Shanghai Cooperation Organisation (SCO) was founded in 1996 by the People’s Republic of China, Russia, Kyrgyzstan, Tajikistan, and Kazakhstan in order to build mutual trust among member states and to encourage regional cooperation under the name “Shanghai Five”. And since the beginning, China has been the leading force of the SCO. Initially, the five SCO members aimed to build closer cooperation on border issues and control terrorism threats. Central Asia has deep ethnic conflict and also China’s Western region of Xinjiang. (Zhao, 2006)

The Shanghai Cooperation Organisation is becoming an important organisation that seeks to build economic and regional cooperation among emerging Asian economies. China is also using it to develop not only security, but also economic and trade cooperation for better economic development on the western borders of China. China is a dominant economy and trading country and accustomed to applying its economic pressure on the other members. China shares very long borders with other Central Asian republics, including Kyrgyzstan, Kazakhstan, and Tajikistan. The SCO can help to build multi-dimensional ties within the region. (Chao, 2022)

Soon after, the membership increased to eight, and a further four were also included as observer countries (Afghanistan, Belarus, Iran, and Mongolia) and six dialogue members (Armenia, Azerbaijan, Cambodia, Nepal, Sri Lanka, and Turkey) were invited. In 2021, the decision was made to start the accession process of Iran to the SCO as a full member, and Egypt, Qatar, as well as Saudi Arabia became dialogue partners. Iran is expected to become a full member in 2023. A growing number of countries across Eurasia and the Middle East are keen to participate as observers and dialogue partners, stretching from Cambodia to Belarus.

This article intends to examine the growing multilateral cooperation among emerging economies under the SCO. I will also try to see how, if successful, such economic, trade, and security cooperation can promote economic development in the region and also play a positive role in facilitating Asian economies as a dominant economy of the world.

The SCO is not a military bloc, nor is it aimed at any one country or group. The SCO summit in Samarkand was recently attended by 15 of the countries’ leaders, including Russian President Vladimir Putin, Chinese President Xi Jinping, Iranian President Ebrahim Raisi, Turkish President Recep Tayyip Erdogan, and Prime Minister Narendra Modi. In the recent summit, it was emphasised that the SCO is a venture for constructive cooperation and peace and stability in the world.

The SCO’s main achievement thus far is to have offered its members a cooperative forum to balance their conflicting interests and ease bilateral tensions. It has built up joint capabilities and has agreed on common approaches in the fight against terrorism and extremism. However, the SCO has major shortcomings, such as institutional weaknesses and a lack of common financial funds for the implementation of joint projects, and conflicting national interests have prevented it from achieving a higher level of regional cooperation in other areas.

South Asia is one of the least integrated regions in the world, with persistent India-Pakistan rivalry acting as a major stumbling block to regional cooperation, but both India and Pakistan became members of the SCO in 2017 and, thus, will gradually become part of the multilateral arrangements and economic cooperation.

Multilateral Cooperation

The European Union is widely seen as a model for regional cooperation and various other regions would like to replicate it. (Aris, 2009) Most Asian countries prioritised economic growth and stability rather than pursuing “Western-style” liberal democracy. The SCO and the Association of Southeast Asian Nations (ASEAN) were formed in very different international contexts. The ASEAN was formed during the Cold War and was fully supported by the West and seen as an important regional unity against communism. (Siddiqui, 2015; 2010)

However, the SCO was formed in the mid-1990s to address regional security concerns in Central Asia after the collapse of the Soviet Union. Initially, the important reason to form SCO was to keep Central Asian countries away from US military and security alliances. And also, these Central Asian countries are ruled by elites who do not have popular support among their people. Both regional organisations were formed with the idea of emphasising the commonality of contexts of the political system. As Acharya (2001:34) notes, “It may be argued that while common values are necessary for community building, these need not be liberal democratic values. A shared commitment to economic development, regime security, and political stability could compensate for a lack of a high degree of economic interdependence.”

Besides security, oil and gas supply is vital for the rising Chinese economy. As Chao notes (2022:294), “Central Asia has substantial energy resources and thus could be an important source of energy for China apart from the Middle East … therefore, establishing close relations with Central Asian countries is a strategic consideration for China. The SCO has become an essential platform for China to establish close bilateral relations with Central Asian countries. … The Chinese government’s view, economic development, modernisation, and increasing prosperity of Xinjiang and Central Asia are another method of reducing terrorism.”

However, there are vast differences among the SCO members. As Zhao (2006: 14) puts it, “disparities in terms of population and geographical size are very significant among member states. In particular, both China and Russia have huge populations and territories compared to the Central Asian member states. Every country also has a different profile in terms of politics, society, religion, culture, not to mention the different pace of economic growth.”

