By Rahmat Poudineh, Anupama Sen, and Dr. Bassam Fattouh

In this article, we argue that investment in renewable energy sources is a no-regret strategy for hydrocarbon exporting economies of the Middle East and North Africa (MENA). It is also in line with some of the pre-renewable energy sector reforms in the region. Indeed, much of their ongoing energy sector reforms – such as the removal of fossil fuel subsidies – complement the move to a strong renewables policy. But their electricity markets, which are currently skewed in favour of hydrocarbons, will need to be carefully designed to support renewables. A holistic approach to energy policy, including establishing stable regulatory frameworks, robust independent institutions, and effective risk mitigation measures will be critical to advancing renewables in the region.

One might wonder that why resource-rich countries of Middle East and North Africa should be interested in renewable energy?

First, rapid energy demand growth is a serious issue in hydrocarbon-rich MENA countries. It is projected that the region’s primary energy demand will be doubled by 2030. Economic and population growth, rapid urbanisation, and heavily subsidised end users’ tariffs are the main factors behind soaring domestic energy demands. Just between 2000 and 2011, energy consumption almost doubled in Oman and tripled in Qatar. Other countries have also more or less a similar experience. The result is that many of these countries have had to divert increasing quantities of crude oil, fuel oil, diesel, and natural gas to satisfy domestic demand away from high-priced international markets. Given their heavy economic dependence on oil and gas export revenues, this puts them on a fiscally unsustainable path. The ability of renewable energy to substitute hydrocarbon fuels in most sectors of economy improves fiscal stability.

Second, energy security is of paramount importance for these countries. Contrary to popular belief, not all countries of the region are fully self-sufficient in terms of natural gas, which is the key fuel for power generation in the region. Indeed UAE and Kuwait are already net importers and there is a possibility that more countries in the region will become net gas importers in the future, if domestic demand is not contained or domestic gas production is not boosted. Other countries that seemingly look self-sufficient are also not very secured. For example, Iran is the third largest global producer of natural gas with 6.1 percent share of the world’s natural gas market. However, Iran’s gas production primarily satisfies subsidised domestic demand. Over the years, the gas production in this country has grown in tandem with consumption, limiting its ability to export any sizeable volume. If for any reason (for example, lack of investment due to sanctions), gas production does not keep pace with demand (or demand outpaces domestic gas production), the gas self-sufficiency of the country will be undermined. Investment in renewable sources can replace existing gas power plants that are used as base load and thus help to restrain or reduce gas demand.

Third, the Middle East region has one of the highest pollutant levels in the world with some of the major cities in Iran and Saudi Arabia being the worst affected. On some days, the recorded air pollution level exceeds 5 to 10 times the limit announced by WHO. Apart from frequent sandstorms that affect some parts of the continent, in recent years, industrial emissions and car emissions have significantly contributed to the poor air quality.

Fourth, the uncertainty about long-term oil demand is rising in the agenda of policymakers in the region. The topic of peak oil demand has especially received much attention in recent years and there are contradictory estimations about its occurrence and time frame. We do not know if and/or when there is going to be a peak oil demand because it is an uncertain phenomenon. However, one thing is certain: renewable investment will benefit MENA oil-rich countries whether or not there is a peak oil demand. The logic is simple: if it turns out that there is a peak oil demand, the optimum strategy for these countries is to maximise their oil export revenue in short to medium term before demand for oil is affected. Alternatively, if it became evident that there is no peak oil demand in a foreseeable future, renewable investment maximises their long-term revenue from hydrocarbon export (given their rising domestic energy demand).

This brings us to the second question on how to enable renewable investment in MENA resource-rich countries. Although, as mentioned above, these countries have different objectives to other developing countries in deploying renewables, the path to achieving these objectives is the same, and it involves creating investment incentives and eliminating or lowering the barriers to investment. Some of the barriers in MENA resource-rich countries are also similar to other developing countries, but the options for investment incentives are different because of their dependence on oil/gas export revenues and massive domestic consumption of subsidised fossil fuels.

