What is it that shapes power obsessions for bringing down constitutional democracies? Some current power-hungry leaders game political systems for personal benefits; others fancy the corruption game as a battle of wits to grip the power they need. Still others are wily wannabes, envying those who hold the powers achieved.

“Americans are entering the most dangerous world they have known since World War II, one that will make the Cold War look like child’s play and the post–Cold War world like paradise. In fact, this new world will look a lot like the world prior to 1945, with multiple great powers and metastasizing competition and conflict.”[1]

– Robert Kagan, a senior fellow at the Brookings Institution and author of Rebelion: How Antiliberalism is Tearing America Apart – Again.

Name a country that has been a constitutional democracy for more than 50 years and turned into an authoritarian state for more than 25 years. It’s hard to name one because those that might pass with ill-defined acceptances are rare and, in some cases, depending on interpretation, do not exist. If you guessed Germany or Venezuela, as many of my acquaintances have in interviews, you would not be correct. Neither fit the year’s criteria.

In each of the last three centuries, there was at least one attempt by a government insider or outsider to challenge morality and gain supremacy beyond constitutional executive power. Authoritarian or totalitarian regimes survive by relying on security police, total control of the media, and military forces to enforce domestic repression, or fighting foreign wars under slogans of nationalism. After all, militaries are a principal component of presidential power in democracies as well as in authoritarian regimes.

As Stephen Kotkin, a Senior Fellow at the Hoover Institute at Stanford University, put it, “authoritarian regimes extravagantly overcommit funds to the agencies, equipment, and training they need for massive repression.” [2]

It may not be a war with guns and bullets, though sometimes it is, but rather a type of war that clashes against political systems. We have seen this before. The Russian Revolution turned Russia from being an authoritarian regime to a totalitarian State, causing an East-West split just as European kingdoms were building showoff armies. Kingdoms were totalitarian, but mostly laissez-faire governments that needed strong armies for their colonialist advances; their domestic pawns accepted their presence, many with pride in their monarchies. At the beginning of the twentieth century, something new came to play out in the geopolitical split started in World War I in 1914, as a test of combatants and materials, and ended as a test of monarchies. Empires broke up in the years between the two world wars, and kingdoms merged with constitutional democracies.

It may not be a war with guns and bullets, though sometimes it is, but rather a type of war that clashes against political systems.

The only emperor in absolute power between the end of WWII and 1974 was Haile Selassie, the Emperor of Ethiopia from 1930 to 1974 when a coup d’état placed him under house arrest at the Imperial palace until his death a year later. We might say he was the world’s last emperor with absolute political power, until roughly now, when we can list at least a dozen leaders who took advantage of geopolitical timing to swing into governing slots of authoritarian power.

Excusing illegal wars

All empires eventually fall. The Mongol Empire is no more. The Akkadian, Macedonian, Ming, Roman, Aztec, Japanese, British, Russian, Spanish, Portuguese, Ottoman, French, and Italian empires no longer exist in the vast territories they once ruled. Some empires grew through political dynasties of transborder governorates. Some were established through defense treaties that formed dominions, colonies, mandates, and protectorates, while others were acquired through states of limited means and unsustainable sovereignty. Many had been created from war victories. They are all gone, now dwarfed by sovereign central political controls. What happened?

The world has changed, partly because some superpowers of the twentieth century fell to corruption and extreme weakness, and control of power by influential people, companies, arms dealers, and public investors. They have no honest ideologies for their nations; rather, they search for shadow policies with tough-scamming disputes that dupe their populations with propaganda that almost everyone is aware of. They gather and trust coconspirators because they cannot grow on their ambitions. Others favor revenge-madness under a policy of exploitation for control, supported by shameless power opportunists, advisors, and loyalists who are hopeful oligarchs, cowardly passive politicians, inexperienced, reckless fanatics, and government lawyers who have studied and stress-tested the loopholes of laws of the political landscape of their states, and aspirants fearing reprisals if they disagree. At the same time, they reward friendly individuals, firms, and organizations with tax incentives, permits, licenses, waived regulations, and lucrative business contracts.

Still, authoritarians, as tough as they seem, don’t fully disobey the constitutional order if it doesn’t twist its legal order to promote dictatorship, which would mean abolishing multipartyism. So far, competitive autocracies in Turkey, Hungary, Tunisia, El Salvator, and India that surfaced since the fall of the Soviet Union continue as electoral autocracies. All have crafted false investigations aimed at prosecuting public agencies disagreeing with government policies. They have weakened civil service protections, fiercely regulated media outlets that oppose government policy, fired professionals in judiciary and military offices and replaced them with loyalists, and rewrote history to favor their so-called accomplishments and delete written notions of their damage. Steven Levitsky and Lucan Way, the authors of Competitive Authoritarianism wrote in a recent issue of Foreign Affairs, “Virtually all elected autocratic governments deploy justice ministries, public prosecutors’ offices, and tax and intelligence agencies to investigate and prosecute rival politicians, media companies, editors, journalists, business leaders, universities, and other critics.” [3]

To note: authoritarian handbooks, in a cloud of secrecy, tell us that a leader should test brutal domestic repression aggressively, keeping it going until the citizenry begins to perceive it as normalcy. In 2018, the U.S. Customs and Border Protection (CBP), an agency that manages border security at ports of entry, had the cruel practice of separating children from their parents who had illegally crossed the southern U.S. border. Approximately 3,000 children were sent thousands of miles away from their parents. Some taken by the government during the zero-tolerance period had still not been reunited with their parents. That now feels normal compared to the current brutal damages by the U.S. Immigration and Customs Enforcement (ICE), an agency enforcing interior investigations and deportations, now witnessed by the citizenry. [4]

The current governing power assumes it can persist with its immorality long enough for protests to decline under exhaustion. If it cannot, it can always fall back on the playbook standard, creating trouble as an excuse to have the military frighten the masses. Americans don’t generally know about that strategy; Russians do. But Americans are starting to notice. As Omar Wasow, Assistant Professor of Political Science at the University of California, Berkeley, adeptly put it in his guest essay for the New York Times, “Regimes that rely on repression face a challenge: The more force they deploy, the more they risk exposing their own brutality to politically persuadable observers. Overreach doesn’t just project strength; it also undermines legitimacy.” [5]

The successful ones are clever enough to breed their policies undercover, slowly building needed security police and militaries geared for domestic repression. With any success they will attempt to take down their rivals through claiming opponent corruption, untrue stories of inflation (that they care nothing about), delegitimizing their challengers by billows of disinformation. Let us not forget how every authoritarian has battened down labor unions. Russia and China have several labor unions, but finding accurate numbers is pointless because the statistics do not exist with ballpark accuracy. Europe’s labor union members average about 16 percent of the population. Scandinavia’s percentage is close to 70 percent, whereas the U.S. population is now less than 10 percent. Consider this, though: The percentage of U.S. labor union members for a few decades just after WWII was close to 35 percent. Labor unions grew and multiplied between 1940 and 1970, then slowly shrunk to just about 10 percent in 2025. Now, why is this relevant to this article? Unions have enormous power and capabilities not just in settling wages, benefits, or working conditions but also in protesting government policies.

When potential authoritarians achieve their goal of leading a state, they – if connivingly clever – govern slowly with mild chaos that expands and hastens their illegal repressive policies to test and collapse the legal order through loopholes that blindsight prosecutors, who are also targets for revenge. Kotkin tells us, “They feel no imperative to satisfy the material aspirations of ordinary people.” [6]If they are not so wickedly clever, they will openly and rapidly create an enemy list, politicize the judiciary and civil service, and punish corporations and media and bring in the military to suppress their rivals.[7] Sound familiar?

A war with no bullets, or maybe just a few

I sleep well at night, but that’s just a blessing of having regular melatonin excretion in my daily cycle. My friends have trouble sleeping these days of authoritarian fear – the clear brutality of ICE’s victims, the revengeful enemy list, the blatant corruption in private gain at the expense of the poor, and our so-called leader’s defective moral and ethical faculties that cannot distinguish between right and wrong.

For now, and I expect for a reasonably short time, we are being governed by leaders without conscience, understanding, and a marginal—though reckless— perception of the structures and pillars supporting both international and domestic benefits.

In 2025, of the 193 United Nations member states, only 29 are considered full democracies, while 45 have turned toward autocracy. During the last thirty years 19 have swung back and forth from autocracy to democracy. [8] Putin got the idea for Russia in 2012 to rebuild the Soviet empire. Other countries that followed are hard to classify. In what position should we put Hungary? Some world leaders, including Victor Orban, the former prime minister of Hungary, consider it to be a democracy, but when digging into its legitimacy, we know he rigged his reelection legally by slinking through loopholes of law. In April 2024, Larry Diamond, a senior fellow at the Hoover Institution at Stanford University, wrote in the Journal of Democracy, “The test of democracy is not whether a regime holds political prisoners and imposes a pervasive climate of fear. It is whether the people can choose and replace their leaders in free and fair elections.” [9]

American democracy is locked into contentious policy issues that divide the country and reshape established governing. Immigration is the principal divider, though crime, abortion laws, inflation, and foreign wars struggle to follow. Subordination and shameless allegiance and obedience to the leader hail the right, while civilians protest peacefully, then aggressively, before surveillance is established and security police step in to goad marchers into violence. It is not yet a war; no bullets have flown, but the trap is set so that bullets can fly. If the state was once a democracy, then autocracy intensifies, elections are staged, and constitutions conflate with the regime’s will. Fortunately, the U.S., unlike the regimes of Putin and Xi, Trump—annoyed and wishing otherwise—must follow constitutional state and federal laws, though lawyers and judges unwittingly read laws through the haze of political self-pressures.