The SCO is also interested in building and developing the organisation on similar lines to the ASEAN. The organisation intends to build trust and consensus among members regarding crucial issues. It is being agreed to strengthen regional cooperation in trade, economic, education, and cultural issues. China, with a very large population and economy, has become a crucial supporter of the SCO, which is termed as “Shanghai Spirit”, which means building on the basis of equality, mutual advantage, trust, consultations, and dialogue to benefit all member countries. The SCO aims to deepen trade relations, increase regional growth, and raise the living conditions of the population. China has increased trade and financial aid to the region. For instance, Chinese trade with Central Asian countries rose to US$45 billion in 2015 from only US$1 billion in 2002. China also extended loans initially of US$10 billion to its SCO five members to reduce the adverse impact of the 2009 global financial crisis. And again in 2012 a further US$10 billion in economic assistance was given to these countries. Russia, too, received financial aid after the imposition of Western sanctions due to its annexation of Crimea in 2014. China’s imports of Russian natural resources rose sharply. China also extended further credits to Russia of US$13.8 billion in 2014. And by 2015, Chinese investment rose sharply, as it became the largest foreign investor in Russia.

China’s imports of gas and oil from the SCO members have increased, so that China is far less dependent on Middle East oil than before. The Chinese National Petroleum Corporation has signed many agreements with Central Asian countries, Russia, and Iran, and has become more dependent for its energy needs in these countries in recent years.

China is the world’s largest energy consumer, and the country consumes 13 percent of the world’s total oil and gas consumption in 2019, which was 400 million tons. Most of its oil is imported and it is now the third-largest oil importer after the US and Japan. Therefore, seeing the global tension, China is very keen to diversify its oil imports and considers them as very important security needs. The availability of large amounts of oil and gas in Central Asia and Russia can help China to diversify its oil supplies, rather than completely relying on Middle Eastern countries, where the US has a strong military and economic presence.

Moreover, in recent years the Belt and Road Initiative has increased Chinese investment in the Central Asian region, which is more dependent on Chinese investment and trade than ever in the past. The BRI includes mega infrastructure projects, such as the building of roads, railways, and ports to increase trade and travel. The development of the Central Asian regions is crucial to the success of the BRI. (Siddiqui, 2019b)

Rise of Asian Economies

The 30-year period from 1991 to 2021 will puzzle researchers. What is the explanation for the triumph of the liberal international order that fused US military hegemony, especially after the collapse of the Soviet Union in 1991, with global US supremacy under multilateral institutions and liberal ideology?

In fact, the US miscalculated that integrating China into the global economy would lead to world prosperity, which would also turn China into a partner in keeping and supporting the US-dominated multilateral order. Such hope failed utterly to make China politically liberal like the US. (Siddiqui, 2020a; 2020b)

Despite benefiting multinational corporations, globalisation, and financialisation since the early 1990s, it sharply increased inequality and eroded the manufacturing sector in the US and European countries. Millions of jobs were lost as industries were moved to low-wage countries, especially China and other East Asian countries. (Siddiqui, 2019a) These developing economies emphasised providing cheap labour while the advanced economies focused on monopolising knowledge-intensive tasks. (Acemoglu and Robinson, 2014)

During the last four decades, China has been transformed from an industrially low-level economy to becoming the world’s prime industrial superpower and a competitor and challenger to the US and European hegemony over modern technology and research. In the 1980s, China forced multinational corporations to diffuse technology to Chinese companies as a condition of their access to cheap Chinese labour and markets. And, due to various factors, in recent years China has emerged from being a high-tech recipient to become an innovator of high-tech. The country has also emerged as a locomotive of the world economy and accounted for 28 per cent of all growth worldwide between 2013 and 2019, more than twice the share of the US.

However, the Chinese economy is marked by several crises, including rising inequalities, regional disparities, surplus capacity, and environmental problems.

There is no doubt that globalisation, economic openness, and trade have performed a critical supportive role in East Asia and China’s economic growth, rather than passive insertion into it. And the role of the government has been crucial to its success. For instance, trade policy was liberal and very supportive of exports, while restrictive of imports. And also the government used foreign capital inflows to facilitate domestic industrialisation. (Siddiqui, 2012; 2010)

Despite the diversity in economic development in the Asian economies, there have been common discernible patterns. (Nakao, 2022) Economic growth drove overall development, and the growth rates of GDP and GDP per capita in Asian economies have been stunning and far higher than elsewhere in the world (see figure 1 and figure 1a).

