The Trans-Pacific Partnership (TPP) currently under negotiation in the Asia Pacific region may drastically change the structure and function of the governance of global trade and investment. Below, Junji Nakagawa argues that the 21st century global economy needs fundamental reform of its governance structure, and suggests that what is needed is an insight into the changing patterns of global economy, and an innovative and evolutionary approach to reinvigorate the existing institutions for global economic governance.

The TPP (Trans-Pacific Partnership), a free trade agreement (FTA) currently under negotiation among 12 countries in the Asia Pacific region, may drastically change the structure and function of the governance of global trade and investment, for the following two reasons.

First, the negotiating countries of the TPP, notably the US, are aiming at concluding a “21st century model of an FTA”, with a high level of trade and investment liberalisation and a set of high level standards on a broad range of economic regulations, thus establishing an optimal regulatory/institutional framework for servicing the pressing needs of firms expanding their business through global value chains (GVCs). Secondly, as several mega-FTAs are under negotiation, and the TPP is most likely the first one to be concluded, the rules and liberalisation commitments of the TPP may become de facto global standards, by its reference in the negotiation of other mega-FTAs, such as TTIP (Transatlantic Trade and Investment Partnership), Japan-EU EPA (Economic Partnership Agreement) and RCEP (East Asian Regional Comprehensive Agreement). Let me elaborate further on these.

When the US decided to join the negotiation of the TPP in December 2009, the then US Trade Representative Ronald Kirk, in his letters to the leaders of the US Congress notifying that decision, stated that US’s goal was “to shape an eventual Trans-Pacific Partnership Agreement that is a new kind of trade agreement for the 21st century”, with ambitious trade and investment liberalisation and high-level rules on a broad range of economic regulation. Why, then, was the TPP meant to become a 21st century model of an FTA?

To fully understand the drastic change in global trade governance, namely the stalemate of the Doha Development Agenda (DDA) and the frenzy of mega-FTAs, we must realise the driving force that has brought this change. The changing pattern of global trade and investment, which is coined in such terms as globalisation of value chains (GVCs), globalisation of supply chains or international production networks, is the driving force. GVCs started in the 1970s in North America (Canada, US, and Mexico) in the automotive industry and expanded in Central and East Europe (Germany and former socialist countries in the region) in a number of manufacturing industries in late 1980s to early 1990s. However, it was in East Asia in the mid-1990s on that GVCs developed on a full scale. Japanese firms took the initiative by aggressively investing in the manufacturing sector (electronic appliances, machinery and automobiles) in several ASEAN countries (Thailand, Malaysia and Indonesia) and Taiwan, with the US and EU as major export markets. Later, Japanese firms expanded their production bases to China, India, and more recently to Vietnam and Myanmar.

Currently, GVCs are getting more and more “global” both geographically and in sectoral coverage, as firms are doing business globally regardless of their size, country of origin and their field of activity. In particular, the services sector has become a major component of GVCs, not only because they provide services indispensable to globalisation of manufacturing (e.g., transportation, telecommunication, logistics and financial services), but also because many services are traded globally (e.g., professional services such as lawyering and accounting, retail and wholesale, tourism, construction and civil engineering, water supply and even health services).

Innovation in information and telecommunication technology (ICT) and the resulting dramatic decline of costs in telecommunication and transportation were the major triggers for GVCs. However, GVCs would not have happened without the drastic change in the policy and regulations of international trade (goods trade and services trade) and investment (FDI and M&A). The Anglo-Saxon countries (US and UK) took the initiative in the latter, by conducting liberal domestic and external economic policy reforms in the early 1980s (Reaganomics and Thacherism). Other countries in Europe and later Japan followed suit. At the same time, several ASEAN countries also adopted export-promotion policy reform in the 1990s by unilaterally liberalising import trade and inward investment.

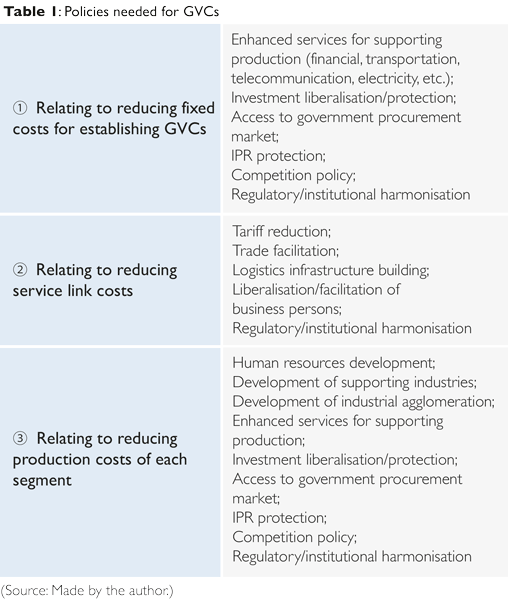

Most of these economic policy reforms were conducted unilaterally in US, Europe and Japan. But, firms in these developed countries demanded the expansion of such policy reforms to cover their global business territory, as they needed a broad based trade and investment liberalisation and a high level of liberal trade and investment rules throughout the countries within their business transactions (see Table 1 below).

The first attempt to establish such liberal economic policy reforms multilaterally, the OECD-sponsored Multilateral Agreement on Investment (MAI) failed in 1998. The second attempt was the DDA of the WTO that started in November 2001. However, perhaps due to the power structure of the WTO which was quite different from that of the GATT, members of the WTO found it much more cumbersome and time-consuming for multilateral trade negotiations to reach consensus. On almost all issues of the DDA agenda, key members, namely, US, EU, China, India and Brazil, couldn’t reach agreement. Although the 9th Ministerial Meeting held in Bali in December 2013 could wrap up negotiations of the Agreement on Trade Facilitation, itself an indispensable component of global regulatory environment for GVCs, for the rest of the long list of DDA agenda there is little hope for early conclusion.

