")

International financial institutions—namely the IMF and the World Bank—serve as instruments of Western financial dominance. Through the enforcement of Structural Adjustment Programs (SAPs) and austerity measures, they facilitate the extraction of wealth from the Global South. Dr. Kalim Siddiqui argues that by imposing debt traps, currency devaluation, trade liberalization, and dollar dependency, these institutions prioritize corporate interests over genuine development, thereby perpetuating neocolonial exploitation. Under the guise of economic reform, they systematically transfer resources from the Global South—home to 84% of the world’s population—to the Global North, exacerbating global inequality.

I. Introduction

The post-World War II economic order, institutionalized at the 1944 Bretton Woods Conference, established the US dollar as the global reserve currency and created the International Monetary Fund (IMF) and the World Bank—key instruments of Western financial hegemony. While these institutions were ostensibly designed to stabilize exchange rates and facilitate postwar reconstruction, they have since evolved into mechanisms that reinforce economic dependency in the Global South.

Much like the British Empire’s reliance on the gold-backed pound sterling in the 19th century, the US has exploited its financial dominance to extract economic surplus from peripheral nations, replacing overt colonialism with structural indebtedness and imposed austerity. Under the Bretton Woods system, global currencies were pegged to the US dollar, which was itself convertible to gold at $35 per ounce. This arrangement effectively subordinated developing countries to US monetary policy. Even after the collapse of the Gold Standard in 1971, the dollar’s hegemony persisted, enabling the US to externalize inflation, enforce sanctions, and dictate credit conditions through the IMF and World Bank.

This paper argues that the IMF and World Bank operate as neocolonial tools, imposing policies that prioritize debt servicing and market liberalization over national sovereignty and sustainable development in the Global South. Through conditional lending, austerity mandates, and dollar-denominated debt traps, these institutions perpetuate the very inequalities and economic crises they claim to mitigate (Siddiqui, 2024a).

Fundamentally, the IMF and World Bank serve as key mechanisms in the perpetuation of global capitalist exploitation. They systematically facilitate the transfer of wealth from the Global South—home to approximately 84% of the world’s population—to the Global North, which comprises less than 16%. This entrenched imbalance reflects a broader global order in which economic policies, development trajectories, and fiscal sovereignty in peripheral nations are subordinated to the interests of international capital, multinational corporations, and Western geopolitical objectives (Chang, 2001).

These international financial institutions have frequently supported authoritarian regimes and controversial interventions, raising serious concerns about their commitment to principles of transparency, neutrality, and democratic accountability (Stiglitz & Tsuda, 2007). A notable example is the IMF’s contentious decision to approve the 2010 Greek loan programme, despite internal reservations and a clear departure from its own lending guidelines (Toussaint, 2023).

Similarly, in Egypt, following the 2013 military coup that ousted democratically elected President Mohamed Morsi and suspended the 2012 constitution, the new regime under General Fattah el-Sisi received substantial financial support from the IMF, as well as from Saudi Arabia and other Gulf States. This case illustrates how IMF assistance can be shaped more by geopolitical alliances than by democratic legitimacy or developmental need (Toussaint, 2023).

The post-1991 transition of the Soviet Union and Eastern European countries toward market economies under IMF and World Bank guidance further exemplifies these issues. Rapid privatisation of public assets enriched former bureaucrats and politically connected elites, or resulted in the sale of national industries to foreign firms. Under President Boris Yeltsin—whose administration was characterized by widespread corruption and growing authoritarianism—the IMF disbursed billions of dollars in loans, primarily to support the regime and maintain political stability and promote neoliberal reforms, despite escalating poverty, rising unemployment, and increasing social and economic dislocation (Siddiqui, 2023a).

The 1997–1998 East Asian financial crisis marked a critical turning point, triggering a major global economic downturn. The crisis pushed approximately 40 percent of the global economy into the most severe recession since the Second World War. Ironically, while East and Southeast Asian economies suffered immense devastation, the US economy experienced a temporary boost. As billions in speculative capital fled collapsing Asian markets, much of it flowed into US financial markets, fuelling a speculative boom on Wall Street and prolonging domestic economic growth. However, this dynamic only reinforced the structural fragility of the global economy, which now rests precariously on what has been termed a “US bubble economy”—increasingly reliant on a volatile and speculative financial sector. The risk of systemic collapse remains significant (Siddiqui, 2021).

II. The US Dollar as Global Reserve Currency: Enforced Dependency

The US dollar functions as the world’s primary reserve currency—a foreign currency held by central banks to stabilize exchange rates, service external debt, and ensure liquidity during crises. Developing economies are forced to maintain dollar reserves to facilitate trade, repay dollar-denominated debts, and guard against balance-of-payments crises. This structural dependency perpetuates a vicious cycle: nations must export raw materials or borrow in dollars to accumulate reserves, further entrenching their subordination to US monetary policy. The US Treasury market, as the deepest and most liquid bond market globally, reinforces this hierarchy by offering “safe” assets while extracting seigniorage profits from the Global South (Toussaint, 2023).

By the 1970, the US no longer held sufficient gold reserves to back the dollars circulating worldwide, risking a collapse of confidence in the system. Then in 1971, President Nixon unilaterally severed the dollar’s convertibility to gold, effectively ending the Bretton Woods fixed-exchange regime. While this shift temporarily devalued the dollar and introduced floating exchange rates, it did not diminish dollar supremacy. Instead, the US forged a new pillar of hegemony i.e. the petrodollar system. Through agreements with Saudi Arabia and other OPEC nations, oil—the world’s most traded commodity—became priced exclusively in US dollars. Oil-importing countries now needed dollar reserves to purchase energy, while oil exporters recycled surplus dollars into US Treasury bonds, further cementing dollar centrality.

III. From Stabilization to Subjugation: The IMF and World Bank’s Role

Though Bretton Woods institutions were ostensibly founded to promote stability and development, their policies have consistently prioritized creditor interests over the sovereignty of debtor nations. Structural Adjustment Programmes (SAPs) – imposed on Global South countries during debt crises – epitomize this dynamic (Siddiqui, 1996). SAPs mandated austerity measures (drastic cuts to public health and education budgets), trade liberalisation (opening markets to subsidized Western goods), and privatisation (transferring state-owned assets to foreign corporations). Framed as “market reforms,” these policies dismantled developmental states, exacerbated inequality, and entrenched borrowing countries in cycles of perpetual debt dependency (Siddiqui, 1994).

