According to Malaysia Islamic Finance Marketplace, Zawya Islamic and Thomson Reuters, Islamic finance has been growing at a double-digit rate since the start of the new millennium. In this article the author discusses the potential of Islamic Finance in Kazakhstan, and its role in the success of Islamic Finance in Central Asia.

Islamic Finance is considered as an alternative financial system that is based on Islamic shari’ah promoting a superior form of ethical and social financial transformation mechanism, shared values and sustainable development. The system prohibits the use of traditional interest rates, promotes profit and loss sharing in investment and financing, and, more importantly, considers the customers as “partners” in business. Financial instruments are designed to fit the above-mentioned goals for the shorter- and longer-terms. Multiple authorities including internal and centralised shari’ah advisory boards monitor the innovation in financial instruments and their performance. Countries in the Middle East, Southeast Asia, North Africa, and South Asia are leading in development of comprehensive halal ecosystems for the users of Islamic finance. Islamic finance has received much attention after the recent global financial crisis while the system has been extraordinarily resilient to risk. Experts have given credits to Islamic finance systems for an embedded risk management system as such the Islamic financial managers have carefully screened investment based on risk adjusted benefits. More countries are gradually registering their interest towards Islamic financial system, and the system has experienced tremendous development from several fronts including banking, equities investment, Islamic bonds (sukuk), mutual funds, microfinance, and insurance (takaful).

Source: Compiled by the writer from various sources

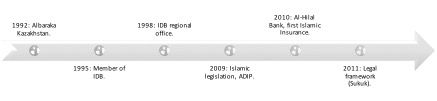

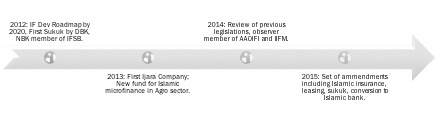

Figure 1 & 2: Timelines of Development of IF in Kazakhstan

Kazakhstan has been in the frontier leading Islamic finance development in the Central Asian region. Above timelines are self-explanatory. There has been a rapid progression since 2009, the year of the first established legislation for Islamic finance industry, to become the Islamic hub of Central Asia. By 2020, Kazakhstan wants its Islamic banking industry to reach 3-5% of its total banking assets. To achieve this vision, the country has already laid down rigorous plans combining regulatory initiatives for Islamic banking, insurance, leasing, sukuk, and microfinance, and has set-up supporting institutions to shift to the next gear of development and enhancement. Astana has given a clear signal to that direction in 2015 by bringing meaningful amendments to the existing regulations. Capital requirements for chartering a new bank has been brought down by 50%, conversion from conventional to Islamic mode of financing has been streamlined, and a centralised Shari’ah board (Council for Islamic Financing Principles) has been activated. Initiatives are taken by National Bank of Kazakhstan to develop halal ecosystems that combine prudential regulations, financial institutions, consumers, and cross-border relations. Positive outcomes have started appearing as well: Thomson Reuters investment outlook (2015) ranked the country in the 5th position out of 57 OIC member countries as a top tiered Islamic investment destination, and a similar survey was conducted in 2014 that ranked Astana 5th on the regulatory initiatives and integration. At present, the country has seen an Islamic bank, Al Hilal Bank, a Sukuk issuance, an Islamic microfinance mostly for the agricultural financing, Islamic leasing firm, and an Islamic insurance (Takaful) firm. Internationally active banks such as the Al Baraka Group and MayBank Group have shown interests to be active in Islamic finance markets in Kazakhstan. With a 17.5 million Muslim population, which is almost untapped, Astana can expect some positive changes in the coming future.

Source: Kulchmanov et al. (2016)

Figure 3: Preparation for Future (based on survey on bank managers)

Note: MY, IND – Islamic banks in Malaysia, Indonesia, IB – Islamic Bank in Kazakhstan, LCB & SCB – Large and Small Conventional Bank in Kazakhstan.

Three major challenges have been identified so far. In an interview with Thomson Reuters, the Deputy Governor of the National Bank of Kazakhstan has identified a shortage of knowledge base, lower level awareness, and limited but gradually developing legislative initiatives as the major challenges. Similar findings are reported by a recent full pledged study done on risk management of Islamic Bank in Kazakhstan by Kulchmanov et al. (2016). Their study has reported that technical and Shari’ah related know-how, limited regulatory assistance, and unavailability of markets for Islamic institutions are the key challenges. This study has found that industry wide development is more important than the firm specific development as future strategies. The study concluded that size of the overall market is a serious contingent variable, meaning that the challenges will gradually disappear with a greater number of institutions, instruments and growth in consumer base. Figure 3 shows that the Islamic Bank is better prepared than overall industry readiness since the Islamic Bank is owned by already established Islamic finance service providers.

