By Kalim Siddiqui

Why do some countries grow faster than others?

In this article the author discusses issues related to the economic growth and the ‘catching-up’ of developing with developed countries.

In the 1950s, the US per capita income, at least on the basis purchasing power, was estimated to be nearly five times greater than the world’s average income. Soon after World War II, due to the rapid growth of the West European and Japanese economies, this income gap was substantially reduced. A similar development was witnessed in the East Asian economies, when the rapid growth they had seen since the 1960s showed remarkable progress, which is especially apparent in South Korea, Taiwan, Singapore, Hong Kong, Malaysia and, since the 1980s, China, and the 1990s, Vietnam.

I will analyse the levels and trends prevalent to income inequality, both between countries and within countries, since the neoliberal (i.e., pro-market) economic reforms were introduced in the 1980s in the majority of countries worldwide, though of course at different levels.

Economic specialisation has been extensively shaped by the history of power relations, namely political economy. Similarly, international trade patterns have been significantly influenced by power relations. In the past, trade policy instruments have always been used by the European powers in their colonies. More recently, the East Asian countries have used the state to promote domestic industrialisation. Not only has trade protection in the past been used as an important tool of development strategy, it has also been used as a welfare policy to expand employment and, further, to build strong and efficient industrial sectors. In contrast, in the late 18th and 19th centuries, economic activity in the colonies was based around industrial policies that were designed to favour imperial interests, which resulted in ruining the manufacturing sector in China and India through the so-called ‘free trade’ policy (Siddiqui, 2018a).1 The supporters of free trade and trade liberalisation conveniently ignore economic history. The recent success of the East Asian economies was largely due to export promotion, easy access to Western markets for their products, state intervention, and industrial policy rather than trade liberalisation, as claimed by the neoclassical (also known as mainstream) economists (Siddiqui, 2016a).2

The process of decolonisation after World War II, did in fact, ultimately mean an end to foreign government domination and control over foreign companies. It was hoped that such policy changes would make room, and extend protection for domestic companies to grow and achieve economies of scale. However, this did not happen. Soon after independence, between 1950 and 1980, most of the developing countries witnessed higher growth rates than in previous decades. However, since the 1980s, due to a number of domestic and international factors including the debt crisis, most of the developing countries contacted the IMF for loans; in return, they were required to adopt a ‘Structural Adjustment Programme’.8

Globalisation and Economic Liberalisation

Globalisation and inequality has been in discussion for long time among the economists. The reason for this continuing debate seems to be that of neoliberal reforms including trade and financial liberalisation and its effects on global inequality. Some studies have pointed out that growth of income inequalities both within and between countries are largely due to globalisation (Wood, 1998). Similar points have been made by John Pilger. He observes (2002:2): “In this world, unseen by most of us in the global north, a sophisticated system of plunder has forced more than ninety countries into ‘structural adjustment programmes’ since the eighties, widening the divide between rich and poor as never before. This is known as ‘nation building’ and ‘good governance’ by the ‘quad’ dominating the World Trade Organisation (US, Europe, Canada and Japan) and the Washington triumvirate (the World Bank, the IMF and the US Treasury) that controls even minute aspects of government policy in developing countries. Their power derives largely from an unrepayable debt that forces the poorest countries to pay $100 million to western creditors every day.” He further observes, “Promoting this are the transnational media corporations, American and European that own or manage the world’s principal sources of news and information.”4

An important aspect of globalisation is trade and capital liberalisation. If the capital from the developed countries is moving into the manufacturing sectors in the developing countries, then this would adversely affect manufacturing employment in the former. The migration of capital from the developed to the developing countries could break the segmentation that existed in the world economy during the colonial period, which implies that the salaries of workers in the developed countries are influenced by developing countries’ labour reserves. Under current globalisation and with capital liberalisation, as long as developing countries’ labour reserves are not exhausted, real wage rates around the world would see little increase even as labour productivity increases, which means that the share of wages in world output would come down while the share of surplus increases.8 In the current era of globalisation, capital is far more internationally mobile than it has ever been in its entire history. In fact, the colonial period was characterised by a segmentation of the world economy where capital from the metropolis did go to the colonies but to limited primary sectors such as plantations and mines, while the labour from the latter was not allowed to move freely to the former.

According to estimates by Pritchett (1997) the income gap between rich and poor has widened sharply between 1870 and 1990. He calculated that the standard deviation of per capita income, a more inclusive measure of inequality, which rose from 0.64 to 1.06 over the same period. Since 1950s both rich and poor countries had relatively higher growth rates than previous period. Dutt (1992) found that role of Atlantic salve trade, use of slave labour in Americas and British colonialism in India had created structural asymmetries that perpetuated global inequality.17

According to Adam Smith some regions perform less than other due to number of reasons including, some devoting more resources to manufacturing, while other to agriculture. Some countries may have better and strong policy environment such as property rights. Some countries have low concertation of population and also have less-developed infrastructure. Smith also emphasised that the division of labour could extend further in manufacture than in agriculture and the possibility of cost reduction is greater in the former than in the latter. He stressed that those countries first to industrialise will be most likely to sustain competitive edge in manufacturing.

