A strategic framework for integrating digital assets through custody, governance, and sustainability

This article proposes a six-pillar framework for private banks to govern digital assets responsibly. By combining custody, compliance, allocation, insurance, governance, and sustainability, the model extends Switzerland’s legacy of trust into the digital era—showing how institutions can embrace innovation without compromising prudence or reputation.

Introduction

Wealth has always sought protection. In the twentieth century, Switzerland became the trusted guardian of global fortunes by mastering two arts: discretion and governance. The vaults of Zurich and Geneva were more than steel and stone—they embodied continuity, stewardship, and the promise that wealth could be preserved across generations.

Today, that legacy now faces a new frontier. Digital assets—cryptocurrencies, tokenized securities, and blockchain-based wealth—have moved beyond speculation. They are emerging as the preferred instruments of entrepreneurs, millennials, and the heirs of tomorrow. By 2030, as much as one-fifth of next-generation wealth could be allocated to digital assets. This reflects broader shifts highlighted in the World Economic Forum’s Future of Wealth and Sustainability initiatives, which stress that next-generation investors expect digital assets to be integrated with impact and responsibility.

For this generation, wealth is not only financial — it is purpose-driven. They expect their capital to be managed responsibly, aligned with sustainability, and governed with the same rigour that built Switzerland’s reputation for trust.

The challenge for private banks is therefore not whether to embrace digital assets — clients already do — but how to govern them in ways that preserve trust while advancing broader goals of responsibility and sustainability.

This paper proposes a framework—Crypto Vault & Governance—built on six strategic pillars that enable private banks to integrate digital assets securely, prudently, and in line with their long-standing DNA of stewardship. The vision is clear: Switzerland once built the world’s most trusted vaults for gold and securities. The new Swiss vault must be digital— forged not only of governance and discretion, but also of sustainability and purpose.

Part I: The Strategic Opportunity

A silent generational revolution is reshaping private banking. Wealth is shifting into the hands of digital natives who view Bitcoin and tokenized assets not as speculation, but as inheritance. More than half of wealthy millennials already hold digital assets, and they expect their banks to provide custody, advice, and governance alongside traditional portfolios. For them, crypto is not an alternative— is it part of the core narrative of wealth, alongside sustainability and purpose.