The dollar’s central role in global payments amplifies US geopolitical power by enabling unilateral financial sanctions. Nearly all cross-border dollar transactions—even those between non-US entities—are cleared through correspondent banks linked to the Federal Reserve, granting Washington extraterritorial control over global commerce. When the US blacklists a country, it can cut off access to dollar liquidity, effectively paralyzing trade and investment. The 2022 sanctions against Russia illustrate this mechanism: by freezing US$300 billion of Russian central bank reserves and disconnecting Russian banks from SWIFT, the US precipitated sovereign debt defaults and forced Moscow to seek alternative arrangements, such as yuan-rubble trade. This reveals the dollar not as a neutral medium of exchange, but as an instrument of coercion—where exclusion from the dollar system functions as a modern-day naval blockade.

The economic disruptions caused by the COVID-19 pandemic and the Ukraine war have intensified scrutiny of dollar supremacy. BRICS countries (Brazil, Russia, India, China, South Africa)—representing 40% of the world’s population—have openly challenged the dollar’s dominance (Siddiqui, 2025a). At their 2023 summit, members debated a shared currency framework aimed at insulating themselves from the US Federal Reserve-induced volatility and sanctions risks. Meanwhile, China has aggressively promoted the internationalization of the renminbi, leveraging bilateral currency swaps (e.g., with Argentina, Iran, Russia, and Saudi Arabia) and piloting digital yuan settlements. However, structural obstacles remain and the renminbi accounts for just 3% of global reserves, constrained by China’s capital controls and geopolitical tensions (Siddiqui, 2024c).

Concerns over the fragility of dollar dependency are not new. At Bretton Woods, John Maynard Keynes proposed the bancor—a supranational currency backed by a global central bank—to prevent reserve hoarding and the asymmetric burden of economic adjustment. Although this idea was rejected in favour of dollar hegemony, its principles still resonate in contemporary calls to expand the IMF’s Special Drawing Rights (SDRs). SDRs, pegged to a basket of five currencies (dollar, euro, yen, pound, and renminbi), could theoretically diversify reserve holdings and reduce reliance on any single country’s monetary policy. However, SDRs remain a technocratic half-measure and their allocation is politically constrained (for example, the US blocked SDR expansions for Venezuela and Iran), and the IMF’s governance structure—with the US holding veto power—prevents genuine autonomy from the US (Toussaint, 2023).

IV. The Post-Cold War Unipolar World: A Delusion of Control?

Following the Soviet Union’s collapse in 1991, the US emerged as the world’s sole superpower, proclaiming a “unipolar world” of unchallenged dominance. However, this hegemony—rooted in military might, dollar supremacy, and institutional control (IMF, World Bank, NATO)—has proven unsustainable and increasingly contested. Despite its economic and military advantages, the US represents just 4% of the global population (330 million people), yet seeks to impose its political and economic order on the remaining 96%. This imperial overreach, exemplified by the containment of Russia and the growing tensions with China reflect an imperial overreach rooted in outdated Cold War logic.

History demonstrates that power diffusion is inevitable. China’s rise (GDP growth averaging 9% annually since 1990) and earlier East Asian miracles (South Korea, Singapore) (Siddiqui, 2010) prove that rapid catch-up development is possible—despite US efforts to maintain asymmetry through sanctions, trade wars, and financial coercion (Siddiqui, 2025b). A world structured around such stark inequality—where the Global North monopolises capital and institutions—is inherently unstable, fostering resentment, conflict, and systemic crises.

