By Mohamed Ali Chatti and Ouidad Yousfi

There are some similarities between Islamic and conventional PE, like for example the active participation, the quick exit of the PE fund and the close partnership. But they display also different features.

Almost everyone today has heard of the terms: private equity (PE), venture capital (VC) and leveraged Buy out acquisitions (LBO). These activities are sources of funding for a large range of unlisted firms.

Supported by state aid programs and tax incentives, the story of PE has its origins in the US. In 1946, Georges Doriot, Ralph Fanders and Karl Compton established the American Research and Development Corporation (ARDC). The objective was to fund private investments of soldiers returning from the World War II. It is officially the first VC institution. Then, the number of PE investments and the volume of raised funds have increased significantly. Indeed, the amount of money raised by PE investors has sometimes exceeded capital issued through Initial Public Offering (IPO).

Over the past thirty years, PE projects have grown dramatically all over the world. In 2007, funds managers raised more than US$ 400 billion and invested more than US$ 600 billion in enterprises all over the world (Gierath, 2010).

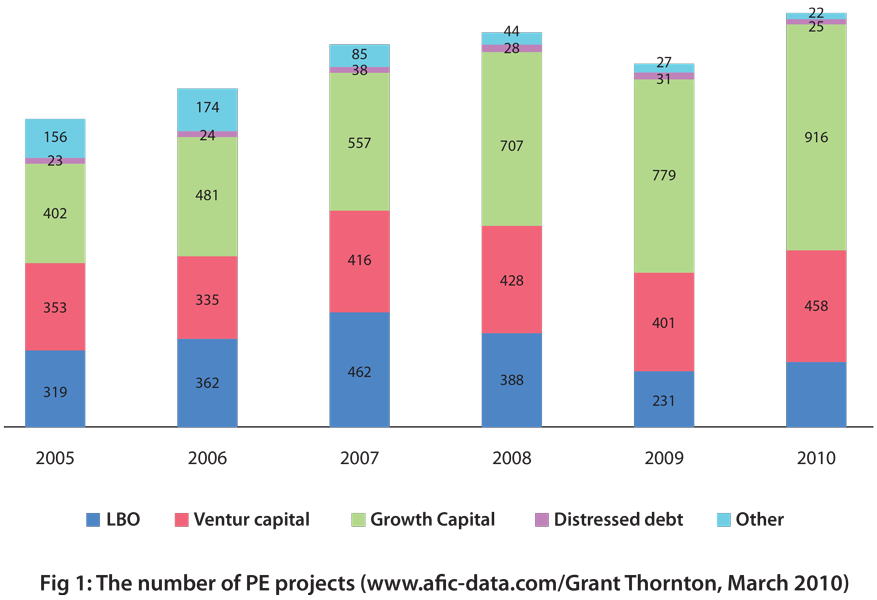

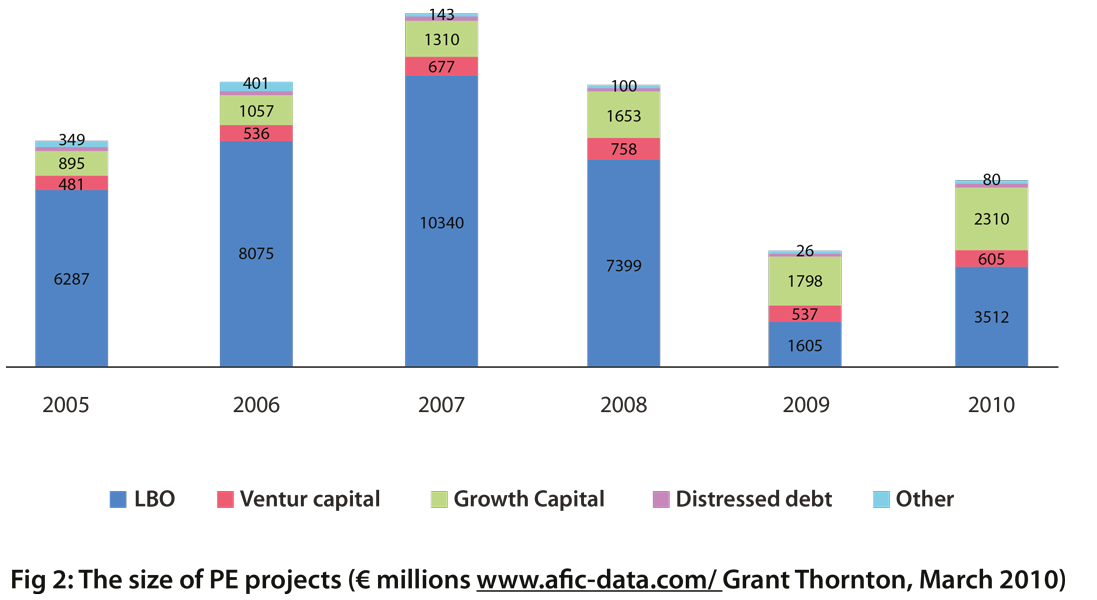

After the financial subprime crisis, it became difficult to secure debt financing for new projects. One explanation is the lack of liquidity in private markets due to the reluctance of institutional investors and the high investment losses. In addition, banks become more selective. As a consequence, investors reduce their commitments to new projects and even raise lower capital in project in which they were involved. Another explanation closely related to the investors’ reluctance, exit routes become tighter in this unpredictable environment. (See Fig 1 and Fig 2)