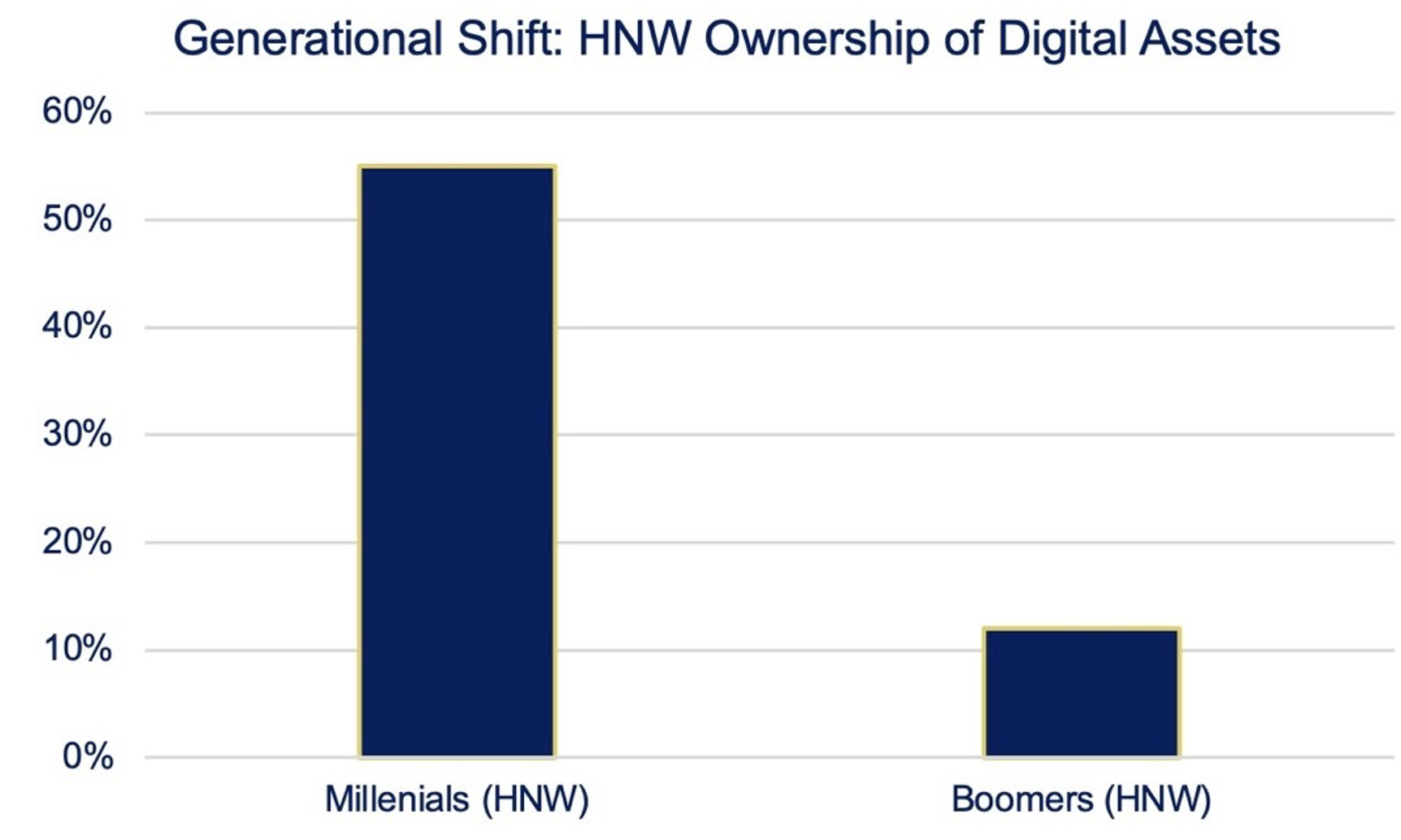

Figure 1: Generational Shift: More than half of HNW millennials (55%) already hold digital assets, compared to barely one in ten boomers (12%). This highlights a profound shift in expectations: younger clients demand integration of digital assets with both traditional portfolios and impact-oriented strategies.

The competitive landscape, however, remains fragmented. Institutions such as DBS in Singapore or Fidelity in the U.S. have launched custody and tokenization platforms, but these efforts are still narrow in scope. In Switzerland, the heartland of private banking, no traditional pure-play private bank has yet delivered a fully institutional, endto-end solution.

This creates both a risk and an opening. The risk is stark: to lose relevance with the very clients who will define the next century of private banking. But the opportunity is equally clear: to become the trusted architect of integrated wealth—traditional and digital, financial and sustainable, present and intergenerational. For the World Economic Forum community, this is not simply about market leadership, but about shaping a financial system where innovation and sustainability advance together.

Part II: The Barriers That Hold Back Private Banks

If the opportunity is compelling, the challenges are equally undeniable. Digital assets do not fit neatly onto a shelf of offerings—they reshape the blueprint of private banking and call for responsible innovation.

- Volatility underscores the importance of disciplined allocation frameworks and transparent risk management.

- Security risks—hacks, fraud, and irreversible transactions—highlight the need for institutional-grade custody, resilience, and collaboration with the cybersecurity sector.

- Regulation and compliance— from KYC and AML to tax reporting—remain complex and evolving, requiring proactive alignment with emerging global standards. As the World Economic Forum’s Global Risks Report 2024 notes, digital assets exemplify the dual challenge of innovation and trust, requiring coordinated governance.

- Reputation risk reminds institutions that trust must be at the centre of digital wealth integration, reinforced by transparency and sustainability principles.

- Infrastructure immaturity signals the urgency of establishing global standards for custody, reporting, and valuation, turning today’s fragmentation into tomorrow’s harmonisation.

It is no surprise, then, that most private banks have remain cautious, often standing as observers rather than actors. But caution is not a strategy. Leadership requires building models that transform these challenges into structured governance — demonstrating that innovation and sustainability can reinforce, rather than undermine, trust.