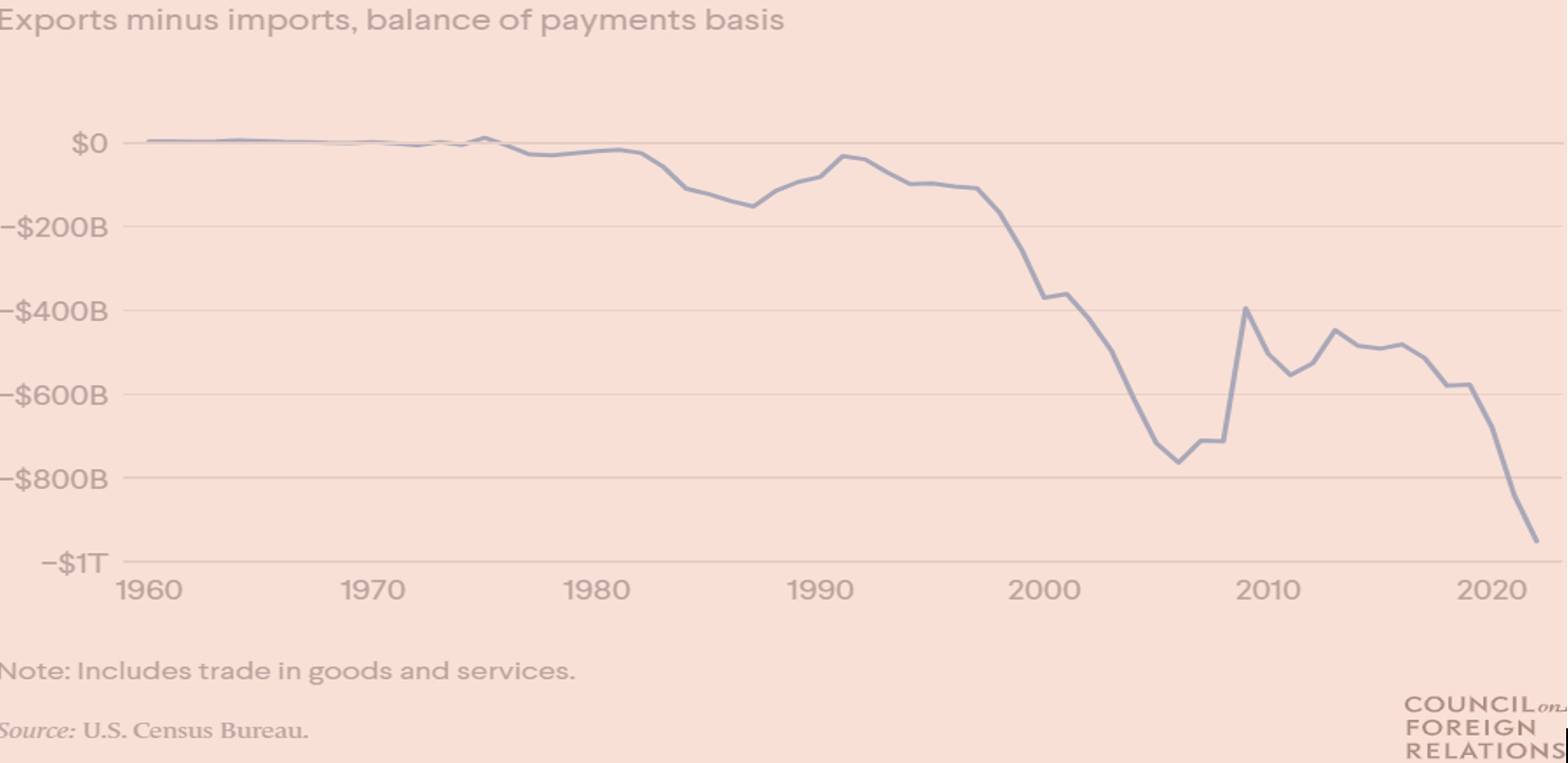

The dollar’s reserve status grants the US unparalleled advantages such as cheap debt; the US borrows at lower interest rates. The US having trade deficits without crisis, while other developing countries face balance-of-payments crises for running deficits, the US exports inflation by flooding markets with dollars. While the dollar’s reserve status grants the US “exorbitant privilege,” it also imposes structural economic distortions. High global demand for dollars artificially strengthens the currency, making US exports more expensive and imports cheaper (Siddiqui, 2020).

This dynamic has fuelled chronic trade deficits, particularly since the 1980s (see Figure 1), as globalisation led to the manufacturing jobs moved overseas. As a result, the US lost 5 million manufacturing jobs (2000-2020). Firms like Apple and Nike exploit strong-dollar arbitrage, producing abroad while booking profits in dollar-denominated assets. “The dollar’s dominance acts like a hidden tax on US exporters, while subsidizing Wall Street’s financialization of the economy.” Joseph Stiglitz, Nobel Economist (Chang, 2001).

Figure 1: The US Trade Balance (1960–2023)

V. Debt as a Weapon: How the IMF and World Bank Enforce Subjugation

The IMF and the World Bank’s macroeconomic policy is based on neoclassical theoretical framework. It involves a process of liberalisation of trade and finance, the creation of opportunities for accumulation through the privatisation and commodification of public goods, the protection of MNCs and foreign direct investments (FDI) (Siddiqui, 2015) and the building of institutions in the Global South a structure of accountability to international financial markets. The IMF and World Bank have institutionalised neocolonial debt traps, turning loans into tools of control and domination (Siddiqui, 2024b).

Developing countries currently owe $2.5 trillion in external debt to Western banks and Bretton Woods institutions (World Bank, 2024). In 2023 alone, debt service payments reached $1.4 trillion, with interest payments surging to $406 billion—funds that could otherwise support healthcare, education, and climate adaptation (UNCTAD, 2025).

These loans come with SAPs that force privatisation, wage suppression, and drastic cuts to social spending. For example, Zambia spends 40% of its government revenue on debt servicing—more than it spends on health and education combined (Jubilee Debt Campaign, 2023). Over 75% of Global South debt is denominated in US dollars, making these countries vulnerable to Federal Reserve interest rate hikes and currency crises.

The debt bondage ensures compliance with US geopolitical interests. For instance, in Venezuela, US sanctions coupled with the IMF’s refusal to restructure debt have crippled the economy. In Sri Lanka, IMF-imposed austerity measures worsened the 2022 economic collapse, sparking widespread protests. In response, some countries are pursuing de-dollarization. China promotes bilateral yuan trade, India advances rupee settlement mechanisms, (Siddiqui, 2023b). and Brazil pushes BRICS currency proposals to reduce dollar dependence.

VI. Debt, Austerity, and the Global South

In fact, over the past four decades the West through the IMF and World Bank have imposed neoliberal reforms (i.e. SAPs) on the developing countries, which had adverse effects on wealth and income distribution and environments (UNCTAD, 2025), especially those who undertook loans from these institutions. Loans were approved only after the acceptance of SAPs, which required the borrower countries privatisation of state-owned enterprises, reduction in social expenditures e.g. healthcare, education, and subsidies to agriculture sector and trade liberalisation, meaning rise of imports. Moreover, loans from IMF are approved only after the agreement to open up natural resources (oil, minerals, agriculture) to Western corporations (Wade, 2001).

This shift coincided with the rise of neoliberal globalization, spearheaded by the US, which aimed to restructure the economies of the Global South. The neoliberal reforms entailed the liberalisation of trade and finance, the privatisation and commodification of public goods, the protection of MNCs and foreign direct investment (FDI), and the establishment of institutional frameworks in developing countries that prioritised accountability to international financial markets over national governments.

In 2023, catastrophic floods in Mozambique displaced over a million people and triggered cholera outbreaks—yet the only $40 million in emergency aid was provided, less than half the $70 million Mozambique pays annually in debt servicing to those same creditors. Decades of IMF-enforced austerity have slashed Mozambique’s health budget to just 1.1% of GDP—a 75% reduction since 2015—leaving the country ill-equipped to handle disease epidemics.

Similarly, Tanzania spends nine times more on debt payments than on healthcare and four times more than on primary education (UNCTAD, 2025). Across sub-Saharan Africa, governments transfer four times more wealth to foreign creditors than they invest in health and education combined—resulting in only half of all children attending school (World Bank, 2023; Muhumed and Gaas, 2016).

In the 1970s, the Global South, led by the Non-Aligned Movement (NAM), demanded a New International Economic Order (NIEO)—a radical restructuring of trade, debt, and technology transfers to redress colonial exploitation. Their demand included: debt cancellation for former colonies, commodity price controls to halt raw material extraction, technology sharing to break MNCs monopoly. But the West sabotaged the NIEO through SAPs replaced sovereign development with austerity.

During the COVID-19 pandemic, the debt burdens of developing countries increased sharply, and the subsequent surge in global interest rates has made it increasingly difficult for many of them to regain financial stability. By 2023, external borrowing had become significantly more expensive for all developing countries and interest rates on loans from official creditors more than doubled, exceeding 4%, while rates from private creditors rose by over a percentage point to reach 6%—the highest level in 15 years.

