Introduction

The 16th BRICS Summit in Kazan, Russia, marks a pivotal moment for the group as it aims to make significant progress in cross-border payments, alternative payment systems, and dedollarization. Russia’s reliance on the US dollar for trade has shifted dramatically, with 90% of its trade with China now conducted in local currencies. This reflects a broader trend of dedollarization, a long-term strategy for BRICS, though challenges may arise from differing priorities between China and India. Despite these challenges, the group could find consensus on key global issues, such as the Palestinian conflict.

China has also made substantial investments in major infrastructure projects across Africa, strengthening its influence on the continent. This stands in contrast to the United States, which has offered no new development policies for Africa, instead promoting a neoliberal model focused on foreign capital and low-value goods exports.

Established in 2006 by Brazil, Russia, India, and China, with South Africa joining in 2010, BRICS was formed to foster economic cooperation and challenge the dominance of Western economies. In January 2024, the group invited several new members, including Egypt, Ethiopia, Iran, Saudi Arabia, and the UAE. With these additions, BRICS now represents 3.5 billion people—approximately 45% of the global population—and accounts for 28% of global GDP. Furthermore, with key oil suppliers like Russia, Iran, Saudi Arabia, and the UAE, BRICS controls 45% of the world’s crude oil production, solidifying its growing influence on the global stage.

Reshaping the Global Economic Landscape

The recent inclusion of nations such as Saudi Arabia, the UAE, and Iran into BRICS is transforming the global economic order and challenging the G7’s long-standing dominance. BRICS members are aiming to expand their economic and geopolitical influence by reforming international financial systems and reducing reliance on the US dollar. The group’s expansion not only strengthens its collective bargaining power but also signifies a shift in the global economic center of gravity towards the Global South. As BRICS now accounts for 45% of the world’s population, its economic and geostrategic importance will continue to rise.

BRICS membership has the potential to enhance regional cooperation among countries already involved in regional forums. (Siddiqui, 2023b) The numbers are telling: the Global North’s share of world GDP fell from 57.3% in 1993 to 40.6% in 2022. The US’s share of global GDP (measured by purchasing power parity, or PPP) also shrank, from 19.7% to 15.6% during the same period—despite its continued monopoly privileges. In 2022, the combined GDP (by PPP) of the Global South, excluding China, surpassed that of the Global North.

The Global Economic Shift

In recent decades, the global economy has undergone radical changes. In 2000, the economies of the G7 were roughly ten times larger than those of the BRICS. However, the global financial crisis of 2008 hit advanced economies hard, reducing their overall output and leading to long-term growth declines. By 2023, the GDP of advanced economies had shrunk to about a third of what it once was. Projections indicate that by 2030, their share could further decrease to just one-tenth. In contrast, the aggregate economic power of the BRICS nations is expected to surpass that of the G7 in terms of GDP.

Challenging the West’s Economic Dominance

The West comprises only a tenth of the world’s total population, yet it dominates all international financial institutions and shapes global rules in its favour. This unequal power dynamic dates back to the colonial era but is now being challenged by the rapid economic growth of developing countries, whose share of global GDP continues to rise. (Siddiqui, 2024)