Asian countries are now the fastest-growing economies in the world thanks to rising growth and booming exports. We also need to look at the recent OECD forecast figure for 2023 for leading economies. (See figure 1a)

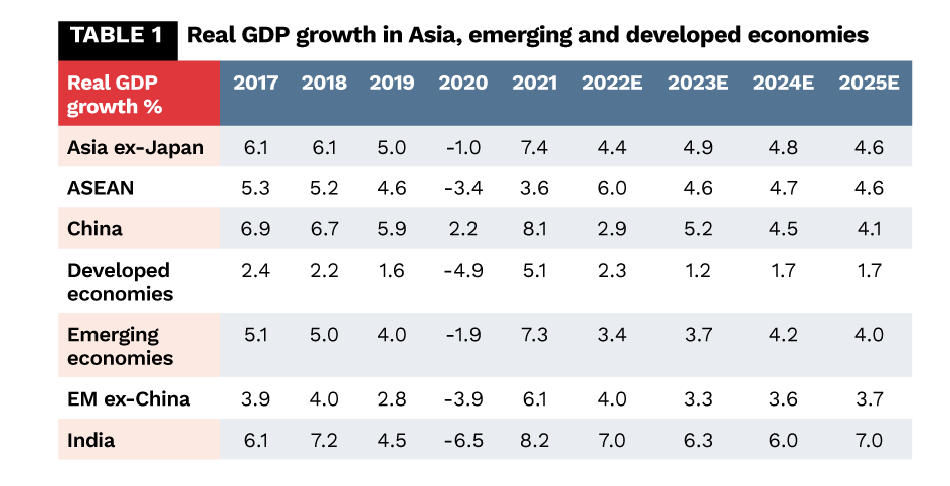

Asian countries are now the fastest-growing economies in the world, thanks to rising growth and booming exports. From 2017 to 2021, the five-year average of real GDP growth for Asia was 4.2 percent, compared to 1.4 percent in the developed markets and 3.9 percent in emerging markets (see table 1). In 2018, China and India were the highest-growth economies, with 6.7 percent and 7.3 percent respectively. (Goldman Sachs, 2022)

This fast-growing GDP can be partly explained by the rapid accumulation of wealth in Asia. (Mahbubani, 2008; 2011) By 2025, wealth in Asia excluding Japan could outstrip the US, while China’s share in the region has moved up to almost 46 percent. Chinese consumers are especially becoming more affluent, and their focus is increasing towards better products and services. In China, the urbanisation ratio has increased to 64.7 percent in 2021 from 26 percent thirty years ago, according to data, although this is still lower than developed economies of around 80 percent.