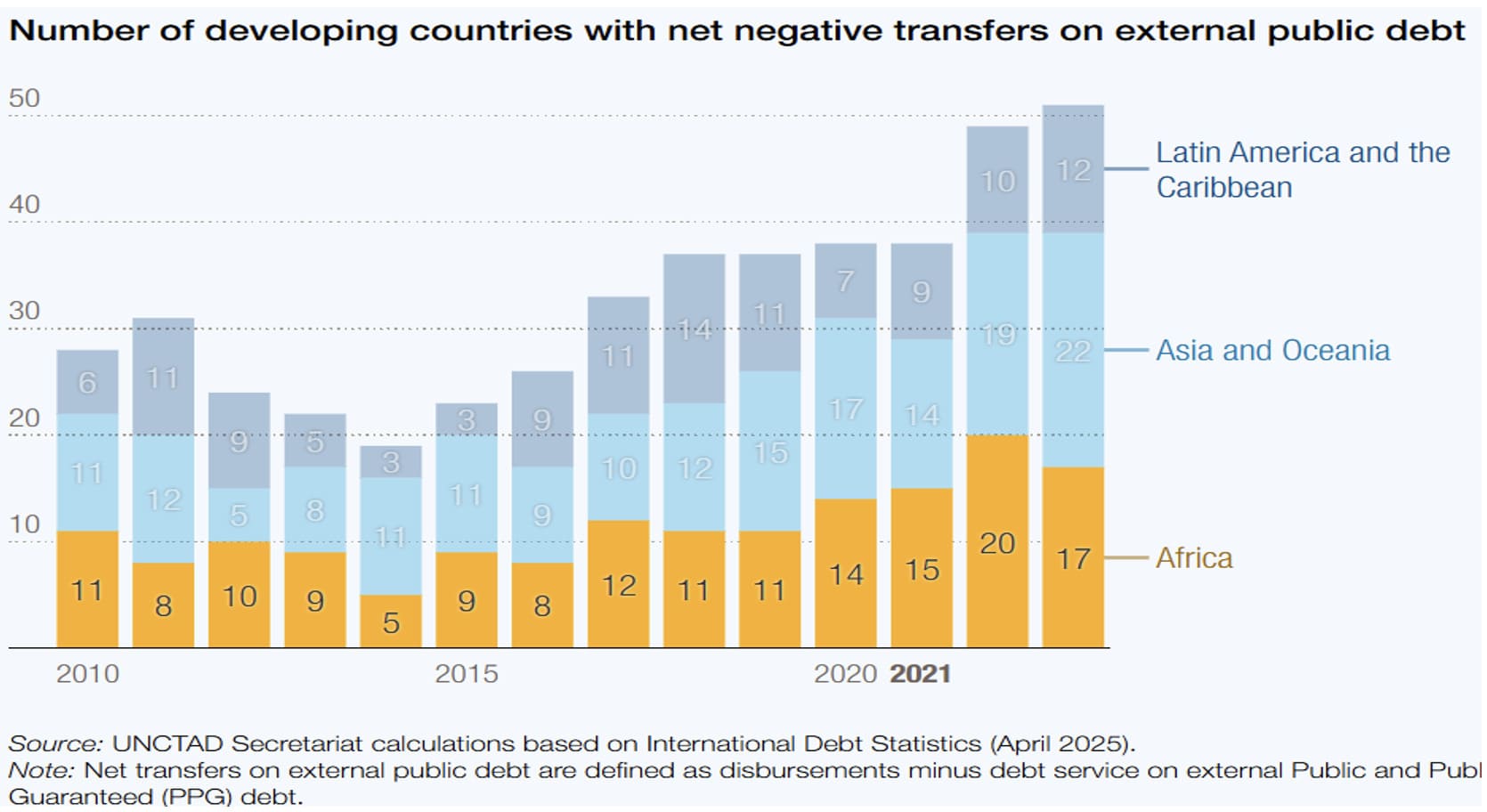

Through the facilitation of capital flows and imposition of neoliberal reforms, the IMF and World Bank enable the extraction of surplus value from the Global South. A substantial net transfer of resources continues to flow from developing countries to external creditors, as illustrated in the Figure 2. In 2023, debt service on external public debt reached $487 billion, highlighting the mounting and unsustainable cost of external borrowing. Half of all developing countries devoted at least 6.5% of their export revenues solely to servicing this debt (Siddiqui, 2024b).

This structural process entrenches the unequal dynamics of the global economy, where the wealth and power of advanced capitalist countries are sustained through the exploitation of developing countries. The role of these financial institutions in maintaining such asymmetries underscores a central radical critique that global capitalism relies on the systematic transfer of value from the periphery to the core (Wade, 2001).

Figure 2: Developing Countries with Net Debt Outflows, 2010–2024.