Regardless these challenges, the PE industry is still a source of job creation and it improves economic growth. It is based on partnerships in non-listed companies, for example, innovative or star-up firms, firms operating in the middle market, firms in financial distress and even public firms that want to go private through buyout acquisitions. Entrepreneurs are very often wealth-constrained and/or have no business experience to turn alone their projects. In addition, they cannot raise financing in the debt market or the public equity market since they do not have real guarantees and collateral.

We should notice that private equity is broad term that refers to funds that have been raised in the private markets. Despite the increase of funds issued in PE investments and its important role in corporate finance, only the venture capital and buyout investments have received considerable attention in the academic literature. But in practice, PE is used in many stages of the cycle life of the enterprise.

One development worth noting here is the tremendous development of private equity based on Shari’ah principles in the Middle East. Despite the fact that the first Islamic banks had been established in the 70s, the first Islamic PE funds appear only in the last decade. Islamic banks like for example Arcapita Bank and Gulf Finance House set up investment funds to take stakes in growing unlisted companies. Last years, they generate high yields in some business lines which were for a long time dedicated to conventional players.

In 2003, there are more than 300 Islamic financial institutions operating in 70 countries. The total amount of deposits is around US$ 120 billion while the amount of raised funds managed by Islamic PE funds varies between US$ 300 and US$ 800 billion. We should notice that US$ 100 billion are invested in the Gulf Cooperation Council (GCC) countries1.

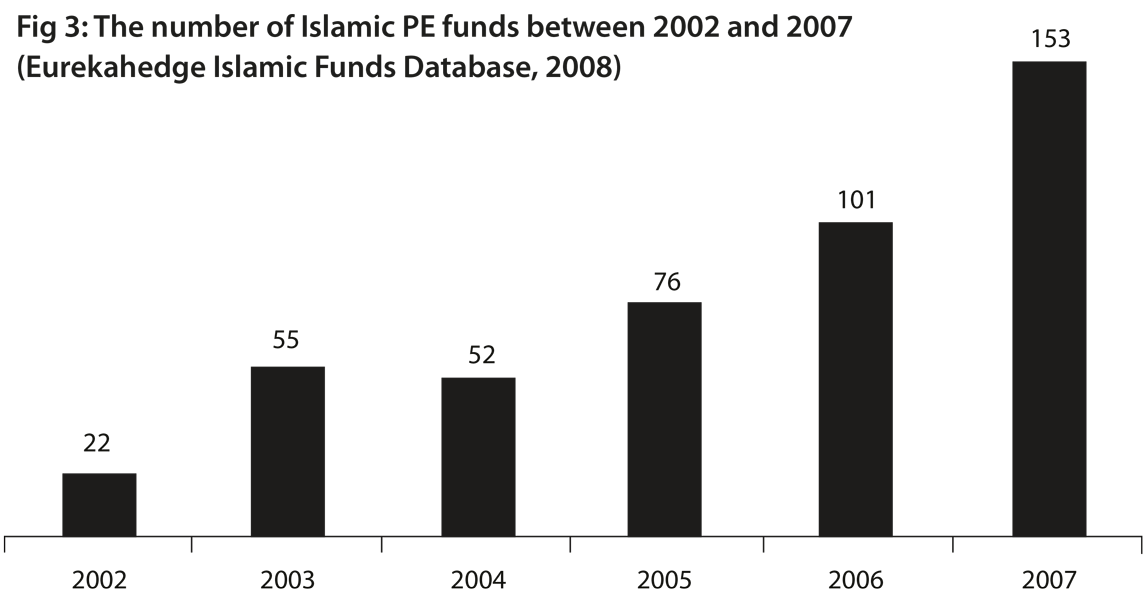

Nowadays, many conventional banks operate Islamic Windows in order to attract both Muslim and non Muslim clients who are more and more cautious particularly after the financial subprime crisis. This shows the attractiveness and the increasing interest for Islamic PE industry. Many international financial centers have set up Islamic benchmarks, like for example the Dow Jones Islamic Market Index2 in New York and the FTSE Global Islamic Index3 in London. (Fig 3)

