")

Image from https://www.worldbank.org/en/archive/history/exhibits/Bretton-Woods-and-the-Birth-of-the-World-Bank

The erosion of US dollar hegemony—driven by structural debt, financialisation, geopolitical fragmentation, and reserve diversification—signals a historic inflection point in the global monetary order. Dr Kalim Siddiqui argues that this crisis of rentier dominance generates acute instability for the Global South, yet also creates opportunities to build sovereign, development-oriented financial institutions beyond dollar-centred extraction.

I. Introduction

The erosion of dollar hegemony—rooted in mounting structural debt, the accelerating financialisation, and geopolitical fragmentation, and the strategic diversification of reserves into gold and alternative currencies—signals a decisive historical inflection point. This transition reflects not merely cyclical instability but a deeper crisis in the rentier foundations of United States (US) global dominance. As Western cohesion weakens and emerging economies pursue monetary and institutional alternatives, the international monetary order is undergoing a structural realignment toward multipolarity.

This study argues that the transformation presents the Global South with profound risks—heightened financial volatility, intensified geopolitical rivalry, and the threat of renewed dependency—yet also opens a historic opportunity to challenge rent-based extraction and construct more sovereign, development-oriented financial architectures. The outcome will depend on whether emerging economies can convert systemic rupture into coordinated institutional innovation.

The 1944 Bretton Woods Conference established a new international monetary order through the creation of the International Monetary Fund (IMF) and the World Bank (Siddiqui, 1994). This agreement solidified the US dollar as the global currency, a position underpinned by the sheer dominance of US. It supplanted the gold standard and institutionalised the US dollar as the de facto global reserve currency for finance and trade. At the time, the US accounted for approximately 35% of global GDP, and its industrial corporations, functioning as the world’s primary exporters, generated substantial trade surpluses. This concentration of economic power enabled the US to accumulate two-thirds of the world’s official gold reserves, thereby rendering the dollar “as good as gold” and anchoring the new system to US fiscal credibility (Siddiqui, 2020).

For over eighty years, the existence of an uncontested hegemonic power—a recognised leader of global capitalism—provided the geopolitical and economic stability necessary for transnational capital accumulation. This unipolar configuration reduced transactional uncertainty, enforced the institutional frameworks of the Bretton Woods system, and created the stable conditions under which international business could be conducted and profits secured. In this regard, the longevity of US hegemony was not merely a political phenomenon but a structural prerequisite for the post-war expansion of global finance and trade (Siddiqui, 2025a).

In the 19th and early-20th century, during the heyday of the British Empire, global finance and trade was conducted within the framework of the ‘Gold Standard’. At that time, British imperialism was the world’s hegemon, playing a similar role to that of US imperialism in the postwar period – providing the stable economic and political foundations upon which world trade and industry could flourish.

The British economists like Adam Smith and David Ricardo then developed the ideas of bourgeois ‘political economy’, championing liberalism, free trade, and the ‘invisible hand’ of the market. By the end of the 19th century, however, it was clear that British capitalism was being overtaken by its rivals. The First World War catalysed the changing balance of forces between the powers. Britain, France, and Germany economies were weakened from the war. The Treaty of Versailles left Germany heavily indebted to Britain and France, who in turn owed huge sums to the US. Meanwhile, the war accelerated the migration of global financial activity from the City of London to New York’s Wall Street.

By the interwar period, Britain could no longer sustain its role as the guarantor of global trade and finance. The Gold Standard, weakened by geopolitical strains and economic instability, collapsed during the Great Depression. In response, capitalist powers adopted protectionist “beggar-thy-neighbour” policies, raising tariffs to curb imports. These measures deepened the global slump, triggering a decade of stagnation.

The collapse of Bretton Woods ended the monetary certainty of the postwar boom. Today, the global economy enters a third era of upheaval. Massive US sovereign debt, rising fiscal deficits and the weaponisation of financial sanctions have accelerated a pivot toward multipolarity. If the twentieth century saw power migrate from London to New York, the current decade witnesses its diffusion—challenging the capitalist equilibrium established eighty years ago.

The structural stability of the US-led order is increasingly undermined by the US diminishing share of global output and its continued reliance on the dollar’s ‘Exorbitant Privilege’. For decades, successive US administrations have sustained a debt pile exceeding $38 trillion through deficit financing and easy money. This model depends on the world’s willingness to absorb US Treasuries—a dynamic that functions as a hidden transfer of surplus from the global periphery to the US (Vasudevan, 2008).

The concept of US hegemony remains inextricably linked to what Valéry Giscard d’Estaing famously termed the “Exorbitant Privilege” of the US—the unique capacity to borrow in its own currency, run persistent balance of payments deficits, and finance external liabilities without the constraint faced by other nations. This privilege endures to the present day, and its persistence counsels against the assumption, prevalent in some analyses, that the dollar’s dominance is undergoing a gradual but inexorable decline (Siddiqui, 2025a).

A more nuanced reading of monetary history suggests that the trajectory of dollar hegemony is neither linear nor predetermined. The Nixon shock of 1971 offers a particularly instructive parallel. When President Nixon unilaterally suspended the dollar’s convertibility into gold, conventional wisdom anticipated the collapse of the Bretton Woods system and, with it, the dollar’s privileged position. What transpired instead was a remarkable feat of monetary alchemy: the dollar was simultaneously devalued and enhanced. The immediate effect was a reduction in the dollar’s external value, stimulating US exports, while bond yields adjusted to reflect the new regime. Yet far from diminishing the dollar’s global role, the Nixon shock inaugurated an era of renewed—indeed, intensified—dollar dominance, as the world shifted to a pure fiat dollar standard with no convertibility constraint whatsoever (Palley, et al, 2024).

This historical precedent suggests that the Trump administration’s apparent objectives—to weaken the dollar while preserving its preeminent status—may be less contradictory than they appear. The successful replication of the Nixon formula would require a delicate balancing act: inducing holders of dollars to sell, thereby depressing the currency’s external value, while simultaneously ensuring that the proceeds of those sales are not channelled into rival currencies capable of challenging the dollar’s reserve status.

The feasibility of this manoeuvre depends critically on the behaviour of other major economic actors, particularly China. More consequential is the trajectory of the yuan and the broader BRICS constellation. The critical question is whether China will pursue a strategy of simple currency internationalization—encouraging the use of the yuan in cross-border transactions—or whether it will aspire to construct a more ambitious institutional framework along the lines of a Bretton Woods system for the BRICS area (Siddiqui, 2024a). In such a system, the yuan would assume the role played by the dollar in the original Bretton Woods architecture, with China, as the surplus country, recycling its surpluses through loans, development finance, and direct aid to other countries.

