The global agricultural landscape is witnessing a series of significant shifts that are reshaping export dynamics and supply chains. America’s abundant harvests are playing a crucial role in balancing the shortfall from the Black Sea region, effectively stabilising corn prices worldwide. However, geopolitical tensions are also exerting their influence, with Russia managing to capture a substantial market share in the wheat trade despite facing sanctions. On the weather front, erratic conditions, ranging from extreme weather events to droughts in key producing regions such as the US, Brazil, and Argentina, are casting a shadow over grain crop yields. Yet, challenges persist on the production cost front, with rising fertiliser prices impacting corn cultivation.

Extreme weather, fertilizer prices and geopolitics are significantly transforming the global agricultural commodity market. Edward Nikulin, weather model expert at Mind Money, explains how each of these factors affects the price of wheat and corn.

As Q3 2025 begins, global grain markets are supported by strong harvests in the EU, India, Brazil, and the U.S., offsetting losses from drought and war. As I mentioned in my Preface, Russia remains a key wheat exporter despite sanctions. Demand looks healthy, but prices stay subdued due to cautious buying and high input costs. As always, futures remain sensitive to weather and policy risks.

Wheat: Global Supply Recovering

Global wheat production is on track for a strong year in 2025, rebounding from last season’s weather-hit output. The International Grains Council now forecasts world wheat output at 808 million tonnes, up slightly from earlier estimates and at a record high. This optimism is underpinned by bumper harvests from several key producers. In the European Union, soft wheat production is projected around 128 million tonnes for 2025/26, a 15% surge from last year’s drought-affected crop. India is also contributing to global abundance with a record wheat harvest of roughly 115–117 million tonnes, thanks to higher plantings and favourable temperature conditions. Even Russia and Ukraine benefited from a mild winter and adequate spring moisture, setting the stage for another large Black Sea wheat crop. All in all, Russia’s wheat exports remain solid, with Russian cash wheat offered around $225/tonne, underscoring its competitive edge on the global market.

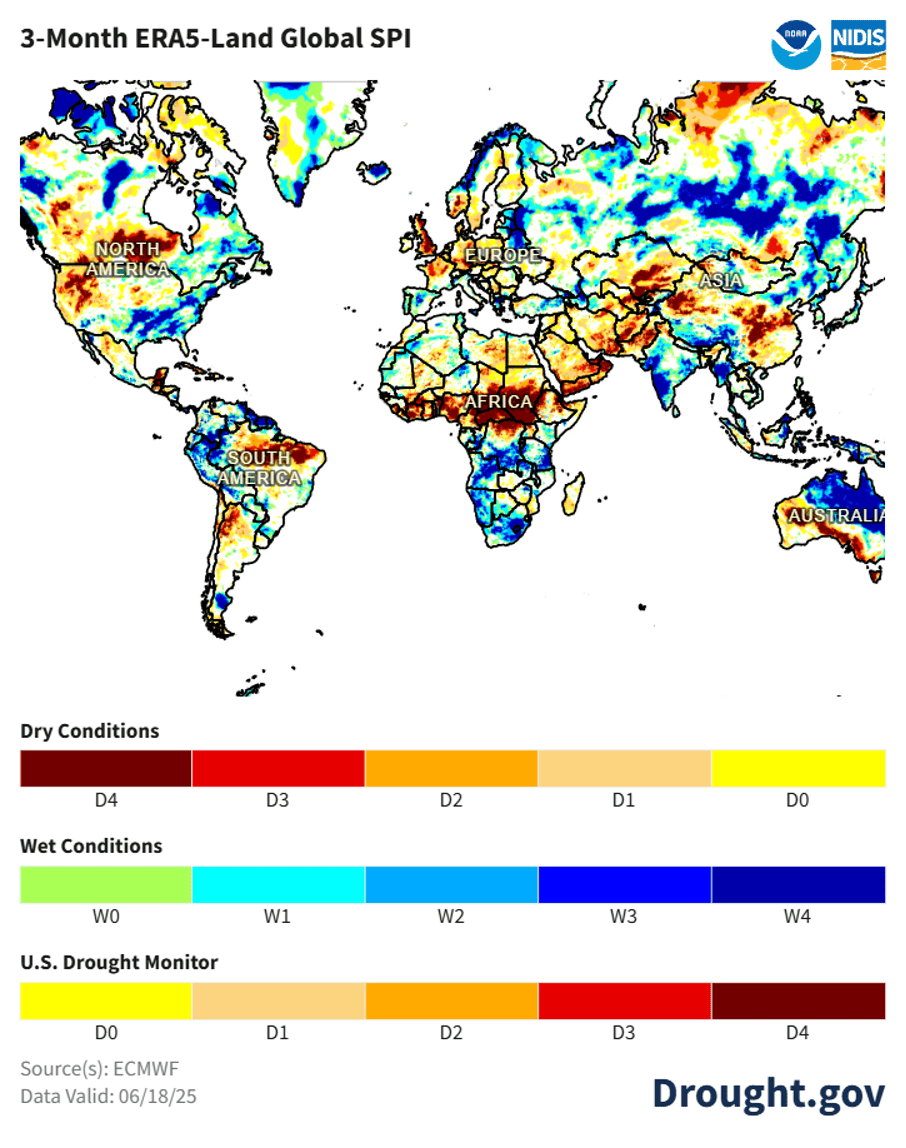

Not all grain producers experienced a smooth season, though. Thus, China’s wheat belt faced severe spring drought and heat, with some crops being halved. Though the 2025 output may be the lowest in seven years, strong irrigation and reserves could limit the impact. China’s imports remain muted. In India, the heat and dryness had a minimal impact on a record crop but highlighted the ongoing weather risks.