The neoclassical economists support trade liberalisation and argue inequality arises due to demand and supply of labour for different skills. They predict the level of inequality should vary in an inverse ‘U’ shape with trade and economic liberalisation. The Kuznets curve first showed inequality to be widening as trade expanded as a result of industrialisation. The developed countries were endowed with skilled labour, while the developing countries have unskilled labourers. David Ricardo, in his book Principles of Political Economy and Taxation (1817), argued that all countries could benefit from free trade, even if a nation was less efficient at producing goods than its trading partners. His trade theory claims under such a situation, both types of nation will benefit from trade. A more recent extension of this theory, the Stolper-Samuelson model of ‘comparative advantage’, argues that as trade increases, resources will shift to export-oriented sectors and, with the adoption of free trade, the developed countries will export skilled labour products and technology and import labour-intensive goods; thus, in the former group, demand for skilled labour increases but falls for unskilled labour, while the opposite will happen in the latter. Contrary to these propositions, the study on inequality during the 1990s by Cornia and Addison (2003) found that it has widened in 48 countries, with 16 remaining the same and nine seeing a slight improvement in the sense of narrowing the income gap.

When we look at past economies and incomes, for instance, during the 16th century, the income levels in Europe, Asia, Africa and Latin America showe that average per capita income was nearly 1:1. However, in the first decade of the 20th century, the ratio of average per capita incomes in Europe and North America and the developing countries had risen to 6:1, and remained so until the mid-20th century. Most of the wealth of the developed countries was built on slavery and colonial expropriation. This was also the period when the colonies began to gain their independence. Deepak Nayyar’s (2013) study of the post-independence global economy found that between 1950 and 2010, the developing countries not only saw their share of the world population rise, but also saw the same for their average per capita incomes. Moreover, during this period the developing countries also saw an increase in their share of the global economy in areas such as industrial production, international trade, capital investments, and exports of manufacturing goods. However, such development could only be sustained as long as these countries continued to increase their investments in education, health and technology.

Why do some countries grow faster than others? Adam Smith (1776) has tried to analyse the nature and causes of the wealth of nations. Economists differ in opinion about the policy that are actually needed to achieve rapid economic growth. Neoliberals suggest that economic success is due to the adoption of polices such as assigning a greater role for market forces, economic liberalisation, open economies, privatisation, and free trade policies. This is associated with the Washington Consensus (i.e., structural adjustment programme) and said to be a prerequisite for rapid growth and prosperity. The universal recipe suggested by the international institutions for rapid growth is a ‘one-size’ policy for all countries, while critics stress that a number of policy measures must be taken to achieve sustainable and rapid growth such as human resources development, strong institutions, diversification of domestic economy, amongst others.

However, the gains possible from trade liberalisation have been exaggerated by its proponents. The developing countries’ agricultural exports have declined due to increased competition as more developing countries attempt to export more of the same agricultural commodities. For instance, as Malaysia began to increase its export of cocoa, global supply accordingly rose and cocoa prices fell significantly across the world market in the 1980s. Similarly, after Vietnam sharply increased its production of coffee for export in the 1980s, world coffee prices fell drastically.

One should not ignore the fact that European businesses benefitted the most from colonisation by establishing control over the profitable sectors in the colonies in order to enhance accumulation, and did so with the full support of their governments. There was hardly any concern for the deterioration of local people’s wellbeing. For example, in 1944, the US President Roosevelt remarked on Indochina (i.e. Cambodia, Laos and Vietnam). Amsden (2007: 104) notes: “France has had the country – thirty million inhabitants – for nearly one hundred years and the people are worse off than when they were at the beginning…. The people of Indochina are entitled to something better than that.”5

There are a number of examples when European colonial powers did whatever it took to protect their business interests. As Amsden (2007: 110) argues: “In 1914, Shell began producing crude oil in Mexico. Mexico’s hostility toward foreign companies started in the early 1920s, when it demanded a higher share of profits and better conditions for oil workers. The oil companies refused. In March 1938, foreign oil holdings were nationalised. Great Britain broke relations with Mexico and, together with the US, started to put pressure on the Mexican government for compensation.”5 The punishment for nationalisation [of foreign companies] was even harsher in Iran in the early 1950s. Further Amsden (2007: 111) notes: “The British-owned Anglo-Iranian Oil Company refused to grant a comparable demand from Iran’s popularly elected parliament, headed by Dr Mossadegh. Iran’s economy was sinking, but United States withheld a promised loan, and the World Bank, whose president is always American, also reneged on co-lending. After nationalisation, all American oil companies refused to purchase and market Iranian oil… By 1953, the British Navy had established a blockade in the Arabian Gulf to stop shipment of oil to willing buyers… Shah of Iran, an American puppet akin to Ngo Dinh Diem in Vietnam, retook the Peacock Throne with the help of the army, assisted by CIA.”5

