The 2025 Shanghai Cooperation Organisation (SCO) summit in Tianjin, which brought together twenty-six heads of state, underscored the organization’s growing relevance amid intensifying geopolitical fragmentation. Dr Kalim Siddiqui argues that for many Global South countries, unsettled by US protectionism and coercive tariff policies, the SCO offers a strategic alternative to West and a platform for policy coordination, and collective action.

I. Introduction

The international system is undergoing a profound transformation marked by the decline of unipolarity and the rise of competing centres of power. At the heart of this shift is the Shanghai Cooperation Organization (SCO), a regional grouping that has evolved from a narrow security arrangement into a broad platform for political, economic, and strategic cooperation. At present, with 10 full members—including China, Russia, India, Pakistan, Iran, Kazakhstan, Kyrgyzstan, Tajikistan, Uzbekistan and Belarus—and a growing number of dialogue partners such as Saudi Arabia, Türkiye, and Qatar, the SCO represents a potential alternative to Western-led international organisations.

The SCO was established in 2001 by six founding members—China, Russia, Kazakhstan, Kyrgyzstan, Tajikistan, and Uzbekistan—with the primary goal of fostering security cooperation in Central Asia (Siddiqui, 2023). Over two decades, the organization has expanded its membership. Today, the SCO’s agenda spans security, economic development, energy cooperation, connectivity, and cultural exchange.

The 2025 Shanghai Cooperation Organisation summit in Tianjin, which convened a record twenty-six heads of state, demonstrated the organization’s significant growth amidst a period of global geopolitical fragmentation. For many Global South nations alarmed by rising US protectionism and coercive tariff policies, the SCO is increasingly seen as a strategic alternative to Western-dominated institutions. It offers a crucial platform for non-Western countries to align policies, advance mutual interests, and collectively project influence. This paper analyses the SCO’s rising prominence, its internal dynamics with member states, and its broader role in facilitating a multipolar world order.

At the recent SCO summit, Indian Prime Minister Narendra Modi held a meeting with Chinese President Xi Jinping, signalling a potential step toward the normalization of strained bilateral relations. This development must be situated within a broader global context increasingly characterized by geopolitical fragmentation. Although deep-seated challenges persist between India and China—including territorial disputes, strategic competition, and enduring trade imbalances—the SCO provides an institutionalized framework for dialogue and confidence-building among its member states. Such mechanisms are particularly significant in a period marked by heightened instability in the global economy. The continuation of tariff-based trade policies, initiated under former US President Donald Trump, has disproportionately affected India, reinforcing the importance of diversifying multilateral engagement.

India’s active participation in platforms such as BRICS, the Russia–India–China trilateral, and the SCO reflects a deliberate effort to expand its strategic partnerships while mitigating the risks of great-power rivalry. These interactions not only strengthen India’s regional influence but also enhance its role in shaping global governance structures (Siddiqui, 2016).

In this context, India faces the responsibility of demonstrating leadership among developing countries. By advancing the principles of collective strength, multipolarity, and the democratization of international institutions, India can contribute to the construction of a more balanced and representative global order.

For India, participation in the SCO reflects both opportunity and challenge. Situated between the competing influences of China, Russia, and the United States (US), India trying to navigate a complex web of economic dependencies and strategic rivalries. India also faces domestic economic pressures and mounting US trade restrictions, including high tariffs. Diversifying trade with China, while cautiously managing security concerns, may help India reduce external vulnerabilities and strengthen its economic resilience.

The SCO has become an indispensable component of India’s foreign policy strategy, particularly in the context of managing its complex relations with China and Russia. While challenges remain, India’s continued participation in the SCO reflects both pragmatic considerations and its aspiration to shape the contours of a multipolar world order. The organization’s future trajectory will depend on how its members reconcile divergent interests, but it is already clear that the SCO represents a significant arena in which India seeks to project influence and safeguard its long-term strategic interests (Bajpayee and Jie, 2025).

Furthermore, the SCO presents opportunities for India to deepen ties with the Global South and position itself as a bridge between Asia and other developing regions. By leveraging SCO mechanisms, India may enhance regional connectivity projects, promote economic integration, and build coalitions around issues such as climate change, energy security, and equitable development.

The SCO summit brought together some of the strongest emerging economies, including India and Russia, which, along with China, account for more than one-fifth of the world’s gross domestic product (GDP). Trilateral trade between China, India and Russia accounted for $452 bn in 2023, up from $351 bn in 2022.

II. Political and Economic Significance of the SCO Summit

The enlargement and diversification of the SCO underscores its growing geopolitical relevance. For post-colonial countries, participation in the organization offers an alternative platform outside Western-dominated institutions (Siddiqui, 2025a). For India, active engagement in the SCO allows it to advance its strategic autonomy, improve relations with China, and contribute to the construction of a more pluralistic global governance system (Bajpayee and Jie, 2025).

International politics is increasingly shaped by geopolitical fragmentation, India’s engagement with China and Russia acquires heightened significance. While global instability persists—exacerbated by factors such as US tariff policies under former President Donald Trump, which have particularly affected India—multilateral forums like BRICS and the SCO provide important avenues for dialogue and cooperation. As a major developing economy, India is called upon to demonstrate global responsibility, set an example for the Global South, and contribute to advancing the multiploidization of world politics and the democratization of international institutions.

The SCO summit brought together several of the world’s most significant emerging economies, most notably China, India, Russia, and Iran, which collectively account for more than one-fifth of global GDP. The economic interdependence of these countries is evident in trade statistics: trilateral trade among China, India, and Russia increased from US$ 351 bn in 2022 to US$ 452 bn in 2023, highlighting their deepening economic ties despite global disruptions (Aljazeera, 2025).

The improvement in Sino-Indian relations, their cooperation could potentially serve as a driving force in international politics. Such a development might also galvanize the Russia–India–China trilateral process, a format championed by Yevgeny Primakov in the late 1990s. Primakov envisioned a multipolar world order in which Eurasian powers would collaborate to balance Western dominance. Three decades later, the international correlation of forces has indeed shifted in directions broadly consistent with his vision (Siddiqui, 2023).

