting your operations.

Expert Support

The Data Group provides ongoing support to ensure you get the most out of their services. From initial setup to continuous assistance, their team is always ready to help you achieve your marketing goals.

Experience the benefits of accurate and comprehensive customer data with The Data Group. Call 1-800-262-5609 today to start your free trial and see how their data append services can transform your marketing efforts.

Leadership plays a pivotal role in driving change. At the organisational level, cultural transformation—not just policy change—is key to normalising conversations about reproductive health. CEOs and leaders must address reproductive health with the same inclusivity and concern as other health matters.

In today’s rapidly evolving corporate landscape, CEOs play a pivotal role not just in driving financial success but also in spearheading cultural transformations within their organisations.

One area increasingly recognised as crucial but still often overlooked is reproductive health. For business leaders, fostering a culture that integrates awareness and proactive management of reproductive health goes beyond implementing new policies; it involves reshaping the organisational ethos to prioritise inclusivity and proactive care.

For instance, Salesforce has rolled out new benefits including expanding sick time to all US employees and expanding parental support programs. For women who want to have a family, Salesforce offers fertility benefits and a paid six month leave policy. Salesforce has also been vocal about its commitment to reproductive rights, particularly in response to restrictive abortion laws in various US states. For example, the company has offered to relocate employees who are affected by local legislation that contradicts their values on reproductive health.

The leadership imperative

Let’s face it, change starts at the top. When CEOs and other leaders are open about topics like reproductive health, it sets the tone for everyone else. While CEOs and other top executives are uniquely positioned to normalise conversations about reproductive health, it is equally important for other leaders and managers to participate actively. Treating reproductive health with the same level of importance as other health matters is not just about being progressive—it’s essential for a comprehensive and humane approach in managing workforce health. The goal is to transcend mere compliance or superficial engagement and embed these values into the corporate culture genuinely.

Overcoming communication barriers

A significant challenge in many workplaces is the discomfort employees face when discussing sensitive health issues, particularly reproductive health, with their managers. This gap can lead to unaddressed health concerns and increased stress for employees, which in turn affects productivity and job satisfaction. CEOs can set the tone, promoting an environment where such conversations are encouraged and normalised. Training and preparing managers to handle these discussions with empathy and discretion is crucial. Additionally, recognising and respecting cultural differences in discussions about reproductive health can help tailor communication strategies to be more inclusive.

Strategic initiatives for supporting reproductive health

So, how can CEOs and leaders make a real difference? Here are a few practical ideas:

1. Boosting employee benefits through education

Often, employees only seek information about health policies when in crisis. Leaders can facilitate a shift towards preventive health education, providing comprehensive information on topics like menstrual health, contraception, fertility and more. By enhancing awareness and education about reproductive health, CEOs can help demystify these issues and remove associated stigmas, encouraging earlier and more frequent engagement with available health benefits.

2. Thinking long term with a lifecycle approach

Viewing reproductive health as a continuum rather than a series of episodic or emergency-driven, embracing a lifecycle perspective can lead to better health outcomes. This approach acknowledges that employees may experience various health needs over time. Understanding and planning for these can encourage preventative care, ultimately reducing the need for more intensive treatments and supporting continuous workforce participation.

3. Embracing inclusivity

Reproductive health isn’t just a “woman’s issue”. It affects everyone, regardless of gender identity. By educating all employees – women, men, non-binary folks – you’re not only breaking down stigmas but also building a more supportive and understanding workplace.

Broader business benefits i.e. “the bigger picture”

When companies prioritise reproductive health, everyone wins. For CEOs looking to future-proof their businesses, supporting reproductive health can enhance employee retention. Employees who feel valued and supported are less likely to leave, reducing turnover costs and preserving institutional knowledge.

Additionally, addressing reproductive health can play a critical role in narrowing the gender pay gap, which often widens during key life stages such as parenthood and menopause. By creating a supportive environment, companies not only advance equality but also enhance their overall market competitiveness.