In 1956, control over the Suez Canal was seized by Egypt’s President Nasser, who wanted to build the Aswan Dam to both provide electricity to the Egyptian people and its industries, and also for use in irrigation to expand agricultural cultivation beyond the Nile basin. Moreover, the reaction to Egypt’s attempt to expand its economy was not taken as a positive development by the developed countries. As Amsden (2007: 112) argues: “For finance, Nasser had lined up a loan involving the US, the World Bank and the UK. But in the spirit of nonalignment, Nasser asked Britain to remove its air base from Egypt. The US then declined the loan, to repay it… although in theory, the Bank was an independent, multilateral lending organisation.”5

It seems that the collapse of the Soviet Union and, subsequently, its economy in 1990 made the restoration of a single world economy possible for first time since 1914, as based on free trade balanced budgets and unrestricted capital movements, which is a known pre-World War I recipe for economic success implemented at that time within the colonies by the European powers. During that period, these colonies witnessed the fact that the policy of self-regulating markets proved to be illusory; as such, this policy brought famine, deterioration in living conditions, and created mass poverty.

Economic Transformation of East Asia

Moreover, the East Asian economies have witnessed the rapid expansion of their industrial sectors over the last four to five decades, and the rapid growth of the these economies, including that of China, has facilitated an associated structural transformation; indeed, all such countries have followed a course of state intervention so as to promote exports and industrialisation, though of course this intervention was enacted at different levels depending on the country in question.

The transformation of East Asia was driven by rapid economic growth. Over a period that spanned almost five decades, i.e., 1970–2017, the GDP growth rate in East Asia was more than double that in the industrialised countries and almost twice that of the world economy as a whole.7 This was associated with a dramatic change in the composition of output and employment. Economic growth drove structural change from the demand side as the income elasticity of demand for industrial goods was higher than that for agricultural goods, while the income elasticity of demand for services was even higher than that for industrial goods. Structural change drove economic growth from the supply side by transferring surplus labour from low productivity employment in agriculture to higher-productivity employment in industry and services. Structural change was a driver of economic growth in Asia, unlike Latin America and Africa where it was not. The rapid industrialisation, with a marked increase in the share of the manufacturing sector, also provided opportunities for employment.

In recent decades, the rapid and highly successful growth in China has attracted huge interest among academics and, indeed, policy makers in the developing countries. However, in China, institutions have played a crucial role in this growth; by contrast, the majority of developing countries have poor or undeveloped institutions. Due to its size, the huge expansion of the Chinese economy will clearly have a huge concomitant impact on the world economy and will certainly appeal to the poorer economies, as the Russian economy did in the 1950s. Moreover, over the past the last few decades, the East Asian countries including China have used state intervention, i.e., dirigiste, to increase their growth rates and achieve rapid industrialisation.

The modernisation and economic progress seen over the last few decades has been possible due to the international divisions of labour that allowed the East Asian countries to expand industrialisation, diversify their economies, increase productivity and enhance exports, despite the fact that wages and working conditions were generally far from ideal.

Many of the policies that the present developed countries adopted in the early phase of their modernisation in the 19th century are no longer available to the developing countries. Economic growth has been uneven among the developing countries, where a few have experienced higher growth than others. Since the debt crisis of the 1980s and 1990s, Africa and Latin America have seen their growth rates slow down. This phenomenon is also known as the ‘lost decades’.

Privatisation of state-owned enterprises, which is part of the neoliberal reforms, has facilitated the entry of foreign corporations. However, their ownership was transferred to foreign owners, which means that only the fittest would survive (i.e., Western companies). Since the debt crisis, companies operating in the developing countries found it difficult to borrow money in order to fund their investments.18 The companies, who were desperate for capital and any inflow of capital, seemed to be an attractive proposition.6 However, the problem was that those who needed the most (the poorest countries) received almost nothing. The other problem was that for state enterprises, privatisation meant getting rid of loss-making enterprises, with foreigners wanting to buy only the best-performing companies, many of which did not need to be privatised.

Since the early 1990s, neoliberal reforms, including a lower tax burden on the rich, privatisation, and increased pressure from the developed countries and international financial institutions, have led to the sharp accumulation of wealth within the top elites households and global corporates. Recent attempts at globalisation have further facilitated the emergence of global oligopolies and monopolies, which has led to an increase in monopoly rents by the global corporations as accompanied by the weakening of trade unions and increased unemployment, and which have indeed reduced workers’ bargaining power.

According to the Lewis model, in underdeveloped economies (i.e., dual economies) labour is available to the urban industrialised sector at a wage determined by minimum levels of existence in traditional family farming because of ‘disguised unemployment’ in agriculture, where there is practically an unlimited supply of labour and the possibility of industrialisation, at least in the early stages of development. At some later point in the history of dual economics, the supply of labour is exhausted which can only be addressed by an increase in wage, which will in turn draw increasing amounts of labour away from agriculture. Lewis’ main point is that the eventual wide-spread economic growth and development can be initially fuelled by large supplies of cheap labour that result from the initial conditions of economic duality. The Lewis Model supports capital investment in order to raise levels of domestic investment.16

The crucial factor in recent globalisation is the role played by foreign capital. However, despite the overstated role of the foreign capital in the rapid growth of the East Asian economies, the role of FDI in these economies was actually relatively modest (Siddiqui, 2014), accounting for less than 2% of the gross domestic capital formation during the high growth rate periods in Japan, South Korea and Taiwan compared to the developing countries’ average of 5-6% and the greater reliance in the South East Asian countries on foreign capital inflows.6 Whilst FDI had significantly grown in the previous decade, global FDI investment reduced by 23% in 2017 to $1.43 trillion (Figure 1), from a revised $1.87 trillion in 2016, presenting concerns for long-term sustainable industrial development (UNCTAD, 2018).

