College tuition keeps sprinting ahead of everyday prices. According to EducationData.org, published tuition has climbed about 3.9 percent a year since 2000—roughly forty percent faster than overall inflation. Leave college money in a plain savings account, and it falls behind.

The good news: you can outpace costs. In the guide that follows, we unpack the highest-impact inflation fighters, show you how to layer them by time horizon, and reveal the small tweaks that turn today’s planning into tomorrow’s tuition.

How we ranked the tools

You need a clear playbook, not a guessing game. We graded each option on five yardsticks:

- Inflation power: how reliably the tool keeps pace with college-cost inflation

- Safety: risk of losing principal

- Liquidity: how quickly you can tap the money when tuition is due

- Tax efficiency: federal or state breaks that boost net return

- Ease of use: account setup and ongoing upkeep

To keep the focus where it belongs, we weighted the factors as follows: inflation power 40 percent, safety 25 percent, liquidity 15 percent, tax perks 10 percent, and convenience 10 percent. Each tool earned a one-to-five score in every category, and the weighted totals produced the final ranking.

The outcome is a practical pecking order you can plug into real numbers instead of guessing.

Bright Start 529’s 529 College Savings Calculator lets you enter your child’s age, college preference, and a proposed monthly deposit.

Using roughly 5 percent annual tuition inflation and a 6 percent investment return—figures drawn from recent College Board data—the tool projects what share of future costs that contribution could cover.

You see which moves deliver the biggest inflation punch first and which work better as supporting players, so every step you take feels both logical and confident.

Quick comparison at a glance

The table below scores each strategy on the five yardsticks using a one-to-five scale (five is best, one is worst).

| Tool | Inflation hedge (1–5) | Risk level (1–5) | Liquidity (1–5) | Tax benefits (1–5) | Best use case |

| Series I savings bonds | 5 | 5 | 2 | 4 | Mid-term safety with CPI-linked growth |

| Prepaid tuition plans | 4 | 5 | 1 | 4 | Lock in future in-state tuition today |

| TIPS inside a 529 | 4 | 4 | 3 | 5 | Protect the bond slice of your plan |

| Stock allocation tweaks | 4 | 2 | 5 | 5 | Long runway growth to beat tuition |

| High-yield savings | 3 | 5 | 5 | 2 | Money needed in the next one to two years |

| 529-to-Roth flexibility | 3 | 3 | 3 | 5 | Backup plan for unused 529 funds |

| Inflation-indexed contributions | 3 | 5 (behavioral) | 5 | 1 | Keep pace when costs jump |

1. Series I savings bonds: your inflation-linked shock absorber

When inflation jumps, most assets race to catch up. Series I savings bonds rise in tandem with the Consumer Price Index, so real value stays intact even when stocks or nominal bonds sag. The composite rate resets every May 1 and November 1, combining a fixed rate with the latest CPI reading. For bonds issued November 2025 to April 2026, the composite rate is 4.03 percent, while the fixed portion (0.90 percent) keeps earning even if inflation cools.

Why we rank them first

- Inflation guarantee. Each CPI uptick lifts your principal, preserving purchasing power.

- Treasury-backed safety. Your money carries the full faith of the United States government.

- Tax perks. Interest is state tax-free and can be federally tax-free if the bonds are redeemed for qualified higher-education costs and your modified AGI falls below the IRS phase-out (198,800–228,800 dollars for married filing jointly in 2025). Cash out, then roll the proceeds into a 529 plan within 60 days to keep the interest sheltered.

Key rules to know

- Minimum holding period: 12 months

- Cash out before five years: forfeit the last three months of interest

- Purchase cap: 10,000 dollars per Social Security number each calendar year electronically, plus up to 5,000 dollars in paper bonds through your tax refund

Action step: Open a free TreasuryDirect account and schedule automatic purchases each January. Buying bonds three to five years in a row builds an inflation-proof pool of cash for sophomore and junior-year tuition, without market-risk headaches.

2. Prepaid tuition plans: lock tomorrow’s price today

Think of a prepaid plan as inflation insurance on tuition. You buy semesters at today’s price, and the program absorbs every increase until enrollment. If tuition climbs five percent a year, a four-year contract can deliver a 27 percent real return over eight years without touching the stock market.

How the promise works

- Your contract is backed by the sponsoring state or the Private College 529 network.

