The traditional approach to asset-liability management (ALM) practice in banks operated as a reactive process following product origination by the customer-facing business. In the Basel III era a more proactive approach to ALM is required, in order to manage the balance sheet from an effective viability and sustainability standpoint. The article describes proactive “Strategic ALM” discipline and its implementation process.

Banks are by their nature risk taking institutions. This is a requirement of their business, because their corporate clients may wish to tailor their funding to meet the precise needs of their business, so as to achieve some certainty in this area, enabling them to focus on what they do best. Similarly, retail clients may wish to access banking products and services to meet their personal needs, such as purchasing a house or investing for a child’s education. To meet this demand, banks offer the lending terms, maturities, rate options, currency, optionality, and contingencies demanded by their clients, and take on the range of risks that such tailoring represents. Because banks have a wide range of clients with varying borrowing and deposit requirements, exposures may to some degree offset each other, but will not match completely in terms of timing, amount and currency. This is more evident as products become more complex and offer more alternatives.

Therefore a key area of focus for banks is managing their capital, funding, liquidity and interest-rate risk requirements. These all fall under the umbrella of the asset-liability management (ALM) discipline in a bank. When a bank borrows more than it needs, there can be inefficiencies in terms of capital use. This can also result in added interest rate risk, and a loss when lending on. However, failure to have sufficient funding results in the bank having to rely on central bank liquidity, poor market perception and loss of investors, which could ultimately lead to failure. Thus, ALM becomes the most important aspect of a bank’s risk management framework.

In this article we suggest that the discipline of ALM, as practised by banks worldwide for over 40 years, needs to be updated to meet the challenges presented by globalisation and Basel III regulatory requirements. In order to maintain viability and a sustainable balance sheet, banks need to move from the traditional “reactive” ALM approach to a more proactive, integrated balance sheet management framework. This will enable them to solve the multi-dimensional optimisation problem they are faced with at present.

The Origins of Asset-Liability Management (ALM)

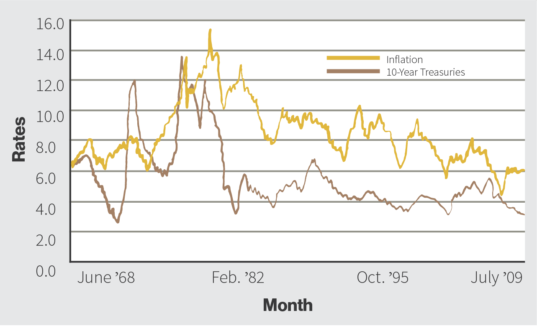

Historically, interest rates were stable and liquidity was readily available to banks in developed nations. Banks focussed primarily on generating assets to increase growth and profitability. However, in the 1970s changes in regulation, inflation, and geopolitics led to greater volatility and thus increased risk from asset and liability mismatches (see Figure 1). This led to the development of Asset-Liability Management (ALM) as a formal discipline, where both sides of the balance sheet are integrated to manage interest rate, market, and liquidity risk. In essence however, this discipline remained reactive in nature, with Treasury and Risk having little or no input to the origination and deposit raising process.

Figure 1: US Treasury yields and US inflation historical levels

Figure 1: US Treasury yields and US inflation historical levels

Source: St. Louis Fed.

Traditionally, ALM was defined by four key concepts:

• Liquidity, defined as

◦ Funding liquidity: the continuous ability to maintain funding for all assets

◦ Trading liquidity: the ease with which assets can be converted into cash

• Term structure of interest rates: the shape of the yield curve at any given time depends on interest rate expectations, liquidity preference, and supply and demand from different borrowers and lenders. ALM strategy would consider how changes to the shape of the yield curve in the short and medium term will impact the bank.

• The maturity profile of the banking book

• ALM would report and monitor the maturities of all asset and liabilities to measure and control risk

• Interest rate risk, essentially the risk of loss of net interest income due to adverse movements in interest rates or interest rate spreads.