The inflow of capital is an important component of economic development for host countries in both developed and developing countries, with globalisation the focus on stimulating inward FDI flows to generate employment has increased. It is emphasised that host countries may gain additional ‘spill over’ benefits from FDI such as product, process, and distribution technology, knowledge transfer, management techniques and marketing. However, the realisation of these benefits between developed and developing countries can be profoundly different. According to UNCTAD’s 2016 Report, during the 1990s more than 80% of the foreign capital in the world consisted of mergers and acquisitions (M&As).15 Even as far as the developing countries were concerned, most such have been acquisitions rather than mergers. In the developing countries, with the exception of China, M&As have mainly involved acquisitions, particularly during the debt crisis and economic distress involving foreign acquisitions.

In 2010, the average share of the FDI in capital formation was 4.4% worldwide, 5% in the EU, 6.5% in the developing countries (including raw materials and plantations) and region-wise was 6.9% in Latin America, 5.3% in Africa, 1% in the Middle East and 11% in China. China is now somewhat venerated by the IMF and World Bank. However, neither China nor India deregulated their financial markets to inflows and outflows of capital.9 If past experience can be learnt from, then it is clear that the successful economies have relied on building manufacturing industries, education and government-promoted domestic business through a hybrid institutional structure.

Comparative Growth Performance:

The growth rates of the emerging economies are higher than the average world GDP growth rates. This is due to a number of reasons, including both national and international economic policies. Figure 2 indicates annual GDP growth in the developed and developing economies from 1990. The period from 2002 to 2007 does show acceleration of growth across economies, but that came to an end in the collapse of 2008-09, and since then GDP growth rates have been similar to those of the 1990s.

Table 1 and 2 show the per capita GDP growth of the developed and developing economies from 1978 to 2015. Here again I find China is on the top of the list with average annual growth of 7.4% and the growth compared to US is estimated to be 461%.

Soon after independence the developing countries saw that industrialisation is imperative towards removal of backwardness, to increase productivity and to diversify its economy. For this task nearly all the developing countries adopted import substitution policies in the manufacturing sector. The exports from the developing countries rose from US$ 20 billion in 1950 to US$ 600 in 1980 and nearly US$ 6400 billion in 2010, but imports rose rapidly as well. The developing countries share in the world exports was 34% in 1950, fell to 19% in 1970, 24.2% in 1990, rose to 31.9% in 2000 and 42% in 2010, while their share of imports in the world economy was 29.6%, 18.5%, 23.1%, 28.8% and 38.9% respectively. The sharp rise since 2000 appears to be due to China’s rising trade (UNCTAD, 2016).15

Since their independence in the 1950s and 1960s, the developing countries share in the global GDP has risen and by 2015 their total share is over 44%, double than in the 1970s. The industrial sector in the developing countries is also increasing and their share of value added in global manufacturing output increased from 13% in 1970 to more than 45% by 2015. However, the region wise increase in manufacturing output was highly unequally distributed. For instance, Latin America’s manufacturing share of global GDP has only marginally increased to 8% between 1970 and 2015, while for manufacturing share of Africa has remained the same i.e. less than 3% for this period. Africa’s share in manufacturing value added in 2015 was only 2%, as it was in 1970. As the Chinese economy is “catching up” fast and also the Indian economy, both are re-emerging as most rapidly growing economies and also major contributors to overall world’s output growth in 21st century.7 China has become the second largest economy after the US, which is a remarkable development of the 21st century.6

Moreover, the patterns of trade are changing as well. For example, the share of manufactures in developing countries exports rose from 12% in 1980 to 64% by 2015, nearly half of this consisted of medium and high technology products. Another key development has been the rise of services in their export components of the developing countries such as information technology and e-commerce. Global income inequality could be measured in a number of ways: the first method of estimation adopted is inter-country inequality, which treats each country as individual and inequality measured is that of the distribution of per capita GDP among countries. The second method is supposed to be a little improved as it takes into account the population size of a country. The third estimation method takes into account the inequality of the world income distribution by combining inequality distribution in individual countries together with per capita income.