The original Bretton Woods system was built precisely on these factors: the US, as the dominant surplus country, provided liquidity to the system through its balance of payments deficits and recycled its surpluses through official channels to reconstruct and integrate the EU and Japanese economies. China’s current position—running substantial trade surpluses with much of the Global South and accumulating claims on future production—bears more than a passing resemblance to the US position in 1944.

The contemporary global order is defined by the US’ capacity to impose financial blockades through its control over the dollar-based payment architecture. This choke point was starkly demonstrated in Venezuela between 2016 and 2021: following aggressive US sanctions, oil production collapsed by 75%. The subsequent economic implosion—hyperinflation and a two-thirds decline in GDP per capita—represented a humanitarian catastrophe more severe than many conventional conflicts. This model of economic crushing, recently reiterated in US policy discussions regarding Iran, confirms that access to the dollar is no longer a commercial right but a geopolitical lever.

This reality has triggered an unprecedented diplomatic realignment. In early 2026, the influx of Western leaders to Beijing—including Keir Starmer, Mark Carney, and Michael Martin—signals a departure from the unipolar era that followed the Soviet Union’s dissolution in 1991. That this marks the first visit for a Canadian Prime Minister since 2017 and a British Prime Minister since 2018 highlights the urgency of the moment. These middle powers, traditionally dependent on the US market, can no longer afford to be collateral damage in a bipolar rivalry they did not create. For an export-dependent economy like Germany, where one in four jobs relies on international trade, the risk of being caught in the crossfire of financial sanctions is an existential threat.

The current global transition is unfolding through a deliberate strategy of systemic insulation. Central banks are no longer merely diversifying; they are actively reducing exposure to long-duration US assets and expanding bilateral settlement frameworks in alternative currencies. As Mark Carney articulated at the 2026 Davos World Economic Forum, the imperative for middle powers is now one of collective agency: “If you’re not at the table, you are on the menu.”

II. The Erosion of US Hegemonic Power

A new equilibrium emerged only after the devastation of the Second World War. The US assumed the role of global stabiliser, providing essential public goods to Europe: military protection, open markets, credits, a stable reserve currency, and lender-of-last-resort functions. The dollar’s status as the global reserve currency allowed the US to borrow at lower interest rates, enjoy cheaper imports, and finance military spending through deficits (Vasudevan, 2008).

Despite robust growth during the post-war period in the West, known as capitalism’s “Golden Age,” however, the US entered a phase of relative decline. Reconstructed rivals—especially West Germany and Japan—regained industrial competitiveness, eroding the market share of US monopolies. By the early 1970s, chronic US fiscal and trade surpluses had turned to deficits. Expanding the money supply to fund foreign wars, acquire overseas assets, and fuel speculation generated systemic inflationary pressures. As a result, dollar–gold convertibility—the cornerstone of Bretton Woods—became untenable. Following speculative attacks on an overvalued currency, President Richard Nixon unilaterally suspended gold convertibility on 15 August 1971. This “Nixon Shock” effectively ended the Bretton Woods system, ushering in an era of floating exchange rates and competitive devaluations (Vasudevan, 2008).

The Nixon Shock precipitated the 1973–75 global crisis, the first of several ruptures marking the exhaustion of the postwar boom. Paradoxically, the collapse of Bretton Woods entrenched the dollar more deeply at the core of the international system.

Though no longer anchored to gold, the dollar persisted as the universal medium of exchange required by an expanding global economy. US institutions were the primary beneficiaries, yet Western ruling classes acquiesced, leveraging the US-led framework to export capital and embed themselves in global supply chains.

This “exorbitant privilege” enabled the US to run massive deficits without currency collapse—effectively taxing the rest of the world to fund US military expansion and domestic consumption. Yet the very dollar outflows that supplied global liquidity eroded confidence in gold convertibility, rendering the fixed-rate system unsustainable.

Moreover, while the Nixon Shock of 1971 forced a transition to floating fiat currencies, 2026 is witnessing a move toward Central Bank Digital Currencies (CBDCs) and a strategic resurgence in sovereign gold reserves. These developments signal a concerted effort by nations to bypass the SWIFT system and insulate their economies from the weaponisation of the US dollar.

Figure 1: The US Dollar Value Against Six Major Currencies, 2026.

By early 2026, the US dollar had retreated to its lowest valuation in four years, triggering a flight to traditional safe havens such as gold and the Swiss franc. Depreciating 1.3% against a weighted basket of currencies—and marking a cumulative 10% decline over the previous year—the downturn reflects a broader global recalibration (See Figure 1). While a weaker dollar can ease debt-servicing burdens for emerging markets, its volatile decline underscores the fragility of the dollar’s so-called exorbitant privilege (The Guardian, 2026).

This ‘exorbitant privilege’ remains a cornerstone of US economic power. Robust global demand for dollar-denominated assets—particularly US Treasuries and equities—enables US firms to borrow at preferential rates, directly bolstering capital accumulation. Moreover, the world’s appetite for US debt has historically granted the federal government exceptional fiscal latitude, allowing it to sustain persistent deficits that would trigger balance-of-payments crises elsewhere.

Furthermore, the dollar-centric architecture serves as a potent instrument of extra-territorial power. By controlling the world’s primary medium of exchange, the US can weaponise finance: seizing foreign sovereign assets, imposing comprehensive sanctions, and effectively excommunicating adversaries from the global economy. This financial statecraft ensures the US dollar remains not merely a tool of trade but a fundamental pillar of imperialist hegemony (Siddiqui, 2023a).

This economic divergence is now manifesting in the monetary sphere. By the end of 2025, the US dollar’s share of global currency reserves had fallen to approximately 57%—its lowest level since 1994 and a sharp decline from 73% in 2001. While the dollar remains dominant, facilitating 88% of foreign exchange transactions and 81% of trade finance, its status is no longer uncontested.

Yet the material foundations of the US currency and economic hegemony are eroding. The US share of global nominal GDP has stagnated at roughly 26%, while China’s share has surged from 2.5% four decades ago to over 22% by 2025. This shift is not merely quantitative but qualitative: Chinese corporations such as BYD and DeepSeek now challenge US dominance in frontier industries like electric vehicles and advanced AI, directly threatening the profit margins of established US capital.

Russia and China are actively constructing alternative financial architectures—most notably the Cross-Border Interbank Payment System (CIPS)—to bypass the SWIFT messaging network and insulate themselves from US-led sanctions. As foreign investors increasingly seek assets beyond the reach of US extra-territorial jurisdiction, the global financial system is transitioning from a unipolar dollar standard toward multipolarity.