In essence however, “ALM” as undertaken in all banks has always been a reactive process, and despite its name has rarely, if ever, managed to integrate origination policy across both sides of the balance sheet. As a discipline, such an approach is no longer fit-for-purpose in the era of Basel III.

The Strategic ALM Concept

Consider exactly how ALM is undertaken in virtually every bank today, irrespective of size, business model or location. A business line in a bank, following an understood medium-term “strategy” articulated either explicitly or implicitly (but in reality aiming usually simply to meet that year-end’s budget target), goes out and originates customer business, be this originating assets or raising liabilities. It will most likely have little interaction with any other business line, and only the formal review interaction with the Risk department. This is often described as creating a “silo mentality” in the organisation, and is typical of all but the very smallest banks. In some banks an individual business line may have practically zero interaction with Treasury. In this respect it will be similar to all other business lines.

Each of these business lines will proceed to undertake business, ostensibly as part of a grand strategy intertwined with other business lines, but in reality to a certain extent in isolation. The actions of all the customer-facing desks in the banks will then give rise to a balance sheet that must be “risk managed”. And the ALM part of this risk management process is then undertaken by Treasury, in conjunction with Finance and Risk.

There is little, or no, interaction between business lines and little, or no, influence of the Treasury function or the risk “triumvirate” of Treasury, Finance and Risk in the balance sheet origination process. In other words, ALM is a reactive, after-the-fact process. The balance sheet shape and structure is arrived at, if not by accident certainly not by active design and certainly not as the result of a process that integrates assets and liabilities origination. The people charged with stewarding the balance sheet through the economic cycle and market crashes have very little to do with creating the balance sheet in the first place. Does this represent best-practice risk management discipline, with separation of duties, four lines of defence, and so on? In a word, no. There is no problem with one department originating assets and another one managing the risk on them. The issue with the traditional approach to ALM is that the balance sheet that is arrived at often lacks a coherent shape, or logic, and this makes the risk management of it more problematic.

One would not wish to have a balance sheet that was composed overwhelmingly of illiquid long dated assets funded by wholesale overnight deposits, or a liabilities strategy that concentrated on raising wholesale or corporate funding that was treated punitively by Basel III liquidity requirements. Another example observed by the author involved the funding of trade finance assets (overwhelmingly very short term) by 10-year MTNs.1

In the era of Basel III, it is evident that balance sheet risk management must become more proactive. The shape and structure of the balance sheet must be arrived at because of an integrated approach to origination. What does this mean? Quite simply, the discipline of ALM must recognise that asset origination and liability raising has to be connected. For the ALM process to be fit-for-purpose for the 21st century, banks must transition and adapt from a traditional reactive ALM process to a proactive strategic ALM process.

Addressing the three-dimensional (3D) balance sheet optimisation problem

The market environment is creating a 3D optimisation challenge for banks, or at least those banks that are serious about competing and serious about being well-respected by customers and peers. This challenge requires banks to run optimised balance sheets in order to maximise effectiveness and stakeholder value; however when we speak of “balance sheet optimisation” we do not mean what it used to mean in the pre-crash era, basically working to maximise return on capital (RoC). Today optimising the balance sheet has to mean structuring the balance sheet to meet the competing but equivalent needs of Regulators, Customers and Shareholders. This is the 3D optimisation challenge that we speak of.

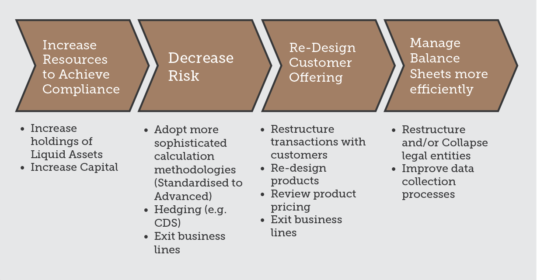

A bank’s risk management practice is an integral part of meeting this optimisation challenge. From the Board level downwards, policy must be geared towards achieving this goal, and strategic ALM is a vital part of the optimising process. However before we consider this let us refresh the regulatory aspects first. We will not cover the myriad requirements of Basel III capital, liquidity and leverage requirements here, which are discussed in depth in other publications. The essence of implementing the demands of Basel III as stipulated by regulators is that many bank’s business models will have to change, to ensure compliance. Figure 2 illustrates this in stylised fashion.