In that scenario, there are two possibilities: One, with enough civilians protesting, the regime is taken down, and there is dancing in the streets. Two, assuming the authoritarians have won, they fear for their future and purposely overreact. They lose balance, and with no way out, they use the excuse of war as the only door open for continuing. Starting a war is the canonical sliding through the cracks of extreme domestic instability and eventual submission.

Submission to what? To everything, including the right to vote. For example, the U.S. commander-in-chief said he will accept the results of the elections only if they are “honest.” One can only suppose the meaning of the word is what he considers it to mean. But his militant policy is a risk that cannot continue. War with Iran is against We the People of the United States, a constitutional document that confirms the rights of domestic tranquility, the promotion of general welfare, the security of liberty to ourselves and our prosperity, and Article I, Section 8, Clause 11, which, among other articles, declares executive measures as temporary and that only Congress has the power to declare war. Article I is part of the core of our Constitution. Destruction happens when the president tells his citizens that what they see is not what he sees. Will he ignore the constitutional requirement for terminating the war without Congress’s approval? Take a guess.

Living with a lie

When Václav Havel became president of what was then Czechoslovakia, he wrote an essay on living with a lie. In that, Havel asked a simple related question: how did the Soviet Union communist system sustain itself?

Mark Carney, Prime Minister of Canada, asked why a grocer living in Soviet times would post a message on his shop window promoting the slogan “Workers of the world, unite!”? That slogan might suggest a trade union, but more broadly, it comes from Karl Marx’s “The Communist Manifesto,” which calls for global solidarity to abolish capitalism. For Gustáv Husák, the Soviet-backed pro-communist President of Czechoslovakia at that time, the slogan meant strict enforcement of loyalty to the regime. So, how would Havel want us to understand the slogan?

In that one question, he packed an introduction that didn’t need an answer. His brilliance showed his power of intelligent leadership by highlighting The Power of the Powerless, a protest manifesto for understanding and uniting a movement against a dictatorship written by Vaclav Havel in 1978, extracting a vignette about a greengrocer, and what Havel called “living with a lie.” Now Carney is using Havel’s manifesto to demonstrate something that has little to do with Havel’s point.

Havel asks, what would happen if the greengrocer took down his sign, simply because he does not believe the slogan is in his interest? Havel tells us that no one really believes the slogan improves life, but people hang that slogan on their windows simply because everyone else does. It is a ritual that everyone knows is false. When everyone is willing to pretend the slogan is true, what would happen if one person were to take down the sign? Havel knew the answer. It took one, and then another, and another before the lie was understood by millions. Havel played a major role in the Velvet Revolution, the November 28th, 1989, non-violent transition of power that toppled the Communist system in Czechoslovakia.

The totalitarian system demands obedience at every step, and that is why the “system is so thoroughly permeated with hypocrisy and lies,” because the working class individual is manipulated by publicly controlled misinformation that systematically flips the meaning of a slogan to its counter-slogan: “the use of power to manipulate is called the public control of power, and the arbitrary abuse of power is called observing the legal code; the repression of culture is called its development; the expansion of imperial influence is presented as support for the oppressed; the lack of free expression becomes the highest form of freedom; farcical elections become the highest form of democracy; banning independent thought becomes the most scientific of world views; military occupation becomes fraternal assistance.” [10] So, everything is falsified to mean the opposite. “It falsifies the past. It falsifies the present, and it falsifies the future. It falsifies statistics. It pretends not to possess an omnipotent and unprincipled police apparatus. It pretends to respect human rights. It pretends to persecute no one. It pretends to fear nothing. It pretends to pretend nothing.” The slogan ends up being a ritualistic symbol of lies that claim to protect the suppressed. Take the case of Donald Trump, a wannabe strongman who has spent an entire lifetime chasing celebrity status. He is jealous of those who truly are strong and know how to work the political gears that move entire political systems through the cogs of power. He looks at Putin and Xi with envy, so he grovels for authoritarian club membership, and therefore lies when he speaks, to follow the showpiece strongmen who lead countries that have seldom ever been democratic.

Trump lies whenever he speaks.

Grocery prices are down.

Prescription drug prices under his watch will be slashed “by 900 percent”, meaning that anyone buying drugs will be given 800 percent of the cost back to the consumer. Hmm… a school child in the sixth grade knows that cannot happen.

Inflation is stopped “in its tracks. I inherited the worst inflation in history.

“Investments in the United States, … secured commitments of over $18 trillion.”

Gas prices are “now at about $2.50 a gallon.”

“Biden gave away $350 billion” in aid to Ukraine. “That’s a massive amount of money.”

“We ended eight wars, and I’ve settled eight wars.”

Regarding alleged drug boat strikes, Trump claims that for “every boat that you see get blown up, we save 25,000 – on average – lives; 25,000 lives.”

Lies that the 2020 election was “a fake election” and “a rigged election.” Trump legitimately lost a free and fair election to Biden.

I could go on to list a hundred more lies, but the ones on this list come from a cabinet meeting. All have been fact-checked and debunked. Every one of those false claims is a wild exaggeration far from the numbers and any reasonable truths. Trump is giving slogans and signs to put in windows. Almost nobody believes him. Most laugh out loud at his lying slogans and cry about the catastrophic global damage done by his incompetence, grift, retribution, and hateful, inhumane tactics. Then we cringe with embarrassment, witnessing his corruption, utilizing public power for his private gain, while the rest of the world feels the pain of economic and health hardships, and struggles with inflation that erodes earning power.

He picked the wrong country to autocratize

It is difficult to know exactly what he wants to accomplish; making sense of his moves is not possible in a rational world.

Trump is the example of the many wannabees waking up to reach for lifetime leadership in politically weak countries, promising headwinds of new right-of-center and far-right entry-level opportunities. It is difficult to know exactly what he wants to accomplish; making sense of his moves is not possible in a rational world. His whims fly in the winds of his own frustrations, whether they be the bogged down wars that he started with no motive at all, but rather an urge of his sparky obsession, moments of expansionist dreams of putting his name not only on buildings but also on reflecting pools, ties, steaks, bibles, gold-plated phones, and wars. Like the Lincoln Memorial Reflecting Pool in Washington, D.C., which once showed dual reflections of the Lincoln Memorial and the Washington Monument, he wants his name mirrored. Like the longings of all wannabes, he wishes his name to be everywhere with immensely large photo portraits hanging from all government buildings, notions far beyond his reach because America still has a relatively strong, yet limited democracy that can be fender-bent but not totaled by recklessness.

America has kept its written constitution as the law of the land for 239 years, far longer than any other country. It has never swung authoritarian, though history tells us there were many attempts, challenges, and warnings. Two centuries of its democracy have case-hardened a system of statutes passed by citizen-elected representatives and approved by a constitutionally semi-guarded supreme court. If Trump wished to autocratize America, he picked the wrong country.

Joseph Mazuris an Emeritus Professor of Mathematics at Emerson College’s Marlboro Institute for Liberal Arts & Interdisciplinary Studies. He is a recipient of fellowships from the Guggenheim, Bogliasco, and Rockefeller Foundations, and the author of eight acclaimed popular nonfiction books. His latest book is The Clock Mirage: Our Myth of Measured Time (Yale).

[6] Stephen Kotkin, “The Weakness of the Strongmen,” Foreign Affairs, Jan.Feb 2026, Vol. 105, No. 1. p 15.

[7] In the U.S., sending the military into its own country to quell civilian disputes require the president to invoke The Insurrection Act, a vague rarely used law that give the president power to deploy the military domestically.

Most homeowners assume that more upgrades mean a higher sale price. But that’s not always true. Some improvements end up costing you money instead of making it back. If you’re thinking about selling soon, it’s worth knowing which upgrades are worth it and which ones are traps.

The Over-Improving Trap

It feels good to renovate. A fresh kitchen, a spa-like bathroom, a backyard makeover. But here’s the thing: your home’s value is tied to your neighborhood, not just your house. If you pour $80,000 into renovations on a street where homes sell for $250,000, you’re unlikely to get that money back. Appraisers call this “over-improving.” The local market sets a ceiling, and no amount of granite countertops will push past it.

This is something local real estate experts see all the time. One of renowned Raleigh realtors, EmpowerHome Team, says, “During times of market uncertainty, our clients find solace in our signature guarantees that stand behind our promises and take the risk out of buying or selling a home.” The takeaway? Before you renovate, understand your market. The smartest sellers do their homework first.

Bold, Personal Design Choices Turn Buyers Off

You love your wine-red accent wall and your custom mural in the dining room. That’s great. But potential buyers may not. Highly personal design choices narrow your buyer pool. The more personalized your home looks, the harder it is for someone else to picture themselves living in it.

Instead, go neutral. Soft whites, warm grays, and earthy tones work for almost everyone. These shades photograph well, look clean, and let buyers imagine their own furniture in the space. A few hundred dollars of paint in the right color can do more for your sale than a $10,000 custom feature wall.