This shift is not merely a change in destination but a total reshaping of currency and investment behaviour. Oil is no longer traded as an isolated commodity; instead, it has become the anchor for comprehensive multi-sector industrial ecosystems. Major Chinese hubs, particularly Shenzhen, are now exporting high-tech industrial equipment and infrastructure solutions to the Gulf countries that are no longer settled in dollars by default. Contracts are increasingly structured around long-term project financing, technology transfer, and digital settlement and infrastructure projects, which bypasses the SWIFT system to enable instant cross-border settlement.

China’s strategy effectively merges energy procurement with industrial integration. By bundling oil purchases with the development of 5G networks, AI infrastructure, and logistics corridors, China has repositioned itself at the centre of long-term global demand growth. This bundled integration alters exporters’ bargaining power and gradually erodes the dollar’s monopoly. As energy trade merges with industrial strategy, the resulting shift in settlement behaviour represents a decisive move toward a multipolar financial order. While the Saudi riyal remains pegged to the dollar, the kingdom has begun negotiating oil sales in alternative currencies—including the yuan—to gain better leverage. In late 2025, major energy contracts between Saudi Arabia, Iran, and China are being settled in yuan, signalling a weakening of the petrodollar’s once-absolute monopoly. (Siddiqui, 2026a).

Mainstream economists frequently underestimate the velocity of this transition by focusing on currency mechanics rather than the underlying payment architecture. The traditional petrodollar system has not merely encountered competition; it has inadvertently incentivised the construction of comprehensive alternatives. The watershed moment occurred in 2022 with the freezing of $300 billion in Russian sovereign reserves. This event demonstrated that a high concentration of reserves in US dollars represents a systemic vulnerability rather than a security. For global central banks, this single act of financial statecraft shifted the logic of reserve management from return on investment to sovereign survivability.

Simultaneously, the economic gravity of the global system has migrated toward Asia. Over the last two decades, East and Southeast Asian economies have accounted for higher economic growth and the vast majority of incremental global energy demand (Siddiqui, 2025c), with China’s consumption now exceeding that of the US and the EU combined. This shift is reinforced by national transformation initiatives, such as Saudi Vision 2030 and the UAE’s industrial diversification plans. These projects require long-term industrial partners capable of delivering integrated packages—including refineries, infrastructure and development of ports, 5G networks, and logistics corridors—rather than simple commodity buyers.

As China has emerged as the primary trading partner for these regions, it has successfully deployed parallel financial institutions. While the Cross-Border Interbank Payment System remains smaller than SWIFT, its growth is driven by bilateral trade deals—such as those with Brazil—that settle in local currencies to bypass dollar-denominated friction. This does not portend a dramatic, overnight collapse of the dollar, but rather a slow leakage of hegemony. Dominance has bred overconfidence in the West, delaying adaptation while emerging economies quietly restructure their supply chains. The result is a gradual evolution toward a multicurrency energy trade, where financial fragmentation rises not through a singular crisis, but through the rational, gradual diversification of countries seeking to insulate themselves from markets attacks.

By strategically engaging with China and fostering parallel payment architectures, these nations are moving to neutralise the risks of weaponised interdependence. This theoretical framework explains how the US, by controlling the choke points of global finance—the dollar and SWIFT—can extract concessions or effectively dismantle rival economies. However, the recent diplomatic surge in Beijing indicates a profound shift. Even core Western allies are now adopting a hedging strategy, refusing to be forced into a binary choice between superpowers. Instead, they seek to maximise their own security and economic sovereignty within a fragmented, multipolar landscape.

III. Tariffs and the Precarious Position of Foreign Creditors

The imposition of tariffs, such as those announced by the Trump administration, presents a complex and often counterintuitive dynamic for the US dollar. While tariffs are ostensibly designed to protect domestic industries and reduce the trade deficit by making imports more expensive, their immediate effect is often to boost the dollar’s value. This occurs because significant trade policy uncertainty drives global investors toward the perceived safety of US assets, increasing demand for the dollar. Consequently, the resulting currency appreciation counteracts the intended price effects of the tariffs, offsetting downward pressure on both imports and the overall trade deficit.

This dynamic is further complicated by concurrent domestic economic policies. Large-scale tax cuts, particularly those favouring higher income brackets and big corporations, are expected to stimulate an influx of foreign capital seeking higher returns. While this influx further strengthens the dollar, it simultaneously exacerbates the underlying structural imbalance that is the root cause of the US trade deficit: the gap between domestic savings and investment. Foreign capital flows into the US are, by accounting identity, the mirror image of the trade deficit, meaning that policies attracting such capital inherently widen, rather than narrow, the deficit.

This phenomenon underscores a fundamental paradox of the US dollar’s near-monopoly in international finance: in times of global economic uncertainty or domestic turmoil, the dollar tends to appreciate. Investors flock to the depth, liquidity, and safety of US Treasury markets, reinforcing the very currency strength that harms the competitiveness of US exports. This creates an inherent tension: the very tools used to project economic strength and protect domestic industry often reinforce the structural conditions that perpetuate the trade imbalance.

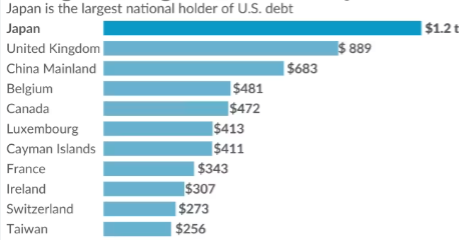

Recent data from the Treasury Department reveals a significant shift in the composition of foreign holders of US debt, challenging the conventional narrative that the US government relies primarily on Japan and China to finance its fiscal deficits (see Figure 2). According to the latest report, all foreign entities combined added $170 billion to their holdings of US Treasury securities in the most recent period, bringing total foreign holdings to a record $8.67 trillion. Notably, well over half of this increase was attributable to the Euro Area. Over the past 12 months, foreign holdings have increased by a substantial $880 billion, representing a growth rate of 15.4 percent.