1. These illustrations are made to emphasise a point, but they are a few of the very many examples observed by the author at different banks over the years.

Figure 2: Mitigating the Impacts of Basel III

Figure 2: Mitigating the Impacts of Basel III

© Christopher Westcott 2014, 2017. Reproduced with permission

The inescapable conclusion since the bank crash of 2008 is that banks must manage their balance sheet more efficiently. This gives rise to the 3D optimisation problem. We articulate it thus:

1. Regulator requirements: banks must adhere to the capital, liquidity and leverage ratio requirements of their regulator. With only a handful of exceptions, this means meeting the demands of the Basel III guidelines. The larger the bank, and/or the more complex its business model, the more complicated and onerous this requirement becomes. Related stipulations such as the Fundamental Review of the Trading Book (FRTB) add to the regulatory demands imposed on banks. Every bank must meet its supervisory requirements;

2. Customer franchise requirements: this is not necessarily anything new. In a competitive world, any bank would always wish to meet the demands of its customers. In a more constrained environment this requirement becomes more urgent of course, and this gives rise to the challenge. For instance, a “full service” bank will wish to provide all the products that its customers may demand, and sometimes these products will not be the most optimum from the viewpoint of (1) above. To illustrate one case: the deposits of large corporate customers and non-bank financial customers are considered “non-sticky” under Basel III rules and so carry a greater liquidity cost for banks. From that perspective such deposits are not optimum from a regulatory efficiency view, but the bank must accept them if it wishes to satisfy this part of its customer base;

3. Shareholder requirements: this aspect is of course also not new. The shareholder has always demanded a satisfactory rate of return, and so all else being equal a bank will always want to maximise its net interest income (NII) and enhance or at least preserve its net interest margin (NIM) through changing economic conditions and interest rate environments. But of course the balance sheet mix that meets this objective will not necessarily be the one that is most efficient for (1) and/or (2) above. One example: from a NII perspective a bank will maximise its funding base in non-interest bearing liabilities (NIBLs) such as current accounts (“checking” accounts) or instant access deposit accounts, whereas the demands of Basel III liquidity will often call for an amount of contractual long-term funding, which is more expensive and thus inimical to NII.

We see therefore that the demands of each stakeholder are, in a number of instances, contradictory. To maximise efficiency a bank will need to work towards a balance sheet shape and structure that is optimised towards each stakeholder, and it is not a linear problem. Hence, the 3D optimisation challenge arises.

This illustrates unarguably the need for a new approach to balance sheet origination and the role of the ALM function. This we term “strategic ALM”.

Principles of strategic ALM practice

Strategic ALM is a single, integrated approach that ties in asset origination with liabilities raising. It works to break down “silos” in the organisation, so that asset type is relevant and appropriate to funding type and source, and vice versa. We define it as follows:

A business strategy approach at the bank-wide level driven by balance sheet ALM considerations

Strategic ALM addresses the three-dimensional optimisation problem of meeting with maximum efficiency the needs of:

• the regulatory requirements

• the NII requirements

• the customer franchise requirements

and must be a high-level, strategic discipline driven from the top down. It is by nature proactive and not reactive.

Implementing a strategic ALM process will make it more likely that the bank’s asset type(s) is relevant and appropriate to its funding type and source, and that its funding type and source is appropriate to its asset type. By definition then it would also mean that a bank produces an explicit, articulated liabilities strategy that looks to optimise the funding mix and align it to asset origination. Thus, strategic ALM is a high-level, strategic discipline driven from the top down.

Proactive balance sheet management (BSM) is just that, and not the “reactive” balance sheet management philosophy of traditional banking practice. Proactive BSM means the asset-side product line is managed by a business head who is closely aligned (in strategic terms) with the liabilities-side product line head. To be effective the process needs to look in granular detail at the product types and how they are funded/deployed; only then can the bank start to think in terms of optimising the balance sheet.