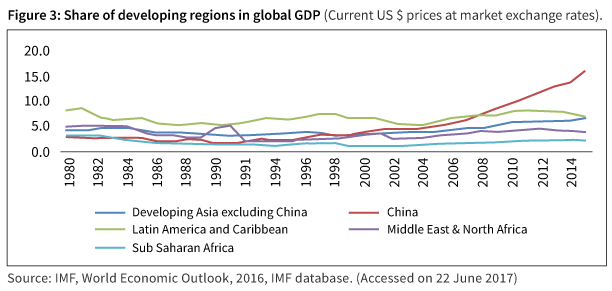

Figure 2 shows the changing share of the GDP of the major developing regions. Here China is plotted separately to show its growing economic share. China’s share in the global GDP rose from 3% to 15% between 2005 and 2016. This was the time when China’s share of the global GDP at market exchange rate rose rapidly to ten percentage points. In fact, such a rapid change in China’s share alone explains 87% of the entire decline of the developed economies for the period of last thirty-five years. Figure 3 indicates the changes in the share of developing regions in global GDP and the largest developing Asian economies excluding China. I find that India’s share in the global GDP has been among the largest and its share increased from 1.8% in 2005 to 3% in 2015. However, it is much less than China, whose share is three times of India’s aggregate share. Indonesia and South Koreas share in the global GDP has increased.17

However, if we exclude China then the share change of other regions provide us a different picture. For example, the Latin American region in the 1980s had experienced a decline, which is also known as lost decade. The region’s economies recovered in the 1990s and early 2000s. Their share in global GDP rose by 5% in 2003 to 8% in 2011, but thereafter again began to decline. The Middle East countries had experienced a rise in the share due to largely high oil prices, but for the last 2 years due to collapse in oil prices, its share in the global GDP has fallen. The sub-Saharan Africa had a long period of stagnation and economic decline i.e. from 1980 to 2002 and since then their share in the global GDP has slightly gone up to 1.1% in 2002 to 2% in 2015. However, its share in global GDP is still below compared to its 1980s share of 3%. In short, among the developing regions, only Asia’s share to global GDP is rising. Due to on-going global recession in the advance economies, the BRICS countries too are facing slowing down economic growth rates and declining their export markets.

During the last three decades, there have been huge economic changes taking place globally and structural changes and changes in patterns of trade have also taken place both in advanced and developing countries. However, some developing countries have achieved faster growth rates than the developed economies, particularly China, India, Indonesia and Turkey. However, they constitute a small number among the developing countries, but accounts large number of its population. In fact, international inequality in terms of distribution of per capita incomes among the countries’ population has declined in the last two decades.12 Trade liberalisation and with the removal of trade barriers did have some positive impact on country’s growth but not all the developing countries have benefitted from it.13 I also find that with globalisation, transnational companies largely from the developed economies driven by competition at home for markets8 and higher wages and low returns, driven rising completion for markets, seeking to cut their costs have started investing abroad and supported by the rise of global value chains since the 1990s.3

As the Chinese economy is “catching up” fast and also the Indian economy, both are re-emerging as most rapidly growing economies and also major contributor to overall world’s output growth in 21st century. The two countries only in the recent past were only known as marginal economies, but now China has become as the second largest economy after the US, which is a remarkable development of the 21st century. However, the global GDP share of Latin America has marginally increased to 8% between 1970 and 2010, while Africa has remained the same i.e. less than 3% for this period. Africa’s share in manufacturing value added in 2011 was only 2%, as it was in 1970.

Moreover, the persistent gap between rich and poor countries seems to be the dominant features of the modern history (Reinert, 2007).14 The Economist (2014) insist that it would take developing countries as a group (excluding China) more than a century or even longer period as three centuries to catch up with the income levels of the rich countries. The average life expectancy in the developing countries has risen in recent decades, but still in the sub-Saharan Africa it is only 56 years compared to 78 years in the United States. It appears that the Western world is punching too far above its weight which could be the main root of on-going crisis. The future cannot be just an extension of the past. More needed to be done in the developing countries, especially those who still have widespread poverty in terms of economic policies and it may involve structural changes. Todays’ developed economies did not attain that status naturally and overnight, but they formed polices and worked consistently to achieve those goals.

Growing Inequality

When we analyse the issue of worldwide inequality we find that, across the countries, the gap between the rich and poor declined in the period between 1950 and 1980. However, since the 1980s, both in the developed and developing countries, the gap between the rich and poor has widened. Thomas Piketty’s (2014) book Capital in the Twenty-first Century considers an immense amount of empirical research into the distribution of wealth and income across the population for a number of developed capitalist countries. Private wealth is concentrated in the hands of a few rich families; only World Wars I and II and the Great Depression disrupted this pattern. High taxation on the rich and the rise in benefit payments, i.e., the growth of the welfare state, caused wealth to shrink dramatically, and ushered in a period in which both income and wealth were distributed in a relatively egalitarian fashion, where the economic policy then adopted was known as the Keynesian model. However, since the 1980s crisis in the West, this has given way to the adoption of neoliberal economic policy, and as a result the inequality in income and wealth has been reasserting itself for some time.8 By various measures, Piketty reasons, the importance of wealth in modern economies is approaching levels only last seen prior to World War I.