In the United States, the winter wheat harvest has experienced significant fluctuations in weather conditions. Early in the season, the Central and Southern Plains endured severe heat and drought, only to be drenched by heavy rains and floods in late May. In Kansas, Oklahoma and Texas – heartlands of Hard Red Winter wheat – downpours turned fields muddy and even caused localised flooding, delaying the harvest in many areas. Canada experienced improved moisture in June, which stabilised its wheat prospects, and farmers there expanded wheat acreage slightly. By late June, only about 20% of Kansas’s wheat had been harvested (versus nearly half by the same time last year) as farmers waited for fields to dry. Argentina is recovering from a drought-hit cycle last year; recent dry weather improved planting conditions, and the government extended reduced export taxes to encourage wheat sowing.

Wheat trade flows are shifting, as I mentioned above, with Russian exports remaining strong, supplying North Africa and the Middle East despite sanctions. At the same time, the Black Sea conflict limits Ukraine’s exports. Ample global supply and low prices benefit traditional importers, but China’s muted buying, due to large reserves, removes a key source of demand. Overall, global wheat demand is at record highs, although growth can be characterised as steady rather than rapid.

In June 2025, wheat futures prices experienced notable volatility, fluctuating between approximately $524 and $574 per bushel. The month began with relatively stable prices near $535, but by June 7–9, prices began to rise gradually amid concerns about adverse weather conditions in the U.S. Plains and parts of Europe. This upward trend accelerated sharply in mid-June, peaking around $574 per bushel on June 20. The rally was driven by mounting speculation and reports of excessive rainfall delaying the wheat harvest in southern U.S. states along with heat stress affecting crops in parts of Central Europe. From June 23 onward, wheat futures steadily declined, hitting a local low of about $520 per bushel by June 27. In the final days of the month, prices showed signs of stabilisation and modest recovery, closing at around $532.23 per bushel on July 1.

Corn: Big Harvests and Healthy Demand Growth

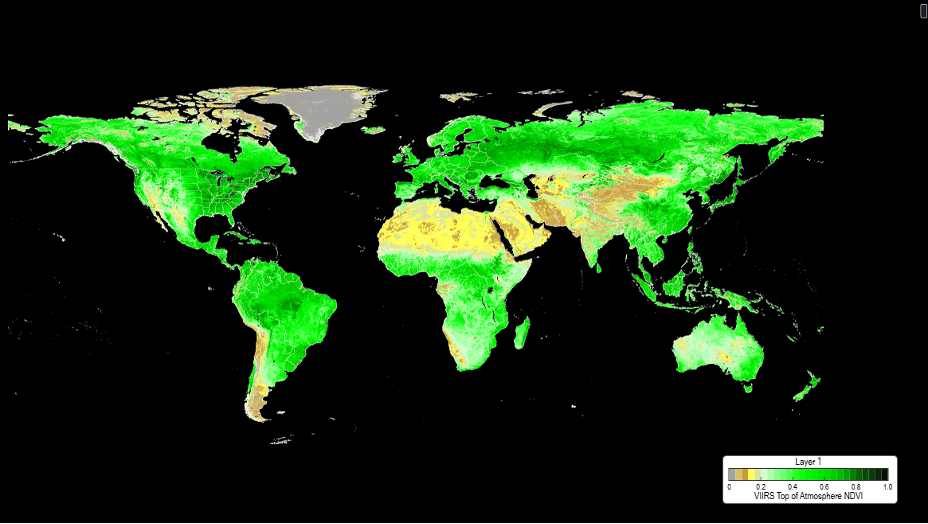

The corn market faces strong global production but ongoing weather risks. Brazil’s 2024/25 crop is set to hit a record 128–150 million tonnes, with good growing conditions despite late harvest delays. Argentina is recovering from last year’s drought, and U.S. output is also expected to be high, with 91 million acres planted and favorable early-season weather. NDVI data shows strong crop health in the U.S., Brazil, and Argentina. However, parts of Eastern Europe and Central Asia show weaker crop vigor, and dryness in the U.S. western Corn Belt remains a concern. July–August weather will be critical for final yields.

Strong global corn demand is keeping pace with rising production. U.S. exports have surged, led by buyers such as China and Mexico, which have tightened domestic stocks to around 1.8 billion bushels. Ethanol output is also supporting demand. Globally, corn use is growing for feed and industrial purposes. China may import more if domestic prices rise, while South Africa and India expect solid crops, which will boost local supply. The global supply-demand balance has improved, with major exporters rebuilding stocks.

In June 2025, corn futures prices trended steadily downward, reflecting strong global supply expectations and ongoing bearish sentiment in the market. The month began with prices near $449 per bushel, but after a brief spike, the market quickly began to retreat. Throughout the first half of the month, prices hovered between $435 and $445. Starting around June 20, prices began a sharper descent, driven by improving crop conditions in the U.S. Corn Belt and aggressive selling by speculative funds. By June 25, corn futures hit a monthly low near $410 per bushel. This decline was further exacerbated by fund positioning, as managed money held one of the largest net short positions in nearly a year. Toward the end of the month, the market attempted a modest recovery, briefly rising above $420, but gains were quickly capped, and the contract closed at $414.05 per bushel on July 1.

About the Author

Edward Nikulin, a weather model expert at Mind Money, is a proficient quantitative researcher and data scientist with more than 8 years of experience in market modeling, systematic trading, and AI-driven analytics. He is the author of the weather model for proprietary trading strategies of Mind Money.

Edward Nikulin, a weather model expert at Mind Money, is a proficient quantitative researcher and data scientist with more than 8 years of experience in market modeling, systematic trading, and AI-driven analytics. He is the author of the weather model for proprietary trading strategies of Mind Money.

{kind=link}