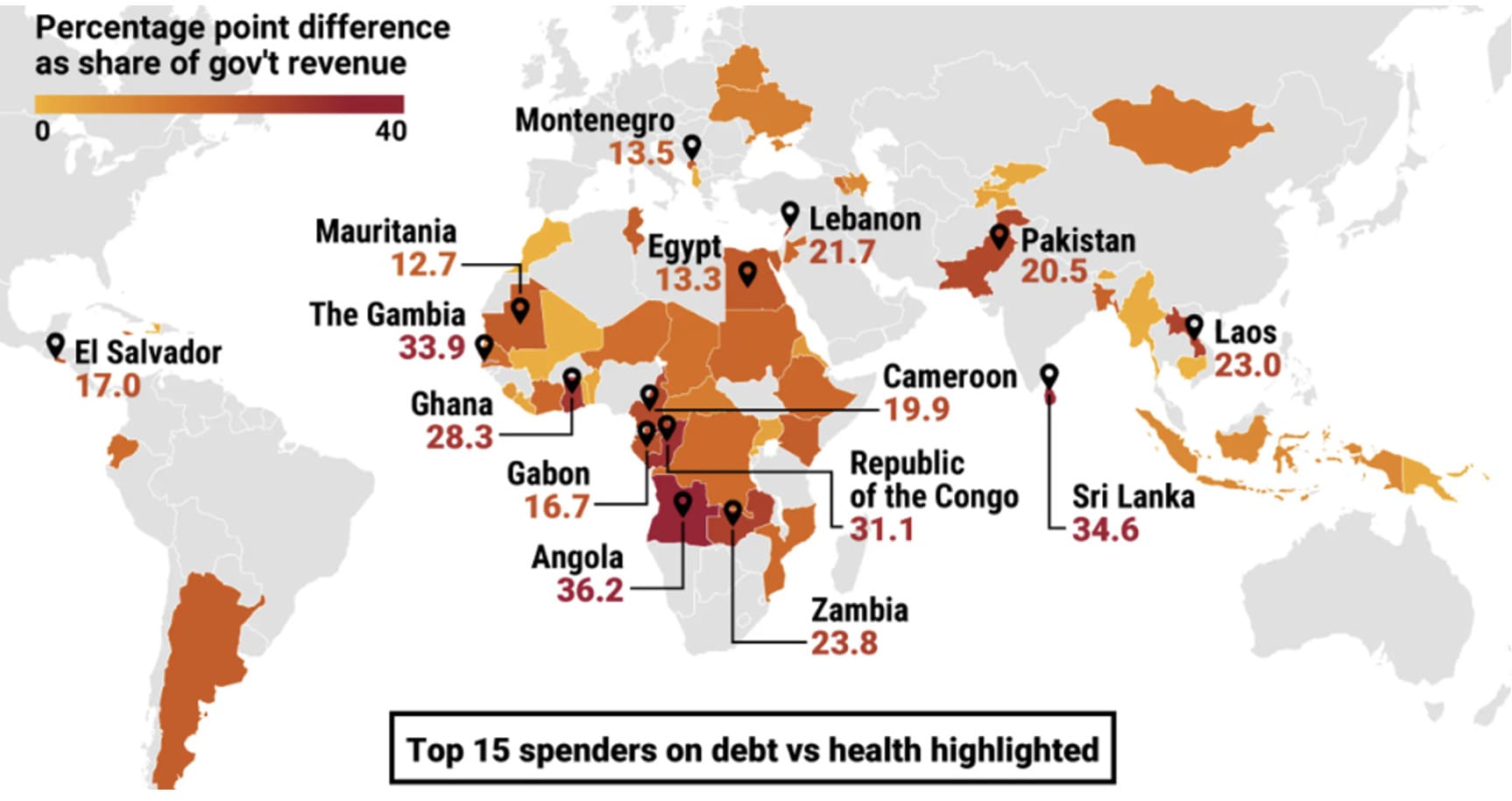

The rising cost of borrowing has intensified an already severe debt crisis. Many developing countries are now spending more on servicing their foreign debt than on essential public services such as healthcare and education (See Figure 3a). In 2023 alone, debt servicing costs reached a record $1.4 trillion, and net interest payments on public debt hit a 20-year high, according to the World Bank. In 2024, net interest payments by developing countries on public debt rose to $921 billion—an increase of 10% compared to the previous year. Alarmingly, a record 61 developing countries devoted 10% or more of their government revenues solely to interest payments.

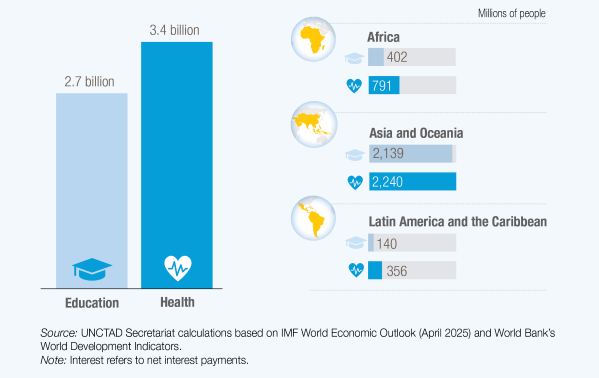

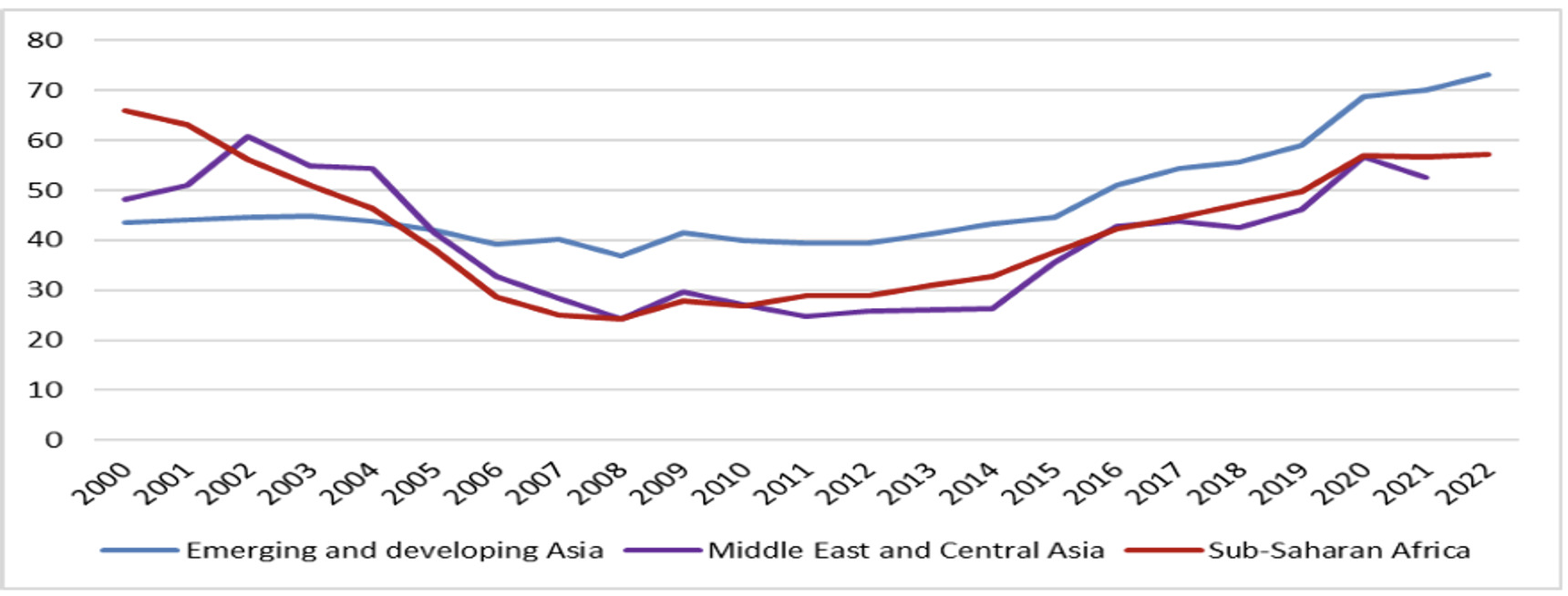

The pressure to meet existing debt obligations is constraining fiscal space, limiting governments’ capacity to invest in sectors essential for long-term, inclusive development. As a result, an estimated 3.4 billion people now live in countries where public spending on interest payments exceeds government allocations for either healthcare or education (as shown in Figure 3b). We also find that public debts to GDP ratio for developing countries have increased for the last decade, especially for Asian and Sub-Saharan countries (as shown in Figure 4).

Figure 3a: Developing Countries that Spend more on Annual Debt Servicing than on Health Care.

Figure 3b: Population in Developing Countries Where Spending on Interest Exceeds Spending on Health or Education (2021–2023)

Figure 4: Trends in Public Debts to GDP ratio in the Developing Countries, 2000-2023.

VII. Inequality, and Structural Dependency: The Global Economic Order and the IMF–World Bank Nexus

Neoliberal globalization has led to a dramatic increase in inequality—both globally and within individual countries (Siddiqui, 2019). Today, wealth is more concentrated than at any time in recorded history. As of recent estimates, three individuals possess as much wealth as populations totalling over 600 million. The world’s 225 richest billionaires —most of them based in the Global North—hold over US$1 trillion in wealth, equivalent to the annual income of nearly 2.5 billion of the world’s poorest people, or approximately 47% of the global population.