- The plan redeems credits at whatever in-state tuition costs when your child enrolls, whether that is 30 percent or 100 percent higher.

- If your student goes elsewhere, most plans pay the average in-state rate or refund your contributions with modest growth.

Where you can still enroll in 2025

Florida, Maryland, Massachusetts, Michigan, Mississippi, Nevada, Pennsylvania, Texas, and Washington remain open to new investors. Other states run legacy programs but no longer accept fresh money.

Taxes and funding risk

Earnings grow tax-deferred and come out tax-free when used for tuition, just like a 529 savings plan. Before you sign, read the plan’s latest actuarial report. Well-funded programs (Florida is more than 100 percent funded) pose less risk than those with gaps.

Smart combo play

Use a prepaid contract to lock tuition, then save for room and board in a traditional 529. The pairing shields you from runaway costs yet keeps flexibility for housing, books, or an unexpected college pivot.

3. TIPS inside your 529: inflation insurance wrapped in a tax shelter

Treasury inflation-protected securities, or TIPS, are U.S. bonds whose principal rises with the Consumer Price Index. If inflation hits four percent, a 1,000-dollar TIPS grows to 1,040 dollars and the next interest check lands on that larger amount. Hold the same security inside a 529 plan and every CPI adjustment compounds tax-free, creating a double shield.

Mind the tuition gap. Over the past decade, private-college prices beat CPI by 1.9 percentage points a year and public in-state tuition by 2.2 points. TIPS may not close that entire spread, but they protect the conservative bucket far better than cash or nominal bonds.

How to add them

- About 30 of the 52 major 529 plans now offer an “inflation-protected” portfolio; a quick switch in your dashboard does the job.

- If your plan lacks one, a low-cost TIPS ETF in a taxable account is another path, though you will owe tax on the yearly CPI adjustments, sometimes called phantom income.

Placement strategy

Increase TIPS weight as college approaches. A sample glide path could shift from 10 percent TIPS at age 10 to 40 percent by freshman year, smoothing volatility while still earning a modest real yield. In late 2025, the five-year TIPS real yield hovered near 1.8 percent above CPI. Growth assets lift the load early; TIPS hold the ground they gain.

Result: a steadier ride and a bond sleeve that does not quietly deflate when prices surge.

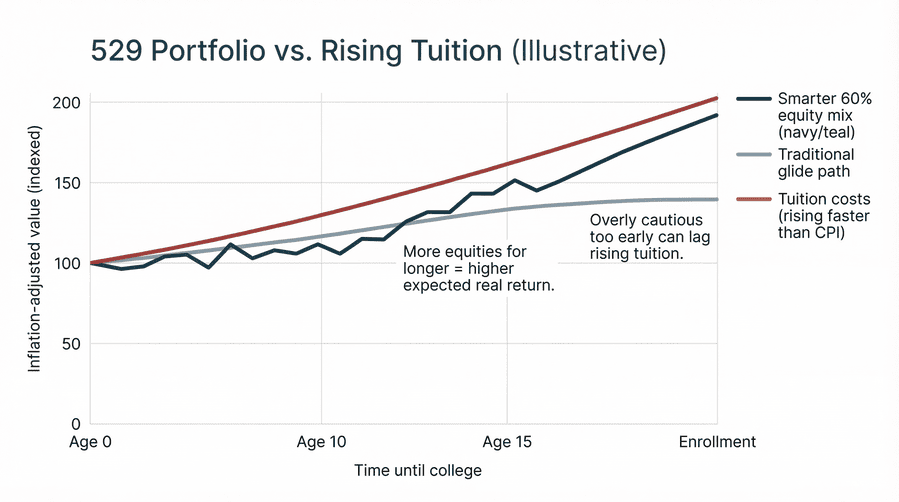

4. Keep growth alive with a smarter stock mix

Inflation does its worst damage over decades, not months, and equities remain the only asset class with a proven long-run edge. From 1926 through 2023, the S&P 500 delivered an average real return of seven percent a year after inflation, according to an analysis by Dimensional Fund Advisors. Leave stocks too early and tuition growth can outrun your portfolio.

Right-size the timeline

- Ages 0–12: An equity-heavy 529 (about eighty to one hundred percent stocks) gives contributions time to rebound from inevitable dips.