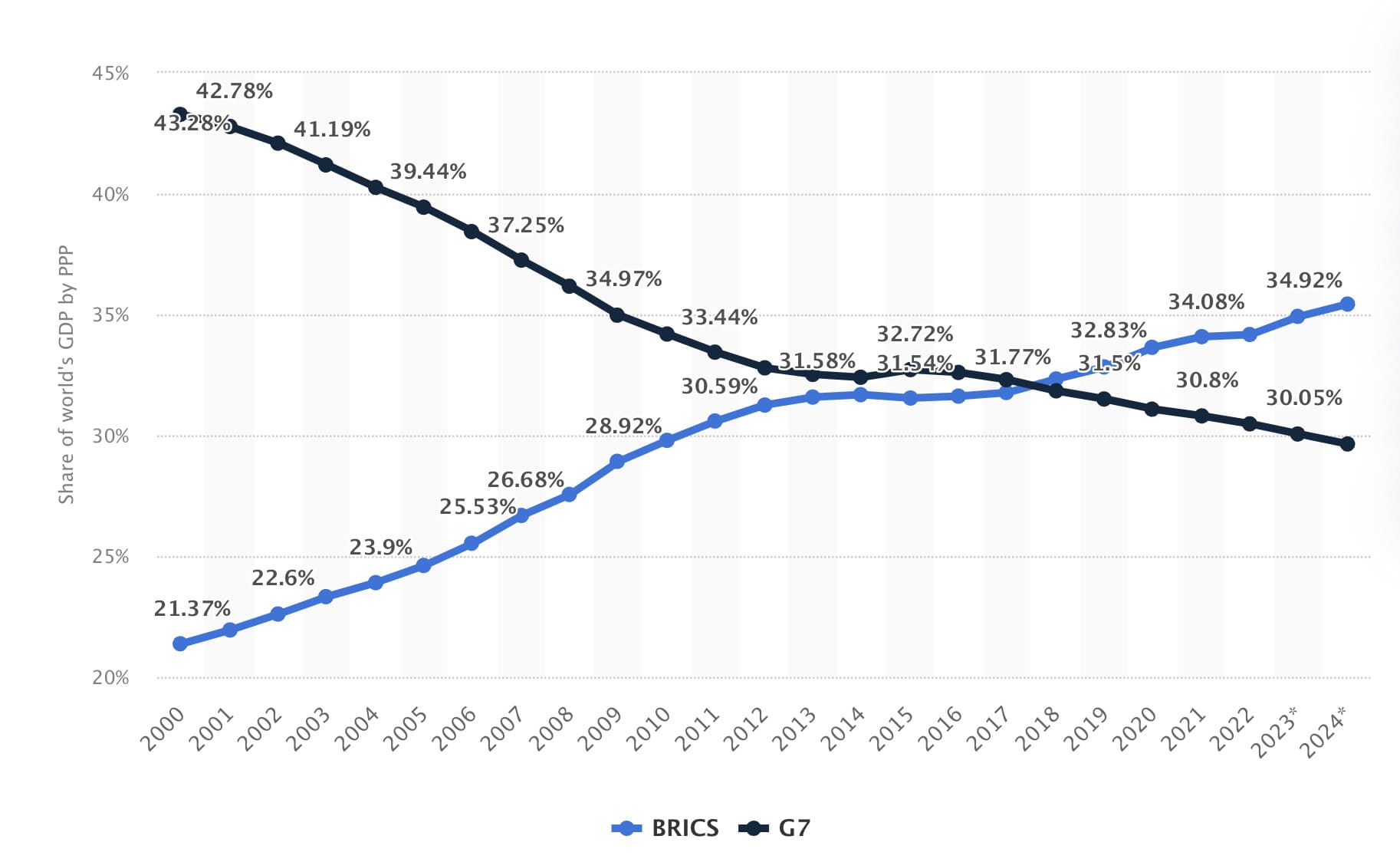

BRICS countries surpassed the G7 in terms of global gross domestic product (GDP) measured by purchasing power parity (PPP) in 2018 (See Figures 1 and 2). By 2024, the gap had widened further, with BRICS accounting for 35% of global GDP, compared to the G7’s 30%. According to the International Monetary Fund (IMF), the BRICS bloc will collectively hold 32.1% of global GDP by 2023, a sharp increase from 16.9% in 1995 and notably more than the G7’s share of 29.9%.

Figure 1: The Share of Global Output Growth Contribution Between G7 and BRICS (in PPP), 2000-2024.

Figure 2: The Share of G7 and BRICS in Global GDP in PPP, 1995-2023.

Despite BRICS’ rise, the US dollar continues to wield enormous financial power in international markets. Although de-dollarization efforts have gained momentum, fully dislodging the US dollar from its dominant position will take time. The dollar’s share in global reserves has slightly declined in recent years, partly due to changes in how gold is categorized under the Basel III framework. In 2020, gold was reclassified as a less risky asset by the IMF and World Bank, prompting central banks to diversify their reserves. Nevertheless, as of 2023, around 60% of global central bank reserves are still held in US dollars, with 20% in euros.