In light of these, notably the DDA stalemate, major firms and industry associations in developed countries began to pressure their governments to shift the trade policy priority from WTO to the negotiation of mega-FTAs. Here again, US took the initiative in March 2008, when the Bush Administration announced its intension to join the follow-up negotiation of the then four-party Trans-Pacific Strategic Economic Partnership Agreement (sometimes called as P4, among New Zealand, Singapore, Chile and Brunei) on financial services and investment. The US decided to join the P4 as a whole in September 2008. The Obama Administration succeeded this and the TPP negotiation started in March 2010 with 8 members. The launch of the TPP negotiation had a strong domino effect and triggered negotiations of other mega-FTAs, which started in 2013 and have been accelerated in 2014.

The TPP is most likely to become the first mega-FTA, as its negotiation may be wrapped up by, in an optimistic scenario, the end of 2014. It is also likely to become “a 21st century model FTA”, as was envisioned by the US. There are two reasons for which the TPP is likely to become a 21st century model FTA. First, the TPP is aiming at a broad based trade and investment liberalisation and a high level of liberal trade and investment rules throughout its member countries. Secondly, the rules and commitments of the TPP are being referred to by the negotiators of other mega-FTAs, notably TTIP and Japan-EU EPA, and will become defacto global standards for international trade and investment.

The emergence of mega-FTAs, and the TPP in particular, in the governance of global trade and investment, is, however, far from an optimal solution to the challenges of global trade and investment governance today. The TPP rules and commitments may become de facto global standards, but they have two intrinsic defects in achieving the goal of providing optimal trade and investment environment for GVCs. First, mega-FTAs will cover their members and exclude non-members, most of which will be LDCs. There will be a split between those included in “mega-FTA clubs” and those excluded. Poverty and income disparity in LDCs will worsen, and this might lead global insecurity. Secondly, membership of “mega-FTA clubs” will not automatically secure that they will be chosen by global firms. The rules and commitments of mega-FTAs are necessary conditions for GVCs but they are not sufficient conditions. Countries must develop human resources, supporting industries and industrial agglomeration to attract global firms. These measures are not covered by mega-FTAs. They are rather provided by the voluntary and unilateral efforts of each country. This means that even non-members of mega-FTAs may have a chance to join GVCs by unilaterally providing rules, commitments and policies that are needed for GVCs. Members of mega-FTAs cannot prevent such efforts.

In light of these, countries in East Asia should think seriously of transplanting the rules and commitments of mega-FTAs, notably TPP, to the WTO. The WTO, with 160 members now, is equipped with several institutional mechanisms by which members at different stages of development and capability may come up with the rules and commitments in a gradual but steady manner (see Table 2).

By transplanting the rules and commitments of mega-FTAs to the WTO, those rules and commitments will become truly global, and WTO members, whether developed or developing, will get a chance to join GVCs gradually but steadily. The WTO will be reinvigorated with new rules and commitments that will match the needs of GVCs, and we may coin it as WTO 2.0.

Will the WTO 2.0 secure an optimal global trade governance of the 21st century? Unfortunately, the answer is negative. GVCs are realised not only by broad based trade/investment liberalisation and a high level of trade/investment rules. They are also realised in a liberal and exponentially growing global financial market (GFM). Although the GFM of the 21st century, coupled with GVCs, may secure continuous growth and prosperity, it is also vulnerable to seemingly unexpected and unpredictable shocks. As was witnessed in the Global Financial Crisis of 2008 and ensuing crisis in Europe triggered by the default of Greece, such shocks, once they occur, may endanger the GFM and GVCs as a whole, and its consequence may be detrimental to global wealth and prosperity, endangering global peace and security.

What is needed is, therefore, not only the WTO 2.0, but the comprehensive reinvention of global economic governance institutions. Such reinvention needs not the complete destruction of existing institutions such as IMF, World Bank, G8, G20, OECD and Basel Committee, to mention a few. Rather it can be achieved by fine-tuning the functions of such institutions and by furthering their coordination and co-operation. I’d like to coin such reform as Bretton Woods 2.0. (See Table 3 below).

70 years have passed since the inception of the Bretton Woods system for governing global trade, investment and finance. The 21st century global economy, characterised by GVCs and GFB, needs fundamental reform of its governance structure. Bretton Woods 2.0 will not be built by totally scrapping the existing institutions and replacing them with new ones. Rather, Bretton Woods 2.0 will be realised by fine-tuning the functions of the existing institutions, strengthening the coordination among them, and giving them new functions to meet the needs of GVCs and GFB. What is needed is an insight into the changing patterns of global economy in the 21st century, and an innovative and evolutionary approach to reinvigorate the existing institutions for global economic governance.

About the Author

Junji Nakagawa has been a professor of international economic law at the Institute of Social Science, the University of Tokyo since 2000. He is currently a visiting professor at the Institute for East Asian Studies, Japanology at Free University of Berlin (April to August 2014). He is an expert of international economic law and has published over 30 books and 150 journal articles and book chapters in that field. His most recent publications are WTO: Beyond Trade Liberalization (Tokyo, Iwanami Publishing, Co., 2013, in Japanese) and Transparency in International Trade and Investment Dispute Settlement (Routledge, 2013).

")

{kind=link}