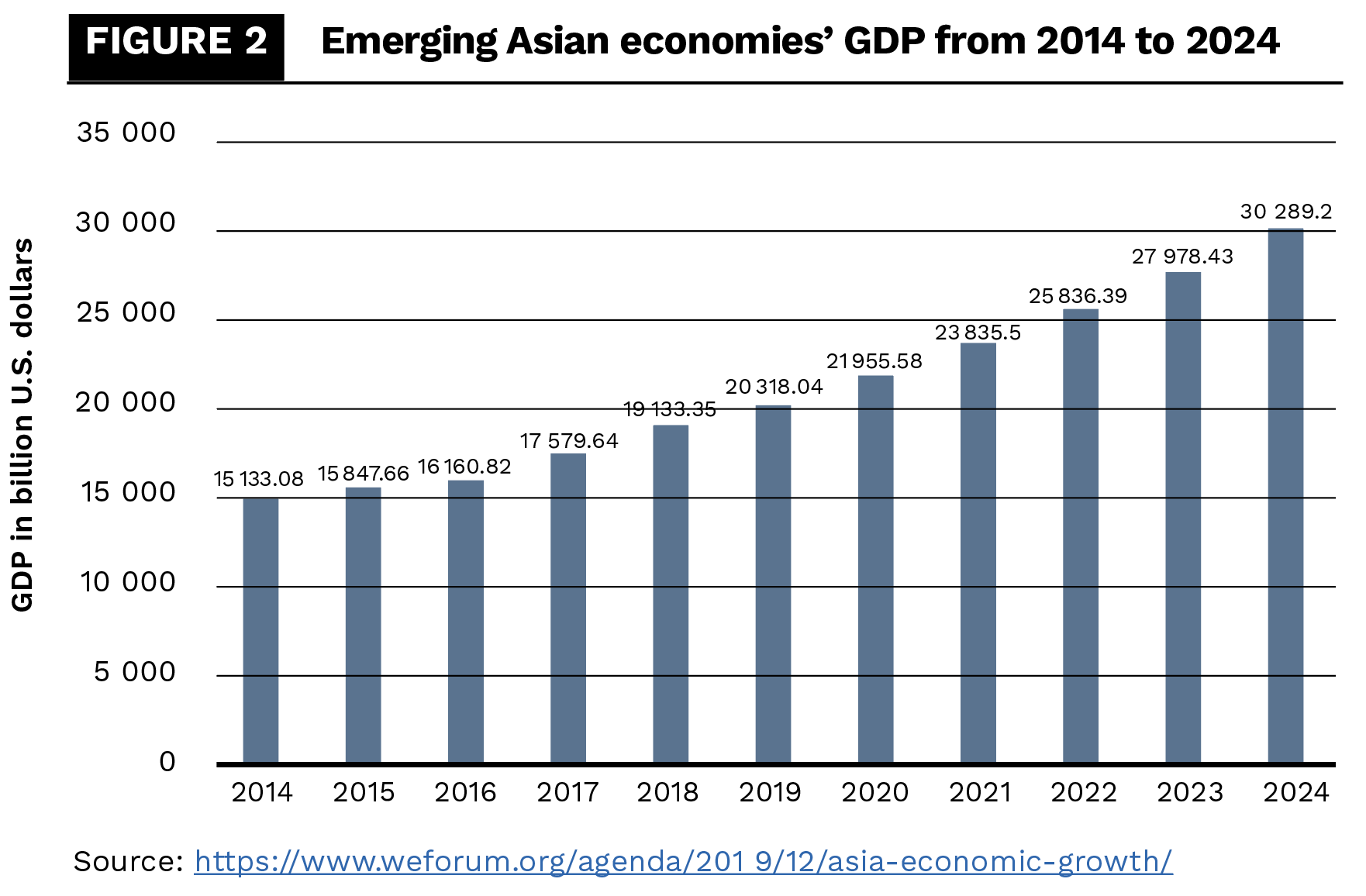

Meanwhile, booming exports have helped contribute to economic growth. Output from Chinese factories is high, improving employment opportunities for many. The country exports more than it imports and in 2021 posted record trade surplus figures of US$670 billion. India is set to have the strongest growth out of all the large economies and has been the second engine of growth for Asia. The country is heading for an average of 7 percent growth over 2022-3 and is expected to contribute 28 percent and 22 percent to Asian and global growth (see figure 2).

Asia is in the middle of a historic transformation. It is projected that by 2050, Asia’s per capita income will increase sixfold in purchasing power parity (PPP) terms to reach EU levels today. This means that about 3 billion Asians will see a rise in their incomes and the region will double its share of global GDP to 52 per cent by 2050. It is said that Asia would regain the world’s dominant economic position it held before colonisation and the rise of Europe since the mid-eighteenth century. It assumes that Asian economies can continue to grow at the same rate for the next four decades and would successfully build comparative advantages. Asia’s GDP (at the market exchange rate) is expected to increase from US$17 trillion in 2010 to US$174 trillion in 2050, i.e. half of the global GDP, similar to its population.

Seven Asian countries have the largest economies (China, India, Japan, Indonesia, South Korea, Malaysia, and Thailand). These seven countries have a combined population of 3.2 billion, which is nearly 78 per cent of the total Asian population, with a GDP of US$15.1 trillion in 2017. It is expected that their GDP will increase to the levels it had three centuries ago (prior to the colonial period). See figure 3.

However, in the late 1960s, Asia was the poorest in the world in terms of income and living conditions. Its social indicators of development were among the worst anywhere, which epitomised its underdevelopment. The deep pessimism about Asia’s economic prospects was narrated by the Swedish economist Gunnar Myrdal in his book Asian Drama. (Siddiqui, 2018a)

For the last five decades, Asia has witnessed a profound transformation in terms of economic development and living conditions. By 2018, the data shows that it accounted for 30 per cent of world income, 40 percent of world manufacturing, and over one-third of world trade. The expansion of manufacturing, and rising investment and savings rates combined with the spread of education were the underlying factors. In short, Asian economic growth was driven by rapid industrialisation, rising investment, and productivity, often led by exports and linked with changes in the composition of output and employment. (Siddiqui, 2021a; 2021b)

Rising per capita incomes transformed social indicators of development, as literacy rates and life expectancy rose everywhere in Asia. There was also a massive reduction in absolute poverty. But the scale of absolute poverty that persists, despite unprecedented growth, is just as striking as the sharp reduction in poverty that happened in recent decades. The poverty reduction could have been much greater but for the rising inequality. Inequality between people within countries rose almost everywhere, except South Korea and Taiwan. Yet the gap between the richest and poorest countries in Asia remains awesome and the ratio of GDP per capita in the richest and poorest countries in Asia was more than 100:1 in both 1970 and 2018.