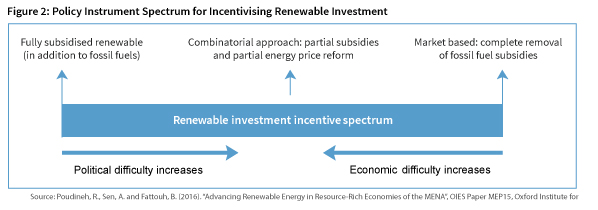

Figure 1 illustrates a framework for enabling renewable deployment in the MENA. As seen to the right of the figure, governments must design policies that create incentives for investment. There are two extreme policy solutions to incentivise renewable investment in resource-rich countries:1

The government introduces a full renewable subsidy programme (in addition to existing fossil fuel subsidies), steering investment towards specific renewables. This requires long-term government support and commitment to create investor confidence.

The government eliminates barriers and lets economics determine market outcomes with respect to the quantity and type of renewable technologies, requiring the complete removal of fossil fuel subsidies (and internalising the cost of externalities) so that those forms of renewable technologies that are already competitive can kick in.

The problem with either of these polar solutions is implementation challenges. For example, market-based approaches are politically difficult to implement in the MENA because it entails full energy price reform within a short period of time to enable the market and that would be nothing short of a revolution. On the other hand, moving towards a fully subsidised renewable programme increases fiscal and economic pressures, particularly as it would be in addition to existing fossil fuel subsidies. Therefore, we argue that investment incentives for renewable deployment in these countries need to be provided through a combinatorial approach, involving partial energy price reform and partial subsidy programme. Figure 2 shows this as a dynamic process. Countries can start from the most feasible point on the policy instrument spectrum based on their current contexts, and gradually move towards phasing out fossil fuel subsidies over medium to long term. This not only reduces the fiscal pressure on government budgets, but also averts political risks by allowing businesses and households to slowly adapt to the new environment where energy carriers are priced at their full economic costs.

As seen in Figure 1, in addition to providing incentives, governments need to design appropriate policies around tackling barriers to renewables deployment, in the areas of institutional challenges, grid connection, and management and risk and uncertainties

Future electricity markets will need new supporting institutions that complement the characteristics of a sector that is predominantly based on renewable energy. This includes renewable energy entities and regulators, their resources, competencies, laws, strategies, and activities. In recent years, many of the MENA’s resource-rich countries have established dedicated agencies to oversee the scaling up of renewable energy. Examples include Renewable Energy and Energy Conservation Directorate at the Ministry of Energy and Mines in Algeria, the Department of Energy (established in 2018) in UAE (Abu Dhabi), Saudi Arabia’s Renewable Energy Project Development Office (REPDO), and the Renewable Energy Organization of Iran (SUNA). However, these institutions are not sufficiently integrated with other energy institutions in these countries, which have been historically dominated by oil and gas, and their role is often confined to administering tenders for private renewable project developers rather than enforcing structural change. These agencies also face powerful state-owned utility companies that oversee generation, transmission, and distribution assets, which may view renewables as a disruption to their business models.

The presence of an independent and robust regulatory entity is another key ingredient of unlocking renewable deployment in these countries, as governments often overturn regulatory decisions with respect to issues that are deemed politically sensitive such as electricy tariffs. Institutions also require a rethinking of the scope and purpose of regulation as new actors may enter the system, or existing actors may change their role, requiring modification to the institutional setting of the power system.

Beyond the traditional concept of institutions in the form of top-down structures, electricity sectors with high penetration of renewables and distributed resources such as batteries and demand response require compatible regulation and operating procedure. This includes universally accepted interfaces, protocols, and standards to ensure a common communication vocabulary among system components within and between networks and the development of appropriate regulations and operativng procedures in conjunction with the development of technologies. Grid connection and management rules (e.g., priority access and priority dispatch) also need to be updated to account for growth of renewables.

No private investment, in any sector, will happen if the problem of risk is not dealt with. Renewable investors face a range of risks including political, policy and regulatory, technology risk, currency and liquidity risk, and finally, power off-taker risks. These risks not only affect the appetite of investors and innovators in renewable energy, but more importantly the cost of capital and ability to finance projects.