Sunrooms and Pools: Think Twice

A sunroom sounds lovely. A private pool sounds even better. However, these are two of the most commonly cited upgrades that fail to return their cost at resale. Pools, in particular, can actually scare off buyers who don’t want the upkeep, the liability, or the safety concerns if they have young children. In cooler climates, a pool can sit unused for half the year and still cost hundreds to maintain. Unless you live somewhere warm and pools are standard in your price range, this is a risky spend.

Sunrooms are similar. They’re expensive to build properly and rarely add equivalent value to the appraised price. Many buyers simply don’t need or want that extra space.

Converting Rooms Removes Flexibility

Turning a bedroom into a home gym or a walk-in closet might feel like a dream upgrade. But bedrooms matter when it comes to value. A three-bedroom home is almost always worth more than a two-bedroom with a yoga studio. If you’ve converted a bedroom into something else, consider converting it back before listing. It’s a simple change that can meaningfully impact how buyers see the home.

The same goes for garages. Many sellers convert garages into entertainment rooms or extra living space. While this sounds appealing, buyers often want a functional garage. It’s storage, it’s security, and it’s practical. Removing that can lower offers.

The Right Upgrades Still Matter

Not all home improvements are a mistake, of course. Some upgrades have a proven track record of returning more than they cost. A new front door, for example, consistently ranks as one of the best investments for resale. It’s the first thing a buyer sees. A clean, updated entryway signals that the rest of the home is well-cared for.

Minor kitchen updates also beat major ones almost every time. Replacing cabinet hardware, updating light fixtures, or swapping out an outdated faucet can refresh the look without the massive price tag of a full remodel. If you’re planning a bigger project, it also helps to understand the full house flipping process so you know exactly where your money will and won’t work for you.

Similarly, fresh neutral paint, clean landscaping, and a power-washed driveway can dramatically improve curb appeal for a few hundred dollars. These small wins add up fast.

Skipping Permits Is a Silent Deal-Killer

Here’s one that catches a lot of sellers off guard. If you’ve added a bathroom, finished a basement, or done structural work without a permit, it can come back to bite you hard. Unpermitted work can delay your closing, reduce your sale price, or even force you to undo the work entirely. Buyers discover this during inspections, and it immediately raises red flags.

Always pull the required permits before starting significant work. It protects you legally and gives buyers peace of mind.

Don’t Chase Trends Right Before Listing

Design trends move fast. What looks fresh today can feel dated in two years. If you’re selling soon, avoid investing in highly trendy finishes that may not age well. Think about what has staying power: clean lines, quality materials, and functional layouts never really go out of style.

When in doubt, focus on the basics. Fix what’s broken, clean what’s dirty, and neutralize what’s too personal. Research on budget-friendly renovation options that actually return value shows that simple updates often outperform expensive overhauls at resale.

More spending doesn’t always mean more value. The sellers who do best are the ones who renovate with their buyer in mind, not their own taste. Know your neighborhood, prioritize practical upgrades, and keep the personal touches to a minimum. That’s the formula that gets homes sold at the best price.

This article examines recent US–China engagement, including President Trump’s visit, to assess evolving economic and geopolitical dynamics. Dr Kalim Siddiqui argues that US trade imbalances stem primarily from structural differences in savings, consumption, and comparative advantage rather than tariffs or exchange rates. The study highlights China’s industrial and technological rise alongside mounting US challenges, including rising debt and trade deficits, deindustrialisation, weak investment, and slow growth.

I. Introduction

During his recent visit to China, Donald Trump appeared to acknowledge significant limitations on US power. Over the past two decades, China has undergone a remarkable transformation, huge expansion of industrial sector, substantial control over the production and supply of critical minerals and huge investment in modern industries, higher education, and infrastructure. Consequently, the United States (US) has become increasingly dependent on China for critical minerals, which are essential to its defence systems and next-generation technologies. This growing dependence not only constrains US strategic autonomy but also raises serious concerns regarding national security and long-term technological competitiveness.

According to United Nations Industrial Development Organization (UNIDO) breakdown of global manufacturing output shares for China, the US, and other major economies the following: As of 2025 data, China alone produces more manufacturing output than the US, Japan, Germany, and India combined. China share of global manufacturing output is 35%, and the US, Japan, and Germany are 12%, 6%, and 4% respectively in 2025. Furthermore, according to UNIDO projection China’s share is expected to continue growing, potentially reaching 45% of global manufacturing by 2030. During the same period, the combined share of the US, Japan, and Germany is projected to fall to just 19% (UNIDO, Industrial Report, 2026).

Nevertheless, this transformation reflects an ongoing reality of the contemporary world economy—however difficult it may be to accept.

Moreover, China’s manufacturing sector is now larger than those of the next several advanced economies combined across many industries. China leads the world in manufacturing value added in sectors such as steel, electronics, solar panels, batteries, consumer goods, shipbuilding, and a wide range of chemical and machinery industries. It also dominates the processing and manufacturing of rare earth elements. As of 2025, China accounts for approximately 90% of global rare earth refining and processing capacity, creating significant strategic dependencies for many advanced economies (Siddiqui, 2025a).

Since 2017, escalating tariff disputes and geopolitical tensions have led China to redirect more exports toward emerging markets, while the US has adopted increasingly protectionist policies. Between 2005 and 2017, bilateral trade grew rapidly following China’s 2001 WTO accession, with rising US imports of Chinese goods contributing to a persistent trade deficit (Siddiqui, 2025b). Following the return of the Trump administration in 2025, US–China goods trade contracted further. By March 2026, US imports from China had fallen 29.7% to $308.4 billion, while US exports to China declined 25.8% to $106.3 billion, narrowing the US trade deficit.

China holds the world’s largest stock of foreign exchange reserves, which exceeded US$3.3 trillion in 2026, and maintains a comparatively moderate level of external debt relative to the size of its economy. By contrast, US gross federal debt surpassed US$39 trillion by May 2026, exceeding annual GDP and generating substantial interest-payment obligations (US Treasury Fiscal data, 2026). China also continues to record large trade surpluses, with its merchandise trade surplus reaching a record US$1.2 trillion in 2025, whereas the US has persistently run trade deficits. These contrasting external and fiscal positions have important implications for the long-term economic resilience and financial flexibility of the two countries.

The US leads in military spending, with some 800 bases worldwide—an unparalleled presence that carries high opportunity costs in forgone industrial and technological investment. These divergences in debt and external balances reflect deeper structural differences in financial integration, savings rates, and reserve currency status. Trump has proposed a 50% increase in defence spending, aiming to stimulate the US economy through a form of military Keynesianism. A parallel situation occurred in the early 1980s, when the US faced a trade deficit with Japan. In response, the US compelled Japan to accept a sharp appreciation of the yen—culminating in the Plaza Accord in 1985—which led to a steep decline in Japanese exports and triggered an economic crisis from which Japan has yet to fully recover, even three decades later (Siddiqui, 2009).

At present, the US appears to be seeking a similar arrangement with China—a “Plaza Accord” for the 21st century. However, China is not Japan, and the global economic landscape has changed dramatically over the past four decades. Today, the US economy and its manufacturing base are significantly weaker than they were in the past. In contrast, China has developed a far more diversified economy and established extensive trade linkages with the rest of the world. Unlike Japan, China possesses a vast domestic market and a robust manufacturing sector, and it does not rely solely on US markets, military protection, or diplomatic support. As a result, China is unlikely to accept an overvaluation of the renminbi that would undermine its manufacturing sector and export competitiveness.

Other major advanced capitalist countries, such as the UK and France, are increasingly recognising that, within a changing global economy, China should not be viewed primarily as a competitor or a threat. Rather, China represents a major economic power with which stable trade relations are essential for peace, prosperity, and mutual economic benefit. China does not perceive EU countries through the lens of confrontation, but as important partners within the global economy.

It is thus necessary to assess where the UK and France can realistically compete with China. China is now the world’s largest automobile manufacturer and leading exporter of electric vehicles. It is advancing quickly in semiconductor and R&D and is poised to become a global leader in that field. More broadly, China has emerged as a dominant force across many strategically significant twenty-first-century industries, including artificial intelligence (AI).

The question, however, is whether China competes with UK and France on equal industrial and technological terms. Evidence suggests it does not. The UK and France should therefore avoid overestimating their current position in global manufacturing and innovation. China’s rapid economic transformation has fundamentally reshaped the global economy, making its investment, trade, and manufacturing increasingly vital—especially for the Global South.

Former European powers like the UK and France must adapt to this new reality rather than pursuing isolation or confrontation. Neither country commands the global dominance it held a century ago, when both controlled major trade routes, colonies, raw materials, and large-scale industrial production. Much of their contemporary influence still derives from structures established during the nineteenth-century colonial era—an observation that applies to several former European colonial powers.

A similar historical pattern can be seen in the US. For decades, Global North economies were integrated into an international system reliant on extracting resources and labour from the Global South. Thus, when a rising power like China openly challenges this historical and economic hierarchy, it generates discomfort in parts of the Global North. Nevertheless, this transformation reflects an ongoing reality of the contemporary world economy—however difficult it may be to accept.

II. Trump’s 2026 China Visit: A Strategic Win for China

President Trump’s recent visit to China appears to have been a significant success for China, as China seeks to revitalise its economy and strengthen bilateral trade relations. At the same time, the US seems to have quietly shifted its stance from strategic competition towards a more conciliatory approach to China.