The developmental states in South Korea, Taiwan, and Singapore coordinated policies across sectors over time in pursuit of national development objectives, using carrot-and-stick policy to implement their agenda, and were able to become industrialised nations in just 50 years. China emulated these developmental states with much success, and Vietnam followed on the same path two decades later, as both countries have strong institutions and one-party communist governments that could coordinate and implement policies.

It is not possible to replicate these states elsewhere in Asia. But other countries, such as India, Indonesia, Malaysia, Thailand, Bangladesh, and Turkey, did manage to evolve some institutional arrangements, even if less effective, that were conducive to industrialisation and development. In some of these countries, the checks and balances of political democracies were crucial to making governments more orientated towards development and the well-being of the poor.

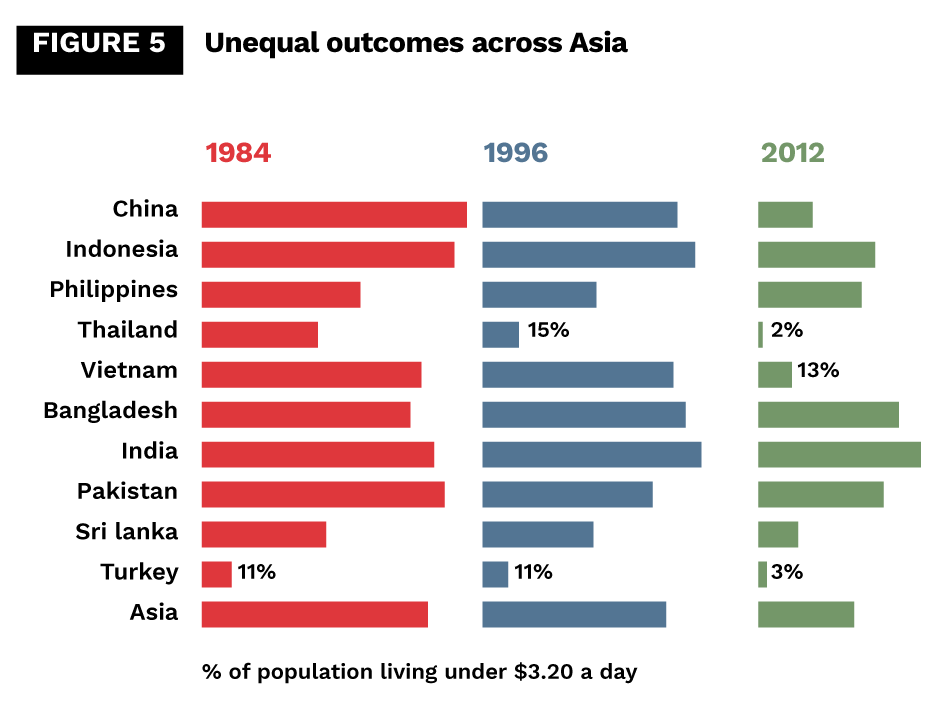

These transformations were unequal across countries and between people (see figure 5). Asia’s economic transformation in this short time span is almost unprecedented in history. It is essential to recognise the diversity of Asia. There have been marked differences between countries in geographical size, embedded histories, colonial legacies, nationalist movements, initial conditions, natural resource endowments, population size, income levels, and political systems. The reliance on markets, government intervention, and the degree of openness of economies has varied greatly across countries and over time.

The Decline of the Supremacy of the US Dollar

The central banks of different countries also hold dollar reserves. The decisions of others, such as private and public dollar holders, depend on expectations about the price of dollars vis-à-vis both other currencies and also commodities. The central banks’ decisions are influenced by an additional factor: since the dollar is the medium of transaction in much of world trade, they carry dollar reserves for settling accounts. At present, the sanctions against Russia have encouraged bilateral payment arrangements between Russia and other countries. The US dollar simply does not enter as the medium of the transaction in such trade. In a bilateral arrangement between Russia and India, for instance, the exchange rate between the two currencies is fixed, and the balance of trade is simply held as a claim by one country upon the other. Such arrangements, therefore, eliminate the demand for US dollars as a reserve currency, replacing it with the rouble and other currencies. (Siddiqui, 2021c)

Moreover, much of the world’s trade is still carried on with the dollar as the medium of transaction. Interest rates in the US had been close to zero since the 2008 global financial crisis, but are now being raised as a means of controlling inflation. This has the effect of sucking in money from all over the world, especially from developing countries, back to the US, causing a depreciation of their currencies vis-à-vis the dollar.