The US dollar remains the world’s most traded currency, involved in nearly 90% of all foreign exchange transactions. (Siddiqui, 2020b) Since 1944, the dollar has been the dominant currency for foreign exchange reserves, currently making up 60% of global reserves, compared to the Chinese renminbi’s 3%. The dollar’s strength lies in its liquidity, wide acceptance as a medium of exchange, and freedom from capital controls, unlike the more tightly regulated currencies of China, Russia, India, and South Africa. However, BRICS countries are increasingly using local currencies for bilateral trade, gradually reducing their reliance on the dollar and their exposure to foreign exchange volatility. (Siddiqui, 2021)

Learning from the Past to Build the Future

Understanding history is crucial to shaping a prosperous future. As the saying goes, “the key to the future lies in the past.” Historically, Asia’s share of global GDP plummeted from 60% in 1820 to just 20% by the 1950s. This sharp decline coincided with the colonization of Asian countries by Western European powers, which impoverished the region. Once self-sufficient and exporters of finished goods, these economies were transformed into suppliers of raw materials, resulting in widespread illiteracy, malnutrition, hunger, and poverty.

After World War II, European colonial powers became economically and militarily weakened, while the United States emerged as the leader of global capitalism. Many colonies gained independence in the post-war period, but the colonial system was soon replaced by a neocolonial structure. (Siddiqui, 1989) Developing countries remained dependent on the West for trade, technology, and finance. In the 1980s, the West engineered a debt crisis in the developing world: as global oil prices surged, the US raised interest rates, causing foreign debt repayments to skyrocket. Many developing nations faced crippling debt crises and were forced to borrow more from international financial institutions just to service their existing debts. (Siddiqui, 2024)

Western Neoliberalism and Its Impact

Since the 1980s, Western economic policy has shifted towards neoliberalism. Unlike earlier forms of capitalism, neoliberalism involved relocating metropolitan capital from advanced economies to poorer countries in order to exploit their low wages and reduce production costs for the global market. This shift marked the end of state intervention in “demand management,” which had been a cornerstone of the post-war economic policy known as the “Golden Age” of capitalism.

Despite the long struggle for independence by developing countries, Western hegemony—particularly that of the United States—continues. However, global power dynamics are changing. The US has seen its control weaken in critical areas such as financial markets, science and technology, and the exploitation of natural resources in developing countries. Yet, in other domains, such as control over information and media narratives, the West still holds a firm grip. The US and NATO also maintain a significant military advantage over much of the developing world. For example, the US and European countries account for nearly 70% of global military spending. Many developing nations fear US influence, given its extensive network of foreign military bases and its ability to destabilize or overthrow governments, impose sanctions, and cripple economies—instilling a fear of retribution.

BRICS and the Potential for South-South Cooperation

Over the past few decades, the BRICS nations have achieved remarkable economic growth. However, their political influence in global governance has not kept pace with their economic transformation, particularly given their growing share of the global economy and international trade. (Duggan, et al 2021) The BRICS bloc is highly diverse: India, for instance, has the world’s largest and fastest-growing population (Siddiqui, 2019b), while Russia’s population is in decline. China is a manufacturing powerhouse, while the Middle East, with the inclusion of nations like Saudi Arabia and Iran, supplies much of the world’s oil and gas. Brazil boasts a vast agricultural and industrial base.

This diversity provides the BRICS countries with an opportunity for South-South cooperation, where they can leverage their unique strengths to create a new, multipolar global order. (Siddiqui, 2020a) Through cooperation, these nations can amplify their voices in international forums and drive reforms in global governance systems that have historically been dominated by the West. (Duggan, et al 2021)

Figure 3: Expanded BRICS GDP in trillions of US dollars.

Figure 4: Share of Manufactures in Exports in 2022 (in %).

The dramatic growth of BRICS economies can be attributed to their increasing participation in global trade, as well as intra-BRICS trade. In 2010, the total trade volume of BRICS countries amounted to US$4.7 trillion. By 2018, this figure had risen to US$6.8 trillion—an increase of 1.4 times. In contrast, the total trade of G7 countries increased from US$10.8 trillion in 2010 to US$13 trillion in 2018, an increase of only 1.2 times. This shows that BRICS nations are increasing their global trade involvement at a faster pace than the G7. In 2010, BRICS accounted for 14.7% of global trade, while G7 controlled 33.8%. By 2018, BRICS’ share had grown to 17.1%, while the G7’s share had decreased to 32.7%.