In many developing countries, a small class of elites has enriched itself through integration into the global capitalist system. However, the broader population faces deepening poverty and increasing exposure to global crises, including climate change, natural disasters, food insecurity, and violent conflict. Since 2000s alone saw over 60 armed conflicts, resulting in hundreds of thousands of deaths and generating more than 20 million refugees.

To access IMF loans, countries must agree to a series of macroeconomic and structural conditions collectively referred to as SAPs. These include measures such as currency devaluation, fiscal austerity (reducing budget deficits) (Siddiqui, 2023a), increasing interest rates, limiting domestic credit expansion, deregulating prices, removing trade restrictions, and privatising public enterprises. While intended to stabilize economies and attract investment, these policies have often produced the opposite effect. SAPs have systematically reduced employment, undermined domestic industries, and exacerbated poverty and inequality (Siddiqui, 2018).

Developing countries frequently find it impossible to compete with imports from the US and EU, where producers benefit from massive government subsidies. As a result, local industries—especially agriculture and small manufacturing—are often displaced, leading to a sharp rise in unemployment. According to Stiglitz, SAPs have made it harder for developing economies to generate sustainable growth, while eroding their capacity to protect vulnerable populations (Chang, 2001).

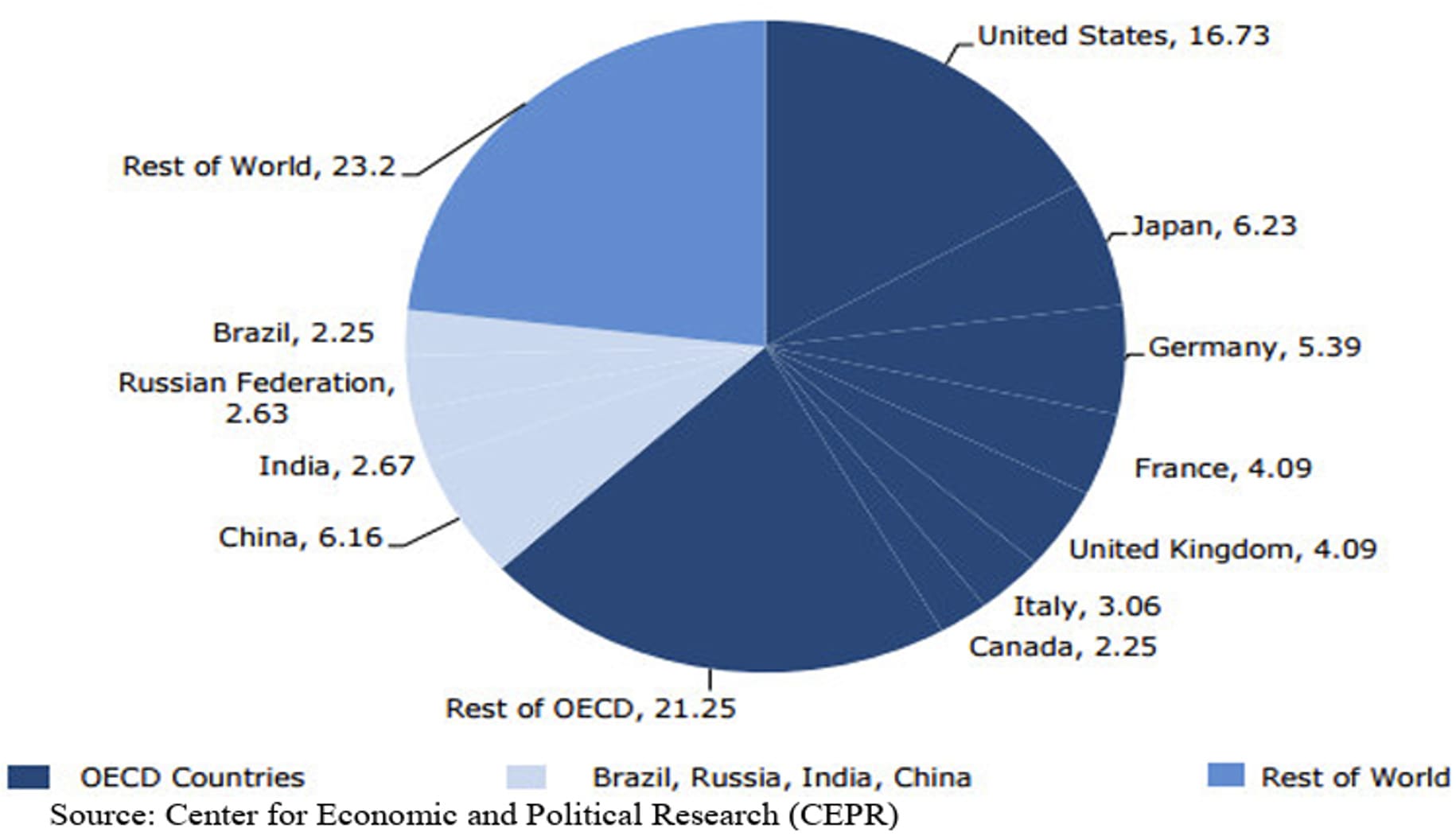

The governance structure of the IMF and World Bank further undermines the legitimacy of these institutions. Voting power is heavily skewed in favour of the Global North. The United States, for example, holds 16.5 percent of the IMF’s voting shares—enough to exercise de facto veto power, as major decisions require an 85 percent majority (see Figure 5). In contrast, Sub-Saharan African countries, despite their substantial combined population, collectively hold less than 5 percent of total voting power. India, home to the world’s largest population of 1.5 billion, possesses only 2.67 percent of voting rights—nearly half the share of the United Kingdom, which, with a population of just 65 million, holds 4.09 percent. Leadership within these institutions also remains dominated by the West: all IMF Managing Directors have been European, while every World Bank President has been American. These so-called “gentlemen’s agreements” regarding institutional leadership are increasingly difficult to justify, particularly as the economic influence of the Global North continues to decline relative to that of the Global South (Muhumed and Gaas, 2016; Wade, 2001).

Figure 5: Voting Shares of IMF Members, 2023.

VIII. Critique of IMF/World Bank’s led Neoliberal Reforms

The IMF and World Bank have long been criticized for perpetuating global inequality and economic exploitation through their lending practices and SAPs. From a radical perspective, these institutions function as instruments of global capitalism, advancing the interests of core capitalist states and their MNCs at the expense of peripheral economies. Their lending practices often create a systemic “debt trap,” wherein developing countries are compelled to allocate a substantial share of national income to debt repayment—primarily to Western creditors (Wade, 2001).