The rising Asian economies and the war in Ukraine are challenging US global hegemony. In fact, the Ukraine-Russian war is part of this challenge; a crucial point is in the transition from a so-called “unipolar world” to a “multipolar world”. (Siddiqui, 2020c; 2020d)

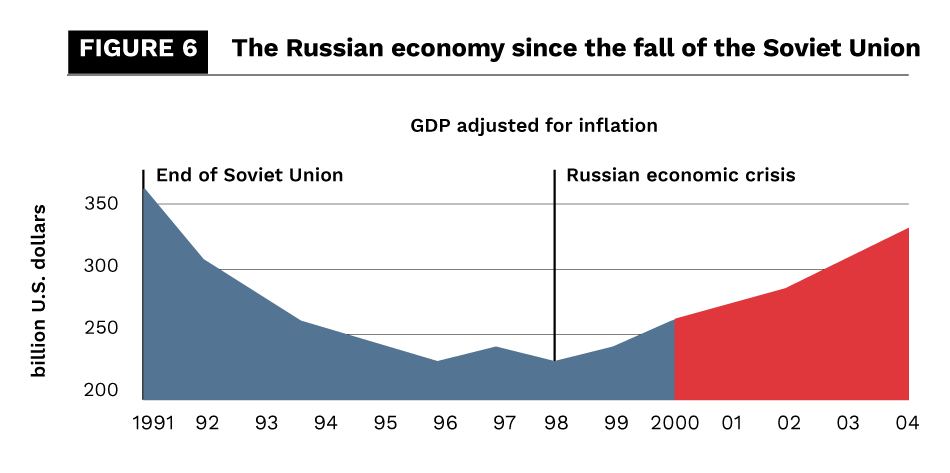

Although Russia still largely relies on exporting natural resources, its economy has improved in recent years. Russia’s economy went into a sharp decline after the break-up of the Soviet Union in 1991. The state-owned industries were privatised to private investors at giveaway prices, while workers’ wages fell sharply, and they faced a sharp drop in their standard of living. The low point was 1998 when an economic crisis led to a big devaluation of the rouble. However, in recent years, soaring oil revenues have boosted state revenues and led to an economic recovery, with Russia paying off its international debts.

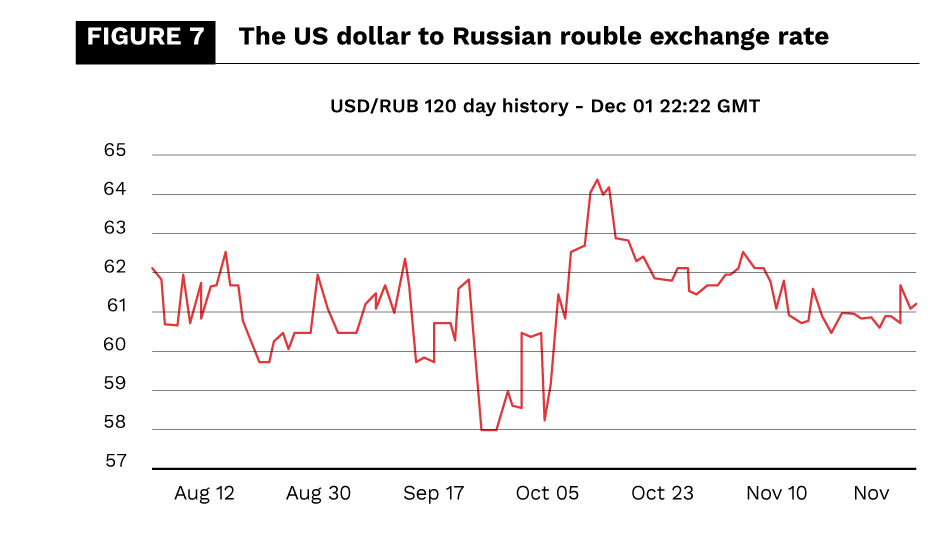

However, the Russian economy is still much smaller than other G8 countries and, measured by income per capita, income is less than one-tenth of G8 levels (see figure 6). The supremacy of the US dollar is being challenged, because of the sanctions it has imposed on Russia following the Ukraine war (Siddiqui, 2022a; 2020e), and because of the closure of industries due to the non-availability of cheap energy from Russia. The US sanctions were imposed to cripple the rouble and to bring Russia to its knees. The US and EU financial sanctions expected to reduce the US dollars Russia earned through its exports, which meant a dollar shortage in Russia that pushed up the price of the dollar against the rouble. From a price of around 77 roubles in mid-February 2022, the dollar rose to 136 roubles in April 2022. However, the rouble strengthened against the US dollar in November 2022, at 60 roubles to the dollar (see figure 7).