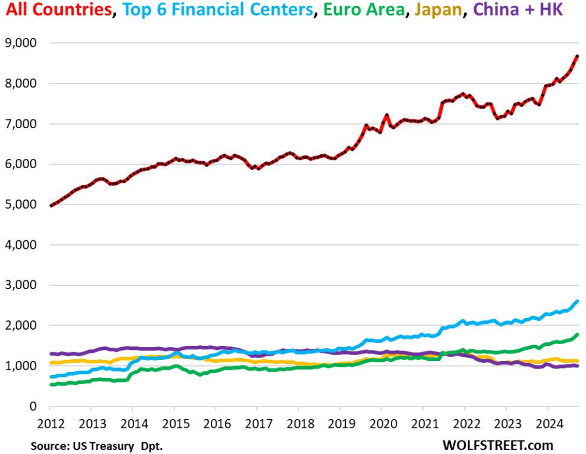

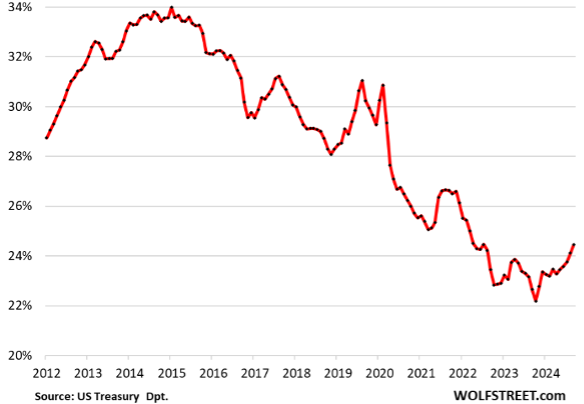

The Figure 3 further disaggregates these holdings by major groups. The Top Six financial centres—comprising London, Belgium, Luxembourg, Switzerland, the Cayman Islands, and Ireland—hold $2.60 trillion (depicted in blue). The Euro Area holds $1.78 trillion (green), followed by Japan with $1.12 trillion (gold), and the combined holdings of China and Hong Kong at $1.0 trillion (purple). This distribution underscores a critical evolution in the geography of international finance: it is no longer predominantly Japan and China upon whom the US government relies to absorb the debt issued to fund its fiscal imbalances. The increasing role of EU financial centres and the Euro Area itself suggests a diversification of the creditor base, with implications for the dynamics of global capital flows and the geopolitical leverage traditionally associated with large bilateral holders of US debt. Moreover, the share of foreign holdings as a percentage of the total treasury debt has declined sharply since 2015 (as shown in Figure 4).

Figure 2: Foreign Holdings of the US Treasurys in 2025 (trillions $).

Figure 3: US Treasury Securities held by Countries, 2012-2025 ($ billions).

Figure 4: Percentage Share of US Treasury Securities held by Foreign Holders, 2012-2025 (%).

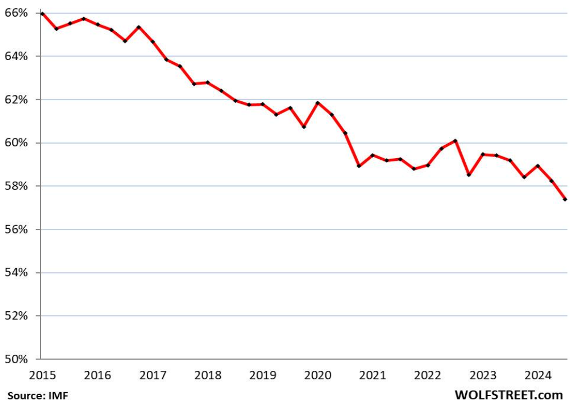

The erosion of the US dollar’s dominance in global finance is no longer merely a theoretical concern but an observable trend substantiated by empirical data. According to IMF data for 2025, the dollar’s share of allocated foreign exchange reserves has fallen to 57.4 percent—the lowest level recorded since 1994. This marks a significant decline from 66 percent in 2015, representing a cumulative drop of 8.6 percentage points over the past decade (see Figure 5).

If the current pace of decline persists, extrapolation of these trends suggests that the dollar’s share of global reserves could fall below 50 percent by the end of 2034. Such a threshold would be more than symbolic; it would represent a fundamental realignment of the international monetary system, potentially diminishing the unique privileges the US has long enjoyed, including the ability to sustain large fiscal and trade deficits with relative impunity. While the US domestic policies may inadvertently reinforce the dollar’s strength in the short term, the longer-term trajectory points toward a more distributed reserve currency landscape, one in which the US may no longer be able to rely on the rest of the world to finance its “excesses” to the same degree as in previous decades.

Figure 5: US Dollar Percentage Share of Global Reserve Currencies, 2015-2025 (%).

IV. The Paradox of Persistence: Dollar Dominance Amidst Structural Decline

The preceding analysis has established that the architecture of global finance operates not as a neutral mechanism for capital allocation but as a system of extraction—a stranglehold on debtor nations. This stranglehold is two-pronged: the debt itself, accumulated under terms set by creditor nations and institutions, and the purpose for which that debt has been incurred. Throughout the Western world, debt has been mobilised not to finance productive industrialization but to underwrite economic rent in its various forms—land rent inherited from feudal structures, monopoly rent extracted through market power, and financial rent appropriated by a usury-oriented banking system. This is the logical extension of classical political economy’s critique: the aims of classical free market economics, as articulated by David Ricardo, were precisely to liberate production from the dead hand of rent-seeking. The contemporary order represents the triumph of the very forces classical economics sought to constrain.

Finance is the instrument through which rent-seeking perpetuates itself—from real estate monopolies controlling urban development to concentrated industries extracting monopoly profits, to central banks captured by financial interests and deployed to discipline government policy. Breaking the stranglehold requires severing the debt relation that binds debtor nations to creditor-imposed austerity and structural adjustment.

Despite the mounting evidence of a multipolar shift in the international monetary system, the US dollar retains its status as the world’s dominant reserve currency. As of 2025, the dollar accounts for more than half of global foreign exchange reserves, maintaining a commanding lead over the euro, its nearest competitor, which represents roughly 20 percent. In nominal terms, the value of dollar-denominated reserves remains substantial, totalling approximately $6.8 trillion in 2025.

This persistence of dollar dominance, however, coexists with the long-term downward trend. The gradual erosion of the dollar’s share—declining from 66 percent in 2015 to 57.4 percent in 2024 and stabilising near 57 percent in 2025—reflects not a wholesale rejection of the dollar system but a measured diversification by central banks responding to evolving geopolitical and financial considerations. Key inflection points, such as the imposition of international sanctions following Russia’s 2022 invasion of Ukraine, have accelerated this trend by prompting reserve-holding nations to reconsider the risks of concentrated exposure to US financial assets. Concurrently, portfolio diversification into alternative currencies and assets, particularly gold, has contributed to the gradual redistribution of global reserves.