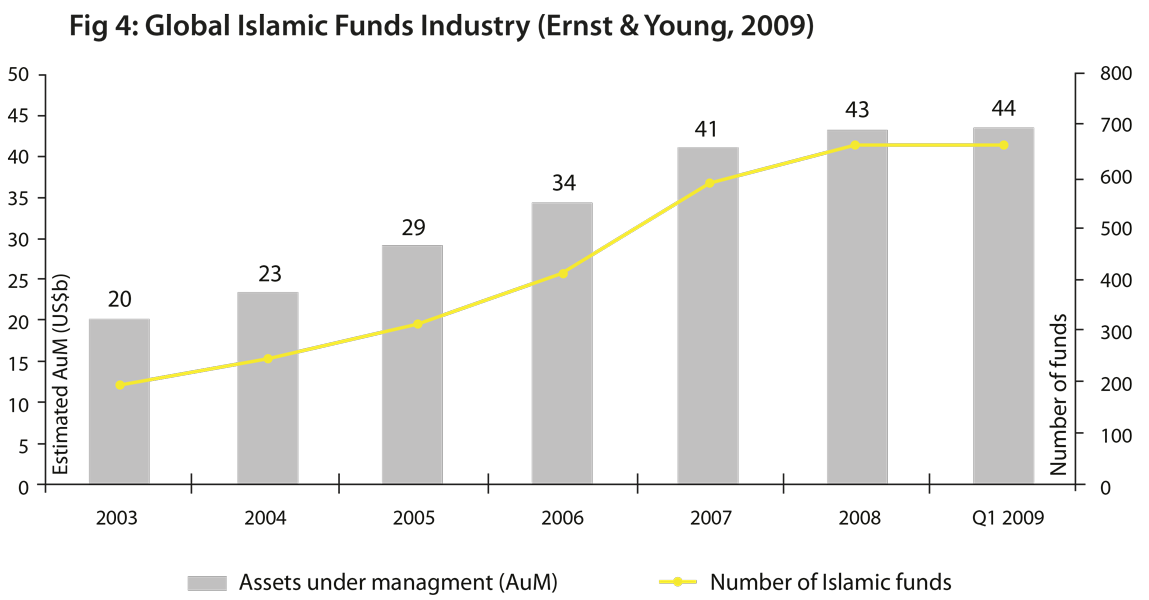

In 2008, the number of Islamic projects in Kuwait has exceeded the number of their conventional counterparts; it increased by 300 per cent compared to 2003. There are more than 130 Shari’ah compliant mutual funds operating in Malaysia – the centre of Islamic finance – and 120 in Saudi Arabia. In the UAE, the number of Islamic PE fund has almost quadrupled between 2005 and 2008: they increased from 15 to 63 (Seera investment Bank and Dow Jones, 2008). (Fig 4)

It is straightforward to see that there are some similarities between Islamic and conventional PE, like for example the active participation, the quick exit of the PE fund and the close partnership. But they display also different features.

1.Similarities between conventional versus Islamic Private Equity

Whether PE is shari’ah compliant or not, it increases the development of SME and contributes significantly to the increase of the productivity of the economy. Indeed, PE industry satisfies the specific needs of growing companies that cannot get credit financing. For each stage, it provides funds, specific services and skills to enable the firm to move to the next stage. The entrepreneur/PE fund partnership is based on sharing experience, skills and on trust. There are four common features in Islamic and conventional PE financing:

First, it is based on a close and active partnership. In contrast with passive financiers, PE investor participates in all the tasks in the selected project. For instance, the entrepreneur benefits from the professional network and contacts of the PE fund. It helps developing business plans, looking for new partners and taking decisions.