- High-school years: Many age-based glides drop to thirty percent stocks by age fifteen. Independent research from Gatewood Wealth Solutions suggests a steadier path—around 60 percent equities until senior year—maintains more purchasing power without a notable jump in volatility.

Build a diversified equity sleeve

Balance large-cap United States funds, international shares, and a dash of real-estate or natural-resource exposure. These segments often zig when others zag during inflationary spurts, giving returns multiple engines.

Stage your withdrawals

Tuition arrives over four years. Pay freshman bills from bonds and cash while letting junior-year money stay in stocks to recover. This layered approach keeps the growth engine running even after the acceptance letter lands.

Result: a college fund that races alongside rising costs instead of trailing them.

5. Park near-term cash in high-yield savings

When college is less than two years away, preservation beats growth. A sudden market dip right before tuition is a risk you can skip. High-yield savings accounts (HYSAs) and money-market funds solve that problem.

Online banks paid 4.5 to 5.1 percent APY in December 2025, roughly ten times the national savings average of 0.39 percent reported by the Federal Deposit Insurance Corporation. At that yield, cash nearly matches today’s three to four percent inflation and stays accessible any morning you need it.

Rates float, so if the Federal Reserve cuts aggressively, yields can fall. Check your HYSA each quarter and be ready to move cash or shift money into your 529’s stable-value option if returns lag inflation.

Rule of thumb: Move one semester’s projected cost into cash each spring of high school, then refill from your 529 as terms pass. You lock in certainty, dodge sequence-of-return risk, and still earn a modest real return.

Tax tip: Interest in a taxable HYSA counts as income. If your 529 offers a money-market portfolio yielding within half a point of your bank, keeping short-term funds inside the plan preserves the tax break.

6. Give your savings a cost-of-learning raise

Colleges raise prices almost every year. In the 2025–26 cycle, published tuition climbed 2.9 percent at public four-year schools and 4.0 percent at private nonprofits before inflation, according to the College Board. If your 529 contribution stays flat, you fall behind.

Treat your deposit like a paycheck and give it an annual raise. Suppose you save 400 dollars a month and boost that amount by the same three to four percent many colleges just posted. After ten years, you would put in about 5,700 dollars more in nominal terms yet end up with roughly ten percent greater real buying power because each raise compounds on the last.

Most plans let you pre-schedule percentage bumps every January. If yours does not, sync the change with your own raise or bonus: the day new money hits your paycheck, redirect a slice to the 529. Matching tuition’s pace year after year turns inflation from a lurking threat into just another line item you have already handled.

Quick check: some 529s allow only two allocation or contribution changes per calendar year. Verify your plan’s rules so your raise goes through without a hitch.

7. Turn leftover 529 dollars into a Roth retirement jump-start

Worried about over-saving? SECURE 2.0, effective 2024, lets you roll unused 529 money into the beneficiary’s Roth IRA tax- and penalty-free within strict guardrails:

- Fifteen-year rule. The 529 must be at least fifteen years old, and contributions (plus earnings on them) made in the last five years are ineligible.

- Annual cap. Each rollover counts toward the beneficiary’s yearly Roth limit—7,000 dollars for 2025, subject to cost-of-living increases. The beneficiary needs earned income equal to the amount transferred.

- Lifetime cap. Total rollovers cannot exceed 35,000 dollars.

- Income limits do not apply. Even if the beneficiary’s income would normally phase out Roth contributions, the rollover still qualifies.

Why it matters: You can now save boldly, knowing any extra tuition money can power decades of tax-free retirement growth. Parents also retain flexibility, because the original Roth contributions—not the earnings—remain available if tuition overruns the 529.

Key move: Check your 529’s start date. When it turns fifteen, set calendar reminders to transfer up to the Roth limit every January until you reach the 35,000-dollar lifetime ceiling or your student’s senior year, whichever comes first.