In recent years, trade between BRICS countries has grown significantly. For example, in 2000, Brazil and China traded US$2.3 billion annually. By 2019, they were trading nearly US$1 billion every 72 hours, reflecting a fiftyfold increase in trade in just 20 years. Similarly, China-India trade rose 28 times, from US$3 billion in 2000 to US$85 billion in 2019. Overall, intra-BRICS trade volumes increased from US$459 billion in 2010 to US$684 billion in 2019. In comparison, trade between the US and the EU (which includes most G7 members) increased from US$409 billion in 2010 to US$625 billion in 2019.

Most economists predict that US economic growth will continue to slow, as it has for the past 30 years, while Asian economies—especially China and India—are expected to rise steadily over the next decade. BRICS countries have not only boosted exports but have also increased the share of manufactured goods in their exports, which demonstrates their growing capacity to produce goods that are in demand globally. However, despite this progress, the share of manufactured exports among BRICS nations averages 48%, compared to 66% for the G7 (See Figure 4). This gap highlights the advantage the G7 still holds in terms of advanced manufacturing capabilities.

While BRICS is gaining economic momentum, the G7 still enjoys key advantages. The G7 consists of rich Global North nations with higher average incomes, greater productivity, and lower unemployment rates. Historically, these nations have dominated the global economy and set trade and economic rules in their favour.

In 2022, the US had a nominal GDP of US$23.1 trillion, while the other G7 economies saw more modest figures: Japan (US$5.1 trillion), Germany (US$3.8 trillion), the UK (US$2.8 trillion), France (US$2.7 trillion), Italy (US$2 trillion), and Canada (US$1.7 trillion). BRICS nations, by comparison, have experienced economic growth, but there are notable discrepancies in their performance. In 2022, China’s nominal GDP was US$16.3 trillion, significantly higher than that of its BRICS counterparts. India, Brazil, and Russia had GDPs of US$3 trillion, US$1.8 trillion, and US$1.8 trillion, respectively, while South Africa’s GDP was much lower at US$351 billion (See Figure 3)

The BRICS group aspires to play a larger role in global governance, driven by the growing disparity between the influence of developing countries in the global system and their ability to participate in that system. As the economic power of developing economies expands and global power shifts toward the Global South, this imbalance becomes increasingly evident. For example, the UN General Assembly reflects this shift, with developing countries moving toward greater cooperation through South-South initiatives. The current global governance system, however, is in crisis, and efforts to reform institutions like the International Monetary Fund (IMF), World Bank, and World Trade Organization (WTO) have largely failed. (Duggan, et al 2021)

Yet, rising inequality and divergent growth rates among developing nations have emerged as significant challenges. While some East Asian countries, including China and India, have experienced rapid economic expansion, many African and Latin American nations have faced slower growth and rising external debt over the past two decades. Trade imbalances are increasing, and even where trade in manufactured goods has grown, much of this is linked to global supply chains, with limited value added by developing economies. The primary gains continue to accrue to headquarters-based activities in advanced economies (UNCTAD, 2018). Moreover, foreign direct investment (FDI) in developing countries remains concentrated in extractive industries and labour-intensive sectors, which often have low environmental standards. This has led to poor governance, low productivity, high unemployment, and rising social inequality.

Economic integration and South-South cooperation among the Global South (former colonies) have long concerned the West. In the 1970s, when developing countries called for a “New International Economic Order” (NIEO), the West strongly opposed it. Five decades later, the Global South is once again organizing and demanding a greater voice in global governance. (Siddiqui, 1985)

Despite its challenges in shaping the global agenda, BRICS remains the most comprehensive multilateral platform for promoting the interests of the developing world through enhanced South-South cooperation. This cooperation has led to rapid economic growth and deepening economic ties among developing nations. By 2011, exports between developing countries had surpassed their exports to advanced economies (WTO, 2019). The potential for higher growth rates, trade liberalization, and greater industrial cooperation within the Global South appears stronger than with the Global North.