Implementing strategic ALM practice is not a trivial exercise, and can only be undertaken from the top down, with Board approved instruction (or at least approval). Hence we consider an essential prerequisite, which is the Board articulated risk appetite statement, followed by a look at the importance of ALCO.

Implementing Strategic ALM

The approach to implementing an effective strategic ALM practice has several strands. We describe each in turn.

Recommended Risk Appetite Statement

The Risk Appetite Statement is an articulated, explicit statement of Board appetite for and tolerance balance sheet risk, incorporating qualitative and quantitative metrics and limits. It becomes the most important document for Board approval. This may appear to be a contentious statement but it is self-evident when one remembers that the balance sheet is everything. The over-riding objective of every bank executive is to ensure the long-term sustainability and viability of the bank, and unless the balance sheet shape and structure enables this viability, achieving this objective is at risk.

Figure 3 shows a template summary risk appetite statement drafted by the author when he was Treasurer at a medium-sized commercial bank. This statement received Board approval. It is applicable to virtually all banking entities irrespective of their business model, although large multinational banking institutions will need to develop the list of risk metrics much further. It provides a formal guide on the desired Board risk appetite framework, including a description of each of the risk appetite pillars and the key measures that will be used to confirm on a monthly basis that the bank is within risk appetite.

Figure 3: Example Board risk appetite statement

Figure 3: Example Board risk appetite statement

© Moorad Choudhry 2011, 2017

As we see from Figure 3, for each of the measures identified an overall bank-wide “macro-tolerance” is set, which is then broken down into tolerances for individual business lines (e.g. Retail, Corporate). The range of quantitative limits is user-defined; for example, in the section on liquidity limits:

• a vanilla institution with no cross-border business may content itself with setting limits for the primary liquidity metrics such as loan-deposit ratio and liquidity ratios, as well the regulatory metrics such as LCR and NSFR;

• a bank transacting across currencies will wish to also incorporate FX exposure tolerance;

• a bank employing a significant amount of secured funding will wish to add asset encumbrance limits.

The Board risk appetite statement is the single most important policy document in any bank and should be treated accordingly. It requires regular review and approval, generally on an annual basis, or whenever changes have been made to the business model and/or customer franchise. It also should be updated in anticipation or in the event of market stress.

Armed with the Board risk appetite statement, which must be a genuine “working” document and not a list of platitudes, with specific quantitative limits, the implementation of a strategic ALM process becomes feasible. As well as the Board risk statement, the other ingredient that is required to make strategic ALM a reality is an asset-liability committee (ALCO) with real teeth. One cannot emphasise enough the paramount importance of a bank’s ALCO.

Elements of Strategic ALM: paramountcy of ALCO

Consider the executive committees, below Board level, that are responsible for the strategic direction as well as the ongoing viability and sustainability of the bank. Which of them has responsibility for oversight of balance sheet risk? Perhaps it is one or more of the following:

• Executive committee (or “management committee”): this is the primary committee responsible for running the bank, chaired by the CEO;

• Risk management committee: chaired by the CRO, responsible for “managing” all the risk exposures the bank may face, from market and credit risk to technology risk, conduct risk, regulatory risk, employee fraud risk, etc.;

• Credit risk committee: chaired by the head of credit or the credit risk officer, this committee is responsible for managing credit policy including credit risk appetite, limit setting and credit approvals. As credit risk is the single biggest driver of regulatory capital requirement in banks (in some vanilla institutions representing 75%-80% of total requirement) it can be seen that the credit risk committee is also a balance sheet risk committee;

• ALCO: the asset-liability committee, a template Terms of Reference for which were described in the author’s text The Principles of Banking.