Second, the entrepreneur is very often wealth-constrained particularly in start-up firms and has no business experience/skills and no guarantees. Risks exposure increases significantly. This is why the PE fund is very selective: the initial review leads to the rejection of a large number of proposals. Only few projects are chosen after the second review. Business plans are scrutinized particularly in foreign countries because it is facing additional risks (for example, exchange and legal risks). If the entrepreneur’s proposal belongs to the surviving ones, the PE investors organize meetings and telephone discussions with the key staff and sometimes with customers, suppliers and creditors. PE partnership is value enhancing in the sense it decreases risks, creates a real dynamic and provides financial resources, varied skills and more effective governance.

Third, PE financed firms must show high potential for generating cash-flows during a fixed period (it varies between 2 and 8 years). The choice of the exit route is the last way to earn money for both partners. Dividends are very often distributed randomly particularly the first years. There are three main exit routes: IPO for the most successful projects, trade sale and buyback. Living-dead projects are abandoned quickly showing the ability of PE fund to filter goods projects from bad ones.

Finally, PE funds are financed by equity commitments from institutional investors, wealthy individuals and business families, retired managers, corporations and institutions. They are the limited partners LP. Their aim is to diversify their portfolios and to raise capital in exchange of high returns. This equity is invested by the professional PE managers who are the general partners GP. Their mission is to select and manage the target companies and conduct the exit strategy in a fixed period of time. As a consequence, GP cannot keep the entrepreneur’s project for a longer period than the LP money.

2.Conventional versus Islamic Private Equity: what is different?

The tremendous development of Islamic PE is explained by several facts. First, many Muslims (for example, farmers and artisans) still refuse to deposit their savings in banks, particularly conventional ones. These savings are increasing dramatically and captured in the last years by Islamic PE funds.

In addition, many non Muslims investors and depositors become reluctant to the conventional banking system after the financial subprime crisis.

Less investment opportunities

Islamic PE finance only Shari’ah compliant projects to make a halal4 profit. This means that Islamic PE funds have lower investment opportunities than the conventional ones as many investments are not in accordance with the shari’ah principles (haram investments) and are financed by interest-bearing instruments (see figure 5).

However, there is no exhaustive list of halal investments: it depends on the Islamic scholars’ school (Malikite, Hanafite, Chafiite and Hanbalite) and on the degree of religiosity of the country. It varies also from one shari’ah committee to another.

In practice, all the investments related to pork products, blood, pornography or obscenity in any form, gambling, casinos, lotteries, trading on human cloning and human fetuses… are strictly prohibited in Islamic finance. Some conventional projects based on interest, speculation and insurance cannot get Islamic PE financing. In practice some other activities should be avoided as they lead to confused situations, e.g. hotel industry. It depends on the financial criteria retained by Islamic scholars. If the target companies satisfy some ratios, they become shari’ah compliant. For instance, despite the fact that interests are prohibited, Islamic PE fund can raise financing in leveraged investments only if the total interest-based debt divided by assets is less than 33 per cent.

Different financing methods

Islamic PE financing is based on the Profit and Loss Sharing PLS principle: it implies that the entrepreneur and the fund share benefits and losses. There are three methods of financing in Islamic PE:

First, Mudarabah scheme (profit sharing) that is very close the VC financing is used to finance innovative SMEs and start-ups. The Islamic PE raises financing and the entrepreneur brings skills and know-how to the project. The entrepreneur has all the control rights: unlike conventional PE, the fund cannot participate actively to the management of the target. However, the entrepreneur must report regularly information to the PE fund. The latter is considered as an alert partner. If the project is successful, the profit will be distributed according a pre-agreed ratio. Otherwise, losses are borne solely by the capital provider and the entrepreneur losses time and energy.

Second, all parties may contribute jointly to the funding of the target. They are actively involved in the project. This is Musharakah financing mode. Profits and losses are shared between them according to their financial contribution or on pre-agreed ratios. Unlike Mudarabah, Islamic PE is a member of the directors’ board. Musharaka principle looks like non-venture private equity (LBO, growth capital,..). But in the latter case, the project is very often financed through a mixture of debt and equity. The level of debt is significantly high. The project must be very profitable to cover the principal and the interests.

Third, it is also possible to authorize one party to confer the power and rights to act on behalf of the other one, based on agreed terms and conditions. This is the Wakalah financing mode. On the contrary, conventional PE is based on effective control and active monitoring. PE fund issues common and convertible securities5 in exchange for shares of benefit and control. If the entrepreneur takes very risky decisions to enjoy perks (official car, travelling fees, improving their image/market reputation…) or the project does not perform as well as it was expected in business plan, the PE fund converts securities into common stocks to diminish the entrepreneur’s control. Convertible securities and monitoring are mean to decrease agency costs.