Lastly, the external perception of a company that actively supports its employees can significantly boost its brand image. In my experience working with global companies on reputational trends, those that are seen as family-friendly and supportive of balanced work-life dynamics are more attractive to potential candidates, clients, and partners. It is crucial, however, to ensure that these initiatives are implemented genuinely, avoiding tokenism that can undermine trust and authenticity.

Measuring success and legal considerations

To evaluate the effectiveness of reproductive health initiatives companies should establish clear metrics and benchmarks. These could include employee satisfaction surveys, retention rates, and utilisation of health benefits. Additionally understanding the legal and policy implications is vital. Companies must navigate privacy concerns and legal protections while ensuring compliance with relevant regulations.

Conclusion

For CEOs, the message is clear: integrate reproductive health into the corporate wellness framework in a way that respects and supports all employees. By doing so, leaders not only enhance their company’s operational effectiveness but also contribute to a more equitable and health-conscious business environment. In the journey toward comprehensive corporate health requires a collective effort from all levels of leadership, with the CEO playing a transformative and impactful role.

Siera Torontowis co-founder of Girl You Need To Know This. She has worked in roles advising businesses on improving their reputation and ESG ratings. Siera has worked for some of the world’s largest healthcare companies for over 10 years, with the purpose of bringing evidence-based content to the point of care. https://girlyouneedtoknowthis.com/

Public discourse on mental health has made significant progress, with mental health becoming recognised as an important focus across organisations globally. This is a positive step forward and raises the importance of addressing mental health in corporate environments. A growing body of research provides guidance on both the root causes of poor mental health and what support structures organisations can implement, and corporate leaders now have an obligation to apply the research.

Recognising the extent of the challenge

Feelings of stress, anxiety, and depression contribute to poor mental health, whether they stem from personal or professional causes. Regarding the latter, we can turn to an extreme professional environment—cybersecurity—to learn more and extrapolate to other industries. Cybersecurity is one of the most fast paced, demanding, high risk sectors, and many folks who work in this environment experience some combination of the factors that contribute to poor mental health.

A new MultiTeam Solutions’ report titled, “Stress & Burnout in Cybersecurity: The Risk of a Thousand Papercuts” has revealed the mental health pressures cybersecurity professionals are facing. The report found that while 52% of cybersecurity professionals felt quite resilient to stress, almost the same number (50%) said that within the next year or sooner they are going to reach a point of burnout (with “burnout” generally representing a point at which employees are no longer having the motivation to do their job well) . Within this, the data indicated that 35% of respondents are going to reach burnout in the next six months.

When asked about the support in place within a professional work environment, four-fifths (81%) felt that Senior Level Management (SLM) at least somewhat understand their stress. Yet concerningly, only 23% of cybersecurity professionals believe that SLM actively works to reduce their stress, with nearly half of respondents perceiving that SLM is adding to their stress.

While the findings from MultiTeam Solutions’ report provide insights into the mental health struggles being faced in cybersecurity, the identified trends can be applied across the broad range of industries that make up the professional services industry, including finance. There are serious implications if these issues are not properly addressed, including employee burnout, low productivity, employee turnover, and a heightened risk of work not becoming completed to required standards. The latter point is important, as this can have grave legal, regulatory, and financial repercussions, and this is not to mention the similarly concerning repercussions of losing employees who take with them the institutional knowledge and expertise they’ve developed while working for an organisation.

Below are two examples of applying this research to address mental health challenges at work.

Breaking down silos

While work silos ensure the effective distribution and management of work, they also isolate departments or divisions from others in their organisation. And, furthermore, silos develop within silos, isolating working groups and individuals. The latter, isolated individuals, is of the greatest concern when it comes to mental health.

Isolation is a common instigator of poor mental health in the workplace, and particularly at the individual level (though also for teams). When a person’s or team’s tasks are being completed and goals are being met, isolation seems effective. On the other side of the spectrum, though, when an individual is overwhelmed by their tasks and goals are seemingly unattainable, isolation can lead to frustration, blame, shame, anger, guilt, etc. with nowhere to turn for support. What people need in these situations, especially isolated individuals, is collaboration to connect with others, support each other, and problem-solve together.