Moreover, the enforcement of capital account liberalisation by the IMF and World Bank—particularly the unregulated flow of capital—exposes developing economies to heightened financial vulnerability and external shocks. The 2008 global financial crisis exemplified the inherent instability of finance-led capitalism and demonstrated the failures of the free-market paradigm that underpins IMF and World Bank prescriptions. Such crises disproportionately affect the Global South, intensifying poverty and underdevelopment while safeguarding the interests of capital in the Global North.

The profits generated by these MNCs are frequently repatriated to their home countries, offering little reinvestment in the host nation. SAPs also emphasise export-oriented growth, urging countries to focus on exporting raw materials, cash crops, garments, or electronic components to earn foreign currency—especially US dollars—rather than developing diversified domestic industries.

SAPs promote a neoliberal agenda that prioritises free markets and diminishes the role of the state in economic planning and public welfare. These policies have been linked to the weakening of domestic industrial capacity, and the erosion of social safety nets. Moreover, the lack of democratic representation within the governance structures of the IMF and World Bank—where voting power is heavily concentrated in Western nations—raises significant concerns about equity and accountability (Stiglitz and Tsuda, 2007).

The disastrous effects of IMF and World Bank policies have occurred in the former Soviet Union and Eastern Europe during the 1990s, when these institutions promoted a rapid transition to free-market capitalism through a policy package known as “shock therapy.” This approach, marked by the abrupt liberalisation of prices, trade, and capital flows, along with the wholesale privatisation of state-owned enterprises, resulted in crony capitalism, hyperinflation, declining life expectancy, and soaring inequality. According to a 2000 United Nations Report, the number of people living in poverty (defined as under US$4 a day in 1990 PPP terms) in Russia and Eastern Europe rose from 13.6 million in 1990 to 147 million by the year 2000. Over the same decade, the region’s overall economic output declined by roughly one-quarter.

Similar outcomes have been observed in many developing countries subject to SAPs imposed by the IMF and World Bank. These programmes typically included price and trade liberalisation, a shift toward export-oriented economies, and extensive privatisation of public services and enterprises. The underlying logic of SAPs was to remove all barriers to trade and capital flows, integrating economies into global markets on neoliberal terms. However, in practice, these policies have often produced devastating results. Across Africa, South Asia, and Latin America, SAPs have been associated with economic stagnation, rising income inequality, mounting unemployment, increased poverty, reduced public investment in social services, and the deterioration of key development indicators—especially in health, education, water access, and food security.

In Egypt, for example, the IMF and World Bank’s proposed reforms as a condition for financial assistance disproportionately impacted the poor and middle classes. The result was greater poverty, worsening inequality, and increasing public discontent. In contrast, countries such as Turkey and Malaysia, which rejected IMF and World Bank prescriptions in the early 2000s, managed to stabilise their economies and achieve relatively strong growth while preserving greater economic autonomy.

The IMF SAPs not only fail to stimulate sustainable economic development, but also exacerbate inequality and retard growth. By imposing one-size-fits-all neoliberal policies, it widened the gap between rich and poor, both within and between nations. Their conditional lending practices are widely seen as undermining economic sovereignty and limiting the policy space of recipient countries. As Stiglitz and Tsuda (2007) argue, these loans are often offered only on the condition that governments adopt policies they might otherwise reject, diminishing their democratic mandate.

Another major concern is the lack of transparency and accountability within these institutions. Historically, both the IMF and World Bank have operated with limited openness, often concealing decision-making processes and key documents from public scrutiny. Although the World Bank has made some progress in expanding transparency in recent years, concerns remain regarding the opacity of policy formulation and loan conditionality, as well as the institutions’ effectiveness and vulnerability to corruption (Siddiqui, 2024b).

Marxist scholars, such as David Harvey (2005), argue that the policy of SAPs has created a global system that subordinates nation-states to the imperatives of capital, undermining their ability to shape independent economic policies. Similarly, Joseph Stiglitz, a prominent critic of the IMF and World Bank, has condemned the SAPs conditionality frameworks attached to their loans. He contends that the austerity measures, privatisation, and deregulation they prescribe often exacerbate poverty and inequality, while imposing one-size-fits-all economic models that fail to account for local contexts of the developing economies (Chang, 2001).

IX. Reforming Global Finance

The United Nations has recommended that the IMF adopt a system of selective Special Drawing Rights (SDR) allocation, in contrast to the current quota-based system, which disproportionately benefits wealthy nations. Under a selective system, additional SDRs would be allocated only to countries facing weak external positions. These allocations would be automatically triggered by predefined conditions—such as climate-related shocks, adverse terms-of-trade movements, rising interest rates, or destabilizing capital flows—arising from broader global dislocations. This mechanism would offer a more equitable and needs-based approach to global liquidity support.

With respect to sovereign debt, the IMF is urged to take a more active role in establishing a multilateral legal framework that ensures the equal participation of all public and private creditors in debt restructuring processes. Such a framework would help prevent fragmented and protracted negotiations, reduce creditor holdout risks, and support timely and orderly debt resolution. Debt relief packages should go beyond mere fiscal consolidation and aim to foster economic recovery, uphold the progressive realization of human rights, and enable countries to invest in sustainable development.

Jayati Ghosh (2024) has been a prominent critic of the current global financial system, particularly in the wake of the COVID-19 pandemic. She has denounced the stark inequalities in vaccine distribution and the inadequate financial assistance provided to developing countries during the crisis. Ghosh advocates for a more coordinated and equitable global response to future pandemics, emphasizing the importance of universal access to public goods and stronger global solidarity. Her proposed reforms include enhanced transparency and accountability within the IMF and World Bank, as well as more effective and inclusive mechanisms for resolving debt crises and advancing sustainable development goals.

X. Conclusion

The IMF and World Bank were initially established to facilitate post-war reconstruction in Europe, but by the 1980s, their focus shifted toward developing countries grappling with balance-of-payments crises. Their loans came with stringent conditionalities, primarily enforcing fiscal discipline through austerity measures and the privatization of public services. These neoliberal reforms, designed to minimize state intervention in favour of market-led policies, have disproportionately benefited multinational corporations (MNCs) while entrenching the dependence of developing countries on global capital. Countries such as Argentina, Egypt, Indonesia, Kenya, Malawi, Pakistan, and Nigeria exemplify the detrimental consequences of these policies—economic instability, weakened public institutions, and social unrest stemming from cuts to essential services.