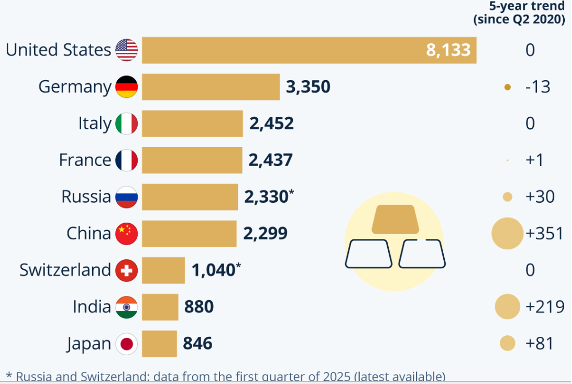

The strategic pivot toward gold as a reserve asset is evident in the accumulation patterns of major central banks. The US maintains the world’s largest official gold reserves, totalling 8,133.5 tonnes. It is followed by Germany, Italy, and France, reflecting the continued preference among Western economies for gold as a store of value. Notably, however, emerging-market economies—particularly China and India—have accelerated their gold purchases between 2020 and 2025, signalling a deliberate strategy to reduce reliance on the dollar. Global gold reserves remain highly concentrated, with nine countries—including Russia, Switzerland, and Japan—accounting for approximately 70 percent of the total global gold reserves.

This dual dynamic—the dollar’s continued dominance alongside active diversification into gold—encapsulates the transitional nature of the current moment (see Figure 6). The infrastructure of dollar hegemony remains intact, but its foundations are being incrementally diversified by state actors seeking to insulate themselves from financial vulnerability. The trajectory suggests that while the dollar’s decline may be gradual, it is also structural, rooted in the same geopolitical and economic forces that have prompted the accumulation of gold and the exploration of alternative reserve architectures discussed throughout this paper.

Figure 6: World’s Gold Reserves, 2025 (in metric tons).

V. Could the Dollar Be Deliberately Collapsed?

The US capacity to address its mounting fiscal imbalances only compounds this vulnerability. Historical precedent suggests that when confronted with unsustainable debt trajectories, policymakers revert to familiar tools—chief among them, electronic dollar creation, euphemistically termed quantitative easing. While such measures provide temporary liquidity and mask the immediate consequences of fiscal excess, they do not alter the underlying reality: excessive money creation inevitably manifests as inflation, eroding purchasing power and exacerbating the very debt dynamics they seek to ameliorate. For foreign creditors already diversifying away from dollar assets, this policy predisposition raises legitimate concerns about the long-term sustainability of US fiscal obligations.

The convergence of these factors—geopolitically motivated diversification, structural shifts in reserve composition, and domestic monetary policies that prioritize short-term stability over long-term credibility—suggests that the era of unchallenged dollar dominance is approaching its terminal phase. This transition has been significantly influenced by the policy environment of the Trump administration and the perceived inadequacy of subsequent US responses to the structural challenges outlined above. While the dollar retains its preeminent position for the moment, the trajectory is unmistakable: the international monetary system is evolving toward a more distributed architecture, one in which the US must increasingly compete for the privilege of financing its deficits, rather than relying on the inertial advantages of a bygone unipolar era.

Within this context, the potential for China to deliberately collapse the US dollar—specifically through the mass divestment of its US Treasury holdings—presents a critical area of inquiry. While not the largest, China remains one of the foremost foreign holders of US Treasury. A strategic sale of these assets, perhaps as retaliation in an escalating trade war, could trigger severe repercussions for both the US and the global financial system. Such an event would not be a mere market correction; it would constitute a financial earthquake, potentially exceeding the severity of the 2008 crisis. The consequences could extend beyond a dollar collapse to a systemic failure of global markets, with a severity possibly mirroring the Great Depression. A crucial amplifying factor is the profound interconnectedness of today’s global economy—a condition far more pronounced than in 1929.

Currently, Japan holds the largest share of US Treasury, followed by China (including Hong Kong), with the remainder distributed among other nations. This concentration raises a pivotal question: could a single actor, or a coalition of major holders such as China and Japan, orchestrate the economic decline of the US, destabilise the dollar, and fundamentally undermine the world’s predominant economic power? The answer is a qualified “maybe.” The scale of the target is immense, with US national debt exceeding $38 trillion and growing at approximately 7 percent annually.

If China were to liquidate all or a substantial portion of its US Treasury holdings, the resulting flood of supply would depress Treasury bond prices and force yields upward. Higher yields would, in turn, increase borrowing costs for the US government, businesses, and consumers, potentially stifling economic growth. Yet while this represents the immediate market mechanism, a more profound and deliberate strategy may already be underway.

China appears to be executing a long-term plan to diminish the dollar’s dominance—all while holding approximately $850 billion in Treasury bonds. As the world’s largest foreign creditor, it is simultaneously building the infrastructure for an alternative financial architecture to replace US-led systems. This multifaceted strategy was evident in June 2024, which saw an acceleration of the digital yuan rollout, concurrent meetings of BRICS nations to discuss a potential alternative reserve currency, and a reported purchase of twenty tons of gold by China. These simultaneous actions suggest a coherent policy aimed at creating a multipolar monetary system, reducing global reliance on the US dollar, and positioning China and its partners at the centre of a new financial order.

VI. Military Keynesianism: Economic Decline Disguised as Strategic Necessity

The US and the European Union (EU) are attempting to resolve the crises of advanced capitalism by resorting to increased military spending (Siddiqui, 2026b). This approach offers, at best, a short-term solution while pushing the world further toward tension and conflict. Within the US, this desperation manifests as resurgent neo-colonial ambitions—evident in interventionist postures toward Venezuela, Greenland, Iran, and Cuba—alongside rumoured consideration of withdrawal from the United Nations. Domestically, these impulses are rationalised through what economists’ term military Keynesianism: the proposition that expanded military expenditure stimulates investment and employment by injecting government money into the economy through deficit spending (Siddiqui, 2025b).

For the EU, however, this logic collides with the structural constraints of the Eurozone. The Stability and Growth Pact’s fiscal rules, which historically limited member states to deficits below 3 percent of GDP (with recent relaxations allowing up to 5 percent), fundamentally restrict the capacity for countercyclical spending. Yet the EU’s present exigencies demand substantial social expenditure: subsidising households grappling with energy costs that have multiplied fourfold as Russian pipeline gas is replaced by more expensive US liquefied natural gas. The continent finds itself trapped between fiscal rules designed for stability and the social requirements of an energy transition imposed by geopolitical realignment.

