The share of U.S. dollar in international payments is disproportionate relative to America’s eroding global position and depends on international goodwill that Washington is shunning. U.S. dollar is changing from a safe haven to a safe house that’s costly and vulnerable. The end of America’s “exorbitant privilege” looms in the horizon.

The privileged position of the U.S. dollar relies on international multilateralism, which shuns unilateralism but which is being undermined by the Trump administration’s “America First” doctrine and the polarized U.S. economy.

Washington’s contested sanctions and tariff hikes are putting U.S. dollar at risk as a global currency reserve. You can’t have your cake and eat it, too.

Anomalies herald a paradigm shift.

The Euro Anomaly

In early fall, as trade tensions once again escalated between the Trump White House and Brussels, the outgoing European Commission President Claude Juncker gave an exceptional speech that raised the eyebrows across the Atlantic: “It is absurd that Europe pays for 80 percent of its energy import bill – worth 300 billion euros a year – in U.S. dollars when only roughly 2 percent of our energy imports come from the United States… The euro must become the face and the instrument of a new, more sovereign Europe.”

Juncker is not just any politician. The Luxembourgian was the longest-serving head of any national government in the European Union (EU). From 2005 to 2013, he served as the first permanent President of the Eurogroup, the elite of finance ministers. In Brussels, his tenure encompassed the climax of the global financial crisis and the European sovereign debt crisis. That’s when Europeans had to come up with real collateral for lost assets, whereas in the U.S., the Bureau of Engraving and Printing needed just a few cents to produce a $100 bill. Decades ago, alternatives were few. But that’s no longer the case.

Not only does the U.S. dollar undermine the interests of major advanced economies. It also penalises the future of emerging and developing economies.

The Emerging Market Anomaly

Recently, foreign exchange rates in emerging economies – particularly Argentina, Turkey, Brazil, and Russia – have suffered significant damage, due to the strengthening U.S. dollar. In each case, geopolitics has played a vital role, from Argentina’s economic destabilisation and Brazil’s soft coup to Turkey’s currency pressures and rounds of U.S. sanctions against Russia. Internationally, the dollar has been fueled by the Fed’s rate hikes, oil price increases, and Trump’s trade wars.

While some of these conditions also apply to Asia’s rapidly-growing emerging economies – including India, Indonesia, and Philippines – their strong fundamentals would not seem to warrant so severe penalties. Indeed, as Modi’s India, Widodo’s Indonesia and Duterte’s Philippines are well-positioned for the future, why are their exchange markets chastised?

In each case, there are some internal pressures (e.g., rising inflation, current account deficit, delayed infrastructure projects, etc), but these explain only part of the story. Intriguingly, in the late summer, emerging markets’ currency sell-off was focussed against the U.S.bilaterally. Among each other, these currencies canceled out most of the adjustment in terms of trade-weighted real effective exchange rate (REER), which generated more moderate outcomes.

In brief, a large advanced economy, in which fundamentals are deteriorating, is causing collateral damage in the world’s most rapidly-growing economies, which have lower relative debt, budget deficit and current account than the U.S.

U.S. Dollar – Minus American Century

When the Bretton Woods system was established in 1944, Europe and Japan were devastated. After two decades of recovery and reconstruction, Western Europe and Japan were not only back on their feet but competing with the United States. For two decades, U.S. dollar had enjoyed an “exorbitant privilege”, as the then French finance minister, Valéry Giscard d’Estaing, put it. The term refers to the benefit – economic rent, really – that the United States enjoys, thanks to U.S. dollar being the international reserve currency. Despite having far more liabilities than assets, the U.S. doesn’t have to face a balance of payments crisis.

In the mid-1960s, President Charles de Gaulle, who shared his finance minister’s views, said he would exchange French U.S. dollar reserves for gold at the official exchange rate. Paris had no intention to subsidise U.S. living standards and U.S. multinationals in perpetuity. As other countries followed the suite, U.S. gold stock decreased, and so did America’s economic influence.