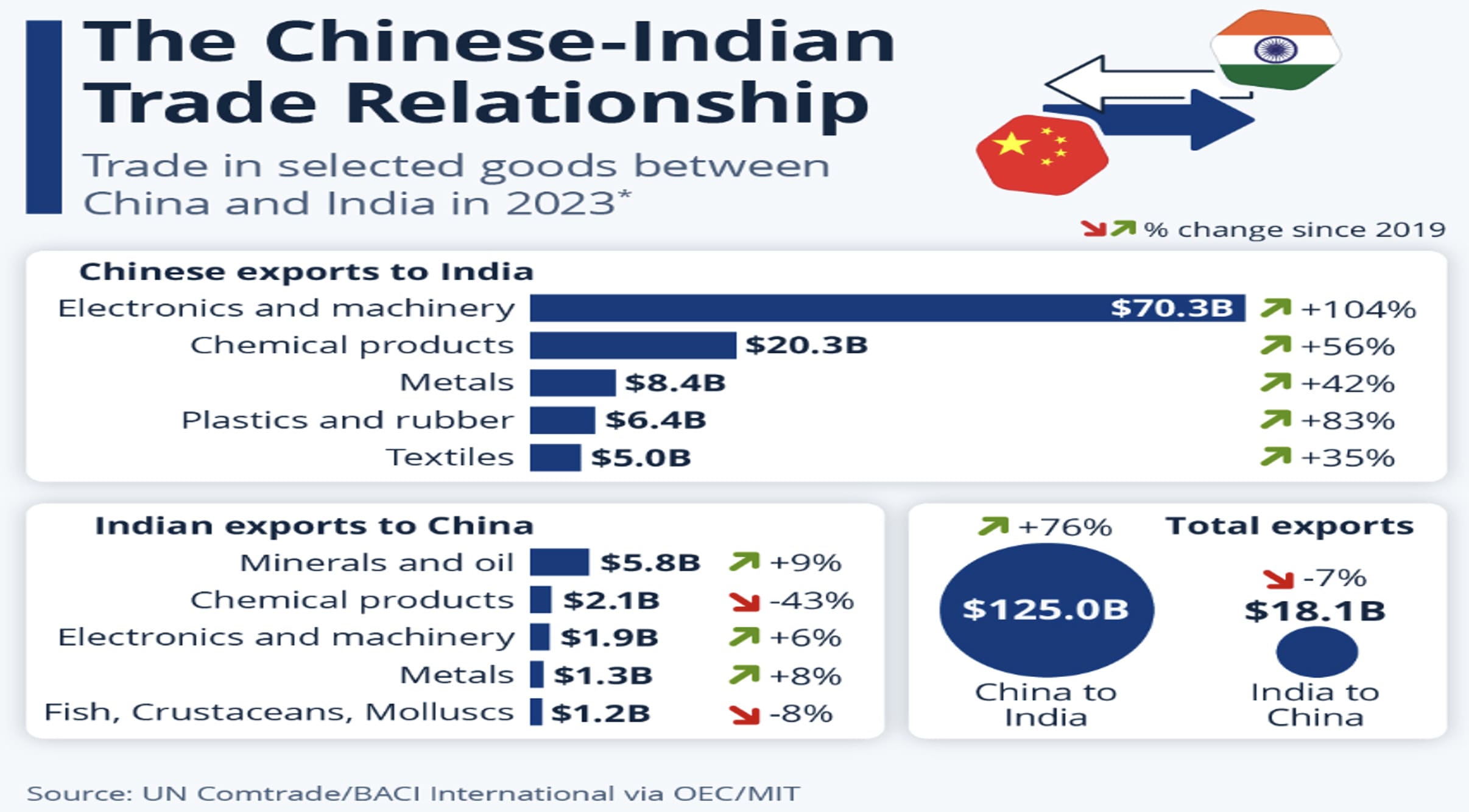

However, on economic front, India runs a substantial trade deficit with China, importing nearly seven times more goods than it exports. In 2023, China exported US$ 125 bn worth of goods to India, mainly machinery and chemical products, while India’s exports to China totalled only US$ 18.1 bn, largely consisting of oil and fuel products. Yet despite asymmetries, the relationship remains vital: India depends on Chinese investments, technologies, and raw materials to sustain its manufacturing and export sectors. India runs a major trade deficit with Russia, importing far more than it exports. In 2023, Russia sold $66.1 bn worth of goods to India, with energy products – primarily crude oil and natural gas – making up about 88 percent of these imports, much of which India buys at a discounted rate.

China is the largest Russia’s trading partner, accounting for 14.6 percent ($72.1bn) of Russian exports in 2021, Russia also had a broad range of European partners. The Netherlands was Russia’s second-largest partner, with 8 percent ($39.5bn) of total exports, followed by the US at 5.5 percent ($27.3bn) in 2021.

Before the Ukraine conflict, Russia maintained a diverse set of trading partners. In 2021, China was Russia’s largest trading partner, absorbing 14.6 percent (US$ 72.1bn) of Russian exports. The Netherlands (8 percent, US$ 39.5bn) and the US (5.5 percent, US$ 27.3bn) also figured prominently.

However, following Russia’s invasion of Ukraine in February 2022, sweeping Western sanctions forced Russia to reorient its trade. By 2023, the bulk of Russian exports shifted decisively toward Asia. China accounted for one-third (US$ 129 bn) of Russia’s exports, while India absorbed 16.8 percent (US$ 66.1bn) and Türkiye 7.9 percent (US$ 31bn). Together, Asian markets consumed more than three-quarters of Russia’s total exports. In 2023, China exported $110bn worth of goods to Russia, led by machinery and transport equipment. The top export items from China to Russia were cars. That same year, Russia sold $129bn worth of goods to China – mostly mineral products, including oil and natural gas. Russia has run a trade surplus with China, mostly due to energy products, which make up nearly three-quarters of its exports (Aljazeera, 2025).

The SCO has increasingly become a critical platform where shifting economic alignments between India, China, and Russia are negotiated against the backdrop of global instability. The redirection of Russia’s trade toward Asia highlights the deepening interdependence within the SCO space, while India’s engagement demonstrates both opportunities and constraints. As India seeks to balance its relations with Russia and China, its active role in the SCO will be central to advancing a vision of a more multipolar and democratized global order.

India continues to experience a significant trade imbalance with China, importing nearly seven times more goods (by value) than it exports. In 2023, China exported US$ 125bn worth of goods to India, dominated by machinery and chemical products. By contrast, India’s exports to China totalled only US$ 18.1bn, with oil and fuel-related products constituting the largest share (Aljazeera, 2025). This persistent deficit underscores both structural asymmetries in bilateral trade and the challenges India faces in diversifying and upgrading its export basket.

The US has expressed strong opposition to India’s purchase of discounted Russian oil, arguing that such transactions provide Russia with significant revenue to sustain its war in Ukraine. Beyond energy, US has also sought greater access to India’s agricultural sector, pressing for the entry of US agribusiness corporations, which could enable them to offload surplus production into Indian markets. At a strategic level, the US increasingly perceives India as a potential systemic challenger to American hegemony, complicating the bilateral relationship despite their growing defence and technological cooperation (Siddiqui, 2025b).