While all of these committees have an element of responsibility for the bank’s balance sheet, it is the ALCO that is responsible for this and nothing else. It alone has the bandwidth to discharge this responsibility effectively and to help ensure that the balance sheet shape and structure is long-term viable. The executive committee that is most closely concerned with balance sheet risk on a strategic and integrated basis (both sides of the balance sheet and all aspects of risk) is ALCO. Given this, what is the most effective way to ensure above-satisfactory and effective governance from Board perspective? We suggest that it is to ensure the paramountcy of ALCO, as illustrated in the organisation chart given at Figure 4.

Figure 4: Recommended bank executive committee organisation structure

Figure 4: Recommended bank executive committee organisation structure

© Moorad Choudhry 2011, 2017

The key highlight of the structure shown at Figure 4 is that ALCO ranks pari passu with the ExCo and that it also has an oversight role over the Credit Committee. The former ensures that balance sheet strength and robustness is always given equal priority with shareholder return, and the latter ensures that ALCO really does exercise control over the assets and liabilities on the balance sheet, as suggested in its name. For instance, it would be ALCO, and not ExCo or the Risk Committee, that would design, drive and monitor the bank’s early warning indicator (EWI) metrics, as it would be the committee with the required expertise and understanding of the balance sheet.

With this structure in place, implementing strategic ALM practice can become a reality.

Elements of Strategic ALM: integrated balance sheet origination

At its heart the objective of the strategic ALM process is to remove the “silo mentality” in place at banks in order to ensure a more strategically coherent origination process. This will help the bank to arrive at a balance sheet shape and structure more by design than by well-intentioned accident.

In the first instance, a bank’s liquidity and funding policy should not be concerned solely with its liabilities. The type of assets being funded is as important a consideration as the type of liabilities in place to fund those assets. For a bank’s funding structure to be assessed on an aggregate balance sheet approach, it must measure the quality and adequacy of the funding structure (liabilities) alongside the capital and asset side of the balance sheet. This gives a more holistic picture of the robustness and resilience of the funding model, in normal conditions and under stress. The robustness of funding is as much a function of the liquidity, maturity and product type of the asset base as it is of the type and composition of the liabilities.

Typical considerations would include:

• Share of liquid assets versus illiquid assets

• How much illiquid assets are funded by unstable and/or short-term liabilities

• Breakdown of liabilities:

◦ Retail deposits: stable and less stable

◦ Wholesale funding: secured, senior unsecured

◦ Capital: subordinated / hybrid; equity

As part of an active liabilities strategy, on the liability side ALCO should consider:

• Debt buy-backs, especially of expensive instruments issued under more stressful conditions at higher coupon;

• Developing a wide investor base

• Private placement programme

• Fit-for-purpose allocation of liquidity costs to business lines (FTP)

• Design and use of adequate stress testing policy and scenarios

• Adequate risk management of intraday liquidity risk

• Strong public disclosure to promote market discipline

On the asset side, strategic action could include:

• Increasing liquid assets as share of the balance sheet (although liquidity and ROE concerns must be balanced)

• De-linking the bank – sovereign risk exposure connection

◦ The LCR HQLA does not have to be exclusively sovereign debt, but claiming a “shortage” of eligible assets is disingenuous: the HQLA can be exclusively cash

• Avoiding lower loan origination standards as the cycle moves into bull market phase

• Addressing asset quality problems.

◦ Ring-fence NPLs and impaired loans? (A sort of “non-core” part of the balance sheet that indicates you are addressing the problem and looking at disposal)

• Review the bank’s operating model. Retail-wholesale mix? Franchise viability? Comparative advantage?