Varied and different risks

Islamic and conventional PE fund are exposed to significant and negative fluctuations of prices and therefore to the market risk, as well as default and liquidity risks and adverse selection problems of targets.

However, to overcome these risks, they have different techniques. In conventional PE, future contracts decrease this risk. But they very often lead to speculation which is prohibited in Islamic transactions. In the same sense, Islamic PE does not allow forward sale of goods we do not own at the date t=0. Thus, futures contracts such as options and futures are not suited for Islamic one. But we find different variation of these contracts. Despite the fact that these products are largely inspired by conventional ones, they do not offer the same guarantees particularly in terms of coverage of risks. The objective of these products is to protect both parties by sharing profits and losses between the entrepreneur and the PE fund.

Because they cannot invest in many prohibited projects, diversification among sectors and activities is not always possible. Thus, Islamic PE funds face higher risks than their conventional counterparts. For instance, the entrepreneur bears lower risks than in interest based financing system and does not provide collateral and guarantees: damages and losses as well as benefits are shared between the two parties. As a consequence, Islamic PE funds are more selective than conventional one. They are also exposed to a different structure of risks because of the high number of agreements that should be written in each stage of the transaction. This takes time and need the involvement of many contractors (the bank, the fund, shari’ah board, the entrepreneur, the vendor,…) to ensure transparency. In addition, regulation varies significantly from one country to another. We should notice that there is no unified disclosure code. This poses new legal risk particularly for Islamic PE operating in conventional systems or conventional PE operating in Islamic countries. This explains why the average financing cost in Islamic banks is higher than in conventional ones.

Finally, Islamic PE funds cannot convert their shares into cash money because they must hold them for a fixed period of time (5 years in average). They can sign a diminishing Musharaka contract which is standard Musharaka contract but that enables them to sell gradually their shares to the entrepreneur: the money invested is therefore recovered and they have not to wait for the exit date to get their capital back.

Different structure of PE fund

In each Islamic PE fund, there is a shari’ah committee called the Shari’ah Supervision Board SSB to define and set the shari’ah policy of the fund. It consists of three (or five) scholars who are expert in Islamic Jurisprudence (Fiqh el Muamalat) and the financial law.

SSB interprets the Qur’an, the Sunna6 and the Hadith7 (the sources of Islamic laws) and relies on Ijma’8, Qiyas9 and Ijtihad10 when the previous sources do not provide clear answers on the compliance of some projects. The intuition is to facilitate future development and implementation of the Islamic judicial system (Pervez, 1990). It checks whether the projects selected by the GP are shari’ah compliant or not.

Some scholars argue that SSB and GP should be independent to avoid conflicts of interests. New elements could transform the project into harem one, e.g. R&D activities that could be used in weapon industry.

As consequence, Malaysia recommends the appointment of Shari’ah Compliance Officer SCO to supervise the financed targets and report irregularities to the SSB. In addition, SCO provides shari’ah expertise on documentation, structuring and investment instruments.

3.Challenges facing Islamic Private Equity

As would be expected in a young industry, a number of structural issues remain. Some challenges faced by the sector need to be overcome in order to reach its full potential.

The first defy concerns the cost of running funds. According to PricewaterhouseCoopers (2009), there are few relevant studies to date on the Islamic fund universe, but anecdotal evidence suggests that Shari’ah compliant funds add single-digit basis points to the cost of funds. The costs relate partially to the setting up and financing of Shari’ah boards. The best-known scholars can receive total compensation in the millions of dollars per year – a cost that the conventional fund industry does not have to bear. The screening process can also be expensive depending on the type of asset the fund invests in. In addition, the lack of scale in many funds magnifies the effect of costs.

The second challenge is related to the lack of sufficient experienced professionals who can execute properly Shari’ah compliant deals. In fact, in this industry, there is a lack of suitably qualified and experienced professionals who can advise on the establishment and successful operation of such funds. As the market develops and products expand, there will be increased demand for human resources, for people with key skills. At the same time, specific Islamic expertise – while still important – is likely to become subordinated to investing and business expertise as the sector matures.

Finally, this industry is facing a legal challenge. In fact, the organization and the working of the Islamic fund must be Shari’ah compliant. However, there are some restrictions in the form and the content of the legal documents to make them in accordance with the Shari’ah principles. For example, the guarantee of the exit price (thus ensuring the benefits and excluding the risks of losses) is contrary to the Shari’ah. One example is the guarantee used to fix the exit price and exclude the risks of losses. This is contrary to the Shari’ah. At the exit date, the value of the target company is given by the fair market value, in contrast with conventional PE where this value may be fixed at the date of signature of financial contracts.