This predicament is exacerbated by a curious policy consensus that appears to conjure existential threats to justify otherwise impermissible spending. The amplification of fears surrounding conflict with Russia over Ukraine—and the corresponding resistance to any diplomatic resolution that might permit the US to reorient its strategic focus—reflects what might be termed the tunnel vision of neoliberal economists. The underlying assumption appears to be that governments must manufacture geopolitical crises to authorize deficit spending as an economic stimulus, as though the mere act of expenditure, regardless of its object, can revive stagnant economies (Siddiqui, 2025b).

The European Commission’s proposed trillion-euro rearmament initiative exemplifies this fallacy. Arms production, unlike the manufacture of consumer durables such as washing machines, TV, or automobiles, does not enhance civilian living standards. Unlike capital goods and industrial machinery, weapons do not expand productive capacity or generate future income streams. They are, by design, goods destined for destruction—assets whose economic utility is realised only when they cease to exist. Investing in armaments rather than in consumption or productive investment represents a misallocation of capital with profound implications for the EU’s underlying structural challenges.

Foremost among these challenges is deindustrialization. The global distribution of industrial production is undergoing transformative shifts driven by digitalization and what many scholars term the Fourth Industrial Revolution—the increasing capacity of digital technologies to manipulate the physical world. The EU, rather than positioning itself at the forefront of this transformation, is redirecting productive capacity toward military. The German case is illustrative: having lost competitive advantage in automobile manufacturing, the proposed solution is to manufacture tanks instead. This substitution of military for civilian production does not address the fundamental erosion of industrial competitiveness; it merely masks it behind the facade of strategic necessity (Siddiqui 2023b).

The tragedy of military Keynesianism, in both its US and EU variants, is that it mistakes fiscal stimulus for economic revitalization. Injecting government money into the economy through weapons procurement creates employment and generates economic activity, but it does so without expanding the productive base upon which long-term prosperity depends. It is, in essence, a policy of digging holes and filling them—except that the holes, in this case, are designed to be filled with ordnance, and the filling process itself consumes the very resources that might otherwise have been invested in education, health care, infrastructure, research, protection of environment, and the industries of the future.

VII. The Economic Base of Rupture: Investment Power versus Military Power

As that structure fractures under the combined weight of US unilateralism, the rise of alternative poles, and the internal contradictions of neoliberalism, the Global South faces both unprecedented danger and unprecedented opportunity. The danger lies in being crushed between a declining hegemon unwilling to accept limits and a still-unformed multipolar order incapable of providing stability.

The postwar order consolidated the EU and Japan as effectively subordinate partners of the US, their economies reconstructed through Marshall Plan aid to serve as markets for US industrial production, their security guaranteed—and their sovereignty circumscribed—by a network of US military bases and the NATO alliance.

This integration of the dominant classes across the Global North did not produce the “ultra-imperialism” predicted by Karl Kautsky—a peaceful cartel of advanced capitalist powers jointly exploiting the periphery. It did, however, forge a durable unity against perceived common threats: first the Soviet Union, then a succession of so-called “rogue” states—Cuba, North Korea, Iran, Venezuela—whose defiance was construed by the US as obstacles to the “New US Century.”

It is this unity that Canadian Prime Minister Mark Carney has now declared broken. However, as Governor of the Bank of England in 2018, he had complied without hesitation when the US demanded that the British government deny Venezuela access to its own gold reserves—31 tonnes valued at approximately $4.8 billion today. The Canadian connection to Venezuelan subversion runs deeper. Peter Munk, founder of Barrick Gold (now Barrick Mining), had openly called for the overthrow of the Venezuelan Bolivarian Revolution because it obstructed his company’s extraction of Venezuelan gold on terms overwhelmingly favourable to the Canadian mining giant.

Mark Carney’s address at Davos, following his diplomatic engagement with China, offered a remarkable admission from within the citadel of Western power. While avoiding explicit reference to the sordid details of Venezuelan gold seizures or Canadian mining interests, Carney articulated what might be termed the “open secret” of the postwar order: Western leaders have long understood that the much-vaunted “international rules-based order” was partially fictitious. He acknowledged, that the strongest powers exempted themselves when convenient, that trade rules were enforced asymmetrically, and that US hegemony was maintained through practices that diverged sharply from proclaimed principles. Yet they accepted this arrangement because, in Carney’s words, “US hegemony was useful.” They participated in the rituals, avoided calling out the gaps between rhetoric and reality, and collected the benefits of a system organised ultimately around US interests but with sufficient spillovers to reward junior partners.

What has changed, according to Carney, is not a sudden awakening to principle but a practical calculation: the bargain no longer works. The US has turned its expansionist ambitions upon its own allies—Greenland, a territory of NATO member Denmark, and Canada itself. When Chilean President Gabriel Boric, no sympathizer with Maduro, condemned the illegal kidnapping of Venezuelan President with the warning that “today Venezuela, tomorrow anyone,” he spoke to a Latin America long familiar with US coups and invasions. But for Carney, the crucial threshold was crossed when the guns were aimed at the Collective West itself.

The leaders of the G-7 states now confront a hegemon that has abandoned even the pretence of reciprocal benefit. Yet it would be naive to interpret this rupture as a repudiation of hyper-imperialism by EU or Canada. They tolerated the system’s asymmetries and extra-legal practices as long as the costs were borne by others—by Venezuela, by the Global South, by those outside of the Global North. Their discomfort arises not from the nature of the system but from its redirection toward themselves.

Beneath this political rupture lies a deeper economic contradiction. The US, Carney observed pointedly, lacks the investment capacity to generate its own net fixed capital formation, let alone to export capital for the development of allies like Canada and EU. Its productive base eroded by decades of financialization, overseas wars, and offshoring, the US now covets the resources and territory of other nations rather than offering the inducements of investment and development.

China, by contrast, possesses immense surplus capital seeking productive outlets. Before Davos, Carney visited Beijing to sign a range of trade agreements—a testament to the shifting gravitational center of global economic power. The US, despite its still-formidable military apparatus, can no longer project economic hegemony in the classical sense of offering its partners a pathway to development through integration with US capital. This disjuncture between military power and economic capacity—between the ability to coerce and the ability to construct—defines the hyper-imperialism of our time.

The rupture within the G-7 is worth exploiting precisely because it is not a fundamental repudiation of imperialism’s logic but a breakdown of the coalition that long enforced it. The EU and Canadian remain committed to the agenda of hyper-imperialism insofar as it serves their interests; they merely object to being its targets.

For Global South and for middle powers navigating this turbulent landscape, the Carney rupture presents both danger and opportunity. The danger lies in being caught between a declining hegemon lashing out unpredictably and a still-unformed multipolar order incapable of guaranteeing stability. The opportunity lies in the space opened for genuine sovereignty—for countries to assert their independent interests without immediate subordination to either bloc.