By 1971, President Nixon ended unilaterally the convertibility of the dollar to gold. That resulted in a price shock that reverberated across the world. It was initially portrayed as a temporary measure, yet it made U.S. dollar a permanently floating fiat money. As gold no longer offered a yardstick for value, the perception of value replaced value itself. In geopolitics, the U.S. continued to lean on major Western economies and Japan, but in international economy it refused to renounce the exorbitant privilege.

After the 2008–2009 global crisis, U.S. Dollar Index (DXY), which measures the currency against a basket of half a dozen major currencies, lingered at barely 80 until the rate hikes began. Indeed, since the late 1960s and the eclipse of the gold standard in the early ‘70s, three periods of dollar surges have been followed by periods of decline that have caused much international collateral damage (see sidebar, U.S Dollar Index: Structural Trend, 1970 – 1980*).

* Trend line in black color.

* Trend line in black color.

In the ‘70s, the eclipse of the Bretton Woods agreement, the Nixon price shock and the twin oil crises resulted in high inflation, which Fed chief Volcker subdued with 20% rate hikes causing the U.S. dollar to soar to 160 that paved way to huge twin deficits and a lost decade in Latin America. The second surge ensued at the turn of the 2000s, when the dotcom bubble pushed the Index to 120. This time collateral damage included Asia’s financial crisis and Russia’s debt default followed by the rise of anti-globalisation movements and Jihad terrorism. Today, after the burst of the housing bubble and the severe global recession, we are still amid the third surge, but late in the cycle. With the Trump election triumph, the Index surged again to 105, fueled by the rising government bond yields, the Fed’s anticipated hikes and expected acceleration in privatisation, liberalisation and deregulation. But as the Trump administration began the reversal of U.S. postwar globalisation, tariff wars against the world’s largest trading economies, the nullification of nuclear deals with Iran and Russia, the Index began to fluctuate amid new pressures of decline.

Despite the continued strength of the U.S. dollar, each of these surges reflects the progressive relative erosion of the dollar (the black trend line in the US Dollar Index). What we call a strengthening dollar today is barely 60% of the 1960s greenback.

American Century may be gone, yet U.S. dollar prevails – but not without alternatives.

Expanding Euro, Eroding Dollar

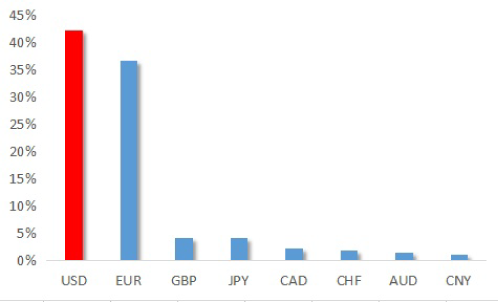

According to data by the broad-based SWIFT (Society for Worldwide Interbank Financial Telecommunication), the share of the U.S. dollar as an international payments currency continues to account for more than two-fifths of the total (42%). In historical view, the share of U.S. dollar in the world economy has suffered a massive shrinkage. However, today, the world economy is not controlled by the U.S. dollar monopoly, but a dollar/euro duopoly. The share of euro (37%) is almost at par with the dollar in international payments.

Other major currencies feature the Japanese yen and British pound (4% each). The historical precursor of the U.S. dollar, the pound dominated the world economy through the 19th century until its position was undermined by the British overstretch in two world wars. The postwar yen’s glory peaked in the 1980s until Tokyo agreed to the terms of Washington’s Plaza Accord in 1986, which paved the way for the Japanese asset bubble and its burst in the early 1990s, and the subsequent three lost decades. The pound and the yen are followed by Canadian dollar, Swiss franc, Australian dollar and Chinese yuan (see Figure 1).

Figure 1. Shares of International Payments Currencies (%)

* International Payment Currencies: Share as an international payments currency Customer initiated and institutional payments. Excluding payments within Eurozone. Messages exchanged on SWIFT. Based on value.

* International Payment Currencies: Share as an international payments currency Customer initiated and institutional payments. Excluding payments within Eurozone. Messages exchanged on SWIFT. Based on value.