Part III: The Six Pillars of the New Swiss Vault

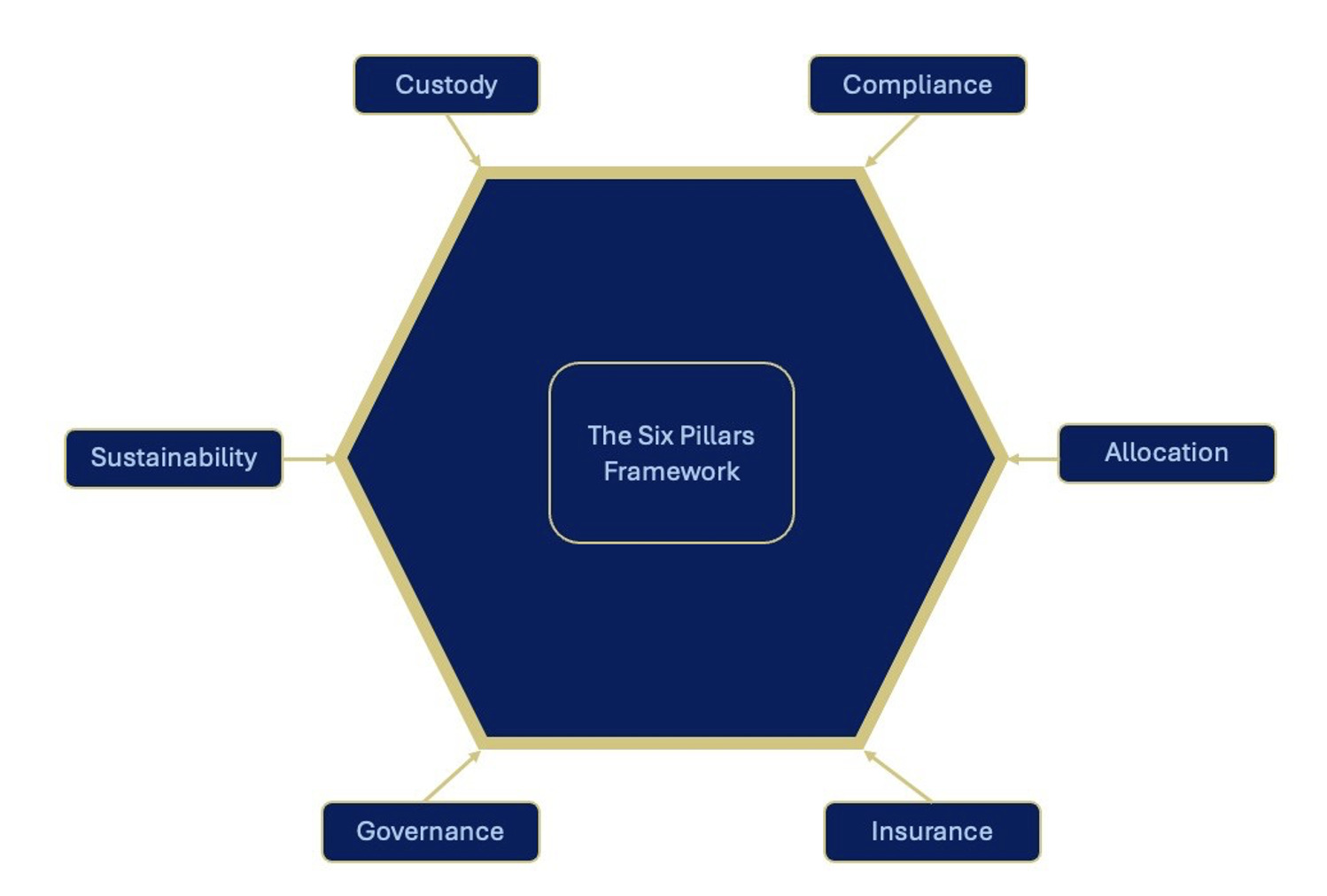

To integrate digital assets without losing trust, private banks must construct a system as rigorous as the vaults that once made Switzerland a synonym for safety. This rests on six strategic pillars:

Figure 2: The Six Pillars Framework: A governance-driven architecture that extends Switzerland’s tradition of trust into the era of digital wealth, while aligning innovation with responsibility and sustainability.

1. Institutional Custody & Multi-Signature Safeguards

Wealth cannot rest on fragile infrastructure. Custody must combine cold-wallet storage, multi-signature protocols, and independent verification. It should be auditable, insurable, and built to institutional standards— the digital equivalent of Switzerland’s most trusted vaults.

2. Integrated Compliance by Design

Trust begins with legitimacy. Every asset must be screened for origin, legality, and tax impact. Automated blockchain analytics, anchored in rigorous compliance protocols, act as a filter—ensuring that only clean and transparent assets enter the vault.