Despite the US pressure, India has deepened its energy and trade relations with Russia. By 2024, Russia accounted for approximately 37 percent of India’s total oil imports, highlighting Russia’s centrality to India’s energy security. Bilateral trade between the two countries reached a record US$ 68.7bn in the 2024–25 financial year, with Indian imports from Russia valued at around US$ 64 bn, compared to exports worth only US$ 5bn. The trade relationship remains heavily skewed in Russia’s favour, largely due to energy purchases, but both governments have articulated ambitions to expand bilateral trade to US$ 100 bn by 2030.

The SCO represents more than a regional forum; it embodies the aspirations of non-Western powers to shape a multipolar world order. For India, success will depend on reducing border tension with China and taking a clear stand to diversify its economy and building relations with China, Russia and other emerging economies to advance its long-term interests. As envisioned by prominent Russian diplomat Yevgeny Primakov, the shifting correlation of forces suggests that the world is indeed moving toward multipolarity, even if the path remains fraught with rivalry and uncertainty.

III. India, China, and US Power Politics: Interdependence and Strategic Rivalries

The Indian diaspora in the US, particularly the Gujarati business community, and the large number of Indian-origin CEOs leading major US corporations, highlight the depth of India–US economic linkages. Moreover, India’s IT sector is deeply integrated with US businesses and markets, while bilateral cooperation also extends to the nuclear sector (Siddiqui, 2025c).

At the same time, India’s manufacturing capacity is closely tied to Chinese investment and raw material supplies. Many of India’s export-oriented industries depend on Chinese inputs, technologies, and critical minerals, underscoring India’s economic dependence on China. This dual reliance on both the US and China complicates India’s foreign policy, especially in an era of heightened great-power rivalry.

India’s foreign policy choices are further complicated by internal divisions. A strong pro-American lobby exists within India, encompassing sections of the intelligentsia, the diaspora, and segments of the political and business elite. This camp champions a deepening strategic partnership with the US, often describing it as the defining relationship of the 21st century.

During the Trump administration, the tension between India and US became explicit. Peter Navarro, a senior adviser to President Trump, argued in the Financial Times that the US should not transfer “cutting-edge” military technologies to India as long as India appeared to be “cozying up” to Russia and China. Such statements underscore the limits of US trust in India’s strategic choices and highlight the ongoing challenge for India in pursuing multi-alignment without alienating major partners.

The US has adopted a strategy of containing China, viewing China’s rapid economic rise as a precursor to military strength and geopolitical influence. For much of the past quarter century, economic interdependence between major powers was seen as a pathway to shared prosperity. Indeed, both India and China benefited substantially from globalization over the last 25 years. However, China’s ascent has been far more dramatic, enabling it to emerge as the principal power in East Asia. Since 2017, the rise of Chinese economy and technology is seen by the US as challenger to its dominance in Asia.

Over the past three decades, China has achieved remarkable economic growth, enabling it to emerge as a regional power in East Asia with global ambitions (Siddiqui, 2024a). As China strengthens both its economic and military presence in the region, the US views this as a direct challenge to its long-standing hegemony. US’s approach toward China mirrors its earlier strategies of containing other rising powers. In this respect, China’s current trajectory parallels the US experience in the 19th century, when US asserted dominance over the Western Hemisphere through the Monroe Doctrine (Siddiqui, 2025a).

However, India’s relations with China remain clouded by negative perceptions and longstanding mistrust, which cannot be easily overcome. Despite increasing reliance on trade and investment cooperation with China, Indian domestic narratives often highlight China as a strategic rival, reinforcing scepticism toward closer engagement despite growing economic interdependence (Bajpayee and Jie, 2025).

The India–Pakistan military conflict has underscored the limitations of the SCO as a security platform. The organization has struggled to respond effectively to intra-member crises, revealing weaknesses in its flexibility and crisis management mechanisms. These shortcomings highlight the need for structural reforms and enhanced internal coordination. There is a need for resolving conflict between India and Pakistan because both are members of the SCO. And if it continues to be constrained by bilateral disputes, its geopolitical relevance risks further erosion in comparison to Western-led alliance systems, which maintain more cohesive structures and crisis-response capabilities.

Another conflict, namely the India–China border dispute, which has its origins in British colonialism, particularly the agreements and maps drawn by the British Raj in the early 20th century. The McMahon Line of 1914, intended to demarcate the boundary in the eastern sector, left several regions ambiguous, including Aksai Chin in the western sector. These colonial-era arrangements were insufficient for the needs of an independent India and have contributed to ongoing territorial disputes since Britain’s withdrawal.

The 2020 border clashes marked the most serious tensions in over four decades, placing the issue at the forefront of bilateral relations. De-escalation and stabilization along the border are now widely regarded as prerequisites for broader engagement, including economic and strategic cooperation. A breakthrough in resolving the border dispute could transform regional dynamics in Asia, reduce decades of hostility, and potentially diminish US influence over India in regional affairs.

Despite recurring challenges, particularly over the disputed Himalayan border, India and China have simultaneously cultivated growing economic and trade ties. In recent years, both countries have recalibrated their approaches to bilateral engagement, aiming to stabilize the border while enhancing commercial collaboration (Xue and Balazs, 2025).