Source: SWIFT, Sept 2018

Since there is a correlation between rate hikes and the strength of the U.S. dollar, the expectation was that as the Fed begins tightening, the dollar would strengthen. Yet, between mid-2015 and today, the share of U.S. dollar as an international payment currency has moderately fallen, along with Chinese yuan, whereas British pound has plunged by 5 percentage points. While Japanese yen has expanded more than a percentage point, euro has soared by a whopping 8 percentage points (see Figure 2).

Figure 2. Changing Shares of International Payments Currencies,

2015 – 2018

* International Payment Currencies: Share as an international payments currency Customer initiated and institutional payments. Excluding payments within Eurozone. Messages exchanged on SWIFT. Based on value.

* International Payment Currencies: Share as an international payments currency Customer initiated and institutional payments. Excluding payments within Eurozone. Messages exchanged on SWIFT. Based on value.

Source: SWIFT, Sept 2015 – Sept 2018

In the past half a decade, currencies of countries that support global cooperation through trade and investment have been strengthening (euro, yen). In contrast, the currencies of those countries that have turned inward have been stagnating in relative terms (U.S. dollar) or under-performing (pound).

Today, America’s sovereign debt is almost $22 trillion, and there is no credible, bipartisan, medium-term debt-cutting plan. Moreover, America’s role in the global economy has shrunk to about a fourth of the total and it has suffered from trade deficits since the early ‘70s. This dramatic decline has not been registered by vital international indicators, such as the Special Drawing Right (SDR) basket by the International Monetary Fund (IMF). The share of the U.S. dollar in the IMF basket remains 42% of the world economy, as it was in 1981, even though the Dollar Index has plunged by 40% and the relative share of the U.S. in the global economy has halved. Meanwhile, China’s GDP (PPP) already exceeded those of the U.S. and the EU in 2016.

Furthermore, while SWIFT data indicates that Chinese yuan is stagnating, it may no longer reflect rapidly-changing realities.

Eclipse of Petrodollar, Rise of Petroyuan

After the 1945 Yalta Conference, which effectively divided Europe, the ailing President, Franklin D. Roosevelt, met Saudi Arabia’s King Ibn Saud. Bypassing the Brits, FDR and Saud agreed to a secret deal, which required Washington to provide Saudi Arabia military security in exchange for secure access to supplies of oil. Despite periodic pressures, the pact survived until the 1971 “Nixon Shock” and U.S. dollar was decoupled from gold.

To deter the marginalisation of U.S. dollar, Nixon negotiated another deal, which ensured that Saudi Arabia would denominate all future oil sales in dollars, in exchange for U.S. arms and protection. Led by Riyadh, other OPEC countries agreed to similar deals and global demand for U.S. petrodollars soared. Thereafter, the US-Saudi strategic partnership weathered another four decades of multiple regional wars. To seal the old alliance, President Trump signed a historical $110 billion arms deal with King Salman in 2017.

Nevertheless, the structural conditions that supported the alliance between Washington and Riyadh are softening, as evidenced by increasing bilateral PR nightmares from the 9/11 terrorist attack to the Khashoggi affair. By the same token, if those structural conditions melt, U.S. dollar will soften accordingly. Petrodollar is no longer the only alternative in the town.

In the past few years, the internationalisation of the Chinese yuan has accelerated significantly. In addition to its inclusion in the IMF international reserve assets basket, China has established a payment-versus-payment system for transactions involving Chinese yuan and Russian ruble. The China Foreign Exchange Trade System (CFETS) hopes to launch similar systems with other currencies based on China’s huge multi-decade, multi-trillion One Belt One Road (OBOR) initiatives. As the OBOR expands links between major economies in Asia, Africa, Europe and Latin America, member countries are candidates for RMB-denominated payments. However, the diffusion venues of Chinese renminbi differ significantly from those of U.S. dollar since the postwar era.

Recently, China has also become the largest global oil consumer. Last year, its oil imports exceeded those of the United States (see Figure 3). With major oil exporters like Russia, Venezuela, Iraq, Iran, and Saudi Arabia, China’s market means leverage, and many of these suppliers have either already agreed to price their sales to China in RMB, or are actively considering it. In turn, major commodity exporters, such as Indonesia, have joined in non-dollar trades.