The period between 1950 and 1970 represents a remarkable break, which created an impression that capitalism had become more egalitarian, that inherited wealth had ceased to matter as much as before, that the individual’s “ability” rather than patrimony determined his or her position in the socio-economic hierarchy, and so on. To be sure, the bottom 50% of the population in most capitalist countries could barely be said to own much wealth at any time, and hence hardly earned any income from wealth; however, the period from 1950 to 1970 saw the middle class raise its share of wealth and income at the expense of the rich. The radical political economy argues that the distribution of property generates conflict and struggle, thus determining income distribution. This has been witnessed in the form of the positive relationship between union strength and greater equality. As with the recent globalisation, the organised strength of unions has been weakened while the organised strength of capital has strengthened, in essence because capital can move globally with little or no hindrance, while workers clearly cannot.9

The unequal distribution of income affects employment levels in capitalist economies. The distribution of purchasing power bares no relationship to the distribution of peoples’ needs. Under a monopolistic industry structure, income tends to be distributed towards profit and not wages, which means a higher proportion, is saved rather than consumed. Low levels of aggregate demand and lack of investment present a problem for prosperity and growth.8

The above assumes the existence of a reserve army of labour, without which a capitalist system, as Marx showed, simply cannot function. Inequality also arises as a result of the dispossession of peasants and traditional petty producers through what Marx (1992) called the process of “primitive accumulation of capital”, which is very much underway in the current era of globalisation, and also the inequality that arises due to the “centralisation of capital”.10 Marx analysed centralisation of capital in terms of the fact that big capital drives out small capital due to the former’s superior capacity to introduce new technology.10 Big capital has the capacity to find prospective investment projects with higher rates of return, and it can do so within the global arena since its capacity to “go global” is considerably greater than that of small capital.

Trends in global inequality have been debated in the past. The 19th century saw the rise of capitalism in Europe, which Marx (1992) pointed out inevitably leads to extreme wealth concentrations, while its defenders argued that the gap between rich and poor would narrow in the future. There has been an increase in wealth concentrations in recent decades thanks to the lobbying power of the elites to influence any associated decision processes. Statistically, in both developed and developing countries, the concentration of wealth within the elite class has increased significantly in recent decades. One possible explanation for the rise in inequality seems to be the policies of neoliberalism, which have reduced the taxation on the rich and a decline in workers’ bargaining powers and trade union activities due to current globalisation.3

Four decades ago Margret Thatcher became Prime Minster in the UK with the argument that allowing the rich to get richer would benefit the entire society. She adopted pro-market policies, which included: free movement of capital, lower taxes on rich, lower welfare spending, weaker trade union and privatisation of state-owned industries. All these policies, it was claimed ‘would unleash a wave of entrepreneurship’ that would lead a faster growth, higher investment and prosperity for everybody. However, four decades later, the picture is quite different. For example, the share of income going to top 1% has risen from the 3% in 1979 to 8% at present. In 2018, the chief executive of a FTSE 100 company earned 145 times the salary of the average worker, up from 7 times two decades earlier. However, those on the lowest income earn little more than they did in 1990. A cursory look at what happened to growth, productivity, investment and trade balance shows that UK’s economic performance has not improved. Moreover, the weakening of trade unions has allowed capital to increase its share of national income at the expense of labour. Lax corporate governance has allowed executives to raise their earnings each year, and also cuts in the top rate income tax have allowed the rich to multiply their wealth further.