Trump’s previous visit to China took place in 2017, at a time when the world was still largely unipolar and the US occupied a very different global position. China was then viewed as a weaker economy that needed to be contained and undermined. In 2019, the US banned the Chinese telecommunications companies Huawei and ZTE from involvement with the US Department of Defence, and earlier, in 2018 (Siddiqui, 2018), Trump signed the National Defence Authorization Act. However, following Trump’s 2026 visit to China, the US removed export controls on Nvidia H20 chip exports to China (The New York Times, 2026).

In his opening remarks during the visit on 14 May 2026, President Xi Jinping stated that the world had arrived at a crossroads and was becoming increasingly multipolar. He questioned whether China and the US could transcend the “Thucydides Trap.” The concept was popularised by Harvard professor Graham Allison in 2017. In his study of 500 years of history, Allison identified sixteen cases in which a rising power challenged an established one; in twelve of those cases, the rivalry ultimately resulted in war.

The ancient Greek historian Thucydides argued that the Peloponnesian War (431–404 BCE) became inevitable because of Sparta’s fear of Athens’ growing naval, economic, and political influence. This dynamic has since become known as the ‘Thucydides Trap’. The 27-year conflict pitted democratic and commercially oriented Athens against militaristic and conservative Sparta.

The ‘Thucydides Trap’ suggests that when a rising power threatens to displace an established hegemon, the resulting structural tensions often lead to war. This framework is frequently applied to contemporary US–China relations. Since the Second World War, the US has remained the dominant global economic power, while China has rapidly expanded its economic influence, particularly through manufacturing and the ‘Belt and Road Initiative’. Tensions stem from US concerns over China’s economic growth, trade surplus, and technological advancement.

Today, it raises the question of whether the US and China will repeat history or avoid conflict. Rivalry is evident in trade disputes, tech restrictions, AI, semiconductors, cybersecurity, and tensions in the South China Sea and over Taiwan. Yet the current context differs fundamentally from ancient Greece. The US and China are economically interdependent, both possess nuclear weapons, and share global institutions like the UN and WTO—factors that deter direct war.

Trump’s recent visit to China took place from a considerably weaker position. One of the central issues on his agenda was reportedly an attempt to persuade China to support the opening of the Strait of Hormuz. However, President Xi Jinping continued to support Iran’s position on the matter and instead called on the US to cease its attacks on Iran and lift its blockade.

Global economic cooperation and peace are fundamental to sustainable development and regional prosperity. Within the global economy, the Middle East retains strategic importance due to its energy resources, market potential, and investment opportunities. As John Mearsheimer and Stephen Walt (2007) have argued, Israeli influence within US political structures remains deeply entrenched. More recently, Ilan Pappe (2025), in Israel on the Brink, contends that lasting peace in the region hinges on acknowledging decades of historical injustices inflicted upon Palestinians—including the Nakba, ongoing violence in the West Bank, and the devastation in Gaza. Pappe calls for accountability, equal rights, and an end to systemic discrimination and violence against the Palestinian people.

The modern Middle East was profoundly shaped by the 1916 Sykes–Picot Agreement, in which Britain and France carved up the region to serve imperial interests. These externally imposed borders fragmented local societies and sowed enduring geopolitical strife. Meanwhile, since its establishment in 1948, Israel has been widely analysed as a settler-colonial project. Scholars point to policies of dispossession, territorial expansion, genocide, and regional military aggression as part of a broader strategy for domination in the Middle East (Siddiqui, 2026b).

Another apparent objective of Trump’s visit was to project the US as the world’s preeminent superpower and to reinforce his “Make America Great Again” (MAGA) narrative among the US public. In practice, however, Trump appeared to return in a weakened position. The US no longer seems to enjoy unquestioned superiority over China. Trump himself implicitly acknowledged this shift when he praised Xi Jinping as a great leader and described China as a great country.

Overall, Trump did not achieve all of his objectives, whereas China appeared to derive greater benefit from the meeting between the two leaders. Consequently, the encounter may mark the beginning of a new phase in US–China relations. China has never openly sought to replace the US as the sole global power; rather, it has consistently advocated for a multipolar international order.Bottom of Form

China is not generally regarded as an expansionist country. Rather, it views Taiwan as a legacy of historical and colonial division that emerged during a period of Chinese weakness, commonly referred to in Chinese history as the “Century of Humiliation.” This was the period during which China faced repeated aggression and intervention from the major European powers of the time. Consequently, China regards Taiwan as a core national interest and a non-negotiable red line. President Trump’s approval of $25 billion in arms exports to Taiwan will almost certainly heighten tensions and increase the risk of conflict (The New York Times, 2026).

The Chinese leadership has repeatedly stated that it has no interest in becoming the world’s hegemonic power or replacing the US as the leading global power. China’s rise has been driven primarily by geoeconomics, with trade serving as the foundation of its remarkable growth over the past forty-five years. To improve the living standards of its people, China seeks economic cooperation and peace rather than confrontation (Siddiqui, 2024a).

President Xi Jinping is likely to believe that the summit demonstrated how dependent the US and much of the world have become on Chinese manufacturing and supply chain. China now produces roughly one-third of the world’s manufactured goods, processes over 90% of rare earth minerals, and dominates global production of solar panels, wind turbines, and electric vehicles.

Xi Jinping emphasized the need for expanded cooperation in trade and agriculture, signalling that China may be willing to increase purchases of US soybeans, beef, and Boeing aircraft. Meanwhile, the US seeks to maintain access to rare earth supplies, establish trade mechanisms for non-sensitive sectors, and secure Chinese purchasing commitments. The limited scope of these objectives, compared with the broader strategic rivalry between the two powers, suggests that both sides are focused more on managing tensions than resolving them (The Financial Times, 2026),

For global trade partners, little is likely to change. Economic hedging and trade diversification will remain prudent policies. The true significance of the summit will depend less on political rhetoric and more on whether economic commitments are implemented in practice, particularly regarding trade, technology, and artificial intelligence cooperation.

Since Trump’s return to the White House in January 2025, international politics has become increasingly unpredictable. Nevertheless, the Xi Jinping –Trump summit of May 2026 was unlikely to produce any dramatic strategic breakthrough. Neither China nor the US appears ready for a grand bargain, but neither side wants a complete breakdown in relations that could further damage the fragile global economy. Key issues remain the durability of the trade truce, cooperation on technology and AI safety, and whether China will use its influence to help reduce tensions with Iran.

Although China continues to rise as the world’s leading manufacturing power, with the Belt and Road Initiative extending across multiple regions (Siddiqui, 2019), it also faces serious long-term challenges. Many discussions overlook the scale of China’s demographic and environmental pressures. China’s working-age population peaked in 2011, and by 2050 the country is projected to have more people over the age of 65 than the entire current population of the US. The workforce that powered China’s economic transformation is aging rapidly, while the number of younger workers entering the labour market continues to decline.Top of Form

Although surprises are always possible, the Trump–Xi Jinping summit is likely to be defined by a narrow set of issues: Taiwan, export controls, trade deficits and supply of critical minerals. These will be the key indicators in assessing whether the meeting represents a success for the US.

China’s primary objective is to reduce US support for Taiwan. China hopes to pressure The US into abandoning the proposed $14 billion arms package expected this year, in addition to the $11 billion deal announced previously. Notably, the Trump administration has yet to approve the new package, reportedly delaying the decision to avoid provoking China ahead of the summit.

Trade will also dominate discussions. Trump has pressed China to increase purchases of US goods in order to reduce the US trade deficit. The summit is therefore expected to produce Chinese commitments to buy more US soybeans, beef, aircraft, and other exports, offering relief to US farmers and businesses affected by bilateral tariffs. At the same time, China will attempt to use these purchase agreements to secure broader access to advanced US technologies, including semiconductor chips and aircraft engines.

During their previous meeting in South Korea in October 2025, Trump and President Xi Jinping agreed to suspend retaliatory tariffs for twelve months. Those record-high tariffs inflicted economic damage on both countries, giving China and The US a shared interest in extending the trade truce. Some form of extension therefore appears likely.

Following that meeting, the White House stated that China had committed to easing restrictions on critical minerals, including rare earths, gallium, germanium, and graphite through expanded licensing arrangements for US users. These measures were presented by the US as a significant easing of export controls imposed since 2023.

III. Persistent Imbalances in US–China Trade

There have been persistent trade imbalances between the US and China since 1986, when the US began running a sustained trade deficit with China. The deficit grew especially large during the 1990s and expanded rapidly after China joined the World Trade Organisation (WTO) in 2001. Although US trade policy toward China has undergone significant changes over the years, these shifts have had surprisingly little impact on overall trade balances. In 2025, the US trade deficit with the rest of the world remained highly volatile, reaching approximately $918 billion. The US continues to run large trade deficits with countries such as China, Mexico, Vietnam, and Germany.

While China ran a large trade surplus with the rest of the world, it has steadily expanded due to rising exports of manufactured goods, increased industrialisation, and greater value addition to final products. A massive growth in supply chains—critical to advanced economies—has further fuelled this trend. China currently runs the world’s largest trade surplus. For instance, in 2025, it reached a record high of nearly 1.2trillion in goods trade. This surplus is driven by strong exports of electronics, machinery, solar panels, batteries, and electric vehicles. Although China’s surplus with the US has declined in recent years, exports to Southeast Asia, Europe, Latin America, Africa, and the Middle East continue to grow.