Figure 3. U.S. & China Crude Oil Imports, 1980 – 2017

Source: BP Statistical Review of World Energy 2017 (1,000 Barrels Per Day)

Source: BP Statistical Review of World Energy 2017 (1,000 Barrels Per Day)

As an increasing share of China’s oil imports will be priced in renminbi, that will result in large yuan reserves in oil exporting countries, which will be spent on Chinese exports, or recycled into China’s financial markets. And as demand for yuan assets will increase, the role of U.S. dollar for trading purposes will lessen. In secular terms, the petroyuan will mean a paradigm shift in global asset allocations to China’s financial markets, as long as China will continue to remove or significantly reduce capital controls for yuan-priced oil trading. Between 2014 and 2017, global institutional investors already tripled their China holdings of onshore bonds.

In the 1944 Bretton Woods, the dramatic rise of the U.S. dollar was a top-down, multilateral event. In contrast, Chinese yuan is a bottom-up process that mainly relies on transacting parties’ arrangements, which may be bilateral, multilateral, or transnational. That’s why the SWIFT data about international currency payments may today be less valid than only a decade ago. It lacks data on non-SWIFT venues.

After the Cold War, Washington has also increasingly used SWIFT mechanisms to penalise countries that it perceives as “threats,” such as the U.S. unilateral withdrawal from the multilateral Iran nuclear deal (JCPOA). The backlash includes Russian Central Bank’s alternative to U.S.-dominated SWIFT (System for Transfer of Financial Messages), which Moscow started after the 2014 post-Crimea sanctions following threats that it could be cut off from SWIFT. The latter is based in Belgium, but is effectively controlled by the U.S. Treasury.

More recently, Russia and China have reduced reliance on the dollar by increasing the amount of bilateral trade conducted in rubles and yuan. Similarly, the U.S. withdrawal from the Iran deal prompted Germany’s foreign minster to call for the EU to free itself from dependence on the U.S. and adopt its own international payments channel. Brussels has developed a parallel system to SWIFT that will allow Iran to interface with EU-centered financial, clearing and banking systems. After months of pressure by Washington’s EU allies, the Trump administration signaled acceptance of Iran remaining in SWIFT. That, however, prompted neoconservative lawmakers and hawks to pressure Trump and to complain that Iran sanctions are “too soft.”

U.S. Dollar as a “Fear Index”

Ironically, strengthening secular forces are driving rising U.S. dollar risks. In 2016, the Bank for International Settlements (BIS) released an intriguing report, which argued that U.S. dollar has replaced the volatility index as the “new fear index”. The mantle of the barometer of risk appetite and leverage used to belong to the VIX (i.e., Chicago Board Options Exchange volatility index). Before the 2008–2009 financial crisis, there was a close correlation between leverage and the index. When the VIX was low, the appetite for borrowing went up, and vice versa. As a result, the VIX soared to its record 80.9 at the eve of the global financial crisis. With the EU sovereign debt crisis and the US debt limit crisis up, it still peaked at 47. While there have been minor crises thereafter, most have remained significantly lower.

After a decade of ultra-low interest rates and negative levels, and multiple rounds of quantitative easing that remain in effect in Europe and Japan, one would expect the VIX to be elevated. And yet, it is currently less than 20. Monetary easing by the world’s leading central banks in advanced economies has suppressed volatility for stocks, while compressing credit spreads. In the process, the VIX’s predictive power has diminished, while U.S. dollar has become the indicator of risk appetite and leverage. This dynamic has distressing implications as it has pushed international borrowers and investors toward the dollar, with dollar appreciation exposing borrowers and lenders to valuation changes. In this view, recent dollar rallies may not precipitate market confidence, but new risks. Market skeptics have highlighted dollar illiquidity issues for years. If they are right, then the Fed rate hikes will boost the price of the U.S. dollar as a kind of a global Fed funds rate, with the rising dollar tightening economic conditions worldwide.

According to October data, the Trump White House’s offensive international policies have led several countries – not just China but Japan – to reduce their Treasury holdings, even dump their Treasuries (as Russia did last spring when it divested some 90% of its holdings), while many countries have sought to expand their gold holdings, perhaps preparing for a return for a gold standard of some sort. As a result, the reserve status of the U.S. dollar has plunged to a half-a-decade low.