During the debt crises of the 1990s and 2000s, the IMF, in particular, evolved from helping countries facing balance of payments crises into an enforcer of creditor interests, prioritizing debt repayment and corporate profits over national sovereignty. Empirical evidence demonstrates that these institutions’ economic prescriptions often undermine local policymaking, exacerbating inequality and hindering self-determination. Despite profound shifts in the global economy—including industrialization, trade expansion, and financial globalisation—the IMF and World Bank have maintained a rigid, market-centric approach that neglects demand-side factors, public investment multipliers, and socio-economic rights, including employment, social protection, and environmental sustainability.

Ultimately, these institutions have functioned as instruments of capitalist consolidation, reinforcing US economic dominance and the interests of MNCs. While the World Bank and IMF have distinct mandates, their policies increasingly converge, perpetuating a neocolonial framework that sustains Global South dependency on Western financial systems. SAPs have exacerbated vulnerabilities, deepening debt crises and austerity’s socio-economic toll. The recurring need for external assistance underscores the failure of this paradigm, necessitating a fundamental shift toward inclusive, sustainable models that prioritize equitable development over market dogma. Moving forward, debt relief and fairer global financial architectures are imperative to break this cycle of dependency and crisis.

This study finds that both institutions have consistently operated within a narrow, market-centric economic paradigm that has failed to resolve the structural challenges facing indebted and economically vulnerable countries. Their rigid frameworks often neglect demand-side factors, the multiplier effects of public investment, and broader socio-economic rights, including employment, equity, access to essential services, social protection, and environmental sustainability. The persistence of volatility, recurrent crises, and reliance on external assistance underscores the need for a fundamental paradigm shift. Development models must become more holistic, inclusive, and sustainable—placing human well-being and ecological integrity above narrow market imperatives.

In short, the implementation of IMF and World Bank led SAPs have frequently deepened economic vulnerabilities, intensified debt crises, and magnified the harmful effects of austerity on developing countries. These outcomes have led to reductions in public spending on critical sectors such as health and education, thereby worsening inequality and impeding sustainable development. The growing burden of unsustainable debt highlights the urgent need for comprehensive debt relief and the creation of more equitable global financial structures.

About the Author

Dr. Kalim Siddiqui is an economist specializing in International Political Economy, Development Economics, Trade and Economic Policy. Since 1989, he has been teaching economics at various universities in Norway and the UK. Dr. Siddiqui’s research interests encompass a wide range of topics, including political economy, international trade, and economic history, South Asia, and emerging economies. He has presented papers at international conferences across numerous countries, reflecting his global engagement in the field. His scholarly pursuits span six broad domains: Political Economy, Development Economics, Economic History, Economic Policy, Globalization, and International Trade. Dr. Siddiqui has made significant contributions to research in areas such as trade policy, globalization, and political economy. His work has been published in chapters of edited books and articles published in peer-reviewed journals. For inquiries, Dr. Siddiqui can be reached at: [email protected]

Dr. Kalim Siddiqui is an economist specializing in International Political Economy, Development Economics, Trade and Economic Policy. Since 1989, he has been teaching economics at various universities in Norway and the UK. Dr. Siddiqui’s research interests encompass a wide range of topics, including political economy, international trade, and economic history, South Asia, and emerging economies. He has presented papers at international conferences across numerous countries, reflecting his global engagement in the field. His scholarly pursuits span six broad domains: Political Economy, Development Economics, Economic History, Economic Policy, Globalization, and International Trade. Dr. Siddiqui has made significant contributions to research in areas such as trade policy, globalization, and political economy. His work has been published in chapters of edited books and articles published in peer-reviewed journals. For inquiries, Dr. Siddiqui can be reached at: [email protected]

References

- Chang, H-J. (2001) Joseph Stiglitz and the World Bank: the rebel within, Cambridge: Anthem Press.

- Ghosh, J. (2024) “The “Billions to Trillions” Charade”, Project Syndicate, May 14.

- Muhumed, M.M. and Gaas, S.A. (2016) “The World Bank and IMF in Developing Countries: Helping or Hindering?” International Journal of African and Asian Studies,28.

- Stiglitz, J. and Tsuda, K. (2007) “Democratizing the World Bank” Brown Journal of World Affairs, 13(2), p.79-86.

- Toussaint, E. (2023) The World Bank: A Critical History, UK: Pluto Press.

- Siddiqui, K. (2025a) “Indian Economy at 75: Transformation and Challenges” American Review of Political Economy, 19(1):6-28.

- Siddiqui, K. (2025b) “The Rise of Asian Economies and Implications for the Global Economy” World Financial Review, June.

- Siddiqui, K. (2024a) “Neo-colonialism: An analysis of international factors on the development of the Global South” World Financial Review, December-January.

- Siddiqui, K. (2024b) “Rising Foreign Debts of the Developing Countries and Deepening Economic Crisis” World Financial Review,

- Siddiqui, K. (2024c) “Trends and Prospects of De-Dollarization in the Rapidly Changing Global Economy” (Part 1 & Part 2), World Financial Review, December.

- Siddiqui, K. (2023a). “The New Cold War: Struggle for Global Domination” (Part I & Part 2) World Financial Review, July & August,

- Siddiqui, K. (2023b) “From Rapid Growth to Cronyism: Explaining India’s Economic Development” Asian Profile, 51(4):313-329. December.

- Siddiqui, K. (2021) “Can the 21st Century be an Asian Century?” Asian Profile, 49(1):1-19, March.

- Siddiqui, K. (2020) “The US Dollar and the World Economy: A critical review” Athens Journal of Economics and Business, 6(1):21 – 44.

- Siddiqui, K. (2019) “The Political Economy of Inequality and the issue of ‘Catching up’” World Financial Review, July-August.

- Siddiqui, K. (2018) “Imperialism and Global Inequality: A Critical Analysis” Journal of Economics and Political Economy, 5(2):266-291.

- Siddiqui, K. (2015) “Foreign Capital Investment into Developing Countries: Some Economic Policy Issues” Research in World Economy 6(2):14 – 29.

- Siddiqui, K. (2010) “The Political Economy of Development in Singapore” Research in Applied Economics 2(2): 1 – 31.

- Siddiqui, K. (1996) “The Debt Crisis – Need for a New Strategy”, The News, May 17.

- Siddiqui, K. (1994) “World Bank: 50 Years of neo-liberalism and Diktat”, The Nation, September 5 & 6.

- UNCTAD (2025) A world of debt Report, Geneva: UNCTAD.

- Wade, R. (2001) “Showdown at the World bank” New Left Review, Vol.7, January.

{kind=link}