IV. Economic Ties Between India and China

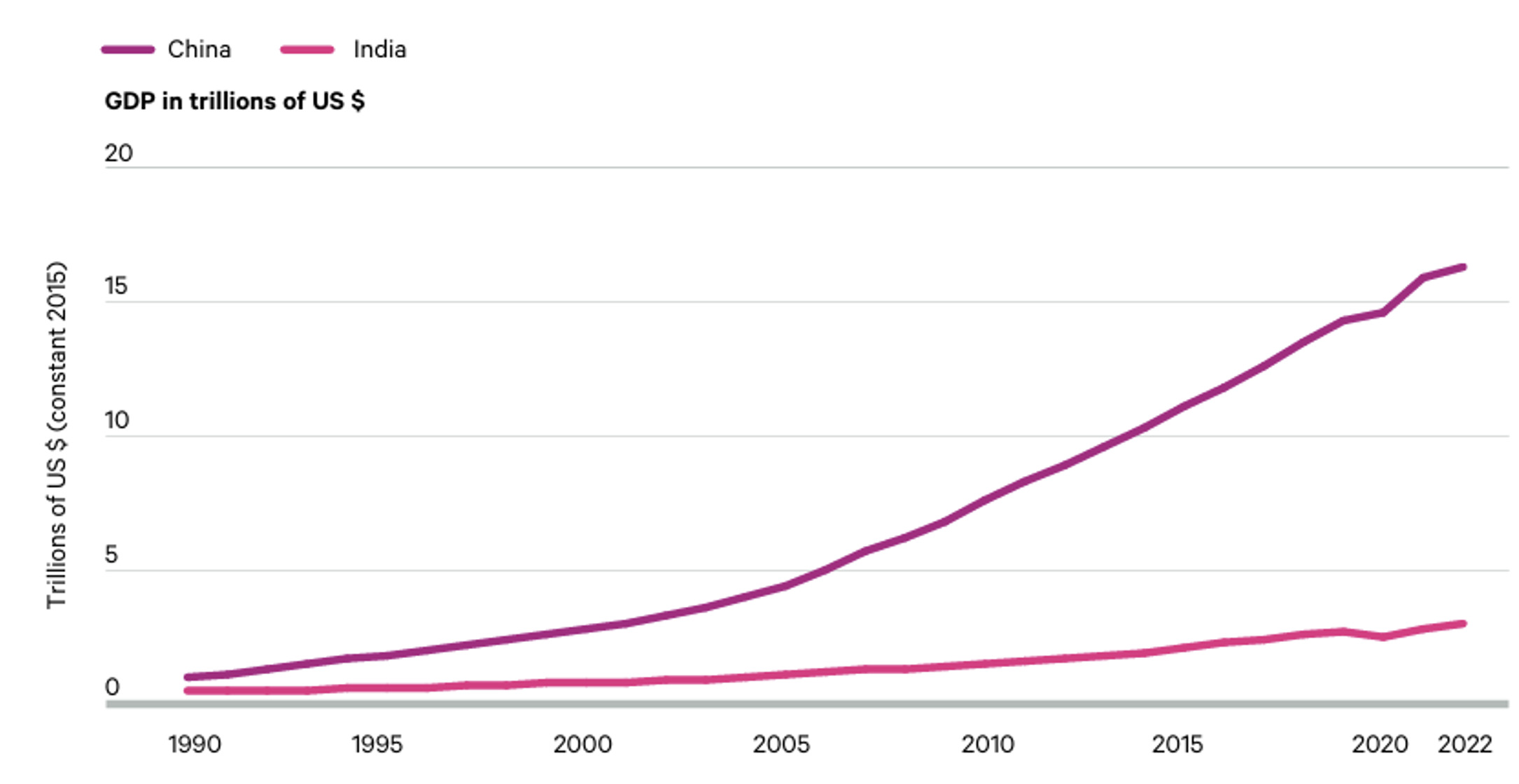

China’s economy is nearly six times larger than India’s in terms of GDP in 2023 (see Figure 1) (Siddiqui, 2020). In addition, China has become a leading global supplier of critical raw materials with high economic importance in the 21st century. These include rare earth elements, lithium, cobalt, copper, gallium, germanium, natural graphite, silicon, and platinum. Such minerals are indispensable for the green and digital transitions, powering technologies like electric vehicles, solar panels, wind turbines, and advanced electronics. They are, therefore, central to future economic competitiveness and strategic autonomy. Against this backdrop, Chinese cooperation is vital not only to strengthen India’s manufacturing capacity—through the supply of raw materials, technology, and capital investment—but also to expand its export sector (Xue and Balazs, 2025).

Figure 1: The Growth of Gross Domestic Production of China and India, 1990-2022 (US$ trillions)

India’s growing manufacturing sector presents opportunities for economic convergence with China. As the two most populous economies in the world, enhanced collaboration in trade, investment, and industrial development could generate mutual benefits. India has the potential to attract manufacturing transfers, which may complement or, in some sectors, compete with Chinese exports. Strengthening communication and cooperation between the two countries could therefore drive regional economic growth and foster stability while balancing broader geopolitical pressures (Siddiqui, 2024d).

The significant decline in foreign direct investment (FDI) inflows from China to India is largely attributable to India’s revised FDI policy for countries sharing land borders, implemented in response to the Sino-Indian border tensions of 2020. Despite this, Chinese investment in India continues to focus on strategic sectors such as electronics (smartphones, telecom equipment), household appliances, power equipment, steel, engineering machinery, and e-commerce. Prominent investors include Xiaomi, VIVO, OPPO, Huawei, Haier, Shanghai Automotive, Sany Heavy Industry, and TBEA.

Conversely, Indian investment in China has also declined, with FDI totalling US$ 6.32 million in 2021, representing a 47.4 percent year-on-year decrease. Nevertheless, Indian companies have increasingly established operations in China across diverse sectors, including pharmaceuticals, manufacturing, IT services, and trade, specifically on manufacturing industries, such as pharmaceuticals, auto components, and renewable energy (wind power).

FDI flows between the two countries have fluctuated due to geopolitical tensions, yet both governments continue to explore joint ventures in emerging sectors, including electric vehicles (EVs) and telecommunications. China remains a critical supplier of industrial goods to India, while India seeks to attract Chinese firms to establish local production facilities.

This pattern of investment reflects both economic pragmatism and a shared understanding that stable economic relations are essential for broader political and strategic stability, particularly amid the complex security and geopolitical environment in Asia.

This reliance persists even as India restricts Chinese investment in sensitive sectors and bans several Chinese-owned apps, including TikTok and WeChat. The reality is that India’s ambitions to become a global manufacturing hub cannot be achieved without Chinese components and raw materials. As the Economic Survey 2023–24 cautions, “it may not be the most prudent approach to think that India can take up the slack from China vacating certain spaces in manufacturing.” Instead, the report argues, India’s integration into global supply chains is contingent on its integration into China’s supply chain.

Despite political frictions, China remains India’s leading trading partner. The trade data highlights a widening imbalance: Chinese exports to India exceeded US$100 bn, while Indian exports to China totalled just over US$15 bn in 2022. In strategically significant sectors—such as pharmaceuticals and renewable energy—India’s dependence is especially pronounced. More than 40 percent of India’s pharmaceutical imports originate in China, and India’s largest supplier of generic drugs to the US relies on China for over half of its active pharmaceutical ingredients (Bajpayee and Jie, 2025).