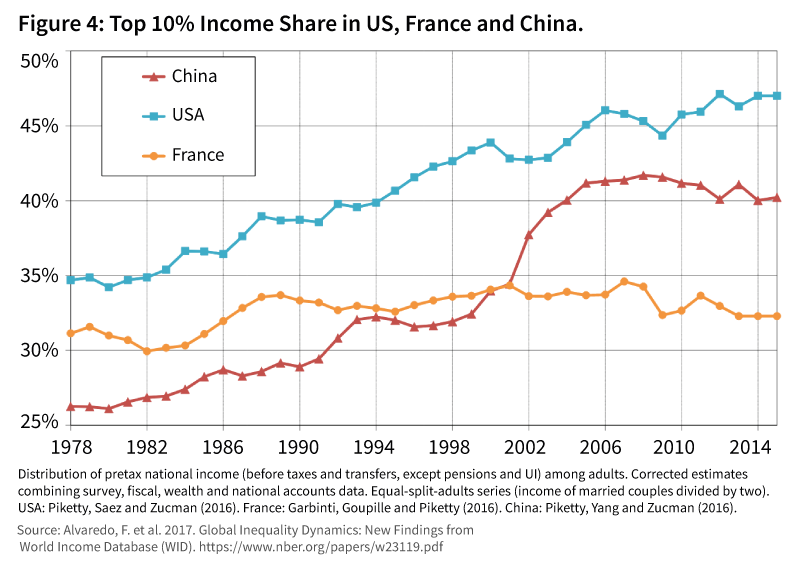

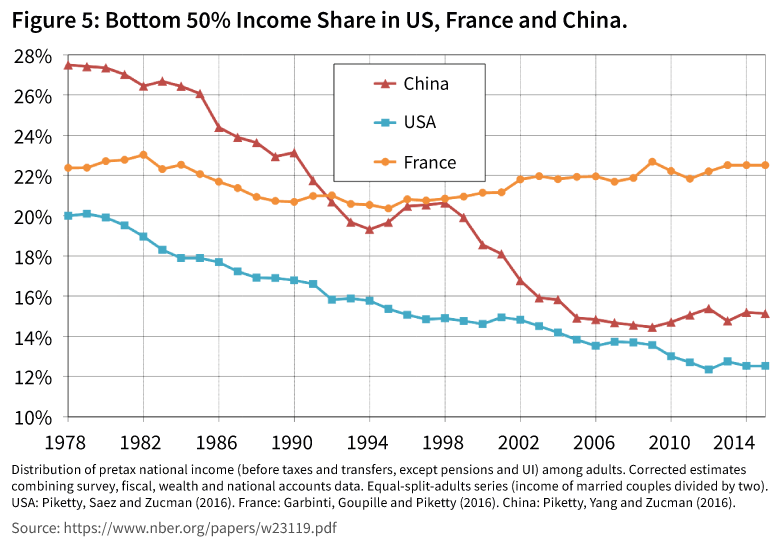

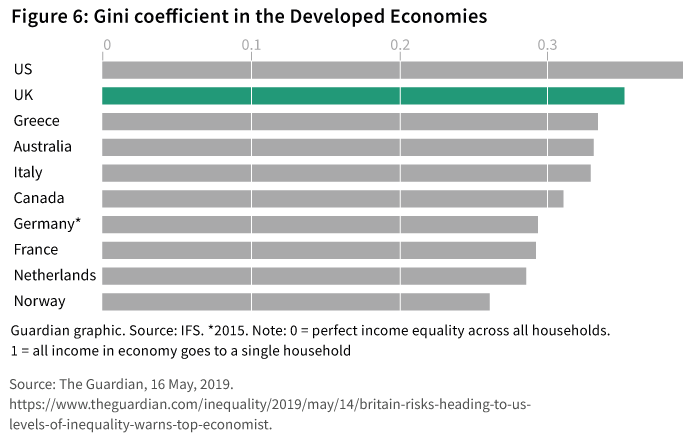

The Gini coefficient focusses on the distribution of income or wealth of a nation’s residents, and is the most commonly used measurement of inequality. As noted earlier, the Gini coefficient rose from 18.3% in 2013 to 85.4% in 2018, which clearly tells us that growth has only benefitted the rich. The Gini coefficients in the developed countries range between 0.3 and 0.4 for income and vary between 0.5 and 0.9 for wealth. According to the data, the estimated share of wealth held by the top 1% of households varies across the range of 15-35%. Credit Suisse (2016) estimates that the level of global wealth inequality between 2000 and 2012 increased by 60%. Table 3 indicates the statistics from 2000 to 2012. It shows that the 2012 Gini coefficient in Brazil was 81.2, China, 68.9, and India, 81.3, while in Japan it was 59.6. As Figure 4 also shows, the top income share for the US, France and China has risen sharply since the 1980s, while the bottom 50% income share has consistently declined for these countries, which is shown in Figure 5 (also see Figure 6).

China, the East Asian countries and India have relatively low income inequalities and have also managed to invest in and build large industrial sectors, in contrast to the Latin American countries such as Argentina, Brazil and Mexico who were unable to build domestic industries and, further, show greater inequalities. In the latter group, the foreign capital largely went into acquisition and mergers, which resulted in increased control by foreign corporations. Only in the last decade with the Lula Presidency, has inequality reduced to any extent, due in this case to strong government initiatives.

According to Stockhammer (2015), the current crisis in the developed countries is due to rising inequality which is a result of the financial deregulation in the last decades of the 20th century. He identified four factors which contributed to the crisis: 1) rising inequality creating downwards pressure on aggregate demands since the poor have a higher propensity to consume compared to the rich; 2) international financial deregulation, which has allowed countries to run current account deficits; 3) despite stagnant wages and welfare cuts, the poor have been under some considerable social pressure to attempt to keep up with social consumption norms; and, finally, 4) the rich have received disproportionately more money, which has increased the propensity to speculate and in speculation activities.11

The changes to the financial system, i.e., financial deregulation in 1999 in the US, allowed the property and estate sector financial bubble, which in turn allowed for the massive increase in household debt, which in turn contributed to increased consumer demand.9 At the same time, capital inflows helped to keep interest rates low, which has further fuelled debts. Since the 1980s wage shares have fallen by 10 percentage points in the EU, and indeed in Japan. The decline in the US and UK was a bit lower, at 5 percentage points (Stockhammer, 2015). In the US, the income of the top 1% has risen in terms of its share of national income from 8% to more than 22% in 2010. Similar trends are seen in other EU countries. Stockhammer’s (2015: 941) study, conducted by using panel analysis for 71 developing and developed economies, found that “financialisation, globalisation and welfare retrenchment all have contributed to falling wage share…”11

Inequality has risen almost everywhere in South Asia since the 1990s. Consequently, in India, for example, this rapid growth has not always transformed into improving living conditions amongst the populace, particularly in periods when job creation was slow or where income inequality was high to start with. Economic growth had a greater impact on the living conditions of ordinary people where the creation of employment was rapid or where the initial income distribution was less unequal. The spread of education in society and the delivery of health services to the general populace have directly contributed to people’s wellbeing and were thus constitutive of development. Better education and health were also drivers of economic growth via productivity growth.