The task for those seeking to transcend the logic of exploitation is not to choose sides in an intra-imperial rivalry but to use the spaces opened by that rivalry to construct genuine alternatives—alternatives that address the rent-extraction mechanisms at the heart of the debt relation, that build toward the symmetrical adjustment Keynes envisioned, and that ultimately render both the hyper-imperialism of the declining hegemon and the still-ambiguous project of the rising one subject to democratic control and genuine development priorities (Siddiqui, 2018).

The German invasion of Poland in 1939 was an act of unprovoked aggression that precipitated the World War II in Europe. The ensuing declarations of war by Britain and France helped consolidate an international norm that treats violations of territorial sovereignty as among the gravest breaches of order. Yet this norm has never been applied consistently. From a political economy perspective, its enforcement has depended less on the violation itself than on the identity of the actor and the strategic context.

Colonial interventions by European powers—and later the US—frequently involved invasion, occupation, economic destabilisation, and regime change across the Global South in pursuit of economic and strategic objectives. Despite the profound human costs of these actions, they have rarely drawn the level of condemnation directed at similar violations within Europe. This discrepancy highlights how the principle of sovereignty has long been subordinated to geopolitical and economic interests.

This double standard persists today. The forceful response of European leaders to Donald Trump’s interest in acquiring Greenland, for instance, stands in stark contrast to the comparatively muted reactions to interventions affecting nations in the Global South. Moreover, Western media outlets that champion liberal norms at home often remain silent when those same values are breached by Western powers abroad. Such selectivity underscores a persistent asymmetry in global political discourse.

VIII. The Bancor Vision and China’s Contradictions: Toward a Post-Hegemonic Monetary Order

The preceding analysis has established that China possesses the institutional capacity and economic weight to construct an alternative monetary architecture within the BRICS sphere. This would represent a qualitative shift beyond existing initiatives such as BRICS Pay, which currently functions primarily as a technical alternative to the SWIFT messaging system. To transcend mere payment infrastructure and create a genuine systemic alternative, however, China and its partners must consciously decide to challenge the ‘exorbitant privilege’ of the dollar. Here a profound irony emerges—one that the architects of Trump-era policy, if not Trump himself, appear to recognize: China currently serves as the greatest ally of dollar hegemony. Its accumulation of dollar-denominated assets, its continued participation in US financial markets, and its reluctance to force a systemic rupture all contribute to the very dominance it ostensibly seeks to escape (Palley, et al, 2024).

This paradox invites reconsideration of alternative architectures that might transcend the logic of hegemonic currency altogether. The most sophisticated such alternative remains the International Clearing Union (ICU) proposed by John Maynard Keynes between 1941 and 1944. Conceived as a genuine alternative to the Bretton Woods system that ultimately prevailed, the ICU represented the antithesis of hegemonic monetary organization. Its central innovation was the “bancor”—a neutral international unit of account, neither national currency nor commodity money, through which trade imbalances would be settled multilaterally.

The genius of Keynes’s design lay in its symmetrical adjustment mechanism. Under the ICU, both creditor and debtor nations would bear responsibility for correcting imbalances. Countries accumulating excessive surpluses would face penalties, including the requirement to deposit excess bancor into a reserve fund, while deficit nations could access overdraft facilities. The ICU would function as a bank for central banks, enabling international trade to operate with the same frictionless settlement characteristic of domestic transactions. Fixed exchange rates to national currencies would provide stability, while the bancor’s neutrality would insulate the system from the geopolitical asymmetries inherent in any national-currency-based reserve system. The objective was not merely to manage financial speculation but to promote global economic stability, shield deficit nations from deflationary pressures, and foster real economic growth.

The crucial insight for contemporary purposes is the intergovernmental character of this debt. Keynes’s proposal does not require a political union in the sense of a federal state with centralized fiscal authority—the absence of which precludes a genuine BRICS common currency (Siddiqui, 2016).

What it enables instead is an intergovernmental clearing mechanism governing the debts between surplus and deficit countries. In the contemporary context, the surplus countries would likely be occupied by China and certain oil-producing states, while deficit nations of the Global South would constitute the other side.

Keynes’s vision included a radical mechanism for addressing chronic and exploitative imbalances. At the point where accumulated surpluses came to be deemed exploitative—where a dominant surplus country’s position had been achieved at the expense of dependent trading partners—those accumulated claims could be written down, with the debts of dependent countries effectively erased. Keynes had in mind, of course, the prospective dominance of the US and the subordination of post-imperial Britain. He foresaw that the postwar order being constructed by the US was designed to dismantle the British imperial preference system, secure a loan that would prevent early devaluation of an overvalued sterling, and structure international markets under US political domination. The IMF and World Bank, in this analysis, would become instruments of that domination—imposing austerity and anti-labour policies on debtor nations while preventing the development of autonomous capacity, particularly in food production, that might reduce dependence on the US (Siddiqui, 2023c).

The contemporary conjuncture presents a paradoxical opportunity. The Trump administration’s expansive use of sanctions, ostensibly designed to isolate China, Russia, and other target nations, has had the unintended effect of isolating the US itself. By weaponizing the dollar-based financial system, US policy has incentivized the very diversification it seeks to prevent, creating space for what might be termed the “global majority”—the constellation of nations outside the immediate US orbit—to construct alternatives.

The philosophical foundations of such an alternative could draw upon classical political economy’s aspiration to free markets from exploitation, particularly exploitation in the form of economic rent. This includes not only land rent, the classical focus, but also monopoly rent and, most critically for present purposes, financial rent. The exorbitant privilege of the dollar is, at its core, a form of financial rent extracted by the US from the rest of the world economy. An alternative order would seek to eliminate such unearned advantages.

Here China’s experience offers both instruction and caution. China’s signal advantage has been its treatment of money creation and banking as a public utility rather than as a domain for private enrichment. This institutional choice has enabled China to resist the financialisation of industry that has deindustrialised the US and EU economies. By maintaining the subordination of finance to productive investment, China has preserved industrial capacity that its Western competitors have lost.

The path to a post-hegemonic monetary order thus requires more than the construction of alternative institutions. It requires confronting the internal contradictions within each potential pole of a multipolar system—China’s incomplete reforms, EU’s fiscal fragmentation, the Global South’s dependency legacies—while simultaneously resisting the gravitational pull of the still-dominant dollar system. Whether the bancor vision can be realized in the twenty-first century depends not only on the strategic choices of states but on the resolution of these deeper structural tensions.