Political risks include political events that negatively impact the value of investment, such as war, civil disturbance, expropriation, and non-honouring of contracts. Policy and regulatory risks refer to changes in investment incentives (for example, removal of renewable subsidies), network codes, grid connection costs model, and permitting processes, among others. In resource-rich MENA countries, renewable investors face uncertainty in both where there is no specific renewable policy as well as after policy incentives are designed and implemented. Pre-implementation uncertainties include not knowing if, when, or what type of policy will be implemented to incentivise renewables, whereas post-implementation uncertainties are related to the stability, transparency, trust, and insurance for long-term support. Developers also face technology risks related to nascent renewable technologies which may not have a proven track record of operation in the MENA region, or where the local workforce may lack the skills needed to operate renewable technologies. The currency risk pertains to the volatility of domestic currency value with respect to foreign currencies. This is particularly important as most renewable power producers’ costs are in hard currency (e.g., dollar or euro because of loans), whereas their revenue is in local currency (e.g., feed in tariff paid in domestic currency). The credit and/or default risk arises when the market structure has only one offtaker of renewable electricity (e.g. public utility company) and power producers have no choice but to contract with the single buyer and bear the credit risk.

Another important but often overlooked factor in unlocking the potential for renewable investment is that renewable policy should be integrated into the current power sector reform. The current ‘idealised’ model of liberalised electricity markets (comprising wholesale markets for in generation, and competition in retail supply, with network regulation in transmission and distribution), in which prices are set based on marginal cost of electricity, was pioneered in OECD countries and is based on a market designed for fossil fuel electricity with positive marginal costs. This ‘energy-only’ market relies on the price signal to organise both short-term coordination for dispatching, and long-term coordination for investment in generation capacity2. The imposition of intermittent renewables that have near-zero marginal (but high capital costs) onto this market has led to a breakdown in this model and a tension between the goals of decarbonisation and liberalisation.

Several MENA countries have begun undertaking power sector reforms, with the aim of restructuring the energy sector, allowing private-sector participation, removing energy subsidies, and reducing reliance on the public budget. The challenge that they face is in designing a reform model that incentivises investment and delivers efficient outcomes, while simultaneously integrating a rising proportion of intermittent renewable resources. Failure to adopt a reform model that balances these goals and does so in alignment with their unique contexts could frustrate or reverse the process of reform at later stages.

Resource-rich MENA countries have the opportunity to design their electricity markets around the incorporation of renewables at the outset. They can further tap into years of international experience by adopting market structures that avoid the risk of market breakdown under fully liberalised electricity systems with a high share of non-dispatchable resources.

About the Author

Rahmat Poudineh is lead senior research fellow of electricy programme at the Oxford Institute of Energy studies. He is experienced in the economics and regulation of electricity sector. Rahmat has published numerous academic articles on network regulation, electricity market design, power sector reform, renewable support schemes, and gas and power interdependence.

Rahmat Poudineh is lead senior research fellow of electricy programme at the Oxford Institute of Energy studies. He is experienced in the economics and regulation of electricity sector. Rahmat has published numerous academic articles on network regulation, electricity market design, power sector reform, renewable support schemes, and gas and power interdependence.

Anupama Sen is a Senior Research Fellow at the Oxford Institute for Energy Studies. She has published extensively on the applied economics of energy in developing countries, spanning the oil, gas and electricity sectors. Anupama is also a Fellow of the Cambridge Commonwealth Society and was a Visiting Fellow at Wolfson College, Cambridge.

Anupama Sen is a Senior Research Fellow at the Oxford Institute for Energy Studies. She has published extensively on the applied economics of energy in developing countries, spanning the oil, gas and electricity sectors. Anupama is also a Fellow of the Cambridge Commonwealth Society and was a Visiting Fellow at Wolfson College, Cambridge.

Dr. Bassam Fattouh is Director of the Oxford Institute for Energy Studies and Professor at the School of Oriental and African Studies. He is widely published on oil and gas topics and his publications have appeared in academic and professional journals. He also acts as an adviser to governments and industry, and is a regular speaker at international conferences.

Dr. Bassam Fattouh is Director of the Oxford Institute for Energy Studies and Professor at the School of Oriental and African Studies. He is widely published on oil and gas topics and his publications have appeared in academic and professional journals. He also acts as an adviser to governments and industry, and is a regular speaker at international conferences.

References

1. Poudineh, R., Sen, A. and Fattouh, B. (2016). “Advancing Renewable Energy in Resource-Rich Economies of the MENA”, OIES Paper MEP15, Oxford Institute for Energy Studies.

2. Roques, F. and Finon, D. (2017). ‘Adapting electricity markets to decarbonisation and security of supply objectives: Toward a hybrid regime?’, Energy Policy, 105, 584–96.

{kind=link}