More insights are gathered when I analyse the most recent published income statement and balance sheet information for the only Islamic bank in Kazakhstan. Al Hilal Bank’s profit has increased three times from 2014 to 2015. Around 90% of their income from Islamic finance activities is earned using Ijara and similar methods. The bank has paid only 3.5% of its income (from IF activities) as expenses for Islamic finance activities. Total assets are doubled between 2014 and 2015; however, the major portion (42% of total assets) is kept as cash and equivalents. 54% of the assets in 2015 have been invested in Islamic financial alternatives such as Islamic derivatives (7%), commodity Murabaha agreements (38%), Wakala investment deposits (7%) and Ijara (2%). Notably, Ijara and Wakala investment deposits have decreased in 2015 when compared to the value in 2014. An excessive amount of cash holding indicates that the bank is looking for profitable investment, which is unavailable at this moment.

Al Hilal Bank has reported an equally distributed capital structure in 2015 with 49% of the funds from equity and 51% in debt. This is quite a contrast to the figures in 2014 while the bank has sourced 85% of the funds from equity and only 15% from debt. Among many, consumer deposit has increased by 2.5 times from 2014 to 2015, even though in overall financing the percentage of consumer deposits is only 17% (of total assets in 2015). With a massive size of equity capital, it is expected that the bank has much higher capital adequacy than expected. The bank has not reported the portion of the bank’s owners’ Zakah, which the bank expects the shareholders to calculate on their own. Finally, there has been no reporting on profit-and-loss-sharing instruments and Qard Hasan that are more socially responsible and Shari’ah-centric.

Based on the operating outlook of the Al Hilal Bank, we can look at a larger set of challenges for Islamic finance development in Kazakhstan. Interestingly, none of these are new, as such these challenges have been common for any nation with a plan to become the Islamic finance service providers. We will, however, have a look at these challenges from a critical and market-oriented approach.

Figure 4: Islamic finance ecosystems for Kazakhstan

By 2020, Astana is planning to reach an adequate stage of Islamic financial legislative development that will help attract new investment in this area. It is easily understandable that the components of Islamic finance should be integrated in a chain to work efficiently. For instance, Islamic banking should be seamlessly supported by Islamic capital markets, insurance and other allied services. Similarly, being in a multi-racial environment, authorities should take extra care while opening opportunities for Islamic entrepreneurship, which is the largest demand side stakeholder of the Islamic financial services. The ecosystems cannot work unless the financial systems and the business environment are not equally Shari’ah compliant. Thirdly, Islamic banks would eventually compete with their conventional counterparts. Hence, it is partly their responsibility to help increase the financial literacy at the various consumption levels to achieve a superior growth of adoption. Government should tie up with financial institutions and educational institutions in reaching a higher level of financial literacy. These developments in human capital must also be supported by adequate incentives.

Islamic financial institutions should gradually move towards a socially responsible financial model that is more sustainable and covers a greater proportion of population. Some of the recent day socio-economic development agendas, such as the SDGs and MDGs, can be accomplished easily if Astana can target a higher level of inclusion alongside existing legislative and performance-related indicators. Moreover, Islamic financial institutions are expected to enhance their capabilities to handle profit and loss sharing contracts for an efficient socio-economic transformation. If PLS is ignored any further, Islamic banks will eventually turn to conventional institutions having no soulless efforts to maximise value of a limited number of shareholders. Finally, a successful Islamic ecosystem should uphold relationships with other likeminded institutions and authorities across border. Learning from the best practices from other Islamic financial institutions will help reaching the Astana Islamic finance vision-2020.

About the Author

Mamunur Rashid holds a PhD in Behavioural Finance, and currently is an Assistant Professor of Finance, and the Deputy Director of the Centre for Islamic Business and Finance Research (CIBFR), at the University of Nottingham Malaysia Campus. He has been teaching International Finance, Financial Economics, Islamic Capital Markets, and Corporate Finance for the last twelve years in different countries. An active researcher, Dr Mamunur publishes widely in financial economics, Islamic economics, investor behavior, and corporate social responsibility, and has presented papers in 25 international conferences. In 2016-17, Dr Rashid has co-edited a special issue for International Journal of Mamunur has worked on several corporate and government projects. Mamunur Rashid can be contacted at: [email protected].

Mamunur Rashid holds a PhD in Behavioural Finance, and currently is an Assistant Professor of Finance, and the Deputy Director of the Centre for Islamic Business and Finance Research (CIBFR), at the University of Nottingham Malaysia Campus. He has been teaching International Finance, Financial Economics, Islamic Capital Markets, and Corporate Finance for the last twelve years in different countries. An active researcher, Dr Mamunur publishes widely in financial economics, Islamic economics, investor behavior, and corporate social responsibility, and has presented papers in 25 international conferences. In 2016-17, Dr Rashid has co-edited a special issue for International Journal of Mamunur has worked on several corporate and government projects. Mamunur Rashid can be contacted at: [email protected].

References:

1. Annual report of Al Hilal Bank Islamic Bank JSC (2015)

2. A new frontier of Islamic Finance – Thomson Reuters Islamic Finance country report of Kazakhstan.

3. Kulchmanov, A., Hassan, M.K. & Rashid, M. (2016). Contingency theory approach to risk management practices in Islamic banks: A case study on Kazakhstan, International Journal of Islamic Business, 1(2), 35-67.

{kind=link}