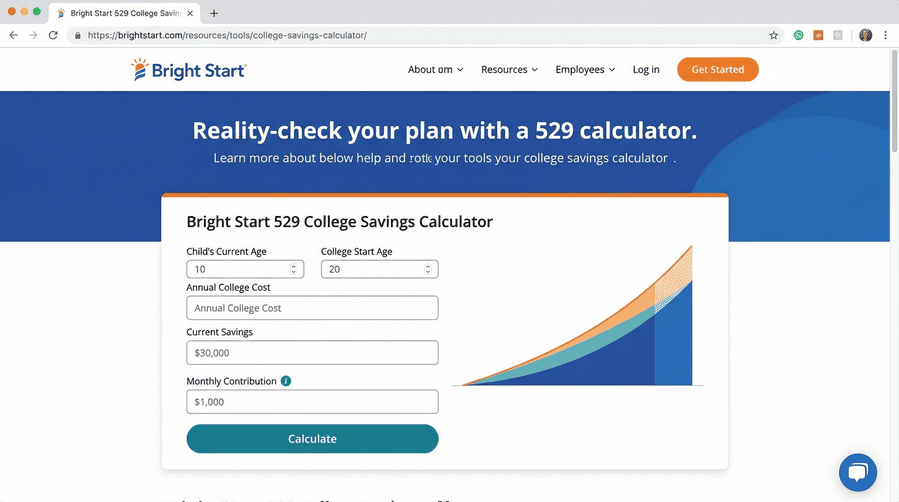

8. Reality-check your plan with a 529 calculator

The smartest portfolio still misses if the target is wrong. A dedicated college-cost calculator shows line by line how inflation will swell your child’s bill and whether today’s savings rate keeps up.

Why most parents are surprised: Fidelity’s annual College Savings Indicator finds that families hope to cover 69 percent of future costs but are on track for only 27 percent.

What to plug in

- Child’s age and college type (public versus private)

- Expected investment return

- Latest published tuition increase (public four-year schools averaged 2.9 percent for 2025–26; private nonprofits, 4.0 percent)

- Special factors such as a gap year, graduate school, or an early payoff plan

Run “what-ifs” for higher inflation, lower returns, or a scholarship windfall, then adjust your monthly transfer before the shortfall hurts.

Treat the calculator like an annual check-up. Update each spring; if rising prices or weak markets open a gap, boost deposits, add I bonds, or tweak your glide path. Data replaces guesswork and keeps every other strategy in proper proportion.

Common pitfalls and easy ways around them

Even with the right tools, families often stumble on a few repeatable mistakes. Dodge them early and your inflation shield stays intact.

- Waiting for “extra” money to fund a 529. Inflation never pauses. Starting fifty dollars a month today beats five hundred dollars a year from now once compounding and rising tuition kick in.

- Treating the age-based glide path as set and forget. Plans rely on averages, not your child’s exact start date. Review the mix each spring; adjust if the equity share feels too timid or too bold.

- Parking big balances in cash years before college. Cash loses roughly three to four percent of purchasing power in a typical inflation year. Keep only the next twenty-four months of expenses in a high-yield account; invest the rest.

- Ignoring state tax perks. Thirty-four states, plus Washington, DC, offer a deduction or credit for 529 contributions. Skipping it is like leaving a small scholarship on the table.

- Thinking calculators are one and done. Update figures annually. If tuition jumps or returns lag, a quick recalculation exposes the gap while the fix is still painless.

Your action checklist

- Buy this year’s I bonds. Open (or sign in to) TreasuryDirect and schedule up to 10,000 dollars per person before December 31.

- Compare prepaid options. In one sitting, check your state plan or the Private College 529 network to see if locking tuition now fits your child’s likely path.

- Review your 529 allocation. If you have less than ten to fifteen percent in an inflation-protected option (TIPS fund), shift that slice today.

- Run a fresh calculator check. Feed in the latest College Board tuition-inflation figure, then raise your auto-contribution to the new target. Schedule this recalculation every April.

- Fund next-year cash. Set a calendar alert to move one semester of costs into a high-yield savings or 529 money-market twelve months before each bill.

- Plan Roth rollovers. Note your 529’s opening date; once it turns fifteen years old, move up to the annual Roth limit (7,000 dollars for 2025) each January until you reach the 35,000-dollar lifetime cap.

- Give deposits a raise. Every January 1, increase your monthly contribution by last year’s published tuition-inflation rate (see the College Board’s Trends in College Pricing report).

A clear seven-step roadmap turns high-inflation college planning into a manageable to-do list

Work through the list in order; each action strengthens the next, creating a layered defense against rising college costs.

Disclaimer: This article contains sponsored marketing content. It is intended for promotional purposes and should not be considered as an endorsement or recommendation by our website. Readers are encouraged to conduct their own research and exercise their own judgment before making any decisions based on the information provided in this article.

{kind=link}