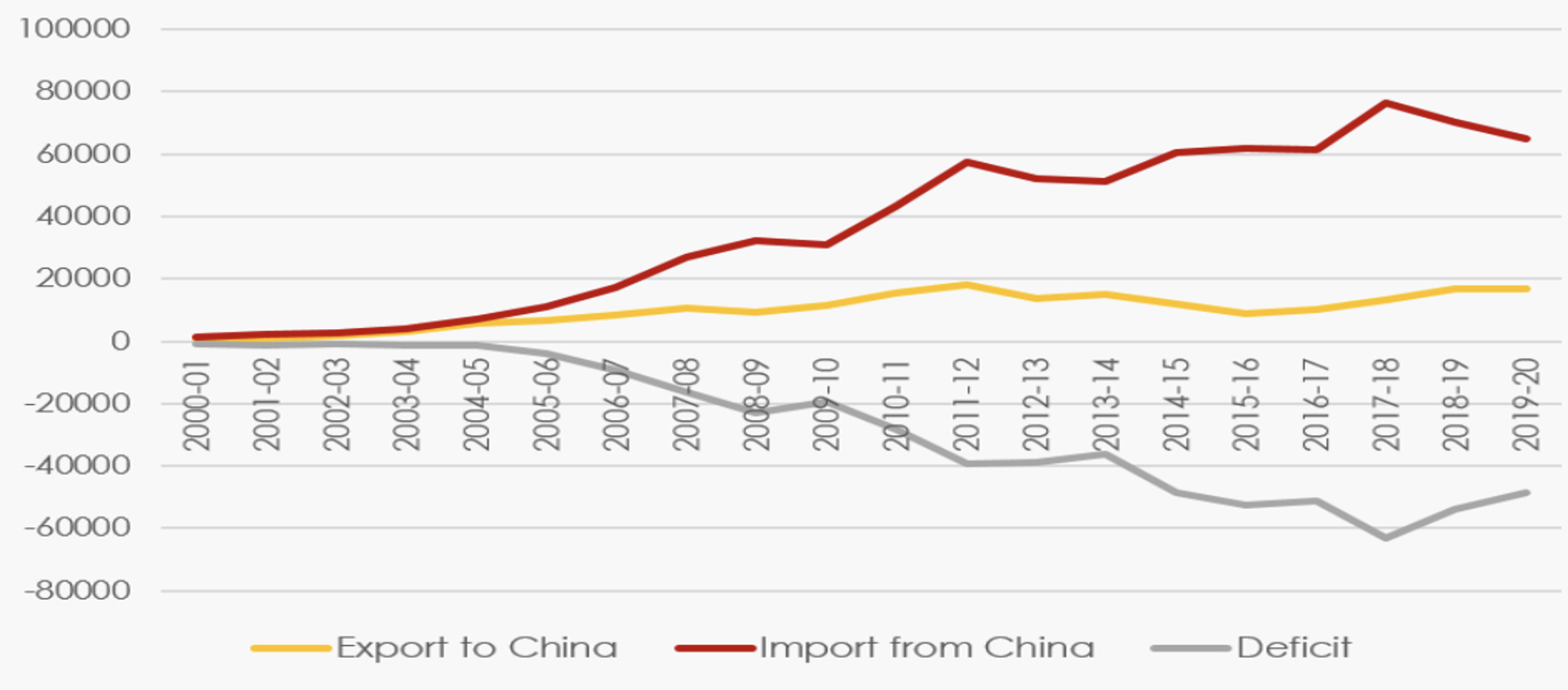

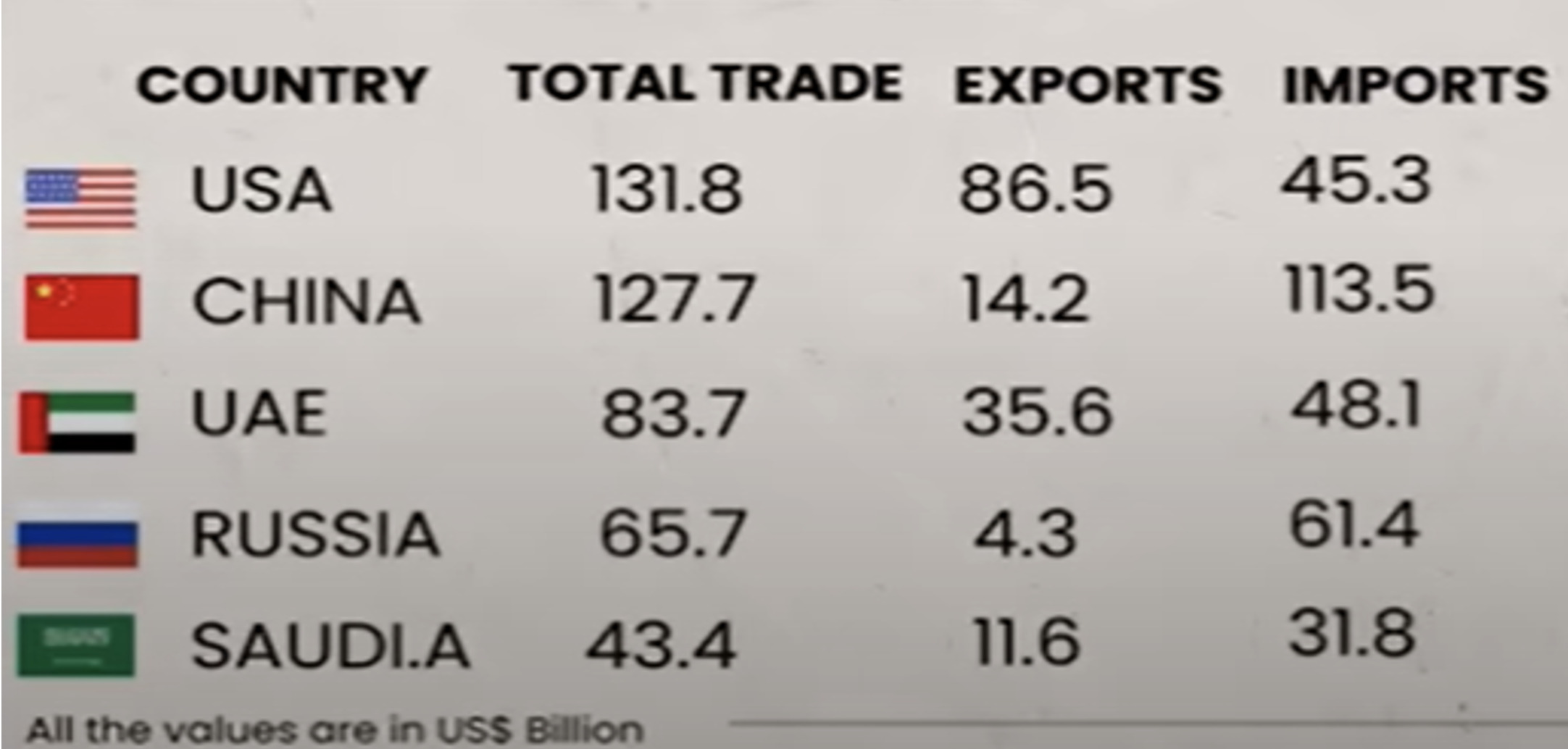

Trade has long functioned as a stabilizing factor in India-China relations, even amid political frictions. In 2024, bilateral trade reached US$ $118.4 bn, with India importing $101.7 bn worth of goods while exporting only $16.67 bn (See Figure 2). However, despite border disputes and trade between India and China has steadily grown over the years (as illustrated in Figure 3). China is second among the top trading countries for India (as shown in Table 1) and also China is the key supplier of critical raw materials for India’s manufacturing.