Since 2000, the G7’s share of global GDP (measured by purchasing power parity, PPP) has declined from 43% to 30%, while the original five BRICS countries’ share has increased from just over 21% to 35% during the same period. When measured in nominal US dollars, the G7 still holds a higher share at 43%, but the gap between the two groups is narrowing. With the addition of countries that have applied to join BRICS, the group’s share of global GDP is set to rise significantly. Furthermore, the recent expansion of BRICS, which now includes Egypt, Ethiopia, Iran, Saudi Arabia, and the United Arab Emirates, marks what Chinese President Xi Jinping described as a “historic” moment. This expansion is expected to generate trillions of dollars in additional output, bringing BRICS’ total output to US$29 trillion and accounting for 28.4% of global GDP.

The US economy alone accounts for more than 25% of global economic output, with the European Union contributing approximately another 17%. When combined with other advanced economies such as Canada, the UK, Australia, and Japan, the total GDP of these countries constitutes about 45% of the global economy. Despite this, BRICS countries, though currently characterized by lower per capita incomes, are experiencing much faster economic growth compared to the G7 nations, a trend expected to continue until 2050.

However, there are significant disparities in the economic performance of the BRICS members. For example, China’s economy dominates the group, with a GDP of $18 trillion, accounting for roughly 63% of the BRICS’ total GDP. India’s per capita GDP ($2,389) is less than one-fifth of China’s ($12,720) and one-sixth of Russia’s ($15,345). This gives China disproportionately greater leverage within the group. While India is the second-largest BRICS economy, China’s economy is more than five times larger in terms of GDP.

China and India are two of the world’s leading emerging economies. As of 2022, China and India are the 2nd and 4th largest economies globally on a nominal basis (see Table 1). On a purchasing power parity (PPP) basis, China ranks 1st and India 3rd. Together, these countries account for 21% and 26% of the world’s total wealth in nominal and PPP terms, respectively, and they jointly contribute to over half of Asia’s GDP.

In terms of sectoral GDP composition in 2022, China’s GDP was made up of agriculture (8.3%), industry (39.5%), and services (52.2%). For India, the composition was agriculture (14.9%), industry (23%), and services (61.5%). (The Economist, 2023)

Table 1: China and India’s Macroeconomic Indicators in 2022.

| China | India | |

| Population | 1.43bn | 1.43bn |

| GDP growth (%) | 4.7 | 5.6 |

| GDP per head (US$) | 13,680 (PPP: 23,460) | 2,430 (PPP: 8,810) |

| Inflation (%) | 2.9 | 5.2 |

| Budget balance (% of GDP) | -4.2 | -6.0 |

Source: The Economist, 2023, p.103.

To address the infrastructure needs of member countries, the BRICS established the New Development Bank (NDB) in 2015. By 2022, the bank had provided loans totaling $32 billion to developing countries for infrastructure projects, with a focus on funding sustainable development. However, under the leadership of Dilma Rousseff, the former president of Brazil and current director of the NDB, the bank has made it clear that it will not provide loans for debt servicing. This stance means that BRICS member countries will continue to rely on institutions like the International Monetary Fund (IMF) for financial support, often accompanied by the implementation of “structural adjustment programs” that enforce neoliberal reforms and austerity measures.

The global financial crisis of 2008 marked a pivotal moment for G7 countries and also had a significant impact on developing economies. Unlike previous crises in Latin America (1980s) and East Asia (1997), which were region-specific, this crisis originated on Wall Street—the epicenter of global capitalism. In November 2008, the U.S. invited G20 finance ministers, including those from emerging economies, to discuss the global economic crisis. This marked the first time that emerging economies were included in the global governance and economic management discussions, which had previously been dominated by Western countries.

In recent years, particularly following U.S. sanctions on Russia and the removal of Russian banks from the SWIFT payment system, BRICS members such as China, Russia, and Brazil have developed alternative settlement platforms. These platforms provide alternatives to the Society for Worldwide Interbank Financial Telecommunication (SWIFT) payment system, signaling a shift toward greater financial independence from Western-dominated institutions.

Conclusion

The study concludes that the global economy and governance are gradually shifting towards a multipolar world—a positive development for the Global South, signaling a potential end to Western dominance and hegemony. Over the past three centuries, inequality has been deeply entrenched through slavery, wars, and both colonial and neo-colonial policies.