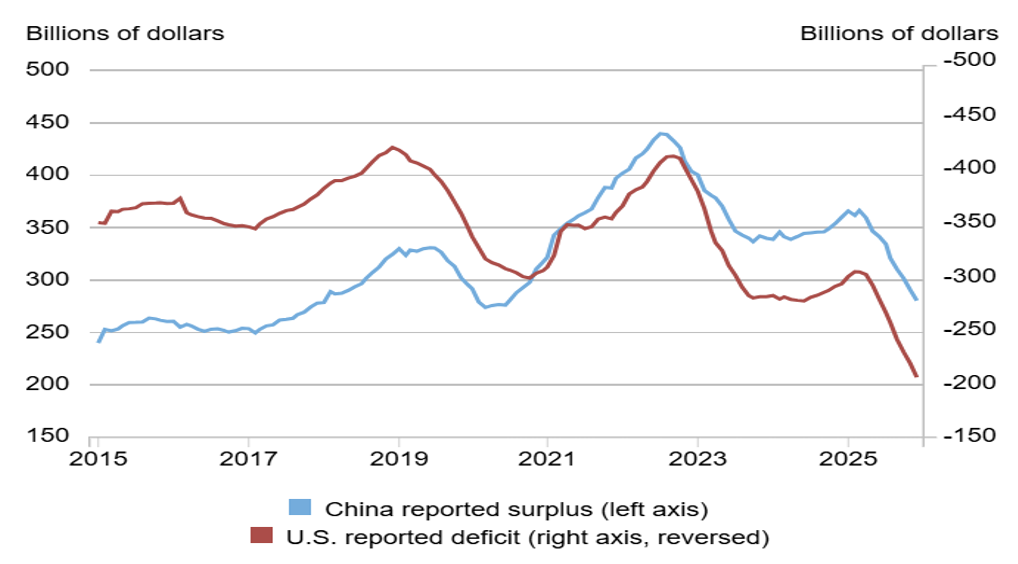

However, bilateral trade balances are shifting. Figure 1 shows US-China trade from 2015 to March 2026. Since 2025, trade has weakened: both US imports from and exports to China have declined following Trump’s tariffs aimed at reducing US imports.

Figure 1: United States Trade with China, between January 2015 and March 2026 (in billions of $).

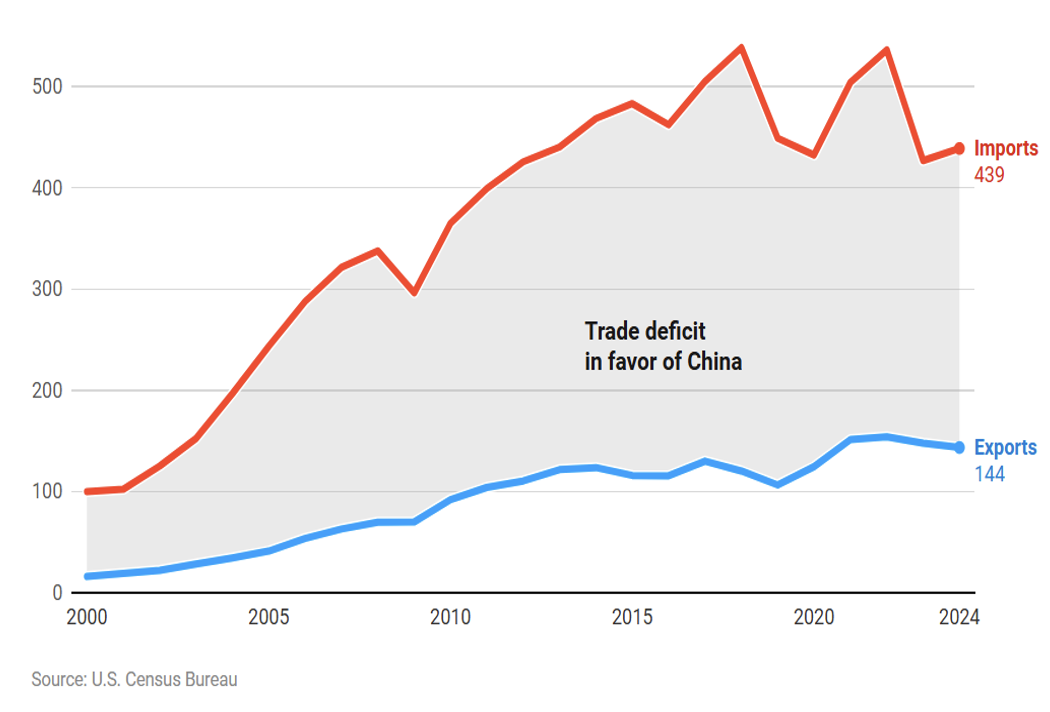

US exports to China totalled $143.5 billion in 2024, a decline of 3% compared with 2023. Meanwhile, imports from China increased to $438.9 billion, resulting in a widening US–China trade deficit that exceeded $295.4 billion last year. This increase highlights the persistent imbalance in bilateral trade from 2000 to 2024, which has continued to deepen since the beginning of the 21st century, as illustrated in Figure 2. According to official data, the flow of goods continues to Favor China. Chinese imports accounted for 12% of total US imports, second only to Mexico, which represented 13.8%.

Figure 2: United States Exports and Imports with China, 2000-2024 (in billions of $).