This stark asymmetry underscores both the depth of India’s dependence on Chinese supply chains and China’s centrality to India’s economic calculations. Rare earth elements provide another critical layer of interdependence. While India possesses domestic reserves, it lacks advanced processing capabilities, leaving it strategically vulnerable to China’s dominance in global rare earth supply chains—essential for electronics, renewable energy, and defence applications.

Figure 2: The Chinese-Indian Trade Relationship in 2023.

Figure 3: India’s Trade with China, 2000-2020 (US$ Million).

Table 1: Top Five Trade Partners of India, 2024-25 (US$ bn)

V. US Hegemony and Strategic Objectives

For centuries, Europe and North America controlled the bulk of global resources and technological innovation while dictating political and economic terms to the rest of the world. Today, that asymmetry is diminishing. Rising powers such as China, India, Russia, Indonesia, and South Africa—propelled by rapid growth, expanding higher education, and technological development—are altering the global balance of power, as underscored by the recent SCO summit. These dynamics point to the emergence of a genuinely multipolar order (Siddiqui, 2020b).

The Monroe Doctrine of the 1820s exemplified this long-standing ambition by asserting US dominance in Latin America and excluding European interference. In the 20th and 21st centuries, this logic has extended globally. Whether in Europe, Asia, or the Middle East, US strategy has consistently aimed to prevent the rise of peer competitors, ensuring that US remains the world’s preeminent military and economic power. The US relies not only on military superiority but also on preventing peripheral nations from challenging its position, compelling smaller states either to align with it or remain too weak to act independently. More broadly, the West maintains its influence through enduring notions of superiority (Siddiqui, 2025b)

The underlying driver of US foreign policy is a determination to maintain global primacy; a posture historically aimed at ensuring no rival power can challenge its dominance. This hegemony has its roots in a world order where the West (Global North), representing just 14% of the global population, controlled the remaining 86% residing in what is now the Global South. Despite significant post-independence strides in economic development, education, and living standards across these former colonies, the US has consistently acted to preserve its superior position. Since establishing regional hegemony in the Western Hemisphere and emerging as a global power around 1914, it has played a decisive role in containing successive rivals, from Imperial Germany and Japan to the Soviet Union (Tooze, 2018; Siddiqui, 2025a).

For instance, history illustrates that weak states are often vulnerable to external exploitation. China’s experience between the 1840s and 1940s, widely referred to as the “century of humiliation”, exemplifies this reality. During this period, China’s weakness left it unable to resist invasions by Britain, France, Japan, and other European powers.

A more recent example is Russia in the post–Cold War era. Following the collapse of Soviet Union, the US pursued NATO expansion despite Russia’s opposition. Under President Bill Clinton, NATO admitted the Czech Republic and Hungary in 1999, followed by the Baltic states in 2004. At the time, Russia was economically fragile, dependent on IMF and World Bank bailouts, as well as foreign investment (Siddiqui, 2012). Lacking economic strength, it was unable to prevent NATO enlargement. Only in the past 16–18 years has Russia stabilized its economy, regained strength, and reasserted itself internationally.

The US, long the principal beneficiary of free-trade globalization, now appears to be retreating from it. US increasingly employs tariffs and economic coercion as tools of statecraft, using its market power to extract political concessions and higher prices from its partners. This shift undermines the liberal economic principles the US once championed, while silence or acquiescence from other states risks normalizing such practices and reinforcing perceptions of US economic unilateralism (Siddiqui, 2022).

The Western-led international order is undergoing a profound transformation. The period in which Western powers exercised near-total dominance over global resources, institutions, and norms is drawing to a close. Former colonial states are now significantly more educated, technologically capable, and industrially advanced than in previous decades. Many have moved up global value chains, producing and exporting high-value goods once monopolized by the West. Many have acquired nuclear technology and have world’s highest economic growth rates and rising incomes. This shift marks the gradual erosion of an order that began with Columbus’s arrival in the Caribbean in 1492, expanded through centuries of European colonialism, and was consolidated by the rise of the US as the leader of the Western bloc after World War I.

The China–US relationship is often described as the defining geopolitical rivalry of the 21st century. Yet the trajectory of China–India relations may hold even greater long-term significance. Together, these two Asian giants account for 40 percent of the world’s population and are home to the world’s second-largest and soon-to-be third-largest economies. Their interactions will not only shape Asia’s strategic environment but also exert a profound influence on global governance, trade, and security (Siddiqui, 2021a).

For the West—particularly the US, which often views India primarily as a counterbalance to China—it is essential to recognize both the scope and the limits of the India–China relationship. China remains India’s largest trading partner, and economic realities constrain how far India can align against China. More realistic expectations of India’s strategic choices are therefore necessary if US and its allies wish to sustain meaningful cooperation without demanding commitments that run counter to India’s core national interests.

Despite Western criticism of India’s neutral stance on the Russia-Ukraine war, India has preserved its long-standing partnership with Russia. This relationship is grounded in defence cooperation, energy security, and a shared interest in counterbalancing China’s regional dominance. Even as protectionist pressures from US threaten to destabilize the Indo-US partnership, India has refused to compromise its ties with Russia. As institutions like the SCO and BRICS expand to incorporate more China-friendly states, India views its Russia connection as a vital counterweight—an internal balancing mechanism to mitigate China’s growing influence within these forums.

Moreover, China and India share certain broad similarities. Both aspire to promote a more multipolar international order that dilutes Western dominance. However, India’s vision is not explicitly anti-Western, but rather rooted in its pursuit of strategic autonomy and greater recognition within global institutions. This distinction is significant: it provides the US and its allies with an opportunity to engage India constructively and prevent forums such as BRICS from evolving into overtly China-led, anti-Western platforms (Siddiqui, 2024b)

VI. US, India and Independent Policy

US policy toward India increasingly reflects a pattern of coercion consistent with its broader imperial posture. Historically, US sought to draw newly independent India in the 1950s into its Cold War alliance structures such as SEATO and CENTO. India’s refusal to join and its pursuit of non-alignment, national planning, self-reliance, and the development of a state-led industrial base instead aligned with Soviet Union. Soviet Union’s (now Russia) assistance in building India’s heavy industries (Siddiqui, 2021b) and public sector laid much of the foundation for India’s early industrialisation and economic sovereignty (Siddiqui, 2018).