3. Prudent Allocation: The Crypto Bucket

For today’s private banks, the question is not whether clients hold digital assets—they already do. The strategic task is to integrate them into a disciplined allocation framework. Depending on client profile, this may mean 5-10% of total wealth, managed with full transparency on performance, correlation, and risk. Digital assets must be treated with the same discipline as equities or bonds, not as speculative sidelines.

4. Insurance & Risk Hedging

Trust is built on guarantees. While volatility has created some of the largest fortunes in digital assets, the mandate of a private bank is different: to preserve and govern wealth. Institutional insurance against hacks and fraud, coupled with structured hedging instruments, allows clients to benefit from upside exposure while ensuring that downside risks are contained.

5. Governance & Succession

Wealth is not just money—it is continuity. Multi-signature arrangements that involve heirs or trustees, integration of digital assets into family governance structures, and targeted education for clients all ensure that crypto holdings can be transferred and inherited rather than lost or forgotten.

6. Sustainability by Design

Private banks cannot ignore their broader responsibility. The vault of the future must prioritize proof-of-stake and energy-efficient protocols, while also channelling capital into tokenized sustainable assets— from renewable energy projects and biodiversity finance to blockchain-enabled carbon markets and green bonds. In this way, digital wealth becomes fully aligned with the evolving purpose of global finance: to accelerate the transition to a net-zero economy and ensure that wealth creation is consistent with planetary stewardship.