• Limit asset encumbrance: this contradicts pressure for secured funding

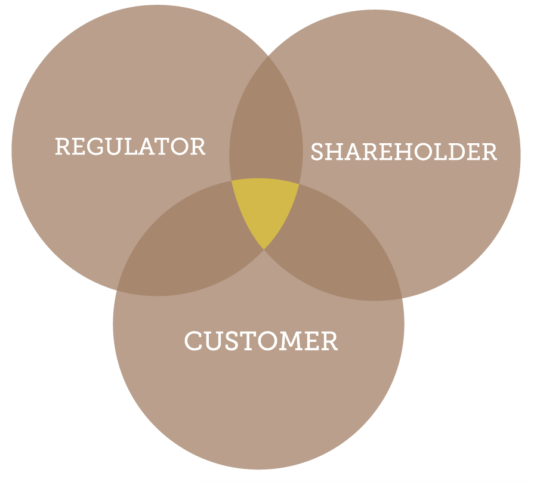

In essence, as far as possible a bank’s balance sheet should aim to maximise those assets and liabilities that hit the yellow-shaded “sweet spot” shown in the Venn diagram at Figure 5, where the requirements of all three stakeholders are served. Of course, a “full service” commercial bank will still need to offer loan and deposit products that meet customer needs but may be less optimum from a regulator or shareholder requirement perspective. This is the nature of banking and must be accepted. Nevertheless for efficiency and optimisation reasons,the process of strategic ALM is still needed so as to ensure maximisation of the origination of assets and liabilities that cover off all three stakeholder needs, and minimisation of the origination of product types that meet the needs of just one or two stakeholders.

Figure 5: Product mix optimisation

Figure 5: Product mix optimisation

© Moorad Choudhry 2011, 2017

We emphasise strongly one of the bullet points above, namely

Strong public disclosure to promote market discipline.

A bank that discusses the structure and strength of its balance sheet is assisting the industry as a whole, as regulators point to it (off the record, it is unlikely that a bank supervisor would make this point formally) as a benchmark and as its peers look to it when comparisons are made by analysts.

We present at Figure 6 a summary high-level asset-liability policy guide, to be followed as part of the strategic ALM process.

Figure 6: Summary of asset-liability policy guide

Figure 6: Summary of asset-liability policy guide

© Moorad Choudhry 2011, 2017

Conclusions

Bank assets and liabilities are inextricably linked. Banks cannot manage risk and return without considering both sides of the balance sheet at the same time and continuously throughout the business origination process. All areas of the bank must come together to understand interest rate and liquidity risks in setting and pursuing high level strategy.

Traditionally “ALM” meant managing liquidity risk and interest-rate risk. But this isn’t full “ALM” if what one wishes to manage is all the assets and all the liabilities from one integrated, coherent aggregate viewpoint. The balance sheet is everything – the most important risk exposure in the bank. Managing ALM risk on the balance sheet therefore is managing everything that generates balance sheet risk. Proactive ALM or what we call “Strategic ALM” is self-evidently best-practice in the Basel III environment, where one can’t expect to originate assets and raise liabilities in isolation from each other and still “optimise” the balance sheet.

We have addressed a number of factors with respect to implementing strategic ALM, from a high-level standpoint. The correct approach to ALM discipline demands a keen appreciation and understanding of other related factors, including:

• product type and behaviour;

• behavioural tenor characteristics of assets and liabilities (something required to some depth now anyway with implementation of Basel III);

• relevant reference interest rate benchmarks;

• the Libor-OIS spread, the Libor term premium and determinants of the swap spread;

as well as other related aspects such as peer benchmarking and understanding net interest margin (NIM) behaviour. ALM is an all-encompassing discipline and one that should be understood by all senior bankers, particularly the executive committee.

In the Basel III era, in order to meet the 3D optimisation challenge faced by banks one must seek to achieve maximum balance sheet efficiency, and that calls for the risk “triumvirate” of Treasurer, CFO and CRO, operating through ALCO, to have a bigger influence in origination and customer pricing. This is now the future of risk management practice in banks. Without this approach, it will be difficult to optimise the asset-liability mix that addresses the “3D” problem of regulatory compliance, NIM enhancement and customer franchise satisfaction.

About the Author

Professor Moorad Choudhry lectures on the MSc Finance programme at University of Kent Business School. He was previously Treasurer, Corporate Banking Division at The Royal Bank of Scotland, and is author of The Principles of Banking.

Professor Moorad Choudhry lectures on the MSc Finance programme at University of Kent Business School. He was previously Treasurer, Corporate Banking Division at The Royal Bank of Scotland, and is author of The Principles of Banking.

{kind=link}