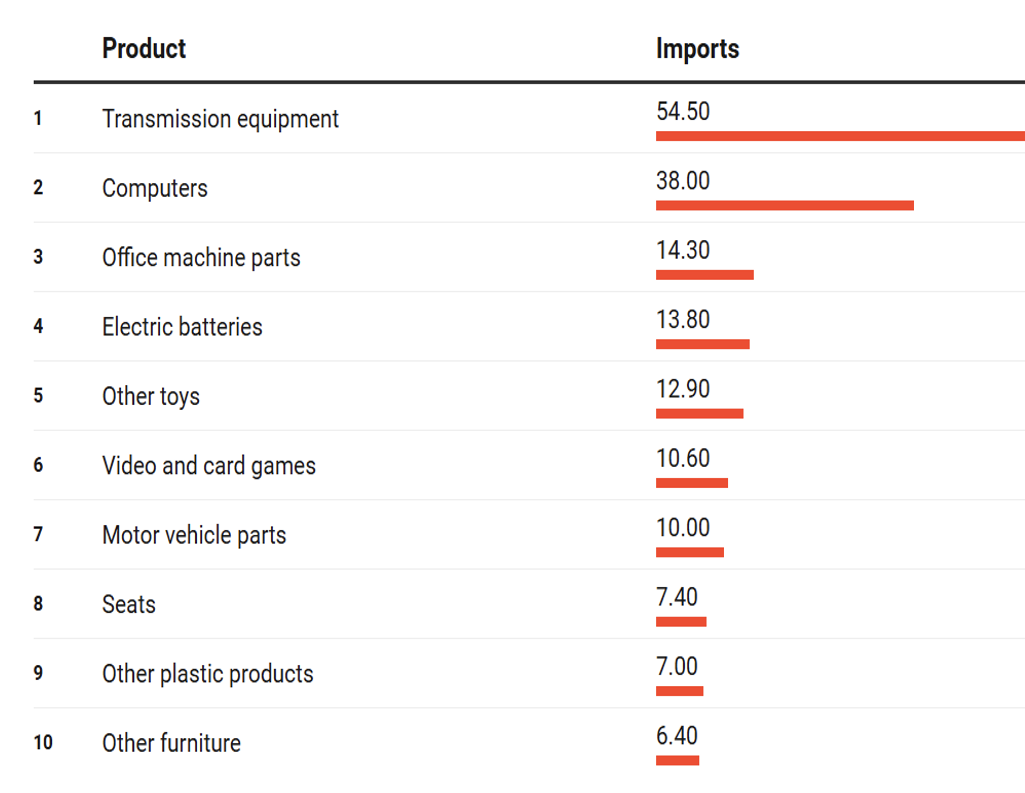

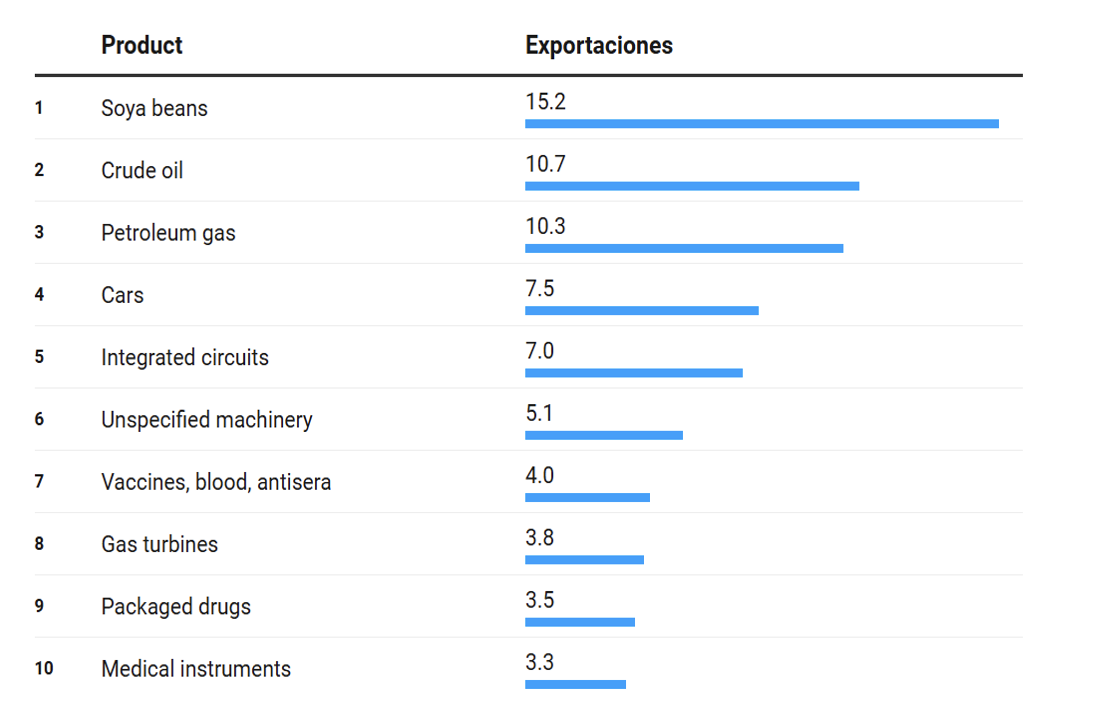

The US relies heavily on Chinese manufacturing to meet domestic demand for consumer goods and technology products. According to official statistics, in 2025 the main imports from China include telephones, computers, semiconductors, furniture, toys, and textiles. Electronics and machinery alone accounted for more than 50% of the total value of imports (See Table 1). In contrast, US exports to China are more diversified, although considerably lower in volume. These exports primarily consist of products such as aircraft, vehicles, semiconductors, industrial machinery, and agricultural goods, including soybeans and beef. While these sectors are important to the US economy, exports to China remain significantly smaller than US imports from China (as shown in Table 2).

Table 1: United States Imports from China, 2025 (in Billions of US Dollars)

The trade balance shows that, since 2000, the US has purchased far more goods from China than it has sold to the Asian economy. (Siddiqui, 2024b). As a result, the US–China trade deficit reached a historic high of $418.2 billion in 2018. Since then, the deficit has declined moderately due to changes in trade policy and disruptions caused by the COVID-19 pandemic.

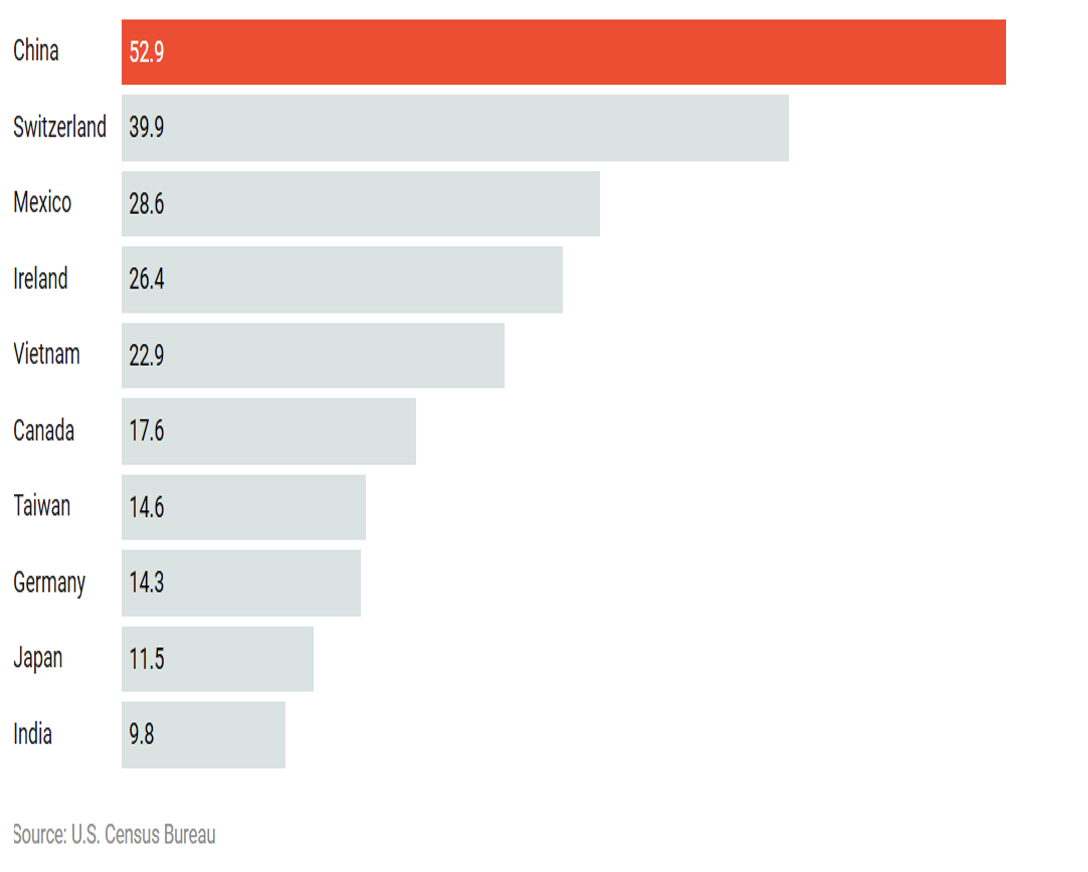

Notably, the largest trade imbalance occurred during President Trump’s first term, when the administration imposed extensive trade restrictions on Chinese products. These measures contributed to a slowdown in China’s economy and were accompanied by a sharp decline in US exports to China by the end of 2018. In March 2026, the US’ largest trading partners were China, Switzerland, and Mexico, as shown in Figure 3.

However, an analysis of the US trade imbalance between imports and exports indicates that the country runs its largest trade deficits with three countries that have been primary targets of President Trump’s trade policies: China, Mexico, and Canada. Mexico became the largest exporter to the US in 2023, overtaking China. This shift was driven largely by the preferential market access established under the US–Mexico–Canada Agreement (USMCA), which enabled Mexico to capitalize on its geographic proximity and strong trade integration with the US market.

Figure 3: Countries with which the US Has the Largest Trade Deficits in January and February 2026 (in Billions of Dollars)

IV. Beyond Tariffs: The Domestic Origins of Trade Imbalances

Macroeconomic analysis focuses on three main categories: savings (households, firms, and government), investment (primarily firms and government), and consumption (households, firms, and government). From this perspective, achieving a more balanced trade position requires increasing national savings by reducing private consumption and/or lowering government expenditures relative to revenues.

Behind this lie broader dynamics related to household consumption, savings behaviour, and the allocation of national income toward investment, infrastructure, and economic growth. When income is distributed unevenly among households, firms, and government, structural imbalances can emerge. For example, households may experience insufficient purchasing power, or firms may accumulate excessive capital relative to productive investment opportunities. Such conditions can generate crises of underconsumption or over investment, both of which have significant implications for trade patterns and trade policy (Liu and Woo, 2018).

But during the US–China trade conflict, particularly throughout the 2016 and 2024 US presidential election campaigns, issues such as savings, investment, and consumption received relatively little attention in political discourse. Karl Marx argued that capitalism contained internal contradictions that could eventually lead to crisis through the dynamics of capital accumulation. However, his analysis did not develop a rigorous model of capitalist crises beyond broad observations concerning periodic episodes of underconsumption and over- or underinvestment. More importantly, Marx largely analysed national economies as relatively closed systems, which limited his ability to account for the central role of international trade and capital flows in modern economic crises (Siddiqui, 2025b).

It was not until John Maynard Keynes that economists developed a more systematic explanation of the cyclical instability of capitalism and its implications for trade (Siddiqui, 2018). Keynes argued that disequilibrium was not an abnormal condition, but rather a recurring and structural feature of capitalist economies. Periods of overinvestment and underinvestment, excessive or insufficient consumption, fluctuations between low and high savings, as well as financial crises and crashes, were all viewed as normal characteristics of the capitalist economic system.

Although US–China trade became a major political issue during the 2016 US presidential election, tensions between the two countries had been building for many years. China’s large population, abundant labour supply, and comparative advantage in labour-intensive manufacturing positioned it as a potential economic powerhouse long before its rapid economic rise. According to trade models based on relative factor abundance, particularly the Stolper–Samuelson theorem (1941), China’s vast labour supply implied that it would specialise in and export labour-intensive goods (Liu and Woo, 2018, Siddiqui, 2016).

However, the full impact of this shift on workers in importing countries only became evident several years after China joined the WTO in 2001. China’s rapid economic growth was matched by an even faster expansion of its exports. Today, China is the world’s second-largest economy (at current exchange rates) and the largest manufacturer and exporter of industrial goods. Given this transformation, it is unsurprising that China’s rise has fuelled economic and political tensions with established global powers (Hopewell, 2020).

V. The Dollar’s Exorbitant Privilege and the US Debt Paradox

Since the 2008 global financial crisis, the US economy has faced sluggish growth, rising unemployment and inequality, weak productivity growth, and chronic under-investment in domestic manufacturing. Yet despite being the world’s largest debtor—with $38.9 trillion in total debt and a federal debt-to-GDP ratio of 122.5%—yet the US has avoided a sovereign debt crisis. This paradox stems from the dollar’s “exorbitant privilege” as the world’s primary reserve and trade currency, a status actively constructed through the 1974 petrodollar agreement with Saudi Arabia, which priced global oil sales in US dollars and recycled petrodollars into US Treasuries (Siddiqui, 2026a).