From the 1980s onward, however, the global ascendancy of neoliberal economic policies—promoted by US-backed financial institutions—reshaped India’s economic orientation (Siddiqui, 2025c). And in 1991, India accepted neoliberal policies in return for IMF loans. India accepted privatisation of public companies, removal of tariffs on imports, and trade and investment liberalisation. The dominance of global finance capital marked a shift away from the earlier state-led developmentalist model toward more reliance on foreign capital and markets, and deeper integration into Western-led globalization (Siddiqui, 2025d).

When neoliberal reforms were introduced in India in the early 1990s, the rationale was that globalization represented a permanent new order: capital would become globally mobile, and low-wage countries of the Global South would emerge as the primary destinations for industries once housed in the Global North. This relocation, it was argued, would alleviate poverty and underdevelopment in the Global South. Yet neoliberal globalization created new vulnerabilities. Once an economy becomes heavily trade-dependent, any disruption in external markets can inflict significant damage. Unless a country is prepared to fundamentally restructure its economic regime, it risks compromising its sovereignty whenever US pressure is applied.

In India’s case, such restructuring faces formidable resistance. The domestic beneficiaries of neoliberalism—the big bourgeoisie and the urban upper middle class—have profited substantially from the existing order and would oppose a shift toward greater economic autonomy.

Today, under Donald Trump’s second term, US economic coercion has intensified. Tariffs are increasingly deployed as instruments of pressure. US’s imposition of a 25 percent tariff on Indian exports to the US, coupled with the threat of additional penalties over India’s continued oil purchases from Russia despite Western sanctions, illustrates this dynamic. The recent announcement of a 50 percent tariff on Indian goods further compounds the strain on India’s economy.

The Trump administration’s imposition of 50 percent tariffs on Indian exports, ostensibly in response to India’s continued purchase of Russian energy, underscores the asymmetries of contemporary trade politics. China, by far the largest buyer of Russian energy, faces considerably lower tariff rates on most exports, revealing that such measures are less about principle than power. The US calibrates coercion according to perceived vulnerability: China possesses credible retaliatory capacity—notably in rare earth exports—while India has neither threatened nor mobilised equivalent countermeasures. Brazil, the only other country subjected to the 50 percent tariff, has at least initiated retaliation, further highlighting India’s relative passivity.

This weaponisation of tariffs signals an imperialist turn in trade policy, where economic instruments are redeployed as tools of geopolitical dominance. Post-colonial states of the Global South once sought to secure autonomy through dirigiste strategies that prioritised self-reliance, domestic market expansion, and state-led industrialisation. The new tariff regime undermines such strategies by constraining policy space, reinforcing dependency, and entrenching asymmetries in the global order. In this sense, trade sanctions are not simply commercial measures but disciplinary mechanisms that reassert imperial hierarchies within international political economy (Siddiqui, 2025b).

Against this backdrop, Prime Minister Modi’s decision to attend the SCO summit underscores India’s search for alternatives. By engaging with China, Russia, and other regional partners, India signals its desire to resist unilateral US pressure and to promote a regional order oriented toward peace, development, and multipolarity in Asia.

Russian oil remains the cheapest option available to India. Pressuring India to halt imports therefore amounts to demanding that it act against its own economic interests. Crucially, the sanctions imposed on Russia are not UN-mandated, unlike those once enforced against apartheid South Africa. Instead, they are unilateral measures initiated by the US and other Western powers against countries—such as Russia, Cuba, Iran, and Venezuela—that resist their dictates. Forcing states to comply with such sanctions effectively compels them to act against both their sovereignty and their self-interest.

Trump’s tariff threats already illustrate these vulnerabilities. The Indian rupee has weakened under the pressure of higher tariffs, and further depreciation is likely as these measures intensify. Without decisive interventions—such as the imposition of capital controls and selective trade restrictions—India’s foreign exchange position will deteriorate. Such measures would mark a retreat from the neoliberal framework and the gradual emergence of an alternative economic regime more insulated from external coercion.

China has broadly followed the classic pattern of economic growth and structural transformation: moving from agriculture to manufacturing and, more recently, to services. India, by contrast, has followed what many analysts describe as a “peculiar” trajectory, one not replicated in other major economies. While the share of agriculture in total output has steadily declined, the sector’s employment levels have remained largely unchanged. Manufacturing, which in most development pathways absorbs surplus agricultural labour, has failed to expand sufficiently to provide large-scale employment. As a result, much of India’s workforce remains trapped in low-productivity agricultural activities (Siddiqui, 2024c).

This stalled diversification underlies many of India’s broader socioeconomic challenges. To put it starkly, if workers cannot transition into higher-productivity sectors, aggregate welfare will remain constrained regardless of headline GDP growth. Even under India’s relatively expansive definition of formal employment—any job with a contract, paid leave, or social security—the share of the workforce in such employment is only around 4 percent. This underscores both the persistence of informality and the limits of India’s growth model to deliver broad-based, secure employment.

Beyond economics, both China and India articulate visions of a more multipolar world order rooted in Global South solidarity. Yet they pursue these aspirations in markedly different ways. India emphasizes its democratic credentials and seeks to project a benign, non-Western—but not anti-Western—alternative within global institutions. By contrast, China leverages its financial resources and state-led initiatives to reshape existing governance structures according to its preferences.

VII. Conclusion

India’s participation in the SCO should thus be viewed as a deliberate strategy of strategic balancing. Despite recent high tariffs imposed by the Trump administration, the US remains one of India’s largest trading partners (Siddiqui, 2025e). India now faces a critical juncture, forced to choose between acquiescing to US pressure and actively diversifying its economic ties by deepening cooperation with Asian and European partners, particularly within the SCO. While China remains a structural rival, it is also an indispensable economic partner. By engaging with China-led multilateral institutions like the SCO and BRICS, India signals a pragmatic and ambitious foreign policy: it seeks the economic benefits of cooperation while steadfastly protecting its strategic autonomy.

The SCO provides India with a broader platform to project its vision of a multipolar order, strengthen its ties with the Global South, and reinforce its role as a credible alternative to Western dominance. India is seeking to position itself as both a defender of multipolarity and an advocate of regional engagement. Prime Minister Modi’s participation in the SCO, coupled with India’s willingness to recalibrate its relationship with China despite unresolved border disputes, reflects a strategic commitment to avoid entrapment in any single geopolitical camp. Re-engagement with China demonstrates India’s insistence on preserving strategic autonomy in the face of intensifying great-power competition.

India has long term very close economic cooperation with Russia and it has deepened over time. However, for India, China’s growing influence, from the Belt and Road Initiative to its expanding influence in South Asia and the Indo-Pacific (Siddiqui, 2019). By maintaining dialogue and engagement, India seeks to safeguard its long-term economic interests while managing geopolitical competition. This approach underscores India’s role as a pivotal power—one capable of bridging geopolitical divides and shaping the contours of an emerging multipolar order.