Conclusion

Private equity is a lucrative industry not only for investors but also for the overall advancement and development of economic and innovative activity. Even though some financial instruments used in conventional private equity structures are not Shari’ah compliant, there are alternatives already available and used.

The challenges are considerable for this industry and the pace of change is appreciable. But the ride is likely to be exciting for those participating, and the rewards highly attractive.

About the authors

Mohamed Ali Chatti is at the Islamic Development Bank (IDB) as a financial analyst in the Treasury Department, Investment division.(Email : [email protected])

Ouidad Yousfi is at the University of Montpellier II and at MRM. (Email: [email protected].

Notes

1.GCC consists of Bahrain, Kuwait, Oman, Qatar, Saudi Arabia and the United Arab Emirates.

2.The Dow Jones Islamic Market Index was the first benchmark of investment performance for the global universe of Shari’ah compliant equities. Since the launch of this global index in 1999, the DJIM index has expanded to provide a wide variety benchmarks tracking Shari’ah-compliant securities including indexes for specific countries, regions, industries and market capitalization ranges.

3.The FTSE Global Islamic Index Series (GIIS) are equity benchmark indices designed to track the performance of leading publicly traded companies whose activities are consistent with Islamic Sharia law. In essence, it is an indicator of the performance of global stocks that are available to an Islamic investor.

4.Halal: strictly conform to the precepts of shari’ah.

5.It issues common stocks, convertible preferred stocks, and subordinated and convertible debt.

6.It is the second source of Islam faith, refers to the Prophet’s acts and words which are related to his practice of faith. It explains and transmits the Qur’an.

7.They refer to tradition or stories of the Prophet. In contrast with the Sunna which was practiced, the Hadith are records of what was practiced. They have become a controversy between Islamic groups since there are a number of interpretations of them.

8.It is the consensus of the Islamic community called Ummah, by which democracy makes its impact on the conduct of Islamic policy.

9.It is a deductive analogy by which a jurist applies to a new case a ruling made previously in similar cases.

10.It is independent judgment provided by scholars of Islamic laws for which clear principles and procedures are stipulated in the Qu’ran and Sunna.

References

Al-Rifai and Khan, (2000), « The Role of Venture Capital in Contemporary Islamic Finance”

Ba, (1996), “SMEs and Islamic financial institutions“, Synthesis of Berangere, DELATTE, ADA Dialogue Journal N°2.

Battini (2006), “Financing your business from creation to transmission by the Private equity“, Maxima Editor.

Chekir, (1992), “Introduction to Islamic financing techniques”, Published by the Islamic Research and Training Institute, Islamic Development Bank, Act of seminar No.37, p.56-71.

Demaria (2006), “Introduction to Private Equity”, Canadian bank Edition.

Ernst & Young, (2009), “The Islamic Funds and Investments report: Surviving and adapting in a downturn”.

Fenn G.W., N. Liang and S. Prowse (1995), “The economics of the private equity markets”, Federal Reserve edition, Washington DC. 20551, p 168-237.

Gierath, (2010), “Islamic Private Equity Funds”, Investing in the GCC Markets.

Mughal, (2007), “No Pain, No Gain: The State of the Industry in Light of an American Islamic Private Equity Transaction”, Chicago Journal of International Law Vol. 7 No. 2, p 469 – 494.

Kaplan and Strömberg, (2009), “Leveraged buyouts and private equity”, Journal of Economic Perspectives 23(1), 121-146.

Lachmann (1992), “The Seed Capital, a new form of venture capital”, Economica.

Wouters, P., (2009), « Islamic Private Equity Opportunities in the Middle East”, presentation at the « Islamic venture capital & private equity conference 2009 ».

Pervez, I.A. (1990), “Islamic finance”, Arab Law Quarterly, Vol. 5 No. 4, pp. 259-81.

PriceWaterHouseCoopers, (2009), “Shariah-compliant funds: A whole new world of investment”.

Wouters, P., (2008), “Islamic Private Equity Funds”, Islamic Finance News.

Yunis, (2006), “Growth of Private Equity Funds using Islamic Finance”, www.islamicfinancenews.com

Disclaimer: This article contains sponsored marketing content. It is intended for promotional purposes and should not be considered as an endorsement or recommendation by our website. Readers are encouraged to conduct their own research and exercise their own judgment before making any decisions based on the information provided in this article.

{kind=link}