Critically, this privilege has enabled the US to finance massive fiscal deficits without market discipline, even as it spent over $8 trillion in the last two decades on wars and destabilising interventions in Afghanistan, Iraq, Syria, Libya, Somalia, Venezuela and Iran (Siddiqui, 2026b). Rather than productive investment, these expenditures have fuelled military Keynesianism and geopolitical overreach, further hollowing out the domestic economy while dollar hegemony artificially suppressed borrowing costs (Siddiqui, 2026c).

However, this precarious equilibrium is eroding. Rising oil exporters (Russia, and Iran) are settling trades in renminbi, and Saudi Arabia has signalled openness to non-dollar transactions. Should the petrodollar system collapse, the US would face currency depreciation, soaring interest rates, and a debt crisis long deferred. Policy implications are urgent: gradual fiscal consolidation, a manufacturing industrial policy, diplomatic preservation of dollar pricing as a transition, and preparation for a multipolar reserve system.

But if countries stop using dollars for oil—if China, Russia, Saudi Arabia, and others switch to other currencies (Siddiqui, 2024c)—then that advantage will disappear. Once it’s gone, the US will no longer be able to hide the consequences of its over spending and military overreach. Interest rates will rise, debt payments will become unaffordable, and a real financial crisis could follow.

The 20th-century wave of neoliberal globalisation now appears exhausted, marked by imperialist wars, rising nationalism, intensifying trade conflicts (Siddiqui, 2025c), and global social unrest. Beneath these symptoms lie deep structural imbalances and widening social inequalities, both within and across nations.

The first globalisation wave, driven by late-19th-century Western colonialism, saw nationalism and militarism unravel the British-centred order and shatter the post-1815 European peace. A militarized Germany and intensifying inter-imperialist rivalries overwhelmed Britain’s dominance. Economic liberalism and free trade weakened after the 1880s and collapsed entirely when Germany sought European hegemony in 1914. This first phase of Western globalisation ended with the outbreak of World War I (Siddiqui, 2025d).

Karl Polanyi’s (1944) book The Great Transformation discusses on the collapse of liberalism and the outbreak of another world war. He argued that transnational capitalist cooperation—embodied by pan-European networks of high finance whose functional role was to avert general wars—had ultimately succumbed to national power politics. Power, he contended, took precedence over profit. However closely their realms interpenetrated, it was ultimately war that laid down the law to business. Despite the high degree of European economic integration achieved in the latter part of the 19th century, the webs of capitalist interdependence were swept away by the rising nationalist tide.

Polanyi’s insights offer a valuable analytical framework for understanding the impasses of our own era. Powerful disintegrative forces have been unleashed, threatening the edifice of the contemporary liberal order. At the societal level, intensified social resistance manifests both in the emergence of a global democratic movement for social transformation and in the rise of authoritarian right-wing populism. At the level of state power, the most telling reaction—one that has actively accelerated disintegration—has been the spectacular revival of nationalism in China, Russia, Japan, Europe, and elsewhere. In the US, the core state of the global capitalist system, nationalism has taken a particularly exacerbated form: imperialism.

During the 1990s, many believed that information technology, transnational capital, and global production networks would shift power from public to private actors, eventually eroding the territorial state as the primary locus of world power. Evidence cited included the rise of a transnational capitalist class with global interests. Classical imperialism—competing expansionist nation-states—was seen as unsustainable under an interdependent system governed by supra-state institutions. Capital is capitalism’s central power institution, driving the transformation of power relations. Its accumulation must be examined conceptually, historically, and empirically—from pre-capitalist origins to world dominance—through competing theories of value (Van der Pijl, 1984).

Concurrently, the US has waged “endless wars” (especially post-2001) to maintain global order, suppress rival economic models, and preserve capitalist hegemony (Siddiqui, 2025e). Two competing tendencies have shaped this system: “money-capital” (liberal internationalists favoring market mechanisms, sound money, and bankers/merchants) and “productive-capital” (proponents of politically managed arrangements and industrial cartels). Free trade serves money-capital by enabling cross-border mobility to maximize profits. Productive capitalists, tied to fixed facilities, often seek state protections. This divergence extends to labour, healthcare, and all spheres of political economy.

The Great Depression of the 1930s provided a major impetus for the ascendancy of the state-monopolist tendency. Free trade began to collapse as governments increasingly adopted tariff barriers, while Fordism, Keynesianism, and the New Deal all tended to favour industrial capital at the expense of finance capital. At the same time, a strong isolationist current emerged among sections of the US capitalist class, particularly among Chicago-based industrialists and domestically oriented manufacturers such as International Harvester and Sears, Roebuck and Company. This tendency also gained support within heavy industry — especially sectors producing inputs for the means of production — which resisted mounting pressure for intervention beyond the Western Hemisphere. Instead, these industries favoured the establishment of a sphere-of-influence arrangement with German industrial capital.

However, the Second World War dramatically accelerated Keynesian state expenditure on productive capacity in the US. Following Allied victory, productive capital retained its dominant position as the US manufacturers expanded exports across global markets. A new form of internationally oriented industrial capitalism emerged, facilitated in large part by the wartime destruction of major industrial competitors in Europe and Asia. Out of these conditions emerged a new synthesis: corporate liberalism (Van der Pijl, 1984).

VI. Hegemony, Bipolarity, Multipolarity, and Trade

China’s rapid rise between 1980 and 2025 established it as the world’s largest exporter and the second-largest economy after the US. During these forty five-year periods, China maintained an extraordinary average growth rate of about 8% annually. Part of this expansion reflected “catch-up dynamics,” whereby developing economies benefit from adopting technologies pioneered by advanced industrial economies. However, China went beyond simple technological imitation by developing globally competitive firms such as Alibaba and Huawei, while also emerging as a major innovator in areas such as artificial intelligence and electric vehicles. China’s Fifteenth Five-Year Plan aims to expand the use of artificial intelligence in both production and services throughout its economy. Although China’s rise generated significant economic benefits domestically and internationally, it also produced predictable economic and geopolitical tensions with other major power i.e. the US (Siddiqui, (2024a; Hopewell, 2020).

China’s conflicts with the US are not fundamentally rooted in direct competition over market share or industrial specialisation. The two economies have distinctly different factor endowments and occupy different positions within the global economic landscape. China has historically benefited from relatively low wages and an abundance of labour, particularly in labour-intensive manufacturing. In contrast, the US holds advantages in human capital, advanced technology, physical capital, and certain agricultural and raw material sectors. Consequently, the two countries tend to specialize in different types of production and serve different segments of global markets.

Consequently, the primary source of tension has not been competition in third-country markets, but rather the scale and imbalance of bilateral trade between the two economies. The US has repeatedly accused China of currency manipulation, forced technology transfers, and unfair trading practices. While some disputes have focused on specific sectors—such as agricultural subsidies, fisheries, and export financing—the most politically significant conflicts have extended beyond individual industries and affected the broader structure of economic relations between the two countries. In this sense, the dispute is best understood as a macroeconomic and geopolitical issue rather than simply a sectoral trade conflict.

Some disagreements may also stem from differing interpretations of economic developments. For example, the US argument that China’s currency depreciation harms US trade overlooks the fact that the Chinese renminbi has generally appreciated since 2005. Despite this appreciation, the US trade deficit with China has persisted. If exchange-rate adjustments fail to correct trade imbalances, this suggests that the underlying causes lie elsewhere. One possible explanation is the relatively low level of US national savings, which contributes to persistent trade deficits across a broad range of countries rather than with China alone. Indeed, the US runs trade deficits with more than 100 countries worldwide.

The core problem, in simple terms, is that the US consumes too much and saves too little, while China saves too much and consumes too little. China has relied heavily on the purchasing power of US consumers, while the US has depended on China’s excess savings and export capacity. Although this relationship has gradually begun to change, it has long been at the center of the US–China trade imbalance.

Domestic economic imbalances often translate into international trade imbalances. One important aspect of this issue is China’s exceptionally high savings rate, which has played a central role in shaping global trade flows. Despite recurring tensions, the US and China have maintained a long-standing trading relationship that has generated significant economic benefits for both countries. Historically, support for free trade in the US extended across both major political parties, and the US–China Relations Act of 2000 represented a notable bipartisan achievement in Congress.

A second explanation for trade conflicts focuses on the distribution of power within the international system. Two major forms of power distribution are bipolarity and multipolarity. Bipolar systems tend to encourage trade integration within competing geopolitical blocs while discouraging economic exchange across bloc boundaries. Multipolar systems, by contrast, involve shorter and less predictable alignments among states, resulting in less clearly defined geopolitical trade divisions.

There are also important differences between the current US–China rivalry and the bipolar structure of the Cold War. One major distinction is that the Soviet–US bipolar order left relatively little room for geopolitical “in-between” states; most countries were clearly aligned with one bloc or the other. This is not the case in contemporary US–China relations. During the Cold War, most European states were either members of one of the two opposing blocs or formally neutral states operating within relatively stable geopolitical rules. Countries rarely shifted from one alliance system to another. In contrast, the strategic landscape in Asia today is far more fluid, with many states maintaining complex and flexible relationships with both the US and China.

As Professor Mearsheimer puts it, “In Asia, there is no clear dividing line like the Iron Curtain to anchor stability. Instead, there are a handful of potential conflicts that would be limited and would involve conventional arms, which makes war thinkable” (Mearsheimer, 2021, p. 57).