The erroneous belief that international trade benefits all nations equally, based on the assumption of full employment of all factors of production (including labour), both before and after trade, was a myth propagated by colonizers in the 19th century. It claimed that trade merely reshaped production towards comparative advantages, but this oversimplified view ignored the realities of exploitation and underdevelopment in many regions.

The neoliberal economic order, characterized by relatively unrestricted flows of goods, services, and capital, was built on the bourgeois argument that trade benefits all. However, after the 2008 collapse of the American housing bubble, which triggered a global financial crisis and prolonged overproduction, this narrative began to unravel. Advanced economies increasingly adopted protectionist measures to shield their industries from imports, contradicting the free-trade ethos of neoliberalism.

The last few decades have witnessed a significant transformation in the global economy. In 2000, the G7 economies were ten times larger than those of the BRICS. However, the 2008 financial crisis in advanced economies significantly reduced their output, leading to a long-term decline in growth rates. By 2023, the GDP of these advanced economies had shrunk considerably. It is predicted that by 2030, their share in the global economy will further decrease, while the BRICS nations are expected to surpass the G7 in terms of GDP.

The BRICS group is now striving to improve the stability, reliability, and fairness of the global financial system through the increased use of local currencies, alternative financial arrangements, and alternative payment systems. This shift signals a broader transformation toward a more balanced and inclusive global order, with the BRICS countries playing a leading role in shaping this new landscape.

About the Author

Dr Kalim Siddiqui is an economist specialising in International Political Economy, Development Economics, International Trade, and International Economics. His work, which combines elements of international political economy and development economics, economic policy, economic history and international trade, often challenges prevailing orthodoxy about which policies promote overall development in less-developed countries. Kalim teaches international economics at the Department of Accounting, Finance and Economics, University of Huddersfield, UK. He has taught economics since 1989 at various universities in Norway and the UK.

References

- Niall Duggan, N., Hooijmaaijers, B.and Arapova, E. (2021) “The BRICS, Global Governance, and Challenges for South–South Cooperation in a Post-Western World”, International Political Science Review, 43(4).

- Siddiqui, K. (2024) “Neocolonialism: An analysis of international factors on the development of the Global South” World Financial Review, December-January. pp.2-11.

- Siddiqui, K. (2023a). “De-dollarisation, Currency Wars, and the End of US Dollar Hegemony” World Financial Review, August-September, pp.2-14.

- Siddiqui, K. (2023b). “The Political Economy of Shanghai Cooperation Organisation (SCO) and the Growing Regional Multilateral Ties” World Financial Review, February-March, pp. 2-14.

- Siddiqui, K. (2021) “The Bilateral Swap Agreements and the Demise of US Dollar” World Financial Review, September-October, pp.56-64.

- Siddiqui, K. (2020a) “Prospects of a Multipolar World and the Role of Emerging Economies” World Financial Review, November-December, p.65-77.

- Siddiqui, K. (2020b). “The US Dollar and the World Economy: A critical review” Athens Journal of Economics and Business. 6(1):21-44. January.

- Siddiqui, K. (2019a). “One Belt and One Road, China’s Massive Infrastructure Project to Boost Trade and Economy: An Overview” International Critical Thought. 9(2): 214-235.

- Siddiqui, K. (2019b). “A Century of India’s Economic Transformation: A Critical Review” Journal of Perspectives on Financing and Regional Development, 7(1): 1-22, Jan.-Feb.

- Siddiqui, K. (2016). “Will the Growth of the BRICs Cause a Shift in the Global Balance of Economic Power in the 21st Century?” International Journal of Political Economy 45(4):315-338.

- Siddiqui, K. (1989) “Neo-Classical Economic Theory: A critical perspective”, Klassekampen, (in Norwegian) August 31& September 1, Oslo, Norway

- Siddiqui, K. (1985) “South-South Economic Co-operation and its Future Prospects”, Bergens Tidende, October 4, Norway.

- United Nations Conference on Trade and Development (UNCTAD) (2018) Trade and Development Report 2018: Power, Platforms and the Free Trade Delusion. New York, NY: United Nations.

")

")

(1)")

Charlotte Koep

Charlotte Koep")

")