The key for organisations is to open up channels of communication between silos, first by identifying specific employees to connect as boundary spanners between silos, and second by shifting toward a more matrix structure that allows individuals and teams to share functions and responsibilities. Additionally, leaders need support, because managing these processes requires resources to enact key leadership behaviours such as connecting goals within silos to higher-order goals that everyone is working toward together and coordinating the sharing of information across silo boundaries.

Challenging the imposter syndrome

Imposter syndrome is a common feeling experienced across all organisational levels, from senior management through to junior teams. It is often triggered by self-doubt, whereby individuals consistently question their ability to fulfil what is required of them at work. According to a survey conducted by Reed Recruitment, 40% of workers in the UK admitted to experiencing self-doubt in their abilities during their career. This is usually accompanied by fears of being exposed by colleagues, which then enables feelings of anxiety, sensitivity to minor mistakes and feedback, and fear of failure—all of which take a toll on one’s mental health.

Importantly, there are strategies that can be deployed in a corporate environment to address imposter syndrome, with a focus on the individual who is experiencing these feelings. First, supporting employees to mentor their peers or subordinates on separating fact (e.g., demonstrable examples where they have excelled in their position), from fiction (e.g., their own self-doubting interpretation of their performance) is a meaningful exercise. Often with imposter syndrome, the feeling of dissatisfaction stems from the individual’s own interpretation, which sets them against a hypothetical benchmark that cannot be reached. Second, organisations can create forums with employees of all levels within the organisation to share challenges they might be facing from a professional standpoint. This approach brings people into connection and community to see they are not the only one experiencing challenges.

A focus on the individual

Of the strategies offered above, the common factor is that the focus starts with the individual. Clear actions can be taken, from breaking down work silos that isolate individuals (and teams) to addressing the human and workplace factors that contribute to feelings of imposter syndrome, burnout, and workplace stress.

There is a clear business case for such initiatives as well. A positive work environment, regardless of industry, lends itself to increased creativity, motivation, work satisfaction, performance, and, overall, employee retention. It’s the reason why mental health needs to be a priority for the corporate sector.

Dr. Daniel Shoreis an expert in workplace psychology. He focuses on teams, multi-team systems, and leadership with a human-centred approach to fostering connections within and between teams. He is the co-founder of the Integr8 training program, which is built on 5 years of US- and European-government funded research.

By Terence Tse

CFOs are evolving into AI-driven transformation orchestrators, balancing finance, technology, and strategy while upskilling teams, managing risks, and driving measurable business value.

A key insight from this year’s AI for CFOs event, organized...

The World Financial Review uses cookies to improve site functionality, provide you with a better browsing experience, and to enable our partners to advertise to you. Detailed information on the use of cookies on this Site, and how you can decline them, is provided in our Privacy Policy and Terms and Conditions. By clicking on the accept button and using this Site, you consent to our Privacy Policy and Terms and Conditions. ACCEPT

Privacy & Cookies Policy

Privacy Overview

This website uses cookies to improve your experience while you navigate through the website. Out of these cookies, the cookies that are categorized as necessary are stored on your browser as they are essential for the working of basic functionalities of the website. We also use third-party cookies that help us analyze and understand how you use this website. These cookies will be stored in your browser only with your consent. You also have the option to opt-out of these cookies. But opting out of some of these cookies may have an effect on your browsing experience.

Necessary cookies are absolutely essential for the website to function properly. This category only includes cookies that ensures basic functionalities and security features of the website. These cookies do not store any personal information.

Any cookies that may not be particularly necessary for the website to function and is used specifically to collect user personal data via analytics, ads, other embedded contents are termed as non-necessary cookies. It is mandatory to procure user consent prior to running these cookies on your website.

")

")

")

")

")

Siera Torontow

Siera Torontow")

Dr. Daniel Shore

Dr. Daniel Shore