The international trade system is not only multilateral in terms of participation—with 164 members of the WTO—but also in its foundational principles, including most-favoured-nation treatment and generalized reciprocity. From this perspective, China’s exports to the US exceed what standard gravity models would predict. This deviation is largely explained by the high share of foreign value added embedded in Chinese exports, reflecting the integration of regional supply chains across East Asia, including inputs from South Korea, Taiwan, and other economies (Siddiqui, 2021).

The US–China trade deficit has persisted over time, partly due to structural differences in comparative advantage rooted in relative factor endowments. The US is a capital-rich economy compared with China, while China retains a strong comparative advantage in labour-intensive production. Following the Stolper–Samuelson theorem (1941), this implies that the US will tend to import labour-intensive goods, while China will import more capital-intensive goods. Although many countries produce both types of goods, shifts in trading partners are constrained by significant opportunity costs. In many cases, China is able to supply goods more cheaply than alternative exporters, making substitution difficult.

China remains the US largest import partner, followed by Mexico, Canada, Japan, and Germany. The relatively higher production costs in these alternative economies imply substantial “switching costs” for reconfiguring supply chains. This reality has been widely recognized by major US retailers such as Costco, Walmart, and Target, which rely heavily on established global sourcing networks to maintain low prices and stable supply.

VII. Conclusion

This study finds that persistent US–China trade imbalances stem primarily from deep-seated structural macroeconomic differences rather than short-term policy interventions. The US operates as a consumption-driven political economy, characterized by persistently low savings, sharply rising defence expenditures, mounting foreign debt, and strong aggregate demand. In contrast, China maintains a growth model centred on high savings and state-guided, investment-led industrial expansion. These divergent structural logics generate chronic trade deficits in the US and surpluses in China—patterns further amplified by comparative advantage and deeply integrated global production networks. Consequently, policy instruments such as tariffs or exchange rate adjustments have only limited capacity to fundamentally alter the underlying imbalance.

Although many countries produce both types of goods, shifts in trading partners are constrained by significant opportunity costs.

China’s trade surplus with the US narrowed to $51.13 billion in March 2026, its lowest level since early 2025 and well below expectations, as export growth slowed to 2.5% following seasonal distortions and a high base effect from the previous year. At the same time, imports surged by 27.8% to a record $269.90 billion, driven by supply chain pressures, geopolitical tensions, and increased demand for high-tech inputs.

These developments must be understood within the broader geopolitical and economic evolution of the bilateral relationship. A recent visit by President Trump underscores the limited leverage the US holds in reshaping China’s economic trajectory. Over the past decade, China has significantly expanded and transformed its industrial and technological base. In contrast, the US economy has faced growing structural pressures, including rising public debt, persistent trade deficits, deindustrialization, slow growth, and comparatively weak investment performance.

Despite recurring tensions since China’s accession to the WTO, US–China trade remains deeply interdependent. Highly integrated supply chains—particularly across East Asia—continue to bind the two economies together, with substantial switching costs limiting near-term decoupling. Overall, the evidence suggests that resolving bilateral trade imbalances requires addressing underlying domestic macroeconomic structures in the US, rather than relying primarily on external trade restrictions or diplomatic pressure.

Dr. Kalim Siddiquiis an economist specializing in International Political Economy, Development Economics, Trade and Economic Policy. Since 1989, he has been teaching economics at various universities in Norway and the UK. Dr. Siddiqui’s research interests encompass a wide range of topics, including political economy, international trade, and economic history, South Asia, and emerging economies. He has presented papers at international conferences across numerous countries, reflecting his global engagement in the field. His scholarly pursuits span six broad domains: Political Economy, Development Economics, Economic History, Economic Policy, Globalization, and International Trade. Dr. Siddiqui has made significant contributions to research in areas such as trade policy, globalization, and political economy. His work has been published in chapters of edited books and articles published in peer-reviewed journals. For inquiries, Dr. Siddiqui can be reached at: [email protected]

References

Hopewell, K. (2020) Clash of Powers: US-China Rivalry in Global Trade Governance, Cambridge: Cambridge University Press.

Liu, T. and Woo, W.T. (2018) “Understanding the US-China trade war”, China Economic Journal, Taylor & Francis.

Mearsheimer, J. (2021), “The inevitable rivalry: America, China, and the tragedy of great power politics”, Foreign Affairs 100 (6):48-59.

Siddiqui, K. (2026a) “The United States, the Petrodollar, and Multipolarity: Strategic Intervention in an Age of Monetary Decline”, World Financial Review, January.

Siddiqui, K. (2026b) “US-Iran Conflict: Oil Volatility and Global Economic Crisis”, World Financial Review, April.

Siddiqui, K. (2026c) “The Unravelling of Dollar Hegemony: Debt, Rentier Power, and the Crisis of US Global Dominance”, World Financial Review, February.

Siddiqui, K. (2025a) “Rare Earth Critical Minerals: Geopolitics, Supply Chains, and Emerging Tensions”, World Financial Review, September.

Siddiqui, K. (2025b) “Reconfiguring US Hegemony: Militarism, Empire, and the Crisis of Capitalist Accumulation”, World Financial Review, August.

Siddiqui, K. (2025c) “Decolonisation and Economic Sovereignty: The Bandung Conference and the Making of the Global South”, World Financial Review, June.

Siddiqui, K. (2025d) “The United States’ Future in an Imperial Mirror: Lessons from Britain, Spain, Abbasids, Rome, and Beyond”, World Financial Review, November.

Siddiqui, K. (2025e) “The Reasons Behind the Decline of the United States Economy”, World Financial Review, May.

Siddiqui, K. (2024a) “China’s Growth Miracle and Development Strategy Since the 1980s”, World Financial Review,

Siddiqui, K. (2024b) “China’s Trade and Growing Economic Influence with East Asia”, World Financial Review, May.

Siddiqui, K. (2024c) “Trends and Prospects of De-Dollarization in the Rapidly Changing Global Economy”, World Financial Review (Part 1 & Part 2), December.

Siddiqui, K. (2021). “Can the 21st Century be an Asian Century?”, Asian Profile, 49(1):1-19, March.

Siddiqui, K. (2020). “The US Dollar and the World Economy: A critical review”, Athens Journal of Economics and Business, 6(1):21-44, January.

Siddiqui, K. (2019). “One Belt and One Road, China’s Massive Infrastructure Project to Boost Trade and Economy: An Overview”, International Critical Thought. 9(2):214-235.

Siddiqui, K. (2018). “US – China Trade War: The Reasons Behind and its Impact on the Global Economy”, World Financial Review, November/December.

Siddiqui, K. (2016). “International Trade, WTO and Economic Development”, World Review of Political Economy, 7(4):424-450.

Siddiqui, K. (2009). “Japan’s Economic Crisis”, Research in Applied Economics 1(1):1-25.

The New York Times (2026) “Trump Touts ‘Fantastic Trade Deals’, but Details Are Scarce”, 15thMay.

The Financial Times (2026) “US-China relations – Boeing shares slide as Trump’s China summit”, 15thMay.

Van der Pijl, K. (1984) The Making of an Atlantic Ruling Class, London: Verso Books.

Top institutional crypto platforms have become a core layer of the digital asset market. What used to be a retail-driven space now runs on institutional flows, and you can feel it in the way liquidity behaves. Large orders are absorbed differently, spreads are tighter, and execution matters more than ever.

Introduction to Top Institutional Cryptocurrency Platforms

Institutional participation has changed how exchanges operate. The top institutional cryptocurrency platforms are no longer just marketplaces—they are full infrastructure providers. From my perspective as a trader, the biggest difference is how these platforms prioritize execution quality over interface design.

When we talk about crypto trading for institutions, we are referring to an environment where orders are often algorithmic, positions are hedged across venues, and capital efficiency is critical. That means exchanges must deliver consistent performance under pressure, not just during calm market conditions.

What Makes the Best Institutional Crypto Exchange

The definition of the best institutional crypto exchange is fairly straightforward when you look at it from a practical angle. Liquidity is the first filter. If a platform cannot handle large orders without significant slippage, it is simply not viable for institutional use.

The second factor is infrastructure. Most institutional participants rely on API connections rather than manual trading. This is where crypto solutions for market makers become essential. Low latency, stable connectivity, and predictable execution are not optional—they are the baseline.

Compliance also plays a key role. Funds, fintech companies, and market makers operate within regulatory frameworks. They need reporting tools, transparent processes, and a platform that can integrate into their existing risk management systems.

Top Institutional Crypto Platforms in 2026

There are several strong players in this segment, but only a handful can be considered true top institutional crypto services.

1. Coinbase Institutional

A dominant force in the US market. It is often the default choice for funds that prioritize regulatory clarity and integration with traditional finance. Execution is reliable, though sometimes less aggressive than offshore venues.

2. WhiteBIT

The institutional crypto exchange WhiteBIT has built a solid position by focusing on infrastructure rather than hype. In practice, crypto trading for institutions on WhiteBIT feels streamlined. The platform offers access to deep liquidity across more than 900 trading pairs and supports an API-first trading environment. Its ecosystem integrates lending, margin, and execution tools to align with real trading workflows. For firms running liquidity strategies, its crypto solutions for market makers allow direct access to trading infrastructure without unnecessary complexity.

3. Binance Institutional

Still one of the deepest liquidity hubs globally, especially in derivatives markets. It is widely used for large-volume execution, though some institutions approach it selectively from a regulatory standpoint.

4. Kraken Institutional