In fact, after the US sanctions, Russia began selling oil against rouble payments, and embarked on speculative activity to increase oil prices in the world market. Because of the rise in the dollar price of oil in the world market, Russia’s export earnings have increased, despite lower export volumes. The higher oil price is also a major contributor to the acceleration of the inflation rate in the US and EU countries, leading to the threat of recession. (Siddiqui, 2022b)

The US miscalculated and hoped that most countries of the world would fall in line with the US diktat, but the fact is that not only China, but many others including India, Bangladesh, Iran, Indonesia, and South Africa, have carried on trade with Russia despite the US and EU sanctions. And also on the oil production front, the major oil producers had offset the measures by raising production and increasing oil exports. Saudi Arabia, despite being a close ally of the US, declined to raise its output, citing various logistical reasons. As a result, sanctions against Russia have lowered overall oil output, raised prices, and contributed to a global economic recession. (Siddiqui, 2022b)

Conclusion

The rise of Asia represents the beginnings of a shift in the balance of economic power in the world and a decline in the political dominance of the West. The future will be shaped partly by how Asia exploits the opportunities and meets the challenges and partly by how the difficult economic and political conjuncture in the world unfolds. Yet it’s plausible to suggest that by around 2050, a century after the end of colonial rule, Asia will account for more than a half of world income and will be home to more than half of the people on earth. It will have an economic and political significance in the world that would have been difficult to imagine 50 years ago, even if it was the reality in 1820.

The transformation of Asia is reflected in its demographic transition, rising productivity, and skills, and living conditions have been phenomenal. From 1970-2018, the economic growth in GDP and per capita GDP in Asia was much higher than in other regions. For instance, Asia’s share of world GDP rose from less than one-tenth, while its income per capita converged towards the world average.

On industrial production, its share sharply rose from merely 4 per cent to more than 40 per cent. This unprecedented development indicates a sharp contrast with the dramatic decline of Asia’s manufacturing during colonial rule. (Siddiqui, 1989; 1985) Their independence, leading to economic sovereignty, and the global tension and Cold War between 1945 and 1990 resulted in rapid transformation and economic development. However, there were great variations in economic development between the Asian countries, so that East Asia has done much better than South Asia, while within the East Asia region, Southeast Asia is in the middle.

|

The study concludes that the SCO’s economic and trade cooperation will further strengthen multilateral cooperation in the region. In 2019, China exported more than US$2.6 trillion in goods and services, slightly ahead of the US figure of US$2.5 trillion. It seems that not only have the US and EU lost economic ground to Asia, in terms of volumes of trade, investment, and economic growth, but the capacity to guide and influence political developments, serve as a moral yardstick, and ultimately its use of military power to influence events has been severely eroded.

However, environmental problems are rising across Asia. The impact of climate change is much more visible across Asia, such as rising sea levels, changing weather patterns, and rising temperatures. Transparent governance is crucial to benefit the vulnerable sections of the population and governments also need to address rising inequalities in income and wealth. The governments must spend more on safeguarding public health and education and providing social welfare.

This article was originally published on March 2, 2023.

About the Author

Dr. Kalim Siddiqui is an economist specialising in International Political Economy, Development Economics, International Trade, and International Economics. His work, which combines elements of international political economy and development economics, economic policy, economic history and international trade, often challenges prevailing orthodoxy about which policies promote overall development in less-developed countries. Kalim teaches international economics at the Department of Accounting, Finance and Economics, University of Huddersfield, UK. He has taught economics since 1989 at various universities in Norway and the UK.

Dr. Kalim Siddiqui is an economist specialising in International Political Economy, Development Economics, International Trade, and International Economics. His work, which combines elements of international political economy and development economics, economic policy, economic history and international trade, often challenges prevailing orthodoxy about which policies promote overall development in less-developed countries. Kalim teaches international economics at the Department of Accounting, Finance and Economics, University of Huddersfield, UK. He has taught economics since 1989 at various universities in Norway and the UK.

References

- Acemoglu, D. and Robinson J. (2014) Why Nations Fail – The Origin of Power, Prosperity and Poverty, Crown Publishers, New York.

- Acharya, A. (2001) Constructing a Security Community in Southeast Asia: ASEAN and the problem of regional order, London: Routledge.

- Aris, S. (2009) “A new model of Asian regionalism: does the Shanghai Cooperation Organisation have more potential than ASEAN?”, Cambridge Review of International Affairs, 22(3):451-67.