IX. Conclusion

The era of unchallenged US dollar dominance is ending—not through sudden collapse, but a multifaceted unravelling. The dollar’s exorbitant privilege has become systemic fragility. US debt exceeds $38 trillion, growing at seven percent annually, while its creditor base fragments. Japan and China—once reliable Treasury anchors—have been joined by EU with only transactional loyalties. The dollar’s reserve share has fallen to 57.4 percent, the lowest in three decades, and extrapolation places it below 50 percent by 2034 (Siddiqui, 2025d).

That future is not inevitable. The US dollar retains formidable structural advantages: deep and liquid markets, powerful network effects, and the absence of a coordinated alternative. Still, the trajectory is unmistakable. The unravelling is already underway. The question is no longer whether the old order will give way, but what will replace it—and whether the new order can transcend the extraction, asymmetry, and exploitation that defined the old.

Yet the crisis is qualitative too. The 1971 Nixon shock allowed devaluation and enhancement simultaneously; today offers no such alchemy. When BRICS nations accumulate gold, develop alternative payments, and explore Keynesian clearing mechanisms. The weaponization of sanctions after Russia’s 2022 invasion accelerated this shift, incentivizing the de-dollarization the US fears most. (Siddiqui, 2024b).

Domestically, US policy compounds these pressures. Military Keynesianism substitutes weapons for productive investment. Tariff policy risks shrinking global demand. Having lost capacity to export capital for allies’ development, the US now covets their resources directly—Greenland’s minerals, Canada’s land—revealing the extractive logic beneath partnership rhetoric.

Mark Carney crystallizes this moment. When Canadian Prime Minister acknowledges the “rules-based order” was partially fictitious and the “bargain no longer works,” the ideological scaffolding crumbles. This is not a transition but a breakdown, precipitated by US unilateralism turned against traditional allies.

The study concludes that for the Global South, this juncture presents both peril and possibility: the risk of being crushed between a declining hegemon and an emergent multipolar order not yet capable of stability—or the opportunity to carve out space for genuine sovereignty. Learning from the past is essential. Unlike the postwar order, in which a single currency dominated international finance and trade, the future must be genuinely multipolar—where no single currency holds monopoly power, and where a group of currencies from large emerging economies can coexist and compete. The Keynesian vision of an International Clearing Union in which no currency enjoys exorbitant privilege, and the monetary order serves development rather than extraction.

About the Author

Dr. Kalim Siddiqui is an economist specializing in International Political Economy, Development Economics, Trade and Economic Policy. Since 1989, he has been teaching economics at various universities in Norway and the UK. Dr. Siddiqui’s research interests encompass a wide range of topics, including political economy, international trade, and economic history, South Asia, and emerging economies. He has presented papers at international conferences across numerous countries, reflecting his global engagement in the field. His scholarly pursuits span six broad domains: Political Economy, Development Economics, Economic History, Economic Policy, Globalization, and International Trade. Dr. Siddiqui has made significant contributions to research in areas such as trade policy, globalization, and political economy. His work has been published in chapters of edited books and articles published in peer-reviewed journals. For inquiries, Dr. Siddiqui can be reached at: [email protected]

Dr. Kalim Siddiqui is an economist specializing in International Political Economy, Development Economics, Trade and Economic Policy. Since 1989, he has been teaching economics at various universities in Norway and the UK. Dr. Siddiqui’s research interests encompass a wide range of topics, including political economy, international trade, and economic history, South Asia, and emerging economies. He has presented papers at international conferences across numerous countries, reflecting his global engagement in the field. His scholarly pursuits span six broad domains: Political Economy, Development Economics, Economic History, Economic Policy, Globalization, and International Trade. Dr. Siddiqui has made significant contributions to research in areas such as trade policy, globalization, and political economy. His work has been published in chapters of edited books and articles published in peer-reviewed journals. For inquiries, Dr. Siddiqui can be reached at: [email protected]

References

- Palley, T., Caldentey E.P., and Vernengo, M. (Eds.) (2024) Dollar Hegemony: Past, Present, and Future, London: Edward Elgar Publishing.

- Siddiqui, K. (2026a) “The US, the Petrodollar, and Multipolarity: Strategic Intervention in an Age of Monetary Decline” World Financial Review, January.

- Siddiqui, K. (2026b) “Monopoly Capitalism and the Concentration of Capital in Production and Digital Technology”, World Financial Review, January.

- Siddiqui, K. (2025a) “The US’ Future in an Imperial Mirror: Lessons from Britain, Spain, Abbasids, Rome, and Beyond” World Financial Review, November.

- Siddiqui, K. (2025b) “Reconfiguring US Hegemony: Militarism, Empire, and the Crisis of Capitalist Accumulation” World Financial Review, August.

- Siddiqui, K. (2025c) “The Rise of Asian Economies and Implications for the Global Economy” World Financial Review, June.

- Siddiqui, K. (2025d) “The Reasons Behind the Decline of the US Economy” World Financial Review, May.

- Siddiqui, K. (2024a) “The BRICS Expansion and the End of Western Economic and Geopolitical Dominance” World Financial Review, November.

- Siddiqui, K. (2024b) “Trends and Prospects of De-Dollarization in the Rapidly Changing Global Economy” (Part 1 & Part 2), World Financial Review, December.

- Siddiqui, K. (2023a). “De-dollarisation, Currency Wars, and the End of US Dollar Hegemony” World Financial Review, August/September.

- Siddiqui, K. (2023b) “Marxian Analysis of Capitalism and Crises” International Critical Thought 13(4): 525-545.

- Siddiqui, K. (2023c). “The New Cold War: Struggle for Global Domination” (Part I & Part 2) World Financial Review, July & August.

- Siddiqui, K. (2020). “The US Dollar and the World Economy: A critical review” Athens Journal of Economics and Business, 6(1):21-44.

- Siddiqui, K. (2018). “Imperialism and Global Inequality: A Critical Analysis” Journal of Economics and Political Economy, 5(2):266-291.

- Siddiqui, K. (2016). “Will the Growth of the BRICs Cause a Shift in the Global Balance of Economic Power in the 21st Century?” International Journal of Political Economy 45(4):315-338.

- Siddiqui, K. (1994) “World Bank: 50 Years of neo-liberalism and Diktat”, The Nation, September 5 & 6.

- The Guardian (2026) “The dollar is losing credibility’: why central banks are scrambling for gold”, 16th January, London.

- Vasudevan, R. (2008) “Finance, Imperialism, and the Hegemony of the Dollar”, Monthly Review 59(11):35-50, New York.

")

{kind=link}