India’s relationship with China remains profoundly shaped by economic interdependence, particularly in trade, rare earth elements, and technology. Despite persistent security tensions, India has avoided complete disengagement from Chinese capital and technology. Instead, it has pursued a dual-track strategy: erecting firewalls around sensitive sectors such as telecommunications and defence while permitting cooperation in areas of mutual economic benefit. This calibrated approach aligns with India’s broader vision of pursuing autonomous yet interconnected growth. Ironically, the protectionist policies of former US President Donald Trump—especially tariff escalation—have nudged India and China into a pragmatic, if uneasy, alignment on certain economic issues.

The security dimension, however, remains deeply contested. The long-standing territorial dispute between the two countries has repeatedly strained ties. The violent clashes along the border in June 2020 underscored the fragility of bilateral trust. The October 2024 border agreement represents an important attempt to establish “guardrails” for managing disputes and reducing the risk of escalation, but it does not eliminate the structural rivalry between the two powers.

In short, economic interdependence among Shanghai Cooperation Organisation (SCO) members is poised to deepen. This trend holds significant benefits for India, which remains heavily reliant on China for critical components and raw materials vital to its industrial sectors—particularly pharmaceuticals, electronics, and renewable energy. Despite India’s efforts to diversify its supply chains, China continues to occupy a central role in its economic ecosystem. This dependency adds a layer of complexity to India’s strategic calculus, necessitating a balance between cooperation and geopolitical competition.

Furthermore, the economic growth of China, India, and Russia has consistently surpassed the average GDP growth of Western economies. This disparity in growth rates is projected to continue, heralding a decline in the five-century-long domination of the global economy and politics by the West. We are witnessing a seismic shift towards a multipolar world order—a development that is both inevitable and welcome.

About the Author

Dr. Kalim Siddiqui is an economist specializing in International Political Economy, Development Economics, Trade and Economic Policy. Since 1989, he has been teaching economics at various universities in Norway and the UK. Dr. Siddiqui’s research interests encompass a wide range of topics, including political economy, international trade, and economic history, South Asia, and emerging economies. He has presented papers at international conferences across numerous countries, reflecting his global engagement in the field. His scholarly pursuits span six broad domains: Political Economy, Development Economics, Economic History, Economic Policy, Globalization, and International Trade. Dr. Siddiqui has made significant contributions to research in areas such as trade policy, globalization, and political economy. His work has been published in chapters of edited books and articles published in peer-reviewed journals. For inquiries, Dr. Siddiqui can be reached at: [email protected]

Dr. Kalim Siddiqui is an economist specializing in International Political Economy, Development Economics, Trade and Economic Policy. Since 1989, he has been teaching economics at various universities in Norway and the UK. Dr. Siddiqui’s research interests encompass a wide range of topics, including political economy, international trade, and economic history, South Asia, and emerging economies. He has presented papers at international conferences across numerous countries, reflecting his global engagement in the field. His scholarly pursuits span six broad domains: Political Economy, Development Economics, Economic History, Economic Policy, Globalization, and International Trade. Dr. Siddiqui has made significant contributions to research in areas such as trade policy, globalization, and political economy. His work has been published in chapters of edited books and articles published in peer-reviewed journals. For inquiries, Dr. Siddiqui can be reached at: [email protected]

References

- Aljazeera. (2025) “How much do India, Russia, China trade and what goods do they buy?” September 3.

- Bajpayee, C. and Jie, Y. (2025) “How China–India relations will shape Asia and the global order”, Research Paper, April, London: Chatham House.

- Siddiqui, K. (2025a) “Decolonisation and Economic Sovereignty: The Bandung Conference and the Making of the Global South” World Financial Review, June.

- Siddiqui, K. (2025b) “Reconfiguring US Hegemony: Militarism, Empire, and the Crisis of Capitalist Accumulation” World Financial Review, August.

- Siddiqui, K. (2025c) “International Financial Institutions as Instruments of Western Hegemony Debt, Austerity, and Exploitation in the Global South” World Financial Review, August.

- Siddiqui, K., (2025d) “Indian Economy at 75: Transformation and Challenges” American Review of Political Economy19(1):6-28.

- Siddiqui, K. (2025e) “Donald Trump’s Tariffs: A Prelude to Global Trade Wars?” World Financial Review, April.

- Siddiqui, K. (2024a) “China’s Growth Miracle and Development Strategy Since the 1980s” World Financial Review,

- Siddiqui, K. (2024b) “The BRICS Expansion and the End of Western Economic and Geopolitical Dominance” World Financial Review, November.

- Siddiqui, K. (2024c) “Political Economy of Liberalisation of Agriculture in India” (Part 1 & Part 2) World Financial Review, August.

- Siddiqui, K. (2024d) “China’s Trade and Growing Economic Influence with East Asia”, World Financial Review, May.

- Siddiqui, K. (2023). “The Political Economy of Shanghai Cooperation Organisation (SCO) and the Growing Regional Multilateral Ties” World Financial Review, February/March.

- Siddiqui, K. (2022) “Capitalism, Imperialism, and Crisis” European Financial Review, June/July.

- Siddiqui, K. (2021a). “Can the 21st Century be an Asian Century?” Asian Profile, 49(1):1 – 19, March.

- Siddiqui, K. (2021b) “The Importance of Industrialisation in Developing Countries” World Financial Review, January/February.

- Siddiqui, K. (2020a). “A Comparative Political Economy of China and India: A Critical Review” (edit) Young-Chan Kim. China-India Relations: Geo-Political Competition, and Economic Cooperation,31-58, Springer.

- Siddiqui, K. (2020b) “Prospects of a Multipolar World and the Role of Emerging Economies” World Financial Review, November-December.

- Siddiqui, K. (2019). “One Belt and One Road, China’s Massive Infrastructure Project to Boost Trade and Economy: An Overview” International Critical Thought 9(2):214 – 235.

- Siddiqui, K. (2018). “The Political Economy of India’s Post-Planning Economic Reform: A Critical Review” World Review of Political Economy 9(2):235-264.

- Siddiqui, K. (2016). “Will the Growth of the BRICs Cause a Shift in the Global Balance of Economic Power in the 21st Century?” International Journal of Political Economy 45(4):315 – 338.

- Siddiqui, K. (2012). “Developing Countries’ Experience with Neoliberalism and Globalisation” Research in Applied Economics 4(4):2 – 37, December.

- Tooze, A. (2018) Crashed: How a Decade of Financial Crises Changed the World, London: Penguin.

- Xue, G. and Balazs, D. (2025) “Where India and China Meet: Competing Regional Statecraft in Southeast Asia” Political Science Quarterly, July.

.){kind=link}