In conclusion, I find that colonisation left a huge devastation not just in the economies of the developing countries but also had lasting social and political impact. Their economies fell behind until mid-20th century. However, after they became independent, their economies began to witness higher growth rates than previous decades. Almost all the Asian countries soon after independence adopted ambitious drive towards industrialisation, where state played a leading role. However, the poorest countries have not been able to converge and except largely the two largest ones,12 namely China and India have experienced rapid growth rates and economic changes in recent decades.13

The developing countries need to break the chains of static ‘comparative advantage’ that for centuries has forced them to maintain mining and planation activities and other low value commodity production.14 They need to free themselves in order to choose their own model of development as appropriate to their specific demands and needs. The most successful late developer countries (such as the East Asian countries including China)15 started out with agrarian reforms and also built industries, subsequently addin further value of all kinds of skills and improving their competitiveness in a number of high value industries. From this discussion, it emerges that since neoliberal economic policy was adopted, inequality has increased worldwide. Therefore, there is a need for government to play a greater role in the management of the economy. A new international economic order is needed which promotes greater economic sovereignty, diversification of economies and increased democratisation of international economic relations, which will also encourage greater south-south economic cooperation and trade.

About the Author

Dr Kalim Siddiqui is an economist, specialising in International Political Economy, Development Economics, International Trade, and International Economics. His work, which combines elements of international political economy and development economics, economic policy, economic history and international trade, often challenges prevailing orthodoxy about which policies promote overall development in less developed countries. Kalim teaches international economics at the Department of Accounting, Finance and Economics, University of Huddersfield, U.K.. He has taught economics since 1989 at various universities in Norway and U.K..

Dr Kalim Siddiqui is an economist, specialising in International Political Economy, Development Economics, International Trade, and International Economics. His work, which combines elements of international political economy and development economics, economic policy, economic history and international trade, often challenges prevailing orthodoxy about which policies promote overall development in less developed countries. Kalim teaches international economics at the Department of Accounting, Finance and Economics, University of Huddersfield, U.K.. He has taught economics since 1989 at various universities in Norway and U.K..

References:

1. Siddiqui, K. 2018a “Imperialism and Global Inequality: A Critical Analysis”, Journal of Economics and Political Economy, 5(2): 266-291.

2. Siddiqui, K. 2016a. “International Trade, WTO and Economic Development”, World Review of Political Economy, 7(4): 424-450, winter, Pluto Journals

3. Siddiqui, K. 2017a. “Globalization, Trade Liberalisation and the Issues of Economic Diversification in the Developing Countries”, Journal of Business & Economic Policy 4(4):30-43.

4. Pilger, J. 2002. The New Rulers of the World, London: Verso.

5. Amsden, A. H. 2007. Escape from Empire: The Developing World’s Journey through Heaven and Hell, Cambridge, Massachusetts: MIT Press.

6. Siddiqui, K. 2014. “Flows of Foreign Capital into Developing Countries: A Critical Review”, Journal of International Business and Economics 2(1):29-46, March.

7. Siddiqui, K. 2016b. “Will the Growth of the BRICs Cause a Shift in the Global Balance of Economic Power in the 21st Century?” International Journal of Political Economy 45(4): 315-338, Routledge Taylor & Francis.

8. Siddiqui, K. 2017b. “Austerity as a Tool of Fiscal Consolidation: Theoretical and Empirical Perspective”, in Public Finance and the New Economic Governance in the European Union, (edi.) S. Owsiak, pp.116-166, Warsaw: Wydawnictwo Naukowe.

9. Siddiqui, K. 2017c. “Financialization and Economic Policy: The Issues of Capital Control in the Developing Countries”, World Review of Political Economy 8 (4): 564-589, winter, Pluto Journals.

10. Marx, K. 1992. Capital: A Critical Analysis of Capitalist Production, vol. 1, pp.708, London: Penguin Classics (first published 1848).

11. Stockhammer, E. 2015. “Rising Inequality as a Cause of Present Crisis”, Cambridge Journal of Economics, 39: 935-958.

12. Perkins, J. 2006. Confessions of an Economic Hit Man: The Shocking Story of How America Really Took over the World, New York: Penguin.

13. Siddiqui, K. 2009. “The Political Economy of Growth in China and India”, Journal of Asian Public Policy 1(2):17-35, March. Routledge, Taylor & Francis.

14. Reinert, E.S. 2007. How Rich Countries Got Rich and Why Poor Countries Stay Poor, London: Constable.

15. Siddiqui, K. 2016c. “World Trade Organisation, International Trade and Prosperity”, International Journal of Social and Economic Research 6(2):1-28, April-June.

16. Siddiqui, K. 2018b. “Capitalism, Globalisation and Inequality”, The World Financial Review, November/December, pp. 72-77.

17. Siddiqui, K. 2019a. “A Century of India’s Economic Transformation: A Critical Review”, Journal of Perspectives on Financing and Regional Development (JPPD), 7(1): 1-22, January-February.

18. Siddiqui, K. 2019b. “The Political Economy of Essence of Money and Recent Development”, International Critical Thought 9(1): 85-108. Taylor & Francis Group, Routledge.

{kind=link}