- Asia (2050) Realising their Asian Century. https://www.adb.org/sites/default/files/publication/28608/asia2050-executive-summary.pdf

- Chao, W.C. (2022) “The Political Economy of China’s Rising Role in the Shanghai Cooperation Organization: Leading with Balance”, Chinese Economy, 55(4): 293-304.

- Mahbubani, K. (2008) The New Asian Hemisphere: The Irresistible Shift of Global Power to the East, New York: Public Affairs, 133–4.

- Mahbubani, K. (2011) “Asia Has Had Enough of Excusing the West,” Financial Times, 25 January.

- Nakao, T. (2022) The Riser of Asia Perspective and Beyond, Manila: Asian Development Bank.

- Shanghai Cooperation Organisation. (2022) http://eng.sectsco.org/

- Siddiqui, K. (2022a) “Ukraine-Russia War and the Impact on the Global Economy”, The World Financial Review, November/December, pp. 22-35.

- Siddiqui, K. (2022b) “Is a Global Economic Recession Looming,The World Financial Review, September-October, pp. 17-26.

- Siddiqui, K. (2022c) “Comparing the East Asian and Latin American Countries: The Role of Agricultural Reforms in the Economic Transformation”, The World Financial Review, July-August, pp. 7-18.

- Siddiqui, K. (2021a). “Can 21st Century be an Asian Century?”, Asian Profile, 49(1):1-19, March.

- Siddiqui, K. (2021b) “The Import Substitution Policy in the Post-Colonial Countries”, The World Financial Review, November-December, pp. 76-84.

- Siddiqui, K. (2021c) “The Bilateral Swap Agreements and the Demise of US Dollar”, The World Financial Review, September-October, pp. 56-64.

- Siddiqui, K. (2021d) “The Importance of Industrialisation in Developing Countries”, The World Financial Review, January-February, pp. 60-73.

- Siddiqui, K. (2021e). “The Political Economy of Industrial Policy”, The World Financial Review, May-June, pp. 58-66.

- Siddiqui, K. (2020a) “Can Global Imbalances Continue? The State of the United States Economy”, Argumenta Oeconomica Cracoviensia, 23(2):11-32.

- Siddiqui, K. (2020b) “The Rise of the Chinese Economy and Growing Concerns in the United States”, World Financial Review, September-October, pp. 40-9.

- Siddiqui, K. (2020c) “Prospects of a Multipolar World and the Role of Emerging Economies”, The World Financial Review, November/December, pp. 65-77.

- Siddiqui, K. (2020c) “Globalisation, International Trade and the Developing Countries”, The European Financial Review, August-September, pp. 60-71.

- Siddiqui, K. (2020d). “The US Dollar and the World Economy: A critical review”, Athens Journal of Economics and Business. 6(1):21-44.

- Siddiqui, K. (2019a). “Economic Transformation of China and India: A Comparative Political Economy Perspective”, Asian Profile, 47(3):243-59.

- Siddiqui, K. (2019b). “One Belt and One Road, China’s Massive Infrastructure Project to Boost Trade and Economy: An Overview”, International Critical Thought. 9(2):214-35.

- Siddiqui, K. (2018a). “The Political Economy of India’s Economic Changes since the last Century” Argumenta Oeconomica Cracoviensia, 19:103-32.

- Siddiqui, K. (2018b). “US-China Trade War: The Reasons Behind and its Impact on the Global Economy”, The World Financial Review, November-December, pp. 62-8.

- Siddiqui, K. (2016a). “Will the Growth of the BRICs Cause a Shift in the Global Balance of Economic Power in the 21st Century?”, International Journal of Political Economy 45(4):315-38.

- Siddiqui, K. (2016b). “International Trade, WTO and Economic Development”, World Review of Political Economy, 7(4):424-50, winter.

- Siddiqui, K. (2015). “Political Economy of Japan’s Decades Long Economic Stagnation”, Equilibrium Quarterly Journal of Economics and Economic Policy 10(4):9-39.

- Siddiqui, K. (2012). “Malaysia’s Socio-Economic Transformation in Historical Perspective”, International Journal of Business and General Management, 1(2):1-50.

- Siddiqui, K. (2010). “The Political Economy of Development in Singapore”, Research in Applied Economics 2(2):1-31.

- Siddiqui, K. (1989). “Political Economy of Underdevelopment in South Asia”, Klassekampen (in Norwegian), 14 & 15 March, Oslo, Norway.

- Siddiqui, K. (1985). “South-South Economic Co-operation and its Future Prospects”, Bergens Tidende, 4 October, Norway.

- Zhao, H. (2006) “The Shanghai Cooperation Organisation at 5: achievements and challenges ahead”, China and Eurasia Forum Quarterly, 4(3): 105-23.

{kind=link}