In the past, the Fed’s rate hikes and the collateral international damage was legitimised by the argument that the emerging markets adjustment reflects the strength of U.S. economy and U.S. dollar as safe haven. It was not a bad explanation in the postwar era. But the secular trend erosion of the U.S. dollar is unsustainable and morphing into a global risk. The U.S. debt burden is already at the level where that of Italy was prior to the EU debt crisis. The difference is that Italian lira does not dominate two-fifth of SWIFT data and international currency reserves.

Three Future Scenarios

In the 21st century, the world economy needs a multipolar mix of major reserve currencies by both major advanced and large emerging economies. This change is looming in the horizon, but the question of how and when it will materialise can be illustrated by three generic scenarios.

• Phased Transition. The change may occur through the Phased Transition scenario over time, which would be least costly and most cooperative. In economic view, it would be the preferable trajectory. However, it would require international consensus that is largely missing.

• Disruptive Crisis. Conversely, it may materialise through the Disruptive Crisis scenario, which shuns international consensus, but which would prove most costly and highly frictional. In this case, Washington would increasingly resort to its military superiority and exploit geopolitics to force preferred economic ends.

• Bumbling Through. Or it may happen through a Bumbling Through scenario, which would combine both offensive and accommodative trial-and-error efforts with the best and worst of the first two scenarios. At times, it would seem ideal; at other times, adverse; at all times, inherently erratic and uncertain.

Until recently, Bumbling Through seemed to be the primary trajectory, but as secular stagnation has spread in the U.S., Europe and Japan causing increasing growth deceleration in the large emerging economies, Washington’s new insular policies suggest that Disruptive Crisis could morph into the primary trajectory.

Last spring, Standard & Poor’s published a report on currency manipulation that gave China the lowest manipulation score in Asia-Pacific. In October U.S. Treasury released its bi-annual currency report, which did not label China for manipulation but did include it in its “Watch list”. Reportedly, President Trump publicly and privately had tried to pressure the Treasury to declare China a currency manipulator. While the staff finding averted a severe escalation of the US-China trade war, the latter was precisely what the Trump White House sought. The latter seeks to deter any major currency that could threaten U.S. dollar’s exorbitant privilege – by any means necessary.

In the long term, a gradual, phased transition toward greater diversification in international payments and reserve currencies is vital to the U.S. dollar, which will otherwise be unable to avoid a severe structural correction.

Moreover, persistent efforts to foster dollar supremacy risk not only recovery in advanced economies, but the future of many emerging and developing countries. Since the 2000s, China and Chinese yuan have been central to poor- and middle-income countries whose growth has become strongly associated with China’s growth. Thus, any effort to push China into the kind of precipitous, deflationary currency appreciation as Japan in the early 1990s would drastically undermine the future of emerging and developing countries. And since the latter fuel global growth prospects, such efforts would also derail global growth for years to come.

The presumed strength of the U.S. dollar no longer relies on America’s economic fundamentals, but on a perception that such fundamentals will prevail, despite drastic shifts in the world economy. That’s the contemporary version about the old fairy tale of the Emperor’s new clothes.

U.S. dollar is no longer a sustained safe haven, just a temporary safe house. That’s why the day of reckoning is no longer a matter of principle, just a matter of time.

About the Author

Dr Dan Steinbock is an internationally recognised expert of the multipolar world focussing on international business, international relations, investment and risk among the major advanced economies and large emerging economies. In addition to his global consultancy, Difference Group Ltd, he has served in India China and America Institute (U.S.), Shanghai Institutes for International Studies (China) and the EU Center (Singapore) while cooperating with leading universities and think-tanks in the U.S. and all world regions.

Dr Dan Steinbock is an internationally recognised expert of the multipolar world focussing on international business, international relations, investment and risk among the major advanced economies and large emerging economies. In addition to his global consultancy, Difference Group Ltd, he has served in India China and America Institute (U.S.), Shanghai Institutes for International Studies (China) and the EU Center (Singapore) while cooperating with leading universities and think-tanks in the U.S. and all world regions.

{kind=link}