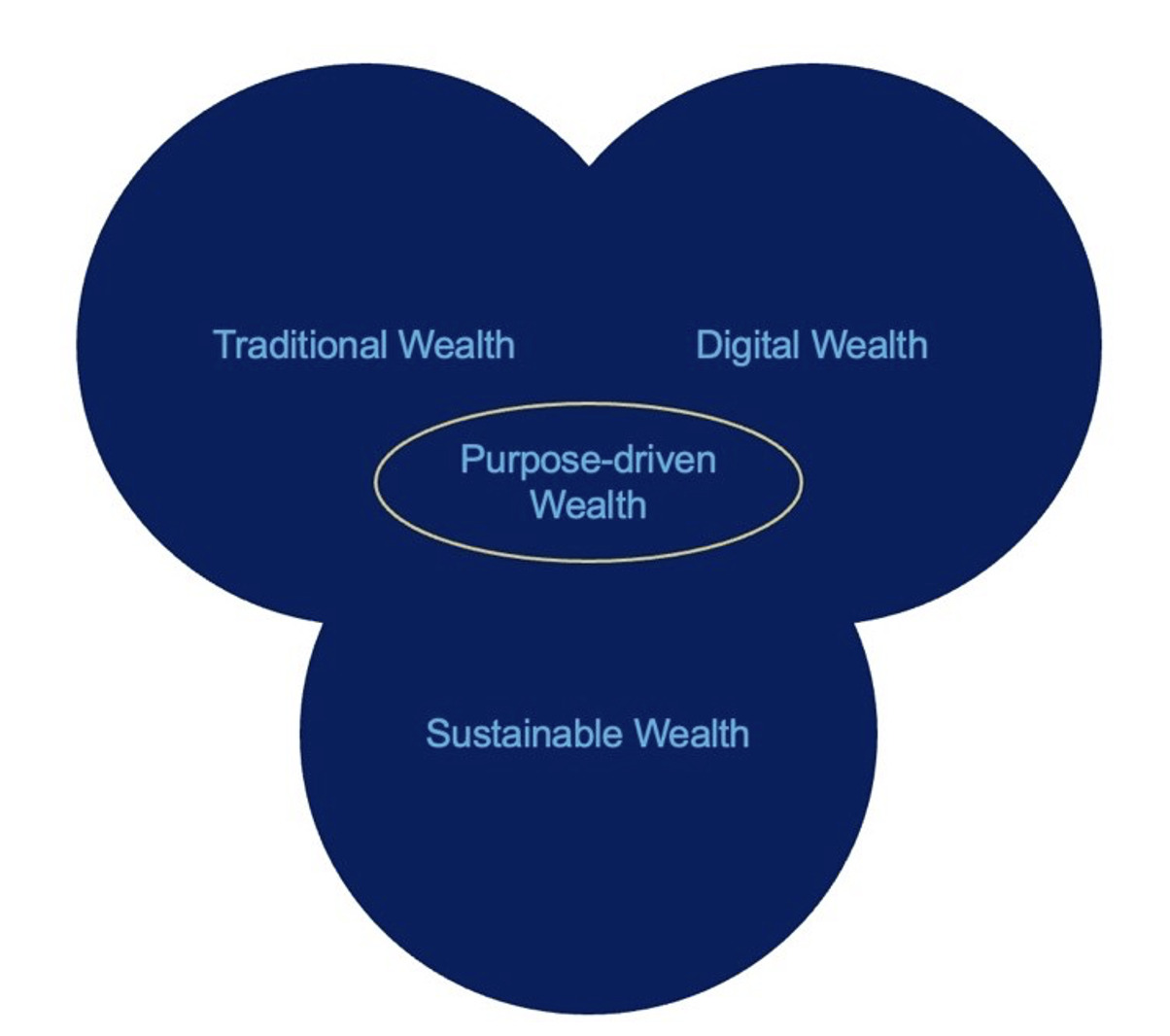

Figure 3: Aligning Wealth: Integrating traditional, digital, and sustainable assets into a unified architecture of trust. Source: Author, inspired by WEF Global Risks Report 2024.

Together, these six pillars create a closed architecture: secure, compliant, prudent, insurable, governed, and sustainable — a model where innovation strengthens trust, and finance contributes directly to long-term resilience.

Part IV: Strategic Advantages for the Bank

Building the New Swiss Vault is not a technical choice—it is a strategic act of positioning. By adopting this framework, private and wealth managers globally can:

- Claim leadership in responsible innovation, integrating digital assets within a comprehensive framework of custody, compliance, governance, and sustainability — and setting a standard for how financial institutions can extend traditions of trust into the digital age.

- Attract and retain the next generation of clients, while deepening confidence among existing UHNW families by demonstrating that digital wealth can be governed with prudence and continuity.

- Reinforce the identity of private banking as a house of governance and stewardship, proving that innovation and discretion are not opposites but complementary strengths.

- Transform sustainability into a differentiator, extending its leadership into the digital realm and turning crypto from a reputational risk into a reputational asset — contributing to the broader alignment of global wealth with net-zero and purpose-driven finance.

Conclusion: Trust as Strategy

The future of wealth will not be defined by whether clients own digital assets — that reality is already here. It will be defined by whether financial institutions can govern them responsibly, sustainably, and inclusively.

The Crypto Vault & Governance framework is more than a safeguard; it is a blueprint for resilience. By embedding digital assets within the same principles that forged Switzerland’s reputation — prudence, governance, and long-term stewardship — private banks and wealth managers can carry their relevance into the digital century.

Trust has always been the defining currency of private banking. In the era of digital wealth, it must also serve as a compass, guiding innovation toward responsibility and sustainability.

The institutions that embrace this mandate will do more than preserve fortunes. They will shape a financial system where digital assets reinforce trust, accelerate the transition to a net-zero economy, and align global wealth with the purpose-driven economy of the 21st century. This aligns with the World Economic Forum’s call to ensure that technological innovation contributes directly to long-term resilience and sustainability.

About the Author

Boecyàn Bourgade is a finance and strategy researcher exploring the intersection of wealth management, digital assets, cybersecurity, and AI. Holding a Private Equity Certificate from Wharton and FMVA® specialization in cryptocurrencies and digital assets, the work centers on designing trust and governance frameworks for the emerging algorithmic economy.

Boecyàn Bourgade is a finance and strategy researcher exploring the intersection of wealth management, digital assets, cybersecurity, and AI. Holding a Private Equity Certificate from Wharton and FMVA® specialization in cryptocurrencies and digital assets, the work centers on designing trust and governance frameworks for the emerging algorithmic economy.

References

- Capgemini. World Wealth Report 2023. Capgemini Research Institute.

- Boston Consulting Group (BCG) & ADDX. Relevance of Digital Assets in Wealth Management. 2022.

- Fidelity Digital Assets. Institutional Investor Digital Asset Study 2023. Fidelity Investments.

- PwC & Elwood. 4th Annual Global Crypto Hedge Fund Report 2023.

PricewaterhouseCoopers. - Deloitte. 2023 Global Crypto Banking Survey. Deloitte Insights.

- UBS Group AG. Future of Wealth 2030. UBS Global Wealth Management, 2022.

- World Economic Forum. Global Risks Report 2024. World Economic Forum, Geneva.

- World Economic Forum. Future of Wealth and Sustainability Initiatives. World Economic Forum, Geneva, 2023.

{kind=link}